What is the 3D Scanning Market Size?

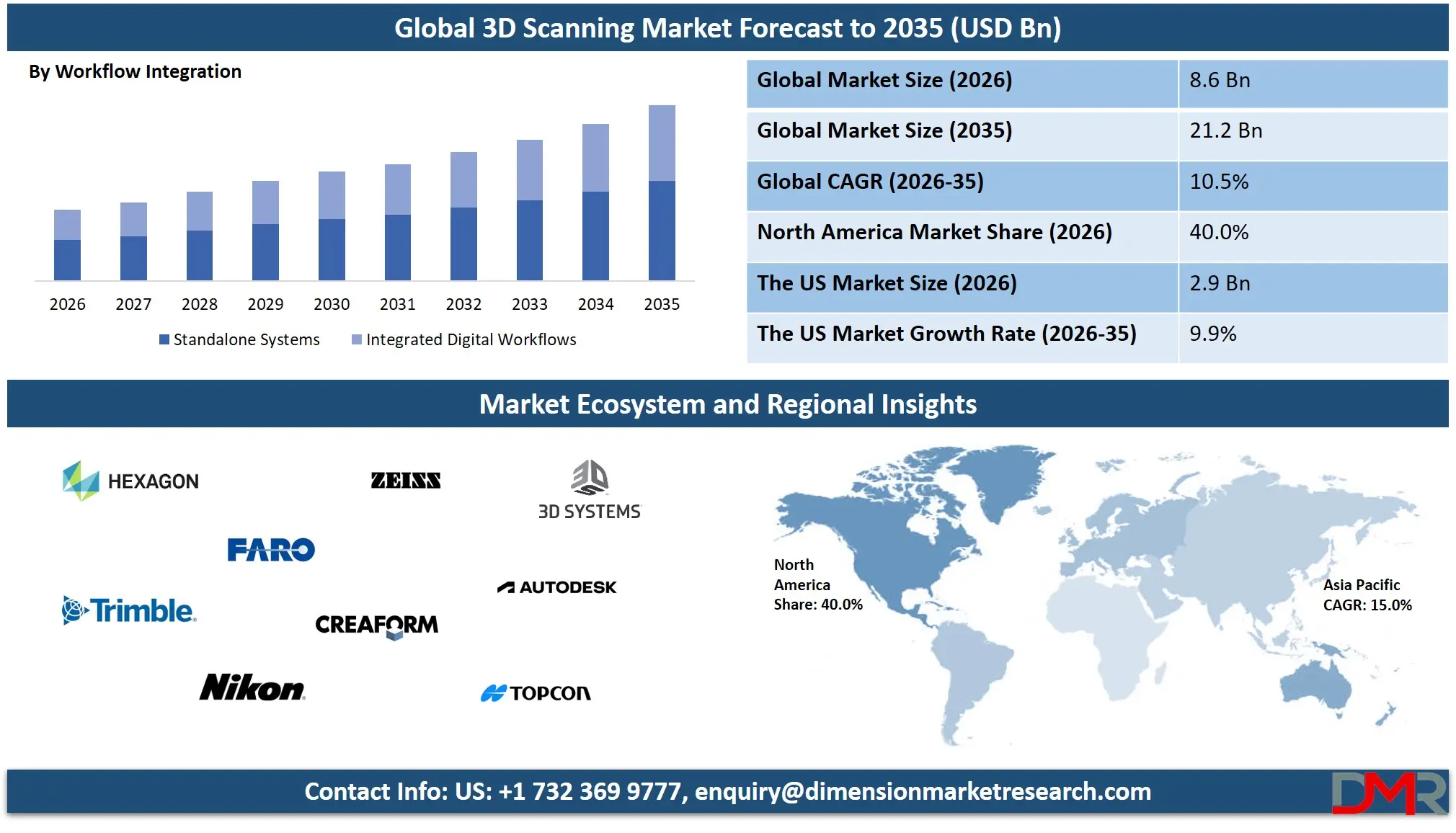

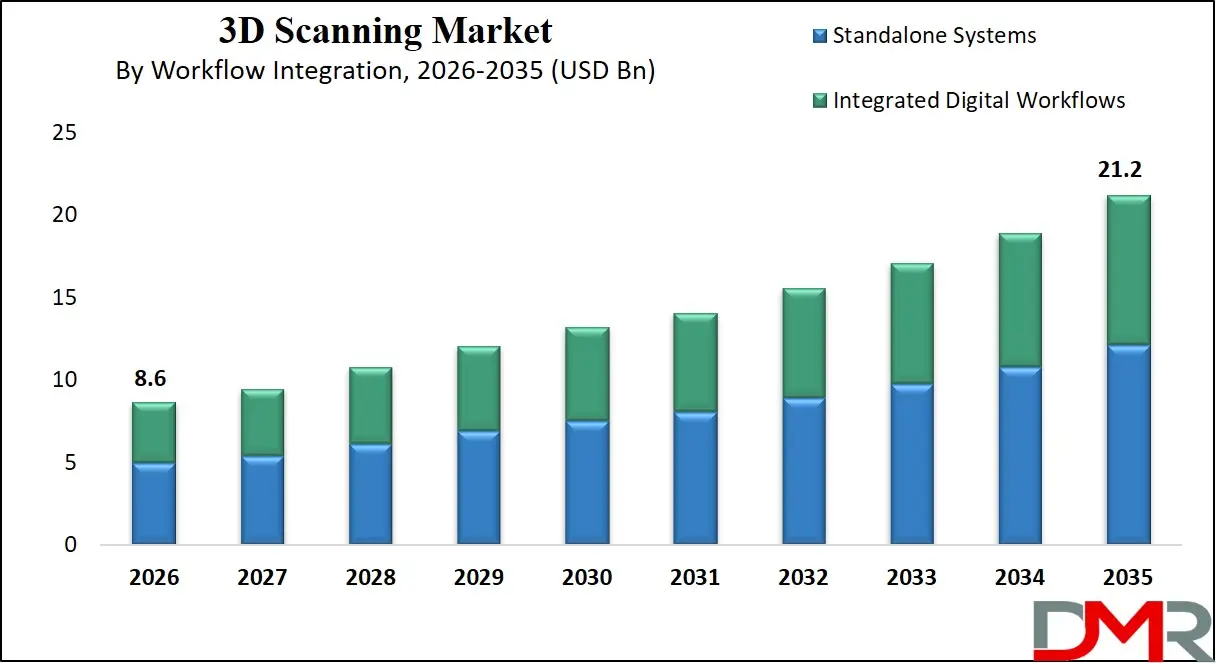

The Global 3D Scanning Market is projected to reach USD 8.6 billion in 2026 and grow at a compound annual growth rate of 10.5%, reaching USD 21.2 billion by 2035, driven by laser scanning, point cloud, digital twin, metrology, and reverse engineering technologies across industrial applications.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The 3D scanning industry provides high-resolution digital measurements of physical objects to be used in manufacturing, health, construction and geospatial fields. It is supported by global digital transformation, Industry 4.0 implementation, and rising automation in all industries, which has led to its growth. The World Economic Forum claims that the high-level digital technologies are becoming a necessity in the industrial competitiveness and efficiency. The proliferation of 3D mapping and digital twins is supported by infrastructure and smart city programs by the World Bank.

The National Institutes of Health in the field of healthcare identifies the increasing use of 3D imaging in the diagnostic process and treatment plan. The market is also backed by the need to have greater accuracy, speed of work and fewer design and production errors. The integration with AI, cloud systems, and digital twin technologies in any industry will become the driver of further growth.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

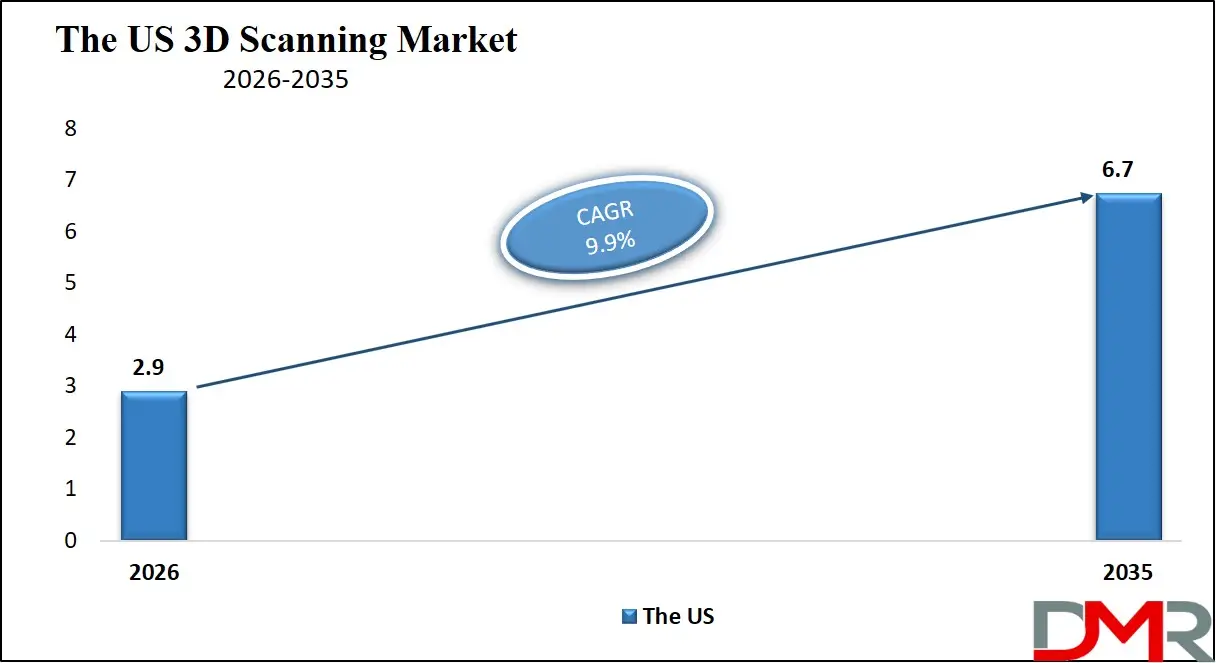

US 3D Scanning Market

The US 3D Scanning Market is projected to reach USD 2.9 billion in 2026 and grow at a compound annual growth rate of 9.9%, reaching USD 6.7 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US 3D scanning market is driven by strong adoption across automotive, aerospace, healthcare, and construction industries, supported by advanced manufacturing infrastructure and R&D investment. Demand is rising for laser scanning, point cloud processing, and digital twin technologies used in precision engineering and quality inspection. Government-backed smart manufacturing initiatives are further accelerating deployment across industrial sectors. According to the National Institute of Standards and Technology, advanced digital measurement systems are key to improving production efficiency and accuracy.

Europe 3D Scanning Market

Europe 3D Scanning Market is anticipated to reach 2.3 Bn in 2026, expanding with a CAGR of 9.6%. The growth is driven by strong adoption across automotive, aerospace, and industrial manufacturing sectors, supported by advanced engineering capabilities. Increasing use of digital twin, metrology, and reverse engineering technologies is further strengthening demand. Rising focus on automation and precision-based quality inspection is also accelerating market expansion across key European economies.

Japan 3D Scanning Market

Japan 3D Scanning Market is anticipated to reach 602.0 Mn in 2026, expanding with a CAGR of 9.4%. The market is driven by strong adoption in automotive manufacturing, robotics, and precision engineering applications. Increasing demand for high-accuracy metrology and quality inspection is further supporting growth across industrial sectors. Rising integration of advanced manufacturing technologies and automation systems is also accelerating market expansion in Japan.

Key Takeaways

- Market Size: The global 3D scanning market is projected to reach USD 8.6 billion in 2026 and expand to USD 21.2 billion by 2035.

- Growth Rate and Outlook: The market is expected to grow at a CAGR of 10.5% from 2026 to 2035, driven by industrial digitization and automation adoption.

- Primary Growth Drivers: Growth is fueled by rising demand for digital twin technology, reverse engineering, precision metrology, and AI-enabled 3D imaging systems across industries.

- By Component Analysis: Hardware dominates with around 69% share in 2026, supported by strong demand for scanners, LiDAR, and structured light systems in industrial applications.

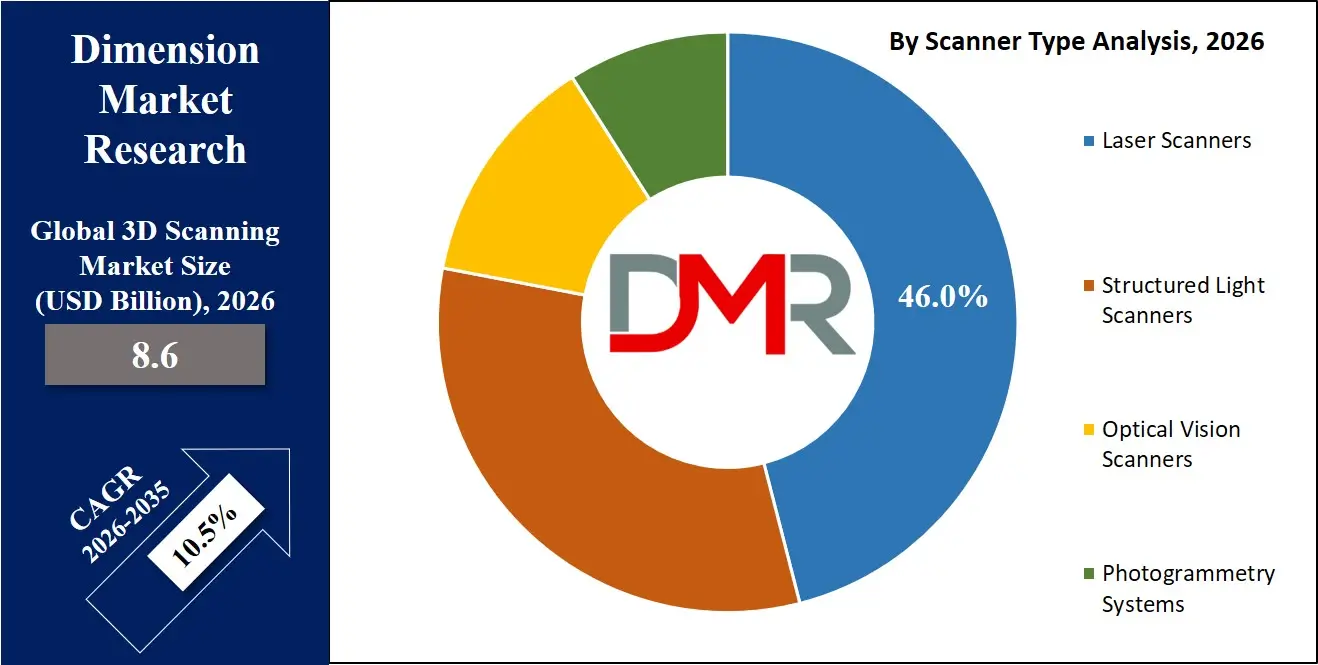

- By Scanner Type Analysis: Laser Scanners lead with approximately 46% share in 2026 due to high accuracy and widespread use in manufacturing, aerospace, and construction.

- By End-use Industry Analysis: Automotive dominates with around 28% share in 2026, driven by extensive use in design, prototyping, and quality inspection processes.

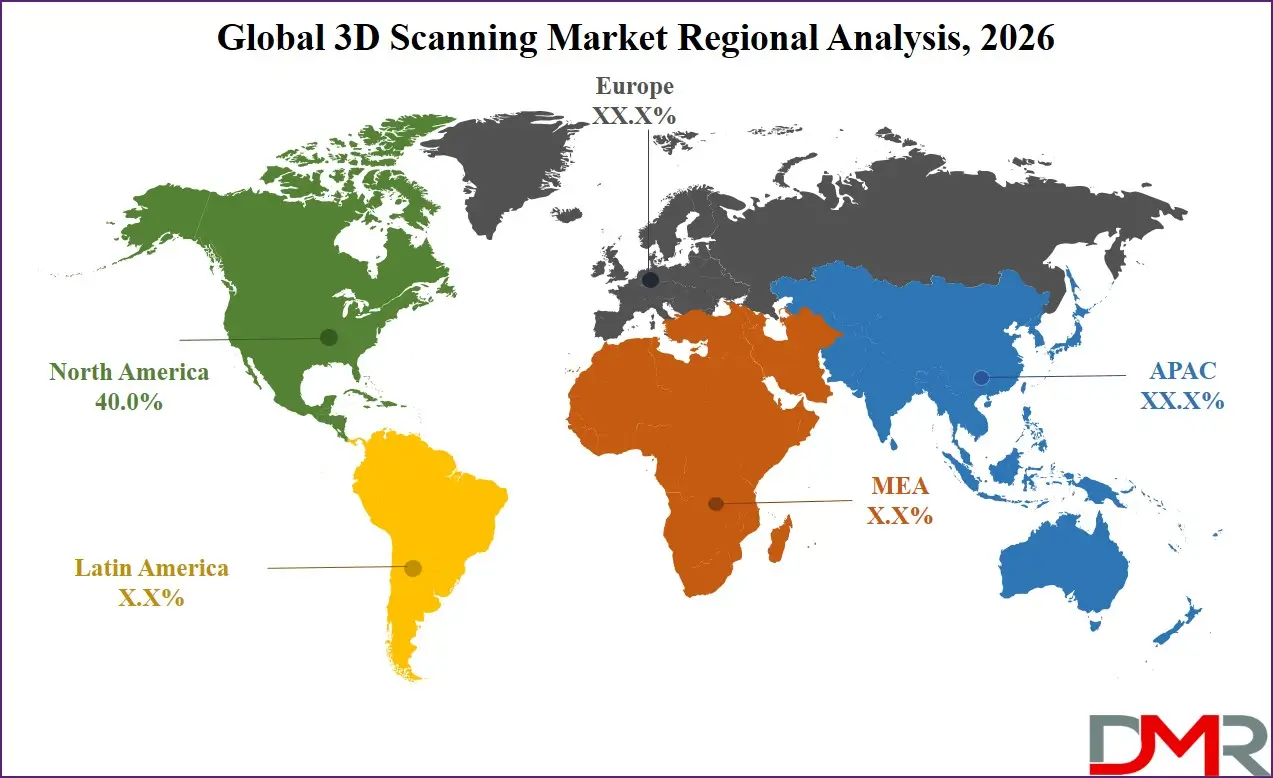

- Regional Leadership: North America leads the market with approximately 40% share in 2026, supported by advanced manufacturing infrastructure and early technology adoption.

What is the 3D Scanning?

3D scanning is a computer-generated measuring instrument that records the real-life objects and transforms them into precise 3D models via the point cloud data. It finds many applications in engineering, medical, and manufacturing in precision design, inspection, and reverse engineering. It allows the digital replication of high accuracy to conduct analysis and test, according to the National Aeronautics and Space Administration. The technology enhances efficiency, minimizes errors and facilitates non-destructive evaluation. It is also important in digital twins and simulation systems. It is a standard government- and research-backed industrial automation tool. On the whole, it improves the accuracy and productivity of contemporary engineering processes.

Use Cases

- Quality Inspection and Metrology: 3D scanning is widely used for high-precision inspection of manufactured components to ensure dimensional accuracy and defect detection. It enables comparison between CAD models and physical parts using point cloud data. This reduces production errors and improves quality control efficiency in industrial environments.

- Reverse Engineering: It is used to digitally reconstruct legacy or complex parts where original design data is unavailable. The scanned data is converted into editable CAD models for redesign and replication. This supports faster product development and cost-effective manufacturing.

- Healthcare and Medical Imaging: 3D scanning assists in creating accurate anatomical models for prosthetics, orthotics, and surgical planning. It enables customized patient-specific treatment solutions with high precision. This improves clinical outcomes and reduces procedural risks.

- Construction and Infrastructure: It is used for site mapping, building information modeling, and structural analysis in construction projects. 3D scans provide real-time spatial data for planning and monitoring progress. This enhances project accuracy, safety, and efficiency.

How AI is transforming the 3D Scanning Market

The market of 3D scanning is undergoing change with AI providing faster and more precise processing of point clouds, and less manual processing in cleaning up the data and creating the model. It improves defect detection and quality inspection as it automatically detects anomalies on a surface more precisely.

Algorithms enhanced by AI are also beneficial in reverse engineering through a more efficient reconstruction of complex geometries into detailed CAD models. Also, 3D scanning is becoming more predictive, automated, and scalable to industries with integration with machine learning and digital twin systems.

Market Dynamics

Key Drivers in the Global 3D Scanning Market

Increasing Industrial Automation and Adoption of Smart Manufacturing

The manufacturing industries in the world are becoming more automized, using robotics and digital production systems, and this is creating a high demand of 3D scanning technologies. These systems allow measurement, real time quality control and quick development of products. The Industry 4.0 is backed by 3D scanning which links physical and digital processes. It also eliminates errors of manual inspection and enhances production. With the transfer of factories to smart modes, there is an ever-growing demand among the smartly scanned solutions with high accuracy.

Widening Applications in Digital Twin and Simulation Technologies

The increasing use of digital twins technology is an important factor in the uptake of 3D scanning in other industries. Digital-to-physical replication needs high spatial resolution data taken on a cutting-edge scanning system to ensure an accurate replication. This finds large applications in aerospace, road vehicle, and road infrastructure monitoring. It facilitates predictive maintenance, optimization of operations and virtual testing of systems. Market growth is being further enhanced as more investment is made in simulation-based engineering.

Restraints in the Global 3D Scanning Market

Expensive Advanced Scanning Systems

Advanced 3D scanning hardware and software is expensive, hindering its adoption, particularly in small and medium enterprises because of their high start-up cost. Structured light systems and precision laser scanners are associated with high acquisition and maintenance costs. Software licensing, calibration and qualified operators are other additional costs that add to total cost of ownership. This renders big-scale deployment hard on cost-sensitive industries. This has meant that penetration in markets is still focused on the industrial high-value industries.

Difficulty in Data Processing and integration.

3D scanning produces large amounts of complicated point cloud data that needs sophisticated processing. Raw scan data is sometimes processed to useful CAD models which can require special software and technical skills. Organizations may also face challenges in integrating it with the existing PLM and CAD systems. The management and storage of data also complicates operations. These contribute to slow pace of adoption in the industries that do not have developed digital infrastructure.

Growth Opportunities in the Global 3D Scanning Market

Increasing Industry Adoptions in the major sectors

The market of 3D scanners is continuously expanding because of the growing applications in the automotive, aerospace, healthcare, and construction markets. There is an increasing demand of high-precision measurement tools to enhance the quality and accuracy of the design. The automation and modernization of manufacturing programs are increasing implementation of scanning systems in manufacturing facilities. Both reduced cost of hardware and accessibility to software tools are contributing to the greater adoption. In general, the main driver of market development is the industrial digitization.

Increased Infrastructure and Smart Project Investment

The surge in large-scale infrastructural development, as well as smart city initiatives, is contributing to the demand of 3D scanning in surveying and mapping projects. Spatial data technologies are becoming popular among governments and the private players in planning and monitoring construction activities. This is enhancing efficiency in projects, minimizing delays, and improving the accuracy of structure. Increasing urbanization is also increasing demand of sophisticated geospatial solutions. Consequently, the modernization of infrastructure is helping to expand the market.

Trends in the Global 3D Scanning Market

ADS Integration with AI-Driven Automation Systems

One of the major market trends is the incorporation of artificial intelligence in the 3D scanning processes. AI is enhancing point cloud processing, error detection, and automatic generations of models. This minimizes human intervention and enhances efficiency in industrial processes. Machine learning is also facilitating quicker scan data to digital models. A change to smart scanning systems is transforming the workflow automation.

Migration to Cloud-Based and Connected Scanning platforms

The tendency in favor of cloud-enabled 3D scanning solutions, which enable real-time data processing and remote collaboration, is on the rise. These platforms provide smooth storage, sharing, and analysis of the large scan datasets. Connected ecosystems are becoming increasingly popular in industries, combining scanning with CAD, PLM, and digital twins. This is enhancing the usability of 3D data in terms of its availability and scalability. Next-generation scanning is taking the form of cloud integration.

Research Scope and Analysis

By Design Analysis

The segment of the 3D scanning market is projected to be dominated by hardware with approximately 69.0% share in 2026 due to the high demand of high-precision scanners, LiDAR, and structured light systems in manufacturing, inspection, and mapping. The ecosystem is assisted by software that facilitates point cloud processing, 3D modeling, reverse engineering and CAD integration. The growing applications of AI and cloud-based tools are enhancing automation and accuracy of data. Although hardware dominates revenue contribution, software is gaining momentum owing to increased demand in intelligent processing and integration of digital workflow.

By Scanner Type Analysis

Laser scanners will dominate the scanner type segment with an approximate market share of 46.0% in 2026 because of their high accuracy, long-range performance, and extensive application in industrial inspection, reverse engineering and mapping.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Projected light patterns are used in structured light scanners to measure detailed surface geometry, and primarily have short-range, high-resolution applications. They are commonly used in health care, product design, and quality check. Although laser scanners dominate the usage cases of heavy industries, the use of structured light scanners is increasing owing to high scanning rate and portability.

By Range Analysis

Short range scanning will control the range segment with an approximate share of 53.0% in 2026 because it is the most precise and it is widely used in the applications that demand a detailed measurement of small to medium sized objects like industrial parts, healthcare models and product design. It is very popular in production and quality control where precision is paramount. Larger objects and environments are scanned using medium range scanning which provides a balance between coverage and precision and therefore it is applicable in industrial facilities, construction sites, and infrastructure inspection. It allows the capture of complex structures effectively at moderate ranges. Even though short range is the leading because of the precision oriented applications, medium range is steadily increasing with the increasing needs in engineering and field based scanning.

By Form Factor Analysis

Tripod-mounted scanners will likely control the form factor market with 38.0% share in 2026 because of high accuracy, stability, and operation in industrial inspection and metrology processes. They have extensive application in controlled settings to make accurate measurements. Handheld scanners are portable and flexible to real-time scan of complex or inaccessible surfaces in construction, health care, and fieldwork. Although tripod systems dominate in the high-precision field, handheld scanners are increasing in popularity as a result of their convenience and portability.

By Accuracy Level Analysis

It is anticipated that high precision scanners (≤50 µm) will dominate the accuracy segment with approximately 48.0% in 2026 because of the high utilisation in aerospace, automotive and industrial metrology which demands ultra-accurate measurements. They are very common in inspection, reverse engineering and precision engineering. Medium accuracy scanners (50-200 um) are applied in construction, manufacturing and infrastructure where accuracy and speed must be balanced. Whereas high precision is used in high stakes, medium precision is increasingly used because of increased industrial uses and reduced cost.

By Workflow Integration Analysis

It is predicted that standalone systems will take the largest share in the workflow integration market with approximately 57.0% by 2026, as they are widely used in industrial inspection, metrology, and reverse engineering where independent scanning systems are adequate. They are favored due to their simplicity, low cost, and simple deployment. Digital workflows are integrated between 3D scanning and CAD, PLM, and digital twin to ensure data is transferred and automated. Although standalone systems dominate the entry level applications, the integrated workflow is on the rise because of the increasing need of connected and automated engineering systems.

By Deployment Analysis

The segment is projected to be dominated by on-premise deployment, which is anticipated to have approximately 68.0% share in 2026 because it is heavily used in aerospace, automotive, and manufacturing industries where precision, control, and data security are crucial. They are mostly used in environments where they handle sensitive engineering and inspection data. Cloud-enabled implementation allows remote access, real-time collaboration and scalable processing of 3D scan data. It is finding its way to digital twin and collaborative engineering uses. On-premise still reigns as the best due to security benefits, but cloud systems are on the rise because of flexibility and scalability.

By Application Analysis

Metrology and inspection are likely to dominate the application segment with approximately 32.0% share in 2026 because of heavy usage in quality control, dimensional measurement and defect detection in the automotive, aerospace and manufacturing sectors. These procedures are very accurate and are designed to meet design standards. Original CAD data is not available, and reverse engineering is used to create digital representations of physical components to aid in the redesigning and development of new products. Metrology is the leader because of the demand on inspection, but reverse engineering is increasing with the demand of more cost-effective speedy product innovation.

By End-use Industry Analysis

Automotive is expected to dominate the end-use industry segment with around 28.0% share in 2026 due to high usage in design, prototyping, and quality inspection for vehicle manufacturing. It improves precision and production efficiency across large-scale operations. Aerospace and defense use 3D scanning for aircraft inspection, reverse engineering, and structural analysis where accuracy and safety are critical. While automotive leads due to volume production, aerospace and defense is growing steadily due to strict quality and engineering requirements.

The Global 3D Scanning Market Report is segmented on the basis of the following:

By Design

- Hardware

- Software

- Services

By Scanner Type

- Laser Scanners

- Structured Light Scanners

- Optical Vision Scanners

- Photogrammetry Systems

By Range

- Short Range

- Medium Range

- Long Range

By Form Factor

- Tripod-mounted

- Handheld

- Fixed Inline

- Robotic-mounted

By Accuracy Level

- High Precision (≤50 µm)

- Medium Precision (50–200 µm)

- Low Precision (>200 µm)

By Workflow Integration

- Standalone Systems

- Integrated Digital Workflows

By Deployment

By Application

- Metrology & Inspection

- Reverse Engineering

- Design & Prototyping

- Surveying & Mapping

- Visualization & Digitization

By End-use Industry

- Automotive

- Aerospace & Defense

- Healthcare

- Construction & Infrastructure

- Energy & Utilities

- Media & Entertainment

- Others

Regional Analysis

Leading Region by Market Share

North America is expected to lead the 3D scanning market with around 40.0% share in 2026, driven by strong adoption in automotive, aerospace, and healthcare industries. The region benefits from advanced manufacturing infrastructure, high R&D investment, and early technology adoption. Increasing use of automation, digital twins, and precision engineering further strengthens its dominance in the global market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia Pacific is the fastest-growing 3D scanning market due to rapid industrialization, expanding manufacturing, and rising automation adoption. Growth is driven by strong demand from automotive, electronics, and construction sectors. Government support for smart manufacturing and digital transformation is further accelerating regional expansion.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the 3D scanning market is characterized by strong innovation-driven rivalry focused on accuracy, speed, and automation capabilities. Companies are investing heavily in AI integration, cloud-based solutions, and portable scanning technologies to strengthen their market position. Competition is intensifying around product differentiation, software-hardware integration, and workflow automation solutions. Strategic collaborations, mergers, and technological advancements are key approaches used to gain competitive advantage in the market.

Some of the prominent players in the Global 3D Scanning Market are:

- Hexagon AB

- FARO Technologies Inc.

- Trimble Inc.

- Nikon Corporation

- Carl Zeiss AG

- Creaform Inc.

- 3D Systems Corporation

- Autodesk Inc.

- Topcon Corporation

- Artec 3D

- GOM GmbH

- Konica Minolta Inc.

- Shining 3D Tech Co. Ltd.

- Maptek Pty Ltd

- RIEGL Laser Measurement Systems GmbH

- CyberOptics Corporation

- Jenoptik AG

- Revopoint 3D Technologies Inc.

- Photoneo s.r.o.

- Polyga Inc.

- Other Key Players

Recent Developments

- July 2025: AMETEK completed the acquisition of FARO Technologies, strengthening its position in 3D metrology, laser scanning, and digital reality solutions.

- April 2025: Artec 3D introduced its metrology-grade Artec Point 3D scanner in India, expanding advanced scanning solutions for engineering, healthcare, and industrial inspection applications.

- March 2025: SCANOLOGY launched its next-generation 3D scanning systems focused on high-precision industrial digitization and smart manufacturing applications, enhancing real-time measurement and metrology capabilities.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 8.6 Bn |

| Forecast Value (2035) |

USD 21.2 Bn |

| CAGR (2026–2035) |

10.5% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Design (Hardware, Software, Services), By Scanner Type (Laser Scanners, Structured Light Scanners, Optical Vision Scanners, Photogrammetry Systems), By Range (Short Range, Medium Range, Long Range), By Form Factor (Tripod-mounted, Handheld, Fixed Inline, Robotic-mounted), By Accuracy Level (High Precision ≤50 µm, Medium Precision 50–200 µm, Low Precision >200 µm), By Workflow Integration (Standalone Systems, Integrated Digital Workflows), By Deployment (On-premise, Cloud-enabled), By Application (Metrology & Inspection, Reverse Engineering, Design & Prototyping, Surveying & Mapping, Visualization & Digitization), By End-use Industry (Automotive, Aerospace & Defense, Healthcare, Construction & Infrastructure, Energy & Utilities, Media & Entertainment, Others). |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the 3D Scanning Market?

▾ The global 3D scanning market is projected to reach USD 8.6 billion in 2026 and expand significantly to USD 21.2 billion by 2035, driven by increasing adoption across industrial, healthcare, and construction applications.

What is the CAGR of the 3D Scanning Market from 2026 to 2035?

▾ The market is expected to grow at a compound annual growth rate (CAGR) of 10.5% during the forecast period 2026 to 2035.

What factors are driving the growth of the 3D Scanning Market?

▾ The growth is driven by rising demand for industrial automation, digital twin technology, precision metrology, reverse engineering, and 3D imaging solutions. Increasing adoption of smart manufacturing and Industry 4.0 practices is further accelerating market expansion.

What are the major trends in the 3D Scanning Market?

▾ Key trends include integration of AI in point cloud processing, cloud-based 3D scanning platforms, portable and real-time scanning systems, and growing use in AR/VR and digital twin ecosystems.

Which region held the largest share of the 3D Scanning Market in 2026?

▾ North America held the largest share of the market in 2026, supported by advanced manufacturing infrastructure, strong R&D investment, and early adoption of 3D scanning technologies.

Which region is expected to grow the fastest in the 3D Scanning Market?

▾ Asia Pacific is expected to be the fastest-growing region, driven by rapid industrialization, expanding automotive and electronics manufacturing, and increasing government support for digital transformation.

Who are the key players in the 3D Scanning Market?

▾ Hexagon AB, FARO Technologies Inc., Trimble Inc., Nikon Corporation, Carl Zeiss AG, Creaform Inc., 3D Systems Corporation, Autodesk Inc., Topcon Corporation, Artec 3D, GOM GmbH, Konica Minolta Inc., Shining 3D Tech Co. Ltd., Maptek Pty Ltd, RIEGL Laser Measurement Systems GmbH, CyberOptics Corporation, Jenoptik AG, Revopoint 3D Technologies Inc., Photoneo s.r.o., Polyga Inc., and Other Key Players.