Market Snapshot

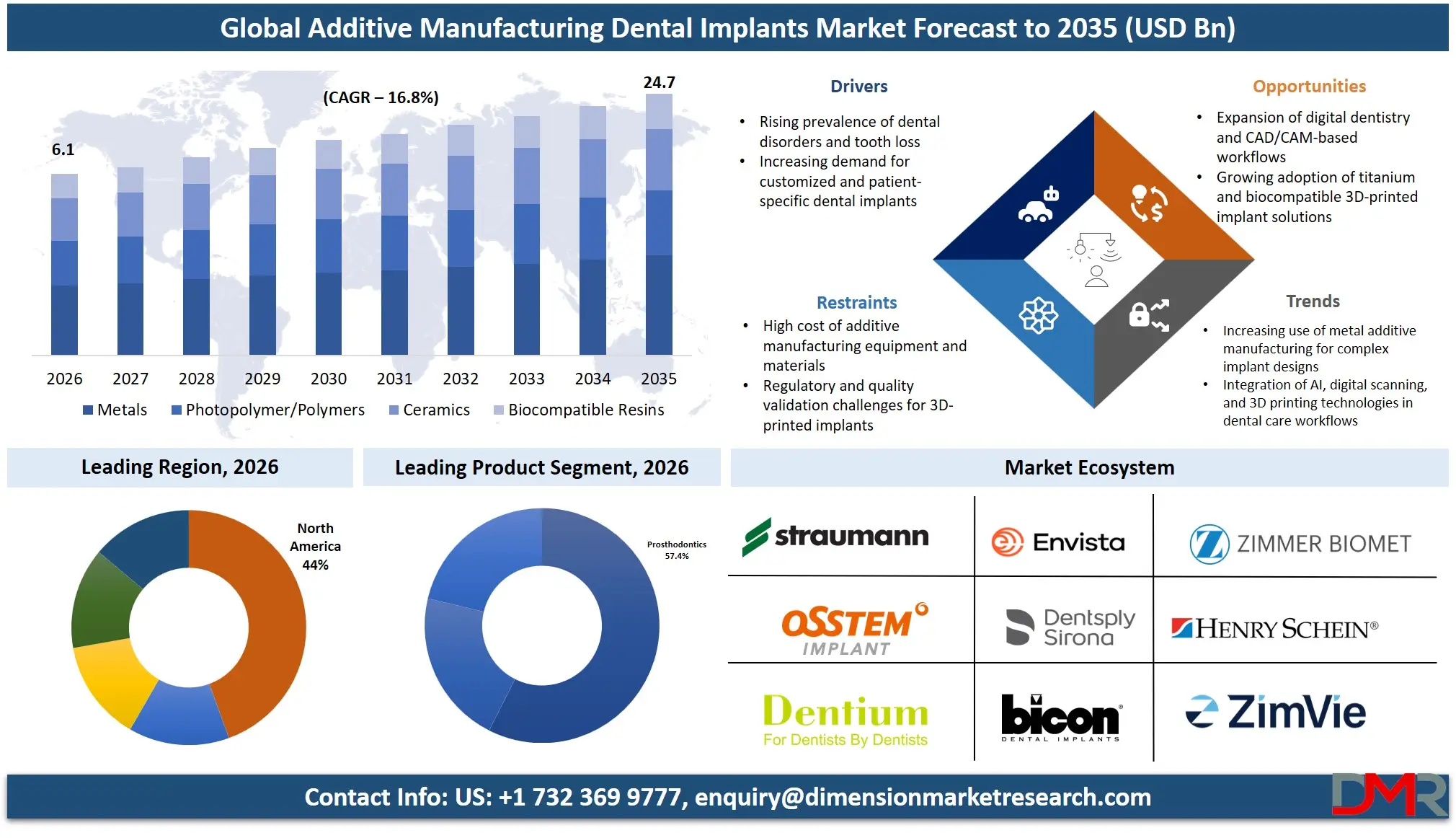

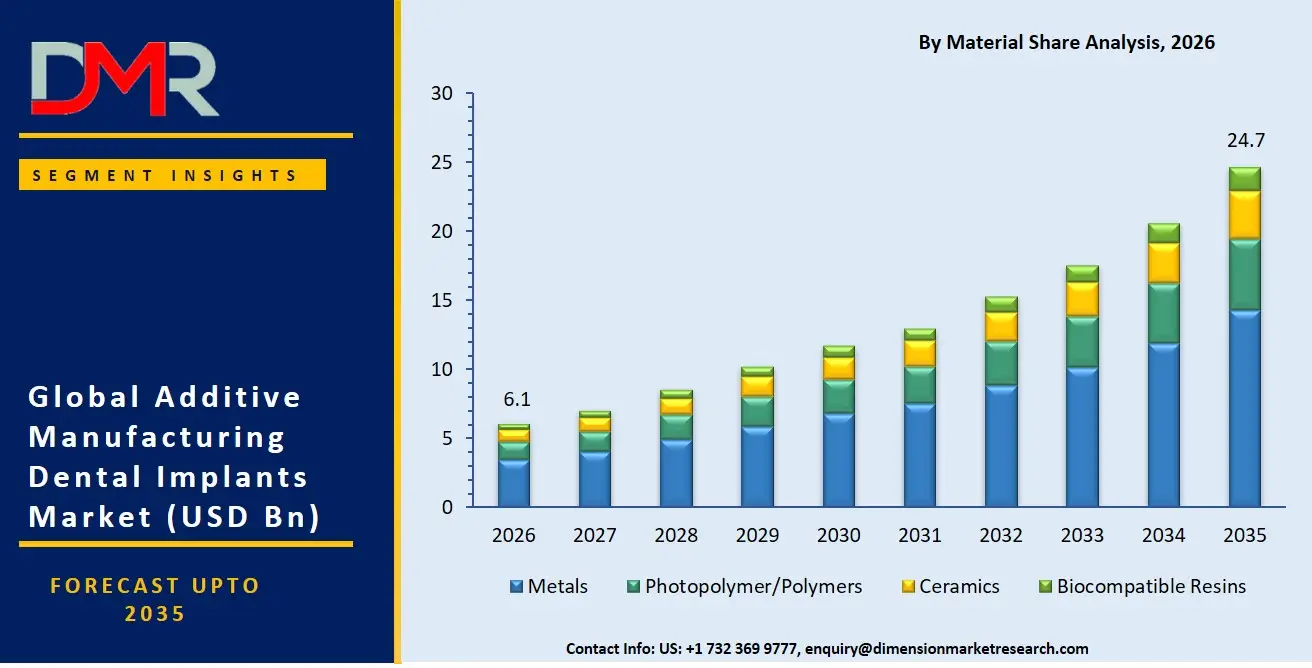

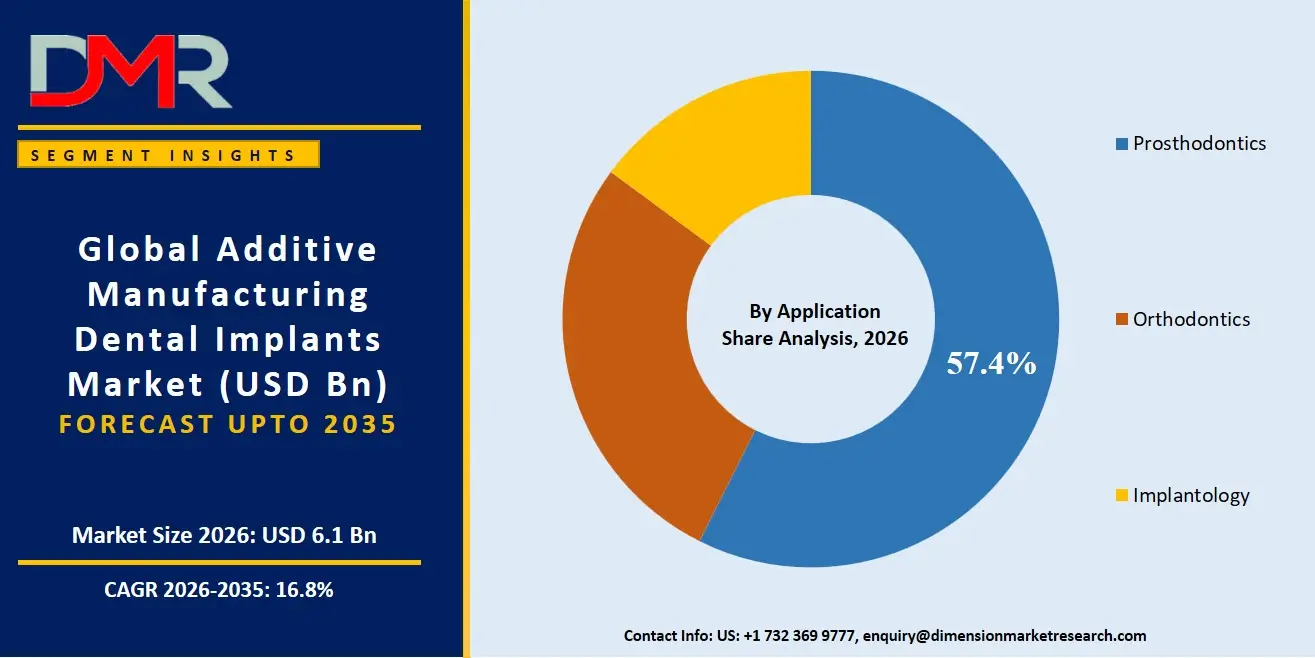

- The global Additive Manufacturing Dental Implants Market is valued at USD 5.2 Billion in 2025, reached USD 6.1 Billion in 2026, and is projected to hit USD 24.7 Billion by 2035 at a CAGR of 16.8%.

- By Material, Metals hold the dominant position with a 57.8% revenue share in 2026.

- By Technology, Laser Beam Melting (LBM) leads with a 48.6% revenue share in 2026.

- By Application, Prosthodontics accounts for the largest share at 57.4% in 2026.

- By End-User, Hospitals and Surgical Centers hold a 45.7% revenue share in 2026.

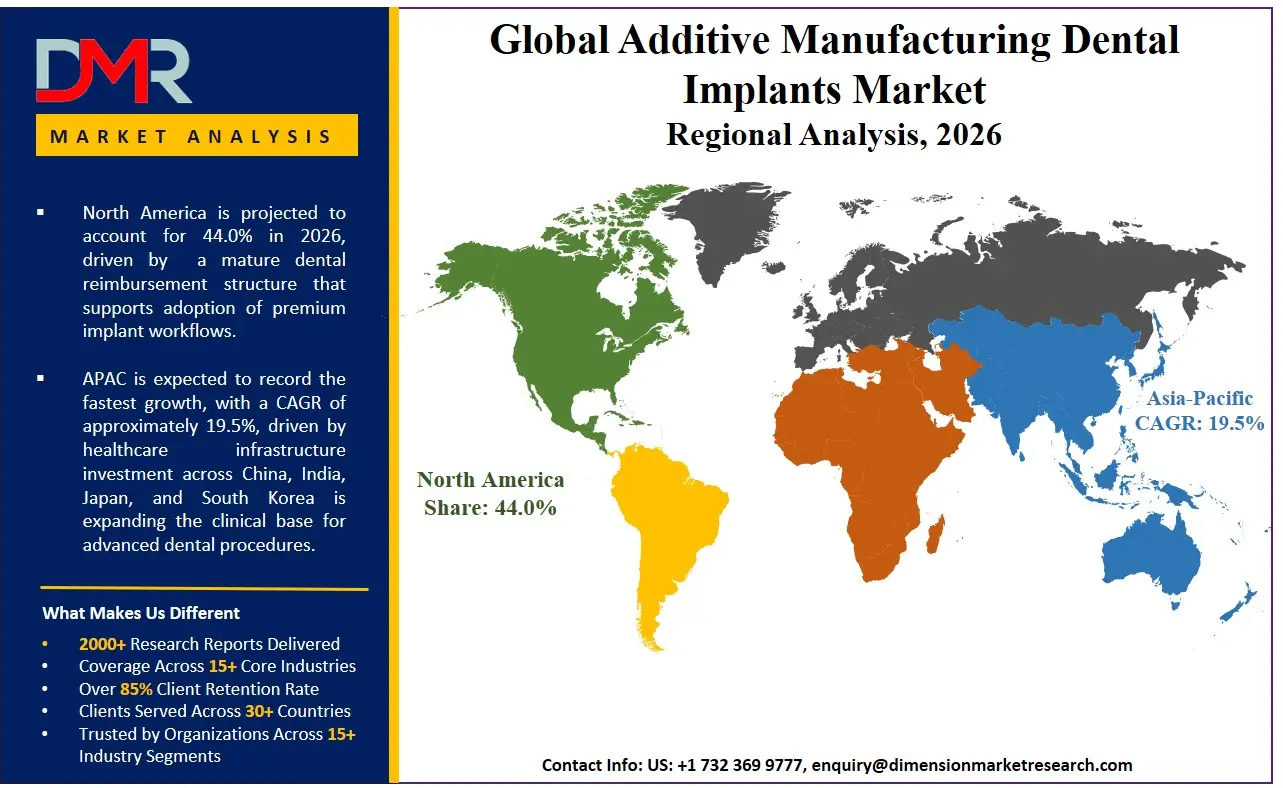

- North America leads all regions with a 44.0% market share, valued at USD 2.7 Billion in 2026.

Market Overview

The additive manufacturing dental implants market covers the production of dental implants, surgical guides, prosthetics, and implant-supported restorations using 3D printing technologies. Metal-based and polymer-based systems operate across clinical, laboratory, and point-of-care settings. Conventionally machined or cast implants produced outside layer-by-layer additive processes fall outside this market's scope.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This market connects directly to the broader digital dentistry ecosystem, including intraoral scanning, CAD/CAM design software, and cloud-based treatment planning. Dental practices are replacing analogue impression workflows with fully digital ones. Manufacturers are expanding biocompatible material portfolios to support a wider set of clinical indications. Both shifts expand the addressable base for additive systems simultaneously.

A November 2024 PubMed-indexed clinical trial of 20 participants measured mean initial ISQ stability values for 3D-printed guide-assisted implant placement at 76 ±8, against 69 ±13 for conventional thermoplastic guides. A UNC clinical assessment separately quantified mean angular deviations for stereolithographic guide-assisted surgery at 3.1°, with platform and apex deviations of 1.6 mm and 1.8 mm respectively. These two benchmarks define the current accuracy ceiling for additive-guided procedures and give manufacturers a measurable target for next-generation system improvement.

Market Size and Forecast

The Global Additive Manufacturing Dental Implants Market size is estimated at USD 6.1 Billion in 2026 from USD 5.2 Billion in 2025, and is projected to reach USD 24.7 Billion by 2035, exhibiting a CAGR of 16.8% during the forecast period.

This baseline of USD 5.2 Billion in 2025 reflects broad adoption across hospital systems, dental laboratories, and emerging chairside production models. The forecast to USD 24.7 Billion by 2035 implies the market will nearly quintuple in absolute value over a decade. Continued expansion of biocompatible resin portfolios by firms such as Formlabs, EnvisionTEC, and SprintRay underpins materials-side growth. FDA and EU MDR regulatory approvals for new additive materials must also continue at a pace sufficient to expand clinical indications for printed implants and prosthetics.

Faster-than-expected adoption of chairside 3D printing by dental service organizations represents the primary upside scenario for this forecast. Asia-Pacific healthcare infrastructure investment advancing at a 18.6% CAGR through 2034 would add substantial volume ahead of schedule in an upside case. The binding downside risk is the FDA Custom Device Exemption, which caps point-of-care 3D-printed custom implant production at 5 units per year per manufacturer. Without policy reform on this ceiling, U.S. point-of-care adoption remains structurally constrained through the forecast period.

Market Dynamics

Precision Gains and Biocompatible Material Expansion Drive Structural Adoption

Additive manufacturing reduces implant placement deviation to 1.3 degrees, a measurable precision gain over conventional methods that directly reduces revision procedure rates. Formlabs received FDA 510(k) clearance for its Premium Teeth Resin in August 2024, covering temporary crowns, inlays, onlays, veneers, and up to seven-unit temporary bridges. This clearance confirms that polymer-based additive outputs are moving steadily toward permanent clinical applications, expanding the commercial case for adoption beyond surgical guides alone.

Providers who previously used 3D printing only for surgical guides can now apply it to final restorations and prosthetics. Buyers treat additive workflows as a risk-reduction tool, not merely a production efficiency tool. This shift in purchasing rationale is structurally important because it moves the adoption decision from capital budget committees to clinical leadership.

Regulatory Burden and Capital Costs Constrain Smaller Operators

Manufacturers must satisfy stringent FDA 510(k) and biocompatibility requirements before commercializing any new additive material or system. This pre-commercialization runway is asymmetric. Larger firms with dedicated regulatory teams absorb it more efficiently than smaller innovators, concentrating market access among established platform providers.

High entry costs for industrial-grade additive systems persist for single-chair private practices in 2026. A practice managing one location cannot justify the capital investment that a dental service organization spreads across dozens of sites. Current market structure therefore favors institutional buyers over independent practitioners, a dynamic that shapes both distribution strategy and product positioning across the forecast period.

Asia-Pacific Infrastructure, Bone Regeneration, and Academic Pipelines Open Growth Pathways

Bone regeneration capabilities emerge as an opportunity through integration of stem cell therapy and 3D-printed scaffold architectures in 2026. Additive manufacturing shifts from a production method to an enabling platform for regenerative dentistry. Firms developing IP at this intersection stand to differentiate beyond current commodity printing services.

Dental schools incorporating advanced 3D printing curricula in 2026 create a downstream demand pipeline that compounds over time. Clinicians trained on additive workflows at school will specify them in practice. Manufacturers partnering with academic institutions now are effectively locking in the next generation of buyers before competitors establish those relationships.

Market Trends

Smart Implants, AI Integration, and Nano-Textured Surfaces Redefine the 3D-Printed Implant Performance Standard

Smart implant technology emerges as an industry standard for monitoring tissue health through integrated sensor systems in 2026. Straumann Group launched the MIDAS chairside 3D printer in June 2025, co-developed with SprintRay, completing an integrated chairside workflow connecting intraoral scanning, planning software, and in-practice additive production. This launch signals that chairside production has crossed from concept to commercial deployment, compressing fabrication turnaround from days to hours for dental service organizations. Nanotechnology integration enhances implant osseointegration as manufacturers adopt nano-textured surface treatments in 2025, giving clinically defensible differentiation that purchasing committees must weigh against price. AI-driven design software deepens integration between intraoral scanners and 3D printing platforms in 2026, reducing manual steps and lowering the skill barrier for broader adoption.

Material Analysis

Metals lead the By Material segment with a 57.8% share, reflecting titanium's unmatched load-bearing validation across decades of peer-reviewed clinical evidence. Additive manufacturing extends this advantage by enabling complex lattice geometries that improve bone ingrowth without compromising structural integrity. No competing material currently matches titanium's combination of mechanical performance and regulatory acceptance for permanent load-bearing implant applications.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Photopolymers and Polymers serve primarily as materials for surgical guides, temporary prosthetics, and implant models rather than final load-bearing implants. Ceramics address metal-free implant needs for patients with titanium sensitivity or anterior aesthetic requirements, though precise sintering controls add process complexity that limits broader adoption. Biocompatible Resins support the fastest-growing application area within the material segment, chairside and direct-print workflows, with regulatory precedent now established for direct-print dental devices that manufacturers are actively extending toward implant-supported components.

Technology Analysis

Laser Beam Melting (LBM) accounts for 48.6% of the By Technology segment, driven by its ability to produce fully dense titanium implant bodies with mechanical properties equivalent to machined parts. This output satisfies the load-bearing requirements that regulatory bodies and clinicians demand for permanent implant applications. LBM's dominance directly mirrors the metals-first clinical bias that gives the material segment its own concentration at the top.

Vat Photopolymerization serves as the umbrella technology for resin-based additive processes and functions as the gateway through which smaller practices and dental laboratories enter additive workflows, given its lower capital cost relative to metal powder bed systems.

Stereolithography (SLA) remains the established standard for surgical guide production, supported by a strong clinical evidence base confirming fewer deviations from preoperative plans versus thermoplastic guides.

Digital Light Processing (DLP) differentiates through throughput, curing entire layers simultaneously, making it the technology of choice for high-volume direct-print workflows where per-unit production cost is the primary competitive metric.

Selective Laser Sintering (SLS) occupies a niche for polymer-based dental components requiring mechanical durability beyond standard resin capabilities, while Electron Beam Melting (EBM) produces lower residual stress titanium structures but remains limited to specialized manufacturers due to higher equipment cost and lower throughput.

By Application Analysis

Prosthodontics captures 57.4% of segment demand, as crowns, bridges, dentures, and implant-supported restorations represent the highest-frequency implant-related procedures in clinical practice. Additive manufacturing reduces fabrication time and cost for these outputs, making prosthodontics the primary commercial driver of dental 3D printing adoption across the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Orthodontics represents the segment where additive manufacturing first achieved industrial scale, though its intersection with the implant market remains primarily through implant-adjacent prosthetic planning rather than direct implant output.

Implantology as a standalone application covers direct production of implant bodies, surgical guides, and bone augmentation scaffolds. This segment will gain share as bone regeneration and scaffold technologies mature through 2035, gradually closing the gap with prosthodontics in revenue contribution.

By End-User Analysis

With a 45.7% share, Hospitals and Surgical Centers hold the strongest position due to high procedural volumes and capital budgets that fund industrial-grade additive systems. Their procurement decisions set the adoption standard that other end-user categories follow, making them the primary reference accounts for hardware and materials vendors seeking market credibility.

Dental Laboratories function as the production backbone of the additive dental implant supply chain, serving multiple clinical accounts simultaneously and absorbing new material certifications efficiently.

Dental Clinics represent the emerging chairside segment most directly targeted by affordable in-practice systems, with dental service organizations managing multi-clinic networks as the most likely near-term adopters.

Academic and Research Institutes drive long-cycle technology validation while creating immediate demand for additive hardware and materials, functioning as a leading indicator of commercial adoption in the regions they serve.

By Implant Design / Morphology Analysis

Custom Root-Analogue Implants represent the design category most aligned with additive manufacturing's core capability, patient-specific geometry matching the precise morphology of the extracted tooth socket. This is the single strongest clinical argument for additive over subtractive production in implantology.

Single-Root Standard Implants constitute the highest-volume category, where additive manufacturing must compete on cost and throughput rather than design uniqueness to unlock the largest addressable volume in this segment.

Multi-Root Implants address anatomically complex replacement cases requiring internal channel architectures and variable cross-sections that additive manufacturing enables with a clear technical advantage over conventional methods.

Zygomatic Implants are used in patients with severe maxillary bone loss, sometimes exceeding 50 mm in length, with complex angulation requirements that make additive manufacturing a natural production fit despite remaining a low-volume, high-complexity sub-segment.

By Production Workflow Analysis

Lab-based 3D Printing currently accounts for the majority of additive dental implant production. Dental laboratories operate validated workflows, maintain material certifications, and serve multiple clinical accounts simultaneously, giving them throughput and compliance efficiency that individual practices cannot replicate. Lab-based production remains the default channel for regulated implant-grade additive output in 2026.

Chairside 3D Printing is the workflow the industry is actively building toward. Affordable in-practice systems are shifting economics for high-volume multi-location dental operators by compressing fabrication turnaround from days to hours. For dental service organizations, this compression directly improves patient throughput and appointment economics at scale.

By Surface Modification Technology Analysis

Laser-Modified Surfaces represent the next generation of implant surface engineering, with nano-textured laser treatments promoting faster and more reliable bone-to-implant contact at the nanoscale level. Clinical evidence linking surface modification to osseointegration outcomes is making laser treatment a meaningful differentiator in premium implant positioning, though revenue share data for this sub-segment is not currently available.

Sandblasting and Acid Etching (SLA) remains the established surface modification standard across the conventional and additive implant market. Decades of clinical validation and lower process cost sustain its widespread adoption. As nano-textured laser surfaces demonstrate superior performance metrics, SLA surface treatment faces gradual displacement in premium product tiers, a transition that additive implant manufacturers are actively navigating in their product roadmaps.

Key Market Segments

By Material

- Metals

- Photopolymer/Polymers

- Ceramics

- Biocompatible Resins

By Technology

- Laser Beam Melting (LBM)

- Vat Photopolymerization

- Stereolithography (SLA)

- Digital Light Processing (DLP)

- Selective Laser Sintering (SLS)

- Electron Beam Melting (EBM)

By Application

- Prosthodontics

- Orthodontics

- Implantology

By End-User

- Hospitals & Surgical Centers

- Dental Laboratories

- Dental Clinics

- Academic and Research Institutes

By Implant Design / Morphology

- Custom Root-Analogue Implants

- Single-Root Standard Implants

- Multi-Root Implants

- Zygomatic Implants

By Production Workflow

- Lab-based 3D Printing

- Chairside 3D Printing

By Surface Modification Technology

- Laser-Modified Surfaces

- Sandblasting and Acid Etching (SLA)

Regional Analysis

North America holds a 44.0% share of the global market, valued at USD 2.7 Billion in 2026. This position reflects the region's concentration of major additive manufacturing firms alongside a mature dental reimbursement structure that supports adoption of premium implant workflows. The FDA regulatory framework, while demanding, creates a validated market where cleared products command pricing power unavailable in less-regulated regions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe benefits from harmonized regulatory pathways through EU MDR, with back-to-back certifications from major platforms in early 2026 signaling accelerating institutional adoption across Germany, France, and the UK. Asia-Pacific advances at a 18.6% CAGR through 2034, the highest regional growth rate in the data, driven by healthcare infrastructure investment across China, India, Japan, and South Korea expanding the clinical base for advanced dental procedures.

Latin America remains an early-stage market concentrated in Brazil and Mexico, where private dental sector awareness of digital workflow gains is rising but limited capital availability constrains near-term penetration. The Middle East and Africa market centers on GCC countries, where public healthcare investment in Saudi Arabia and the UAE includes dental infrastructure modernization that creates institutional entry points for additive system vendors.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The additive manufacturing dental implants market is moderately consolidated at the technology platform level but fragmented at the materials and applications layer. A small number of firms control dominant hardware platforms in metal powder bed fusion and vat photopolymerization, while a larger ecosystem of resin and material suppliers competes for consumables revenue across those platforms. Stratasys consumables revenue reached USD 66.3 million in Q1 2024, growing 9.6%, confirming that the consumables layer rather than hardware is where recurring value accrues among installed base leaders.

Consolidation is compressing the competitive space. Align Technology's 2024 acquisition of Vienna-based Cubicure brought hot-lithography additive technology in-house, while 3D Systems and Stratasys merged industrial portfolios in 2025 to dominate production workflows.

These moves raise the capability threshold required to remain relevant as a standalone platform vendor and push competitive differentiation toward materials science, regulatory breadth, and clinical workflow integration. Firms unable to compete across all three dimensions simultaneously face structural pressure to exit or specialize in narrower clinical niches through the forecast period.

Company Profiles

3D Systems, Inc. positions itself as a full-stack dental additive manufacturing provider competing across hardware, materials, and workflow software. Its Q1 2026 Healthcare division grew 21% year-over-year with gross margin improving to 35.9%, signaling recovery underpinned by dental materials volume gains following a period of customer concentration risk. A February 2026 expansion of its NextDent Jetted Denture Solution portfolio and a nearly USD 250 million clear aligner manufacturing contract confirm that 3D Systems is broadening its dental revenue base beyond any single customer relationship.

Stratasys Ltd. competes through a consumables-led revenue model with dental resins embedded in a broader healthcare and industrial portfolio. Full-year 2025 Adjusted EBITDA reached USD 28.5 million, up from 2024, with dental 3D printing identified as a strategic growth vertical. A December 2025 release of next-generation Form Cure and Form Cure L post-processing units by partner Formlabs, combined with Stratasys's own CE Class IIa certification for TrueDent resins in March 2026, extended its regulatory footprint directly into European clinical accounts operating under EU MDR compliance requirements.

Key Players

- 3D Systems, Inc.

- SprintRay Inc.

- Stratasys Ltd.

- Formlabs, Inc.

- Renishaw plc

- Dentsply Sirona Inc.

- Carbon, Inc.

- EnvisionTEC, Inc.

- SLM Solutions Group AG

Supply Chain and Value Chain Analysis

The additive manufacturing dental implant value chain begins with titanium powder producers, photopolymer resin manufacturers, and ceramic compound suppliers. Titanium powder quality directly determines implant mechanical properties and regulatory compliance outcomes. Suppliers operating to aerospace-grade specifications sit at a strategically critical position with limited substitutability at the quality tier required for implant-grade production. The FDA requirement that prefabricated implants meet Class II 510(k) standards and custom implants potentially Class III Premarket Approval means post-processing and validation are compliance-critical functions, not commodity steps.

Hardware manufacturers producing LBM systems and vat photopolymerization platforms occupy the next layer while simultaneously supplying proprietary consumables, creating a vertically integrated model that captures recurring revenue independent of hardware replacement cycles.

Downstream, dental laboratories and hospital production centers convert raw prints into clinically validated outputs through post-processing, sterilization, and quality control. The shift to chairside production compresses this chain by eliminating the laboratory intermediary for certain prosthetic outputs, with the FDA Custom Device Exemption cap of 5 units per year per manufacturer representing the primary bottleneck preventing full realization of chairside additive manufacturing's efficiency potential at the clinical delivery layer.

Regulatory Landscape

The United States regulatory framework classifies prefabricated titanium and zirconia dental implants, abutments, and bridges as Class II devices requiring FDA 510(k) clearance. Custom dental implants incorporating new materials or biologics fall under Class III, requiring Premarket Approval. This two-tier classification governs all additively manufactured dental implants in the U.S. market, meaning the regulatory pathway a manufacturer follows directly determines its speed to commercialization and its addressable clinical indications at launch.

Biocompatibility requirements add a parallel validation burden to every new material entering the market. LuxCreo's Dental Clear Aligner resin received FDA Class II 510(k) clearance in 2022 as the first direct-print clear aligner material, establishing the regulatory precedent that manufacturers are now extending toward implant-supported components.

In Europe, the EU Medical Device Regulation framework governs dental additive manufacturing under CE marking requirements, with more stringent post-market surveillance and clinical evidence standards introduced after 2021. Firms with established regulatory teams and prior cleared products carry institutional knowledge that accelerates future submissions, concentrating the regulatory advantage firmly among established platform providers and raising the effective barrier for new market entrants.

Investment and White Space Analysis

Investment is currently concentrated at the platform and materials layer, with capital directed toward regulatory clearances and chairside system development. The most underserved segment is small-to-mid-size dental clinics, where capital expenditure barriers prevent independent practices from accessing the full benefit of additive implant workflows.

No current major player has fully addressed this gap with a lower-cost pre-validated chairside system priced within single-location operator budgets, making it the clearest product white space in the market today. Stratasys full-year 2025 Adjusted EBITDA of USD 28.5 million, growing 9.6% from 2024, confirms that established players are generating returns sufficient to fund the next investment cycle in materials and regulatory expansion.

Asia-Pacific presents the clearest regional white space opportunity, advancing at a 18.6% CAGR through 2034 yet receiving disproportionately low infrastructure investment in dental additive manufacturing relative to that trajectory. Bone regeneration integration represents a technical white space with high-value potential.

No major additive dental manufacturer has achieved commercial-scale deployment of combined scaffold-and-implant additive workflows. Straumann's investment in 12,000 educational programs in 2024, with low-and-middle-income country attendance rising from 28% to 40% year-over-year, demonstrates that manufacturers willing to invest in clinical education today are seeding commercial pipelines that compound in value across the full forecast period.

Recent Developments

- April 2026: 3D Systems. EU MDR Certification. Secured Class IIa EU MDR certification for its NextDent Jetted Denture Solution, enabling clinical deployment across EU member states under the updated Medical Device Regulation framework.

- April 2026: 3D Systems. Financial Results. Healthcare Solutions division grew 21% year-over-year in Q1 2026, with gross margin improving to 35.9%, driven by higher dental materials volumes.

- March 2026: Stratasys. CE Certification. Achieved CE Class IIa certification for TrueDent resins in Europe, clearing the way for clinical use across European dental laboratories and institutional end-users.

- February 2026: 3D Systems. Portfolio Expansion. Expanded the NextDent Jetted Denture Solution portfolio, broadening additively manufactured dental prosthetic outputs available through its platform.

- December 2025: Formlabs. Product Launch. Released next-generation Form Cure and Form Cure L post-processing units, upgrading the post-print curing workflow for its dental resin platforms.

- April 2024: Formlabs. Product Launch. Launched the Form 4B 3D printer, adding a dedicated biocompatible printing platform to its dental and medical device lineup.

- April 2024: 3D Systems. FDA Clearance. Received FDA 510(k) clearance for its VSP PEEK Cranial Implant, with the additive workflow using up to 85% less material than equivalent machined implants.

- March 2024: 3D Systems. Commercial Contract. Secured a contract worth nearly USD 250 million for clear aligner manufacturing, the largest single dental additive contract publicly disclosed by the company.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 5.2 Billion |

| Market Value (2026) |

USD 6.1 Billion |

| Forecast Revenue (2035) |

USD 24.7 Billion |

| CAGR (2026 to 2035) |

16.8% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Material (Metals, Photopolymer/Polymers, Ceramics, Biocompatible Resins), By Technology (Laser Beam Melting, Vat Photopolymerization, Stereolithography, Digital Light Processing, Selective Laser Sintering, Electron Beam Melting), By Application (Prosthodontics, Orthodontics, Implantology), By End-User (Hospitals and Surgical Centers, Dental Laboratories, Dental Clinics, Academic and Research Institutes), By Implant Design / Morphology (Custom Root-Analogue Implants, Single-Root Standard Implants, Multi-Root Implants, Zygomatic Implants), By Production Workflow (Lab-based 3D Printing, Chairside 3D Printing), By Surface Modification Technology (Laser-Modified Surfaces, Sandblasting and Acid Etching) |

| Regional Analysis |

North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape |

3D Systems, Inc., SprintRay Inc., Stratasys Ltd., Formlabs, Inc., Renishaw plc, Dentsply Sirona Inc., Carbon, Inc., EnvisionTEC, Inc., SLM Solutions Group AG |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the biggest investment opportunity in Additive Manufacturing Dental Implants Market ?

▾ The clearest investment opportunity is affordable chairside additive systems for small-to-mid-size dental clinics. No major player has addressed this segment with a pre-validated, budget-accessible platform. Asia-Pacific infrastructure gaps relative to its 18.6% CAGR trajectory represent the strongest regional investment case through 2034.

Who are the top companies in Additive Manufacturing Dental Implants Market?

▾ Leading companies include 3D Systems, Inc., Stratasys Ltd., Formlabs, Inc., SprintRay Inc., Renishaw plc, Dentsply Sirona Inc., Carbon, Inc., EnvisionTEC, Inc., and SLM Solutions Group AG. These firms compete across hardware platforms, certified materials portfolios, and integrated clinical workflow solutions.

Which segment is growing fastest in Additive Manufacturing Dental Implants Market and why?

▾ Biocompatible Resins and chairside production workflows are growing fastest within their respective segments. Regulatory clearances expanding clinical indications for resin-based outputs, combined with the commercial arrival of affordable in-practice printing systems, are pulling adoption forward across dental service organizations managing multi-location networks.

Which region is growing fastest in Additive Manufacturing Dental Implants Market and why?

▾ Asia-Pacific is forecast to advance at a 18.6% CAGR through 2034, the highest regional rate in the data. Healthcare infrastructure investment across China, India, Japan, and South Korea is expanding the clinical base for advanced dental implant procedures faster than any other region in the forecast period.

What is the biggest challenge holding Additive Manufacturing Dental Implants Market back?

▾ The FDA Custom Device Exemption caps point-of-care custom implant production at 5 units per year per manufacturer, acting as a structural ceiling on U.S. chairside adoption. High capital expenditure requirements for industrial-grade systems simultaneously limit market access to institutional buyers, leaving independent practitioners largely unable to participate in additive implant workflows.