Market Snapshot

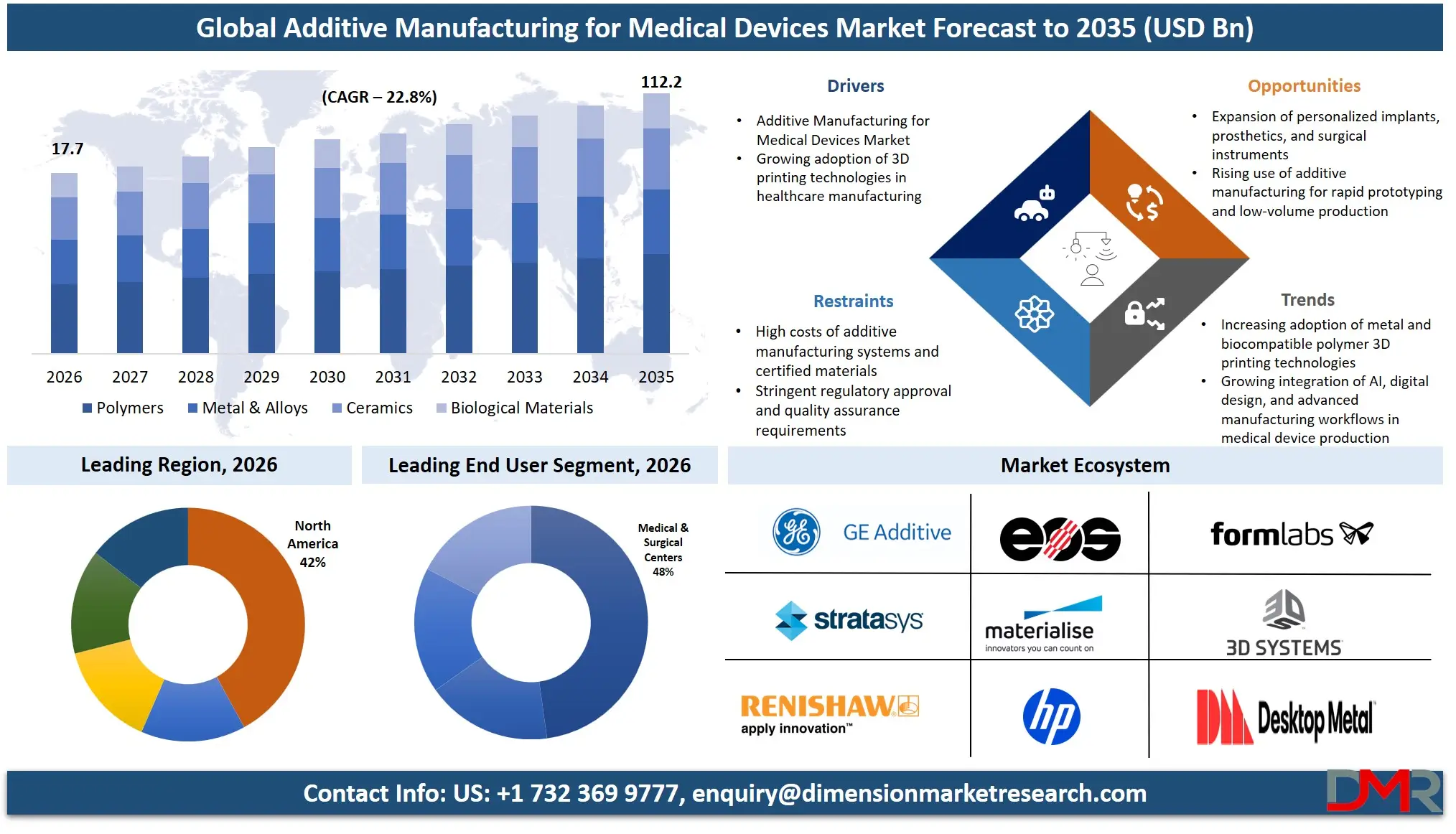

- The global Additive Manufacturing for Medical Devices Market is valued at USD 14.3 billion in 2025, reached USD 17.7 billion in 2026, and is projected to hit USD 112.2 billion by 2035 at a CAGR of 22.8%.

- By Application, Surgical Guides lead with a 51.8% revenue share in 2026.

- By Component, Equipment holds the largest share at 47.7% in 2026.

- By Technology, Laser Sintering dominates with a 32.2% revenue share in 2026.

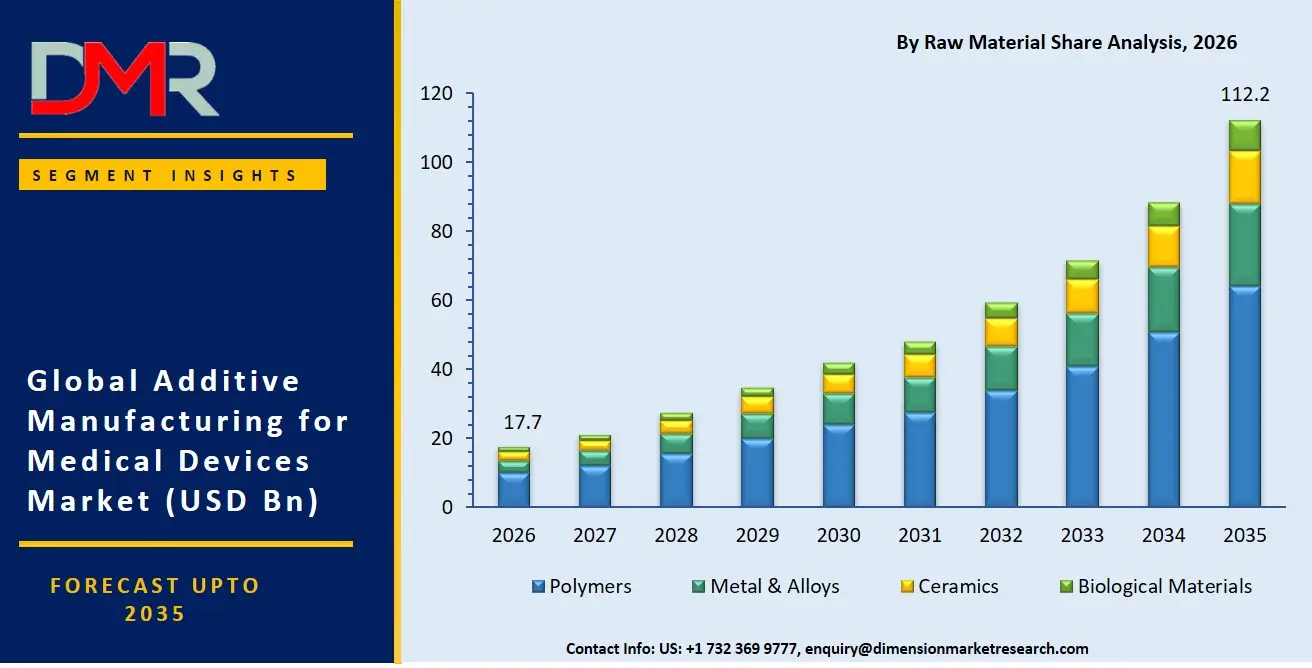

- By Raw Material, Polymers account for 57.2% of the revenue share in 2026.

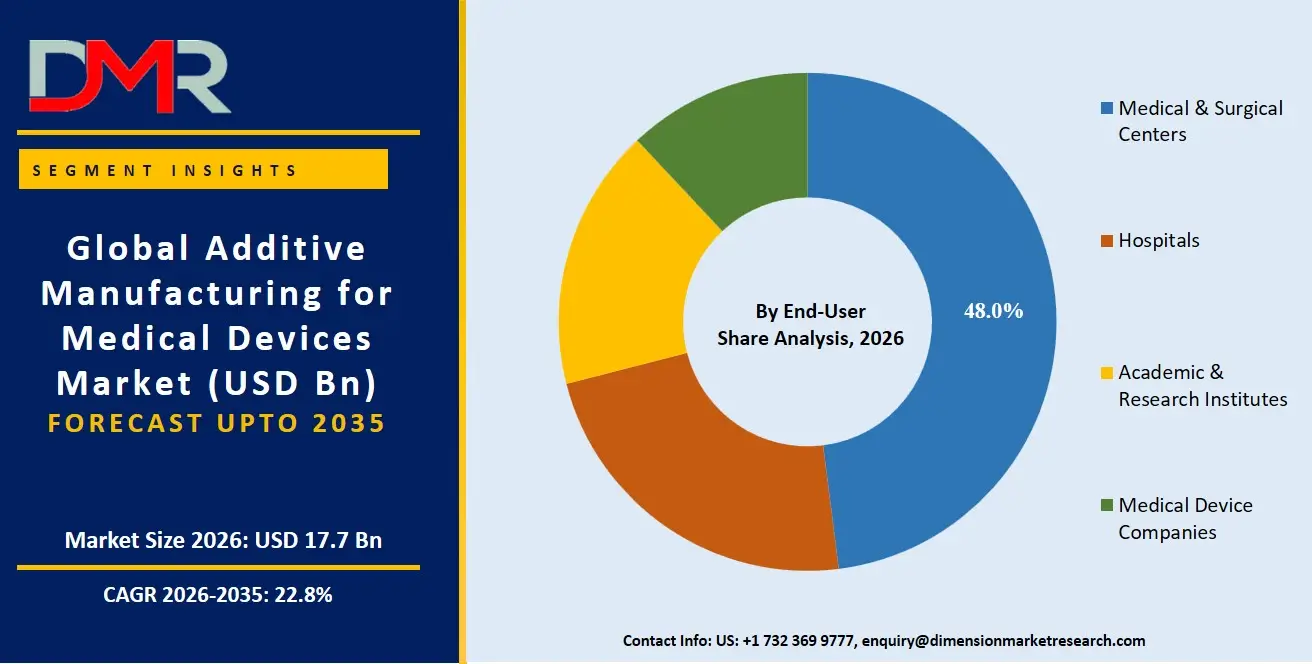

- By End-User, Medical and Surgical Centers lead with a 48.0% revenue share in 2026.

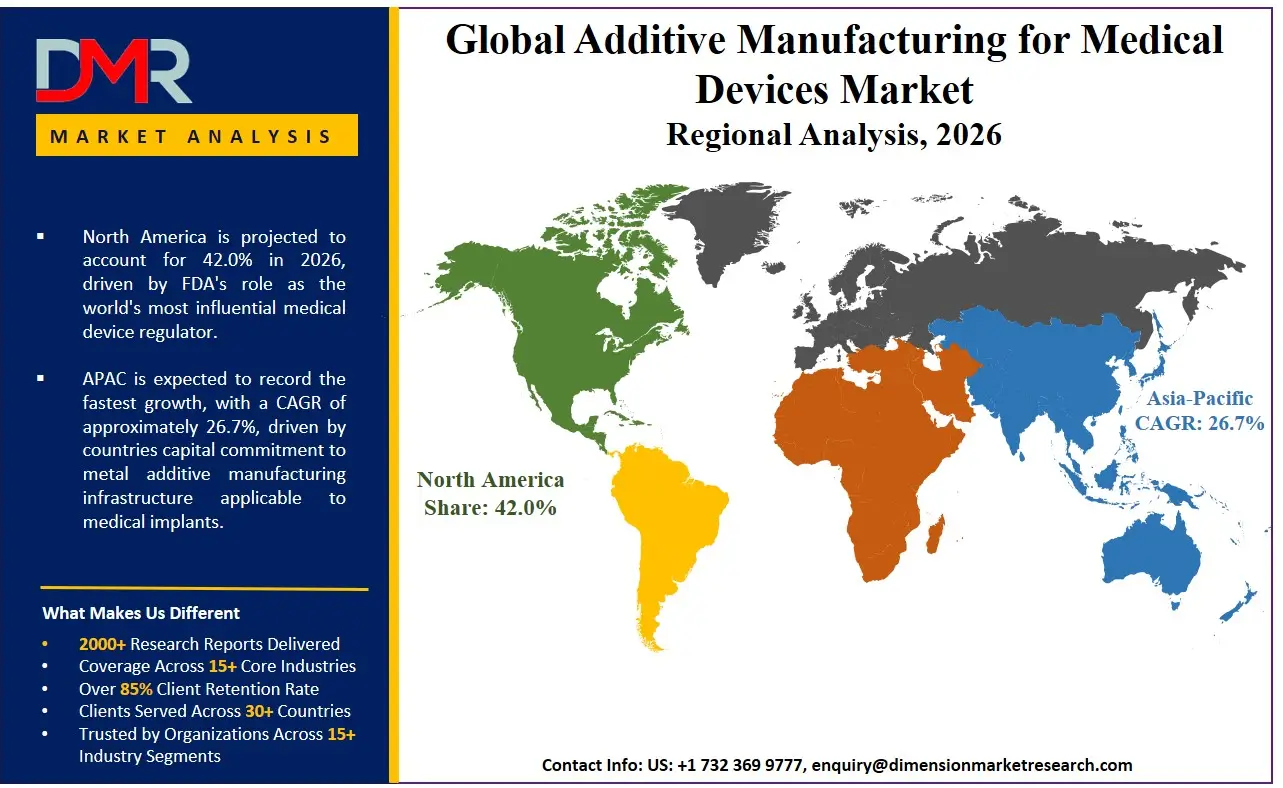

- North America is the dominant region with a 42.0% revenue share, valued at USD 7.4 billion in 2026.

Market Overview

The additive manufacturing for medical devices market covers commercial production, sale, and clinical deployment of 3D-printed components used in patient care. Surgical guides, implants, prosthetics, dental devices, orthopedic guides, external wearables, and tissue engineering applications fall within scope. General-purpose industrial 3D printing not intended for medical use sits outside this market's boundaries.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This market connects directly to FDA clearance timelines, hospital procurement cycles, and reimbursement policy changes. Each variable independently shapes how fast new products reach patients and generate commercial revenue. The market operates across five component categories, with Equipment holding the largest share at 47.7%, reflecting a capital deployment phase where hospitals and device companies are building internal printing capacity before shifting spend toward materials and workflow software.

A 2024 academic study published in PMC surveyed 23 hospitals and found that 54.5% had between 2 and 5 active 3D printing research projects in clinical use. Materialise Medical segment revenue grew 18.7% year-over-year in Q1 2025, with adjusted EBITDA margin improving to 32.0% in FY2025 from 30.6% in FY2024, as reported by Materialise. These two data points together confirm that clinical validation pipelines are converting into commercial financial performance at the market's leading software-enabled specialist.

Market Size and Forecast

The Global Additive Manufacturing for Medical Devices Market size is estimated at USD 17.7 Billion in 2026 from USD 14.3 Billion in 2025, and is projected to reach USD 112.2 Billion by 2035, exhibiting a CAGR of 22.8% during the forecast period.

Reaching USD 112.2 Billion by 2035 requires the market to multiply nearly 8x over a decade. That scale of expansion demands parallel advances in regulatory acceptance, clinical reimbursement, and hospital capital investment. All three are currently in motion. The forecast assumes continued FDA clearance activity for new device categories, sustained OEM capital investment in metal and polymer printing systems, and expanding hospital-based point-of-care printing programs converting research projects into commercial production units.

Blue Cross NC's April 2025 policy update recognizing FDA-approved 3D-printed orthopedic implants as medically necessary represents the upside catalyst most likely to pull demand forward. The cranial reconstruction market alone is anticipated to exceed USD 2 billion by 2030, per 3D Systems, creating a concentrated high-value subsegment with above-average margin potential for cleared platform vendors.

The binding downside risk is the absence of FDA-approved bioprinted implants as of mid-2024 and the FDA custom device exemption cap of five units per year per manufacturer outside standard 510(k) pathways. If product liability litigation risk materializes against 3D-printed device manufacturers, as flagged by legal analysts in 2025, underwriting costs could compress manufacturer margins and delay commercialization timelines across patient-specific device categories.

Market Dynamics

FDA Program Formalization and Clinical Validation of PEEK Implants Drive OEM Investment Decisions

The FDA's 2024 update to its 3D Printing of Medical Devices Program formally covered orthopedic, cranial, dental, and surgical instrument categories. Defined submission pathways now exist for product classes that previously faced ambiguous regulatory treatment. For manufacturers, this directly reduces development risk and enables capital investment decisions that could not previously be underwritten with confidence.

3D Systems' EXT 220 MED completed nearly 40 successful PEEK cranioplasty procedures across European hospitals before receiving FDA clearance in 2025, as reported by MDDI Online. This European clinical track record was central to securing U.S. approval and establishes the evidentiary model that other polymer implant manufacturers must replicate. In April 2025, 3D Systems and University Hospital Basel produced the world's first 3D-printed PEEK facial implant at the point-of-care using the same platform, extending the clinical precedent from cranial to facial reconstruction and confirming that point-of-care polymer implant production is now clinically operational.

Bioprinting Approval Gap and Custom Device Production Ceiling Constrain Commercial Scale

No FDA-approved 3D bioprinted implants existed as of mid-2024 despite active development pipelines at multiple companies. This gap is commercially significant because bioprinting represents the next logical step beyond polymer and metal implants. Without a cleared regulatory pathway, investment in commercial bioprinting infrastructure carries approval uncertainty that corporate finance teams will not underwrite at scale.

The FDA custom device exemption limits production to five units per year per manufacturer outside standard 510(k) pathways, as confirmed by the Pew Research Center. Legal analysts flagged 3D-printed medical devices as a potential next wave of product liability litigation in 2026. Both constraints affect how OEMs structure indemnity agreements with hospital partners and how hospitals manage procurement decisions, creating adoption friction that disproportionately affects smaller manufacturers without dedicated regulatory and legal infrastructure.

Cranial Reconstruction, Point-of-Care Programs, and Surgical Training Models Open Distinct Revenue Pathways

The cranial reconstruction market is anticipated to exceed USD 2 Billion by 2030, per 3D Systems, following the company's FDA-cleared PEEK implant launch in 2025. Additive manufacturing holds a structural advantage over traditional milling in this application specifically because of its ability to produce anatomically matched geometries that conventional subtractive manufacturing cannot replicate cost-effectively at patient-specific scale.

Stratasys' Digital Anatomy technology validated an ultrasound-guided breast biopsy training platform developed at Creighton University School of Medicine in 2025. Surgical training models carry no product liability exposure from patient contact and bypass the regulatory burden of implant clearance entirely. For additive manufacturing companies seeking margin-accretive revenue with shorter commercial cycles, medical education and training applications offer a structurally attractive segment that complements rather than competes with their regulated implant programs.

Market Trends

PEEK Polymer Adoption, Porous Lattice Architecture, and Cleanroom-Certified Systems Define the Next Production Standard

PEEK polymer is replacing titanium in select implant categories where weight, radiolucency, and elastic modulus matching to bone offer clinical advantages over metal. FDA clearance of 3D Systems' EXT 220 MED as the first platform for PEEK cranial implants in 2025 validates this substitution at the regulatory level, giving cleared PEEK implants the same commercial standing as titanium alternatives in cranial applications.

The FDA's 2024 program update explicitly highlighted porous lattice structures and osseointegration-enhancing internal geometries as a defining capability of additive manufacturing, signaling that regulatory reviewers now treat lattice architecture as a differentiating quality attribute. Manufacturers unable to demonstrate controlled porosity in implant designs face a competitive disadvantage as clinical buyers become more specification-literate.

Cleanroom-integrated printing systems are simultaneously becoming the production standard for implantable devices, with the EXT 220 MED establishing a contamination-control benchmark in 2025 that regulators will increasingly expect from other implant-grade printing systems entering the cleared device ecosystem.

Application Analysis

Surgical Guides lead the By Application segment with a 51.8% share, reflecting their well-established FDA clearance track record and direct integration into high-volume orthopedic and cranial procedures. Their single-use nature generates recurring revenue that implants, by contrast, do not produce at equivalent frequency. No competing application currently matches surgical guides on the combination of procedural volume, regulatory clarity, and revenue repeatability.

Medical Implants represent the segment with the most active regulatory development, with the FDA having cleared more than 100 additively manufactured medical devices, predominantly orthopedic implants, per Pew Research Center. Prosthetics serve patients requiring customized fit at a scale traditional manufacturing cannot economically support, benefiting directly from Polymers' dominant raw material position across the weight and flexibility characteristics clinical users require.

By Component Analysis

Equipment commands 47.7% of the By Component segment, driven by hospitals, OEMs, and contract manufacturers still in active infrastructure build-out across metal and polymer printing platforms. Capital investment at this layer sets the technical and regulatory ceiling for what device manufacturers can produce downstream. Biomaterials are the enabling input for implant-grade production most directly affected by FDA clearance activity, with each new material-device combination receiving clearance expanding the proportion of total component expenditure directed toward certified inputs.

Systems encompass integrated hardware-software-process environments that manufacturers deploy for production-grade additive output, with Germany's EOS GmbH representing the class of system-level vendors whose revenue scales with OEM production commitments rather than prototyping budgets.

By Technology Analysis

Laser Sintering accounts for 32.2% of the By Technology segment, reflecting its established role in producing titanium and cobalt-chrome implants at the precision and surface quality levels that orthopedic OEMs require. EOS GmbH's EOS M 300-4 system, used in regulated series production of titanium implants as confirmed by Lincotek, exemplifies the technology's clinical production credentials at industrial scale.

Laser Beam Melting serves dense metal part production where full material consolidation is required, complementing Laser Sintering in facilities producing both porous lattice and solid-geometry implants on the same manufacturing floor. Droplet Deposition serves applications where multi-material capability and anatomical accuracy matter more than structural load-bearing performance, with Stratasys' J750 and J5 MediJet printers using this technology class for surgical planning and training models.

By Raw Material Analysis

Polymers capture 57.2% of the By Raw Material segment, with FDA clearance of PEEK as an implant-grade polymer through 3D Systems' EXT 220 MED in 2026 reinforcing polymer's standing at the highest regulatory tier of the market beyond commodity device categories. Versatility across implant and non-implant applications gives polymers a breadth of addressable clinical volume that no other raw material category currently matches.

Metals and Alloys serve structurally demanding implant categories where mechanical load-bearing performance determines clinical safety, with Stryker's AMagine platform for titanium spinal implants and Renishaw's metal additive systems both operating in this category.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Ceramics offer biocompatibility and wear resistance relevant to dental and joint replacement applications but remain constrained to compressive loading scenarios where brittleness relative to metals and polymers does not compromise structural integrity.

Biological Materials hold the widest gap between technical potential and commercial reality, confined to research and preclinical applications pending implant-grade clearance, though the FDA's 2025 policy shift toward bioprinted tissue in drug testing creates a near-term revenue pathway that does not require implant-grade regulatory approval.

By End-User Analysis

Medical and Surgical Centers hold a 48.0% share, concentrating the highest procedural volumes for orthopedic, cranial, and dental applications: the three categories with the most active FDA clearance activity. Their procurement decisions set the adoption standard that other end-user categories follow, making them the primary commercial channel for both equipment procurement and consumables replenishment across the forecast period.

Hospitals are the primary site for point-of-care additive manufacturing programs, operating under 21 CFR Part 820 and 2017 FDA guidance requirements that concentrate viable in-house programs at larger, better-resourced institutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Academic and Research Institutes function as the clinical validation engine for this market, originating the European cranioplasty procedures that de-risked 3D Systems' FDA submission and the University of Michigan Health partnership that advanced Materialise's bioresorbable splint into pivotal trial.

Medical Device Companies represent the end-user category where additive manufacturing is most visibly transitioning from prototyping tool to full production platform, with Stratasys documenting four OEM deployment trends spanning prototyping, diagnostics, training, and production in 2026.

Key Market Segments

By Application

- Surgical Guides

- Medical Implants

- Prosthetics

- External Wearable Devices

- Tissue Engineering

- Dental

- Orthopedic Guides

By Component

- Equipment

- Biomaterials

- Systems

- Materials

- Software & Services

By Technology

- Laser Sintering

- Laser Beam Melting

- Droplet Deposition

- Stereolithography (SLA)

- Electron Beam Melting (EBM)

- Fused Deposition Modeling (FDM)

- Digital Light Processing (DLP)

- Photopolymerization

By Raw Material

- Polymers

- Metals & Alloys

- Ceramics

- Biological Materials

By End-User

- Medical & Surgical Centers

- Hospitals

- Academic & Research Institutes

- Medical Device Companies

Regional Analysis

North America holds a 42.0% revenue share valued at USD 7.4 billion in 2026, with the United States contributing 80.7% of that regional total. The U.S. concentration reflects the FDA's role as the world's most influential medical device regulator, having cleared more than 100 additively manufactured devices and created a commercial ecosystem that other regions have not yet replicated at equivalent scale. The FDA regulatory framework simultaneously functions as a market barrier and a pricing enabler, giving cleared products commercial standing unavailable in less-regulated geographies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe serves as the primary clinical validation geography for advanced additive applications before U.S. FDA clearance, with Germany hosting EOS GmbH, whose EOS M 300-4 metal system supports regulated titanium implant series production.

Stratasys signed a strategic MOU with VinUni and Vinmec in Vietnam in September 2025 to deploy 3D printing across medical education, research, and healthcare, signaling that Asia Pacific is building additive capacity through institutional partnerships ahead of commercial-scale procurement.

Latin America remains a downstream market tracking equipment procurement from established global vendors rather than independent device development, constrained by the absence of locally established regulatory clearance frameworks equivalent to the FDA's 510(k) pathway.

The Middle East and Africa market depends on government health system modernization programs at large hospital networks and academic medical centers to catalyze point-of-care printing adoption consistent with the institutional trend documented across surveyed hospitals in the 2024 PMC study.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The additive manufacturing for medical devices market is moderately fragmented, with pure-play additive specialists, large medical device OEMs, and diversified industrial technology companies competing across non-overlapping application strengths. No single player commands a dominant share across all application categories. Financial performance diverged sharply across the two most visible pure-play specialists in 2024 and 2025.

One leading player's Healthcare Solutions segment declined 21% to USD 40.4 million in Q4 2024, then recovered to USD 50.1 million in Q1 2026, a 21% year-over-year gain. A competing specialist grew its medical segment revenue 16.3% to EUR 37.0 million in Q4 2025, with Medical adjusted EBITDA reaching EUR 42.9 million in FY2025 versus EUR 35.6 million in FY2024. These divergent trajectories reflect differentiated product portfolios and application mix, not uniform market conditions.

Stratasys acquired Forward AM Technologies GmbH, formerly BASF's additive manufacturing materials business, in May 2025, positioning itself to control both printing hardware and material inputs for clinical production. Vertical integration of this kind raises switching costs for hospital and OEM customers who qualify materials as part of their quality system documentation.

Large medical device OEMs that have internalized additive manufacturing represent the competitive force most likely to reshape market structure over the next five years. When a major orthopedic company expands its internal metal printing facility for titanium spinal implants, it reduces procurement from external additive vendors while simultaneously competing with those vendors in the patient-specific implant segment, compressing the addressable market available to standalone additive specialists.

Company Profiles

3D Systems Corporation achieved the first FDA clearance for an additively manufactured PEEK cranial implant with its EXT 220 MED platform in 2026, following demonstration across nearly 40 cranioplasty procedures in European hospitals. Healthcare Solutions revenue reached USD 50.1 million in Q1 2026, up 21% year-over-year, with adjusted EBITDA turning positive at USD 2.1 million from a USD 23.9 million loss one year earlier.

A December 2025 FDA 510(k) clearance expanding VSP Orthopedics indications to skeletally mature adolescents and a nearly USD 250 million clear aligner manufacturing contract confirm that 3D Systems is building a multi-application dental and medical device revenue base that reduces exposure to single-customer concentration risk.

Materialise NV competes through software-enabled medical device workflows and anatomical planning services, which carry structurally higher margins than hardware sales. The medical segment adjusted EBITDA reached EUR 42.9 million in FY2025 with a 32.0% margin, up from EUR 35.6 million and 30.6% in FY2024, as reported by Materialise.

Stratasys Ltd. generated full-year 2025 revenue of USD 551.1 million with a GAAP gross margin of 41.2%, competing primarily through FDA-cleared anatomical model printers and OEM partnerships in the lower-regulatory-burden training and diagnostics segment.

Renishaw plc reached FY2025 revenue of GBP 713.0 million, up 3.1% from GBP 691.3 million in FY2024, with its Manufacturing Technologies division generating GBP 106.8 million in FY2024 revenue through integration of additive manufacturing with metrology and process control for regulated implant manufacturers.

Key Players

- 3D Systems Corporation

- Stratasys Ltd.

- Materialise NV

- Formlabs

- EOS GmbH

- Renishaw plc

- Nikon SLM Solutions

- GE Additive (Arcam EBM, Concept Laser)

- Desktop Metal / ETEC (EnvisionTEC)

- Nano Dimension Ltd.

- Nanoscribe GmbH

- Prodways Group

- Oxford Performance Materials Inc.

- Cyfuse Medical K.K.

- Axtra3D

- Medtronic

- Johnson & Johnson MedTech

- Stryker

- DePuy Synthes

- Zimmer Biomet

- Smith & Nephew

- Abbott Laboratories

- Siemens Healthineers

- GE Healthcare

- Philips Healthcare

- BD (Becton Dickinson)

- LimaCorporate

- Eminent Spine

- MedCAD

- LightForce Orthodontics

- Amnovis

- 3T Additive Manufacturing Limited

- Precision ADM Inc.

- Tecomet, Inc.

- Vaupell

- Arterex Medical

- Protolabs Inc.

- Amuse3D

Supply Chain and Value Chain Analysis

The additive manufacturing for medical devices value chain begins with raw material suppliers providing polymers, metals and alloys, ceramics, and biological materials. Equipment and systems vendors occupy the next layer and currently capture the largest share of market revenue, setting the technical and regulatory ceiling for what device manufacturers can produce. Stryker's AMagine Institute, operational since 2001 and expanded for titanium spinal implants in January 2024, represents a vertically integrated OEM model where design, printing, and clinical deployment are controlled within a single organization, concentrating margin at the OEM level and reducing dependence on external contract manufacturers.

Hospital point-of-care printing programs represent a structural shift in the traditional value chain. When hospitals print their own surgical guides or anatomical models internally, they capture value that would otherwise flow to commercial device suppliers. All manufacturers and hospital printing sites must comply with 21 CFR Part 820 Quality System Regulation and the 2017 FDA guidance on technical considerations for additive manufacturing, as confirmed by IMTS. This compliance burden concentrates viable point-of-care programs at large, well-resourced academic medical centers and limits the economic benefit of in-house production for smaller institutions that cannot sustain the operational infrastructure required to meet the same quality standards as commercial device manufacturers.

Regulatory Landscape

The U.S. FDA classifies additively manufactured medical devices under the same premarket notification framework as conventionally manufactured equivalents, with the 510(k) premarket notification pathway serving as the primary clearance route. The FDA has cleared more than 100 additively manufactured medical devices, predominantly orthopedic implants, per Pew Research Center. All manufacturers and hospital point-of-care printing sites must comply with 21 CFR Part 820 Quality System Regulation and the 2017 FDA guidance on technical considerations for additive manufacturing, requirements that apply equally to commercial device companies and to hospitals printing internally. Blue Cross NC's April 2025 coverage policy update classified FDA-approved, centrally manufactured 3D-printed orthopedic implants as medically necessary for patients with bone or joint deformity, translating regulatory clearance directly into billable clinical procedures and expanding the commercially addressable patient population without requiring additional regulatory submissions from cleared vendors.

LuxCreo's Dental Clear Aligner resin received FDA Class II 510(k) clearance in 2022 as the first direct-print clear aligner material, establishing a regulatory precedent for direct-print dental devices that manufacturers are now extending toward implant-supported components. Bioprinting faces the most constrained regulatory environment in this market, with no FDA-approved bioprinted implants existing as of mid-2024 despite active development pipelines, per Pew Research Center. The FDA's April 2025 policy update recognizing bioprinted human-derived tissues as valid drug testing methodologies does not clear the way for implantable bioprinted devices, but it validates bioprinted tissue as a recognized scientific tool that future implant submissions can build upon as the regulatory pathway for bioprinted implants eventually develops.

Investment and White Space Analysis

Investment is currently concentrated in metal implant production infrastructure and polymer platform clearance activity, with OEMs and pure-play specialists both prioritizing application categories with defined clearance pathways and confirmed reimbursement. The cranial reconstruction segment represents the most concentrated near-term white space, anticipated to exceed USD 2 Billion by 2030 per 3D Systems, against a near-empty competitive field of FDA-cleared PEEK implant platforms as of 2025. Manufacturers with cleanroom-certified polymer printing capability and neurosurgical clinical partnerships are best positioned to capture share before the segment attracts broader competition. Nikon's long-term plan for SLM Solutions, targeting EBITDA profitability in FY2025 and full operating profit by FY2027, confirms that Japanese capital is sustaining metal additive manufacturing investment with direct relevance to medical implant production infrastructure through the forecast period.

Hospital-based point-of-care printing programs represent an underserved distribution channel where vendors offering turnkey compliance infrastructure can convert research-stage programs into recurring commercial accounts. More than 20% year-over-year growth in 3D Systems' Dental sub-market in Q1 2026, per Stock Titan, confirms that dental offers the most commercially accessible near-term white space for polymer-capable new entrants not yet positioned for the quality system demands of structural implant production. Bioprinting represents the longest-horizon white space with the highest potential return. Vendors that establish bioprinted tissue supply for pharmaceutical validation under the FDA's 2025 policy can build biological material capability and regulatory relationships that position them for eventual bioprinted implant submissions when that clearance pathway becomes available.

Recent Developments

- May 2026: 3D Systems. FDA Clearance. Received FDA 510(k) clearance for the world's first 3D-printed PEEK cranial implants manufactured on its EXT 220 MED system, following demonstration across nearly 40 cranioplasty procedures in Europe.

- December 2025: 3D Systems. FDA Clearance. Received FDA 510(k) clearance expanding VSP Orthopedics indications to include skeletally mature adolescents, broadening the addressable patient population for its surgical planning platform.

- April 2025: Eminent Spine. FDA Clearance. Received FDA 510(k) clearance for its 3D-printed titanium pedicle screw system, described as the first and only such cleared system worldwide.

- March 2025: MedCAD. FDA Clearance. Received FDA 510(k) clearance for its AccuStride foot and ankle surgical guides and planning system, adding a new lower-extremity orthopedic application to the cleared device portfolio.

- March 2025: Materialise and University of Michigan Health. Clinical Trial. Initiated a U.S. FDA pivotal clinical trial for Materialise's 3D-printed bioresorbable tracheobronchial splint device, entering the highest-complexity implant validation stage.

- April 2025: FDA. Policy Update. Removed mandatory animal testing for certain drug evaluations in favor of methodologies including bioprinted human-derived tissues, expanding the addressable regulatory pathway for medical bioprinting companies.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 14.3 Billion |

| Market Value (2026) |

USD 17.7 Billion |

| Forecast Revenue (2035) |

USD 112.2 Billion |

| CAGR (2026 to 2035) |

22.8% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Application (Surgical Guides, Medical Implants, Prosthetics, External Wearable Devices, Tissue Engineering, Dental, Orthopedic Guides), By Component (Equipment, Biomaterials, Systems, Materials, Software and Services), By Technology (Laser Sintering, Laser Beam Melting, Droplet Deposition, Stereolithography, Electron Beam Melting, Fused Deposition Modeling, Digital Light Processing, Photopolymerization), By Raw Material (Polymers, Metals and Alloys, Ceramics, Biological Materials), By End-User (Medical and Surgical Centers, Hospitals, Academic and Research Institutes, Medical Device Companies) |

| Regional Analysis |

North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape |

3D Systems Corporation, Stratasys Ltd., Materialise NV, Formlabs, EOS GmbH, Renishaw plc, Nikon SLM Solutions, GE Additive, Desktop Metal / ETEC, Nano Dimension Ltd., Nanoscribe GmbH, Prodways Group, Oxford Performance Materials Inc., Cyfuse Medical K.K., Axtra3D, Medtronic, Johnson and Johnson MedTech, Stryker, DePuy Synthes, Zimmer Biomet, Smith and Nephew, Abbott Laboratories, Siemens Healthineers, GE Healthcare, Philips Healthcare, BD (Becton Dickinson), LimaCorporate, Eminent Spine, MedCAD, LightForce Orthodontics, Amnovis, 3T Additive Manufacturing Limited, Precision ADM Inc., Tecomet Inc., Vaupell, Arterex Medical, Protolabs Inc., Amuse3D |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the biggest investment opportunity in Additive Manufacturing for Medical Devices Market?

▾ The cranial reconstruction segment offers the most defined near-term opportunity, anticipated to exceed USD 2 Billion by 2030 per 3D Systems, against a near-empty field of FDA-cleared PEEK implant platforms as of 2025. Hospital point-of-care printing programs running active clinical projects represent a scalable distribution channel for vendors offering turnkey 21 CFR Part 820 compliance infrastructure.

Who are the top companies in Additive Manufacturing for Medical Devices Market?

▾ Leading companies include 3D Systems Corporation, Stratasys Ltd., Materialise NV, Renishaw plc, EOS GmbH, Stryker, Medtronic, Johnson and Johnson MedTech, Zimmer Biomet, and GE Additive. These firms compete across hardware platforms, certified materials portfolios, software-enabled workflows, and integrated clinical production programs spanning prototyping through regulated device manufacturing.

Which segment is growing fastest in Additive Manufacturing for Medical Devices Market and why?

▾ Dental is among the fastest-advancing sub-segments, with more than 20% year-over-year growth confirmed by 3D Systems in Q1 2026. High procedural volume, shorter scan-to-print workflows, and established material qualification pathways make dental the most commercially accessible segment for polymer-capable manufacturers not yet positioned for the quality system demands of structural implant production.

Which region is growing fastest in Additive Manufacturing for Medical Devices Market and why?

▾ Asia Pacific is building additive manufacturing medical capacity through institutional partnerships and sustained capital investment, with Stratasys signing a strategic MOU with VinUni and Vinmec in Vietnam in September 2025. Nikon's long-term plan for SLM Solutions targeting EBITDA profitability in FY2025 and full operating profit by FY2027 confirms continued Japanese capital commitment to metal additive manufacturing infrastructure directly applicable to medical implant production.

What is the biggest challenge holding Additive Manufacturing for Medical Devices Market back?

▾ No FDA-approved bioprinted implants existed as of mid-2024, constraining commercial translation of bioprinting pipelines despite active development at multiple companies. The FDA custom device exemption caps non-510(k) production at five units per year per manufacturer, creating a structural commercial barrier for companies seeking to scale patient-specific device production without completing full premarket notification clearance.