What is the Global Advanced Wound Care Market Size?

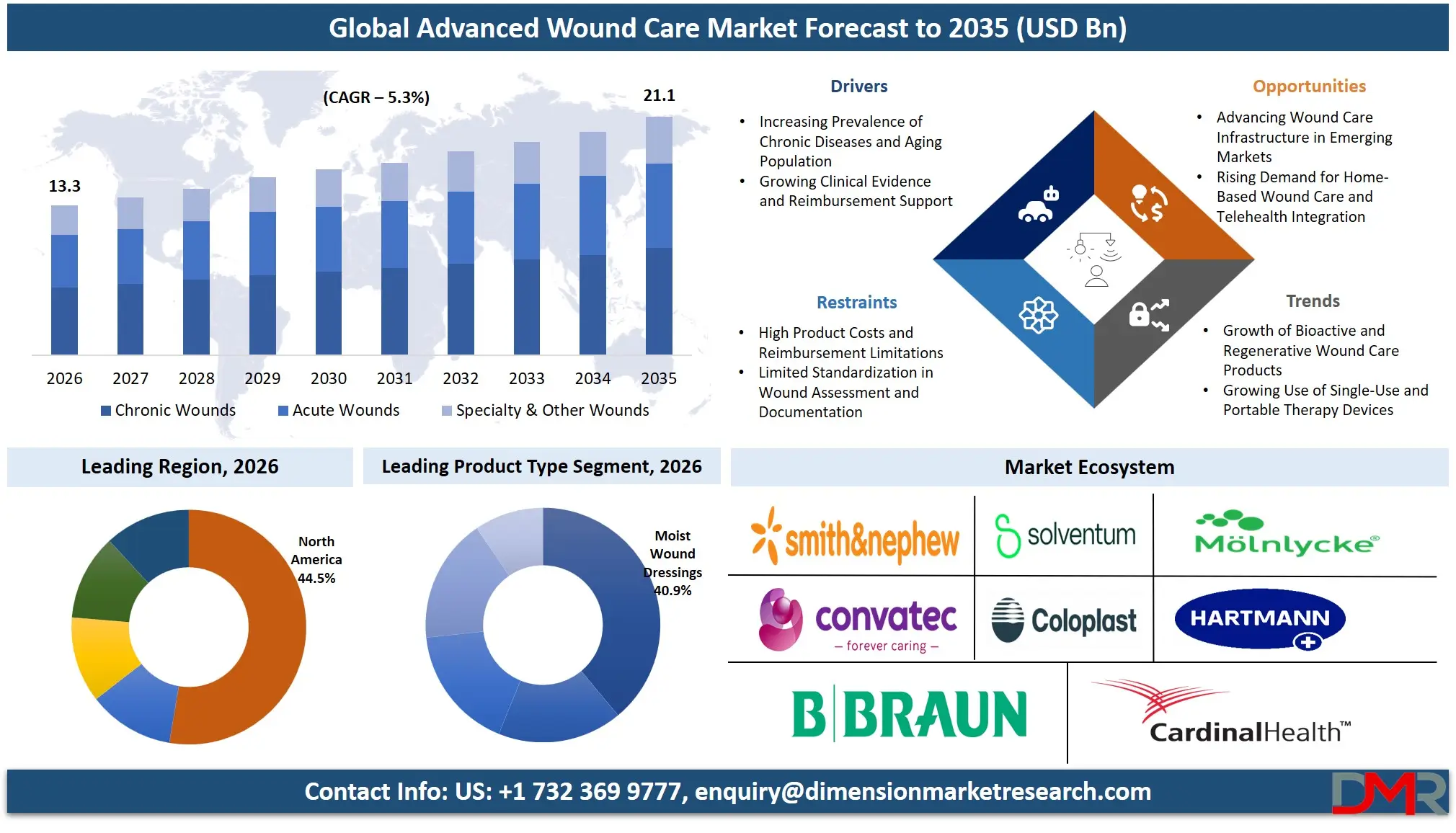

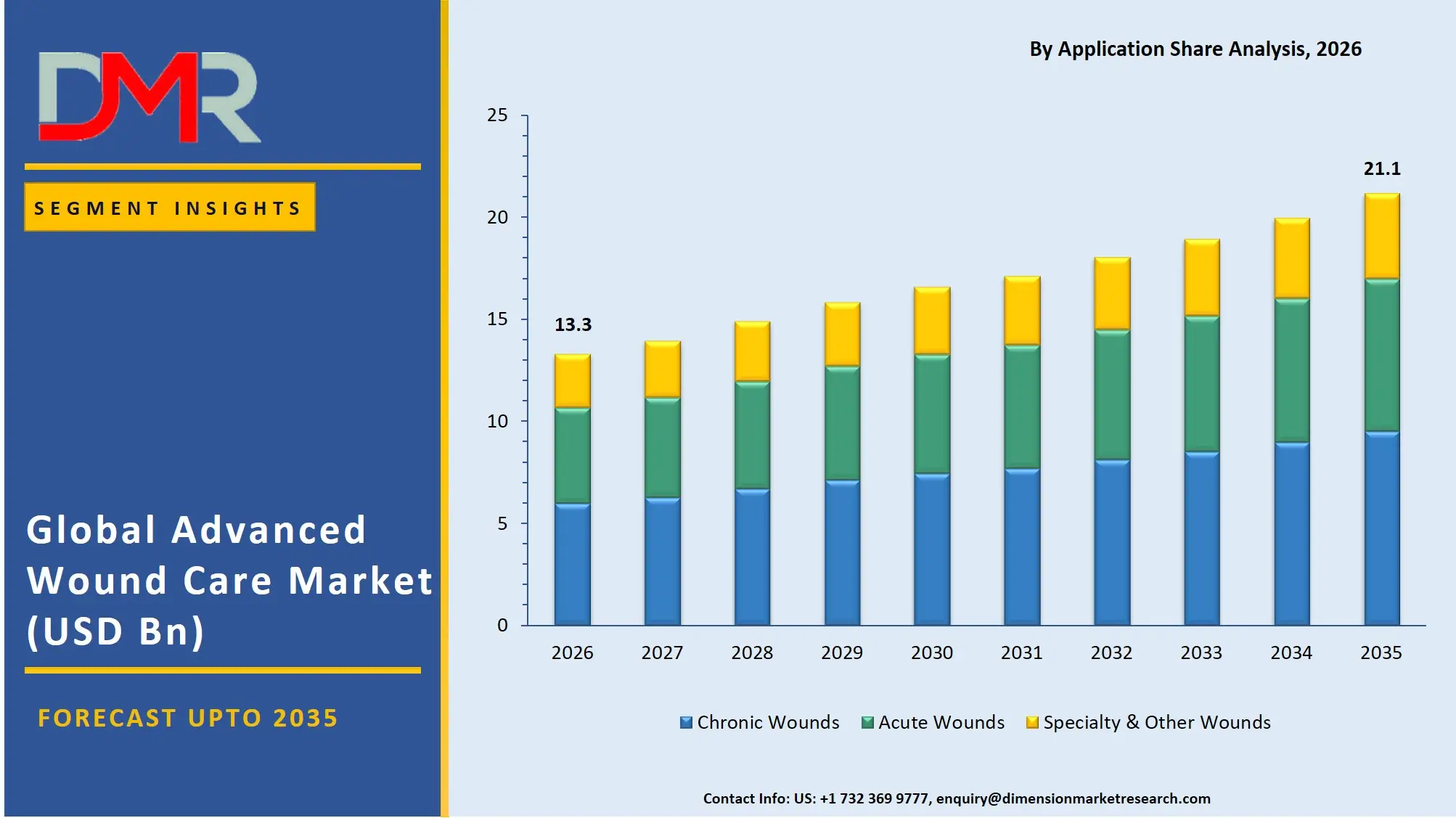

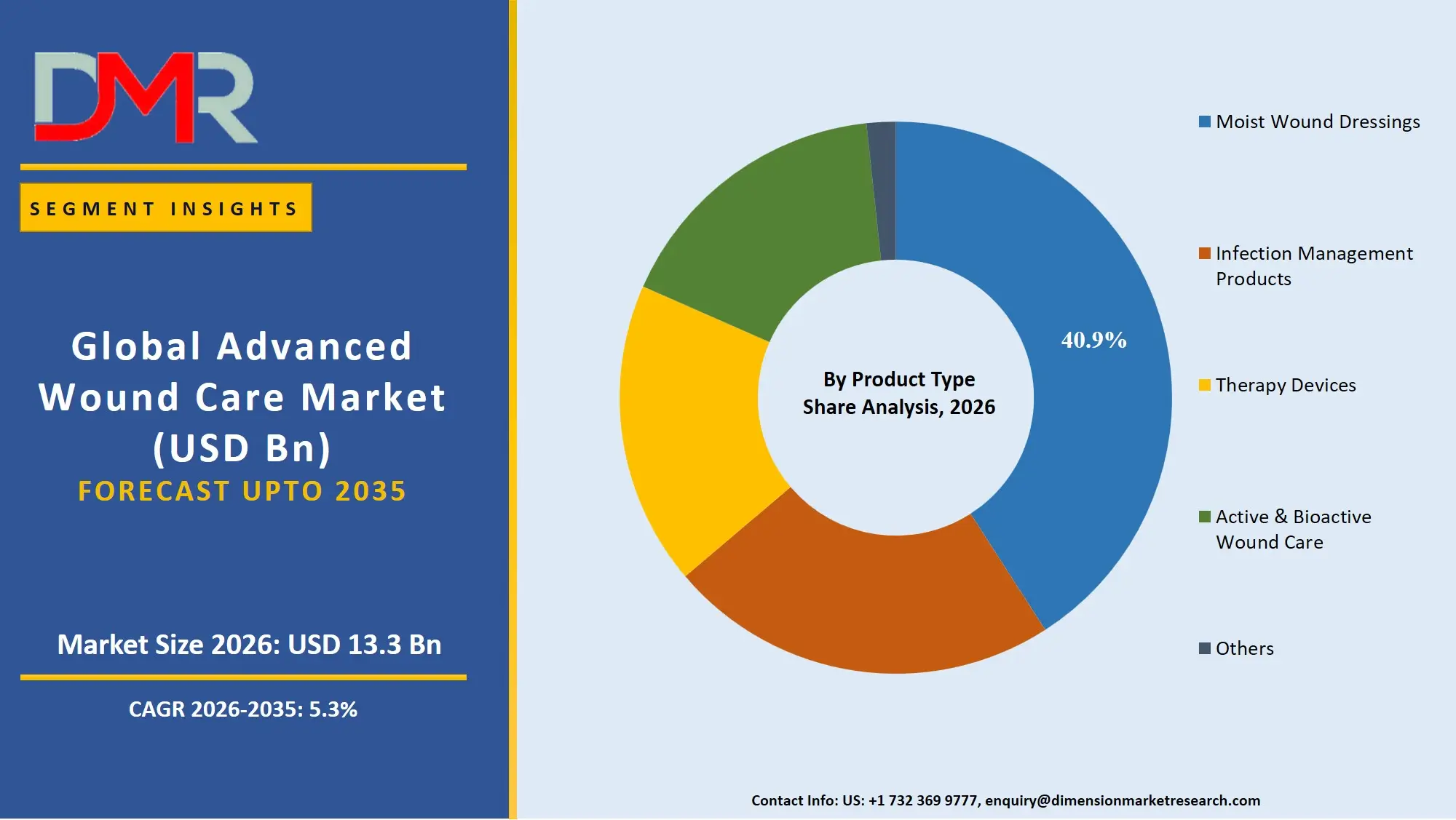

The Global Advanced Wound Care Market size is expected to reach a value of USD 13.3 billion in 2026, and it is further anticipated to reach USD 21.1 billion by 2035, growing at a CAGR of 5.3% during the forecast period, attributed to the rising prevalence of chronic wounds such as diabetic foot ulcers and pressure ulcers, increasing geriatric population, and growing adoption of bioactive dressings and negative pressure wound therapy.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global advanced wound care market is growing steadily, mainly because more clinical evidence now shows that advanced dressings can speed up healing and offer better protection against infections. At the same time, treatments such as skin substitutes and growth factors are becoming more widely accepted, helping improve patient outcomes and making it easier to introduce new products.

Rising healthcare spending on wound care across both hospitals and outpatient settings is also supporting market growth. In addition, advancements like biofilm detection, the use of biomarkers to assess healing risks, improved wound documentation, telehealth-based monitoring, and better reimbursement frameworks are further contributing to the expansion of the market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

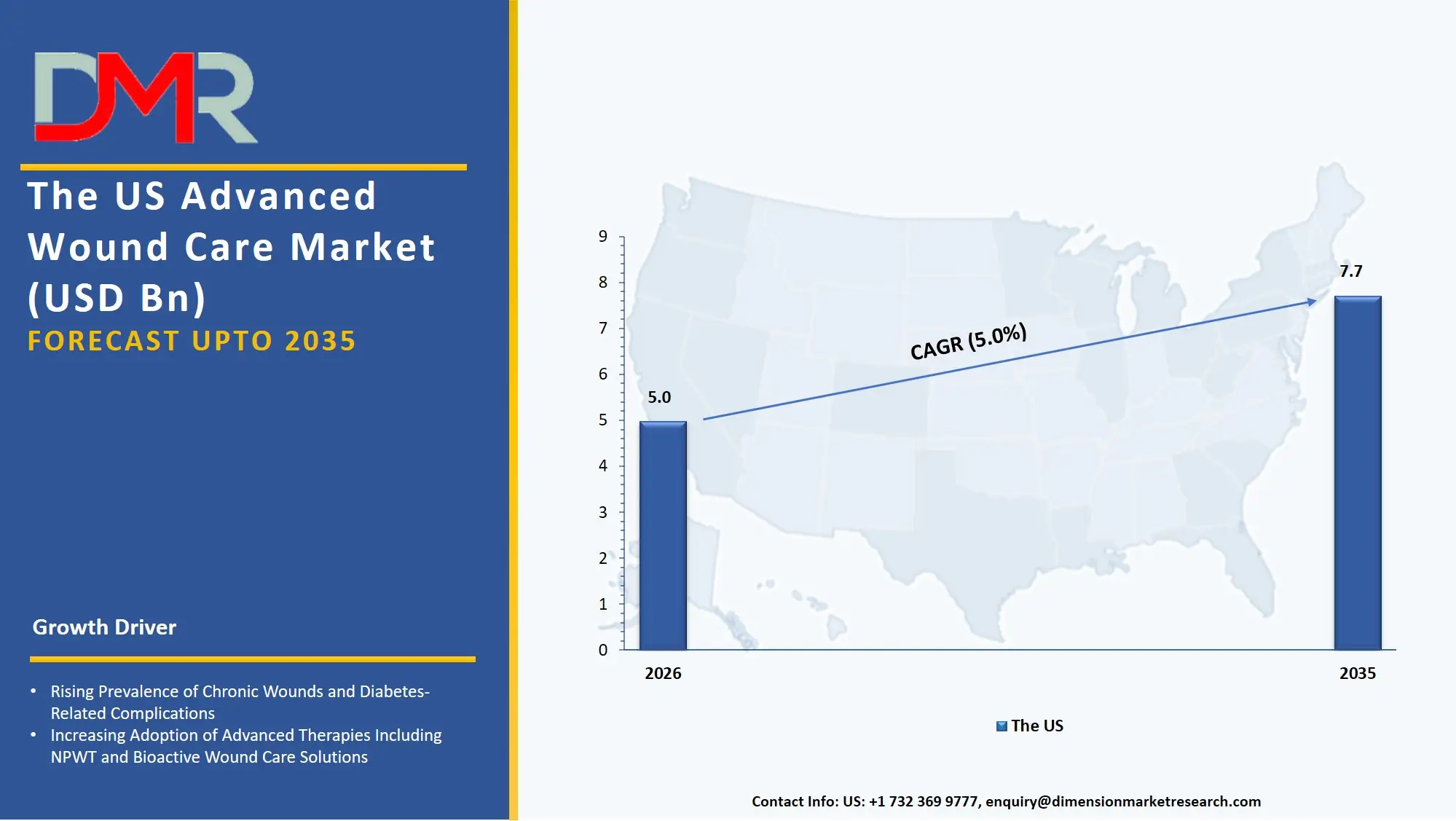

The US Advanced Wound Care Market

The US Advanced Wound Care Market is estimated to grow to USD 5.0 billion in 2026 with a compound annual growth rate of 5.0% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In the US, the programs are related to federal and state efforts in the management of chronic conditions, CMS reimbursement policies for wound care based on Medicare Part B, inpatient hospital stays, and NIH research initiatives on biomaterials and regenerative medicine. There is an emphasis on promoting wound assessment based on evidence, documentation of immediate healing, and standardized approaches to treatment. Wound assessments using electronic medical records are progressing rapidly; however, the US is gradually developing interoperability among skilled nursing facilities, hospital networks, and home health networks. The providers of these services are influenced by several acts, such as the 21st Century Cures Act and the Inflation Reduction Act, in terms of drug pricing.

Europe Advanced Wound Care Market

The European Advanced Wound Care Market is estimated to be valued at USD 4.0 billion in 2026, witnessing growth at a CAGR of 5.1%, during the forecast period.

Different European policies have impacted the development of the wound management market in Europe, including those of the European Wound Management Association, the new EU Medical Device Regulation (MDR), whose high standards require strong clinical evidence, as well as national policies such as the German DRG program for wound management and the chronic care coordination programs in France 2030. Countries are also standardizing wound formularies to align hospital and community care and enable consistent use of advanced dressings across borders. The market grows due to new tools like antimicrobial silver dressings with sustained release and scoring systems for pressure ulcer risk. Adoption is simplified through collaboration between public health institutions and private firms in addition to clinical practice guidelines. Private firms benefit from the presence of well-developed logistical channels for distribution and reimbursement, while Europe leads in cost-effectiveness research for high-tech wound care solutions.

Japan Advanced Wound Care Market

The Japan Advanced Wound Care Market is projected to be valued at USD 698.9 million in 2026, progressing at a CAGR of 5.8%, during the period spanning from 2026 to 2035.

Japan's advanced wound care market is well developed, with foam and alginate dressing of high quality, home healthcare connected patient monitoring systems, and a great variety of infection management products. National focus on aging-in-place, efficiency in long-term care, and hospital length-of-stay reduction is delivered via pressure ulcer prevention protocols and smart wound documentation systems. Growth opportunities are helped by government measures under the Society 5.0 program by Japan's Ministry of Economy, Trade and Industry (METI), and continued investment in home healthcare infrastructure. Clinical wound analysis for condition-specific product development and diabetic foot ulcer diagnostics all need effective clinical evidence to keep pace with national health insurance revisions. The rising cost of the approval of new bioactive products and their application in the existing nursing practice is a matter of concern but there is a possibility of exporting Japanese wound care technologies to other Asian markets, which have a high rate of aging.

Key Takeaways

- Market Size & Forecast: The Global Advanced Wound Care Market is estimated to be valued at USD 13.3 billion in 2026 and is expected to grow to USD 21.1 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 5.3% in the forecast period.

- Primary Growth Drivers: The increasing prevalence rates of diabetes and obesity across the world, the growing number of surgical cases, aging population vulnerable to chronic wounds and the reimbursement policies are favorable to advanced wound care products in the developed countries are the major growth drivers.

- Key Market Trends: The shift toward bioactive and regenerative wound care products, increasing adoption of NPWT in home settings, and the integration of digital wound assessment tools into electronic health records are key market trends.

- By Product Type: Moist Wound Dressings are expected to take the largest revenue share in 2026 in the global advanced wound care market.

- By Application: Chronic Wounds are expected to take the largest revenue share in 2026.

- By End-User: Hospitals is estimated to take the lead in 2026 with the largest share in the advanced wound care market.

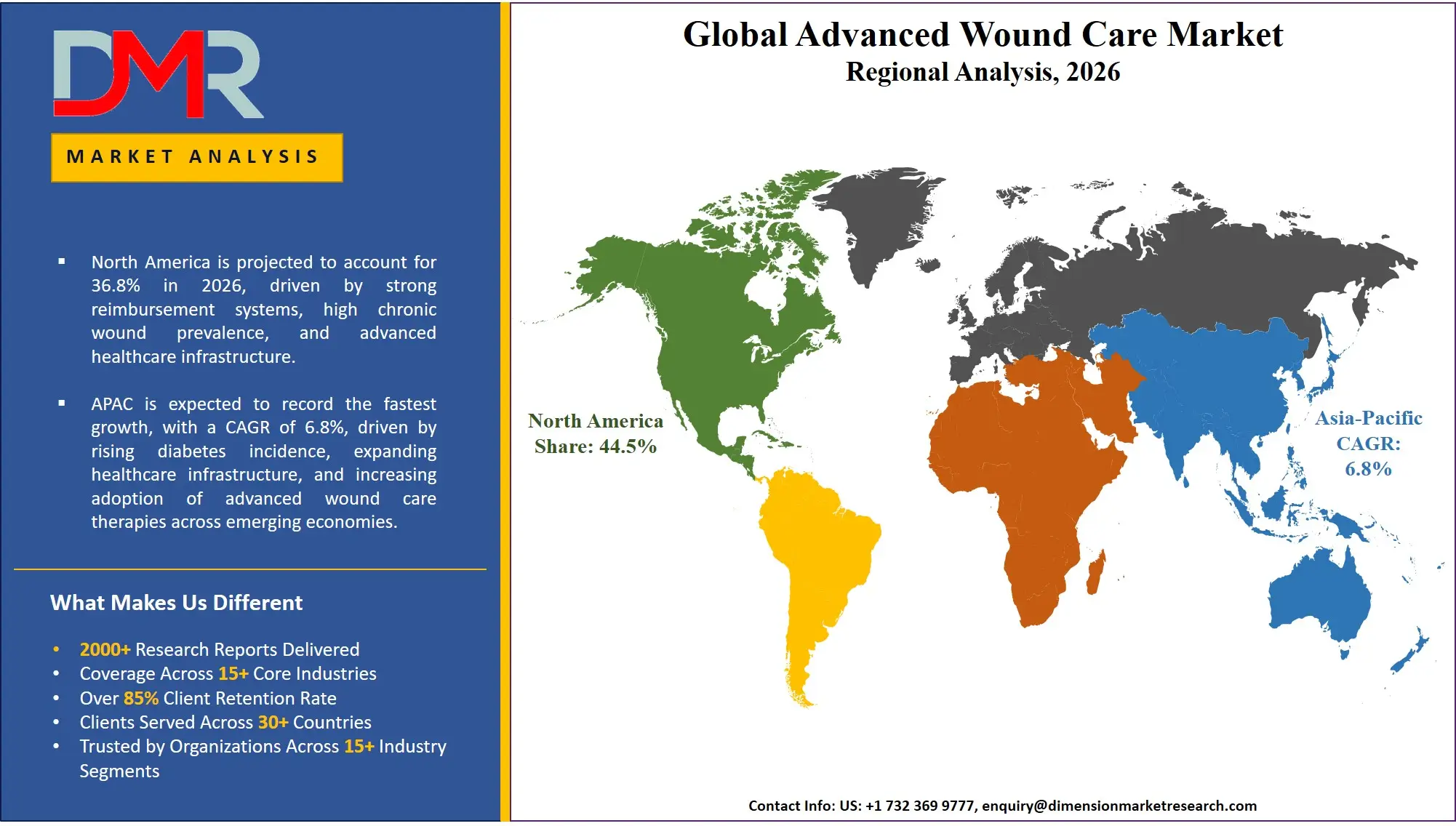

- Regional Leadership: North America is estimated to take the lead in 2026 with 44.5% share in the advanced wound care market, owing to high healthcare spending, rapid adoption of bioactive products, and strong reimbursement infrastructure.

What is Advanced Wound Care?

Advanced wound care involves the application of specific treatments and technologies that can help treat complex and chronic wounds in a manner superior to the traditional means of wound treatment using simple dressing material such as gauze. This field emphasizes creating a moist environment, controlling exudate, protecting against infections, and facilitating tissue repair and regeneration. The technologies associated with advanced wound care include advanced dressings (foam, hydrocolloid, alginate), antimicrobial agents, biological approaches such as skin substitutes and growth factors, and negative pressure wound therapy devices. Advanced wound care techniques are frequently employed in the treatment of conditions such as diabetic foot ulcers, pressure ulcers, venous leg ulcers, and burns.

Use Cases

- Diabetic Foot Ulcer Management: A 65-year-old diabetic patient with a non-healing plantar ulcer is managed with a silver-based antimicrobial dressing to reduce biofilm and a collagen dressing to enhance granulation to lower the risk of amputation (25% to less than 5% at 12 weeks).

- Pressure Ulcer Prevention in Long-Term Care: A nursing home uses alternating pressure mattresses and prophylactic foam mattresses on high-risk sacral sites, decreasing the occurrence of pressure ulcers in the hospital by 12% to 3% in six months.

- Post-Surgical Wound Healing: A patient receiving an abdominal surgery is given a negative pressure wound therapy (NPWT) device during 7 days after surgery, which lowers the surgical site infection rates by 50% in comparison to a patient receiving regular gauze.

- Burn Care in Emergency Settings: A patient with a second-degree of a burn is treated with a hydrogel dressing to help relieve pain and keep the area moist, and a skin substitute to shorten the time of healing that was expected to be 21 days to 10 days.

How AI Is Transforming the Global Advanced Wound Care Market?

Advanced wound care is increasingly using artificial intelligence (AI) to enhance healing prediction, automatically measure the wound area in smartphone photos, and identify which wounds are at risk of infection. The use of AI in wound assessment mobile apps can now determine the size of the wound, the tissue composition (granulation, slough, necrosis), the temperature variations with high accuracy, and decrease inter-clinician variability. This enables quicker clinical decision making as nurses and physicians will be able to send wound pictures remotely and they will be automatically analyzed. The records of patients and electronic reports of inspection are simpler to research and enable clinicians to discover healing stalling, make modifications to treatment strategies sooner, and enhance overall patient results. This has made care to be more affordable, faster and efficient compared to manual measurements of using a ruler.

Research and development is also getting boosted by AI through analysis of clinical trial data to determine the best patient subgroups that can respond to particular skin substitutes or growth factors. It helps manufacturers predict demand for different dressing types by geographic region and monitor real-world evidence from electronic health records more effectively. In addition, automation of wound documentation and progress tracking is reducing nursing workload, lowering documentation errors, and improving compliance with reimbursement requirements. This is leading to better financial results for wound care centers and more consistent care across the advanced wound care delivery chain.

Market Dynamics

Key Drivers of the Global Advanced Wound Care Market

Increasing Prevalence of Chronic Diseases and Aging Population

The market is expanding owing to the rise in the prevalence of diabetes, obesity, and vascular conditions, which put individuals at risk of developing chronic wounds. There are more than 500 million diabetic adults worldwide, and about 15%-25% of them will develop a diabetic foot ulcer at some point in their lives. Moreover, the number of people aged 65 years or older is expected to double by 2050. Individuals belonging to this age group are more likely to suffer from pressure ulcers and venous leg ulcers. The healthcare industry understands that investing in innovative wound care solutions lowers expenses by avoiding amputations, rehospitalizations, and long-term nursing care.

Growing Clinical Evidence and Reimbursement Support

There is a greater focus on evidence-based approaches to wounds, which has been shown through randomized clinical trials that advanced dressings treat chronic wounds quicker compared to gauze. New treatment recommendations for specific wound types have been issued by various bodies including NPIAP, EWMA, and IWGDF. The Centers for Medicare & Medicaid Services (CMS) has also increased payment of skin substitutes and NPWT within their hospital outpatient and home health benefit categories in the US. In Europe, health technology assessments from various countries are now considering cost-effectiveness analysis of bioactive wound care. This reimbursement support is encouraging more structured treatment protocols and strengthening the need for effective management systems in both government and private healthcare providers.

Restraints in the Global Advanced Wound Care Market

High Product Costs and Reimbursement Limitations

The initial cost of advanced wound care products, including skin substitutes (ranging between 1,000-2,000 per application) and negative pressure wound therapy (NPWT) (ranging between 50-100 per day), is still considerably more expensive than basic wound care dressings such as gauze or saline dressings. The lack of reimbursement of these products by the majority of developing nations and some well-endowed healthcare systems in developing nations makes their use difficult. In addition, prior authorization and step therapy plans where the patient has to be treated with lower-cost treatment options are other barriers to adopting wound care products.

Limited Standardization in Wound Assessment and Documentation

The market has not yet achieved complete fragmentation on wound measurement methods, photographic protocol and documentation of progression of healing. Even though there are structured electronic wound records implemented in some large hospital systems, in many smaller clinics still manual tracing and ruler-based measurement with uneven follow up intervals is used. The absence of a standardized wound assessment hinders comparisons of clinical outcomes of different products and leads to inefficiency in product selection and treatment planning. It also makes the design of clinical trials and regulatory approval of new products more difficult due to this variability.

Growth Opportunities in the Global Advanced Wound Care Market

Advancing Wound Care Infrastructure in Emerging Markets

The emerging markets, such as Brazil, India, Indonesia, Nigeria, and Vietnam, are experiencing increased incidences of diabetes cases and establishment of healthcare facilities. The emerging markets provide a great prospect for growth due to increased interest in quality care among the middle class, knowledge of innovative techniques, and government initiatives to reduce amputations. These markets do not have established procedures; hence, it will be easy to adopt innovations. The joint ventures between foreign companies and the local manufacturers and price differentiation are factors that make the emerging market for wound care products lucrative for multinational companies.

Rising Demand for Home-Based Wound Care and Telehealth Integration

The transition of healthcare towards home services, especially because of the impact of the COVID-19 pandemic, leads to a quick adoption of NPWTs designed for single-use applications, easily applied foam dressings, and wound care solutions integrated with telemedicine technology. Patients' interest in wound care at home rather than in hospitals and lower payments for home visits versus inpatient services encourage the use of portable therapy equipment, wound measurement applications via smartphones, and online sales of bandage and other products.

Global Advanced Wound Care Market Trends

Growth of Bioactive and Regenerative Wound Care Products

There is a gradual change from passive to active wound healing. The use of skin equivalents (either natural or artificial), growth factors (for example, platelet-derived growth factor), and extracellular matrix is increasing among non-healing wounds that cannot be healed using conventional dressings. These products are supported by clinical trials showing complete wound closure rates of 60-80% compared to 30-40% with standard care. This move is slowly turning the industry toward biologic and cell-based therapies in wound management instead of being purely reliant on traditional dressings.

Growing Use of Single-Use and Portable Therapy Devices

The use of single-use negative pressure wound therapy (sNPWT) systems is currently becoming a basic part of today's wound care operations. Unlike traditional rentable NPWT pumps, sNPWT devices are disposable, lightweight, and battery-operated, allowing patients to move freely and receive therapy at home. These systems allow real-time pressure monitoring, centralized therapy administration tracking, and better coordination between home health nurses and wound care physicians. Portable oxygen therapy and electromagnetic therapy devices are also emerging for hard-to-heal wounds. Single-use platforms are improving the efficiency and patient adherence of advanced wound care in home settings by removing the need to return rented equipment and allowing operations to scale more easily.

Research Scope and Analysis

The global advanced wound care market involves advanced dressings, biologics, and therapy devices used for managing chronic and acute wounds. The study covers segmentation by product type, application, distribution channel, and end user, driven by rising chronic diseases, ageing population, and technological advancements.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Type Analysis

The Moist Wound Dressings segment is likely to continue dominating the market in 2026, with 40.9% of the global advanced wound care market share. This is due to its key role in covering diabetic foot ulcers, pressure ulcers, surgical wounds, and burns, and its usefulness in various clinical settings where maintaining a moist healing environment is the standard of care. Among these, Foam Dressings hold the largest sub-segment due to high fluid handling capacity, conformability, and reduced nursing change frequency. Hydrocolloid and Alginate Dressings follow for moderate-to-heavy exudate management. The Infection Management Products segment is also growing rapidly, with increasing demand for silver-based dressings needed in chronic wounds with biofilm suspicion. The fastest-growing segment is Active & Bioactive Wound Care (including skin substitutes and growth factors), driven by rising adoption in diabetic foot ulcer protocols and hospital outpatient departments. Therapy Devices, especially single-use NPWT, are seeing strong adoption in home healthcare settings.

By Application Analysis

The Chronic Wounds segment is expected to account for 67.8% share in 2026, due to rising diabetes and obesity rates, an aging population, and longer treatment durations (weeks to months) compared to acute wounds. Within chronic wounds, Diabetic Foot Ulcers represent the largest sub-segment, driven by increasing amputation prevention programs, IWGDF guideline adoption, and favorable reimbursement for skin substitutes. Pressure Ulcers are the second-largest sub-segment, driven by hospital-acquired condition non-payment policies and long-term care quality measures. Venous Leg Ulcers follow, supported by compression therapy plus advanced dressings protocols. Acute Wounds, including Surgical & Traumatic Wounds and Burns, are also significant due to high surgical volumes globally. The fastest-growing area is Specialty & Other Wounds, including radiation wounds and necrotizing fasciitis, where advanced biologics are increasingly used off-label.

By Distribution Channel Analysis

The Direct Tenders (Institutional Sales) segment is expected to dominate with around 58.4% market share in 2026, driven by group purchasing organizations (GPOs) in hospitals, integrated delivery networks (IDNs), and government healthcare systems (e.g., VA, NHS) seeking standardized formularies and long-term supply contracts. Retail Pharmacies represent the second-largest channel, serving home healthcare patients and those with mild chronic wounds requiring routine dressing changes. The fastest-growing area is Online Pharmacies & E-commerce Platforms, where convenience, home delivery, subscription models for recurring wound care needs, and direct-to-consumer education are gaining traction among caregivers and elderly patients with mobility limitations.

By End-User Analysis

The Hospitals segment is the largest end-user in 2026, accounting for 44.2% share, driven by high patient volumes for surgical wounds, burns, and complex chronic wounds, availability of advanced therapy devices like NPWT and oxygen therapy, and specialized wound care teams (often part of general surgery or plastic surgery departments). Wound Care Centers are the second-largest segment, offering dedicated, multidisciplinary care (nurses, podiatrists, vascular surgeons) for complex chronic wounds, often affiliated with hospital outpatient departments. The fastest-growing area is Home Healthcare Settings, where aging populations, cost containment pressures (NPWT at home costs 30-50% less than inpatient), and portable sNPWT devices enable patients to receive advanced wound care outside institutional settings. Ambulatory Surgical Centers, Clinics & Physician Offices, and Long-term Care Facilities also contribute significantly, particularly for minor wounds, post-op follow-up, and pressure ulcer prevention.

The Global Advanced Wound Care Market Report is segmented based on the following:

By Product Type

- Moist Wound Dressings

- Hydrocolloid Dressings

- Foam Dressings

- Alginate Dressings

- Hydrogel Dressings

- Infection Management Products

- Silver-based Dressings

- Non-silver Antimicrobial Dressings

- Collagen Dressings

- Active & Bioactive Wound Care

- Skin Substitutes

- Growth Factors

- Therapy Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Oxygen Therapy Devices

- Electromagnetic Therapy Devices

- Others

By Application

- Chronic Wounds

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Leg Ulcers

- Arterial Ulcers

- Acute Wounds

- Surgical & Traumatic Wounds

- Burns

- Specialty & Other Wounds

By Distribution Channel

- Direct Tenders (Institutional Sales)

- Retail Pharmacies

- Online Pharmacies & E-commerce Platforms

By End-User

- Hospitals

- Wound Care Centers

- Ambulatory Surgical Centers

- Home Healthcare Settings

- Clinics & Physician Offices

- Long-term Care Facilities

Regional Analysis

Leading Region in the Advanced Wound Care Market

It is projected that North America will take the lead in the global advanced wound care market (by value), covering a market share of about 44.5% in the year 2026. The region's dominance is driven by high prevalence of diabetes and obesity, strong reimbursement for advanced products under Medicare and private insurance (including coverage for skin substitutes and NPWT), higher average product prices compared to other regions, a mature distribution network for medical supplies, and the presence of major wound care manufacturers (Smith+Nephew, ConvaTec, 3M, Medtronic) and specialized wound care centers. The widespread adoption of evidence-based treatment protocols and electronic wound documentation systems further strengthens North America's leading position. Additionally, ongoing investments in clinical research and regulatory pathways for novel biologics further reinforce the region's technology and innovation leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Advanced Wound Care Market

Asia-Pacific is the fastest-growing region, supported by rapidly increasing diabetes prevalence (China and India together account for over 200 million diabetic patients), rising healthcare spending, improving reimbursement for chronic disease management, and growing adoption of modern wound care protocols. The region benefits from large patient populations, increasing penetration of private health insurance, and alignment with national non-communicable disease prevention roadmaps. Countries such as Japan, South Korea, and Australia have established universal health coverage that includes advanced dressings for specific indications. China and India are actively upgrading hospital infrastructure and training wound care specialists. Growing focus on local manufacturing to reduce costs and structured clinical evidence development will further speed up market expansion. Moreover, increasing government support for diabetes amputation prevention and aging-in-place initiatives is expected to keep growth momentum high.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The advanced wound care market is highly competitive, with product innovation and clinical evidence shaping the competitive environment. To gain an advantage, companies are focused on developing better bioactive materials (such as next-generation skin substitutes, sustained-release silver dressings, and growth factors), generating randomized controlled trial data, and expanding into home healthcare and emerging markets. Barriers to entry are high due to the cost of clinical trials and regulatory approval (FDA PMA or 510(k), CE Mark under EU MDR), specialized manufacturing expertise, and the need for established relationships with group purchasing organizations and hospital systems.

Strategic approaches include partnerships with academic medical centers and wound care societies, mergers and acquisitions between dressing manufacturers and biologics companies, and long-term group purchasing contracts with hospitals, nursing home chains, and government agencies.

Some of the prominent players in the Global Advanced Wound Care Market are:

- Smith & Nephew plc

- Solventum Corporation

- Mölnlycke Health Care AB

- ConvaTec Group plc

- Coloplast A/S

- Paul Hartmann AG

- B. Braun Melsungen AG

- Cardinal Health, Inc.

- Medline Industries, LP

- Organogenesis Holdings Inc.

- Integra LifeSciences Holdings Corporation

- MiMedx Group, Inc.

- Vericel Corporation

- Advanced Medical Solutions Group plc

- Urgo Group (Laboratoires Urgo)

- Lohmann & Rauscher GmbH & Co. KG

- Hollister Incorporated

- 3M Company

- Ethicon, Inc. (Johnson & Johnson Services, Inc.)

- Medtronic plc.

- Other Key Players

Recent Developments

- March 2026: Smith & Nephew plc launched its ALLEVYN COMPLETE CARE Foam Dressing, a next-generation advanced wound dressing designed to improve exudate management and reduce pressure injury risk, strengthening its advanced wound care product portfolio in hospital and acute care settings.

- December 2025: Coloplast A/S continued expansion of its advanced wound care portfolio following integration of Kerecis fish-skin graft technology, enhancing its biologic wound healing capabilities for chronic and complex wounds.

- August 2025: ConvaTec Group plc expanded its Avelle Negative Pressure Wound Therapy (NPWT) system commercialization across additional European markets, strengthening its position in single-use NPWT devices for acute and chronic wound care management.

- March 2025: Mölnlycke Health Care AB announced the acquisition of P.G.F. Industry Solutions GmbH, the manufacturer of Granudacyn wound cleansing and moisturizing solutions, expanding its advanced wound cleansing and moist wound care portfolio globally.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 13.3 Bn |

| Forecast Value (2035) |

USD 21.1 Bn |

| CAGR (2026–2035) |

5.3% |

| The US Market Size (2026) |

USD 5.0 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Product Type, By Application, By Distribution Channel, By End-User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

Which region held the largest share of the Global Advanced Wound Care Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 44.5%.

What is the CAGR of the Global Advanced Wound Care Market from 2026 to 2035?

▾ The market is growing at a CAGR of 5.3% over the forecasted period.

Who are the key players in the Global Advanced Wound Care Market?

▾ Some of the major key players in the Global Advanced Wound Care Market are Smith & Nephew plc, Mölnlycke Health Care AB, Coloplast A/S, 3M Company, Medtronic plc, Organogenesis Holdings Inc., MiMedx Group, Inc., and many others.

How big is the Global Advanced Wound Care Market?

▾ The Global Advanced Wound Care Market size is estimated to have a value of USD 13.3 billion in 2026 and is expected to reach USD 21.1 billion by the end of 2035.

What factors are driving the growth of the Global Advanced Wound Care Market?

▾ The market is driven by rising global prevalence of diabetes and obesity, increasing geriatric population, growing number of surgical procedures, clinical evidence supporting faster healing with advanced products, and favorable reimbursement policies in developed countries.

What are the major trends in the Global Advanced Wound Care Market?

▾ The key market trends include the shift toward bioactive and regenerative products (skin substitutes, growth factors), increasing adoption of single-use NPWT systems in home healthcare, and integration of AI-powered wound measurement tools into clinical workflows.

Which region is expected to grow the fastest in the Global Advanced Wound Care Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

How is the Global Advanced Wound Care Market segmented?

▾ The market is segmented by product type, by application, by distribution channel, and by end-user.