Market Snapshot

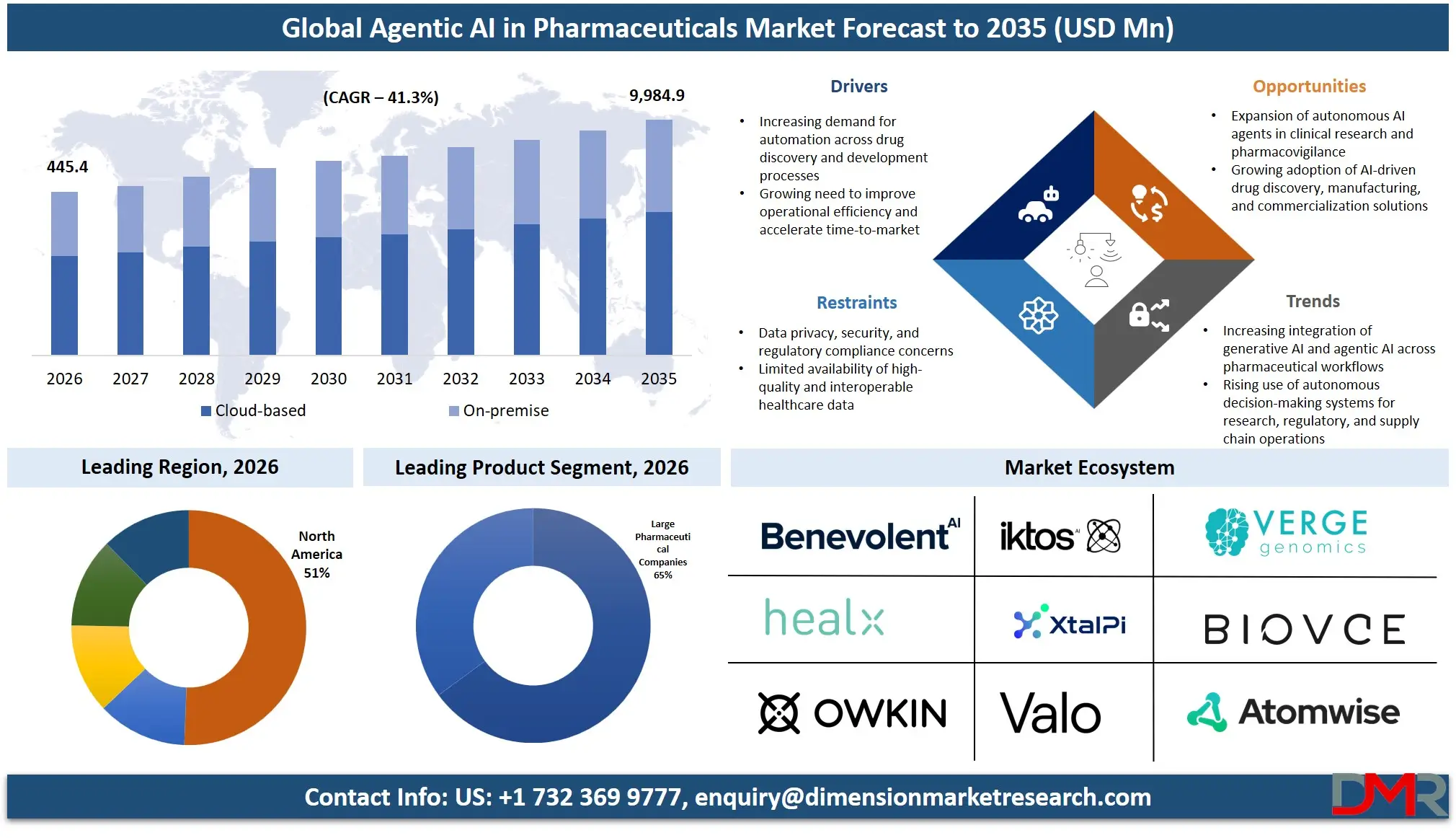

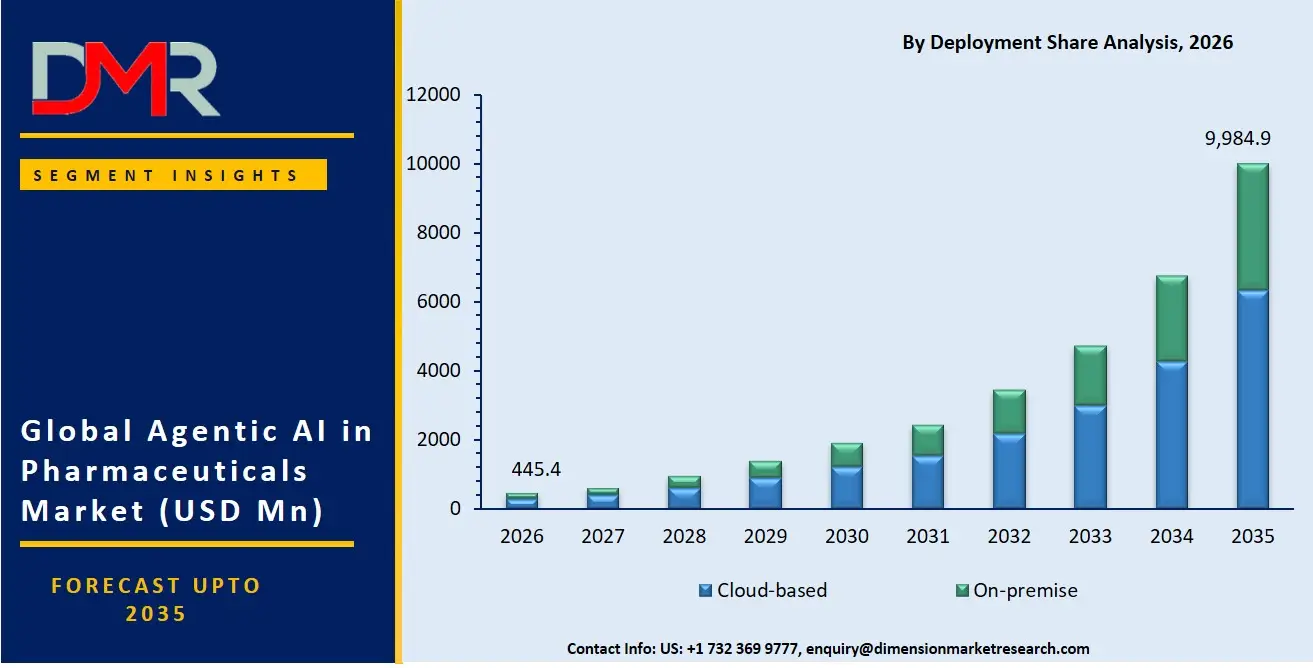

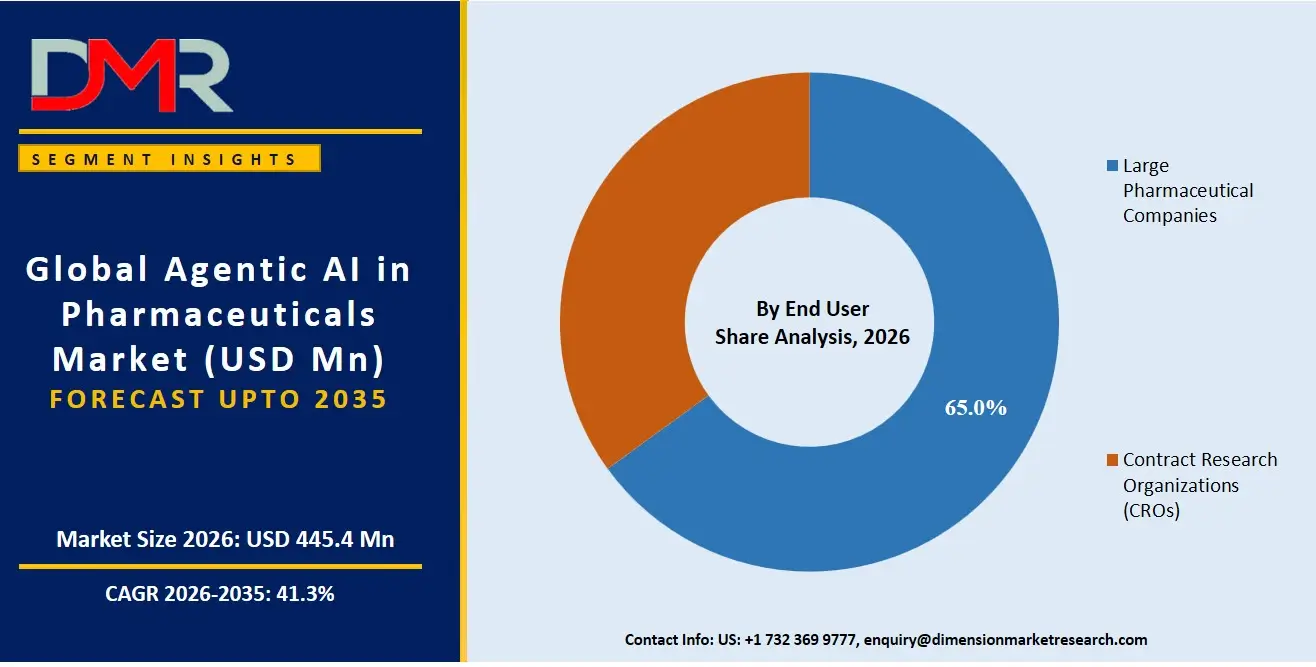

- The Agentic AI in Pharmaceutical Market size is USD 312.2 Million in 2025, reached USD 445.4 Million in 2026, and is projected to hit USD 9,984.9 Million by 2035 at a CAGR of 41.3%.

- Drug Discovery and Lead Identification leads the Application segment with a 40.5% revenue share in 2026.

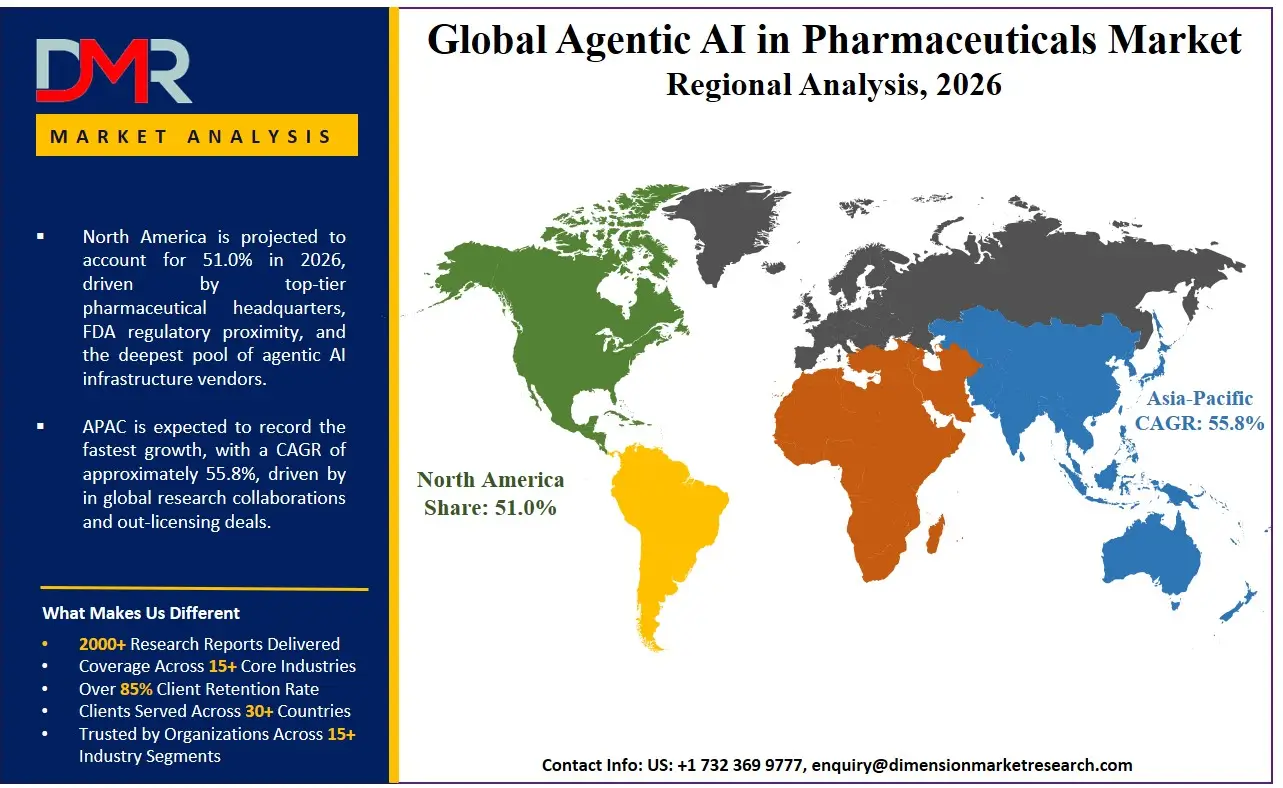

- North America holds the dominant regional position with a 51.0% share in 2026; the United States alone accounts for 89.2% of North American revenue.

- Cloud-based deployment leads with a 62.3% revenue share. Large pharmaceutical companies account for 65.0% of end-user demand.

Market Overview

The Global Agentic AI in Pharmaceutical Market covers autonomous multi-step software systems that plan, execute, and adapt drug discovery, clinical development, regulatory strategy, and commercial operations workflows without continuous human intervention. Generative AI tools that require manual prompting for each output fall outside Agentic AI in Pharmaceutical Market's scope.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Pharmaceutical pipelines face compounding structural pressure. The volume of drug launches alone does not capture the underlying complexity: each program now involves multi-modal data streams, decentralized trial sites, and regulatory submissions across three or more jurisdictions simultaneously. Agentic AI systems are the only scalable architecture capable of coordinating this complexity without proportional headcount expansion.

The broader pharmaceutical AI market is evolving past proof-of-concept. Cohere acquired biopharma AI specialist Reliant AI in May 2026 to accelerate its domain-specific agentic workbench "North for Pharma," signaling that horizontal AI infrastructure companies now see pharmaceutical autonomy as a dedicated product category rather than a vertical extension. Boards and C-suites are no longer evaluating agentic AI as experimental technology. Capital allocation decisions are being made at the enterprise level.

Market Size and Forecast

The Global Agentic AI in Pharmaceutical Market size is estimated at USD 445.4 Million in 2026 from USD 312.2 Million in 2025, and is projected to reach USD 9,984.9 Million by 2035, exhibiting a CAGR of 41.3% during the forecast period.

The forecast rests on two converging structural pressures. Patent cliff expirations worth USD 180 Billion between 2024 and 2030 force top pharmaceutical executives to compress discovery timelines or face irreversible revenue erosion. Further, the 5-year cumulative novel active substance count of 270 compounds reaching the U.S. market by end of 2025 also signals sustained pipeline productivity that agentic orchestration tools are directly supporting. Downside risk is real but bounded. Strategic feasibility studies project that 40% of agentic AI projects face cancellation by 2027 due to misaligned capabilities and unclear ROI metrics, a figure that caps near-term adoption velocity among mid-tier pharmaceutical firms without dedicated AI operations teams.

Application Analysis

Drug Discovery and Lead Identification accounted for 40.5% of Application demand in 2026, the highest of any category.

Drug discovery commands this share because agentic systems deliver their highest measurable ROI at the front end of the pipeline. Autonomous agents simultaneously screen billions of molecular candidates, validate targets against multi-omics databases, and generate synthesizable lead structures without researcher intervention between steps. The U.S. FDA fast-tracked 12 oncology drugs assisted by AI target identification frameworks in 2024, creating a direct regulatory validation signal that enterprise R&D directors use to justify agentic platform investment.

Clinical trial design and recruitment represent the next-fastest scaling application as sponsors seek to offset rising protocol complexity. Preclinical discovery workflow automation is emerging as a distinct sub-segment as CROs seek to offer agentic capabilities as a differentiated service. Small molecule candidates account for 62% of all active Phase I clinical trials in 2026, concentrating agentic chemistry demand on structure-generation and ADMET prediction agents.

Deployment Analysis

With a 62.3% share in 2026, Cloud-based deployment outpaced all other Deployment categories.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Cloud infrastructure dominates because agentic pharmaceutical systems require elastic compute for high-throughput molecular simulations and real-time clinical data ingestion that on-premise hardware cannot provision cost-effectively. AWS reinforced this position by launching "Amazon Bio Discovery" in April 2026, an agentic platform allowing scientists to orchestrate drug discovery pipelines using natural language without coding. Enterprise pharma adopters now treat cloud-native agentic deployment as the default architecture. Firms that built on-premise AI infrastructure between 2021 and 2023 are already evaluating hybrid migration paths.

On-premise deployment retains relevance for organizations where patient data sovereignty regulations prohibit cloud transfer, particularly in Germany, Japan, and South Korea.

End-User Analysis

Large pharmaceutical companies captured 65.0% of the End-User segment in 2026, ahead of all rivals.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Large pharmaceutical companies hold this share because they possess the data volumes, IT infrastructure, and regulatory affairs teams required to deploy and govern multi-agent systems at scale. Firms facing the steepest patent cliff exposure have the strongest incentive to invest. The board-level capital allocation urgency this creates translates directly into enterprise license agreements with agentic platform vendors, not pilot subscriptions.

Contract Research Organizations represent the highest-growth end-user segment. CROs that embed agentic clinical trial design and patient recruitment agents into their service offering can undercut competitors on timelines and offer sponsors transparent AI-assisted trial execution. Sponsors increasingly specify agentic capability as a procurement requirement in CRO RFPs, shifting market power toward technology-enabled service providers.

Key Market Segments

By Application

- Drug Discovery and Lead Identification

- Clinical Trial Design and Recruitment

- Clinical-Trial Applications

- Preclinical Discovery Workflow

By Deployment

By End-User

- Large Pharmaceutical Companies

- Contract Research Organizations (CROs)

By Commercialization & Sales Operations

- Sales Pipeline Lead Prioritization

- Automated HCP Follow-up & Personalization

- Medical Affairs & Marketing Content Drafting

By Pharma Market Research Analytics

- Simulated Respondent Panels & Scenario Modeling

- Dynamic Survey Querying & Synthesis

- Multi-signal Continuous Trend Tracking

Regional Analysis

North America held a 51.0% share in 2026, valued at USD 164.8 Million.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

North America's structural dominance reflects the concentration of top-tier pharmaceutical headquarters, FDA regulatory proximity, and the deepest pool of agentic AI infrastructure vendors in a single geography. The United States accounts for 89.2% of North American revenue, anchored by enterprise deals between large pharma and domestic AI platform providers. The FDA's formal integration of AI-assisted submissions into oncology fast-track reviews removes the regulatory ambiguity that slows adoption in other regions.

Asia-Pacific is the fastest-growing region. Japan-headquartered pharmaceutical firms recorded a net increase in clinical trial starts during 2025 by deploying automated clinical planning tools, while China-based sponsors reached an all-time high in global research collaborations and out-licensing deals that same year. Europe presents a more complex picture. Western Europe holds a 27% share of global clinical trial country utilization in 2026, yet the region saw a 17% structural decline in trial starts versus 2019 baseline levels, pushing European sponsors toward autonomous site monitoring software to recover efficiency. France demonstrated strategic commitment when Servier entered an USD 888 Million discovery alliance with Insilico Medicine in 2026, targeting complex biological mechanisms unavailable through legacy research methods.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Patent Cliff and Workflow Transformation Force Enterprise AI Adoption

Enterprise-wide commitment to agentic AI accelerates as 45% of Pharma IT leaders and 41% of R&D Discovery leaders target end-to-end workflow transformation via agentic systems in 2025. AWS launched "Amazon Bio Discovery" in April 2026, enabling scientists to orchestrate complete drug discovery pipelines autonomously using natural language. The convergence of executive mandate and ready infrastructure removes the two barriers that previously stalled enterprise deployment: capability uncertainty and integration complexity.

Clinical development productivity gains compound the investment case. Life sciences firms project 35% to 45% time savings across core functions as organizations reengineer workflows around semiautonomous collaborators. Firms that complete this structural shift by 2027 will hold a durable speed advantage over competitors still running manual protocol design and trial monitoring.

Regulatory Enforcement and ROI Uncertainty Slow Mid-Market Adoption

The U.S. FDA issued its first warning letter in 2026 citing an automated manufacturer for improperly delegating operations to AI agents, establishing that regulatory enforcement for cGMP compliance now explicitly extends to agentic systems. Pharmaceutical manufacturers cannot treat AI autonomy as an internal IT decision. Every agentic deployment that touches a regulated manufacturing or quality process requires documented human oversight protocols and validation evidence before it goes live.

Strategic feasibility data projects that 40% of agentic AI projects face cancellation by 2027 due to misaligned capabilities and unclear ROI metrics. Mid-tier pharmaceutical companies without dedicated AI operations teams face the highest cancellation risk. Vendors that cannot demonstrate measurable pipeline acceleration within 12 months of deployment will lose renewal contracts to more narrowly scoped point solutions.

Multi-Agent Ecosystems and Venture Capital Open a USD 30 Billion Value Window

Life sciences multi-agent system ecosystems target an annual value-capture range of USD 18 Billion to USD 30 Billion across pharmaceutical pipelines, R&D, and quality assurance workstreams. Enterprise risk orchestration startup Geordie AI secured EUR 25 Million (USD 28.9 Million) in early 2026 to mitigate multi-agent vulnerabilities specifically for Owkin, confirming that AI governance infrastructure is now an investable category alongside the platforms themselves. The governance layer represents a recurring revenue opportunity that did not exist three years ago.

Venture allocations to specialized clinical agentic architectures have exceeded USD 3.8 Billion as major life sciences corporations deploy strategic funding into biotech co-development programs. Capital concentration at this scale signals that the market is past the seed-stage experimentation phase. Investors are funding commercial-scale deployments, and the competitive window for new entrants is narrowing to specialized niches where general-purpose platforms cannot match domain depth.

Market Trends

Semiautonomous Orchestration Shifts From Pilot to Production Across Regulated Pipelines

Global Capability Centers report 40% to 45% execution cost reductions and doubled speed-to-insight metrics after shifting execution-heavy tasks to autonomous agents in 2026. Insilico Medicine and Liquid AI jointly launched the "LFM2-2.6B-MMAI" model in March 2026, the first compact scientific foundation model built through a specialized curriculum for pharmaceutical science tasks, demonstrating that the market is now generating purpose-built foundation models rather than adapting general-purpose architectures.

Market Competition Overview

The Global Agentic AI in Pharmaceutical Market is fragmented, with no single vendor holding a dominant share across all application segments. Competition divides along three structural lines: pure-play AI drug discovery platforms, pharmaceutical IT infrastructure providers scaling into autonomy, and hyperscale cloud vendors building pharmaceutical-specific agentic environments.

Strategic co-development commitments exceeded USD 100 Million in single-month milestones in 2026 as Eli Lilly, GSK, and Pfizer partnered with Chai Discovery, Noetik, and Boltz to embed domain-specific models in production pipelines. These deals restructure competitive positioning in real time: AI platform vendors that secure a co-development anchor with a top-20 pharma company gain exclusive data access and deployment scale that pure-software competitors cannot replicate.

Company Profiles

Schrödinger, Inc. operates as the deepest physics-based AI molecular discovery platform in the market, generating total revenue of USD 256 Million in FY2025, a 23% year-over-year increase. Software revenue reached USD 199.5 Million, growing 11% from 2024, while the drug discovery division more than doubled to USD 56.4 Million. The company's institutional software gross profit margin of 73% in Q3 2025 signals a scalable software economics model rather than a services-dependent revenue structure, which gives it durable pricing power as enterprise contracts expand.

Recursion Pharmaceuticals pursues a data-at-scale strategy, generating total revenue of USD 74.7 Million in FY2025 versus USD 58.8 Million in 2024, with Q4 2025 revenue alone reaching USD 35.5 Million compared to USD 4.5 Million in Q4 2024, driven by milestone payments from Roche, Genentech, and Sanofi. Recursion allocated USD 475.3 Million to R&D expenses in FY2025 and achieved a cumulative payout exceeding USD 500 Million across platform partnerships by December 2025. Insilico Medicine's USD 2.75 Billion collaboration with Eli Lilly, which included a USD 115 Million upfront cash payment in March 2026, sets the benchmark that Recursion's partnership architecture is now being measured against. Recursion's risk is that milestone-dependent revenue creates quarterly volatility that pure software subscription models avoid.

Key Players

- Atomwise Inc.

- XtalPi

- BenevolentAI

- BioAge Labs

- Valo Health

- Verge Genomics

- Cloud Pharmaceuticals

- Relay Therapeutics

- Schrödinger Inc.

- Cyclica Inc.

- DeepCure

- Envisagenics

- Evaxion Biotech

- Healx

- Iktos

- Insilico Medicine

- Owkin

- Peptone

Regulatory Landscape

The U.S. FDA moved 63% of its internal AI use case portfolio into active production by FY2025, and authorized more than 1,000 AI/ML-enabled medical and clinical software devices by early 2026, with 258 to 295 individual devices cleared in calendar year 2025 alone. The FDA's first warning letter in 2026 citing improper AI agent delegation in manufacturing establishes that regulatory accountability for autonomous systems now extends to operational decisions, not only to model outputs. Pharmaceutical manufacturers must document the boundary between AI-initiated actions and human-approved actions or face enforcement.

Federal health agency adoption reinforces the regulatory direction. The NIH retired 16% of its legacy machine learning use cases in FY2025 to optimize support for modern agentic architectures. HHS deployed generative language systems to 100% of core employees in September 2025. CMS maintained 55% of its AI pipeline in development during FY2025, signaling a structured evaluation posture rather than accelerated deployment. The European Medicines Agency deployed its autonomous internal tool "Elsa AI," while the FDA issued contextual risk credibility guidelines, establishing parallel regulatory frameworks across the two largest pharmaceutical markets that vendors must navigate simultaneously.

Investment and White Space Analysis

Recursion Pharmaceuticals' cumulative payout exceeding USD 500 Million across platform partnerships by December 2025 establishes the commercial validation benchmark for AI-native pharmaceutical platforms seeking enterprise licensing deals. Isomorphic Labs built a total pipeline partnership value of nearly USD 3.0 Billion in early 2024 through strategic collaborations with Eli Lilly and Novartis alone. Both data points confirm that top-20 pharmaceutical companies are allocating nine-figure partnership budgets to AI platform vendors with proven structural biology or molecular simulation capabilities. The white space lies in mid-market pharmaceutical companies and regional biotechs that have not yet signed anchor partnerships and cannot afford bespoke platform development.

Clinical operations automation represents the most underserved application category relative to pipeline value. Venture capital has concentrated on molecular design and target identification, leaving autonomous trial monitoring, regulatory submission drafting, and medical affairs content agents undercapitalized relative to their addressable market. Vendors entering the clinical operations autonomy segment in 2026 and 2027 face lower competitive density and direct access to procurement budgets that clinical operations heads control independently of R&D IT governance cycles.

Recent Developments

- March 2026: Horizon Europe Consortium. Partnership. A consortium under the Horizon Europe framework initiated a collaboration offering physics-informed autonomous AI agents to break down multi-step pharmaceutical tasks including GPCR modeling workflows.

- Early 2026: Sanofi. Licensing Agreement. Sanofi expanded global R&D efficiency through a multi-year commercial licensing agreement for BenchSci's "ASCEND" AI workbench, targeting autonomous experimental design and evidence synthesis across research programs.

- May 2026: U.S. Department of Health and Human Services. Policy Release. HHS released its official FY2025 AI Use Case Inventory, formally documenting the emergence and pre-deployment tracking of agentic AI systems across the CDC, FDA, CMS, and NIH.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 312.2 Million |

| Market Value (2026) |

USD 445.4 Million |

| Forecast Revenue (2035) |

USD 9,984.9 Million |

| CAGR (2026–2035) |

41.3% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 – 2024 |

| Forecast Period |

2026 – 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Application (Drug Discovery and Lead Identification, Clinical Trial Design and Recruitment, Clinical-Trial Applications, Preclinical Discovery Workflow), By Deployment (Cloud-based, On-premise), By End-User (Large Pharmaceutical Companies, Contract Research Organizations), By Commercialization & Sales Operations (Sales Pipeline Lead Prioritization, Automated HCP Follow-up & Personalization, Medical Affairs & Marketing Content Drafting), By Pharma Market Research Analytics (Simulated Respondent Panels & Scenario Modeling, Dynamic Survey Querying & Synthesis, Multi-signal Continuous Trend Tracking) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

Atomwise Inc., XtalPi, BenevolentAI, BioAge Labs, Valo Health, Verge Genomics, Cloud Pharmaceuticals, Relay Therapeutics, Schrödinger Inc., Cyclica Inc., DeepCure, Envisagenics, Evaxion Biotech, Healx, Iktos, Insilico Medicine, Owkin, Peptone |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF). |

Frequently Asked Questions

What is the current size of the Agentic AI in Pharmaceutical Market?

▾ The market was valued at USD 312.2 Million in 2025. By 2026, the market is estimated to reach USD 445.4 Million based on the stated growth trajectory. This scale reflects an active commercialization phase where pilot programs are converting into multi-year enterprise contracts.

What is the growth rate of this market?

▾ The market grows at a CAGR of 41.3% through the forecast period from 2026 to 2035. This rate is underpinned by the USD 180 Billion patent cliff, board-level capital allocation urgency, and measurable productivity gains already validated through enterprise deployments.

Which application segment leads the market?

▾ Drug Discovery and Lead Identification leads with a 41.2% revenue share in 2026. Autonomous systems deliver their highest measurable impact at this earliest pipeline stage, where target identification from large biological datasets compresses timelines that would otherwise take human researchers’ months.

Which application segment grows fastest?

▾ Clinical Trial Design and Recruitment and Clinical Trial Optimization and Monitoring are growing fastest as pharmaceutical firms extend autonomous orchestration downstream from discovery into mid-pipeline execution. The 14% net expansion in active Phase II immunology trial starts from 2024 to 2025 is creating demand for high-throughput multi-agent monitoring across complex patient groups.

Which region leads the Agentic AI in Pharmaceutical Market?

▾ North America leads with a 52.0% share in 2026, with the United States accounting for 88.8% of that total. The FDA's systematic authorization of AI/ML-enabled clinical devices and its formal acceptance of AI-assisted drug submissions create a commercial environment unmatched globally for deploying autonomous pharmaceutical platforms.

Which region grows fastest?

▾ Asia-Pacific is the fastest-growing region. China reached an all-time high in global research collaborations and out-licensing deals in fiscal year 2025, while Japan recorded a net increase in clinical trial starts through automated planning systems. Both trends signal accelerating institutional investment in agentic pharmaceutical infrastructure across the region.

Who are the leading companies in this market?

▾ Insilico Medicine and Schrödinger, Inc. are among the most commercially prominent players. Insilico secured up to USD 2.75 Billion in partnership value with Eli Lilly in March 2026, while Schrödinger reported USD 256 Million in total revenue for fiscal year 2025, a 23% year-over-year increase driven by its physics-based and AI molecular discovery platform.

What are the biggest drivers of this market?

▾ The USD 180 Billion patent cliff between 2024 and 2030 is the primary structural driver, compelling pharmaceutical executives to compress discovery timelines through autonomous systems. Regulatory validation from the FDA's fast-tracking of 12 oncology drugs using AI target identification in 2024 removed a critical deployment barrier and accelerated enterprise procurement decisions.

What are the biggest challenges facing this market?

▾ Regulatory enforcement risk and ROI ambiguity are the two most immediate challenges. The FDA's 2026 warning letter citing improper delegation of operations to AI agents under cGMP rules introduced compliance liability for unprepared organizations. Strategic feasibility studies project that 40% of agentic AI projects face cancellation by 2027 due to misaligned capacities and unclear return on investment metrics.

What is the investment opportunity in this market?

▾ Life sciences firms stand to capture between USD 18 Billion and USD 30 Billion annually through multi-agent system ecosystems targeting pipeline, R&D, and quality assurance optimization. Venture allocations to specialized clinical AI architectures have already exceeded USD 3.8 Billion, with the clearest white space in clinical trial automation for mid-tier pharmaceutical companies and CRO-focused agentic platforms serving Asia-Pacific and Western Europe.