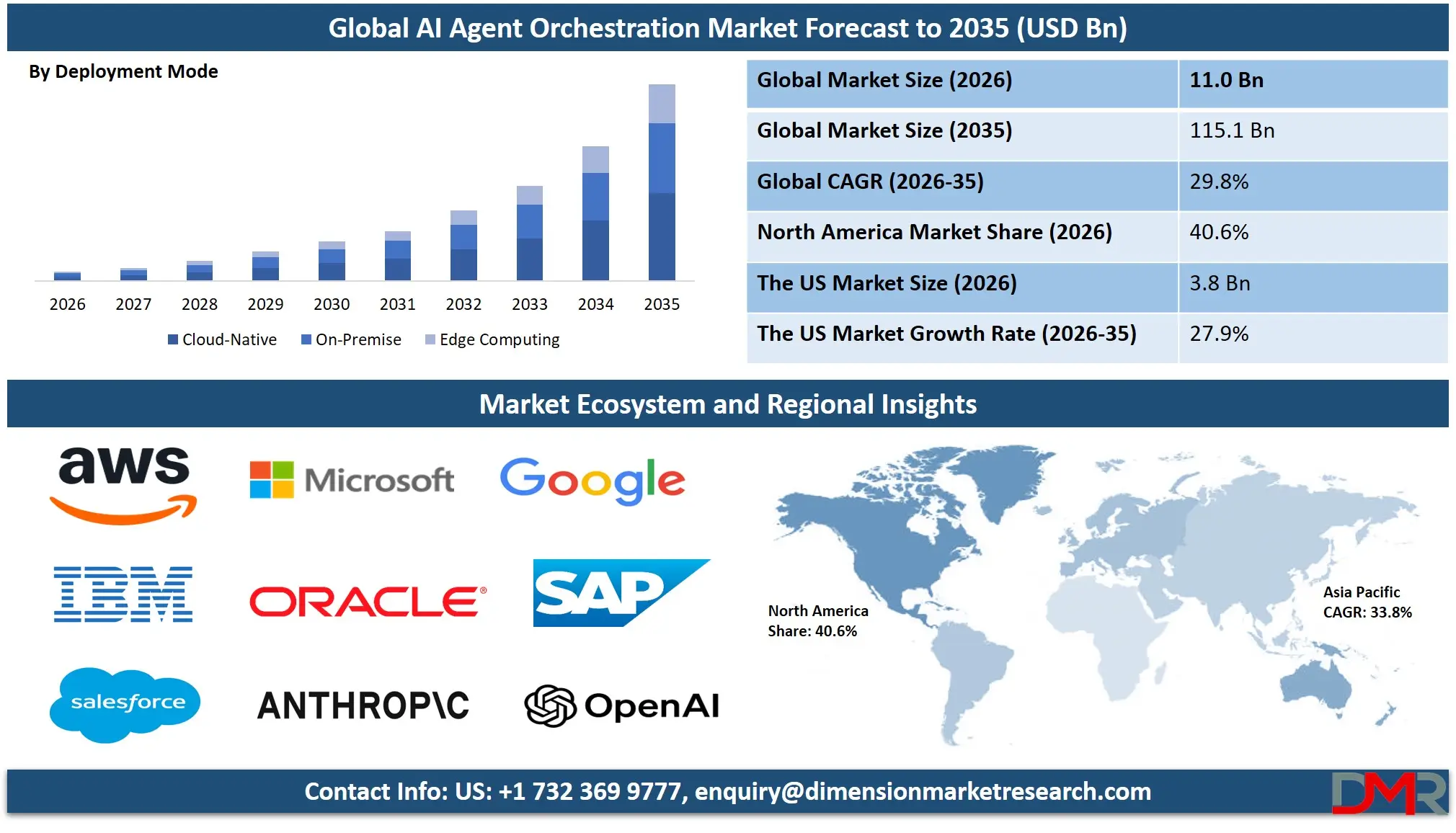

What is the Global AI Agent Orchestration Market Size?

The Global AI Agent Orchestration Market size is estimated at USD 11.0 billion in 2026 and is expected to reach USD 115.1 billion by 2035, expanding at a CAGR of 29.8%, driven by advancements in multi-agent coordination, real-time workflow inference, integration of memory-augmented agent pipelines, and the development of interoperable enterprise IT ecosystems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The AI agent orchestration market is experiencing steady growth, driven by increased adoption of autonomous agent swarms in enterprise automation, regulatory pressure to reduce decision latency, and rising public and private investment in computational agent coordination initiatives across research and production environments. The market is further shaped by advancements in real-time state management, predictive task decomposition, automated agent conflict resolution, and interoperability frameworks supporting multi-agent deployment.

Enterprises, payers, and IT vendors are increasingly investing in digital modernization to improve system resilience, reduce workflow failure rates, and enhance overall operational productivity. The move towards automation, predictive scaling of agentic workflows, and smart workload splitting (initial agent planning + final human validation) is increasing adoption. Moreover, the need to operationalize national AI strategies and the importance of sustainable evidence-based orchestration are driving digital changes in computational enterprises, and AI agent orchestration has become an essential part of the future intelligent automation economy on a global scale.

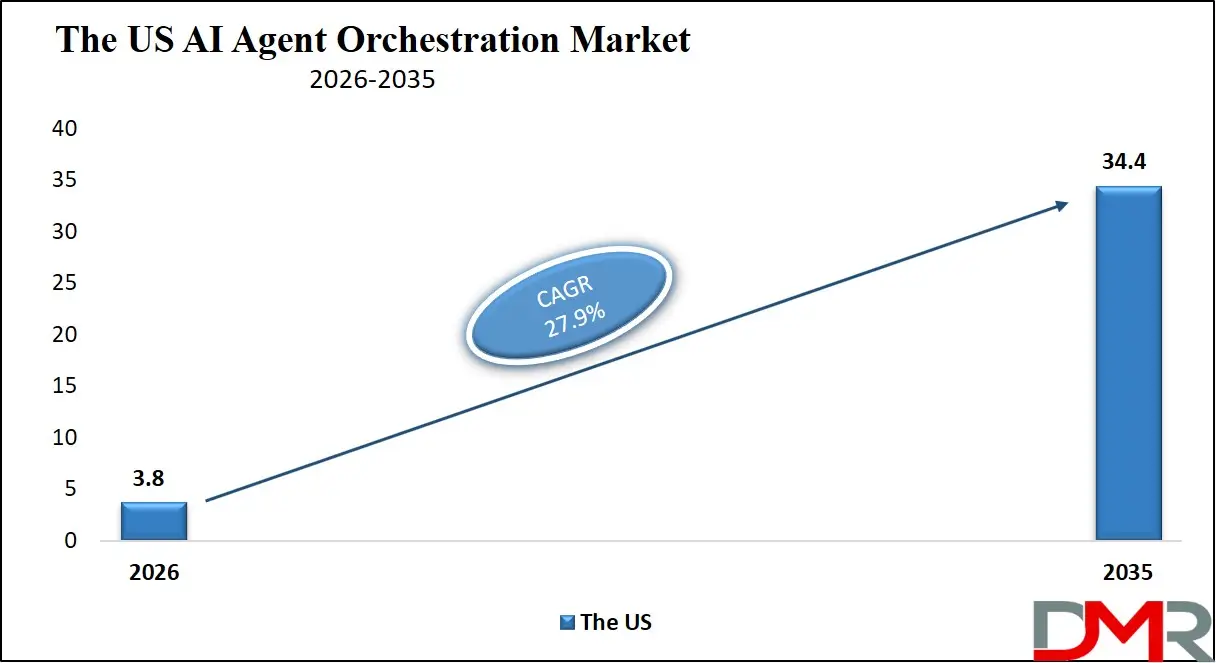

The US AI Agent Orchestration Market

The US AI Agent Orchestration Market is estimated to grow to USD 3.8 billion in 2026 with a compound annual growth rate of 27.9% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US market is characterized by the presence of substantial federal funding programs such as ARPA-H, the NSF's National AI Research Resource, and the DARPA's Adaptive Agent Orchestration program, all of which contribute to the growth of the need for AI-driven agent coordination, real-time telemetry, and predictive success modeling. Agent orchestration engines and state management layers continue to be adopted faster within the region, with the US requiring advanced interoperability frameworks, real-world workflow integration, and verifiable agentic AI assurance. Also, service providers are being pressured by initiatives like the Executive Order on AI and national AI in enterprise strategies to create dedicated integration and deployment services to guarantee data interoperability, security, and compliance across a variety of industrial and academic orchestration ecosystems.

Europe AI Agent Orchestration Market

The Europe AI Agent Orchestration Market is estimated to be valued at USD 2.4 billion in 2026, witnessing growth at a CAGR of 27.6%, during the forecast period.

Europe has a mature AI agent orchestration market, and this has a significant influence on the regulatory requirements and regional policies such as the EU AI Act, the European Data Strategy, and national digital enterprise programs (e.g., France's AI for Industry and Germany's Sovereign Cloud initiative). Countries are also striving for smart orchestration modularization to harmonize industrial and academic workload requirements and interoperability of the cross-border data supply chain. Advanced technologies, like real-time state engines and high-reliability agent scoring systems with built-in predictive algorithms for task drift, drive innovation. Public-private partnerships and harmonization of agent orchestration standards facilitate adoption. Technologies like real-time computational workload balancing and smart contract-based data sharing are commonly practiced as research-centric programs, and Europe is a frontrunner in terms of the digital transformation of safe and efficient AI agent orchestration.

Japan AI Agent Orchestration Market

The Japan AI Agent Orchestration Market is projected to be valued at USD 616.2 million in 2026, progressing at a CAGR of 25.9%, during the period spanning from 2026 to 2035.

Japan boasts a mature AI agent orchestration market supported by high-performance robotic process automation, diagnostic integration technology, and a wide network of robotic IoT AI innovations. Automation, precision, and operational integrity are the priorities in the country and are achieved by predictive orchestration logic wear models and intelligent power management systems for agentic assets. Growth is stimulated by government actions under the Society 5.0 initiative and constant investment in digital infrastructure. The high volume of aging population care, chronic disease management, and industrial automation requires efficient agent orchestration for real-time evidence-based inference. The difficulties are high validation costs for new orchestration logic architectures and integration with legacy workflow systems, yet the prospects are in exporting developed agent orchestration technologies to Asian and Pacific markets.

Key Takeaways

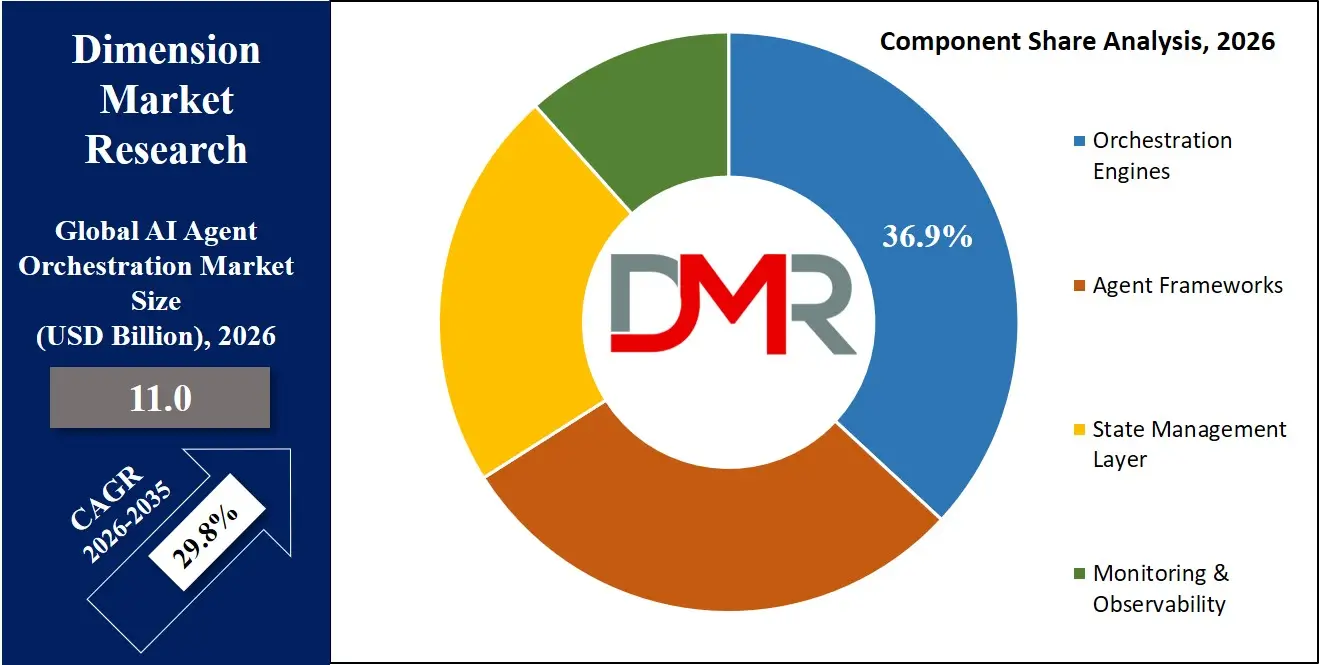

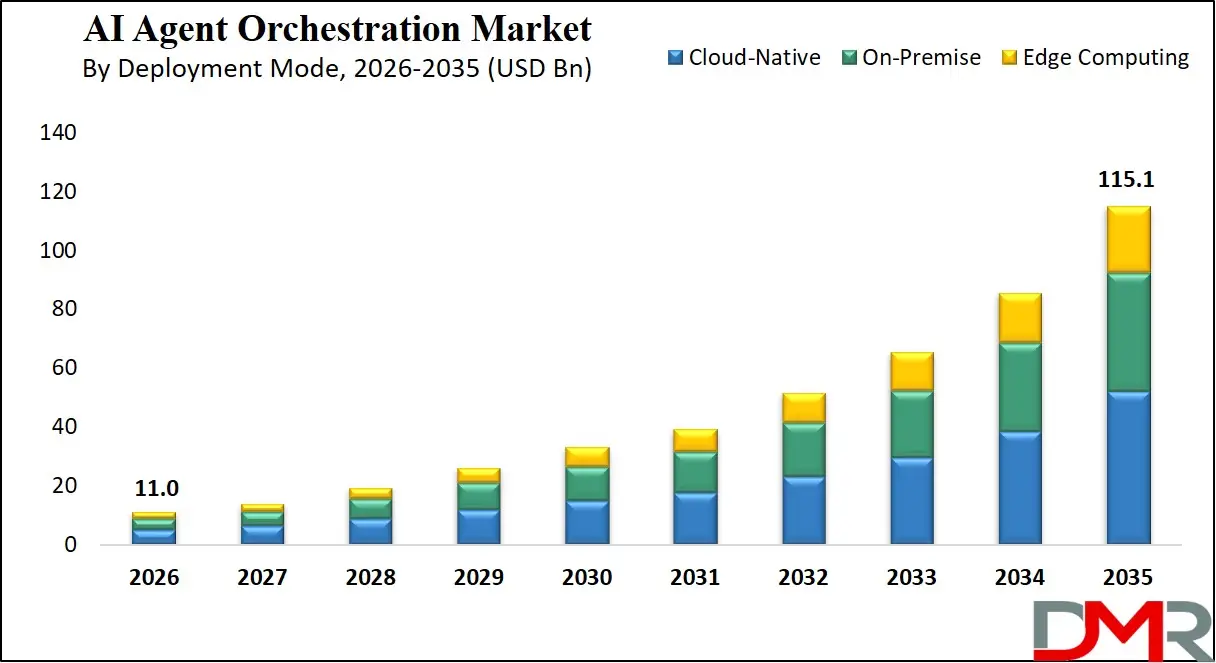

- Market Size & Forecast: The Global AI Agent Orchestration Market is estimated to be valued at USD 11.0 billion in 2026 and is expected to grow to USD 115.1 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 29.8% in the forecast period.

- Primary Growth Drivers: Technological progress in multi-agent task decomposition and real-time evidence-based inference, regulatory requirements for faster decision-making and lower operational costs, and enterprise deployment of intelligent orchestration platforms are some of the key drivers of growth in the market.

- Key Market Trends: The use of predictive orchestration success management, real-time state graph optimization, and transition to cloud-native agent telemetry and fleet management systems are some of the primary market trends.

- By Component: The Orchestration Engines segment is anticipated to get the majority share of the AI agent orchestration market in 2026.

- By Deployment Mode: The Cloud-Native segment is expected to occupy the largest revenue share in 2026 in the AI agent orchestration market.

- By End-User Industry: The Healthcare segment is expected to get the largest revenue share in 2026 in the AI agent orchestration market.

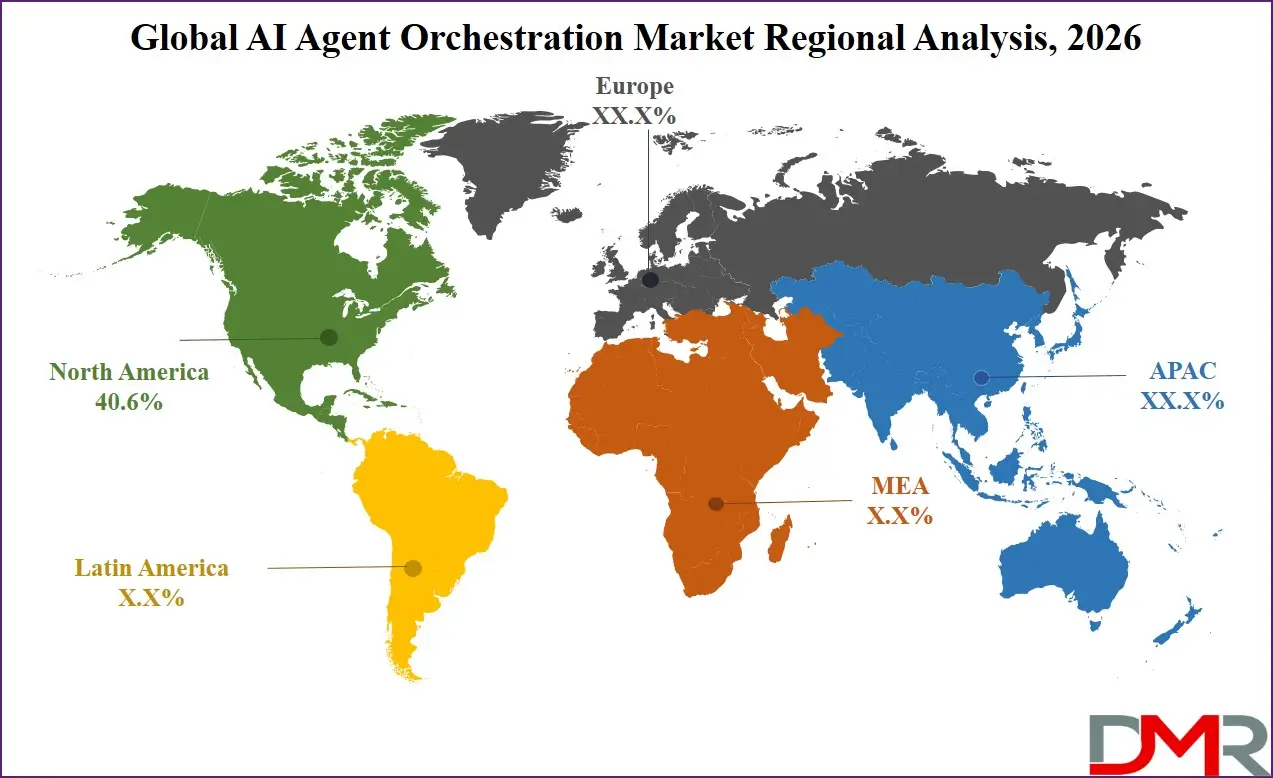

- Regional Leadership: North America is predicted to dominate the market with an estimated 40.6% share in 2026, with high enterprise AI spend and agentic AI investment.

What is AI Agent Orchestration?

AI agent orchestration is a specialized computational application that mimics evidence-based workflow reasoning to assist organizations in coordinating autonomous agents, predicting task handoffs, and real-time state monitoring. It employs state graphs, reinforcement learning algorithms, operational guidelines, and real-time multi-modal data integration to provide high-accuracy task decomposition and extreme workflow efficiency. The contemporary systems have real-time telemetry, REST/gRPC-based interoperability, and AI-assisted confidence scoring to ensure transparency, efficiency, and operational reliability. These orchestration platforms are capable of supporting efficient automation workflows, sustainable evidence-based operations, and help direct the funds of enterprises, government, and research stakeholders towards scalable, long-period IT infrastructure. They also facilitate accountability by making sure that orchestration performance data is quantified, tracked, and in line with global enterprise automation objectives.

Use Cases

- Task Decomposition & Allocation: AI orchestration supports real-time task-agent interaction prediction, conflict alerts, and workload guidance with sub-second latency, reducing workflow failure rates by orders of magnitude compared to manual rule-based systems.

- Orchestration Success Prediction Modeling (Ops Risk): Operational data, including cumulative predicted task success per agent and validation costs, is modeled to provide workflow adjustments and continue safe operation without disruption to maintain operational stability and operator trust.

- Real-Time State & Memory Management: Enterprise deployments are employing state graphs and multi-agent reinforcement learning accelerators to perform on-device drift detection, off-target agent interaction suggestion, and anomaly detection with quantifiable and proven accuracy.

- Industry & Government Programs: More efficient AI orchestration contributes to the success of supply chain resilience, fraud detection, and smart surveillance, facilitate national AI adoption, contribute to deployment reliability, and help implement policies, such as the AI governance policy and enterprise automation policy.

How AI Is Transforming the Global AI Agent Orchestration Market?

Artificial intelligence is transforming agent orchestration by enabling predictive modeling of orchestration success probability, automatic identification of anomalies in workflow logic performance data, and real-time optimization of task thresholds per operational context. Telemetry and multi-modal data can be analyzed with AI algorithms to determine any degradation or performance drift and scale-optimize orchestration outcomes. This saves time, is verifiable and cheaper than manual data analysis.

Moreover, AI enhances operational assurance through offering adaptive computational event-based scheduling, anticipating workflow threats to orchestration logic, and intelligent prioritization of agent health monitoring. It is also involved in reducing the cost of baseline testing and ongoing performance tracking, allowing enterprise IT operators to reduce the cost and physical footprint of on-prem test campaigns and improve the reliability of orchestration workloads and their financial returns.

Market Dynamics

Key Drivers of the Global AI Agent Orchestration Market

Rapid developments in Multi-Agent Learning and Real-Time Workflow Inference

The market is being pushed by a fast uptake of AI-driven task-agent association scoring, high-efficiency state graph processing units, gRPC-based interoperability, and real-time telemetry analytics. These technologies will allow monitoring of the health of orchestration modules in real-time, identify performance anomalies early, predict orchestration success rates, and simplify the process of computational validation. Consequently, operational uptime and inference efficiency are highly enhanced as well as minimizing the expenses of manual telemetry analysis. The growth of multi-agent models for task discovery, in particular, is also accelerating the need for intelligent orchestration, as enterprise operators are more inclined towards automation and workflow optimization based on operational data.

Growing Focus on Enterprise Automation Regulation and Sustainable AI

The world is becoming more and more involved in policies of AI safety, with governments and international bodies proposing automation efficiency policies, like the EU AI Act's transparency provisions and the US NIST's AI Risk Management Framework. These structures are driving a high demand for efficient agent orchestration that can be used to perform ultra-low-latency inference and continuous learning. In parallel, global initiatives such as the OECD's AI Principles are encouraging the adoption of evidence-based orchestration architectures. The increasing calls for transparency in AI automation and reduction in operational costs are also enhancing the necessity of verifiable and safe orchestration in both public and private enterprise systems.

Restraints in the Global AI Agent Orchestration Market

High Costs of Integration and Computational Validation

Orchestration platforms are costly and time-consuming to develop, requiring extensive validation in sandbox environments, testing of task logic reliability, and long-term performance analysis of emerging components. Additionally, regulatory restrictions and data privacy laws (e.g., GDPR, HIPAA, CCPA) further increase development complexity and cost. These factors create barriers for new entrants, extend deployment timelines, and increase upfront capital requirements.

Limited Standardization Across Agentic Data and Workflows

The industry continues to rely on multiple orchestration architectures, including state graph-based, RL-based, LLM-based, and hierarchical agent-based systems. However, the lack of standardized agent handshake protocols beyond frameworks like LangChain and AutoGen remains a key challenge. AI orchestration lacks universal plug-and-play standards compared to traditional workflow engines, making integration complex and limiting interoperability of orchestration logic models.

Growth Opportunities in the Global AI Agent Orchestration Market

Expansion of Emerging Enterprise Automation Programs

Developing markets such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are investing in digital infrastructure and advanced orchestration capabilities. These regions present strong growth potential due to increasing demand for automated decision-making, predictive maintenance, and fraud detection applications. With limited legacy automation infrastructure, they provide opportunities for the deployment of modern orchestration optimized for academic and enterprise environments.

Rising Demand for Cloud-Native Orchestration Deployment

The increased requirement for advanced orchestration is being generated by the growth of decentralized operations, remote collaboration, and real-time multi-agent applications. These technologies play a vital role in virtual enterprise platforms, academic labs, and industry innovation hubs. With the rising importance of sub-second orchestration latency as a major industry concern, cloud-native orchestration inference capabilities are likely to be fundamental to future enterprise and government IT infrastructure.

Global AI Agent Orchestration Market Trends

Predictive Orchestration Success Monitoring and Computational Analytics

Orchestration platforms are being monitored and computational logic anomalies are detected in real time, and task override patterns are predicted using on-system learning. The use of digital twin models and multi-agent algorithms is enhancing computational workflow scheduling, system lifespan, and deployment reliability. This shift is transforming orchestration management from manual workflow review to a fully automated, continuously optimized system monitoring.

Cloud-Native Telemetry and Fleet Management Systems

Cloud computing and digital twin technologies are taking centre stage in the operations of orchestration clusters. These platforms enable real-time storage and analysis of workflow performance data, centralized fleet management, and remote monitoring of agent health. Cloud-native systems enhance transparency, lower on-prem infrastructure expenses, and provide quicker responses to workflow changes across operational nodes, as experienced by operators of large enterprise agent fleets.

Research Scope and Analysis

By Component Analysis

The Orchestration Engines segment is expected to remain the largest in 2026, accounting for about 36.9% of the global AI agent orchestration market, driven by its dominant use in large-scale workflow automation, seamless IT integration, and flexibility across diverse computational frameworks where real-time operational data access and software ecosystem maturity are essential.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Meanwhile, the State Management Layer segment is witnessing strong growth, driven by rising demand for memory retention, context continuity, and session persistence in multi-turn agent interactions where customization and validation are critical. Adoption is further supported by AI-based workflow throttling, real-time efficiency diagnostics, and modular configurations that integrate multiple task logic types for improved workflow flexibility and operator satisfaction.

By Deployment Mode Analysis

The Cloud-Native segment is expected to dominate in 2026, accounting for 43.9% share, driven by the central role of elastic scaling and microservices in executing multi-agent coordination and task discovery. The On-Premise segment forms the second-largest category, as regulated industries heavily rely on data sovereignty and low-latency processing. The Edge Computing segment is witnessing the fastest growth, driven by the ability to run orchestration logic on local devices for real-time inference in manufacturing and telecom environments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By End-User Industry Analysis

The Healthcare segment is expected to hold the largest share in 2026, accounting for 33.3% of the market, driven by the critical need for patient journey coordination, clinical trial automation, and high operational costs. Meanwhile, the Manufacturing segment is witnessing the fastest growth, driven by the ability of orchestration to coordinate robotic agents and predictive maintenance workflows. The BFSI and Retail segments also represent significant shares, driven by fraud detection, customer service automation, and supply chain optimization initiatives. The Telecom segment is emerging for network slicing automation and customer churn prediction applications.

The Global AI Agent Orchestration Market Report is segmented based on the following:

By Component

- Orchestration Engines

- Agent Frameworks

- State Management Layer

- Monitoring & Observability

By Deployment Mode

- Cloud-Native

- On-Premise

- Edge Computing

By End-User Industry

- BFSI

- Healthcare

- Manufacturing

- Retail

- Telecom

Regional Analysis

Leading Region in the AI Agent Orchestration Market

It is projected that North America will take the lead in the global AI agent orchestration market (by value), covering a market share of about 40.6% in the year 2026. The region's dominance is driven by strong enterprise AI workload cadence (US-based NSF and DARPA programs), high orchestration software prices relative to other regions, a mature IT supply chain for advanced interoperability and high-speed data exchange, and the presence of key orchestration vendors and computational research labs. The widespread adoption of advanced multi-agent and state graph-based orchestration for healthcare, manufacturing, and government automation programs further strengthens North America's leading position in the market. Additionally, continuous investments in AI-enabled orchestration logic monitoring and interoperability capabilities are further reinforcing regional technological leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the AI Agent Orchestration Market

Asia-Pacific is the fastest-growing region, supported by strong digital transformation targets (China, India, Japan), increasing enterprise AI sovereignty initiatives, rising investments in domestic orchestration capabilities, and growing adoption of multi-agent systems. The region benefits from well-established IT manufacturing capacity, increasing commercial participation, and alignment with national digital roadmaps. Countries across the region are actively deploying orchestration to enhance operational productivity-per-dollar and strengthen automation infrastructure. Growing emphasis on orchestration R&D and structured computational logic development further accelerates market expansion in the region. Moreover, increasing government support and commercial enterprise commitments are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The AI agent orchestration market is very competitive, with innovation and strategic alliances being the order of the day. In order to achieve a competitive advantage, companies and research labs are oriented towards the creation of new advanced computational orchestration architectures (e.g., multi-agent RL-based, state graph-driven, generative agent-based), AI-powered workflow telemetry, and digital twin-enabled operations monitoring platforms. There are high barriers to entry because of capital-intensive computational validation infrastructure, technical AI/ML know-how, and the need for software ecosystem maturity and enterprise IT certifications.

Strategic approaches in the market to increase market presence include partnerships with enterprise automation vendors, mergers between orchestration designers and system integrators, and long-term orchestration support contracts with enterprise and academic operators. Moreover, research and development in advanced interoperability frameworks and event-driven computational software frameworks are important factors in staying competitive and meeting the changing needs of the enterprise industry.

Some of the prominent players in the Global AI Agent Orchestration Market are:

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC

- IBM Corporation

- Oracle Corporation

- Salesforce, Inc.

- SAP SE

- OpenAI, Inc.

- Anthropic PBC

- Meta Platforms, Inc.

- LangChain, Inc.

- LlamaIndex, Inc.

- CrewAI, Inc.

- deepset GmbH

- Pydantic Services Inc.

- ServiceNow, Inc.

- UiPath, Inc.

- Appian Corporation

- Pegasystems Inc.

- Databricks, Inc.

- Other Key Players

Recent Developments

- April 2026: Microsoft expanded its enterprise AI agent ecosystem through a strategic partnership with Stellantis, focusing on AI-driven workflow automation, predictive maintenance, and digital service deployment across automotive operations using Azure AI and cloud-based agent systems.

- January 2026: Amazon Web Services, Inc. enhanced Amazon Bedrock Agents with improved multi-step reasoning, tool orchestration, and enterprise API integration, enabling more autonomous AI agents for business process automation across cloud environments.

- November 2025: Anthropic's Claude models were integrated into Microsoft's enterprise ecosystem, including Microsoft Foundry and Copilot platforms, enabling cross-cloud deployment of frontier AI models for agent-based workflows.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 11.0 Bn |

| Forecast Value (2035) |

USD 115.1 Bn |

| CAGR (2026–2035) |

29.8% |

| The US Market Size (2026) |

USD 3.8 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Component (Orchestration Engines, Agent Frameworks, State Management Layer, Monitoring & Observability), By Deployment Mode (Cloud-Native, On-Premise, Edge Computing), By End-User Industry (BFSI, Healthcare, Manufacturing, Retail, Telecom) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global AI Agent Orchestration Market?

▾ The Global AI Agent Orchestration Market size is estimated to have a value of USD 11.0 billion in 2026 and is expected to reach USD 115.1 billion by the end of 2035.

What is the CAGR of the Global AI Agent Orchestration Market from 2026 to 2035?

▾ The market is growing at a CAGR of 29.8% over the forecasted period.

What factors are driving the growth of the Global AI Agent Orchestration Market?

▾ The market is driven by advances in multi-agent task decomposition and real-time evidence generation, regulatory pressure to accelerate decision-making and reduce operational costs, and increasing government investment in national enterprise AI infrastructure.

What are the major trends in the Global AI Agent Orchestration Market?

▾ The key market trends include the adoption of predictive alert fatigue management and real-time operational decision monitoring, along with a growing shift toward cloud-native orchestration platforms and telemetry-enabled workflow management systems.

Which region held the largest share of the Global AI Agent Orchestration Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 40.6%.

Which region is expected to grow the fastest in the Global AI Agent Orchestration Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global AI Agent Orchestration Market?

▾ Some of the major key players in the Global AI Agent Orchestration Market are Microsoft Corporation, Google LLC, AWS, IBM Corporation, Salesforce, ServiceNow, Inc., and many others.

How is the Global AI Agent Orchestration Market segmented?

▾ The market is segmented by component, deployment mode, and end-user industry.