What is the AI-Generated Video Content Market Size?

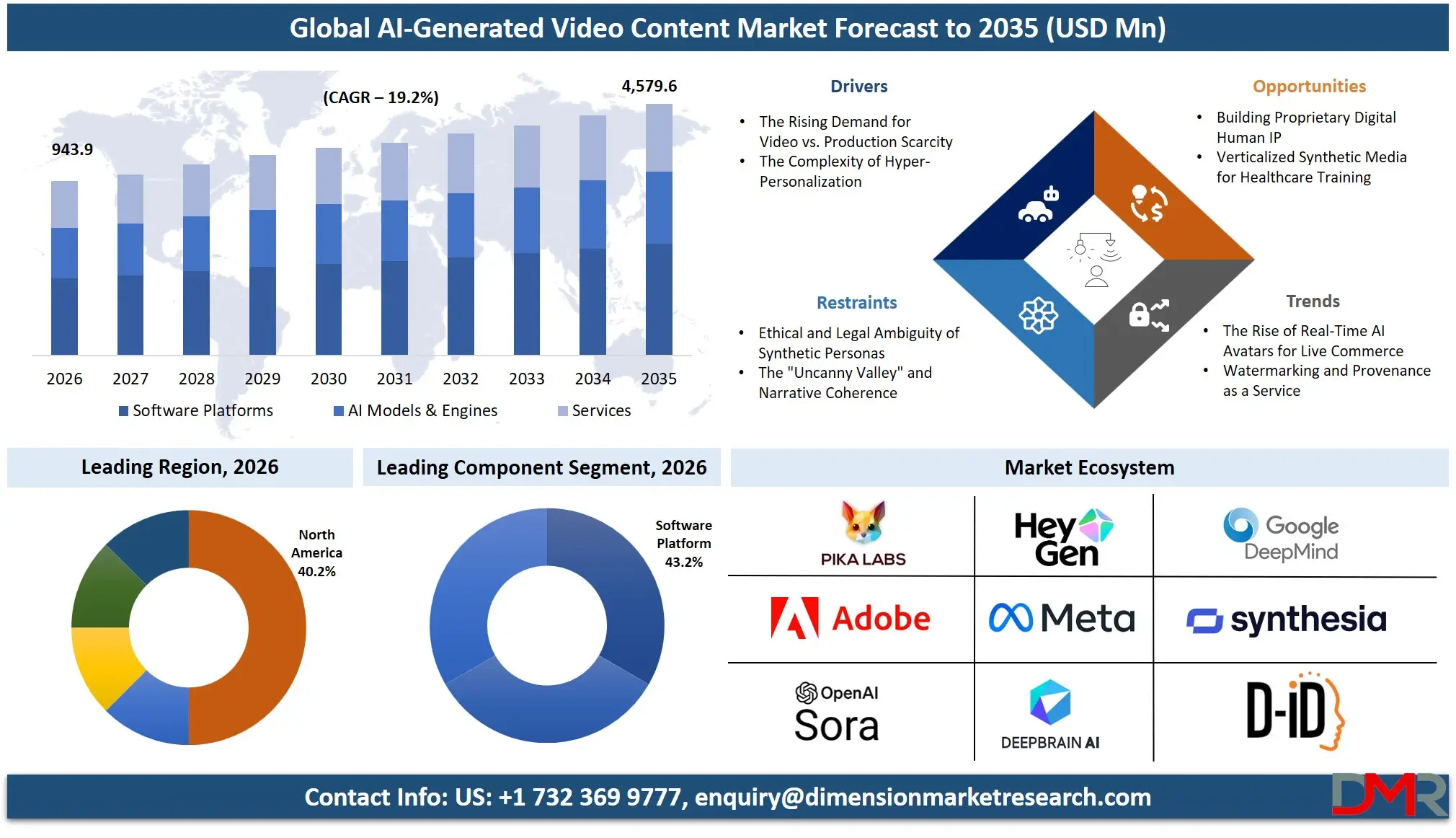

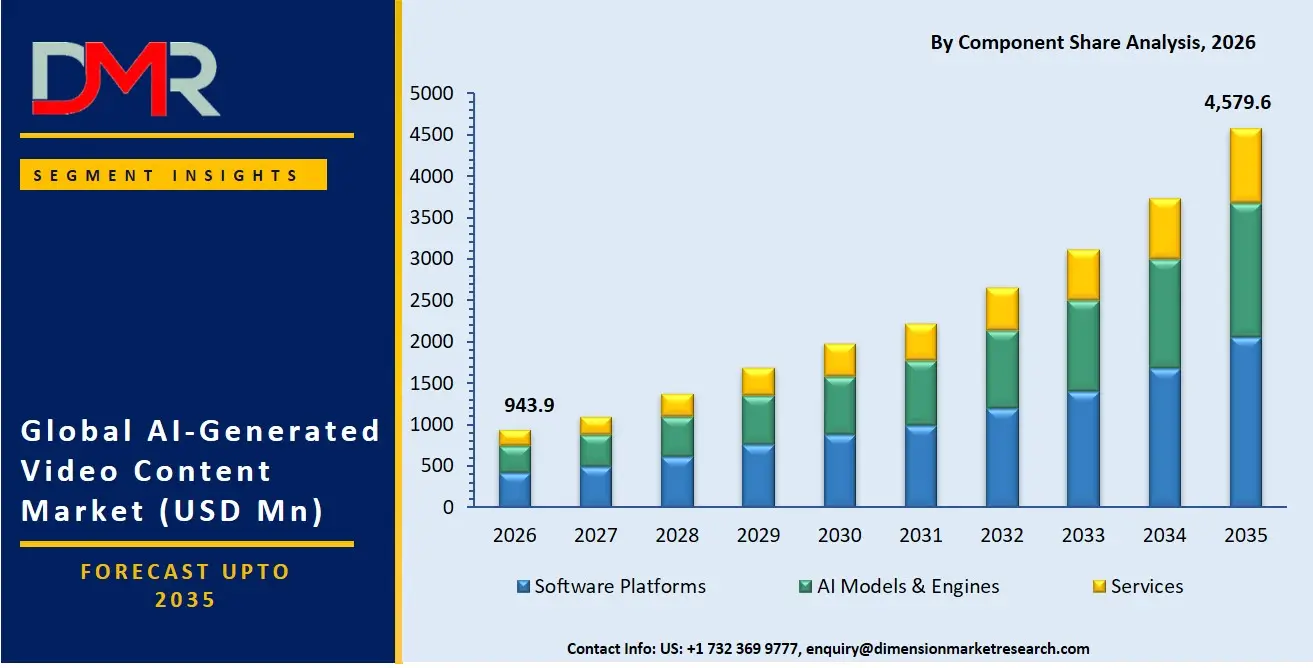

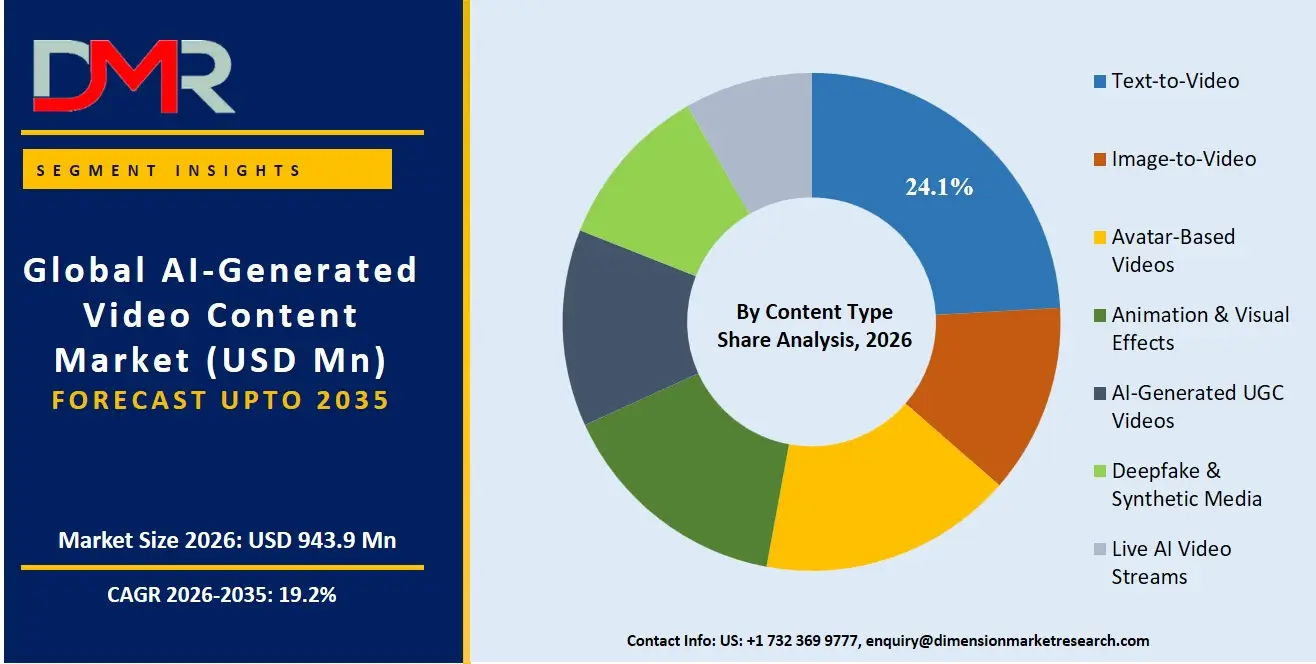

The Global AI-Generated Video Content Market is expected to reach a value of USD 943.9 million in 2026, and it is further anticipated to reach USD 4,579.6 million by 2035, growing at a CAGR of 19.2% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The AI-generated video content market has been expanding at an exponential rate, as businesses and creators are striving to keep up with the skyrocketing demand for video content without any linear rise in production costs or time commitments.

It comprises software platforms, AI models and engines, and specialized services which facilitate the automated or assisted production of video content from textual, pictorial, or audio inputs. As businesses seek to create personalized marketing materials, immersive virtual environments, and scalable e-learning content, the need for specialized generative AI video tools is growing. Among the most common are enterprises and digital-native creators, who are consistently generating video content using cloud-based, API-driven video generation because of its scalability and integration options. The media and entertainment industry, the advertising industry and the education industry are significant players as they demand high velocity, low cost and highly engaging video ecosystem.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

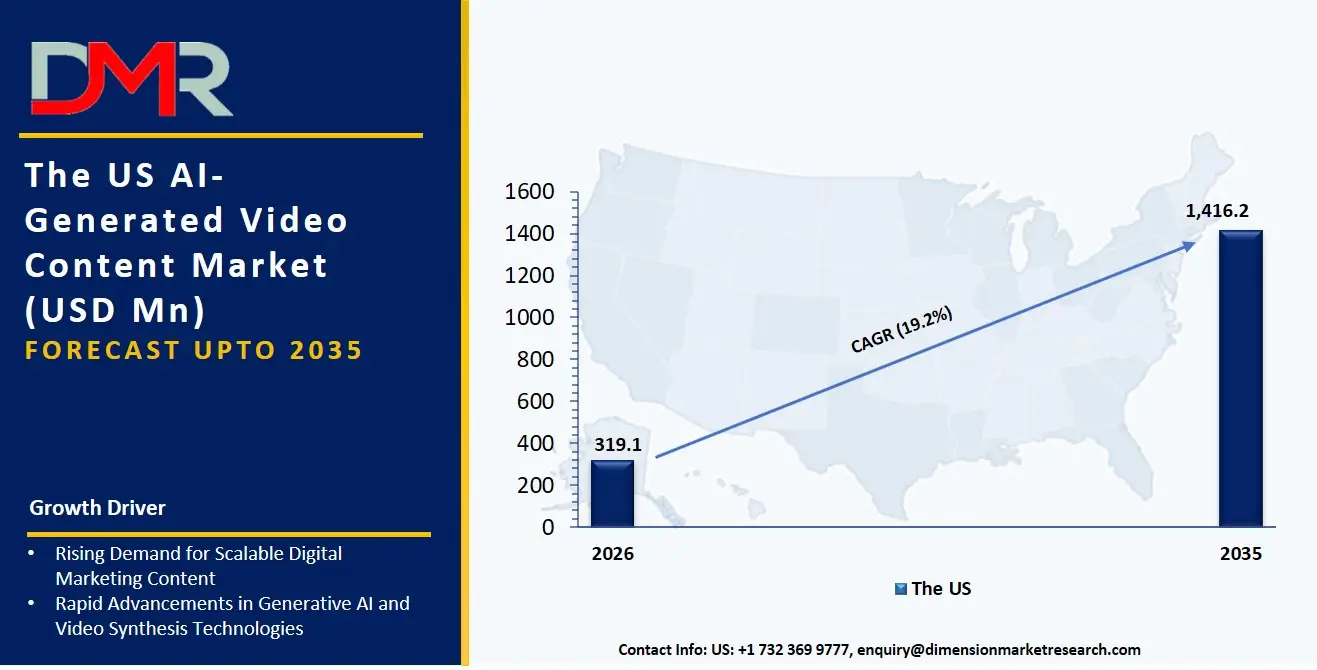

The US AI-Generated Video Content Market

The US AI-Generated Video Content Market is projected to reach USD 319.1 million in 2026 at a compound annual growth rate of 18.0% over its forecast period, culminating in a value of USD 1,416.2 million by 2035.

The US continues to be the largest and most developed market in AI-generated video content due to the aggressive content strategies of Fortune 500 brands and the massive concentration of AI research labs and talent. High demand for Avatar-based videos, animation, and VFX services typify the market, where organizations are targeted to produce a video of their spokesperson on a large scale without the need for traditional video shooting. Besides, the implementation of Generative Adversarial Networks (GANs) and Diffusion Models in visual workflows is producing a similar need in professional Services for custom model fine-tuning to regulate brand safety, deepfake ethics, and content authenticity frameworks.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe AI-Generated Video Content Market

The Europe AI-Generated Video Content Market is estimated to be valued at USD 272.1 million in 2026 and is further anticipated to reach USD 1,280.7 million by 2035 at a CAGR of 18.8%. The regulatory frameworks including GDPR and the upcoming EU AI Act have a significant impact on the European market and drive the need to employ ethical AI Services and synthetic media detection tools. Accelerated growth of on-premises and hybrid Deployment Modes is also being experienced in the region as European broadcasters and automotive advertisers in Germany and France are trying to strike a balance in data privacy with AI-driven content production. Moreover, the work to define trusted AI standards is testing software platform providers and their capacity to build separate, consent-based digital replica and avatar systems for safeguarding creator rights and content provenance throughout European media systems.

The Japan AI-Generated Video Content Market

The Japan AI-Generated Video Content Market is projected to be valued at USD 99.5 million in 2026. It is further expected to witness robust growth, holding USD 420.3 million in 2035 at a CAGR of 17.4%. The Japanese market is special because of a corporate push towards content localization and a shrinking traditional animation workforce. A significant portion of the spend is on Avatar-Based Videos and AI-Generated UGC Videos, which enable large media conglomerates and gaming studios to scale virtual influencer video activations and localize video content in multiple languages without manual dubbing or subtitling. Furthermore, a pressing need exists to delve into the local market and eliminate the disconnect between the style of hand-drawn animation and the adoption of novel neural rendering techniques, creating a niche in the field for Transformer Model fine-tuning for generating content in the manga and anime styles.

Key Takeaways

- Market Size & Forecast: The Global AI-Generated Video Content market is projected to reach USD 943.9 million in 2026, expanding dramatically to USD 4,579.6 million by 2035, driven by the dual forces of hyper-personalized advertising and the creator economy's demand for high-volume, low-cost video production.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 19.2%, fuelled by the urgent demand to produce scalable video and the increasing sophistication of diffusion models that can generate high-resolution, coherent video sequences on standard cloud GPUs.

- Primary Growth Drivers: Widespread shift from static ads to dynamic AI-Gen UGC videos, Enterprise-grade Software Platforms must ensure brand safety when generating content on social media, and the need for Speech Synthesis & Voice Cloning necessitates API-based video generation tools.

- Key Market Trends: The growing popularity of interactive live AI video streams, the integration of Large Language Models (LLMs) in script-to-video workflows for auto-generation of narrations, and the adoption of certified ethical synthetic media by corporate boards in response to the threats of misinformation are some of the key trends in the market.

- By Deployment Mode Analysis: Cloud-Based models are projected to dominate this segment as a result of computational gravity and collaborative workflow needs. There is an increased need for Professional Services to create seamless hybrid pipelines that integrate on-premise GAN models that are proprietary with cloud-based distribution engines.

- By Application Analysis: Marketing & Advertising and Social Media Content Creation are poised to lead the application segment, because of rapid A/B testing of visual creatives. The fastest growing industry is E-Learning & Training, where corporate knowledge bases need to be quickly transformed into multilingual AI avatar led training modules.

- Regional Leadership: North America is poised to dominate this market with 40.2% of the market share in 2026 as it has a well-established ecosystem of generative AI startups and hyperscale cloud providers to make maximum use of this infrastructure and make it a leader in this market.

What is the AI-Generated Video Content?

AI-Generated Video Content is the specific software, models, and expert guidance provided by third-party AI labs, platform providers, and system integrators that can help organizations and creators navigate the synthetic media lifecycle. These services deal with the automated "how" of creating videos, rather than the manual "how" that is known as video editing (post-production). These include Software Platforms for a no-code user experience for business users, AI Models & Engines as the neural backbone to render pixels from latent representations, and dedicated Services for custom model training and integration. By 2030, it is estimated that 80% of digital content will be synthetically influenced, thus, by AI investments, having professional-grade AI tools is essential for creative control, brand consistency and ethical transparency as opposed to technical unmanageability to translate into production velocity.

Use Cases

- Personalized Video Prospecting at Scale: B2B sales teams use API-Based Video Generation Tools to synthesize thousands of unique Text-to-Video messages—with a digital avatar talking directly to each prospect by name and referencing their company website, it's like a one-to-one recording, but without the camera.

- Corporate E-Learning Localization: Services and Avatar-Based Video platforms enable global corporations to translate a single English language training script into 40+ languages via Speech Synthesis & Voice Cloning without having to re-shoot any video footage of a human presenter.

- Newsroom Automation in Journalism: Media organisations adopt Software Platforms that interact with LLMs to automatically transcribe text articles into short-form videos summarised by a synthetic news anchor, which are published almost instantly after a story breaks and are suitable for social media.

- Interactive Virtual Shopping: E-commerce platforms employ Live AI Video Streams and transformer models to build AI sales assistants that showcase products in real-time, provide voice answers to queries, and demonstrate product features within a dynamically-generated video environment.

Market Dynamics

Key Drivers in the Global AI-Generated Video Content Market

The Rising Demand for Video vs. Production Scarcity

Consumer demand for short-form video creation is limitless, while physical hardware to film, edit and render is limited. As a result of this structural gap in the content supply chain, there is a growing trend of enterprises relying on AI video generation platforms for content creation, instead of relying solely on in-house video teams or agencies. These AI tools can help with vital tasks such as Text-to-Video, avatar narration, and video editing, enabling videos to be scaled up exponentially. By using such technologies, marketing departments can speed up the delivery of their omnichannel campaigns and reduce the opportunity cost of slow manual production.

The Complexity of Hyper-Personalization

Larger businesses will also be more likely to need highly personalized content, such as video variations targeted to specific micro-segments of audiences on platforms like TikTok, Instagram, and YouTube. However, there is no way to use traditional video editing methods to manage a hyper-personalized video campaign logistically. Organizations must coordinate data-driven scripting, dynamic scene assembly, and localized voiceovers with thousands of variations. Without an automated AI pipeline, this complexity potentially leads to creative dilution and a significant amount of human resource investment. Therefore, the demand for API-Based Video Generation Tools to create customized videos through programming has increased.

Restraints in the Global AI-Generated Video Content Market

Ethical and Legal Ambiguity of Synthetic Personas

Despite the advancements in human-like avatar technology, most businesses are still wary of relying on AI generated human avatars, given the unfurling legal landscape of digital likeness rights, legislation against deepfakes and copyright of AI-generated performances. Even though synthetic media can help reduce costs, these issues remain unsolvable and are a major barrier to adoption. The use of Deepfake & Synthetic Media can be legally and reputationally challenging to manage if there are no clear consent regimes and means to prove the origins of content. The groups are concerned about liability of hosting faux talent, regulatory fines and public backlash. This legal uncertainty slows down the adoption of Avatar-Based videos and often hinders large-scale adoption in sectors such as BFSI and Healthcare where regulations are strict.

The "Uncanny Valley" and Narrative Coherence

Although the fidelity of the images is rapidly improving, the fidelity of the temporal models may still lead to physical glitches, disjointed motion and the unsettling "uncanny valley" when dealing with human forms. While an AI-generated clip of 90 seconds may look cool, the absence of logical flow over longer periods of time (several minutes) makes it hard for the higher-stakes audience to trust. In today's business landscape, communication professionals are tasked with safeguarding a company's reputation, and any AI-generated errors can derail a communication strategy's reputation. This technical restriction displaces the attention of the professional service providers from the generation itself back to post generation editing and manual cleanup, somewhat undermining the time saving that was promised.

Growth Opportunities in the Global AI-Generated Video Content Market

Building Proprietary Digital Human IP

A major growth opportunity in the market is to help global brands and celebrities, create their safe and exclusive digital human doubles. Now, A-listers, influencers, and corporate mascots want to be represented by their own AI avatar, with robust governance, monetisation, and aesthetic rules in place. The creation of these intricate digital twins relies on dedicated expertise in custom GAN fine-tuning, Speech Synthesis cloning and blockchain-based identity verification through professional Services. Cloud and AI suppliers can help brands create scalable, unique virtual talent ecosystems that can seem in movies, promote merchandise at live events and on streams, and attend events, all without the constraints of the actual talent. It has the potential to generate a high demand for heavily custom and managed service engagements in the area.

Verticalized Synthetic Media for Healthcare Training

AI video capabilities and a grasp of the unique requirements of regulated sectors are increasingly important, leading healthcare and pharmaceutical companies to seek HIPAA-compliant training solutions. This involves using medical-centric AI video platforms to create patient scenarios for surgical practice or mental health simulations. Healthcare companies must follow strict standards for de-identification of patient information and medical accuracy. Therefore, they need implementation partners with an understanding of Diffusion Models and medical compliance frameworks. Professional service providers might want to consider patient avatar learning using transformers integrated with Learning Management Systems, medical board credits and tailoring symptoms to a specific disease module.

Trends in the Global AI-Generated Video Content Market

The Rise of Real-Time AI Avatars for Live Commerce

Platform engineering is evolving toward real-time, interactive video streams in the video domain. Brands are abandoning their pre-rendered ads and replacing them with AI-powered Live AI Video Streams capable of engaging in conversations, answering product questions, and taking voice commands in real-time during a shopping event, and using digital influencers to do so. AI video platform vendors are stepping up to offer their expertise in neural rendering, ultra-low latency inference and interactive script design. These platforms let you easily integrate corporate databases, sales avatars, and personalities.

Watermarking and Provenance as a Service

As businesses and governments graple with the pressures of misinformation and the drive for transparency, content authenticity is also taking center stage in AI video decisions. AI video strategies that can assist companies to scale their content and then add invisible cryptographic provenance data that complies with the C2PA standard are now of interest. This has brought about the need for anti-deepfake consulting services. Professional service providers can help organizations choose strong fingerprinting methods for GANs, add embedded signals to the GAN when it is being rendered, and create content verification dashboards for end-users.

Research Scope and Analysis

The Global AI-Generated Video Content Market is segmented by component, content type, deployment mode, platform type, enterprise size, technology, application, and end user. The market covers AI-powered video creation platforms, generative technologies, cloud and on-premises deployment models, diverse enterprise applications, and multiple industry verticals globally.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

The component segment of the AI-generated video content market is projected to be dominated by software platforms, as businesses are in need of user-friendly, no-code platforms before they invest heavily in custom AI models. Diffusion Models and Transformer Model APIs often require fine-tuning, and in many cases, creative marketing teams don't have the in-house expertise to do so. Platform services help businesses with storyboarding, template management, compliance guardrails, and multi-channel distribution. Integrations with Web-Based Platforms and Studio & Editing Software are especially popular. With the rise in the use of omni-channel video campaigns by enterprises, the demand to use specialized, all-in-one platform solutions increases. Such platforms minimize technical complexity, enhance creative collaboration, speed up iteration cycles, and enhance long-term returns of content investments.

By Content Type Analysis

Text-to-Video is poised to be the primary content type, as it is the most creative and easy-to-conceptualize. Organizations favor Text-to-Video for its low barrier to entry, where a marketer can type a script and a URL and instantly receive a promotional video with matching b-roll, backing music, and avatar narration. It allows social media teams to activate on-the-moment topical content within minutes, not days, with the model. Thus, the professional services ecosystem has blossomed around Text-to-Video, with key related functions such as complex prompt engineering for guaranteeing uniformity of brand aesthetics, custom Large Language Model (LLM) script crafting, and post-generation polishing to make sure that the output b-roll properly communicates a product's unique traits without AI hallucination artifacts.

By Deployment Mode Analysis

By deployment model, Cloud-Based is projected to dominate this market as it is essentially changing the way economics works for media companies to offer unprecedented access to GPU clusters, global CDN delivery, and lower overall total cost of rendering than building and operating internal rendering facilities. Creative studios use public cloud elasticity when they need to do GPU-heavy rendering, but don't want to invest in over-provisioned hardware. However, the dynamic, consumption-based model for cloud-based rendering also drives the need for professional Services. Companies must have the expertise to advise on cost-per-video optimization, batching video files, managing the render queue to prioritize the most valuable video campaigns, and integrating with API to ensure that cloud-rendered video content seamlessly feeds into a DAM or social media scheduling tool.

By Platform Type Analysis

Web-based platforms is poised to dominate the platform type segment because they provide instant accessibility, cross-device compatibility, and simplified content creation without requiring software installation. Users can access AI-generated video tools directly through browsers, enabling seamless collaboration, editing, and publishing from any location. Businesses increasingly favor web platforms for their scalability, centralized updates, and lower infrastructure requirements. These platforms also support integration with cloud services, social media channels, and digital marketing ecosystems, improving workflow efficiency. The rising popularity of subscription-based SaaS models has further accelerated adoption among enterprises, agencies, educators, and independent creators. Additionally, web-based solutions allow providers to deploy advanced AI features, such as avatar generation, voice cloning, and automated editing, more efficiently. Their convenience and cost-effectiveness continue to drive widespread global market dominance.

By Enterprise Size Analysis

The enterprise size is projected to be dominated by large enterprises with regards to AI generated video content, considering the scale and complexity of their brand portfolio and global marketing footprints. They have big media budgets and huge product visuals libraries which need localized versions for dozens of foreign markets, and for which painstaking creative resizing is necessary. While small content creators can quickly embrace generic AI avatars, large businesses are dealing with thorough brand safety screening and rigorous corporate identity policies. Their AI journeys involve complete professional services, from custom fine-tuning AI models using proprietary product images to complex API-Based Video Generation for automated localization and managed integration services to coordinate simultaneous asset management across global teams.

By Technology Analysis

The Diffusion Models segment is poised to dominate the technology landscape, as it represents the fundamental architectural breakthrough that has unlocked photorealistic, coherent video generation. Unlike older GANs that struggled with temporal consistency and mode collapse, diffusion-based transformers methodically denoise video patches, resulting in smoother motion and lighting. Large enterprises rely on diffusion backbones for product demonstration videos, where textile textures, reflections, and fluid dynamics must appear perfectly authentic. In addition, the industry is subject to a highly dynamic model release cycle. AI departments require cloud providers and service partners that design solutions striking a balance between pursuing bleeding-edge model weights and maintaining the stable, deterministic outputs required for reproducible corporate communications.

By Application Analysis

Social Media Content Creation and Marketing & Advertising are poised to command the market with the highest share in this segment as the ecosystem undergoes a radical transformation driven by algorithmic demand for fresh, short-form video. Brands are creating AI assets at a lightning quick rate in order to participate in TikTok trends in real-time, AI-Generated UGC Videos that are as sophisticated as authentic customer videos, and more robust always-on video calendars. Also, the synthetic media labelling policies of social networks are very dynamic. Marketing companies need AI video platforms that can create solutions that balance viral content velocity with adherence to different social oversight agency platform disclosure requirements around the world.

By End User Analysis

The Media & Entertainment industry is the top end-user, which has an existential need to scale visual effects production and dubbing without a proportional increase in budget. AIs are being used in studios to generate anime content, pre-visualize intricate scenes, and substitute for expensive second shoots. This vertical requires the most amount of photorealism and the most amount of narrative control through the use of Neural Rendering. But the biggest growth is in end-user sector Retail & E-Commerce. Online retailers need more than just filmic quality here, they need speed and volume, with API based tools for turning static product catalog images into dynamic automated product demonstration videos and AI generated UGC “unboxing” experiences directly influencing conversion rates.

The Global AI-Generated Video Content Market Report is segmented on the basis of the following:

By Component

- Software Platforms

- AI Models & Engines

- Services

By Content Type

- Text-to-Video

- Image-to-Video

- Avatar-Based Videos

- Animation & Visual Effects

- AI-Generated UGC Videos

- Deepfake & Synthetic Media

- Live AI Video Streams

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By Platform Type

- Web-Based Platforms

- Mobile Applications

- Studio & Editing Software

- API-Based Video Generation Tools

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Technology

- Generative Adversarial Networks (GANs)

- Diffusion Models

- Transformer Models

- Large Language Models (LLMs)

- Neural Rendering

- Computer Vision

- Speech Synthesis & Voice Cloning

By Application

- Marketing & Advertising

- Social Media Content Creation

- Entertainment & Media Production

- E-Learning & Training

- Gaming & Virtual Worlds

- Corporate Communications

- News & Journalism

- Product Demonstrations

- Customer Engagement

- Other Application

By End User

- Media & Entertainment

- Retail & E-Commerce

- Education

- Healthcare

- BFSI

- IT & Telecommunications

- Gaming Industry

- Advertising Agencies

- Influencers & Content Creators

- Other End Users

Regional Analysis

Leading Region by Market Share

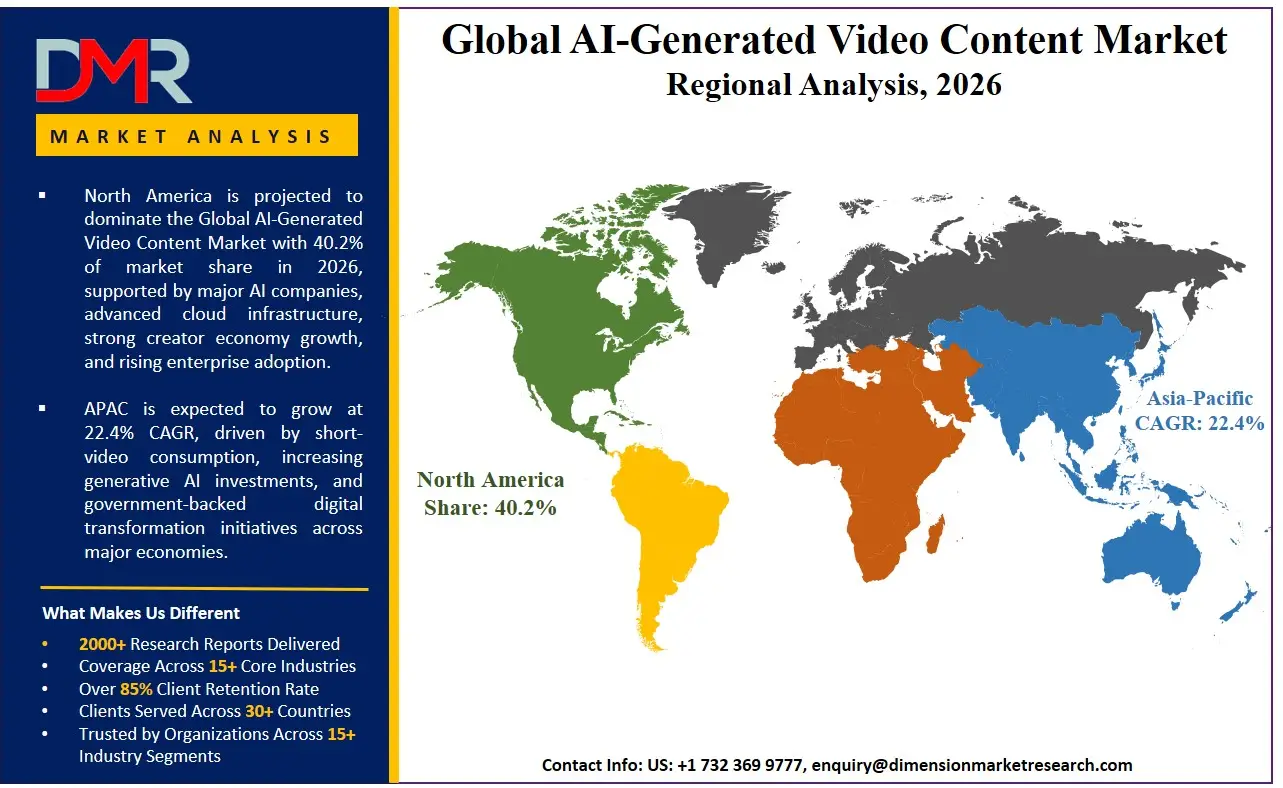

North America is poised to dominate the global AI-generated video content market as it is projected to hold 40.2% of the market share by the end of 2026. The U.S., which dominates North America, has the biggest share in the market due to an unmatched density of generative AI research labs, venture capital for AI startups in media and advertising, and Hollywood studios and Madison Avenue agencies' aggressive digital transformation programs. There are already a number of platform providers on a global level, specialized artists putting the diffusion models to work, and a wealth of talent in prompt engineering and video data curation. The increasing demand for Personalized Commerce, Advanced Virtual Production and overall reduction of production overhead is driving enterprise investment in the platform of Image-to-Video and Avatar-Based Video, as well as continuous model fine tuning Services. Furthermore, the highly competitive social media environment constantly funds new creator tools that require professional services to become viral and compliant with content safety standards.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

The Asia-Pacific region is projected to see the fastest growth in the AI video content generation market, primarily owing to the government-initiated widespread AI programs and a significant mobile-first video consumption in the region, encompassing India, China, Japan, and Southeast Asia. Rapidly expanding live commerce, a new middle class of creators and the vibrant growth of the gaming and virtual idol industry are driving media giants and e-commerce providers to abandon inefficient manual video pipelines. Avatar-Based Video and Live AI Video Stream consulting is in high demand to help these large platforms head in the direction of interactive, AI-native live selling. Additionally, there is a significant shortage of AI model trainers who are also fluent in the region's linguistic and cultural styles and nuances, and the need to hire professional fine-tuning services for diffusion models and speech synthesis to address the skills gap and expedite video content localization projects.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The global competitive landscape of AI-generated video content is dynamic and diverse, featuring a wide range of well-funded AI research institutes, divisions within the large hyperscalers dedicated to generative media, and niche generative media startups. The key to success will be the profound strategic alliances with diffusion model pioneers and open-source communities like Stability AI or dedicated video architectures because they will open the necessary early access to the new model checkpoints and capabilities. In the drive for market consolidation, traditional creative software behemoths such as Adobe have been buying up AI video generation and neural rendering startups to keep their heads above water. Proprietary intellectual property such as digital twin datasets exclusively licensed to the specific company, custom fine-tuned diffusion model weights for specific ethnic groups, and industry-specific content guardrails, are increasingly the ground for differentiation, not generic generation interfaces or just API wrappers.

Some of the prominent players in the Global AI-Generated Video Content Market are:

- Synthesia

- Runway

- Pika Labs

- HeyGen

- OpenAI (Sora)

- Google DeepMind (Veo)

- Meta AI

- Adobe

- D-ID

- DeepBrain AI

- Hour One

- Colossyan

- Elai.io

- Tavus

- Rephrase.ai

- Other Key Players

Recent Developments

- January 2026: A major expansion of Runway's Gen-4 Professional Services division, which provides support to Media & Entertainment and Advertising Agency clients in building their own custom Diffusion Models using the company's API-Based Video Generation Tools, was announced in January 2026, and includes emphasis on maintaining character consistency in long-form narratives.

- November 2025: Synthesia expands its enterprise capabilities and launches a targeted practice, "Ethical Digital Twin Consulting and Voice Cloning Integration", helping BFSI clients transition to custom Avatar-Based Videos on a secure cloud, while adhering to global financial promotion regulations.

- October 2025: Adobe acquired a European provenance technology enterprise to further its "Content Authenticity" Cloud Strategy and API-Based Video Generation solutions, to support the complicated requirements of News & Journalism and Government end-users in labeling and tracing AI-Generated Video Content from creation to consumption.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 943.9 Mn |

| Forecast Value (2035) |

USD 4,579.6 Mn |

| CAGR (2026–2035) |

19.2% |

| The US Market Size (2026) |

USD 319.1 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Content Type, By Deployment Mode, By Platform Type, By Enterprise Size, By Technology, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global AI-Generated Video Content Market?

▾ The Global AI-Generated Video Content market is poised to be valued at USD 943.9 million in 2026 and is projected to reach USD 4,579.6 million by 2035, driven by the universal need for scalable, cost-efficient video production and hyper-personalization at scale.

What is the CAGR of the Global AI-Generated Video Content Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 19.2% from 2026 to 2035, reflecting the accelerating sophistication of Diffusion Models and Transformer Models and the persistent shortage of traditional video production bandwidth.

What factors are driving the growth of the Global AI-Generated Video Content Market?

▾ Key drivers include the insatiable consumer demand for video content, the need to produce thousands of localized ad variations instantly, the rise of digital avatars for cost-effective corporate communications, and the surging demand for ethical synthetic media Services amid evolving global deepfake regulations.

Which region held the largest share of the AI-Generated Video Content Market in 2026?

▾ North America is poised to dominate this market with 40.2% of the market share in 2026, driven by a mature AI research ecosystem and aggressive enterprise investment in Marketing & Advertising and AI-driven visual effects for the entertainment industry.

Which region is expected to grow the fastest in the AI-Generated Video Content Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by mobile-first social commerce booms in India and China, where Live AI Video Streams and Avatar-Based Videos are critical for transitioning massive retail audiences to interactive, AI-driven shopping experiences.

What are the major trends in the Global AI-Generated Video Content Market?

▾ Major trends include the integration of LLMs into video scripting workflows, the rise of real-time 3D neural avatars for live streaming, the demand for watermarked and provably authentic content, and the focus on mobile-first AI-Generated UGC Videos that mimic authentic user content.

Who are the key players in the Global AI-Generated Video Content Market?

▾ Key players include AI-native platform providers like Synthesia, Runway, and Pika Labs, as well as the generative AI research divisions of hyperscalers like OpenAI (Sora) and Google DeepMind (Veo), alongside legacy creative software giants like Adobe and specialized avatar-focused startups like HeyGen and D-ID.

How is the Global AI-Generated Video Content Market segmented?

▾ The market is segmented by Component By Content Type, By Deployment Mode, By Platform Type, By Enterprise Size, By Technology, By Application, and By End User.