What is the AI Security Operations Center (SOC) Platforms Market Size?

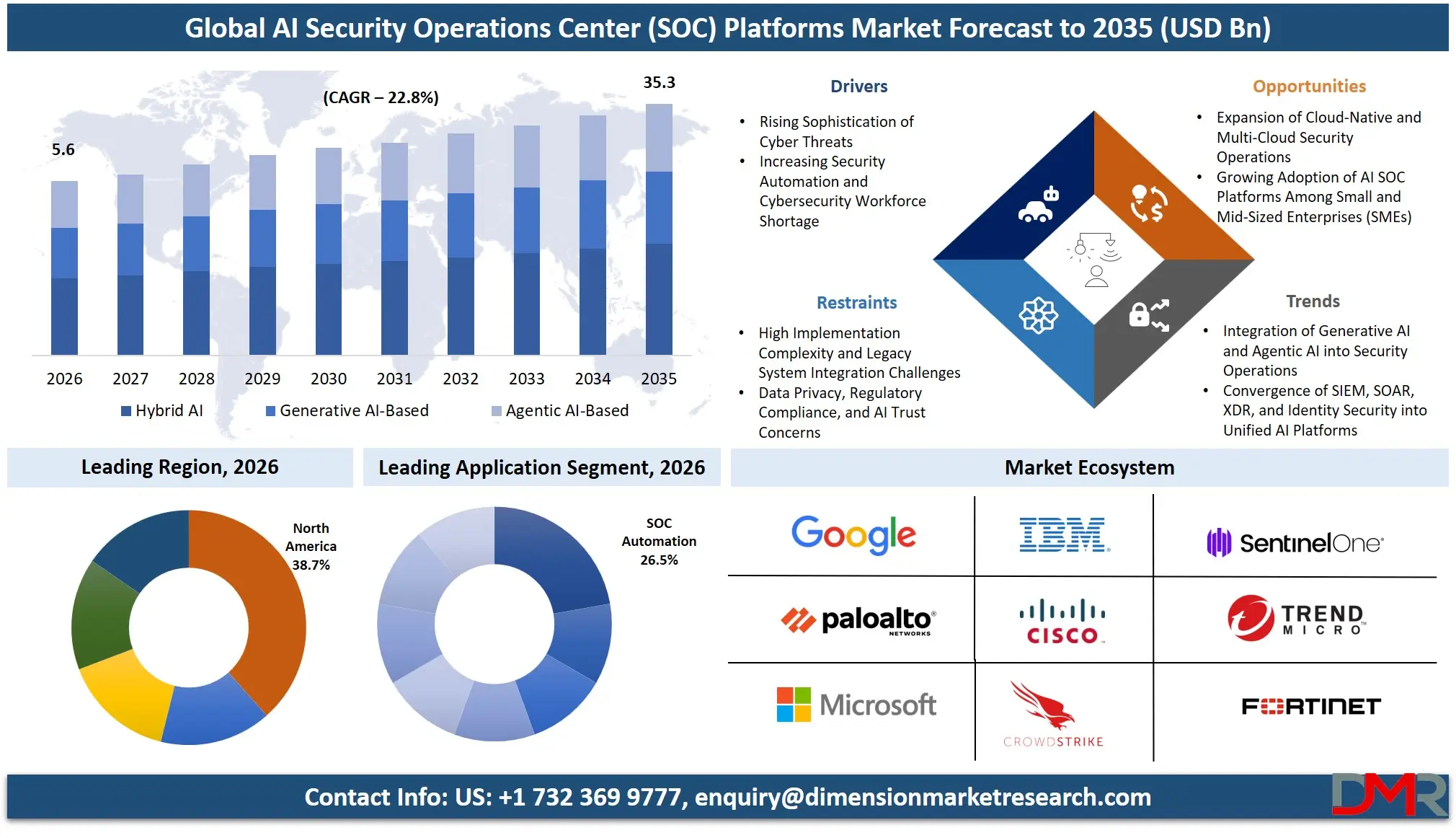

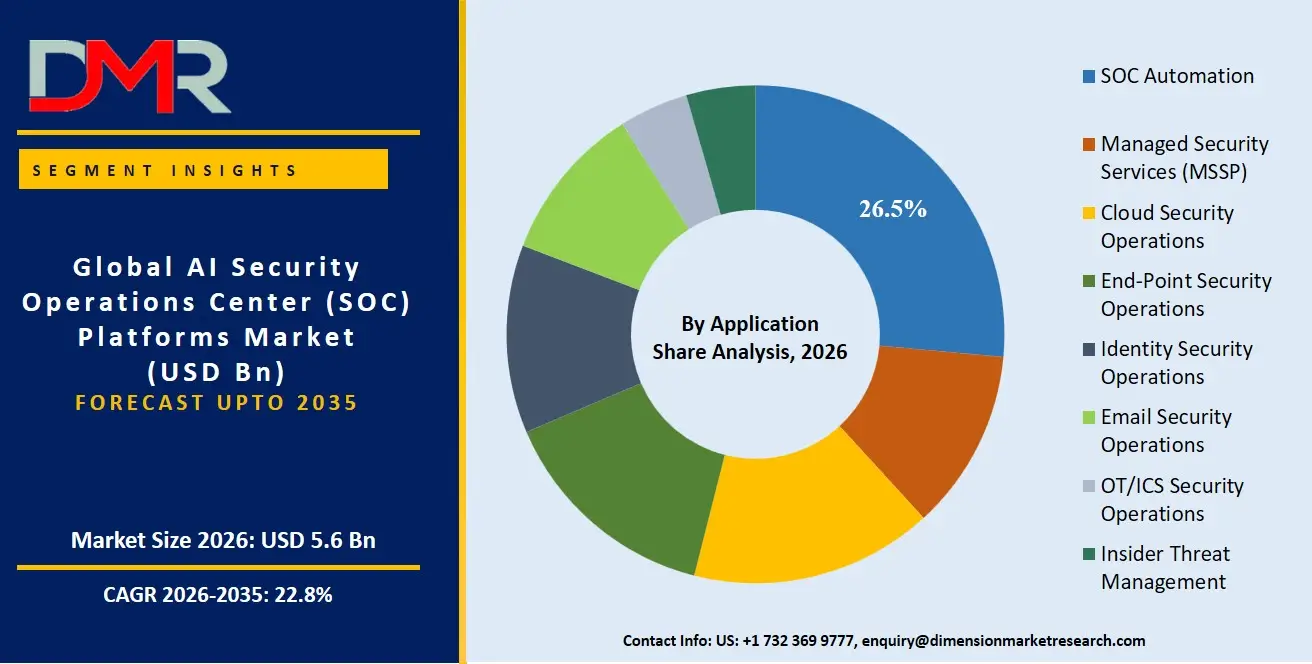

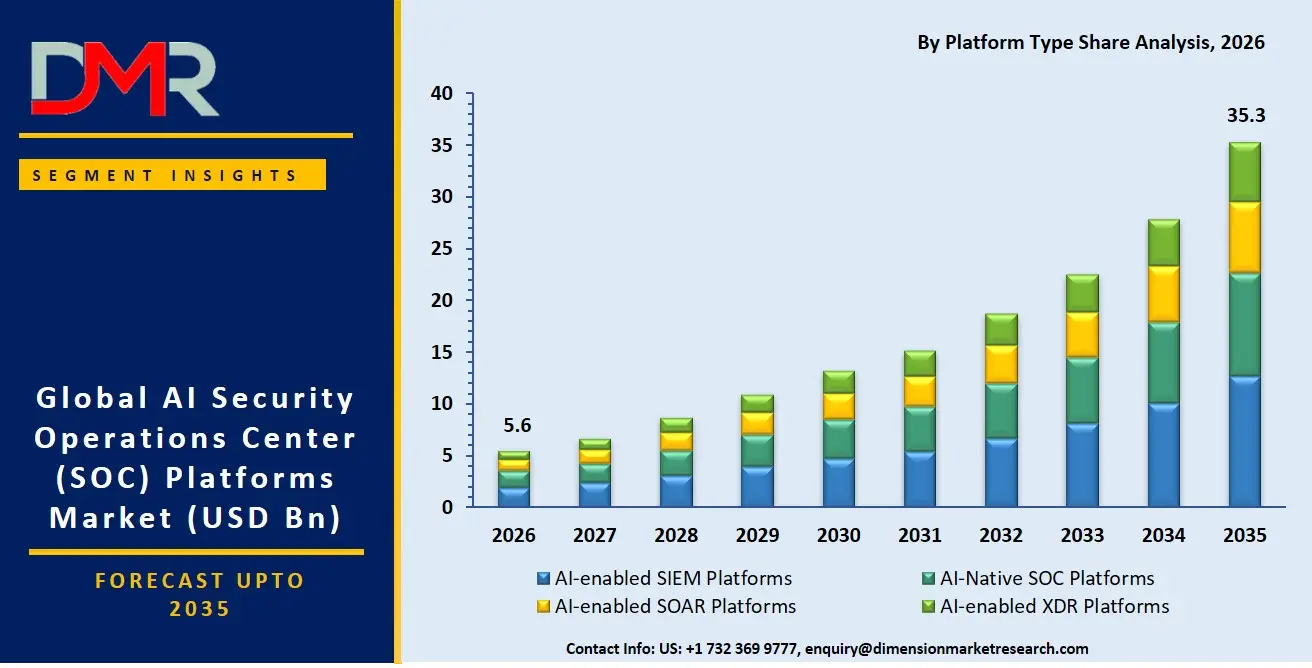

The Global AI Security Operations Center (SOC) Platforms Market is expected to reach a value of USD 5.6 billion in 2026, and it is further anticipated to reach USD 35.3 billion by 2035, growing at a CAGR of 22.8% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The AI SOC platforms market is experiencing exponential growth as security teams grapple with an unrelenting surge in alert volumes and sophisticated, AI-generated cyberattacks. Enterprises are rapidly transitioning from legacy, rules-based security information and event management (SIEM) to AI-native and AI-enabled platforms that can automate threat detection, investigation, and response at machine speed. The market encompasses solutions that embed machine learning, generative AI, and agentic AI directly into SOC workflows, including autonomous triage, predictive threat hunting, and adaptive orchestration. The increasing complexity of hybrid and multi-cloud environments, the proliferation of identity-based threats, and a critical global shortage of human security analysts are driving the urgent need for autonomous and agentic AI SOC platforms that can reason, decide, and act with minimal human intervention.

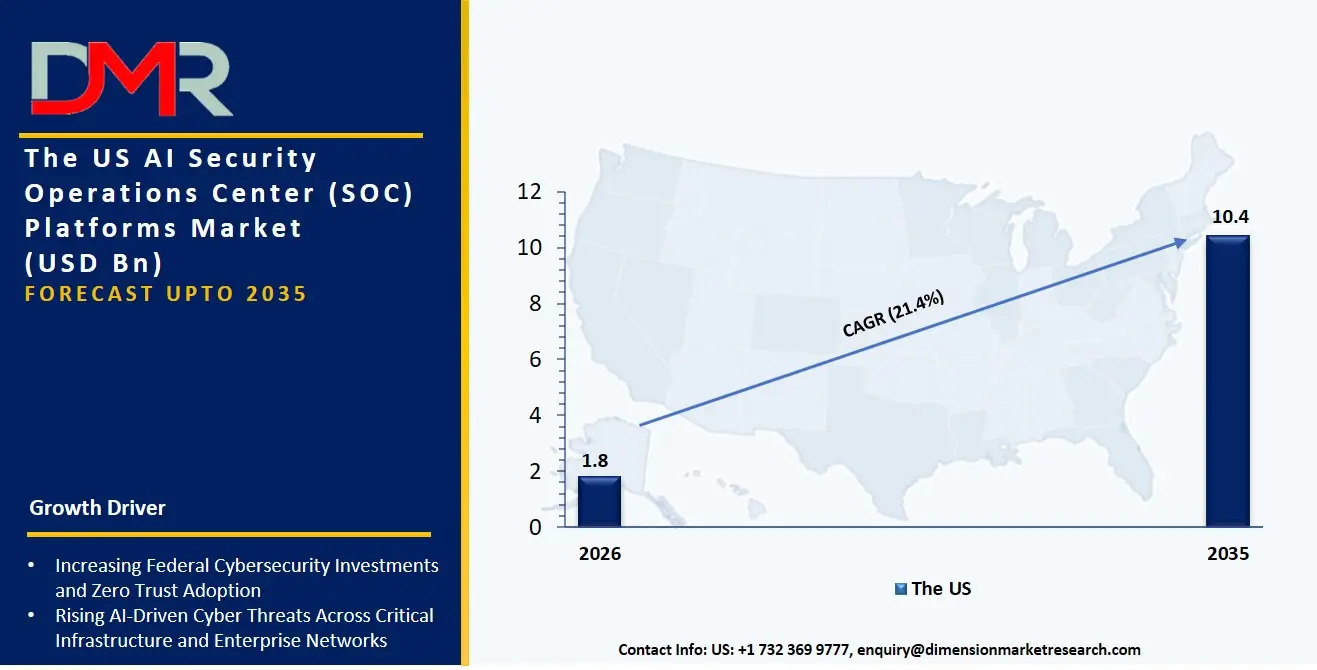

The US AI Security Operations Center (SOC) Platforms Market

The US AI SOC Platforms Market is projected to reach USD 1.8 billion in 2026 at a compound annual growth rate of 21.4% over its forecast period, culminating in a value of USD 10.4 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US remains the epicenter of innovation and adoption in the AI SOC market, driven by the advanced cyber threat landscape facing Fortune 500 companies and the rapid modernization of critical national infrastructure defense. The market is characterized by high demand for AI-native SOC platforms that replace, rather than augment, traditional SIEMs, enabling autonomous security operations. Furthermore, the deployment of Generative AI-based co-pilots for automating threat hunting reports and incident response playbooks is creating a parallel surge in demand for agentic AI-based architectures that can execute complex, multi-step containment actions across sprawling cloud-native environments without analyst approval for every step.

The Europe AI Security Operations Center (SOC) Platforms Market

The Europe AI SOC Platforms Market is estimated to be valued at USD 1.6 billion in 2026 and is further anticipated to reach USD 9.8 billion by 2035 at a CAGR of 22.2%. The European market is profoundly shaped by stringent data protection and digital operational resilience regulations, including GDPR and DORA, which mandate robust risk management and incident reporting frameworks. This regulatory pressure is driving demand for AI-enabled SIEM and SOAR platforms with built-in compliance reporting and privacy-preserving machine learning models. Accelerated growth is also seen in managed security services (MSSP) applications, as mid-sized enterprises seek to outsource the operation of complex AI SOC platforms. Additionally, sovereignty-focused initiatives are compelling service providers to offer dedicated deployment options that ensure threat intelligence and response data remain within European borders, fueling the adoption of hybrid and on-premises models for critical sectors like energy and government.

The Japan AI Security Operations Center (SOC) Platforms Market

The Japan AI SOC Platforms Market is projected to be valued at USD 543.4 million in 2026 at a CAGR of 21.8%. The Japanese market is uniquely propelled by a national imperative to secure digital transformation (DX) initiatives and critical manufacturing and OT/ICS environments against rising state-sponsored threats. As large conglomerates modernize their IT-OT convergence strategies, there is significant spending on AI-enabled XDR platforms and OT/ICS security operations applications. A strong demand exists for hybrid AI architectures that can correlate threats across on-premise factory floors and cloud-based enterprise systems. The acute domestic shortage of cybersecurity professionals necessitates a focus on Agentic AI capabilities that can autonomously manage Level 1 and Level 2 SOC analysis, a niche being rapidly filled by global and local platform providers through deep, localized managed service partnerships.

Key Takeaways

- Market Size & Forecast: The Global AI SOC Platforms market is projected to reach USD 5.6 billion in 2026, expanding dramatically to USD 35.3 billion by 2035, fueled by the dual drivers of an untenable alert-to-analyst ratio and the emergence of autonomous, AI-generated adversarial attacks that require machine-speed defense.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 22.8%, driven by the shift from reactive, rules-based security to proactive, predictive defense. The evolution from AI-assisted investigation to fully autonomous SOCs, powered by agentic AI, is the central axis of this hypergrowth.

- Primary Growth Drivers: Key forces include a critical global cybersecurity skills gap of millions of unfilled positions, the escalating sophistication of ransomware and supply chain attacks, and the impossibility of securing ephemeral cloud-native architectures with manual processes, which demands AI-native SOC platforms.

- Key Market Trends: Major trends include the transition from co-pilots to fully autonomous AI agents capable of executing containment and remediation, the convergence of XDR, SIEM, and SOAR capabilities into unified AI-native platforms, and the rise of vertical-specific AI SOC solutions for BFSI, healthcare, and critical infrastructure compliance.

- By Deployment Mode Analysis: Cloud-Based models are expected to lead due to their ability to ingest hyperscale telemetry. However, Hybrid deployments are critically important for securing OT/ICS environments and for organizations navigating strict data residency requirements in sectors like Government & Defense and BFSI.

- By End-Use Industry Analysis: Banking, Financial Services & Insurance (BFSI) and Government & Defense are the most lucrative verticals due to their zero-tolerance for breaches. Healthcare & Life Sciences is the fastest-growing sector as the weaponization of medical IoT devices and patient data requires specialized AI-enabled security operations for life-critical systems.

- Regional Leadership: North America is poised to dominate this market with 38.7% of the market share in 2026, driven by its high concentration of hyperscale cloud providers, AI-first security startups, and a maturing venture capital ecosystem that aggressively funds the next generation of autonomous security platforms.

What is the AI Security Operations Center (SOC) Platforms?

AI SOC Platforms are advanced software solutions that fundamentally transform cybersecurity operations by embedding artificial intelligence into the core of threat detection, investigation, and response. Unlike first-generation security tools that merely generate alerts, these platforms consume and fuse vast telemetry across endpoint, network, cloud, identity, and email layers to create a single, intelligent data fabric. They go beyond correlation to provide autonomous reasoning and action. This involves an AI-enabled SIEM that uses machine learning for anomaly detection, a SOAR platform that dynamically generates response playbooks, or, most radically, an AI-native SOC platform that rearchitects the entire analyst workflow around an autonomous AI brain. With over 50% of SOC alerts going uninvestigated due to volume, these platforms are necessary to move from a state of perpetual alert fatigue to proactive risk reduction, making security outcomes a direct function of AI capability rather than human headcount.

Use Cases

- Autonomous Phishing Remediation in BFSI: Financial institutions deploy AI-enabled SOAR platforms with agentic AI capabilities to go beyond deleting reported phishing emails. The AI agent autonomously traces all internal propagation of the malicious email, automatically isolates compromised mailboxes, blocks related IOCs network-wide, and generates a complete timeline report for regulatory audit, all in seconds.

- Ransomware Defense in Healthcare: Hospital networks use AI-native SOC platforms to protect life-critical medical devices. The AI model identifies subtle precursors to ransomware, such as anomalous data staging or credential misuse patterns invisible to rules, and autonomously shuts down specific switch ports to isolate an infected infusion pump without disrupting other clinical systems.

- OT/ICS Anomaly Detection in Manufacturing: A global manufacturer employs an AI-enabled XDR platform to monitor its converged IT-OT environment. The platform's Hybrid AI architecture correlates an unusual engineering workstation login from the IT side with a micro-stop event on a packaging line on the OT side, identifying a potential insider threat or compromised operational technology channel that manual monitoring would never connect.

- Threat Hunting in Government & Defense: National cyber defense agencies leverage Generative AI-based platforms to revolutionize threat hunting. Analysts query the data lake using natural language, and the AI generates and iteratively tests complex hunting hypotheses across petabytes of intelligence data, returning a visualized graph of a previously unknown nation-state adversary's lateral movement path in minutes instead of weeks.

Market Dynamics

Key Drivers in the Global AI Security Operations Center (SOC) Platforms Market

Rising Sophistication of Cyber Threats

The rapid evolution of ransomware, advanced persistent threats (APTs), phishing campaigns, and AI-powered cyberattacks is significantly driving demand for AI Security Operations Center (SOC) platforms. Traditional security tools struggle to process the enormous volume of security telemetry generated across cloud, endpoints, identities, and networks, creating gaps in threat detection. AI-powered SOC platforms use machine learning, behavioral analytics, and predictive intelligence to identify anomalies, correlate events, and prioritize high-risk alerts in real time. This enables organizations to detect sophisticated attacks earlier, reduce false positives, and improve response accuracy. As cybercriminals increasingly leverage automation and artificial intelligence, enterprises are investing in intelligent SOC platforms to strengthen cyber resilience and maintain continuous security operations.

Increasing Security Automation and Workforce Shortage

Organizations worldwide continue to face an acute shortage of skilled cybersecurity professionals while simultaneously managing rapidly expanding attack surfaces. AI SOC platforms address this challenge by automating repetitive security tasks including alert triage, incident classification, threat enrichment, forensic analysis, and response orchestration. Automation significantly reduces analyst fatigue, accelerates investigation timelines, and improves operational consistency without requiring proportional increases in staffing. Enterprises also benefit from faster Mean Time to Detect (MTTD) and Mean Time to Respond (MTTR), improving overall security posture. As digital transformation expands enterprise IT environments, AI-driven automation has become essential for maintaining efficient, scalable, and cost-effective security operations, making it a major driver of market growth.

Restraints in the Global AI Security Operations Center (SOC) Platforms Market

High Implementation Complexity and Integration Challenges

Deploying AI-powered SOC platforms often requires integration with numerous existing cybersecurity solutions, including SIEM, XDR, SOAR, identity management, endpoint protection, and cloud security platforms. Many organizations operate heterogeneous IT environments containing legacy systems that lack interoperability with modern AI technologies. Integration complexities increase deployment timelines, implementation costs, and operational disruptions while requiring specialized expertise for configuration and optimization. Data normalization across multiple security tools further complicates AI model performance. Small and medium-sized enterprises frequently lack the financial and technical resources required for comprehensive deployment, slowing adoption despite growing cybersecurity needs. These implementation barriers remain a significant restraint for broader market expansion.

Data Privacy, Regulatory Compliance, and AI Trust Issues

AI SOC platforms process enormous volumes of sensitive operational, user, and security data, creating concerns regarding data privacy, regulatory compliance, and AI transparency. Organizations operating across multiple jurisdictions must comply with evolving cybersecurity and data protection regulations while ensuring secure handling of confidential information. Many enterprises remain cautious about AI-generated recommendations because explainability and model transparency are critical during incident investigations and compliance audits. False positives, biased algorithms, and inaccurate automated decisions can undermine trust among security analysts. These governance challenges require additional oversight, validation mechanisms, and human intervention, increasing operational complexity and slowing adoption of highly autonomous AI security operations.

Growth Opportunities in the Global AI Security Operations Center (SOC) Platforms Market

Expansion of Cloud-Native and Multi-Cloud Security Operations

The rapid adoption of cloud computing, hybrid infrastructure, and multi-cloud environments presents substantial growth opportunities for AI SOC platform providers. Organizations increasingly require unified visibility across public cloud platforms, private clouds, SaaS applications, and distributed endpoints. AI-powered SOC solutions capable of continuously monitoring cloud workloads, detecting anomalous behaviors, and automating cloud-specific incident response are becoming essential. Vendors are developing cloud-native architectures with scalable analytics, API-driven integrations, and centralized management capabilities that simplify security operations across diverse environments. As enterprises continue migrating mission-critical workloads to the cloud, demand for intelligent cloud-focused SOC platforms is expected to accelerate significantly over the coming years.

Growing Adoption Among Mid-Sized Enterprises

Historically, AI-powered SOC platforms were primarily adopted by large enterprises due to high implementation costs and infrastructure requirements. However, cloud-based delivery models, subscription pricing, and managed AI security services are making advanced SOC capabilities increasingly accessible to mid-sized organizations. These businesses face cyber threats comparable to large enterprises but often lack dedicated security teams and sophisticated security infrastructure. AI-powered automation enables them to strengthen cybersecurity while minimizing operational complexity and staffing requirements. Vendors offering scalable, modular, and affordable AI SOC solutions tailored for mid-market organizations have significant opportunities to expand their customer base and drive long-term market growth.

Trends in the Global AI Security Operations Center (SOC) Platforms Market

Integration of Generative AI and Agentic AI into SOC Operations

A major trend transforming the AI SOC Platforms Market is the integration of Generative AI and Agentic AI into everyday security operations. Generative AI assists analysts by summarizing incidents, generating investigation reports, explaining attack patterns, and accelerating threat hunting through natural language interaction. Agentic AI extends these capabilities by autonomously executing predefined workflows, coordinating multiple security tools, and recommending or initiating response actions with minimal analyst intervention. This combination significantly improves operational efficiency while reducing response times and analyst workload. Vendors continue investing heavily in AI copilots and autonomous security assistants, making advanced AI capabilities a defining feature of next-generation SOC platforms.

Convergence of SIEM, SOAR, XDR, and Identity Security Platforms

The market is witnessing a strong trend toward unified security operations platforms that integrate SIEM, SOAR, XDR, threat intelligence, identity security, and cloud security into a single AI-driven ecosystem. Organizations increasingly seek centralized platforms capable of correlating data from multiple security domains while eliminating operational silos. Unified platforms provide comprehensive visibility, simplified management, automated workflows, and improved incident response across increasingly complex digital environments. AI enhances these integrated ecosystems by identifying relationships between disparate security events and prioritizing the most critical threats. This platform consolidation trend is reshaping cybersecurity strategies as enterprises pursue more efficient, intelligent, and scalable security operations.

Research Scope and Analysis

The Global AI Security Operations Center (SOC) Platforms Market is segmented by platform type into AI-enabled SIEM, AI-Native SOC, AI-enabled SOAR, and AI-enabled XDR platforms. Based on AI architecture, it includes Hybrid AI, Generative AI, and Agentic AI. The market is further categorized by AI capability, deployment mode, application, and end-use industries, including BFSI, IT, government, healthcare, manufacturing, retail, energy, education, media, critical infrastructure, and others.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Platform Type Analysis

AI-enabled SIEM Platforms is projected to dominate the Global AI Security Operations Center (SOC) Platforms Market because they serve as the foundational technology for collecting, correlating, and analyzing security events across enterprise IT environments. Organizations increasingly integrate artificial intelligence into SIEM solutions to automate alert prioritization, reduce false positives, and accelerate incident investigations while leveraging existing security infrastructure.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Their widespread deployment across regulated industries such as BFSI, healthcare, government, and telecommunications reinforce their market leadership. Modern AI-enabled SIEM platforms also integrate seamlessly with XDR, SOAR, cloud security, and threat intelligence solutions, creating centralized visibility and operational efficiency. Continuous advancements in behavioral analytics, predictive threat detection, and automated compliance reporting further strengthen their adoption, making AI-enabled SIEM Platforms the largest and most established segment.

By AI Architecture Analysis

Hybrid AI is the is anticipated to dominate AI architecture because it combines the strengths of generative AI with deterministic machine learning models and rule-based analytics, enabling more accurate, explainable, and reliable security operations. Security teams increasingly require architectures capable of balancing automation with governance, minimizing hallucinations while improving threat detection and investigation. Hybrid AI supports multiple SOC functions including anomaly detection, malware classification, threat hunting, incident summarization, and response recommendations within a unified platform. Enterprises prefer this approach because it integrates seamlessly with existing cybersecurity tools while maintaining compliance and auditability. As organizations adopt AI gradually, Hybrid AI provides flexibility to incorporate emerging AI capabilities without replacing established security workflows, ensuring broad adoption across industries.

By AI Capability Analysis

AI Assisted solutions is poised to represent the dominant capability segment because enterprises continue to prioritize human-in-the-loop security operations over fully autonomous decision-making. AI-assisted platforms enhance analyst productivity by automating repetitive tasks such as alert triage, threat correlation, log analysis, and incident summarization while allowing experienced security professionals to validate critical decisions. This approach improves operational efficiency without introducing unacceptable risks associated with autonomous response systems. Regulatory requirements, governance concerns, and organizational trust also encourage gradual AI adoption rather than complete automation. Most organizations view AI as a force multiplier for existing SOC teams instead of a replacement, making AI Assisted platforms the preferred deployment model across both public and private sectors.

By Deployment Mode Analysis

Cloud-Based deployment is expected to dominate the market because organizations increasingly require scalable, continuously updated, and globally accessible security operations platforms. Cloud-native SOC solutions support remote workforces, multi-cloud infrastructures, hybrid IT environments, and distributed enterprise operations without requiring extensive on-premises infrastructure investments. Vendors deliver AI model updates, threat intelligence feeds, and security enhancements in real time, enabling customers to respond quickly to evolving cyber threats. Cloud deployments also reduce implementation complexity while offering subscription-based pricing that lowers capital expenditure. Their ability to integrate with SaaS applications, cloud workloads, and modern security ecosystems further accelerates adoption, making cloud-based platforms the preferred choice for enterprises of all sizes.

By Application Analysis

SOC Automation is projected to be the leading application segment because organizations face growing cybersecurity workloads alongside persistent shortages of skilled security professionals. AI-powered automation significantly improves operational efficiency by handling repetitive activities such as alert triage, log correlation, threat enrichment, incident prioritization, ticket generation, and response orchestration. Automated workflows reduce mean time to detect (MTTD) and mean time to respond (MTTR), enabling security teams to focus on high-priority threats and strategic investigations. Enterprises also benefit from standardized response procedures, improved consistency, and reduced operational costs. As cyberattacks become more sophisticated and security data volumes continue to expand, SOC automation remains the most valuable and widely adopted AI-driven application.

By End-Use Industry Analysis

The BFSI sector is anticipated to dominate the Global AI Security Operations Center (SOC) Platforms Market due to its exposure to sophisticated cyber threats, stringent regulatory requirements, and extensive handling of sensitive financial and customer information. Banks, insurers, payment providers, and financial institutions invest heavily in AI-driven SOC platforms to detect fraud, prevent ransomware attacks, secure digital banking channels, and maintain regulatory compliance. The industry's large-scale adoption of cloud computing, digital payments, open banking, and real-time financial services has significantly increased cybersecurity complexity, driving demand for intelligent security operations. Continuous monitoring, rapid incident response, behavioral analytics, and automated compliance capabilities make AI-powered SOC platforms an essential component of modern cybersecurity strategies within the BFSI sector.

The Global AI Security Operations Center (SOC) Platforms Market Report is segmented on the basis of the following:

By Platform Type

- AI-enabled SIEM Platforms

- AI-Native SOC Platforms

- AI-enabled SOAR Platforms

- AI-enabled XDR Platforms

By AI Architecture

- Hybrid AI

- Generative AI-Based

- Agentic AI-Based

By AI Capability

- AI Assisted

- Agentic AI

- Autonomous AI

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By Application

- SOC Automation

- Managed Security Services (MSSP)

- Cloud Security Operations

- End-Point Security Operations

- Identity Security Operations

- Email Security Operations

- OT/ICS Security Operations

- Insider Threat Management

By End-Use Industry

- Banking, Financial Services & Insurance (BFSI)

- IT & Telecommunications

- Government & Defense

- Healthcare & Life Sciences

- Retail & E-Commerce

- Manufacturing

- Energy & Utilities

- Critical Infrastructure

- Media & Entertainment

- Education

- Other End Users

Regional Analysis

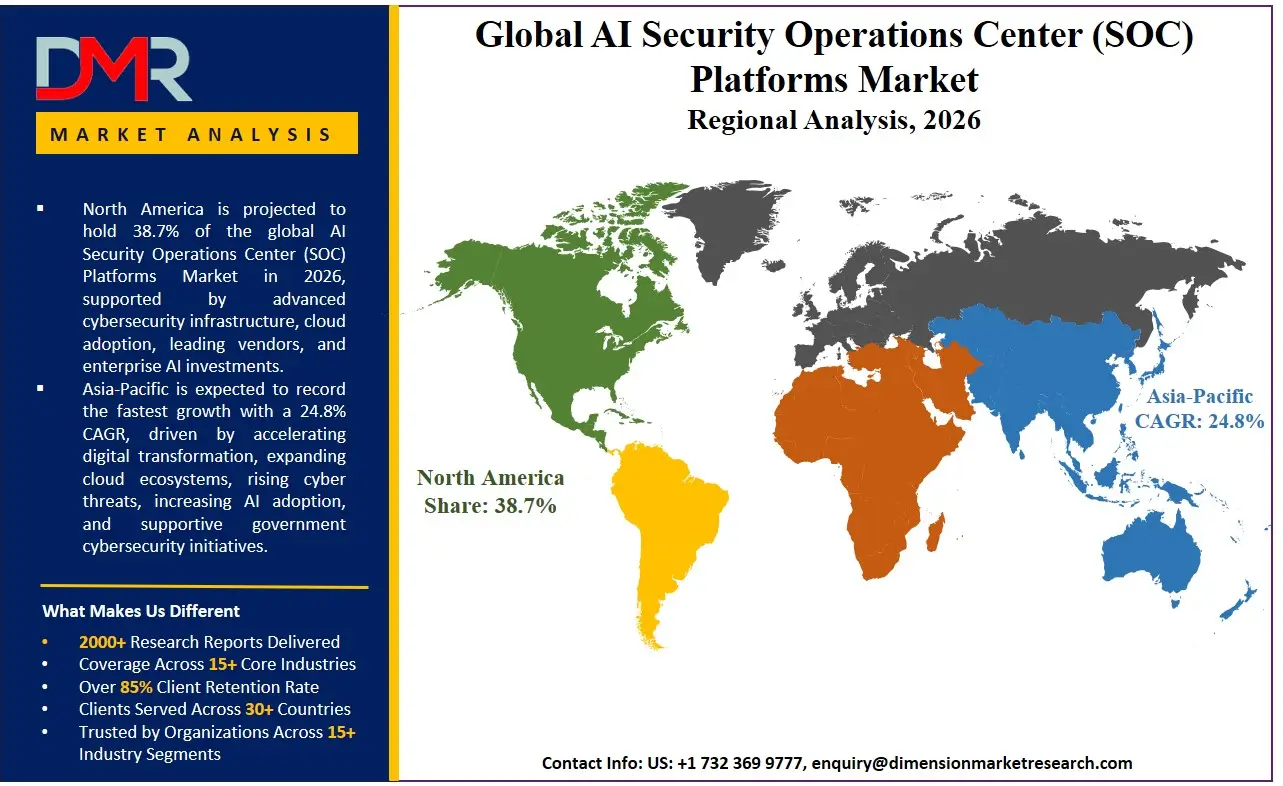

Leading Region by Market Share

North America is poised to dominate the global AI SOC platforms market, projecting to hold a 38.7% market share by the end of 2026. The United States, which anchors this regional dominance, is the epicenter for the development and adoption of next-generation cybersecurity platforms. This leadership is fueled by an unparalleled concentration of both the world's most targeted enterprises and the most innovative security platform vendors, from AI-native startups to established hyperscalers. The aggressive, AI-first modernization strategies of Fortune 500 companies, coupled with the extreme sophistication of the threat landscape, mandate the rapid deployment of autonomous AI SOC capabilities. The region's rich venture capital ecosystem consistently finances the bleeding edge of agentic and autonomous AI development, ensuring a continuous cycle of innovation that first matures in the US market before expanding globally.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding AI SOC platforms market, driven by a various factors like digitalization, a massive and escalating cybercrime landscape, and a severe scarcity of cybersecurity talent. Governments and massive conglomerates in India, China, Japan, and the ASEAN nations are rolling out sweeping digital transformation and smart city initiatives, which simultaneously create a vast, new attack surface that legacy security programs are unprepared to defend. An acute regional shortage of experienced threat hunters and SOC analysts makes the proposition of AI-assisted and agentic SOC platforms an operational necessity, not a luxury. The region is "leapfrogging" directly to AI-native architectures, bypassing heavy investments in traditional SIEM, making it a strategic battleground for both global and local platform providers offering managed security services.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the global AI SOC platforms market is a fierce three-way contest among established cybersecurity leaders pivoting to AI-native architectures, AI-native security platform startups, and the professional service divisions of hyperscale cloud providers. The primary competitive axis is no longer about feature lists but about AI efficacy and trust the platform that can demonstrate the highest-fidelity autonomous detection with the lowest false-positive rate and a transparent audit trail wins the account. Strategic partnerships are essential, with AI platform vendors embedding directly into cloud service provider marketplaces for seamless data ingestion and co-sell motions. Market consolidation is accelerating as legacy SIEM and SOAR vendors aggressively acquire AI-native and agentic AI startups to close critical technology gaps and prevent customer churn, recognizing that their future depends entirely on a credible autonomous AI roadmap.

Some of the prominent players in the Global AI Security Operations Center (SOC) Platforms Market are:

- Microsoft

- Google Cloud

- IBM

- Cisco Systems

- Palo Alto Networks

- CrowdStrike

- SentinelOne

- Fortinet

- Check Point Software Technologies

- Trend Micro

- Splunk

- Elastic

- Exabeam

- Securonix

- Rapid7

- Darktrace

- Arctic Wolf Networks

- Vectra AI

- Sophos

- ReliaQuest

- Other Key Players

Recent Developments

- January 2026: CrowdStrike announced a major new version of its Charlotte AI, moving beyond an AI-assisted co-pilot to an Agentic AI-based engine that can autonomously execute complex investigation and containment workflows across its Falcon XDR platform, specifically targeting identity security operations for BFSI clients.

- November 2025: Palo Alto Networks deepened its Cortex XSIAM (AI-native SOC Platform) capabilities by integrating a new Generative AI-based playbook generator. This module automatically creates and tests custom SOAR playbooks for novel threats observed in the wild, significantly reducing the defender's time to respond to zero-day vulnerabilities for its Managed Security Services (MSSP) partners.

- October 2025: Microsoft launched an autonomous threat hunting agent within its unified SecOps platform, a specific application of its Security Copilot. This agent uses a Hybrid AI architecture to proactively query customer security data lakes nightly, hunting for latent threats and generating actionable incident reports in natural language for compliance and audit functions in the Government & Defense sector.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 5.6 Bn |

| Forecast Value (2035) |

USD 35.3 Bn |

| CAGR (2026–2035) |

22.8% |

| The US Market Size (2026) |

USD 1.8 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Platform Type, By AI Architecture, By AI Capability, By Deployment Mode, By Application, and By End-Use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global AI SOC Platforms Market?

▾ The Global AI SOC Platforms market is poised to be valued at USD 5.6 billion in 2026 and is projected to reach USD 35.3 billion by 2035, driven by the universal need to automate cyber defense against an untenable volume of machine-speed attacks.

What is the CAGR of the Global AI SOC Platforms Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 22.8% from 2026 to 2035, reflecting the accelerating complexity and volume of enterprise threats and the persistent, global shortage of security operations analysts.

What factors are driving the growth of the Global AI SOC Platforms Market?

▾ Key drivers include the unbridgeable cybersecurity skills gap, the speed and sophistication of AI-powered adversarial attacks, the management complexity of hybrid cloud and OT/ICS environments, and the imperative to move from a reactive, human-dependent SOC to a proactive, autonomous one.

Which region held the largest share of the AI SOC Platforms Market in 2026?

▾ North America is projected to hold a 38.7% market share in 2026, driven by a mature venture capital ecosystem and aggressive enterprise investment in Agentic AI and autonomous SOC platforms to counter a highly sophisticated threat landscape.

Which region is expected to grow the fastest in the AI SOC Platforms Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by breakneck digitalization, a massive cybercrime surge, and an acute cybersecurity talent shortage, which compels organizations to leapfrog directly to AI-native SOC solutions.

What are the major trends in the Global AI SOC Platforms Market?

▾ Major trends include the definitive shift from AI-assisted tools to fully Autonomous AI SOCs, the convergence of SIEM, SOAR, and XDR into unified AI-native platforms, and the rise of preemptive security posture management powered by AI-driven digital twins.

Who are the key players in the Global AI SOC Platforms Market?

▾ Key players include platform leaders like Microsoft, Google Cloud, CrowdStrike, and Palo Alto Networks, alongside established SIEM/XDR vendors pivoting to AI such as Cisco (Splunk) and IBM, and AI-native security startups like SentinelOne and Darktrace.

How is the Global AI SOC Platforms Market segmented?

▾ The market is segmented by Platform Type, AI Architecture, AI Capability, Deployment Mode, Application, and End-Use Industry.