What is the AI Supercomputing Platform Market Size?

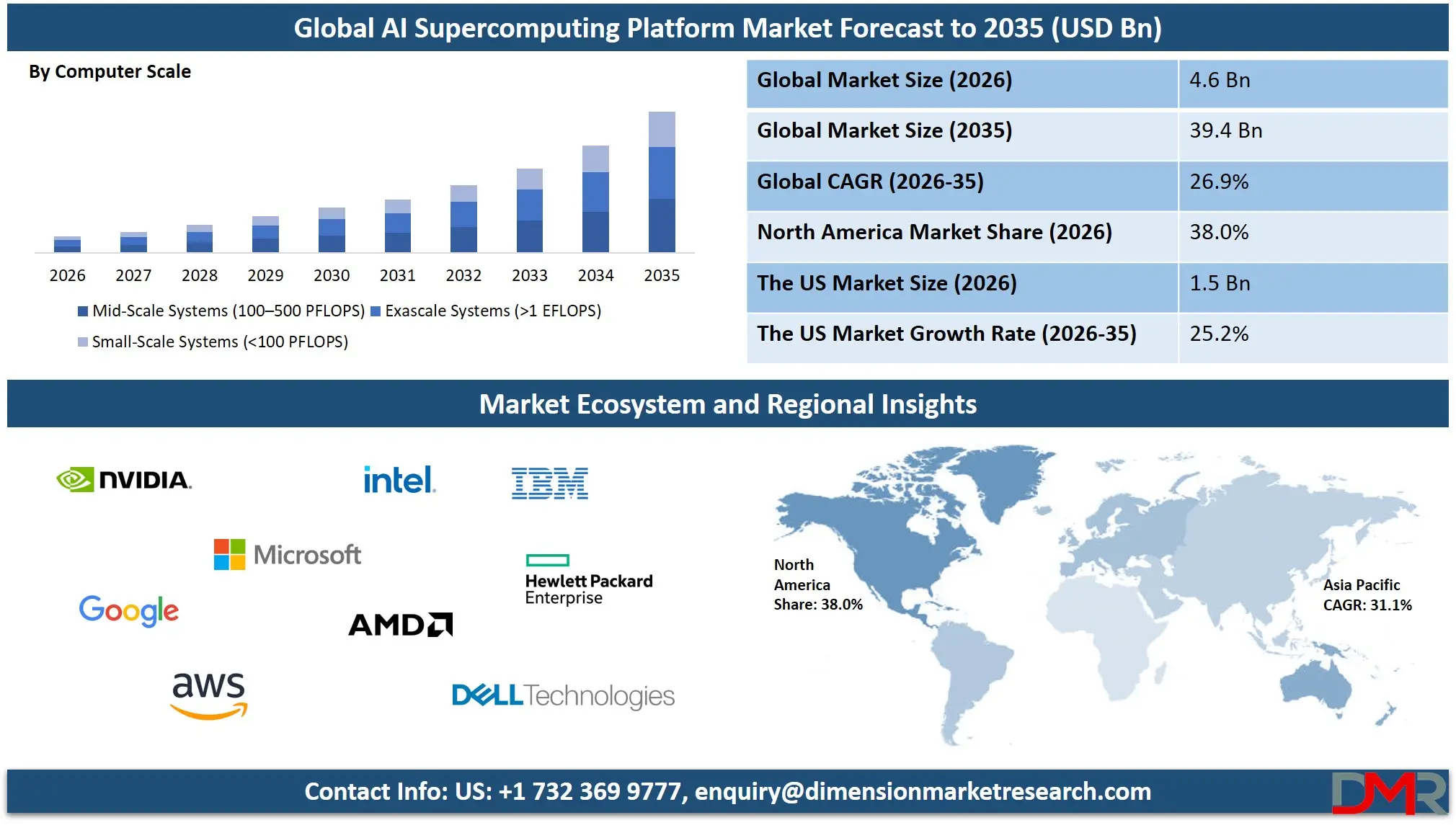

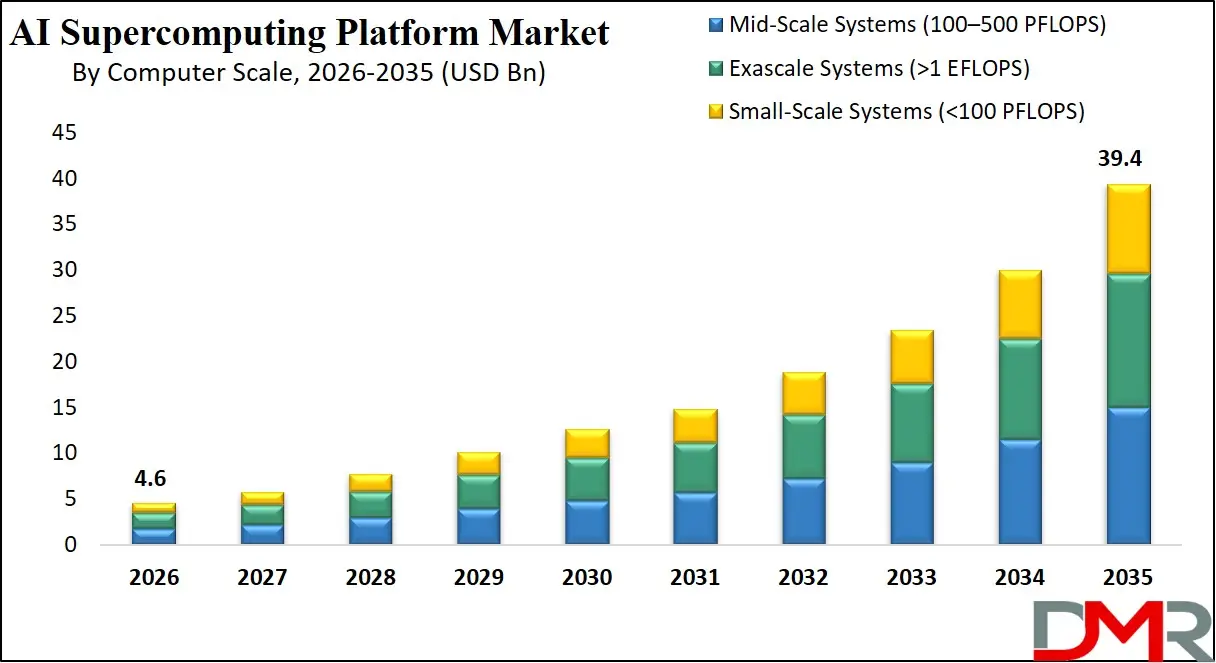

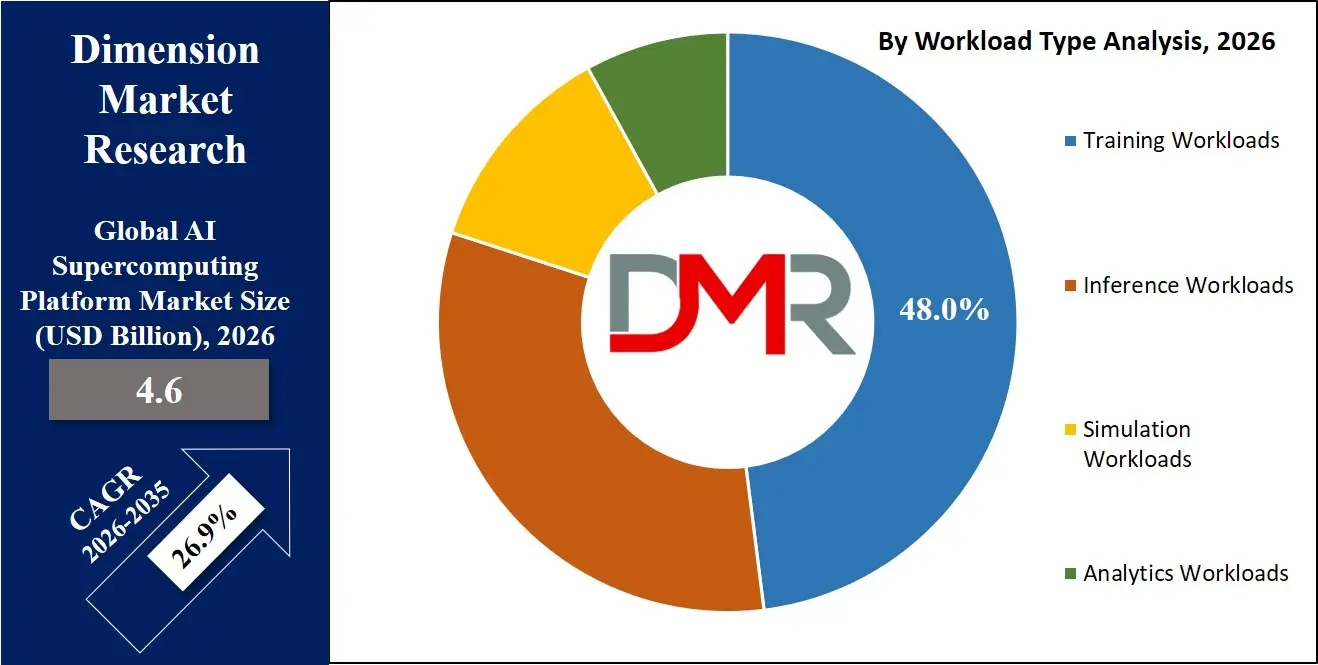

The Global AI Supercomputing Platform Market is projected to reach USD 4.6 billion in 2026 and USD 39.4 billion by 2035, growing at a CAGR of 26.9%, driven by HPC systems, GPU AI clusters, and exascale infrastructure supporting generative AI and cloud-based model training ecosystems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The AI Supercomputing Platform Market comprises highly sophisticated HPC platforms built on GPU, AI accelerator, and fast interconnection technologies utilized for massive AI training and simulations. This market is booming as a result of an exponential rise in computing requirements from generative AI and scientific simulation models. Programs by government agencies such as the exascale program by U.S. Department of Energy (DOE) and EuroHPC in Europe are fueling infrastructure investments at a national level.

These supercomputers support trillion-parameter models and real-time inference applications within fields like health care, defense, and climate studies. The DOE of the United States reports that an exascale computer can process over a quintillion calculations every second, signifying massive computing power. Looking ahead, energy efficiency, sovereignty, and cloud supercomputing will lead future growth.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

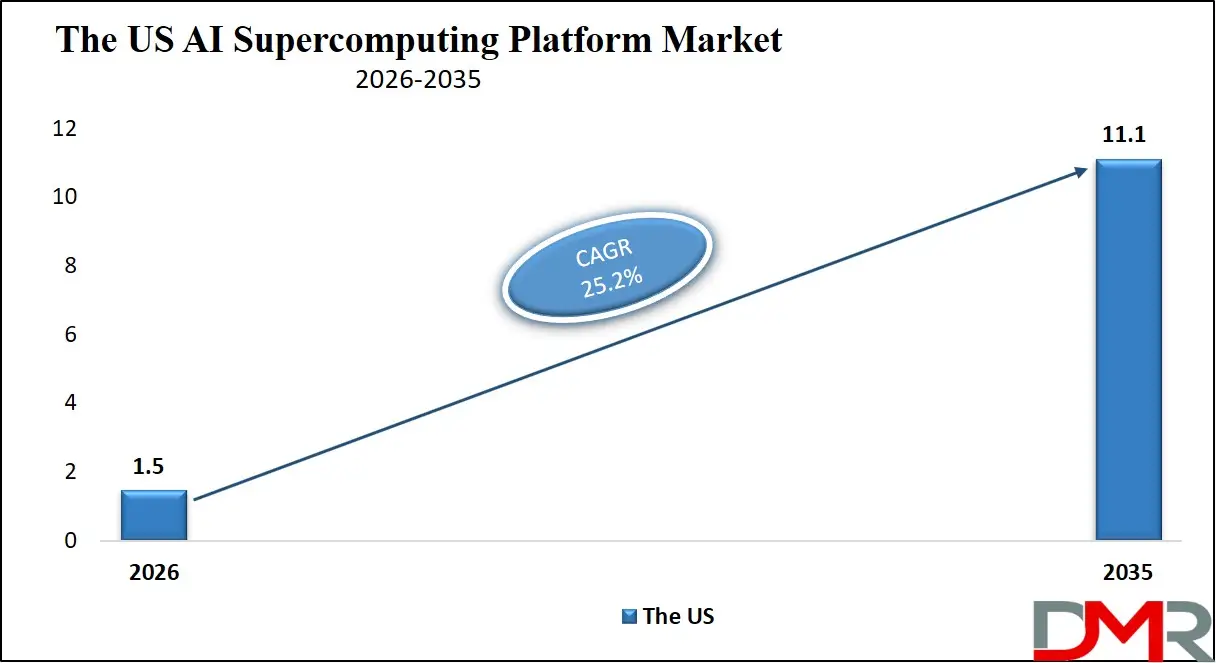

US AI Supercomputing Platform Market

The US AI Supercomputing Platform Market is projected to reach USD 1.5 billion in 2026 and USD 11.1 billion by 2035, growing at a CAGR of 25.2%.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States AI Supercomputing Platform market leads the world owing to its robust hyperscaler base, highly evolved semiconductor industry, and widespread deployment of exascale HPC platforms backed by federal programs run by organizations such as the Department of Energy and the National Science Foundation. Market growth is being propelled by increasing requirements for generative AI, GPU-based data centers, and advanced AI training platforms.

Europe AI Supercomputing Platform Market

Europe AI Supercomputing Platform Market is anticipated to reach USD 1.2 billion in 2026, expanding with a CAGR of 25.2%. The growth is driven by strong investments in sovereign AI infrastructure, HPC modernization, and EU-backed supercomputing initiatives. Increasing adoption of AI workloads across automotive, manufacturing, and research sectors is further accelerating demand. Expansion of energy-efficient and liquid-cooled data centers is also supporting regional market growth.

Japan AI Supercomputing Platform Market

Japan AI Supercomputing Platform Market is anticipated to reach USD 460 million in 2026, expanding with a CAGR of 26.6%. Growth is driven by strong government focus on advanced supercomputing programs and AI-driven digital transformation initiatives. Increasing adoption of robotics, autonomous systems, and industrial AI is further boosting demand for high-performance computing infrastructure. Additionally, rising investments in semiconductor innovation and next-generation data centers are strengthening Japan's position in the global AI supercomputing ecosystem.

Key Takeaways

- Market Size: The Global AI Supercomputing Platform Market is projected at USD 4.6 billion in 2026, reaching USD 39.4 billion by 2035.

- Growth Rate and Outlook: The market is expected to grow at a CAGR of 26.9%, driven by rapid expansion of AI workloads and exascale computing infrastructure.

- Primary Growth Drivers: Growth is fueled by rising demand for generative AI, large language model training, GPU-accelerated computing, and hyperscale cloud adoption.

- By Component Analysis: Hardware dominates with 68.0% share, reflecting strong compute infrastructure demand.

- By Deployment Model Analysis: Cloud-based HPC leads with 58% share due to scalable AI training platforms and hyperscaler-driven infrastructure expansion.

- By Workload Type Analysis: Training workloads dominate with 48% share, driven by large-scale AI model development and generative AI systems.

- Regional Leadership: North America leads the market with 38% share in 2026, supported by strong hyperscaler presence and advanced AI supercomputing infrastructure.

What is AI Supercomputing Platform?

AI Supercomputing Platform refers to an advanced supercomputing platform which utilizes GPU, AI chips, and parallel computation to train and deploy large-scale AI models. According to U.S. National Science Foundation, supercomputers are capable of carrying out quintillion computations within a second. Thus, these supercomputers facilitate highly sophisticated research and applications in science and AI. This includes generative AI, deep learning, and big data processing, among others. The United States Department of Energy utilizes HPC in simulations related to climate change, energy, and national security. Such systems are used in exascale and cloud-based data centers.

Use Cases

- Training AI Models: These platforms train AI models such as LLMs and deep learning models through massive parallelization on GPUs to reduce training time for large-scale AI models.

- Scientific Simulations: Advanced scientific simulations are carried out on these platforms in areas of climate change, physics, and energy. Government agencies such as the U.S. Department of Energy utilize them to carry out highly accurate simulations that involve solving highly complex equations.

- Life Sciences Research: Genomics, protein analysis, and drug discovery simulations are performed through AI supercomputing in life sciences. These operations aid researchers in discovering potential treatment options through large-scale simulation of biological models.

- Autonomous Systems: The training of AI models used in autonomous vehicles, robotics, and unmanned aerial vehicles is accomplished through these platforms.

How AI is Transforming the AI Supercomputing Platform Market?

Artificial intelligence is revolutionizing the AI supercomputing platform space through enhanced parallel computing and large scale training of models using GPU clusters.

AI is promoting the use of exascale and cloud-native infrastructures in the context of generative AI computing. Through AI optimization, resource utilization is improved, and computational costs reduced.

Market Dynamics

Key Drivers in the Global AI Supercomputing Platform Market

Rising demand for generative AI and LLMs

Demand for generative AI and large language models is rapidly increasing the need for high-performance AI supercomputing platforms. Training these models requires massive GPU clusters and parallel processing capabilities. Enterprises and research institutions are investing in scalable compute infrastructure. This is driving adoption of exascale and cloud-based HPC systems. The need for faster AI training cycles continues to fuel market growth.

Expansion of hyperscale cloud infrastructure

Hyperscale cloud providers are expanding AI-optimized data centers to support growing compute workloads. These facilities integrate GPUs, accelerators, and high-speed networking for scalable performance. Increasing enterprise shift toward cloud AI platforms is boosting infrastructure investment. This enables on-demand access to supercomputing power. It also reduces reliance on traditional on-premise systems.

Restraints in the Global AI Supercomputing Platform Market

High infrastructure and operational costs

AI supercomputing systems require very high capital investment in hardware, cooling, and networking. Operational costs are also elevated due to energy consumption and maintenance needs. Advanced exascale systems further increase setup complexity and expense. This limits adoption among small and mid-sized organizations. Cost remains a key barrier to widespread deployment.

Energy consumption and cooling challenges

These systems consume large amounts of power, creating sustainability concerns. Managing heat from dense GPU clusters requires advanced cooling solutions. Data centers face pressure to improve energy efficiency while maintaining performance. Rising electricity costs add further operational burden. This restricts scalability in energy-constrained regions.

Growth Opportunities in the Global AI Supercomputing Platform Market

Development of sovereign AI systems

Governments are allocating funds for their AI and supercomputing systems in order to achieve digital sovereignty. Such investments will satisfy the needs related to research, security, and reliable computing. This factor fuels interest in locally built HPC systems. Public investment boosts exascale systems creation. It will also bolster local AI innovation ecosystems.

AI accelerator developments

Modern AI accelerators make computations more effective and reduce training time. Thus, such technologies allow the development of more powerful but smaller supercomputers. Advancements in semiconductors boost enterprise AI technology adoption as they offer better scalability options.

Trends in the Global AI Supercomputing Platform Market

Shift toward exascale and distributed systems

The market is moving toward exascale computing and distributed AI architectures. These systems enable massive parallel processing across global data centers. Cloud-native HPC is becoming increasingly common. This improves scalability and workload flexibility. It is reshaping supercomputing infrastructure design.

Adoption of advanced cooling technologies

Liquid cooling is becoming a key trend due to high heat output from AI workloads. It offers better efficiency than traditional air cooling systems. Data centers are increasingly adopting direct-to-chip and immersion cooling. This supports higher compute density and performance. It is essential for next-generation AI supercomputing systems.

Research Scope and Analysis

By Component Analysis

The hardware component is anticipated to be the market leader, accounting for nearly 68% in 2026 owing to rising demand for GPUs, AI accelerators, and high-performance computing components for AI model training and exascale computing. The software layer complements the above scenario through providing support for the development of AI frameworks, workload management, and performance optimization in distributed computing clusters. The software layer helps in optimizing resource use and faster model training.

By Deployment Model Analysis

Cloud-based HPC will take the lead with a market share of almost 58% in 2026 because of the need for scalable and on-demand computing resources for training machine learning models and generative AI. Cloud-based HPC can provide scalability, reduced capital expenditure, and accessibility to GPU technology. On-premise HPC serves governments and companies requiring maximum security and complete control over their data. But its expensive and complex nature restricts its usage.

By Workload Type Analysis

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The training workload category is projected to take a leading role, with around a 48% market share in 2026 because of a strong requirement for training huge AI models like LLMs and generative AI that require large amounts of GPU compute power. The inference workload category deals with running already trained models and generating immediate output in areas like prediction and decision-making.

By Computer Scale Analysis

Mid-Scale Systems (100 to 500 PFLOPS) will dominate the compute scale market space, contributing up to 38% market share in 2026 owing to their excellent balance of speed, cost efficiency, and scalability for enterprise AI applications and cloud training clusters. Mid-scale systems are mainly deployed for the training of big models and AI deployments in industry. The Exascale category (>1 EFLOPS) comprises the highest compute scale systems and is built for extreme-scale training and simulation, including scientific simulation and research programs for the nation. Exascale provides unmatched processing capabilities for advanced Generative AI applications and simulations.

By Cooling Technology Analysis

The air cooling method will lead the way in terms of cooling technologies with approximately 42% market share in 2026 owing to its prevalent use in current data centers because of cost effectiveness, ease of implementation, and infrastructure available for handling heat management in HPC systems. On the other hand, the liquid cooling method is witnessing a fast rise in popularity among AI supercomputers because it performs more efficiently in handling dense GPU clusters and exascale computers. Moreover, rising adoption of direct chip and immersion cooling methods is boosting its adoption rate in future data centers.

By End-User Industry Analysis

It is estimated that Cloud Service Providers will be the leading players in the consumer market segment, with nearly 42% market share in 2026, owing to hyperscalers' AI supercomputer infrastructure for high-end model training, inference, and GPU as a service platforms. These companies have invested heavily in building huge data centers and are witnessing high demand for cloud AI computing power. On the other hand, enterprises are deploying AI supercomputer platforms to gain an edge in terms of improving analysis and decision-making capabilities. Their usage among BFSI, manufacturing, retail, and health care sectors is growing because of their digital transformation and operational efficiency.

The Global AI Supercomputing Platform Market Report is segmented on the basis of the following:

By Component

- Hardware

- GPU Compute Systems

- AI Accelerators (ASIC, TPU, FPGA)

- CPU Compute Nodes

- Memory & Storage Systems

- High-Speed Interconnect Systems

- Software

- AI Framework Stack

- Cluster Orchestration Platforms

- Optimization & Compiler Tools

- Services

- Integration & Deployment Services

- Managed Supercomputing Services

- Consulting & Support Services

By Deployment Model

- Cloud-Based High Performance Computing (HPC)

- Hyperscaler AI Infrastructure

- GPU-as-a-Service Platforms

- AI Training Cloud Clusters

- On-Premise High Performance Computing (HPC)

- Government Supercomputing Systems

- Enterprise Private AI Clusters

- Defense & Security Systems

- Hybrid High Performance Computing (HPC)

- Cloud Burst Architectures

- Edge-Integrated HPC Systems

By Workload Type

- Training Workloads

- Large Language Model Training

- Computer Vision Training

- Multimodal Model Training

- Reinforcement Learning Systems

- Inference Workloads

- Edge AI Inference

- Recommendation Engines

- Autonomous Systems Processing

- Simulation Workloads

- Climate & Weather Simulation

- Drug Discovery Simulation

- Engineering & Physics Simulation

- Analytics Workloads

- Predictive Analytics Systems

- Enterprise Intelligence Platforms

By Computer Scale

- Mid-Scale Systems (100–500 PFLOPS)

- Exascale Systems (>1 EFLOPS)

- Small-Scale Systems (<100 PFLOPS)

By Cooling Technology

- Air Cooling

- Rack-Level Air Systems

- Data Center Airflow Systems

- Liquid Cooling

- Direct-to-Chip Cooling

- Immersion Cooling Systems

- Hybrid Cooling

- Mixed Thermal Cooling

- Adaptive Cooling Architectures

By End-User Industry

- Cloud Service Providers

- Enterprises

- Government & Defense

- Research Institutions

- Life Sciences

Regional Analysis

Leading Region by Market Share

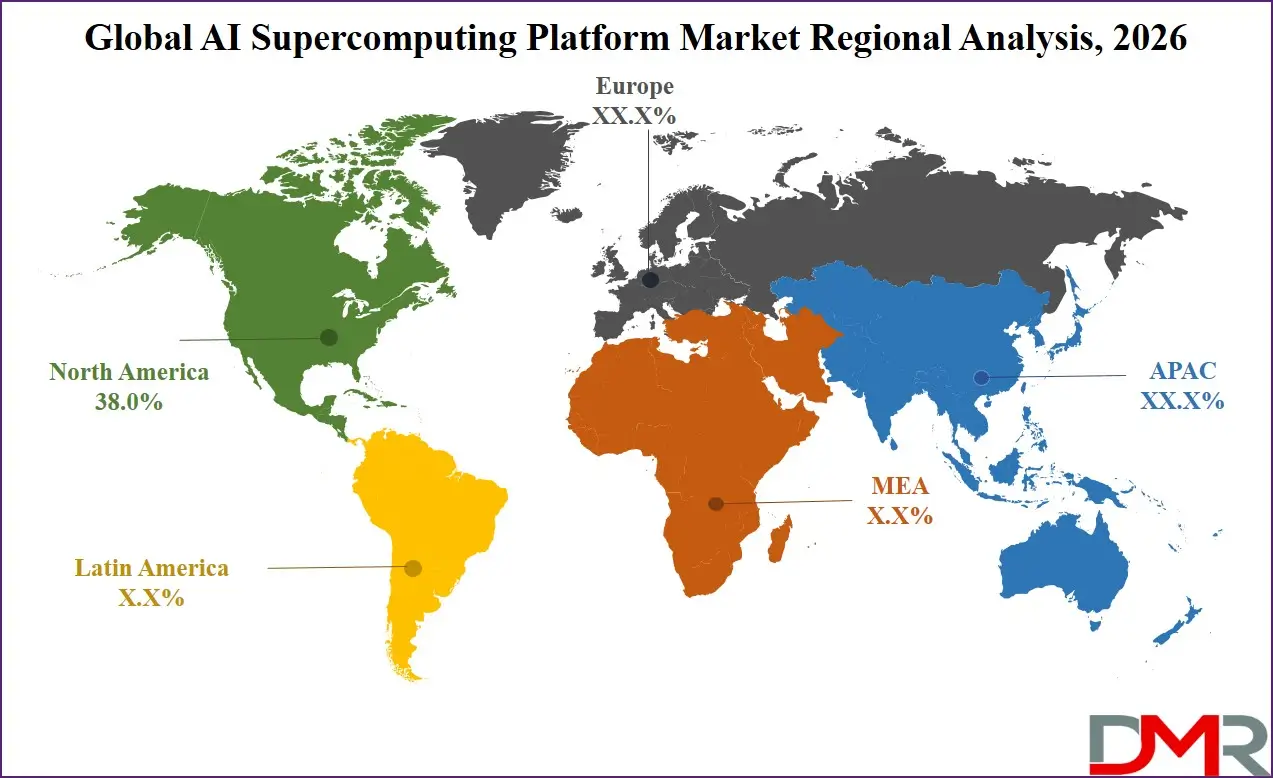

The North American region will dominate the market for AI supercomputing platforms in 2026, accounting for nearly 38.0% of the market, due to its high presence of hyperscalers, robust semiconductor industry, and initial implementation of exascale HPC systems. Funding by government organizations such as the U.S. Department of Energy aids in the building of infrastructure. High levels of AI development, cloud computing, and enterprise deployment enhance its leading position in the market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

The Asia-Pacific region will be the fastest-growing regional market due to the quick expansion of AI infrastructure, semiconductors, and cloud supercomputing in countries like China, India, Japan, and South Korea. The increasing usage of generative AI and national HPC initiatives boosts regional growth.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

High levels of concentration characterize the competitive environment due to dominance by the tech leaders with regard to AI hardware, cloud-based computing, and supercomputing systems. There are rapid innovations fueled by developments in GPUs, AI accelerators, and exascale computer systems. The development of the industry will be facilitated by strategic collaboration among cloud companies, semiconductor companies, and research institutions. Competition is largely centered around efficient computation using energy.

Some of the prominent players in the Global AI Supercomputing Platform Market are:

- NVIDIA

- Microsoft

- Google

- Amazon Web Services

- Intel

- Advanced Micro Devices

- IBM

- Hewlett Packard Enterprise

- Dell Technologies

- Lenovo

- Oracle

- Meta Platforms

- Apple

- Huawei Technologies

- Samsung Electronics

- Fujitsu

- NEC Corporation

- Supermicro

- Cerebras Systems

- Atos

- Other Key Players

Recent Developments

- April 2026: Minisforum unveiled an AI-powered high-performance computing NAS system based on AMD AI processors, targeting edge AI supercomputing and localized compute workloads for enterprise users.

- March 2026: Amazon Web Services confirmed a major agreement to deploy 1 million NVIDIA GPUs across its cloud infrastructure, significantly expanding AI supercomputing capacity for training and inference services.

- March 2026: Hewlett Packard Enterprise introduced an upgraded AI factory and exascale supercomputing platform with NVIDIA integration, enhancing large-scale AI computing capabilities for research labs, sovereign entities, and enterprises.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 4.6 Bn |

| Forecast Value (2035) |

USD 39.4 Bn |

| CAGR (2026–2035) |

26.9% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component (Hardware, Software, Services), By Deployment Model (Cloud-Based High Performance Computing HPC, On-Premise High Performance Computing HPC, Hybrid High Performance Computing HPC), By Workload Type (Training Workloads, Inference Workloads, Simulation Workloads, Analytics Workloads), By Computer Scale (Mid-Scale Systems 100–500 PFLOPS, Exascale Systems >1 EFLOPS, Small-Scale Systems <100 PFLOPS), By Cooling Technology (Air Cooling, Liquid Cooling, Hybrid Cooling), By End-User Industry (Cloud Service Providers, Enterprises, Government & Defense, Research Institutions, Life Sciences) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the AI Supercomputing Platform Market?

▾ The AI Supercomputing Platform Market is expected to be valued at USD 4.6 billion in 2026 and is projected to reach USD 39.4 billion by 2035.

What is the CAGR of the AI Supercomputing Platform Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 26.9% during the forecast period 2026–2035.

What factors are driving the growth of the AI Supercomputing Platform Market?

▾ Growth is driven by rising demand for generative AI, large language models, HPC infrastructure, GPU-accelerated computing, and exascale systems, along with increasing cloud adoption and government investments in AI supercomputing.

What are the major trends in the AI Supercomputing Platform Market?

▾ Key trends include the shift toward exascale computing, cloud-native AI supercomputing, liquid-cooled data centers, AI accelerator integration, and distributed training architectures for large-scale AI models.

Which region held the largest share of the AI Supercomputing Platform Market in 2026?

▾ North America held the largest share in 2026 with 38.0%, driven by hyperscaler dominance and advanced AI infrastructure.

Which region is expected to grow the fastest in the AI Supercomputing Platform Market?

▾ Asia Pacific is the fastest-growing region, supported by rapid AI infrastructure expansion, semiconductor growth, and national supercomputing programs.

Who are the key players in the AI Supercomputing Platform Market?

▾ Key players include NVIDIA, Microsoft, Google, Amazon Web Services, Intel, AMD, IBM, HPE, Dell Technologies, Lenovo, Oracle, Meta, Apple, Huawei, Samsung, Fujitsu, NEC, Supermicro, Cerebras Systems, and Atos.

How is the AI Supercomputing Platform Market segmented?

▾ The market is segmented by Component, Deployment Model, Workload Type, Compute Scale, Cooling Technology, and End-User Industry.