Market Overview

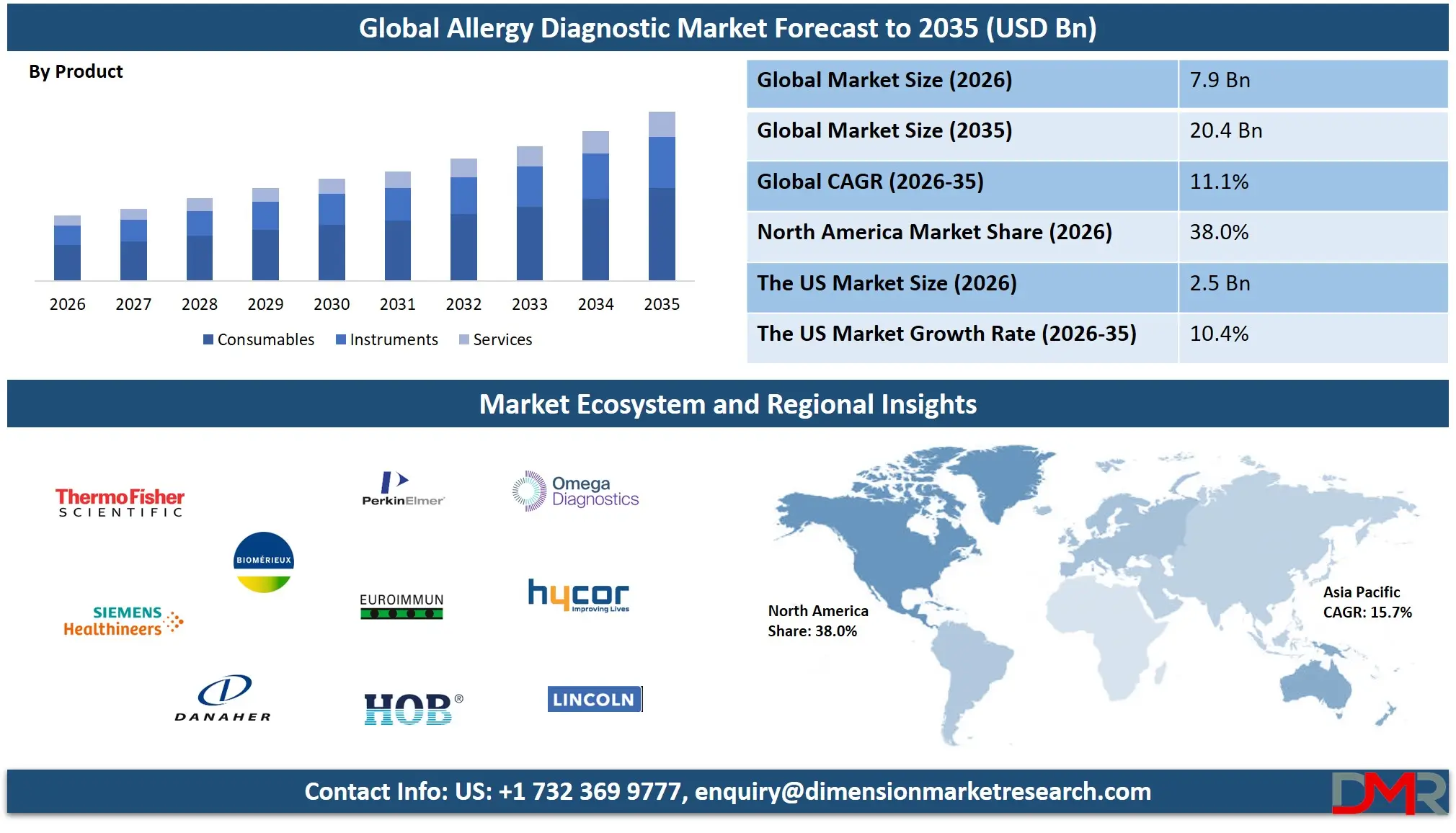

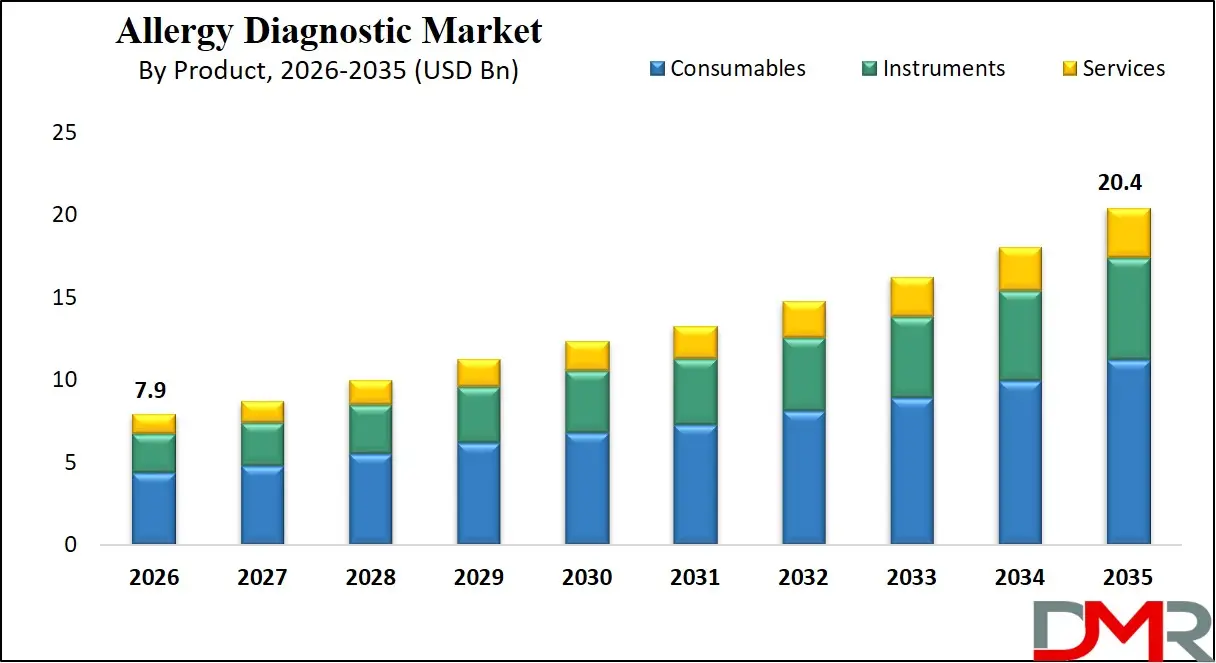

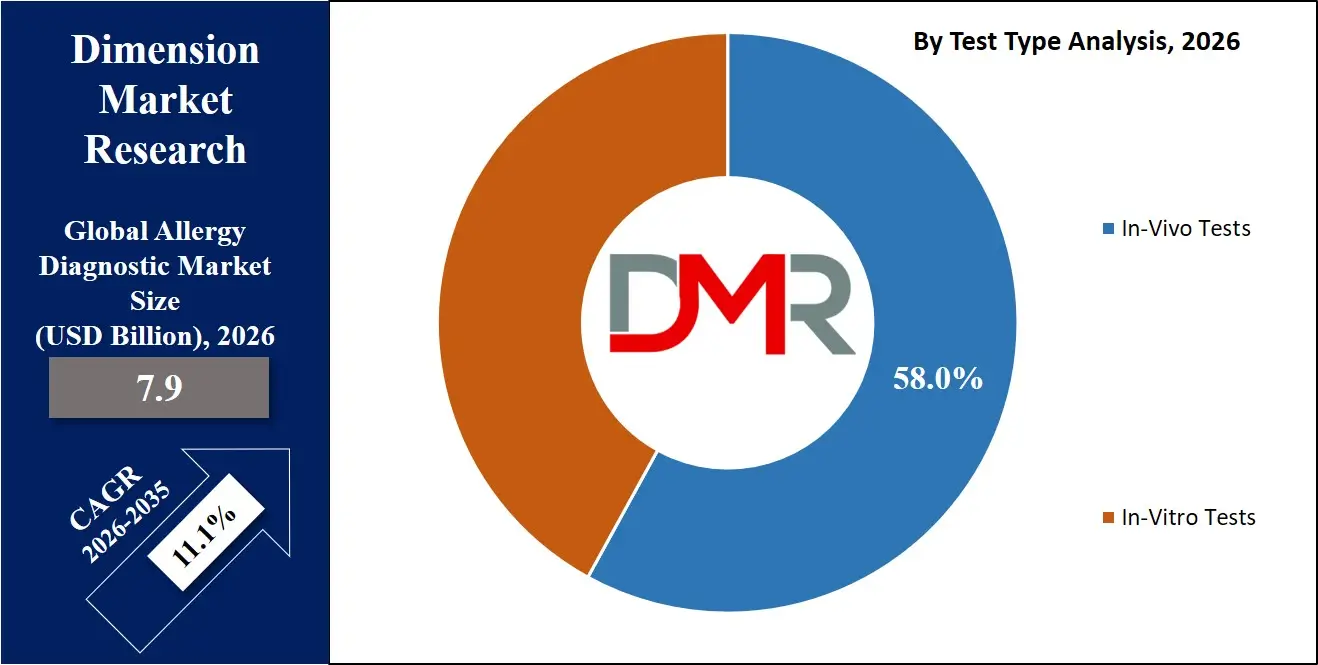

The global Allergy Diagnostic Market is estimated to reach USD 7.9 billion in 2026 and is expected to expand at a CAGR of 11.1% from 2026 to 2035, driven by the rising prevalence of allergic diseases, growing adoption of allergy testing technologies, and increasing demand for advanced immunodiagnostics, reaching approximately USD 20.4 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Allergy diagnostics refers to a range of medical tests and laboratory techniques used to identify substances that trigger allergic reactions in the human body. These tests help physicians determine how the immune system responds to specific allergens such as pollen, dust mites, food proteins, animal dander, insect venom, or certain medications. Diagnostic procedures typically measure immunoglobulin E antibodies or observe the body’s response to controlled allergen exposure through skin testing or blood based analysis. Accurate allergy detection plays an essential role in clinical immunology because it allows healthcare professionals to confirm hypersensitivity conditions, guide treatment plans, and prevent severe allergic reactions. The growing adoption of advanced immunoassays, molecular diagnostic tools, and automated laboratory systems has improved the precision and speed of allergy testing, making early identification of allergic disorders more accessible across healthcare systems.

The global Allergy Diagnostic Market represents the industry involved in developing, manufacturing, and distributing products and services used for detecting allergic diseases. This market includes allergy test kits, reagents, allergen extracts, diagnostic instruments, and laboratory services that support the identification of respiratory, food, drug, and environmental allergies. Increasing prevalence of allergic conditions such as allergic rhinitis, asthma, eczema, and food allergies has significantly expanded the demand for diagnostic testing worldwide. Rising awareness about allergy related health risks and the growing emphasis on early disease detection are encouraging healthcare providers to incorporate specialized allergy testing into routine clinical evaluation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growth in the global Allergy Diagnostic Market is also supported by advancements in immunodiagnostic technologies and the expansion of diagnostic laboratory networks across developed and emerging economies. Automated immunoassay platforms, component resolved diagnostics, and high sensitivity blood testing methods are improving the accuracy of allergen identification. In addition, rising urbanization, environmental pollution, and lifestyle changes are contributing to higher incidence of allergic disorders, which is increasing the need for comprehensive diagnostic solutions. Expanding healthcare infrastructure, increasing investment in laboratory medicine, and continuous research in allergy and immunology are expected to strengthen the global market outlook in the coming years.

The US Allergy Diagnostic Market

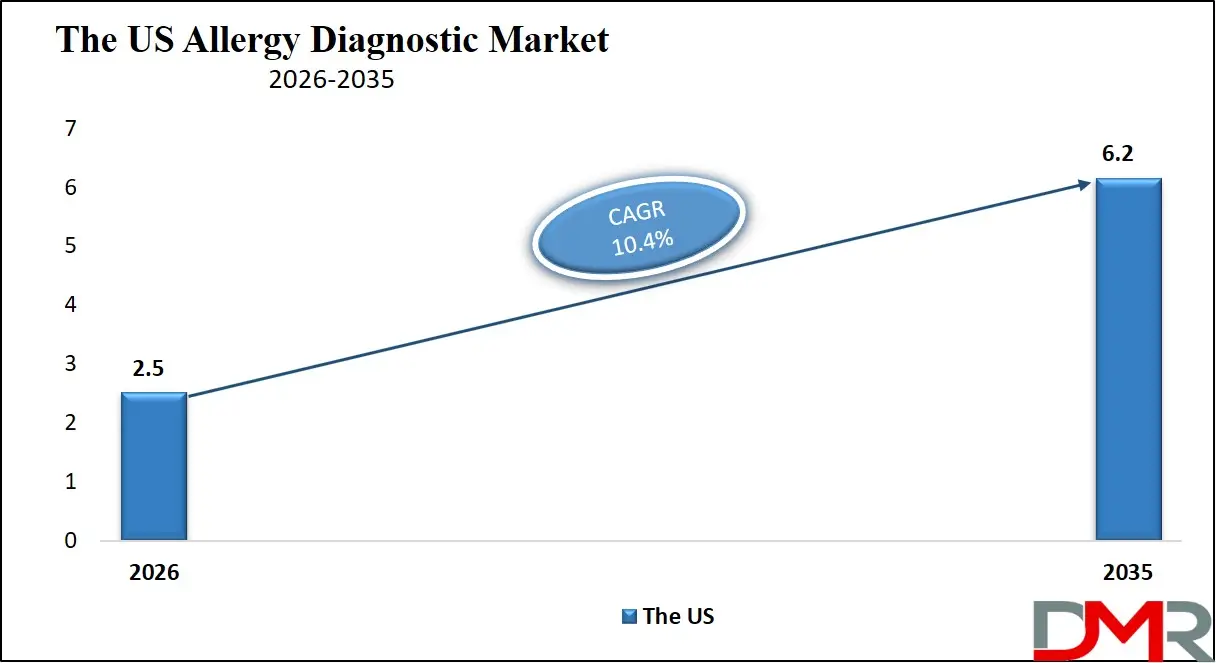

The U.S. Allergy Diagnostic Market size is expected to reach at USD 2.5 billion in 2026. It is further expected to witness subsequent growth in the upcoming period, holding USD 6.2 billion in 2035 at a CAGR of 10.4%.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The allergy diagnostic market in the United States represents one of the most advanced segments of the global healthcare diagnostics industry. The country has a high prevalence of allergic conditions including allergic rhinitis, food allergies, asthma, and eczema, which drives strong demand for accurate diagnostic testing. Healthcare providers widely utilize both skin based allergy tests and blood based immunoglobulin E testing to identify allergen sensitivities. Well established diagnostic laboratory networks, advanced immunoassay technologies, and strong adoption of automated testing platforms further support market growth. Increasing awareness of allergy related complications is encouraging early diagnosis and preventive healthcare practices.

The expansion of the US allergy diagnostic market is also supported by strong healthcare infrastructure, high healthcare expenditure, and continuous advancements in clinical immunology research. Diagnostic laboratories and hospitals are increasingly integrating high sensitivity immunodiagnostic systems and component resolved diagnostic methods to improve the precision of allergen identification. Rising environmental factors such as air pollution, changing dietary habits, and increased exposure to environmental allergens are contributing to the growing burden of allergic diseases. In addition, ongoing investments in biotechnology and laboratory medicine are accelerating the development of innovative allergy testing solutions across the country.

The Europe Allergy Diagnostic Market

The Europe allergy diagnostic market is projected to reach approximately USD 2.4 billion in 2026, reflecting the region’s strong adoption of advanced diagnostic technologies and comprehensive healthcare infrastructure. The high prevalence of allergic disorders such as asthma, allergic rhinitis, and food allergies across Western and Central Europe is driving demand for accurate and timely allergy testing. Diagnostic laboratories and hospitals are increasingly integrating in‑vitro testing methods, immunoassay platforms, and component resolved diagnostics to provide precise allergen identification. The presence of well-established healthcare systems, coupled with rising patient awareness, supports sustained market growth and strengthens the region’s position in the global landscape.

The market in Europe is also benefiting from continuous technological advancements and the expansion of allergy testing services in both urban and semi urban areas. Multiplex immunoassays, automated analyzers, and high sensitivity allergy testing kits are becoming standard tools in laboratories and clinical settings, allowing for faster and more accurate diagnosis. Collaborations between healthcare providers, research institutions, and diagnostic technology companies are accelerating the adoption of innovative testing solutions. With a projected compound annual growth rate of 10.2%, the European allergy diagnostic market is expected to steadily expand, driven by rising incidence of allergic conditions and increasing emphasis on early detection and personalized allergy management.

The Japan Allergy Diagnostic Market

The Japan allergy diagnostic market is projected to reach approximately USD 632 million in 2026, reflecting the country’s growing focus on healthcare innovation and preventive care. Increasing prevalence of allergic conditions such as food allergies, asthma, and allergic rhinitis among children and adults is driving demand for accurate diagnostic solutions. Japanese hospitals and specialized clinics are adopting both in‑vivo and in‑vitro testing methods, including skin prick tests, specific IgE assays, and component resolved diagnostics, to provide precise allergen identification and support personalized treatment plans. Rising public awareness about allergy management is further encouraging early diagnosis and routine testing.

Technological advancements and government initiatives promoting healthcare infrastructure are also contributing to the growth of the Japanese allergy diagnostic market. Automated immunoassay analyzers, multiplex testing platforms, and high sensitivity allergy kits are increasingly used in laboratories to improve efficiency and diagnostic accuracy. Collaboration between healthcare providers and diagnostic solution companies is expanding the availability of advanced allergy testing services across urban and semi‑urban regions. With a projected compound annual growth rate of 9.5%, the market in Japan is expected to grow steadily, supported by rising allergic disease prevalence, modernization of laboratory facilities, and increasing emphasis on preventive healthcare strategies.

Global Allergy Diagnostic Market: Key Takeaways

- Global Market Size and Growth: The global Allergy Diagnostic Market is projected to reach USD 7.9 billion in 2026 and expand at a CAGR of 11.1%, reaching approximately USD 20.4 billion by 2035, highlighting strong long‑term growth driven by rising allergy prevalence and adoption of advanced testing technologies.

- Dominance of In‑Vivo Tests: In‑Vivo tests are expected to dominate the test type segment with 58.0% market share in 2026, indicating continued preference for skin‑based diagnostics in clinical settings.

- Consumables Lead Product Segment: Consumables lead the product segment, capturing 55.0% of total market share in 2026, driven by high usage of reagents, allergen extracts, and assay kits in routine allergy diagnostics.

- Regional Market Insights: North America is anticipated to hold the largest regional revenue share of 38.0% in 2026, while Europe and Japan are projected at USD 2.4 billion and USD 632 million, respectively, with CAGRs of 10.2% and 9.5%, showing regional disparities in market penetration and growth rates.

- Prevalence of Inhaled Allergens: Inhaled allergens dominate the allergen type segment with 60.0% market share in 2026, driven by the rising incidence of respiratory allergies caused by pollen, dust mites, mold, and pet dander, and increasing adoption of precise diagnostic testing.

Global Allergy Diagnostic Market: Use Cases

- Respiratory Allergy Diagnosis: Allergy diagnostic tests are widely used to detect respiratory allergies caused by pollen, dust mites, mold, and pet dander. Techniques such as skin prick testing and specific IgE blood tests help identify triggers of allergic rhinitis and asthma. Early diagnosis supports targeted treatment and allergen avoidance strategies.

- Food Allergy Detection: Allergy diagnostics help identify sensitivities to foods such as milk, peanuts, eggs, wheat, and shellfish. Immunoassay based blood testing and component resolved diagnostics improve accuracy in detecting food allergens and support dietary management and risk prevention.

- Drug Allergy Testing: Diagnostic testing is used to identify allergic reactions to medications including antibiotics and NSAIDs. Accurate drug allergy identification helps physicians prevent adverse reactions and select safer therapeutic alternatives.

- Personalized Allergy Treatment Planning: Allergy diagnostics support personalized treatment by identifying specific allergen triggers. This enables clinicians to design targeted immunotherapy, monitor immune response, and improve long term allergy management outcomes.

Global Allergy Diagnostic Market: Stats & Facts

- CDC – National Center for Health Statistics (Adults, 2024)

- In 2024, 31.7% of U.S. adults had a diagnosed seasonal allergy, eczema, or food allergy.

- In adults in 2024, 25.2% had a diagnosed seasonal allergy.

- In 2024, 7.7% of adults had diagnosed eczema.

- In 2024, 6.7% of adults had diagnosed food allergy.

- Seasonal allergy prevalence was higher in nonmetropolitan adults (28.1%) vs metropolitan (24.8%).

- Women were more likely to have diagnosed eczema (9.5%) than men (5.7%).

- Diagnosed food allergies in 2024 were highest in Black non‑Hispanic adults (9.9%).

- CDC – National Center for Health Statistics (Children, 2024)

- In 2024, 29.5% of U.S. children (0–17) had an allergic condition.

- 20.6% of children had diagnosed seasonal allergies in 2024.

- 12.7% of U.S. children had eczema in 2024.

- 5.3% of children had diagnosed food allergy in 2024.

- Boys aged 0–17 had a higher food allergy rate (5.9%) than girls (4.7%).

- Food allergy rates increased with age: 3.9% (0–5) to 6.9% (12–17).

- CDC – NCHS Press Releases (U.S. Allergic Conditions)

- Nearly 3 in 10 U.S. adults and children reported an allergy in 2024.

- About 25.2% of U.S. adults had seasonal allergy in 2024.

- About 7.7% of U.S. adults had eczema in 2024.

- About 6.7% of U.S. adults had food allergy in 2024.

- 20.6% of U.S. children aged 0–17 had seasonal allergy.

- 12.7% of U.S. children had eczema in 2024.

- 5.3% of U.S. children had food allergy in 2024.

- CDC – FastStats on Allergies (2024 Data)

- Adults ≥18: 31.7% had any allergy in 2024.

- Adults ≥18: 25.2% had seasonal allergy in 2024.

- Adults ≥18: 7.7% had eczema in 2024.

- Adults ≥18: 6.7% had food allergy in 2024.

- CDC – Morbidity Data (Children, 2024)

- Children <18: 29.5% had any allergy.

- Children <18: 20.6% had seasonal allergy.

- Children <18: 12.7% had eczema.

- Children <18: 5.3% had food allergy.

Global Allergy Diagnostic Market: Market Dynamic

Driving Factors in the Global Allergy Diagnostic Market

Increasing Global Burden of Allergic Disorders

The rising incidence of allergic diseases such as allergic rhinitis, asthma, eczema, and food allergies is a major driver for the allergy diagnostic market. Growing exposure to environmental allergens, air pollution, and changing dietary patterns has significantly increased hypersensitivity reactions among both children and adults. Healthcare providers are increasingly recommending early allergy testing to identify allergen triggers and manage chronic allergic conditions effectively. As a result, demand for skin prick testing, specific IgE blood tests, and advanced immunodiagnostic solutions is expanding across hospitals, specialty clinics, and diagnostic laboratories worldwide.

Technological Advancements in Allergy Testing Platforms

Continuous innovation in immunoassay technology and molecular allergy diagnostics is accelerating the growth of the market. Modern diagnostic platforms now offer high sensitivity allergen detection, multiplex testing capabilities, and automated laboratory workflows. Technologies such as component resolved diagnostics allow clinicians to identify specific allergen molecules and improve diagnostic accuracy. These advancements enhance clinical decision making and support personalized allergy management. The integration of automated analyzers and high throughput diagnostic systems is also improving laboratory efficiency and expanding access to precise allergy testing services.

Restraints in the Global Allergy Diagnostic Market

High Cost of Advanced Diagnostic Technologies

The high cost associated with advanced allergy diagnostic instruments and laboratory testing procedures can limit market growth in several regions. Automated immunoassay analyzers, multiplex allergen testing panels, and molecular diagnostic systems require substantial investment in equipment, infrastructure, and trained personnel. Smaller healthcare facilities and diagnostic laboratories may face financial constraints in adopting these advanced testing platforms. In addition, recurring expenses related to reagents, allergen extracts, and diagnostic consumables can increase overall testing costs, making allergy diagnostics less affordable in cost sensitive healthcare markets.

Limited Awareness and Underdiagnosis in Emerging Economies

In many developing countries, allergic diseases remain underdiagnosed due to limited awareness about allergy testing and inadequate access to specialized diagnostic services. Patients often rely on symptomatic treatment without identifying the underlying allergen triggers. A shortage of trained allergists, limited laboratory infrastructure, and lack of standardized testing protocols further contribute to delayed diagnosis. These challenges restrict the adoption of advanced immunodiagnostic technologies and slow the overall expansion of the allergy diagnostic market in emerging healthcare systems.

Opportunities in the Global Allergy Diagnostic Market

Expansion of Precision Medicine and Personalized Allergy Care

The growing focus on precision medicine is creating strong opportunities for advanced allergy diagnostics. Healthcare providers are increasingly using detailed allergen profiling to design personalized treatment strategies for patients with complex allergic conditions. Technologies such as molecular allergy diagnostics and component resolved testing enable clinicians to identify specific allergen components responsible for immune reactions. This allows the development of targeted immunotherapy and individualized treatment plans. As personalized healthcare continues to gain importance, the demand for accurate and comprehensive allergy diagnostic solutions is expected to increase significantly.

Growth of Diagnostic Laboratory Networks in Emerging Markets

Rapid expansion of diagnostic laboratory chains and healthcare infrastructure in emerging economies is creating new growth opportunities for allergy diagnostic providers. Countries in Asia Pacific, Latin America, and the Middle East are investing heavily in laboratory medicine and modern diagnostic technologies. Increasing healthcare expenditure, rising awareness about allergic diseases, and improving access to diagnostic services are encouraging the adoption of allergy testing solutions. The development of centralized diagnostic laboratories and high throughput testing facilities is expected to strengthen the market potential in these regions.

Trends in the Global Allergy Diagnostic Market

Adoption of Multiplex Allergy Testing Panels

One of the key trends in the allergy diagnostic industry is the increasing adoption of multiplex allergy testing panels that allow simultaneous detection of multiple allergens from a single patient sample. These advanced diagnostic platforms improve testing efficiency and reduce the time required for allergen identification. Multiplex immunoassays provide comprehensive sensitization profiles and help clinicians better understand complex allergic reactions. This trend is supporting the growth of automated allergy diagnostic systems and expanding their application in modern diagnostic laboratories.

Integration of Automation and Digital Laboratory Technologies

Automation and digitalization are transforming allergy diagnostics by improving workflow efficiency and diagnostic accuracy. Automated immunoassay analyzers, robotic sample handling systems, and digital laboratory information systems are being widely implemented in diagnostic laboratories. These technologies enable faster processing of allergy tests, minimize human error, and enhance data management. The integration of artificial intelligence based data analysis and digital health platforms is also supporting better interpretation of allergy test results and strengthening the future development of advanced allergy diagnostic solutions.

Global Allergy Diagnostic Market: Research Scope and Analysis

By Test Type Analysis

In vivo tests are anticipated to dominate the test type segment of the global allergy diagnostic market, accounting for around 58.0% of the total market share in 2026. These diagnostic procedures involve exposing the patient’s skin to small amounts of allergens to observe an immediate immune response. Common methods include skin prick tests, intradermal tests, patch tests, and allergen provocation tests, which are widely used in clinical allergy practice. These tests are preferred by healthcare professionals because they provide rapid results, are relatively cost effective, and allow physicians to identify multiple allergen sensitivities during a single clinical visit. The growing prevalence of respiratory allergies, allergic rhinitis, and environmental hypersensitivity conditions is further increasing the demand for skin based allergy testing in hospitals, allergy specialty clinics, and outpatient care settings worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In vitro tests represent another important segment of the allergy diagnostic market and are increasingly used in laboratory based allergen detection. These tests analyze blood samples to measure immunoglobulin E antibody levels associated with allergic reactions. Techniques such as specific IgE testing, total IgE assays, and component resolved diagnostics help laboratories accurately identify allergen sensitization without direct exposure to allergens on the patient’s skin. In vitro testing is particularly useful for patients with severe skin conditions, individuals taking antihistamine medications, or cases where skin testing may pose clinical risks. The adoption of automated immunoassay analyzers, advanced laboratory diagnostics, and high sensitivity allergy testing technologies is contributing to the steady growth of this segment across diagnostic laboratories and healthcare institutions globally.

By Product Analysis

Consumables are anticipated to dominate the product segment of the global allergy diagnostic market, accounting for around 55.0% of the total market share in 2026. This dominance is primarily driven by the continuous and repeated use of reagents, allergen extracts, assay kits, and other testing materials required for routine allergy diagnostics. Every diagnostic procedure, whether skin testing or laboratory based immunoglobulin E analysis, requires consumable products, which creates a consistent demand across hospitals, diagnostic laboratories, and specialty allergy clinics. The rising prevalence of respiratory allergies, food allergies, and environmental hypersensitivity is further increasing the volume of allergy testing procedures worldwide. As a result, the frequent replacement and high usage rate of consumables contribute significantly to the revenue generation within the allergy diagnostic ecosystem.

Instruments also represent a significant component of the allergy diagnostic market as they provide the technological infrastructure required to perform advanced allergy testing. These instruments include automated immunoassay analyzers, enzyme linked immunosorbent assay platforms, and other laboratory diagnostic systems designed to detect allergen specific antibodies with high accuracy. Diagnostic laboratories and hospitals are increasingly investing in automated allergy testing equipment to improve testing efficiency, reduce turnaround time, and handle growing testing volumes. The integration of advanced diagnostic technologies and automated laboratory workflows is enhancing the performance of allergy testing procedures and supporting the gradual expansion of the instruments segment in the global market.

By Allergen Type Analysis

Inhaled allergens are expected to dominate the allergen type segment of the global allergy diagnostic market, accounting for approximately 60.0% of the total market share in 2026. These allergens include substances such as pollen, dust mites, mold spores, and pet dander, which are common triggers for respiratory conditions like allergic rhinitis and asthma. The widespread prevalence of environmental allergies, combined with rising urbanization, increased air pollution, and climate change, has led to a growing demand for accurate detection of inhaled allergens. Diagnostic procedures such as skin prick testing and specific IgE blood tests are commonly used to identify sensitivities to these allergens, enabling healthcare providers to recommend targeted treatment plans, preventive strategies, and immunotherapy. Hospitals, diagnostic laboratories, and allergy specialty clinics are increasingly adopting comprehensive testing solutions to manage the rising burden of inhaled allergies worldwide.

Food allergens represent another important segment of the allergy diagnostic market, focusing on the identification of allergic reactions to foods such as milk, eggs, peanuts, tree nuts, shellfish, and wheat. The growing incidence of food allergies, particularly among children, has increased the demand for accurate and sensitive testing solutions. Laboratory based immunoassays, specific IgE tests, and component resolved diagnostics are widely used to detect food allergen sensitivities and guide dietary management. Early and precise identification of food allergens is crucial to prevent severe allergic reactions, including anaphylaxis, and to support the development of individualized treatment and avoidance strategies. The rising awareness of food related allergic risks is driving adoption of food allergen testing in hospitals, diagnostic laboratories, and pediatric care settings globally.

By Technology Analysis

Immunoassay technology is expected to dominate the technology segment of the global allergy diagnostic market, accounting for approximately 48.0% of the total market share in 2026. This technology involves detecting allergen specific antibodies, primarily immunoglobulin E, in patient samples using methods such as enzyme linked immunosorbent assays, chemiluminescent immunoassays, and fluorescence based immunoassays. Immunoassay platforms are widely adopted in diagnostic laboratories and hospitals due to their high sensitivity, accuracy, and ability to process multiple samples efficiently. The increasing demand for reliable allergy testing and the growing prevalence of respiratory and food allergies are driving the adoption of immunoassay technology, which allows clinicians to accurately identify allergen triggers and support targeted treatment plans. Automation and high throughput capabilities of immunoassay analyzers further enhance laboratory efficiency and contribute to the segment’s dominance in the global market.

Molecular allergy diagnostics represent a rapidly growing segment within the technology category, focusing on the identification of specific allergen components at a molecular level. Techniques such as component resolved diagnostics and recombinant allergen testing enable clinicians to pinpoint the exact proteins responsible for allergic reactions, improving diagnostic precision and supporting personalized allergy treatment. This technology is particularly valuable for complex cases, patients with multiple sensitizations, or those at risk of severe allergic reactions. The adoption of molecular allergy diagnostics is increasing as healthcare providers and diagnostic laboratories seek advanced solutions for precise allergen profiling, enabling better immunotherapy planning, risk assessment, and long term allergy management.

By End User Analysis

Diagnostic laboratories are expected to dominate the end user segment of the global allergy diagnostic market, accounting for around 55.0% of the total market share in 2026. These laboratories serve as the primary hubs for allergy testing, offering a wide range of services including skin prick tests, specific IgE blood assays, and component resolved diagnostics. Their dominance is driven by their ability to handle high volumes of samples, maintain quality control, and provide accurate and standardized results. Centralized laboratories are equipped with advanced immunoassay analyzers and automated testing platforms, which improve efficiency and turnaround time. The growing prevalence of allergic disorders, increasing demand for reliable diagnostics, and the adoption of high throughput testing systems by laboratories are further supporting their leading role in the market.

Hospitals also represent a significant segment within the allergy diagnostic market, providing in house testing and patient care services for allergic conditions. Hospitals often integrate allergy testing into outpatient clinics, immunology departments, and specialized pulmonary or pediatric care units, offering both in vivo and in vitro diagnostic procedures. The presence of skilled medical staff, access to advanced diagnostic instruments, and the ability to provide immediate clinical intervention make hospitals an important end user of allergy diagnostic solutions. Increasing awareness among patients and healthcare providers about the importance of early allergy detection is encouraging hospitals to expand their allergy testing services, which is contributing to steady growth in this segment globally.

The Global Allergy Diagnostic Market Report is segmented on the basis of the following:

By Test Type

- In-Vivo Tests

- Skin Prick Test (SPT)

- Intradermal Test

- Patch Test

- Provocation Test

- In-Vitro Tests

- Specific IgE Blood Test

- Total IgE Test

- Component-Resolved Diagnostics (CRD)

- Basophil Activation Test (BAT)

By Product

- Consumables

- Allergen Extracts

- Test Kits

- Reagents

- Assay Plates

- Disposable Materials

- Instruments

- Immunoassay Analyzers

- ELISA Analyzers

- Automated Allergy Testing Platforms

- Services

- Diagnostic Testing Services

- Laboratory Services

- Allergy Screening Programs

By Allergen Type

- Inhaled Allergens

- Pollen

- Dust Mites

- Mold

- Pet Dander

- Food Allergens

- Milk

- Egg

- Peanut

- Tree Nuts

- Shellfish

- Wheat

- Drug Allergens

- Antibiotics

- NSAIDs

- Other Drug Allergies

- Other Allergens

By Technology

- Immunoassay Technology

- Molecular Allergy Diagnostics

- Skin Testing Devices

- Point-of-Care Diagnostics

By End User

- Diagnostic Laboratories

- Hospitals

- Allergy & Immunology Clinics

- Academic & Research Institutes

Impact of Artificial Intelligence in the Global Allergy Diagnostic Market

Artificial intelligence is increasingly transforming the global allergy diagnostic market by enhancing the accuracy, speed, and efficiency of allergen detection. AI powered algorithms are being integrated into immunoassay analyzers, laboratory information management systems, and digital diagnostic platforms to analyze complex patient data, identify patterns in immune responses, and predict potential allergic reactions. Machine learning models can process large datasets from blood tests, skin testing, and patient histories to provide more precise allergen profiling and risk assessment. This reduces human error, enables early diagnosis, and supports personalized treatment planning. Additionally, AI assists in optimizing laboratory workflows, automating data interpretation, and improving predictive modeling for allergy trends. As healthcare providers adopt AI driven diagnostic solutions, the market is expected to see accelerated growth, greater operational efficiency in laboratories, and improved clinical outcomes for patients with complex or multiple allergies.

Artificial intelligence is also driving innovation in the development of next generation allergy diagnostic tools by enabling predictive and preventive healthcare approaches. AI based analytics can integrate environmental data, genetic information, and patient lifestyle factors to forecast the likelihood of allergic reactions and guide early interventions. This technology supports personalized immunotherapy by identifying the most relevant allergens for individual patients and monitoring treatment effectiveness over time. Furthermore, AI facilitates remote and digital allergy monitoring, allowing clinicians to track patient responses in real time and adjust care plans accordingly. The incorporation of AI into allergy diagnostics is therefore expanding the scope of precision medicine, improving patient safety, and creating new growth opportunities within the global market.

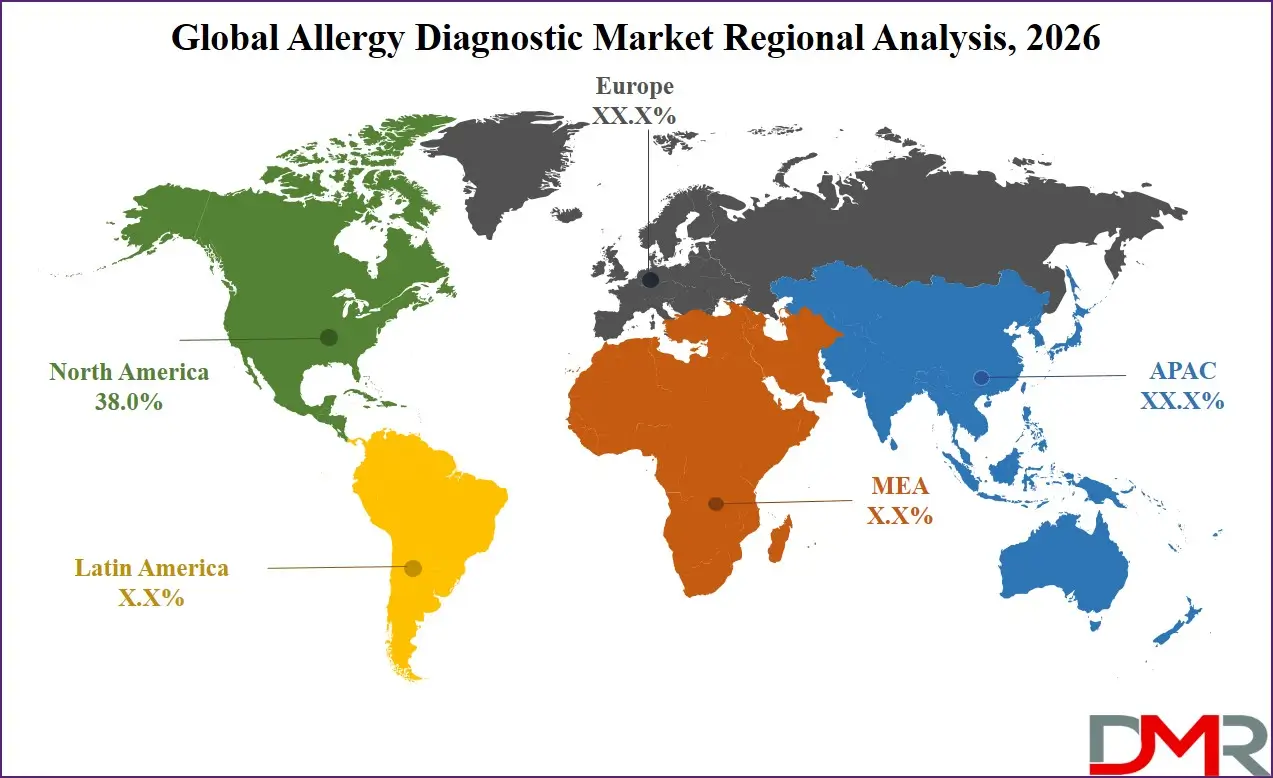

Global Allergy Diagnostic Market: Regional Analysis

Region with the Largest Revenue Share

North America is expected to lead the global allergy diagnostic market, accounting for approximately 38.0% of total market revenue in 2026. The region’s dominance is driven by a high prevalence of allergic disorders, including allergic rhinitis, asthma, and food allergies, as well as widespread awareness about early detection and preventive care. Well established healthcare infrastructure, advanced diagnostic laboratories, and strong adoption of immunoassay and molecular allergy testing technologies contribute to market growth. Increasing healthcare expenditure, the presence of key industry players, and ongoing research in clinical immunology further strengthen North America’s position as the largest regional market for allergy diagnostics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

The Asia Pacific region is expected to register the highest compound annual growth rate in the global allergy diagnostic market over the forecast period. Rapid urbanization, increasing environmental pollution, and changing dietary patterns are contributing to a rising prevalence of allergic conditions in countries such as China, India, and Japan. Expanding healthcare infrastructure, growing awareness about allergy testing, and the establishment of modern diagnostic laboratories are accelerating the adoption of advanced immunoassay and molecular diagnostic technologies. These factors, combined with increasing investments in healthcare and laboratory services, are driving strong market growth in the region.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Allergy Diagnostic Market: Competitive Landscape

The competitive landscape of the global allergy diagnostic market is characterized by intense innovation, strategic collaborations, and continuous product development focused on improving diagnostic accuracy and expanding service offerings. Key players are investing in advanced immunoassay platforms, multiplex testing technologies, and enhanced reagent formulations to meet the growing demand for comprehensive allergen profiling. There is a strong emphasis on research and development to introduce high sensitivity diagnostic solutions and streamline laboratory workflows. Market dynamics are also shaped by mergers, partnerships with healthcare providers, and expanded distribution networks to increase global reach, particularly in emerging economies. As diagnostic laboratories and healthcare facilities seek more efficient and precise testing options, competition continues to drive technological adoption and the introduction of value added services across regions.

Some of the prominent players in the Global Allergy Diagnostic Market are:

- Thermo Fisher Scientific

- bioMérieux

- Siemens Healthineers

- Danaher Corporation

- PerkinElmer

- EUROIMMUN Medizinische Labordiagnostika AG

- Omega Diagnostics Group

- HYCOR Biomedical

- HOB Biotech Group

- Lincoln Diagnostics

- Minaris Medical America

- AESKU.GROUP

- R-Biopharm AG

- DASIT Group

- Stallergenes Greer

- ALK-Abelló

- Eurofins Scientific

- Neogen Corporation

- HollisterStier Allergy

- HAL Allergy Group

- Other Key Players

Recent Developments in the Global Allergy Diagnostic Market

- January 2026: GSK completed the acquisition of RAPT Therapeutics in a deal valued at approximately USD 2.2 billion, expanding its pipeline with RAPT’s IgE‑targeted therapies that aim to prevent severe food allergic reactions and align with broader immunology and allergy care strategies.

- January 2026: Reacta Healthcare, a specialist in pharmaceutical‑grade food allergy diagnostics, reported significant investment support from the Development Bank of Wales and private backers that contributed to strong sales growth and expanded clinical testing reach worldwide.

- July 2025: Thermo Fisher Scientific launched its updated ImmunoCAP multiplex allergy testing panel that enables simultaneous detection of more than 40 common allergens, enhancing throughput and diagnostic precision for clinical laboratories handling large patient volumes.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 7.9 Bn |

| Forecast Value (2035) |

USD 20.4 Bn |

| CAGR (2026–2035) |

11.1% |

| The US Market Size (2026) |

USD 2.5 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Test Type (In-Vivo Tests, In-Vitro Tests), By Product (Consumables, Instruments, Services), By Allergen Type (Inhaled Allergens, Food Allergens, Drug Allergens, Other Allergens), By Technology (Immunoassay Technology, Molecular Allergy Diagnostics, Skin Testing Devices, Point-of-Care Diagnostics), By End User (Diagnostic Laboratories, Hospitals, Allergy & Immunology Clinics, Academic & Research Institutes) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Thermo Fisher Scientific, bioMérieux, Siemens Healthineers, Danaher Corporation, PerkinElmer, EUROIMMUN Medizinische Labordiagnostika AG, Omega Diagnostics Group, HYCOR Biomedical, HOB Biotech Group, Lincoln Diagnostics, Minaris Medical America, AESKU.GROUP, R-Biopharm AG, DASIT Group, Stallergenes Greer, ALK-Abelló, Eurofins Scientific, Neogen Corporation, HollisterStier Allergy, HAL Allergy Group, and other key players. |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Allergy Diagnostic Market?

▾ The Global Allergy Diagnostic Market size is estimated to have a value of USD 7.9 billion in 2026 and is expected to reach USD 20.4 billion by the end of 2035.

What is the growth rate in the Global Allergy Diagnostic Market in 2026?

▾ The market is growing at a CAGR of 11.1% over the forecasted period of 2026.

What is the size of the US Allergy Diagnostic Market?

▾ The US Allergy Diagnostic market is projected to be valued at USD 2.5 billion in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 6.2 billion in 2035 at a CAGR of 10.4%.

Which region accounted for the largest Global Allergy Diagnostic Market?

▾ North America is expected to have the largest market share in the Global Allergy Diagnostic Market with a share of about 38.0% in 2026.

Who are the key players in the Global Allergy Diagnostic Market?

▾ Some of the major key players in the Global Allergy Diagnostic Market are Thermo Fisher Scientific, bioMérieux, Siemens Healthineers, Danaher Corporation, PerkinElmer, EUROIMMUN Medizinische Labordiagnostika AG, Omega Diagnostics Group, HYCOR Biomedical, and many others.