Market Overview

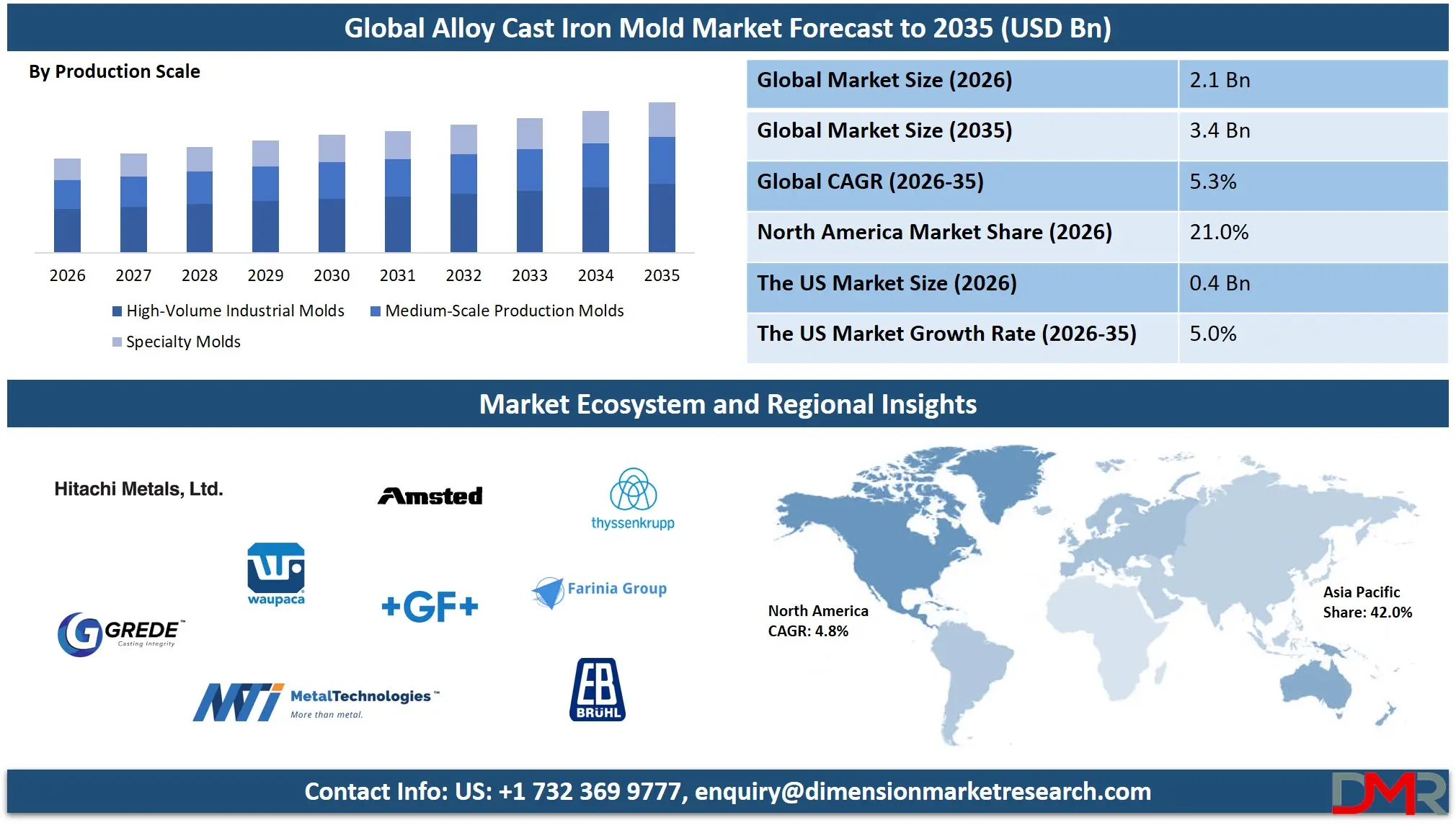

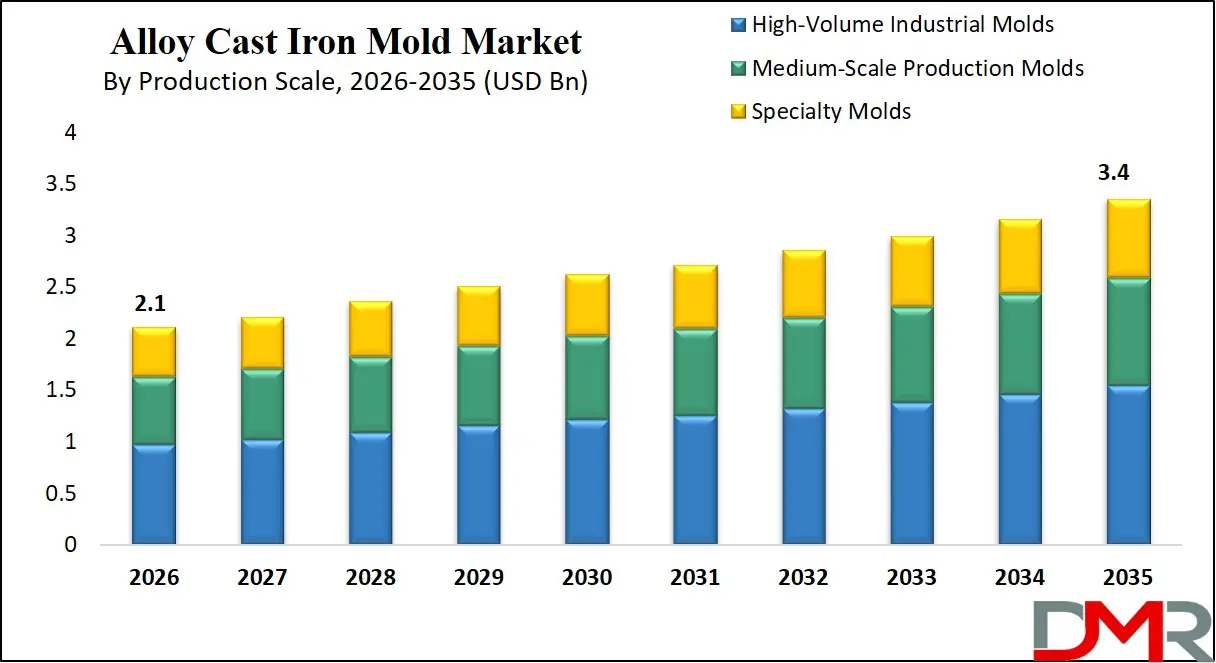

The global Alloy Cast Iron Mold market is expected to reach USD 2.1 billion in 2026 and is projected to grow at a CAGR of 5.3% from 2026 to 2035, reaching approximately USD 3.4 billion by 2035, driven by rising demand for industrial casting molds, metal casting tools, foundry equipment, and automotive component manufacturing.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

An alloy cast iron mold is a durable industrial mold produced from cast iron that contains alloying elements such as chromium, nickel, molybdenum, or silicon to enhance mechanical strength, wear resistance, and thermal stability. These molds are widely used in metal casting and glass forming processes where repeated exposure to high temperatures and molten materials requires exceptional dimensional stability and resistance to thermal fatigue. Alloy cast iron molds are valued for their ability to maintain precise shapes while supporting consistent production cycles in foundries and manufacturing plants. Their enhanced hardness and corrosion resistance make them suitable for producing complex industrial components, automotive parts, machine elements, and engineered metal products in high volume manufacturing environments.

The global Alloy Cast Iron Mold Market refers to the worldwide industry involved in the manufacturing, supply, and utilization of alloy based cast iron molds used in metal casting, industrial tooling, and heavy manufacturing operations. This market includes foundries, mold manufacturers, and industrial equipment producers that design molds capable of supporting repetitive casting processes across automotive, machinery, construction equipment, and energy sectors. Increasing demand for durable casting molds that can withstand high thermal stress and deliver consistent product quality is supporting market growth across both developed and emerging manufacturing economies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growth in the global Alloy Cast Iron Mold Market is strongly influenced by expanding industrial production, rising automotive component manufacturing, and advancements in foundry technologies. Manufacturers are increasingly adopting high performance alloy compositions and precision mold engineering to improve productivity, reduce mold wear, and enhance casting accuracy. Additionally, the integration of automated casting systems, improved metallurgical processes, and demand for complex metal parts in sectors such as infrastructure, transportation, and industrial equipment is creating sustained demand for alloy cast iron molds across global manufacturing hubs.

The US Alloy Cast Iron Mold Market

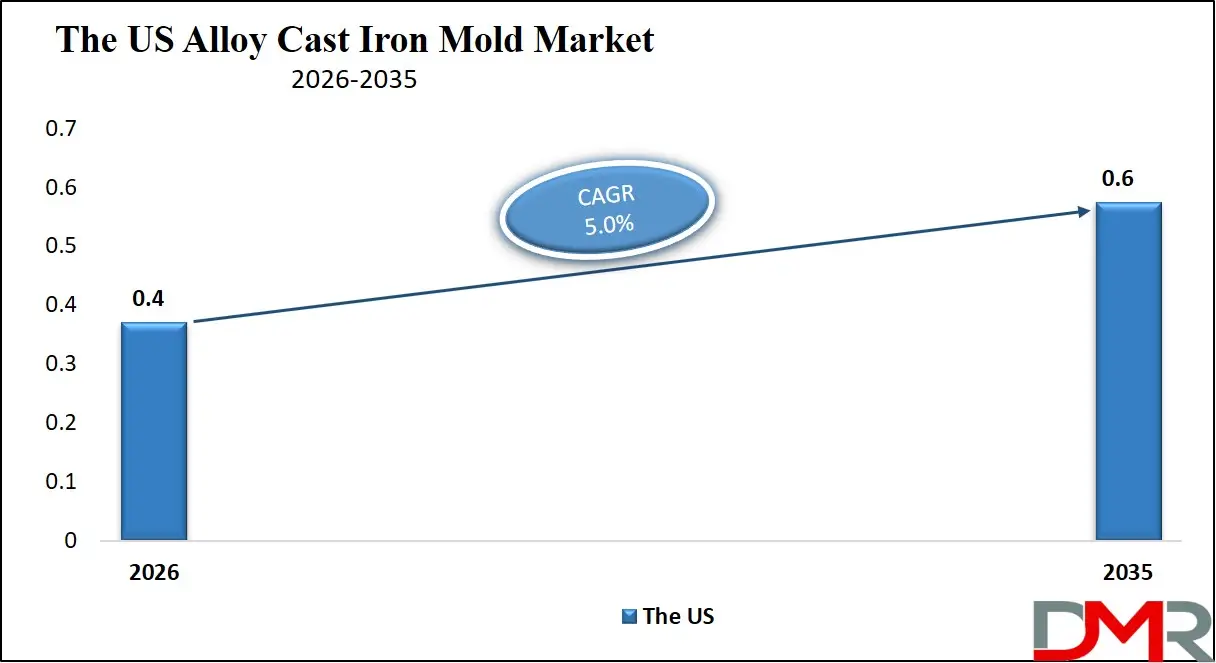

The U.S. Alloy Cast Iron Mold Market size is expected to reach at USD 0.4 billion in 2026. It is further expected to witness subsequent growth in the upcoming period, holding USD 0.6 billion in 2035 at a CAGR of 5.0%.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Alloy Cast Iron Mold Market is a key segment of the North American foundry and industrial tooling industry, driven primarily by high demand in the automotive, machinery, and heavy equipment sectors. Manufacturers focus on producing durable and high-precision alloy cast iron molds capable of withstanding repeated thermal cycles and mechanical stress. Advanced metallurgical processes and alloy compositions such as chromium, nickel, and molybdenum enhance mold performance, ensuring dimensional accuracy and extended service life. The market is supported by both established foundries and specialized mold manufacturing companies catering to diverse industrial applications.

Growth in the US market is further propelled by technological advancements in casting and mold-making processes, including automation, precision engineering, and smart manufacturing solutions. Increasing investment in automotive production, industrial machinery, and energy infrastructure has elevated the demand for high-quality alloy cast iron molds that deliver consistent casting quality. Rising adoption of sustainable and energy-efficient manufacturing practices is encouraging manufacturers to develop molds with improved wear resistance, thermal stability, and longevity, reinforcing the US market's position as a major contributor to the global alloy cast iron mold industry.

The Europe Alloy Cast Iron Mold Market

The Europe alloy cast iron market is projected to reach USD 480 million in 2026, reflecting steady demand across automotive, industrial machinery, and construction equipment manufacturing. The growth is supported by well-established foundries and industrial players that focus on producing high-precision, durable molds capable of withstanding repeated thermal cycles and delivering consistent casting quality. Advanced metallurgical techniques and investments in automation and digital foundry solutions are also contributing to the region's market value, ensuring that manufacturers can meet strict European industrial standards efficiently.

The market in Europe is expected to grow at a CAGR of 4.7%, driven by continuous modernization of foundries, the adoption of high-performance alloy compositions, and increasing demand for energy-efficient and durable molds. Automotive component production, in particular, remains a major driver, as manufacturers seek molds that provide dimensional accuracy and reduce defect rates. Additionally, rising industrial infrastructure projects and investments in heavy machinery further support moderate but consistent growth in the European alloy cast iron mold market over the forecast period.

The Japan Alloy Cast Iron Mold Market

The Japan alloy cast iron mold market is projected to reach USD 170 million in 2026, supported by the country's strong automotive, industrial machinery, and precision equipment sectors. Japanese foundries emphasize high-quality and durable molds that maintain dimensional accuracy under repeated thermal and mechanical stress, which is critical for producing engine components, transmission parts, and heavy machinery elements. The presence of technologically advanced manufacturing facilities and a focus on precision engineering contributes to the steady demand for alloy cast iron molds in the region.

The market in Japan is expected to grow at a CAGR of 4.5%, driven by ongoing industrial automation, adoption of advanced metallurgical alloys, and investments in smart foundry solutions. Rising production of automotive and industrial components, along with infrastructure development, encourages manufacturers to use high-performance molds that offer wear resistance, thermal stability, and extended service life. Continuous innovation and efficiency improvements in Japanese foundries are key factors sustaining moderate growth in the alloy cast iron mold market over the forecast period.

Global Alloy Cast Iron Mold Market: Key Takeaways

- Market Size and Growth: The global alloy cast iron mold market is projected to reach USD 2.1 billion in 2026 and is expected to grow at a CAGR of 5.3%, reaching approximately USD 3.4 billion by 2035, highlighting a strong and sustained demand for industrial and automotive casting molds.

- Regional Market Dominance: Asia Pacific leads the market with a 42.0% share of total global revenue in 2026, supported by rapid industrialization, automotive expansion, and large-scale foundries, positioning the region as both the largest and fastest-growing market globally.

- Segment Leadership: In 2026, gray iron alloy molds dominate the alloy type segment with 40% market share, while high-volume industrial molds capture 46.0% of the production scale segment, reflecting the industry's emphasis on durable molds for large-scale automotive and machinery manufacturing.

- Key National Markets: The Europe market is projected at USD 480 million in 2026 with a CAGR of 4.7%, whereas the Japan market is expected to reach USD 170 million with a CAGR of 4.5%, indicating steady industrial demand in established economies.

- Application Focus: Automotive component casting accounts for 50% of the application segment in 2026, while foundries and metal casting plants dominate the end-user segment with 52% share, emphasizing the critical role of alloy cast iron molds in high-volume, precision-driven production environments.

Global Alloy Cast Iron Mold Market: Use Cases

- Automotive Component Casting: Alloy cast iron molds are extensively used in automotive manufacturing for engine blocks, brake components, and structural parts. Their thermal stability and wear resistance ensure precise, high-volume production, supporting consistent metal casting and foundry operations. The durability of these molds reduces maintenance costs and enhances casting accuracy for critical automotive components.

- Industrial Machinery and Equipment Production: Heavy machinery and industrial equipment manufacturers rely on alloy cast iron molds to produce gears, housings, and mechanical components. The high strength and dimensional stability of these molds ensure long service life, enabling repeatable precision in casting industrial tools and metal parts.

- Energy and Power Sector Applications: In power generation and energy equipment manufacturing, alloy cast iron molds are used for turbine components, pump housings, and boiler parts. Their resistance to thermal fatigue and high-temperature corrosion makes them suitable for producing durable and reliable components for energy infrastructure.

- Construction and Infrastructure Casting: Construction equipment and infrastructure projects use alloy cast iron molds for heavy-duty components such as crane parts, valves, and pipe fittings. The molds' high hardness and abrasion resistance allow large-scale casting with consistent quality, meeting the stringent demands of industrial construction applications.

Global Alloy Cast Iron Mold Market: Stats & Facts

- U.S. Geological Survey — Iron & Steel Industry Statistics: Iron and steel comprise about 95% of all the tonnage of metal produced annually in the United States and globally, indicating the foundational role of iron castings in industrial production.

- Eurostat — Industrial Production (EU): In 2024, the value of sold industrial production in the European Union was €5 860 billion, with decreases in motor vehicles, machinery, and fabricated metal products compared with 2023.

- Eurofer — European Steel in Figures: The European crude steel production data (2023) shows EU producers manufactured 126.3 million tonnes of crude steel, reflecting broader regional metal production trends critical to cast iron casting supply.

- World Steel Association (Global Crude Steel Production): In 2023, world crude steel production was approximately 1.85 billion tonnes, underscoring the scale of raw material supply essential for cast iron and steel cast products.

- Strong Global Manufacturing Output (UNIDO–World Bank Data): According to UNIDO manufacturing output data for 2023, China produced ~28.7% of the world's total manufacturing output, with the U.S., Germany, Japan, and India following — highlighting geographic influence on metal casting capacity and demand.

Global Alloy Cast Iron Mold Market: Market Dynamic

Driving Factors in the Global Alloy Cast Iron Mold Market

Rising Automotive Manufacturing Demand

Rising demand from automotive manufacturing is fueling the global alloy cast iron mold market. High-precision molds are essential for producing engine blocks, brake systems, and chassis components, where dimensional stability and thermal resistance are critical. The expansion of electric vehicle production and advanced automotive manufacturing has further encouraged foundries to adopt durable alloy molds, supporting high-volume, consistent metal casting and reducing operational downtime.

Technological Advancements in Foundries

Advancements in foundry and casting technologies are also driving market growth. Precision molding techniques, automated casting systems, and improved metallurgical processes enhance mold performance, durability, and casting accuracy. Manufacturers benefit from reduced wear, extended service life, and higher output efficiency, making alloy cast iron molds increasingly attractive for industrial production, heavy machinery, and construction equipment applications.

Restraints in the Global Alloy Cast Iron Mold Market

High Production and Maintenance Costs

The high cost of manufacturing and maintaining alloy cast iron molds can limit adoption, especially for small and medium-scale foundries. The requirement for specialized alloy compositions, precision machining, and regular maintenance increases operational expenses, which may reduce the overall market growth in regions with limited industrial budgets.

Complexity of Mold Design

Designing alloy cast iron molds for high-performance industrial applications requires advanced engineering expertise. Complexity in mold design, combined with stringent dimensional accuracy requirements, can create barriers for manufacturers and slow adoption, particularly in emerging markets with limited technical infrastructure.

Opportunities in the Global Alloy Cast Iron Mold Market

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and Africa present significant growth opportunities. Increasing industrialization, automotive production, and infrastructure development in these regions drive demand for high-quality alloy cast iron molds. Local foundries and international suppliers can capitalize on this growth by offering durable, precision-engineered molds.

Adoption of Advanced Manufacturing Techniques

The integration of additive manufacturing, 3D-printed cores, and smart foundry solutions opens new opportunities for improving mold efficiency. These technologies reduce lead time, enhance mold design flexibility, and allow manufacturers to produce complex components with improved wear resistance and thermal stability.

Trends in the Global Alloy Cast Iron Mold Market

Focus on High-Durability and Wear-Resistant Molds

There is a growing trend toward producing molds with enhanced wear resistance and thermal stability. Manufacturers are increasingly using alloying elements such as chromium, nickel, and molybdenum to improve mold lifespan and casting consistency, particularly for automotive, industrial machinery, and energy applications.

Integration of Automation and Smart Foundry Solutions

Automation and smart foundry technologies are becoming prevalent, enabling precise casting, real-time process monitoring, and predictive maintenance. This trend enhances operational efficiency, reduces defects, and supports large-scale industrial production, driving adoption of high-performance alloy cast iron molds globally.

Global Alloy Cast Iron Mold Market: Research Scope and Analysis

By Alloy Type Analysis

In the alloy type segment of the global alloy cast iron mold market, gray iron alloy molds are anticipated to dominate, capturing 40.0% of the total market share in 2026. This dominance is attributed to their excellent thermal conductivity, machinability, and ability to maintain dimensional stability under repeated high-temperature casting operations. Gray iron molds are widely used in automotive, industrial machinery, and construction equipment manufacturing because they provide consistent casting quality, reduce maintenance requirements, and support high-volume production. Their reliability and durability make them the preferred choice for many foundries worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Ductile iron alloy molds also play a significant role in this market segment due to their superior mechanical strength, flexibility, and resistance to cracking compared to gray iron. They are increasingly adopted in applications requiring higher impact resistance and durability, such as heavy machinery components, automotive structural parts, and industrial equipment castings. The enhanced toughness and dimensional stability of ductile iron molds allow manufacturers to produce complex shapes and extend mold life, making them an attractive option for modern foundries alongside gray iron molds.

By Manufacturing Technology Analysis

In the manufacturing technology segment of the global alloy cast iron mold market, sand mold systems are expected to dominate, capturing 34.0% of the total market share in 2026. Their widespread adoption is driven by versatility, cost-effectiveness, and suitability for producing large and complex castings in both low and high-volume production. Sand molds offer excellent thermal insulation, allowing controlled metal solidification, which ensures high-quality castings with minimal defects. They are commonly used in automotive components, industrial machinery, and construction equipment, where flexibility and rapid mold preparation are crucial for meeting diverse casting requirements.

Permanent mold systems also hold an important position in this segment, as they are designed for repeated use in high-precision casting applications. These molds, typically made from durable metals, provide excellent surface finish and dimensional accuracy while reducing post-processing requirements. Permanent mold systems are widely utilized in automotive, aerospace, and industrial equipment manufacturing where consistency and long-term durability are essential. Their ability to support medium to high-volume production while maintaining tight tolerances makes them a preferred choice for foundries seeking efficiency and quality in alloy cast iron mold operations.

By Casting Process Type Analysis

In the casting process type segment of the global alloy cast iron mold market, metal component casting molds are expected to dominate, capturing 44.0% of the total market share in 2026. These molds are widely used in the production of automotive parts, industrial machinery components, and heavy equipment due to their ability to withstand high temperatures and repeated casting cycles. Their excellent dimensional stability, wear resistance, and thermal conductivity ensure precise metal flow and consistent quality across high-volume manufacturing operations. The reliability of metal component casting molds makes them a preferred choice for foundries seeking efficiency and long-term performance.

Glass container molds also play a significant role in this market segment, particularly in the production of bottles, jars, and other glass packaging. These molds require high precision and thermal resistance to shape molten glass accurately and maintain consistent wall thickness. Alloy cast iron molds used for glass containers are designed to endure repeated thermal cycles while providing smooth surface finishes and maintaining dimensional accuracy. The growing demand for packaged beverages, pharmaceuticals, and food products has driven the adoption of glass container molds, making them an important component of the overall casting process segment.

By Production Scale Analysis

In the production scale segment of the global alloy cast iron mold market, high-volume industrial molds are anticipated to dominate, capturing 46.0% of the total market share in 2026. These molds are widely used in large-scale manufacturing operations, particularly in the automotive, industrial machinery, and heavy equipment sectors, where consistent production and repeatability are critical. Their durability, thermal stability, and resistance to wear enable manufacturers to produce large quantities of components with high precision, reducing downtime and maintenance costs. High-volume molds are essential for meeting global industrial demand efficiently while ensuring consistent casting quality.

Medium-scale production molds also hold a notable position in this segment, serving industries that require moderate production volumes with a balance between cost and efficiency. These molds are commonly employed in specialized machinery, custom automotive components, and niche industrial applications where flexibility and precision are important but production volumes are not as extensive as in large-scale operations. Medium-scale molds offer adequate thermal resistance, dimensional stability, and extended service life, making them suitable for foundries that prioritize moderate output while maintaining high-quality standards in their casting processes.

By Application Analysis

In the application segment of the global alloy cast iron mold market, automotive components casting is anticipated to dominate, capturing 50.0% of the total market share in 2026. This dominance is driven by the high demand for engine blocks, brake systems, transmission parts, and structural components, which require molds that can withstand repeated thermal cycles and deliver consistent dimensional accuracy. Alloy cast iron molds provide the strength, wear resistance, and thermal stability necessary for high-volume automotive production, ensuring precise metal flow and reducing defect rates. The growing global automotive industry, including electric vehicle manufacturing, continues to support the extensive use of these molds.

Industrial machinery and equipment also represent a significant portion of the market, as alloy cast iron molds are used to produce gears, housings, and structural components for heavy machinery and manufacturing equipment. These molds offer high durability, thermal resistance, and dimensional precision, enabling manufacturers to meet stringent quality standards for industrial operations. The demand for reliable, long-lasting molds in this sector is driven by the need for efficiency, consistent output, and reduced maintenance in industrial production processes, making this application a critical contributor to the overall market.

By End-User Analysis

In the end-user segment of the global alloy cast iron mold market, foundries and metal casting plants are anticipated to dominate, capturing 52.0% of the total market share in 2026. These facilities are the primary users of alloy cast iron molds, as they specialize in producing a wide range of metal components for automotive, industrial machinery, construction equipment, and energy applications. The durability, wear resistance, and thermal stability of these molds enable foundries to maintain high-volume production while ensuring consistent dimensional accuracy and casting quality. Their extensive use in large-scale industrial operations reinforces their dominance in the end-user segment.

Automotive OEMs and Tier-1 suppliers also play a significant role in this market segment, as they rely on alloy cast iron molds for producing engine parts, transmission components, brake systems, and structural assemblies. These end-users prioritize molds that offer high precision, long service life, and consistent quality to meet strict automotive manufacturing standards. The growing automotive sector, including the rise of electric vehicles and advanced vehicle platforms, continues to drive the adoption of these molds among OEMs and Tier-1 suppliers, making them a key contributor to market growth.

The Global Alloy Cast Iron Mold Market Report is segmented on the basis of the following:

By Alloy Type

- Gray Iron Alloy Molds

- Ductile Iron Alloy Molds

- White Iron Alloy Molds

- Malleable Iron Alloy Molds

- High-Alloy Cast Iron Molds

By Manufacturing Technology

- Sand Mold Systems

- Permanent Mold Systems

- Shell Mold Casting

- Resin-Bonded Mold Systems

- Die Mold Systems

- Automated Mold Systems

By Casting Process Type

- Metal Component Casting Molds

- Glass Container Molds

- Heavy Industrial Equipment Casting Molds

- Precision Tooling & Engineering Molds

- Specialty Industrial Casting Molds

By Production Scale

- High-Volume Industrial Molds

- Medium-Scale Production Molds

- Specialty Molds

By Application

- Automotive Components Casting

- Industrial Machinery & Equipment

- Construction & Infrastructure Components

- Energy & Power Equipment

- Aerospace & Defense Components

- Rail, Marine & Heavy Transport

- Others

By End-User

- Foundries & Metal Casting Plants

- Automotive OEM & Tier-1 Suppliers

- Industrial Manufacturing Companies

- Tooling & Mold Manufacturing Firms

- Engineering & Infrastructure Companies

Impact of Artificial Intelligence in the Global Alloy Cast Iron Mold Market

The impact of artificial intelligence in the global alloy cast iron mold market is becoming increasingly significant as manufacturers integrate AI-driven solutions to enhance production efficiency, quality, and predictive maintenance. AI technologies enable foundries and mold manufacturers to optimize casting processes by analyzing real-time data on temperature, metal flow, and mold wear, which reduces defects and improves dimensional accuracy. Predictive analytics powered by AI can forecast mold fatigue or failure, allowing timely maintenance and reducing downtime, thus extending the service life of alloy cast iron molds.

AI is also transforming mold design and production by enabling simulation-based modeling and digital twin technologies. Manufacturers can simulate complex casting processes, identify potential defects, and optimize alloy composition and mold geometry before physical production, reducing material waste and production costs. In addition, machine learning algorithms support automated quality inspection, process control, and workflow optimization in high-volume industrial and automotive casting operations. The adoption of AI in the alloy cast iron mold market is driving higher productivity, consistency, and cost-effectiveness across automotive, industrial machinery, energy, and construction equipment sectors.

Global Alloy Cast Iron Mold Market: Regional Analysis

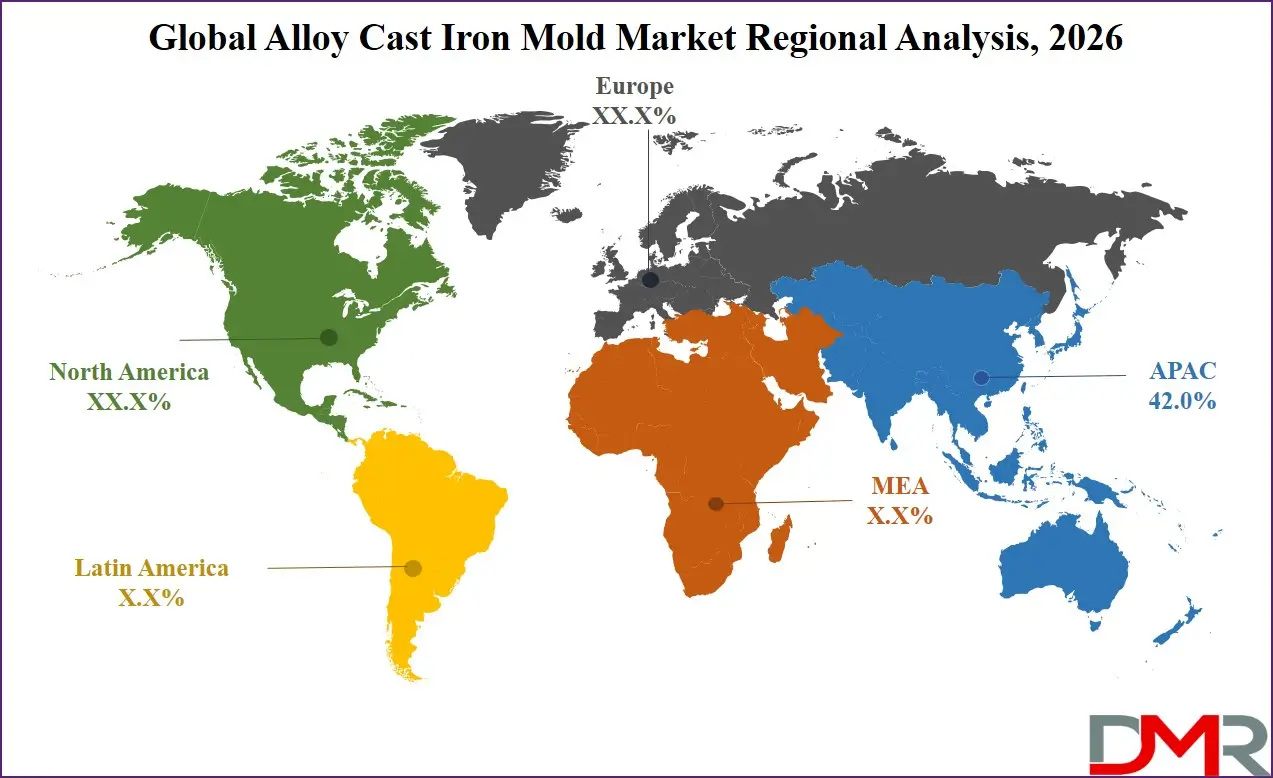

Region with the Largest Revenue Share

Asia Pacific is anticipated to lead the global alloy cast iron mold market landscape, capturing 42.0% of total global market revenue in 2026. This regional dominance is driven by rapid industrialization, strong growth in automotive manufacturing, and expanding infrastructure and heavy machinery production in countries such as China, India, and Japan. The presence of large-scale foundries, increasing adoption of advanced casting technologies, and rising demand for high-precision, durable molds across automotive, industrial equipment, and construction sectors contribute to the region's significant market share. Robust manufacturing activities and cost-effective production capabilities further reinforce Asia Pacific's leadership in the global market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

The Asia Pacific region is expected to register the highest CAGR in the global alloy cast iron mold market during the forecast period, driven by rapid industrial expansion, growing automotive production, and increasing demand for heavy machinery and construction equipment. Countries such as China, India, and Japan are investing heavily in advanced foundry technologies and high-precision mold manufacturing to support large-scale industrial and automotive casting operations. The combination of rising manufacturing activities, cost-effective production, and adoption of modern alloy compositions and automation solutions positions Asia Pacific as the fastest-growing region in the global market.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Alloy Cast Iron Mold Market: Competitive Landscape

The competitive landscape of the global alloy cast iron mold market is shaped by a mix of established foundry specialists, advanced tooling manufacturers, and regional industrial players who focus on innovation, quality, and customization to meet diverse casting requirements. Key participants are investing in research and development to enhance mold design, improve alloy compositions, and integrate automation and digital manufacturing solutions that boost efficiency and durability. Competition is also driven by the ability to offer value‑added services such as precision engineering, rapid prototyping, and after‑sales support, which help foundries and OEMs achieve consistent casting performance and reduce production costs in automotive, industrial, and energy sectors. Continuous focus on strategic partnerships, capacity expansion, and technological advancements underscores the dynamic nature of this market's competitive environment.

Some of the prominent players in the Global Alloy Cast Iron Mold Market are:

- Hitachi Metals Ltd.

- Waupaca Foundry

- Grede Holdings LLC

- Metal Technologies Inc.

- Amsted Industries Incorporated

- Georg Fischer Ltd.

- Thyssenkrupp AG

- Farinia Group

- Eisenwerk Brühl GmbH

- Neenah Foundry Company

- Dotson Iron Castings

- Aarrowcast Inc.

- Cadillac Casting Inc.

- Dandong Foundry

- Brakes India Private Limited

- Castings PLC

- ZOLLERN GmbH & Co. KG

- Electrosteel Castings Limited

- MAT Foundry Group Ltd.

- Harrison Castings Ltd.

- Other Key Players

Recent Developments in the Global Alloy Cast Iron Mold Market

- November 2025: A historic cast iron foundry manufacturer was acquired by a larger pipe and foundry business, integrating its cast iron utility product capabilities and expanding infrastructure manufacturing reach.

- October 2025: A major industrial company signed an agreement to divest its iron foundry operation in Leipzig as part of its strategic transformation, transferring the facility to another global manufacturing firm focused on advanced mobility and industrial solutions.

- October 2025: Foundry Lab introduced a new direct 3D metal casting service combining 3D printing with traditional casting to deliver metal parts faster and reduce lead times by enabling digital metal casting production.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2.1 Bn |

| Forecast Value (2035) |

USD 3.4 Bn |

| CAGR (2026–2035) |

5.3% |

| The US Market Size (2026) |

USD 0.4 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Alloy Type (Gray Iron Alloy Molds, Ductile Iron Alloy Molds, White Iron Alloy Molds, Malleable Iron Alloy Molds, High-Alloy Cast Iron Molds), By Manufacturing Technology (Sand Mold Systems, Permanent Mold Systems, Shell Mold Casting, Resin-Bonded Mold Systems, Die Mold Systems, Automated Mold Systems), By Casting Process Type (Metal Component Casting Molds, Glass Container Molds, Heavy Industrial Equipment Casting Molds, Precision Tooling & Engineering Molds, Specialty Industrial Casting Molds), By Production Scale (High-Volume Industrial Molds, Medium-Scale Production Molds, Specialty Molds), By Application (Automotive Components Casting, Industrial Machinery & Equipment, Construction & Infrastructure Components, Energy & Power Equipment, Aerospace & Defense Components, Rail, Marine & Heavy Transport, Others), and By End-User (Foundries & Metal Casting Plants, Automotive OEM & Tier-1 Suppliers, Industrial Manufacturing Companies, Tooling & Mold Manufacturing Firms, Engineering & Infrastructure Companies) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Hitachi Metals Ltd., Waupaca Foundry, Grede Holdings LLC, Metal Technologies Inc., Amsted Industries Incorporated, Georg Fischer Ltd., Thyssenkrupp AG, Farinia Group, Eisenwerk Brühl GmbH, Neenah Foundry Company, Dotson Iron Castings, Aarrowcast Inc., Cadillac Casting Inc., Dandong Foundry, Brakes India Private Limited, Castings PLC, ZOLLERN GmbH & Co. KG, Electrosteel Castings Limited, MAT Foundry Group Ltd., Harrison Castings Ltd., and other key players. |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Alloy Cast Iron Mold Market?

▾ The Global Alloy Cast Iron Mold Market size is estimated to have a value of USD 2.1 billion in 2026 and is expected to reach USD 3.4 billion by the end of 2035.

What is the growth rate in the Global Alloy Cast Iron Mold Market in 2026?

▾ The market is growing at a CAGR of 5.3% over the forecasted period of 2026.

What is the size of the US Alloy Cast Iron Mold Market?

▾ The US Alloy Cast Iron Mold market is projected to be valued at USD 0.4 billion in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 0.6 billion in 2035 at a CAGR of 5.0%.

Which region accounted for the largest Global Alloy Cast Iron Mold Market?

▾ Asia Pacific is expected to have the largest market share in the Global Alloy Cast Iron Mold Market with a share of about 42.0% in 2026.

Who are the key players in the Global Alloy Cast Iron Mold Market?

▾ Some of the major key players in the Global Alloy Cast Iron Mold Market are Hitachi Metals Ltd., Waupaca Foundry, Grede Holdings LLC, Metal Technologies Inc., Amsted Industries Incorporated, Georg Fischer Ltd., Thyssenkrupp AG, Farinia Group, Eisenwerk Brühl GmbH, Neenah Foundry Company, Dotson Iron Castings, Aarrowcast Inc., and many others.