Market Snapshot

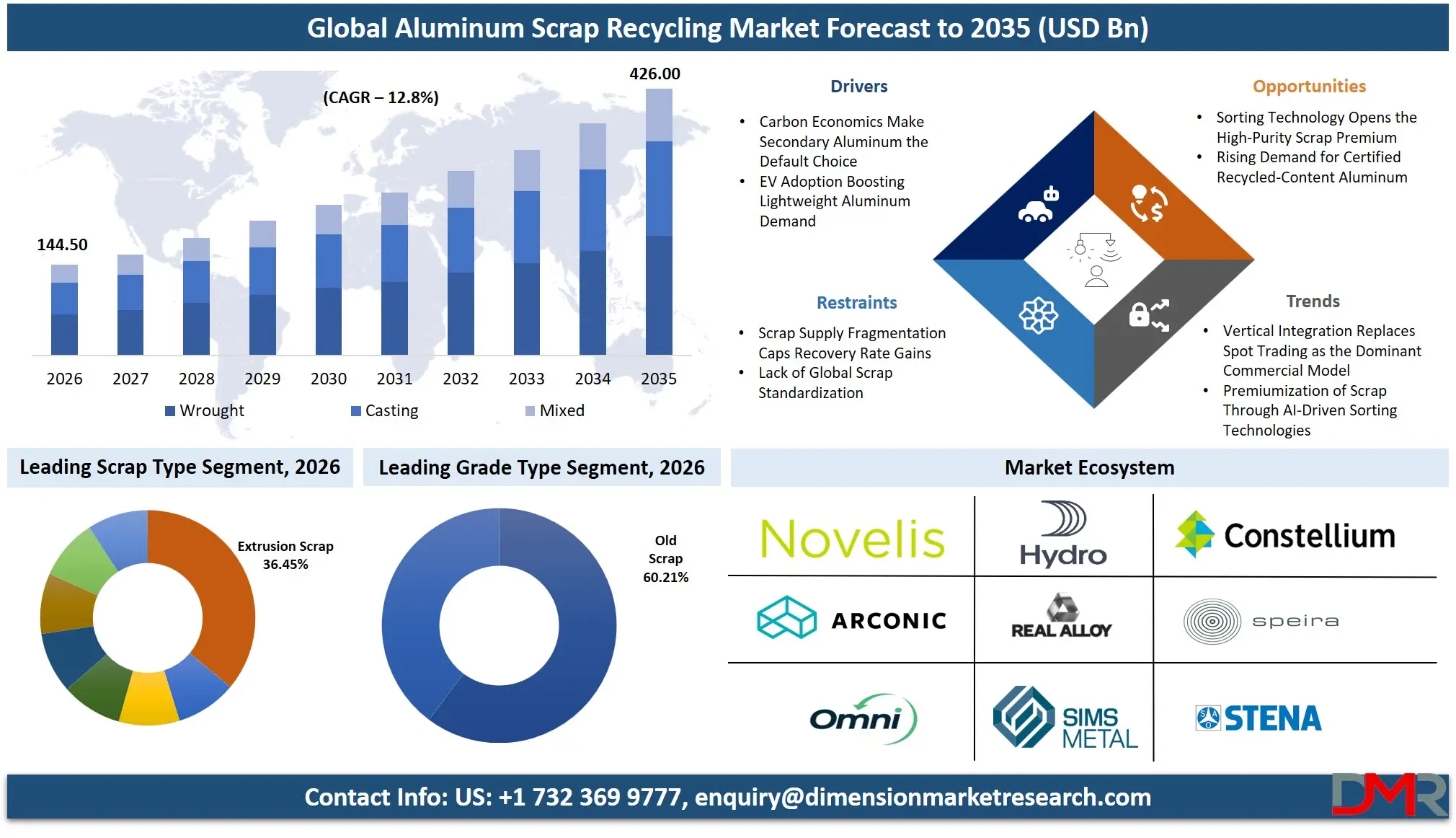

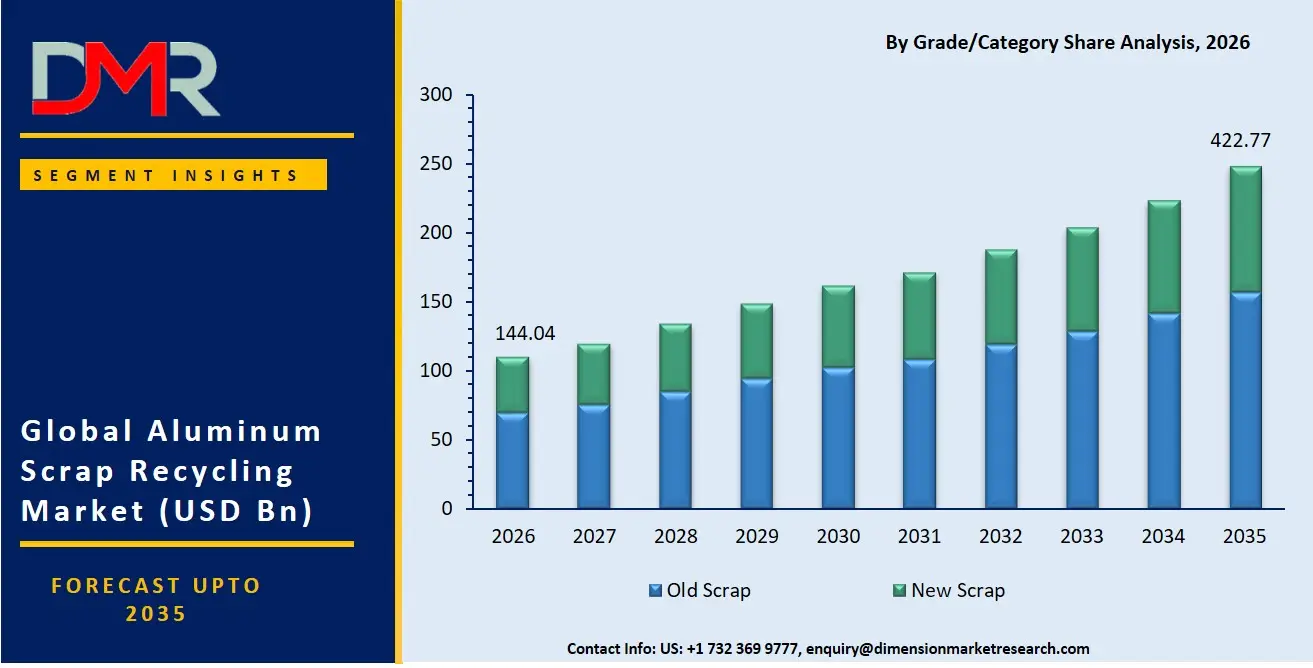

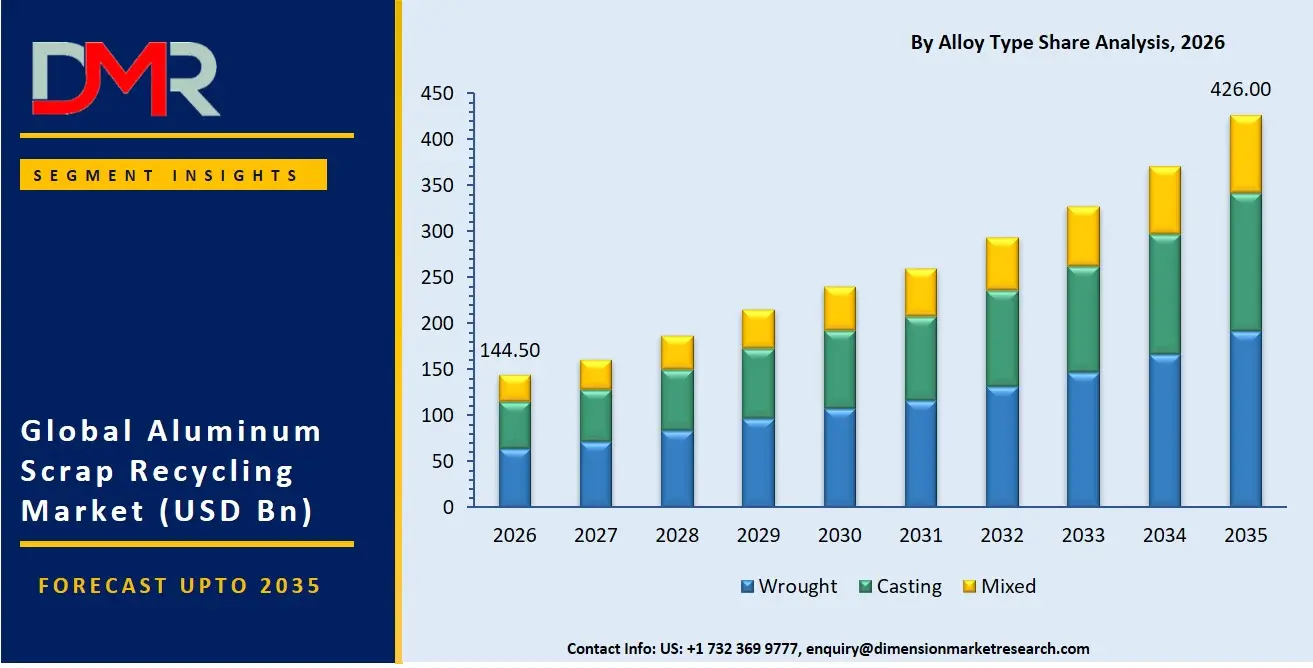

- The Aluminum Scrap Recycling Market size is USD 127.7 Billion in 2025, reached USD 144.04 Billion in 2026, and is projected to hit USD 422.77 Billion by 2035 at a CAGR of 12.8%.

- Old Scrap leads the By Grade segment with a 60.52% share in 2026.

- Wrought alloy holds a 58.23% share in the By Alloy Type segment, reflecting the strong pull from automotive and packaging end-uses.

- Extrusion Scrap accounts for a 36.24% share in the By Scrap Type segment, the largest single product type.

- Building and Construction holds a 28.5% share in the By Application segment.

- Asia Pacific is the dominant region with a 42.81% revenue share, with China accounting for 22.1% of the global market.

- New (Manufacturing) Scrap supplies 62.8% of recovered aluminum by source.

Market Overview

The Global Aluminum Scrap Recycling Market covers the collection, sorting, processing, and remelting of post-consumer and manufacturing aluminum waste into secondary aluminum metal and alloys. The market spans multiple scrap grades including old scrap from post-consumer sources and new scrap from industrial manufacturing operations. End products serve the automotive, packaging, construction, electrical, aerospace, and consumer appliance industries. Primary aluminum smelting, bauxite mining, and virgin aluminum trading fall outside Aluminum Scrap Recycling Market's scope.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Secondary aluminum has become the structural backbone of the global aluminum supply chain, not a peripheral recycling activity. As reported by AlCircle, global aluminum scrap recycling reached approximately 41.9 million tonnes in 2026. Recycled aluminum requires roughly 95% less energy than primary production, which means every tonne of scrap processed delivers a hard cost advantage that primary smelters cannot match on operating economics alone. For industrial buyers under carbon disclosure pressure, this energy differential is no longer just an environmental argument. It is a procurement driver that tilts sourcing decisions toward secondary metal at scale.

The market sits at a structural inflection point where decarbonization policy, manufacturing nearshoring, and sensor-based sorting technology are converging. The EU Carbon Border Adjustment Mechanism, effective January 2026, assigns an embedded-emission benchmark of 1.423 t CO₂ per tonne for primary aluminum versus just 0.091 t CO₂ per tonne for secondary aluminum. This regulatory pricing gap rewards recyclers with a carbon cost advantage exceeding 90% over primary producers, which will accelerate the shift of European manufacturing demand toward scrap-based supply chains through the forecast period.

Market Size and Forecast

The Global Aluminum Scrap Recycling Market size is estimated at USD 144.04 Billion in 2026 from USD 127.7 Billion in 2025, and is projected to reach USD 422.77 Billion by 2035, exhibiting a CAGR of 12.8% during the forecast period.

The forecast rests on two structural supports that are unlikely to reverse within the decade. First, tightening carbon regulations in Europe and parallel sustainability mandates from automotive and packaging OEMs are locking secondary aluminum into long-term supply contracts. Second, processing technology improvements, particularly deep-learning sensor sorting, are lifting scrap yield quality to levels that were previously achievable only through primary production. Higher-purity scrap commands premium pricing, which expands the revenue base of the market faster than volume growth alone would suggest.

The primary downside risk is scrap supply tightness. Global aluminum scrap trade reached only 9.95 million tonnes in the first ten months of 2025, a 3% year-on-year gain that trails the pace needed to match projected secondary production growth. If collection infrastructure does not scale in parallel with processing capacity, margin compression at the smelting stage becomes a real constraint on revenue realization through 2030.

Market Dynamics

Carbon Economics Make Secondary Aluminum the Default Choice

The EU CBAM benchmark assigns a carbon cost of 1.423 t CO₂ per tonne to primary aluminum and just 0.091 t CO₂ per tonne to secondary aluminum. European manufacturers sourcing primary metal now face an embedded carbon liability that recyclers do not carry. This is not a soft preference for green supply chains. It is a hard cost line that will show up in procurement budgets starting in 2026.

The automotive sector reinforces this pressure from the demand side. Recycled aluminum already covers nearly 44% of total aluminum used in global transportation. As automakers commit to lifecycle carbon targets under regulatory mandates, their supplier qualification criteria will increasingly require secondary aluminum certificates. Recyclers who can deliver certified low-carbon metal at automotive-grade purity will hold pricing power that commodity scrap traders cannot match.

Scrap Supply Fragmentation Caps Recovery Rate Gains

Despite an overall recycling efficiency rate of approximately 76%, the remaining 24% of aluminum goes unrecovered, largely because collection infrastructure is geographically uneven. Post-consumer scrap from construction demolition and consumer appliances is difficult to aggregate at commercially viable volumes outside organized urban collection systems. This gap between theoretical recovery potential and actual scrap availability creates a ceiling on secondary production growth that processing technology alone cannot fix.

Salt furnace dross recovery adds a secondary constraint. Dross still contains 30-70% recoverable metal, but reclaiming it requires rotary salt furnace operations that generate hazardous salt cake waste. Facilities without licensed disposal infrastructure lose recoverable yield, which reduces effective output per tonne of scrap processed. Closing this gap requires capital investment in waste handling, not just furnace upgrades.

Sorting Technology Opens the High-Purity Scrap Premium

TOMRA's GAINnext deep-learning sorting system, launched in 2025, is the first application of deep learning in metals sorting. It separates low-alloy cast fractions from wrought fractions with precision that conventional optical sorters cannot achieve. Recyclers using this technology can supply wrought-equivalent scrap to automotive sheet producers, a segment that previously required primary aluminum blending to meet alloy specifications.

Sortera's second Tennessee facility, opened in May 2026 with capacity to process 240 million pounds of material at 90-100% aluminum purity, illustrates how technology-enabled recyclers are repositioning toward premium markets. With aluminum prices up approximately 20% at the time of that facility opening, the economics of high-purity sorting become compelling for new entrants willing to invest in AI-integrated processing lines.

Market Trends

Vertical Integration Replaces Spot Trading as the Dominant Commercial Model

The wave of acquisitions in 2024 through 2026, including EGA's purchases of Leichtmetall, Spectro Alloys, and Eco Green, Derichebourg's move on Scholz, and CP Group's acquisition of Recycleye, signals that large aluminum producers are no longer content to buy scrap on spot markets. They are acquiring the collection, sorting, and processing infrastructure directly. This shift compresses margins for independent scrap traders and creates higher barriers for new entrants who cannot match the capital deployed by integrated players. Early movers who build proprietary scrap collection networks in underserved regions, particularly in Southeast Asia and South Asia where urban aluminum stock is accumulating rapidly, will hold a structural supply advantage that cannot be replicated through spot purchasing strategies.

By Grade / Category Analysis

In 2026, Old Scrap held a dominant market position in the By Grade / Category segment of the Aluminum Scrap Recycling Market, with a 60.52% share. Post-consumer aluminum from end-of-life vehicles, demolished buildings, and discarded packaging represents the largest and most structurally important scrap feedstock. The scale of this segment reflects decades of aluminum accumulation in durable goods now reaching end-of-life cycles, particularly in North America and Europe where vehicle fleet turnover and building renovation activity are highest.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

New Scrap, generated directly from manufacturing operations as offcuts, trimmings, and process rejects, holds the remaining share. Although smaller by volume, new scrap commands a quality premium because its alloy composition is known and consistent, reducing remelting complexity and yield loss. The coexistence of both grades in active supply chains means recyclers who can handle both feedstocks efficiently operate at structurally lower input costs than those dependent on a single grade.

By Scrap Type / Product Type Analysis

With a 36.24% share, Extrusion Scrap holds the strongest position in the By Scrap Type segment, reflecting the volume of aluminum profiles consumed in construction, automotive, and industrial applications that return as recoverable scrap at predictable intervals. Extrusion scrap is relatively clean and alloy-consistent, which reduces sorting costs and supports higher recovery yields compared to mixed-stream inputs.

Aluminum Cans (UBC) represent the most recycled product type by cycle frequency, returning to the supply chain within 60 days on established collection systems. Cast aluminum, Sheet Aluminum, Wire Scrap, Foil, Turnings and Borings, and Ingot Returns each serve distinct downstream alloy specifications. Turnings and Borings, generated by machining operations, carry higher contamination risk from cutting fluids, which increases preprocessing cost. Foil is thin-gauge and energy-intensive to sort, making collection economics marginal unless volumes are large. Wire Scrap, by contrast, has high copper contamination risk that requires careful separation before melting. The diversity of scrap types across this segment means that processing flexibility, not just melting capacity, determines competitive advantage for recyclers operating at scale.

By Alloy Type Analysis

Wrought alloys account for a 58.23% share of the By Alloy Type segment, driven by the dominant use of wrought aluminum in automotive body panels, beverage cans, and aerospace structures where precise alloy composition is non-negotiable. Wrought-grade scrap commands the highest remelting premium precisely because maintaining alloy integrity through the recycling process requires clean feedstock and controlled furnace conditions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Casting alloys hold a meaningful share, serving die-cast automotive components, engine blocks, and industrial housings where tolerances on composition are broader and mixed feedstocks are more commercially acceptable. Mixed alloy scrap, the lowest-purity grade, typically feeds secondary casting foundries that blend inputs to specification. As deep-learning sorting technology improves the ability to separate wrought from cast fractions at input, the Mixed category faces structural volume pressure. Scrap that previously entered the mixed stream will increasingly be upgraded to the higher-value wrought or casting categories, redistributing margin upward in the processing chain.

By Application Analysis

Automotive leads all application segments by revenue, a position supported by the sector's consumption of 12.2-12.5 million tonnes of secondary aluminum globally in 2024, as confirmed by AluminiumChina. Vehicle lightweighting mandates across North America, Europe, and China have made recycled aluminum structurally embedded in body-in-white design rather than an optional substitution. Automakers specifying secondary aluminum in long-term supplier agreements effectively lock volume commitments that give recyclers revenue visibility unusual in commodity markets.

Building and Construction holds a 28.5% application share, the second-largest segment, supplied primarily through demolition scrap recovery as aging infrastructure and commercial real estate undergoes renovation. Packaging, including beverage cans and foil, feeds the highest-frequency recycling loop in the market. Electrical and Electronics, Aerospace and Defense, Machinery and Equipment, and Consumer Appliances round out the application base, each requiring different alloy grades. Aerospace remains the most stringent buyer, accepting only the highest-purity secondary feedstock, which makes it a small-volume but high-value segment for recyclers capable of meeting certification requirements.

By Recovered Aluminum Source Analysis

New (Manufacturing) Scrap captures a 62.8% share of recovered aluminum by source, reflecting the high volumes of process scrap generated in aluminum fabrication, stamping, and machining operations that return to the supply chain at known composition and minimal contamination. Manufacturing facilities with integrated scrap return loops effectively operate closed-cycle aluminum systems, reducing raw material costs and improving alloy consistency in output.

Old (Post-Consumer) Scrap accounts for the remaining share and represents the higher-growth recovery opportunity over the forecast period. As the global installed base of aluminum in vehicles, buildings, and consumer goods ages, post-consumer scrap volumes will expand structurally regardless of near-term production cycles. The constraint on realizing that potential is collection infrastructure, not material availability. Regions that build out municipal and industrial scrap collection systems before this wave peaks will capture disproportionate supply and processing margin through 2035.

Key Market Segments

By Grade / Category

By Scrap Type / Product Type

- Cast Aluminum

- Aluminum Cans (UBC)

- Foil

- Extrusion Scrap

- Sheet Aluminum

- Wire Scrap

- Turnings & Borings

- Ingot Returns

By Alloy Type

By Source

- Industrial

- Household

- Commercial

- Construction & Demolition Waste

By Recycling Process / Method

- Melting & Casting

- Collection

- Sorting

- Shredding & Granulation

- Baling

- Sensor-Based Sorting

By Recovered Aluminum Source

- New (Manufacturing) Scrap

- Old (Post-Consumer) Scrap

By Application

- Automotive

- Building & Construction

- Packaging

- Electrical & Electronics

- Aerospace & Defense

- Machinery & Equipment

- Consumer Appliances

By Scrap Trade Flow

- Imported Scrap

- Domestically Recovered Scrap

Regional Analysis

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In 2026, Asia Pacific held a dominant position with a 42.81% revenue share of the global market. China alone accounted for 22.1% of global market revenue and recorded secondary aluminum consumption of 13.35 million tonnes in 2025, up 5.1% year-on-year. China's dominance reflects both the scale of its aluminum manufacturing base, which generates large volumes of new scrap internally, and its active import program. Chinese aluminum scrap imports rose 12.2% year-on-year in the first eleven months of 2025 to 1.8 million tonnes, confirming that domestic scrap generation alone cannot satisfy its secondary production appetite.

Europe holds the second-largest regional position, bolstered by CBAM-driven demand for low-carbon secondary aluminum and a dense industrial base in Germany, France, and Italy generating consistent manufacturing scrap. North America, anchored by the US automotive and beverage can recycling infrastructure, benefits from high UBC collection rates and proximity to automaker supply chains. Latin America and the Middle East and Africa represent the regions with the largest gaps between aluminum stock accumulation and current recovery infrastructure. The UAE is an exception: EGA's February 2026 commissioning of a 185,000 tonne per year recycling plant in Al Taweelah signals that Gulf producers are repositioning from primary-only operations toward integrated secondary production. That strategic shift, if replicated across the region, could materially alter the MEA share balance before 2030.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The market is moderately consolidated at the top tier, with a small number of vertically integrated producers controlling significant scrap processing and remelting capacity across multiple geographies. The competitive pattern visible in 2024 through 2026 is one of deliberate consolidation: large producers are acquiring mid-size and specialist recyclers to secure captive scrap supply rather than competing on spot markets. This strategy reflects a structural shift in how leading players price their competitive advantage. Scrap access, not just melting capacity, has become the primary moat.

Mid-tier and independent recyclers face a narrowing competitive window. Technology-led differentiators, particularly AI-based sorting systems that enable high-purity output, are emerging as the tool that allows smaller operators to compete on product quality rather than scale. Those who cannot invest in sorting technology risk being repositioned as feedstock suppliers to larger integrated processors rather than finished secondary aluminum producers. The acquisition of AI sorting specialist Recycleye by CP Group in April 2026 confirms that technology capability is now a direct acquisition target, not just an operational improvement initiative.

Company Profiles

Novelis Inc. operates as the world's largest aluminum rolling and recycling company, with a stated target of sourcing 75% of its input from recycled aluminum. Its August 2024 investment of USD 50 million to expand the Ulsan Aluminum joint venture in South Korea lifted regional capacity above 440,000 tonnes per year, while the USD 90 million Latchford UK expansion, with bag houses commissioned in January 2026, directly doubles used-beverage-can processing capacity. Novelis's strategy of co-locating recycling capacity with rolling mills locks in supply chain continuity that pure-play recyclers cannot offer to the same customer base.

Emirates Global Aluminium (EGA) has executed the most aggressive recycling expansion program of any single player in Aluminum Scrap Recycling Market between 2024 and 2026. Acquisitions of Leichtmetall in Germany, Spectro Alloys in the US for USD 80 million, and the pending 80% stake in Italy's Eco Green, combined with the February 2026 commissioning of a 185,000 tonne per year plant in Abu Dhabi, show a deliberate build-out of secondary aluminum capacity across three continents. The December 2025 announcement of a USD 170 million German plant expansion adding 110,000 tonnes of sorting and 153,000 tonnes of melting capacity extends that footprint through 2028. EGA's risk is integration complexity across diverse regulatory and operational environments simultaneously.

Key Players

- Novelis Inc.

- Norsk Hydro ASA

- Constellium SE

- Arconic Corporation

- Real Alloy Holding GmbH

- RUSAL

- OmniSource Corporation

- Sims Metal Management

- Century Aluminum Company

- Kaiser Aluminum

- AMAG Austria Metall AG

- Matalco Inc.

- Speira GmbH

- Stena Metall AB

- Alcoa Corporation

- Ye Chiu Group

- UACJ Corporation

- European Metal Recycling (EMR)

- Tomra Systems ASA

- Aurubis AG

- China Hongqiao Group Limited

- Hindalco Industries Limited

- Kobe Steel Ltd.

- Raffmetal

- Jain Metal Group

Supply Chain and Value Chain Analysis

The aluminum scrap recycling value chain begins at scrap generation points across post-consumer and manufacturing sources, flows through collection and aggregation networks, then into sorting and preprocessing facilities before reaching remelting and casting operations. Maximum value is created at the sorting and alloy-separation stage. A recycler who can deliver wrought-certified scrap to an automotive sheet mill captures a price premium that traders passing unsorted mixed scrap to secondary foundries cannot. The gap between commodity scrap pricing and certified-alloy scrap pricing is where processing technology investment pays back most directly.

The most significant bottleneck sits between collection and sorting. Scrap must be shredded to under 150 mm to optimize melting surface area, then sorted by alloy type before entering rotary or reverberatory furnaces operating at 700°C to 800°C. Facilities lacking sensor-based sorting capability blend scrap inputs and accept yield losses and alloy dilution as a cost of doing business. Salt furnace dross, containing 30-70% recoverable metal, represents a second value recovery point that many facilities fail to capture fully due to hazardous waste handling costs. Supply chain participants who close both the sorting gap and the dross recovery gap simultaneously will operate at structurally higher margins than those addressing only furnace throughput.

Regulatory Landscape

The EU Carbon Border Adjustment Mechanism (CBAM), effective January 2026, is the single most consequential regulatory development for Aluminum Scrap Recycling Market in the forecast period. The mechanism assigns embedded-emission benchmarks of 1.423 t CO₂ per tonne for primary aluminum versus 0.091 t CO₂ per tonne for secondary aluminum. European importers of primary aluminum now carry a carbon cost liability that secondary aluminum suppliers do not. This benchmark difference exceeds 90% in carbon advantage for recycled metal, which effectively functions as a regulatory tariff on primary aluminum entering Europe and a structural subsidy for recyclers supplying the same market.

Beyond CBAM, extended producer responsibility frameworks in Germany, France, and the UK are tightening collection mandates for aluminum packaging and construction waste, expanding the legally recoverable scrap pool available to licensed recyclers. India's regulatory environment is also shifting: Gravita India's March 2026 acquisition of a 98.95% stake in Rashtriya Metal Industries Limited signals that domestic recyclers are positioning ahead of anticipated formal scrap classification and import rules. Markets without clear regulatory frameworks for scrap trade classification, particularly across Southeast Asia and parts of Latin America, create both arbitrage opportunity and compliance risk for operators building cross-border sourcing networks.

Investment and White Space Analysis

Capital deployment in Aluminum Scrap Recycling Market is concentrating in two areas: high-purity sorting infrastructure and geographic expansion into secondary aluminum-deficit regions. EGA's combined investment across Spectro Alloys, the Al Taweelah plant, and the German expansion exceeds USD 450 million across 2024 through 2028, targeting markets where recycled aluminum supply is structurally short relative to manufacturing demand. Sortera's Tennessee facility opening in May 2026 with 240 million pounds of annual capacity, timed alongside a roughly 20% rise in aluminum prices, confirms that investors are treating technology-enabled recycling as a defensible industrial asset, not a commodity play.

The clearest white space sits in South and Southeast Asia. India's secondary aluminum sector remains fragmented and largely informal, yet the country's manufacturing base in automotive and consumer appliances is expanding rapidly. Organized recyclers with certified alloy output and formal collection networks face minimal competition from integrated global players in this geography today. Latin America carries a similar profile: large aluminum stock in end-of-life vehicles and construction material, limited formal recovery infrastructure, and no dominant integrated player controlling supply. Both regions offer early-mover advantages in collection network development that will be significantly harder to replicate once consolidation accelerates post-2027.

Recent Developments

- May 2026: Derichebourg Environnement signed an agreement to acquire Germany's Scholz group, expected to close in the second half of 2026 pending regulatory approval.

- June 2026: CMR Green Technologies launched a ₹630.88 crore IPO with a price band of ₹182–₹192, opening June 3 and closing June 5, with BSE and NSE listing expected June 10, 2026.

- April 2026: CP Group acquired a majority stake in UK-based AI vision-sorting company Recycleye, combining it with CP Group's optical sorting technologies for material recovery facilities.

- March 2026: Loacker announced plans to acquire a 50% stake in Czech non-ferrous metals recycler Saker spol. s.r.o., based in Kroměříž.

- February 2026: EGA began cast metal production at its new 185,000 tonne per year recycling plant in Al Taweelah, Abu Dhabi.

- January 2026: Novelis commissioned new bag houses at its Latchford, UK recycling centre, marking a major milestone in its USD 90 million UBC capacity expansion.

- December 2025: EGA announced a USD 170 million expansion of its German plant, adding 110,000 tonnes per year of scrap sorting and 153,000 tonnes per year of melting and casting capacity, with first hot metal expected in 2028.

- July 2025: EGA completed acquisition of Minnesota-based Spectro Alloys for USD 80 million and restarted expanded production, adding 55,000 tonnes of secondary billet capacity.

- August 2024: Novelis invested USD 50 million to expand its Ulsan Aluminum joint venture in South Korea with Kobe Steel, lifting regional capacity above 440,000 tonnes per year.

- May 2024: EGA acquired German specialty foundry Leichtmetall in Hannover, producing high-strength recycled aluminum.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 127.7 Billion |

| Market Value (2026) |

USD 144.04 Billion |

| Forecast Revenue (2035) |

USD 422.77 Billion |

| CAGR (2026–2035) |

12.8% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020–2024 |

| Forecast Period |

2026–2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Grade/Category (Old Scrap, New Scrap), By Scrap Type/Product Type (Cast Aluminum, Aluminum Cans/UBC, Foil, Extrusion Scrap, Sheet Aluminum, Wire Scrap, Turnings and Borings, Ingot Returns), By Alloy Type (Wrought, Casting, Mixed), By Source (Industrial, Household, Commercial, Construction and Demolition Waste), By Recycling Process/Method (Melting and Casting, Collection, Sorting, Shredding and Granulation, Baling, Sensor-Based Sorting), By Recovered Aluminum Source (New/Manufacturing Scrap, Old/Post-Consumer Scrap), By Application (Automotive, Building and Construction, Packaging, Electrical and Electronics, Aerospace and Defense, Machinery and Equipment, Consumer Appliances), By Scrap Trade Flow (Imported Scrap, Domestically Recovered Scrap) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

Novelis Inc., Norsk Hydro ASA, Constellium SE, Arconic Corporation, Real Alloy Holding GmbH, RUSAL, OmniSource Corporation, Sims Metal Management, Century Aluminum Company, Kaiser Aluminum, AMAG Austria Metall AG, Matalco Inc., Speira GmbH, Stena Metall AB, Alcoa Corporation, Ye Chiu Group, UACJ Corporation, European Metal Recycling (EMR), Tomra Systems ASA, Aurubis AG, China Hongqiao Group Limited, Hindalco Industries Limited, Kobe Steel Ltd., Raffmetal, Jain Metal Group |

| Customization Scope |

Customization for segments and region/country-level analysis will be provided. Additional customization can be done based on specific requirements. |

| Purchase Options |

We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User and Printable PDF). |