What is the Ambulatory Surgery Centers (ASC) Market Size?

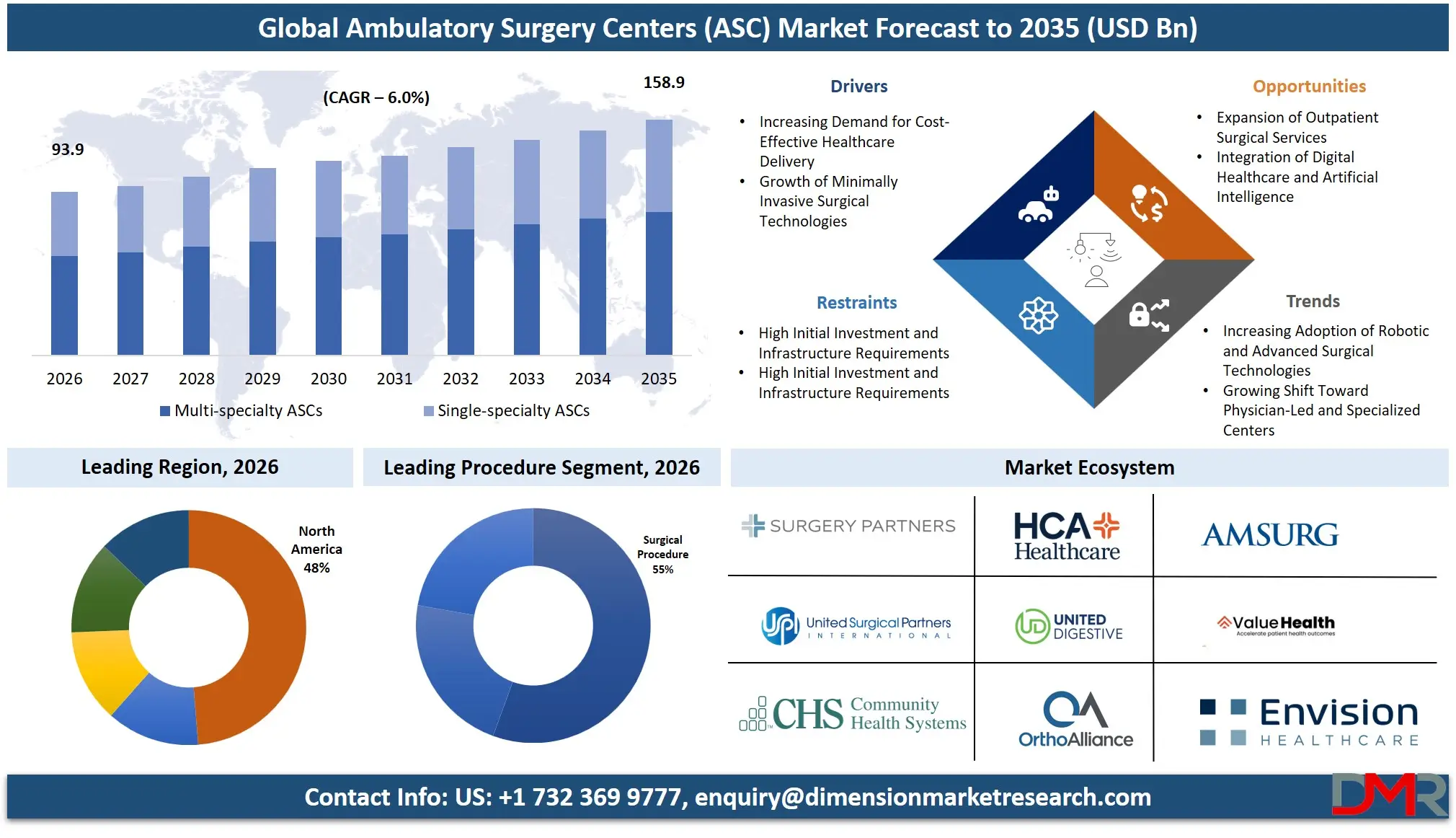

The Ambulatory Surgery Centers (ASC) Market size is expected to be USD 93.9 billion in 2026 and increase at a compound annual growth rate of 6.0% to USD 158.9 billion by 2035 due to increasing demand for cost-effective healthcare delivery.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Ambulatory Surgery Centers (ASC) market refers to healthcare facilities that provide same-day surgical and procedural services without requiring overnight hospitalization. The market includes single-specialty and multi-specialty centers, physician-owned, hospital-affiliated, and corporate-operated facilities offering diagnostic, therapeutic, and surgical procedures across various specialties. ASCs use advanced minimally invasive technologies, digital healthcare solutions, robotic-assisted surgery, and enhanced anesthesia techniques to improve patient outcomes and reduce healthcare costs. The market is gaining importance within the broader healthcare industry due to rising demand for cost-effective outpatient care, increasing surgical volumes, aging populations, and healthcare system shifts toward value-based care models globally.

The US Ambulatory Surgery Centers (ASC) Market

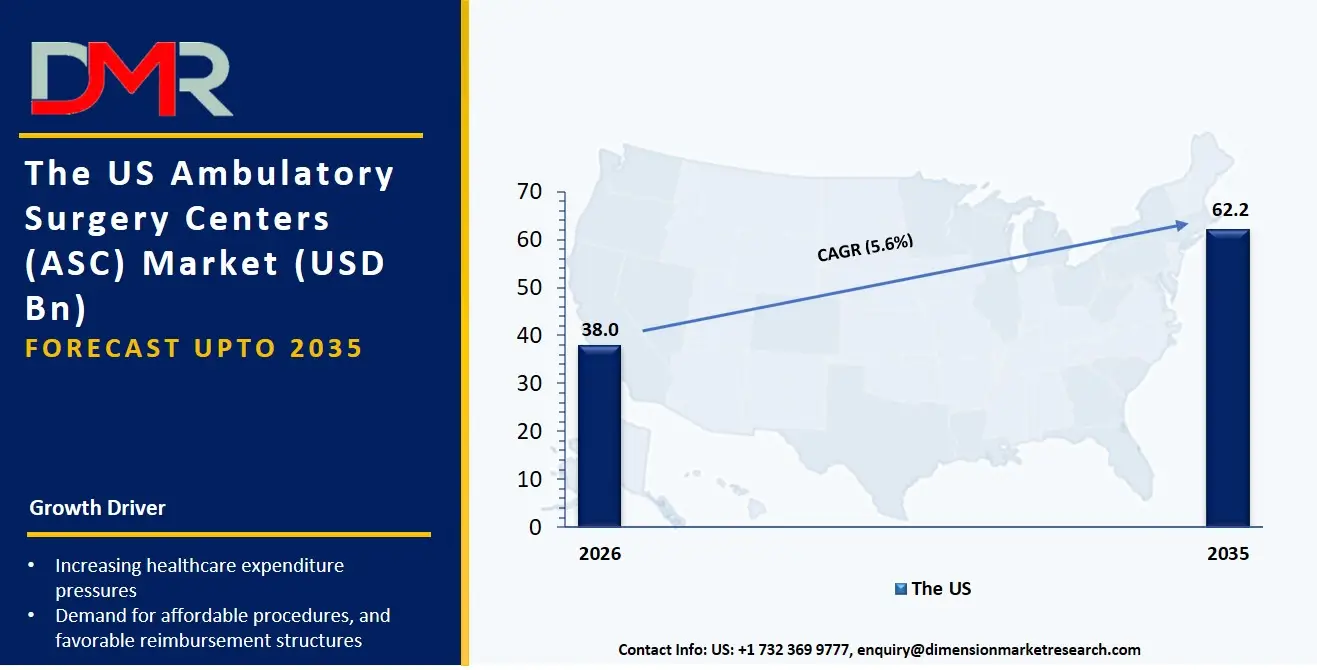

The US Ambulatory Surgery Centers (ASC) Market size is estimated to be USD 38.0 billion in 2026 and is expected to increase at a CAGR of 5.6% over the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US ASC market represents one of the most developed outpatient healthcare ecosystems, supported by increasing healthcare expenditure pressures, demand for affordable procedures, and favorable reimbursement structures. Growth is driven by Medicare expansion of covered ASC procedures, physician migration toward independent facilities, and rising adoption of minimally invasive surgeries. Hospital systems and healthcare organizations are increasingly investing in ASC networks to improve operational efficiency and reduce patient costs. Regulatory support from the Centers for Medicare & Medicaid Services (CMS), along with growing consumer preference for convenient outpatient treatment, continues to strengthen ASC adoption across specialties such as ophthalmology, orthopedics, gastroenterology, and pain management.

Europe Ambulatory Surgery Centers (ASC) Market

The Europe Ambulatory Surgery Centers (ASC) Market size is estimated to be USD 20.6 billion in 2026 and is expected to increase at a CAGR of 5.5% over the forecast period.

The European ASC market is expanding due to healthcare modernization initiatives, increasing pressure to reduce hospital waiting times, and government efforts to improve healthcare efficiency. Countries such as Germany, the United Kingdom, France, and Spain are adopting outpatient surgical models to optimize healthcare resources. Policies focused on cost containment, digital healthcare transformation, and improved patient-centered care are supporting ASC development. The growing emphasis on minimally invasive procedures, aging populations, and public-private healthcare partnerships is accelerating adoption. European healthcare reforms aligned with sustainability goals and efficient resource utilization are encouraging the transition from traditional inpatient hospitals toward specialized ambulatory care facilities.

Japan Ambulatory Surgery Centers (ASC) Market

The market size of Japan Ambulatory Surgery Centers (ASC) will be USD 3.8 billion in 2026 and at a CAGR of 5.8% in the forecast period.

The Japan ASC market is developing as healthcare providers respond to an aging population, increasing chronic disease burden, and demand for efficient medical services. Urbanization and technological advancement are encouraging the adoption of outpatient surgical models, particularly in ophthalmology, orthopedics, and gastrointestinal procedures. Government healthcare reforms aimed at controlling medical expenditure and improving service efficiency are supporting ASC growth. Japan's advanced medical technology ecosystem, including robotic surgery, imaging systems, and digital healthcare infrastructure, creates opportunities for ASC expansion. However, challenges such as strict healthcare regulations and traditional preference for hospital-based treatment influence the pace of adoption.

Key Takeaways

- Market Size & Forecast: The Ambulatory Surgery Centers (ASC) Market size is projected to reach USD 93.9 billion in 2026 and is anticipated to have a value of USD 158.9 billion in 2035.

- Growth Rate & Outlook: The Ambulatory Surgery Centers (ASC) Market size is set to grow at a compound annual growth rate of 6.0% during the forecast period of 2026 to 2035.

- Primary Growth Drivers: Some of the major growth drivers in the market are Increasing Demand for Cost-Effective Healthcare Delivery and more.

- Key Market Trends: Some of the major trends in the market are Increasing Adoption of Robotic and Advanced Surgical Technologies and more.

- By Center Type: Multi-speciality ASCs segment is anticipated to get the majority share of the Ambulatory Surgery Centers (ASC) Market in 2026.

- By Procedure Type: Surgical Procedure is expected to get the largest revenue share in 2026 in the Ambulatory Surgery Centers (ASC) Market.

- Regional Leadership: North America is set to lead the Ambulatory Surgery Centers (ASC) Market with an estimated 48.0% share in 2026.

What is the Ambulatory Surgery Centers (ASC)?

Ambulatory Surgery Centers are specialized healthcare facilities designed to perform surgical and procedural treatments that do not require hospital admission. These centers provide outpatient services using advanced medical equipment, specialized surgical teams, and efficient care models. ASCs focus on improving accessibility, reducing treatment costs, minimizing patient recovery time, and enhancing healthcare delivery through same-day procedures across multiple medical specialties.

Use Cases

- Ophthalmology Procedures: ASCs are widely used for high-volume ophthalmic procedures such as cataract surgeries, glaucoma treatments, and laser eye procedures. These centers provide specialized environments with advanced surgical equipment, shorter recovery periods, and lower operational costs compared with hospitals. The predictable nature of many eye procedures makes ophthalmology one of the strongest ASC applications.

- Orthopedic Surgeries: Orthopedic procedures including joint replacements, sports medicine treatments, and minimally invasive surgeries are increasingly shifting toward ASC settings. Advancements in anesthesia, pain management, and surgical technologies enable same-day discharge while maintaining clinical quality. Rising demand from aging populations and active lifestyles is increasing orthopedic ASC utilization.

- Gastroenterology Services: ASCs are extensively used for gastrointestinal procedures such as colonoscopies and endoscopic treatments. These facilities improve patient convenience through faster scheduling, efficient workflows, and reduced healthcare costs. Increasing colorectal cancer screening programs and preventive healthcare initiatives are contributing to greater adoption of gastroenterology-focused ASCs.

- Pain Management Procedures: Pain management ASCs provide minimally invasive treatments for chronic pain conditions, including spinal injections and nerve-related procedures. Growing prevalence of musculoskeletal disorders and demand for non-hospital-based treatments are driving expansion in this segment. Specialized facilities allow providers to deliver focused care with improved patient experience.

How AI Is Transforming the Ambulatory Surgery Centers (ASC) Market

Artificial intelligence is increasingly influencing the ASC market by improving operational efficiency, clinical decision-making, and patient management. AI-powered scheduling platforms optimize operating room utilization, reduce cancellations, and improve staff coordination. Predictive analytics helps healthcare providers forecast patient demand, manage resources, and identify potential complications before procedures. AI-assisted diagnostic tools and imaging technologies enhance accuracy, particularly in specialties such as ophthalmology, orthopedics, and gastroenterology.

AI technologies are also improving patient experiences through automated communication systems, virtual assistants, and personalized care pathways. Machine learning algorithms support post-operative monitoring by analyzing patient data and identifying recovery risks. Additionally, AI-driven administrative automation reduces documentation workload, improves billing accuracy, and supports regulatory compliance. As ASCs increasingly adopt digital healthcare solutions, artificial intelligence is expected to become a key enabler of cost reduction, quality improvement, and scalable outpatient care delivery.

Market Dynamic

Driving Factors in the Ambulatory Surgery Centers (ASC) Market

Increasing Demand for Cost-Effective Healthcare Delivery

Rising healthcare costs and increasing pressure on healthcare systems to improve affordability are major factors driving ASC market growth. ASCs typically operate with lower overhead expenses compared with hospitals, enabling reduced procedure costs for patients and payers. The shift toward value-based healthcare models encourages providers to adopt outpatient surgery approaches that maintain quality while reducing unnecessary hospitalization expenses. Insurance providers and government healthcare programs are increasingly supporting ASC procedures because of their economic advantages. Additionally, growing patient awareness regarding affordable treatment options, shorter recovery times, and convenient healthcare access is strengthening demand for ASC services globally.

Restraints in the Ambulatory Surgery Centers (ASC) Market

High Initial Investment and Infrastructure Requirements

Establishing an ASC requires substantial capital investment for facility construction, advanced surgical equipment, compliance systems, and skilled medical personnel. Smaller healthcare providers may face difficulties securing funding for technology upgrades and operational expansion. Maintaining accreditation standards, implementing safety protocols, and complying with healthcare regulations increase operational costs. These financial barriers can limit market entry, particularly in developing regions where healthcare infrastructure investment remains limited. Additionally, competition from established hospital networks with stronger financial resources creates challenges for independent ASC operators seeking expansion and market penetration.

Opportunities in the Ambulatory Surgery Centers (ASC) Market

Expansion of Outpatient Surgical Services

The increasing transition from inpatient hospital care to outpatient treatment represents a significant growth opportunity for ASC providers. Advances in surgical techniques and postoperative management are allowing more complex procedures to move into ambulatory settings. Healthcare organizations can expand service portfolios by targeting specialties such as orthopedics, cardiology, and spine surgery. Rising demand for convenient healthcare solutions among patients, combined with payer preference for lower-cost treatment environments, creates strong opportunities for ASC expansion. Emerging markets with developing healthcare infrastructure also provide opportunities for establishing modern outpatient surgical networks.

Trends in the Ambulatory Surgery Centers (ASC) Market

Increasing Adoption of Robotic and Advanced Surgical Technologies

The adoption of robotic-assisted surgery and advanced medical technologies is transforming ASC capabilities. Previously hospital-exclusive procedures are increasingly becoming suitable for outpatient environments due to improvements in surgical precision, anesthesia management, and recovery protocols. ASCs are investing in advanced equipment to attract surgeons, expand procedure offerings, and improve patient outcomes. This trend is particularly visible in specialties such as orthopedics, urology, and gynecology, where minimally invasive techniques are becoming increasingly common.

Research Scope and Analysis

The research scope analyzes the Ambulatory Surgery Centers (ASC) market through key segmentation categories, including center type, ownership, specialty, procedure, and payer. The analysis evaluates market trends, growth drivers, regional dynamics, competitive strategies, technological advancements, and future opportunities influencing ASC industry expansion.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Center Type Analysis

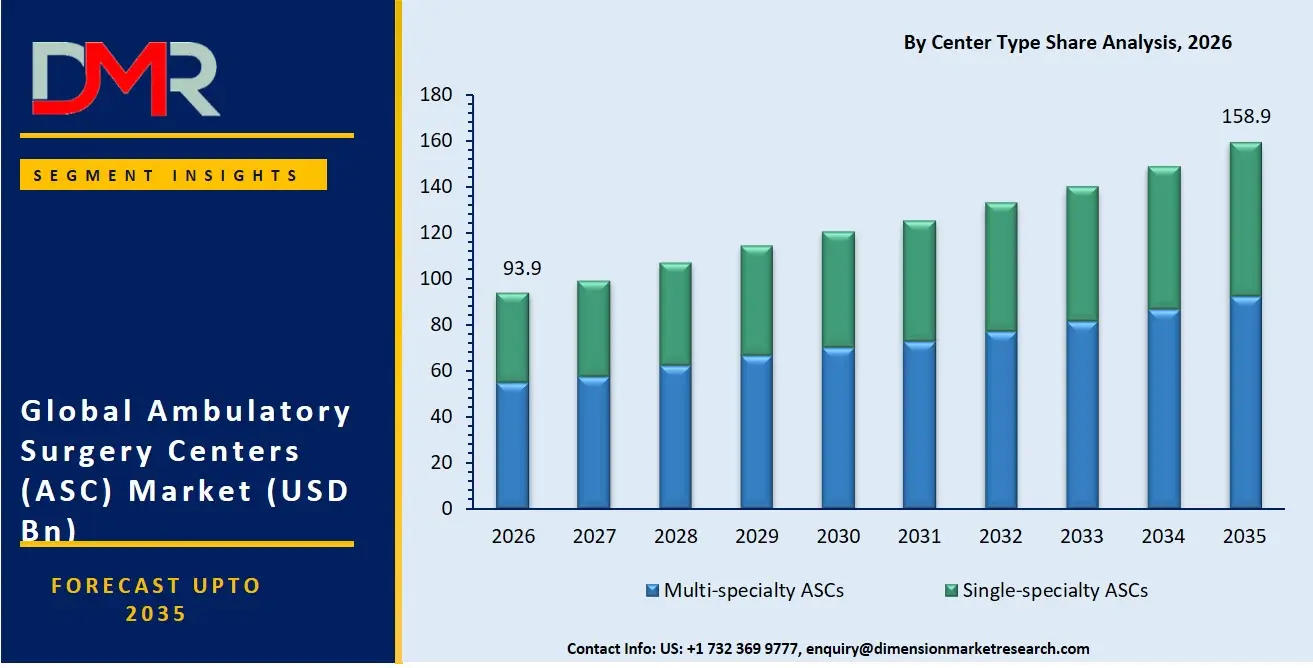

The Ambulatory Surgery Centers (ASC) market by center type is segmented into single-specialty ASCs and multi-specialty ASCs. Multi-specialty ASCs are expected to hold the leading position in 2026, accounting for an estimated 58% market share, due to their ability to provide diverse procedures across multiple medical disciplines, improve facility utilization, and attract broader patient populations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

These centers benefit from operational flexibility and economies of scale by offering specialties such as orthopedics, ophthalmology, gastroenterology, and pain management under one facility. Single-specialty ASCs remain important due to their focused expertise, streamlined workflows, and high procedural efficiency. However, multi-specialty ASCs continue to dominate because healthcare systems increasingly prefer integrated outpatient platforms. The fastest-growing segment is expected to be single-specialty ASCs focused on high-volume procedures, supported by physician ownership models and rising demand for specialized patient care. Specialty-focused facilities allow enhanced clinical expertise, optimized resource management, and improved patient satisfaction, creating expansion opportunities.

By Ownership Analysis

The ASC market by ownership includes physician-owned ASCs, hospital-owned ASCs, joint venture ASCs, and corporate-owned ASCs. Physician-owned ASCs are projected to remain the leading segment in 2026, representing an estimated 42% market share, supported by physicians' preference for greater operational control, improved scheduling flexibility, and participation in facility-generated revenue. Physician ownership encourages investment in specialized services and patient-centered care models. Joint venture ASCs are expected to be the fastest-growing segment due to increasing collaborations between healthcare systems, physicians, and investment groups. These partnerships combine hospital resources with physician expertise while reducing financial risks. Corporate-owned ASCs are also expanding through acquisition strategies and network development. The ownership landscape is shifting toward collaborative models as stakeholders seek cost efficiency, expanded service offerings, and improved competitiveness in the outpatient healthcare market.

By Specialty Analysis

The ASC market by specialty includes gastroenterology, ophthalmology, orthopedics, pain management, gynecology, urology, otolaryngology, dermatology, plastic surgery, cardiology, and other specialties. Ophthalmology is expected to maintain leadership in 2026 with an estimated 24% market share, driven by high procedure volumes, particularly cataract surgeries, predictable treatment pathways, and strong suitability for outpatient environments. Gastroenterology is another major contributor due to increasing screening programs and demand for endoscopic procedures. Orthopedics is projected to be the fastest-growing specialty segment as technological improvements enable complex procedures such as joint replacements and sports medicine surgeries to transition into ASC settings. Rising aging populations, increased prevalence of musculoskeletal conditions, and advancements in minimally invasive orthopedic techniques are supporting rapid growth. Expansion into cardiology and spine-related procedures is also creating new opportunities as regulatory approvals and technology improvements increase procedure feasibility.

By Procedure Analysis

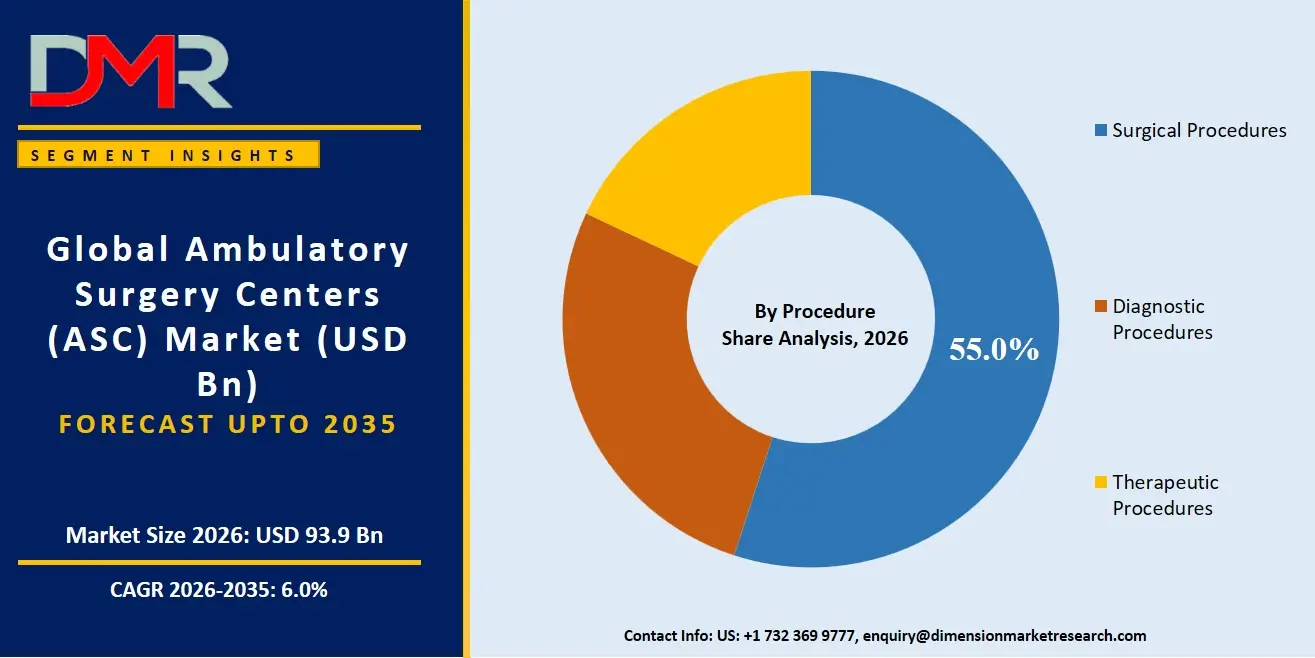

The ASC market by procedure is categorized into diagnostic procedures, therapeutic procedures, and surgical procedures. Surgical procedures are expected to dominate in 2026 with an estimated 55% market share, driven by increasing migration of outpatient surgeries from hospitals to ASCs. Advancements in anesthesia, surgical equipment, and post-operative care have enabled more complex procedures to be performed safely in ambulatory settings. Therapeutic procedures represent a rapidly growing segment due to rising demand for minimally invasive treatments, pain management services, and chronic disease interventions. Diagnostic procedures continue to support ASC growth through increasing preventive healthcare initiatives and screening programs. The fastest-growing segment is expected to be therapeutic procedures as healthcare providers expand outpatient capabilities and patients increasingly prefer convenient treatment options with shorter recovery times and lower costs.

By Payer Analysis

The ASC market by payer includes Medicare, Medicaid, private health insurance, and self-pay categories. Private health insurance is expected to lead the payer segment in 2026, accounting for an estimated 46% market share, due to broad coverage of outpatient procedures and increasing insurer preference for cost-efficient care settings. Private payers are increasingly encouraging ASC utilization because procedures performed in these facilities generally involve lower costs compared with hospital outpatient departments. Medicare remains a significant contributor, particularly in the United States, due to expanding coverage of eligible ASC procedures among older populations. The fastest-growing payer segment is expected to be Medicare, supported by increasing enrollment among aging populations and policy initiatives promoting lower-cost healthcare delivery. Medicaid expansion in several regions also provides additional growth opportunities for ASC adoption among underserved populations.

The Ambulatory Surgery Centers (ASC) Market Report is segmented on the basis of the following:

By Center Type

- Single-Specialty ASCs

- Multi-Specialty ASCs

By Ownership

- Physician-Owned ASCs

- Hospital-Owned ASCs

- Joint Venture ASCs

- Corporate-Owned ASCs

By Specialty

- Gastroenterology

- Ophthalmology

- Orthopedics

- Pain Management

- Gynecology

- Urology

- Otolaryngology (ENT)

- Dermatology

- Plastic & Reconstructive Surgery

- Cardiology

- Other Specialties

By Procedure

- Diagnostic Procedures

- Therapeutic Procedures

- Surgical Procedures

By Payer

- Medicare

- Medicaid

- Private Health Insurance

- Self-Pay

Regional Analysis

Leading Region in the Ambulatory Surgery Centers (ASC) Market

ℹ

To learn more about this report –

Download Your Free Sample Report Here

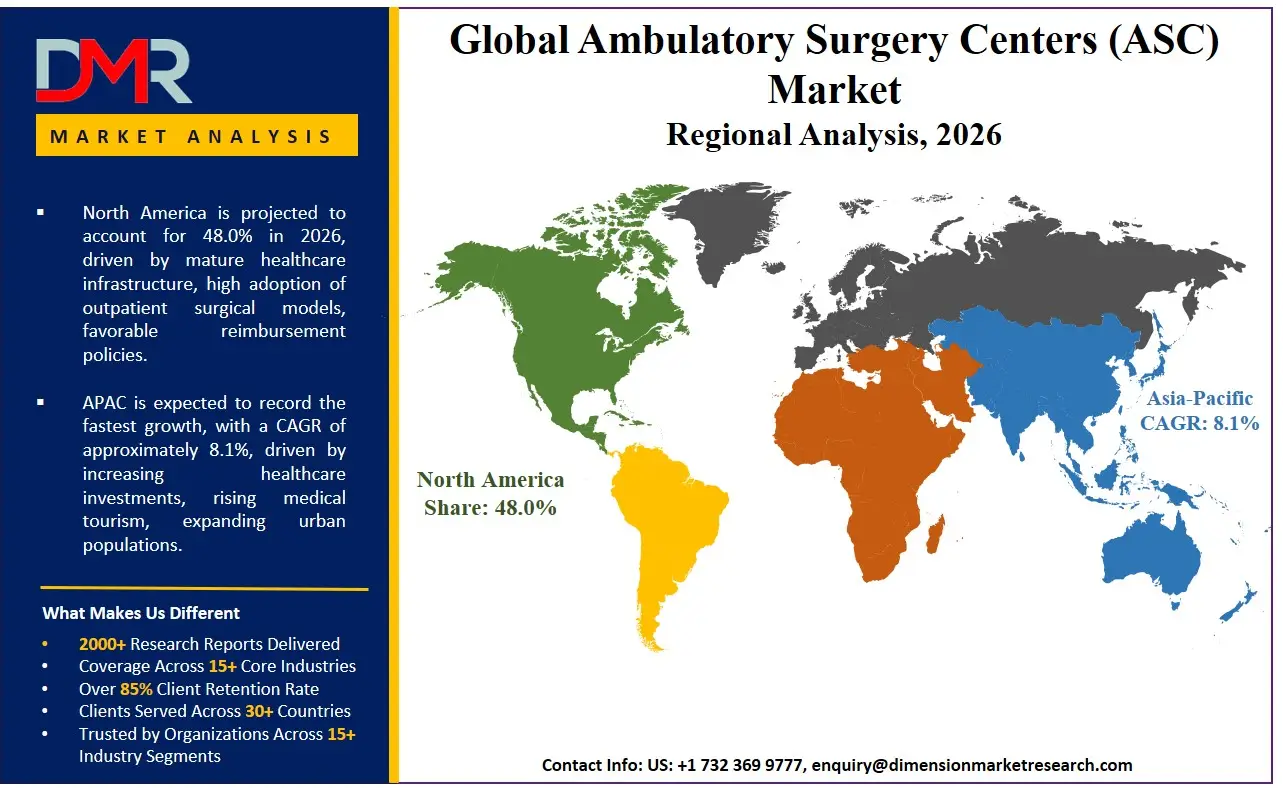

North America is expected to remain the leading region in the ASC market, accounting for an estimated 48% market share in 2026. The region's dominance is supported by a mature healthcare infrastructure, high adoption of outpatient surgical models, favorable reimbursement policies, and strong investment in healthcare technology. The United States represents the largest contributor due to widespread ASC adoption, increasing healthcare cost pressures, and government initiatives supporting value-based care. The presence of advanced medical facilities, experienced healthcare professionals, and strong demand for minimally invasive procedures further strengthens regional growth. Additionally, partnerships between physicians, hospitals, and healthcare organizations are expanding ASC networks. The region's established regulatory framework and high patient acceptance of same-day procedures continue to maintain its leadership position.

Fastest Growing Region in the Ambulatory Surgery Centers (ASC) Market

Asia-Pacific is expected to be the fastest-growing region in the ASC market due to increasing healthcare investments, rising medical tourism, expanding urban populations, and improving healthcare infrastructure. Countries including Japan, India, China, South Korea, and Australia are experiencing growing demand for affordable and accessible surgical services. Government initiatives aimed at strengthening healthcare systems and reducing hospital pressure are encouraging outpatient care adoption. Rising disposable incomes, increasing prevalence of chronic diseases, and growing awareness of minimally invasive procedures are accelerating market expansion. The region also presents significant opportunities for international healthcare operators and domestic providers to develop advanced ASC networks. Technological adoption, including robotic surgery and digital healthcare solutions, is expected to further enhance ASC growth across emerging economies.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The ASC market is characterized by increasing competition among healthcare providers focusing on network expansion, technological advancement, specialty diversification, and operational efficiency. Market participants are strengthening their positions through strategic partnerships, facility acquisitions, investment in advanced surgical technologies, and development of specialized centers. Competitive advantages are created through efficient cost structures, strong physician relationships, accreditation standards, and improved patient experiences. High regulatory requirements and capital investment needs create entry barriers for new operators. Companies are increasingly focusing on digital transformation, AI integration, and value-based healthcare models to differentiate their services and maintain long-term market competitiveness.

Some of the prominent players in the global Ambulatory Surgery Centers (ASC) are:

- United Surgical Partners International (USPI)

- Surgery Partners

- SCA Health

- HCA Healthcare

- Community Health Systems

- Envision Healthcare

- AmSurg

- Compass Surgical Partners

- Regent Surgical Health

- ValueHealth

- Blue Cloud Pediatric Surgery Centers

- Surgical Care Affiliates

- Medical Facilities Corporation

- Nueterra Capital

- Atlas Healthcare Partners

- OrthoAlliance

- Constitution Surgery Alliance

- National Surgical Healthcare

- Physicians Endoscopy

- United Digestive

- Other Key Players

Recent Developments

- In November 2025, United Surgical Partners International advanced technology integration across its ambulatory surgery network by focusing on digital healthcare solutions, operational improvements, and enhanced surgical capabilities. The initiative supported the adoption of modern workflows designed to improve scheduling efficiency, patient management, and procedural outcomes. The company emphasized technology-enabled outpatient care as demand increased for convenient surgical services. Investments in digital infrastructure and facility modernization reflected broader market trends toward automation, data-driven decision-making, and improved patient engagement. The development demonstrated how ASC operators are leveraging innovation to strengthen competitiveness and expand outpatient healthcare delivery capacity.

- In July 2025, Surgical Care Affiliates strengthened its ambulatory surgery network strategy through expanded partnerships focused on improving outpatient surgical access and operational performance. The company continued developing collaborative models involving physicians and healthcare organizations to support specialty-focused surgical centers. The expansion emphasized advanced care delivery, efficient workflows, and improved patient convenience. The initiative aligned with increasing demand for outpatient procedures and healthcare systems' efforts to reduce costs while maintaining quality outcomes. The development highlighted the growing importance of partnership-based ASC models as healthcare providers seek scalable solutions for outpatient surgery growth.

- In March 2025, HCA Healthcare expanded its focus on ambulatory surgical services by strengthening outpatient care capabilities through investments in surgical facilities, technology upgrades, and healthcare delivery networks. The initiative focused on increasing access to same-day procedures while improving operational efficiency across its healthcare ecosystem. The company emphasized expanding lower-cost care settings as demand increased for outpatient procedures. Investments targeted advanced surgical infrastructure, physician collaboration models, and enhanced patient experiences. The development reflected the broader industry movement toward shifting appropriate procedures away from traditional hospital environments into specialized ambulatory settings, supporting healthcare affordability and improving resource utilization.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 93.9 Bn |

| Forecast Value (2035) |

USD 158.9 Bn |

| CAGR (2026–2035) |

6.0% |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Center Type, By Ownership, By Specialty, By Procedure, By Payer |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Ambulatory Surgery Centers (ASC) Market?

▾ The Ambulatory Surgery Centers (ASC) Market size is expected to reach USD 93.9 billion by 2026 and is projected to reach USD 158.9 billion by the end of 2035.

What is the CAGR of the Ambulatory Surgery Centers (ASC) Market from 2026 to 2035?

▾ The market is growing at a CAGR of 6.0 percent over the forecasted period.

What factors are driving the growth of the Ambulatory Surgery Centers (ASC) Market?

▾ Increasing Demand for Cost-Effective Healthcare Delivery, and more are the factors driving the growth of the Ambulatory Surgery Centers (ASC) Market.

What are the major trends in the Ambulatory Surgery Centers (ASC) Market?

▾ Increasing Adoption of Robotic and Advanced Surgical Technologies, and more are some of the major trends in the market.

Who are the key players in the Ambulatory Surgery Centers (ASC) Market?

▾ Some of the key players in the Ambulatory Surgery Centers (ASC) Market include CHS, Amsurg, HCA, and more

How is the Ambulatory Surgery Centers (ASC) Market segmented?

▾ The Ambulatory Surgery Centers (ASC) Market is segmented by center type, ownership, specialty, procedure, payer.

Which region held the largest share of the Ambulatory Surgery Centers (ASC) Market in 2026?

▾ North America is set to lead the Ambulatory Surgery Centers (ASC) Market with an estimated 48.0% share in 2026.

Which region is expected to grow the fastest in the Ambulatory Surgery Centers (ASC) Market?

▾ Asia Pacific is the fastest-growing region in the Ambulatory Surgery Centers (ASC) Market during the forecast period.