Market Overview

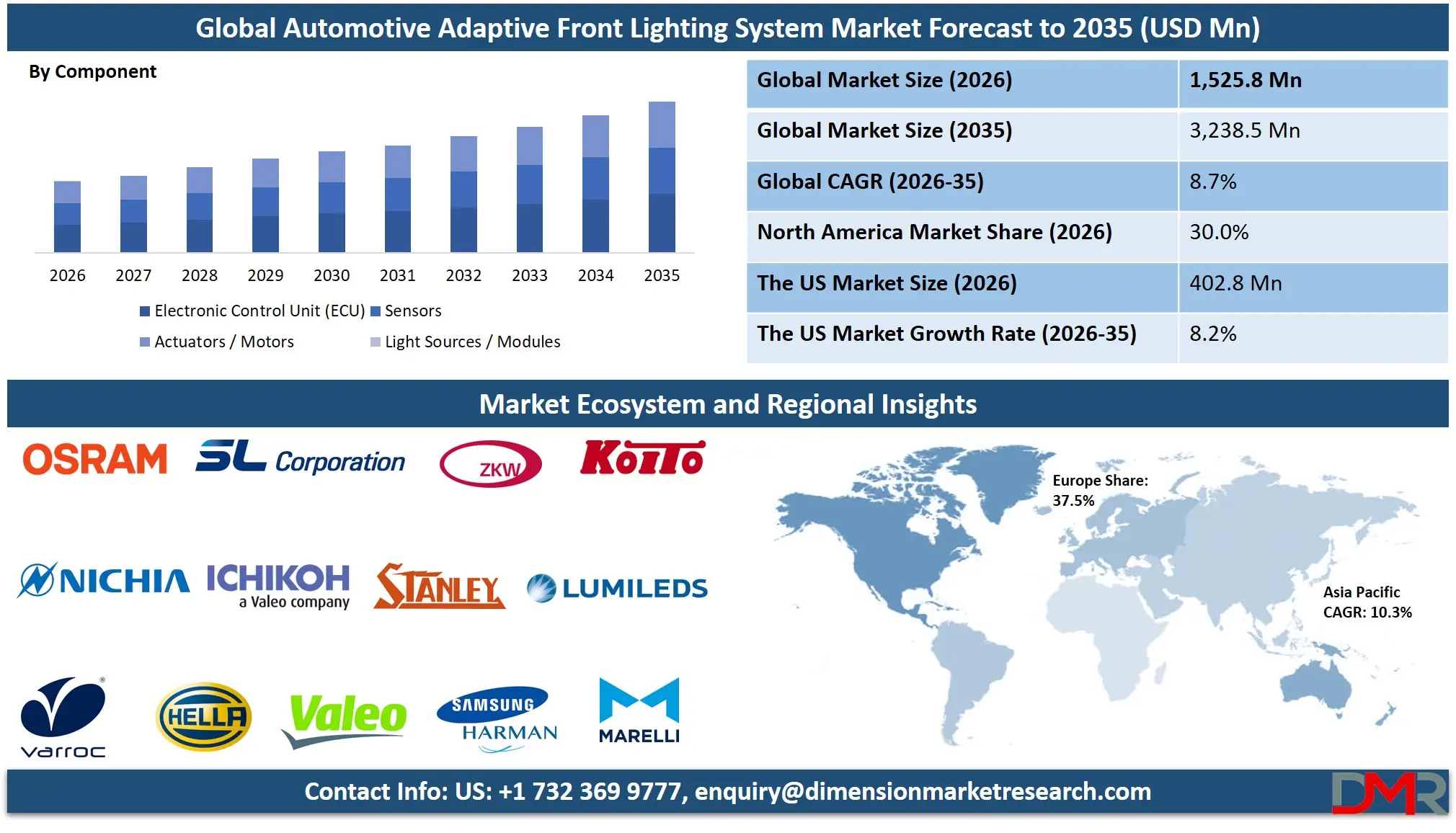

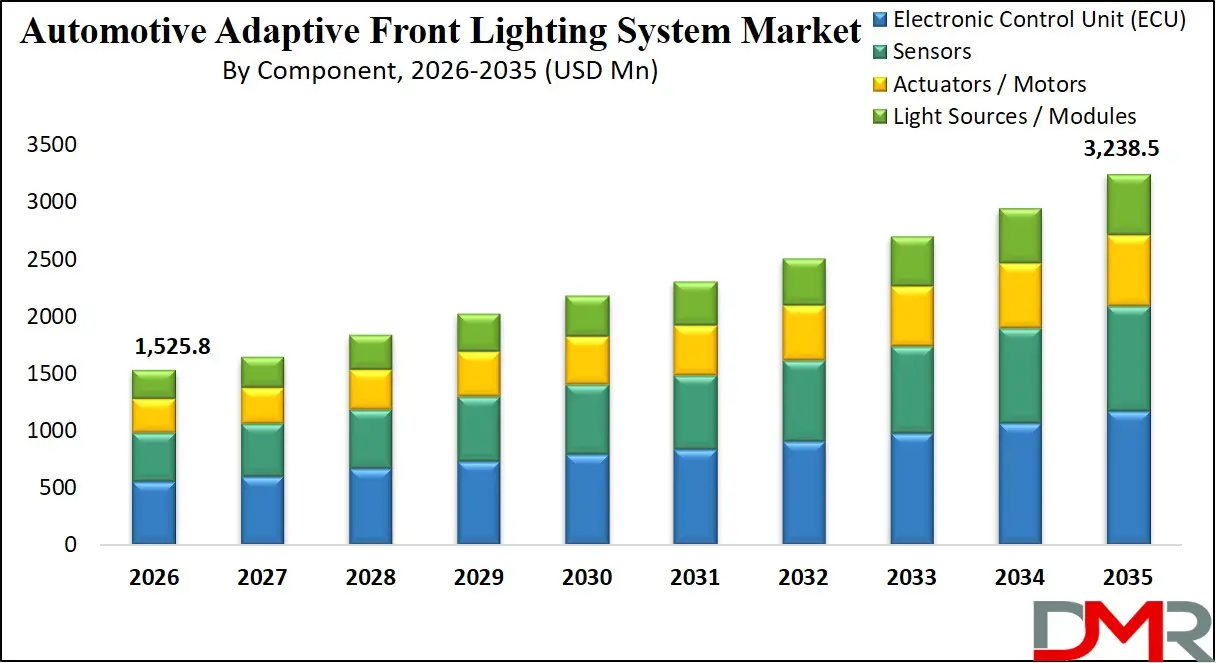

The Global Automotive Adaptive Front Lighting System (AFS) Market is projected to reach USD 1,525.8 million in 2026 and is expected to register a CAGR of 8.7% during 2026–2035, reaching approximately USD 3,238.5 million by 2035. The market's rapid growth is driven by increasing global vehicle production, stringent safety regulations mandating advanced lighting technologies, rising consumer demand for enhanced night-time visibility and aesthetic differentiation, and the accelerated adoption of autonomous and electrified vehicle platforms.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Adaptive Front Lighting Systems enable intelligent beam pattern adjustment based on steering angle, vehicle speed, weather conditions, and oncoming traffic through sensor fusion, actuator-controlled modules, and real-time light distribution algorithms. The model addresses critical industry challenges related to night-time accident reduction, driver fatigue mitigation, regulatory compliance, and premium vehicle differentiation, supporting automakers and lighting suppliers in achieving superior safety ratings and brand prestige.

Technological advancements, including matrix LED pixel control, high-resolution ADB, LiDAR-integrated predictive lighting, OLED surface illumination, and fully software-defined lighting architectures, are transforming the market into a scalable and highly integrated automotive electronics ecosystem. Integration of machine learning algorithms for traffic pattern recognition, predictive beam shaping, and adaptive glare prevention is reshaping automotive safety and human-machine interface standards.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government initiatives mandating autonomous emergency lighting, Euro NCAP scoring incentives for glare-free high beam systems, and smart infrastructure integration in connected vehicle corridors further accelerate global adoption. However, barriers such as high system cost in entry-level segments, complex calibration requirements, varying homologation standards across regions, and semiconductor supply chain dependencies remain. Despite these limitations, the convergence of ADAS, solid-state lighting, and centralized vehicle E/E architectures positions adaptive front lighting as a central driver of global automotive safety transformation through 2035.

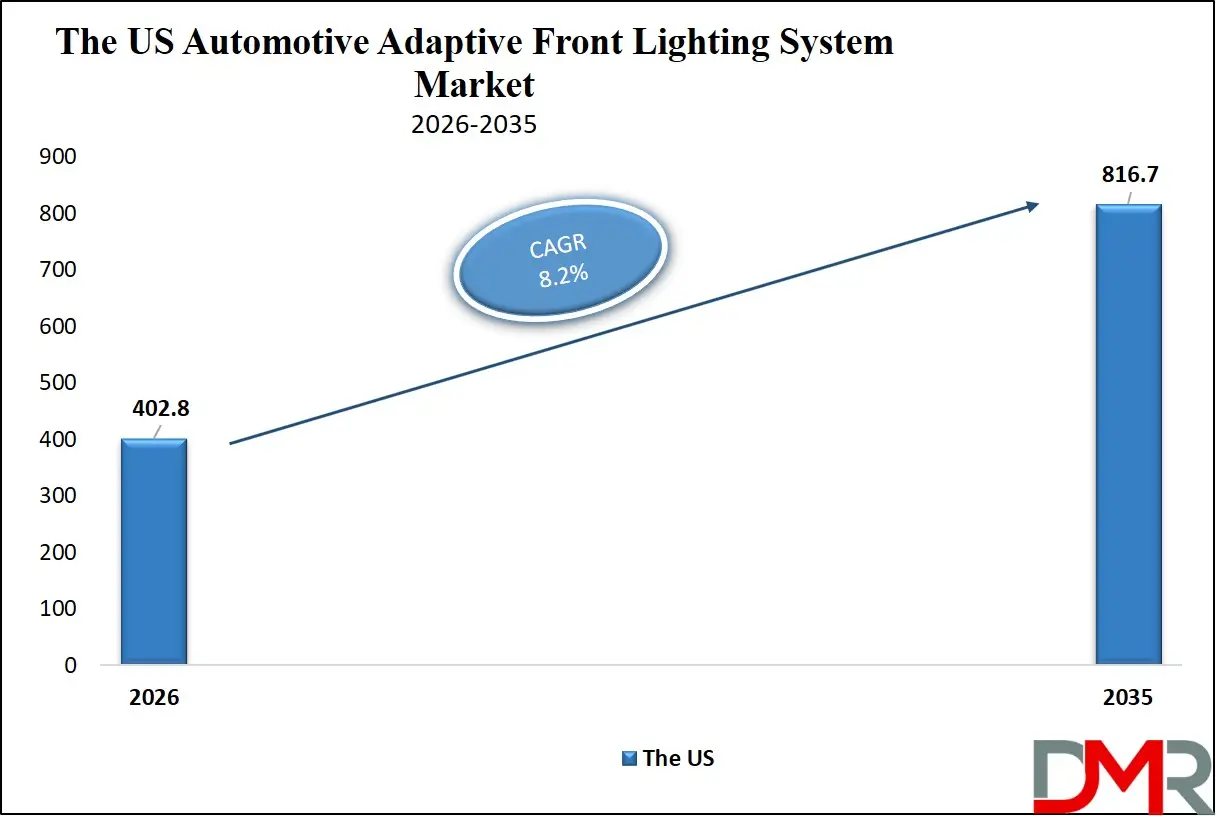

The US Automotive Adaptive Front Lighting System Market

The U.S. Automotive Adaptive Front Lighting System Market is projected to reach USD 402.8 million in 2026 and grow at a CAGR of 8.2%, reaching USD 816.7 million by 2035. The U.S. leads global adoption due to its high SUV and luxury vehicle penetration, NHTSA's modernization of FMVSS 108 permitting ADB systems, and strong consumer willingness for advanced safety packages.

The phase-out of halogen systems in mid-to-premium segments, coupled with rising production volumes of electric pickups and SUVs, fuels demand for matrix LED and glare-free high beam solutions. Major automakers such as Ford, General Motors, Tesla, and Stellantis are integrating adaptive lighting with front camera systems and autonomous driving sensor suites. Tier-1 suppliers including Magna, Valeo, and Hella are expanding U.S. engineering centers to support OEM programs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. regulatory alignment with UN R149 standards for adaptive driving beam, alongside insurance premium reductions for vehicles equipped with crash-avoidance lighting, encourages investment. Training programs and partnerships with SAE International are emerging to standardize lighting performance validation and cybersecurity protocols.

The rapid rise of HD matrix lighting, digital micromirror-based headlamps, and over-the-air updatable light functions continues to redefine the U.S. automotive lighting landscape, positioning the country as a global leader in intelligent front lighting systems.

The Europe Automotive Adaptive Front Lighting System Market

The Europe Automotive Adaptive Front Lighting System Market is projected to be valued at approximately USD 572.2 million in 2026 and is projected to reach around USD 1,214.4 million by 2035, growing at a CAGR of about 8.7% from 2026 to 2035. Europe's leadership is anchored by strong regulatory mandate for mandatory ADB compatibility in new vehicle types, Euro NCAP's five-star safety rating incentives, and mature premium OEM presence.

Countries such as Germany, France, the U.K., Sweden, and Italy are widely adopting adaptive lighting, driven by stringent type-approval requirements, high adoption of LED and laser headlamp technologies, and government-backed initiatives like EU's Vision 2030 road safety strategy. The German premium automakers BMW, Mercedes-Benz, Audi are particularly active in developing and deploying high-definition pixel lighting and predictive light functions.

Europe's dense urban environment requiring precise city lighting patterns, demand for signature lighting for brand identity, and push for energy-efficient low-heat illumination further drive adoption. Funding through Horizon Europe and national E-Mobility funds supports R&D in LiDAR-integrated lighting, OLED rearward projection, and human-centric ambient light.

High-volume EV production and autonomous shuttle programs increasingly deploy 2K-resolution ADB systems, micro-LED projection modules, and ambient light field generation. With strong technical standards, digital light processing integration, and emphasis on sustainable lighting materials, Europe remains one of the most advanced regions in adaptive front lighting penetration.

The Japan Automotive Adaptive Front Lighting System Market

The Japan Automotive Adaptive Front Lighting System Market is anticipated to be valued at approximately USD 76.2 million in 2026 and is expected to attain nearly USD 161.9 billion by 2035, expanding at a CAGR of about 8.7% during the forecast period. Japan's rapidly aging population, high incidence of night-time pedestrian accidents, and leadership in solid-state lighting technology drive high demand for advanced adaptive front lighting systems.

The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) actively supports next-generation lighting through safety regulation modernization, subsidies for SME lighting component suppliers, and integration of pedestrian detection lighting into public transport vehicles. Japan's leadership in ultra-compact optics, phosphor-converted laser diodes, and miniaturized actuator mechanisms accelerates innovation in slim-profile, lightweight adaptive headlamp units suitable for kei cars and global platform exports.

Japan's concept of "Society 5.0" mobility, driven by companies like Toyota, Honda, Nissan, and Koito Manufacturing, integrates V2X-based predictive light control, AI pedestrian intent prediction, and adaptive glare-free functions into seamless nighttime safety ecosystems. Adaptive lighting units are being deployed in next-generation Lexus, Nissan Ariya, and Honda Accord global models. Japan's cultural emphasis on craftsmanship-quality optics, combined with precision electronics integration, positions the country as a high-growth innovator in automotive adaptive lighting.

Global Automotive Adaptive Front Lighting System Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Automotive Adaptive Front Lighting System Market is expected to be valued at USD 1,525.8 million in 2026 and is projected to reach USD 3,238.5 million by 2035, showcasing rapid expansion supported by rising vehicle electrification and safety regulation convergence.

- High CAGR Driven by Technology Migration: The market is expected to grow at an impressive CAGR of 8.7% from 2026 to 2035, fueled by accelerating transition from halogen to matrix LED/laser, AI-driven light distribution algorithms, centralized E/E architectures, and increasing premium vehicle mix worldwide.

- Strong Growth Trajectory in the United States: The U.S. Automotive Adaptive Front Lighting System Market stands at USD 402.8 million in 2026 and is projected to reach USD 816.7 million by 2035, expanding at a CAGR of 8.2% due to ADB legalization, electric truck ramp-up, and high SUV penetration.

- Europe Maintains Regional Dominance: Europe is expected to capture approximately 37.5% of the global market share in 2026, supported by mature premium OEM base, stringent NCAP requirements, and early adoption of HD matrix and laser light systems.

- Rapid Advancement in Lighting Technologies: Innovations including micro-LED pixel arrays, high-resolution DLP projection, OLED surface lighting, LiDAR-homogenized beam patterns, and software-defined lighting functions are significantly accelerating functionality, styling differentiation, and scalability of adaptive front lighting systems.

- Growing Safety Mandates Boost Adoption: Rising global mandates for pedestrian protection, night-time crash avoidance, and glare-free beam compliance, coupled with consumer awareness and insurance incentives, is driving sustained demand for intelligent, predictive, and high-resolution lighting solutions.

Global Automotive Adaptive Front Lighting System Market: Use Cases

- Highway High Beam Assist: Systems automatically toggle between high/low beam and create shadow masks around preceding/oncoming vehicles, enabling maximum illumination without glare.

- Urban / City Intersection Lighting: Predictive lighting activates wider beam distribution at low speeds and intersections to illuminate pedestrians, cyclists, and curbs.

- Adverse Weather Mode: Adaptive algorithms adjust beam intensity, spread, and color temperature in rain, fog, or snow to reduce back-glare and improve road surface contrast.

- Dynamic Bending Light: Actuator-controlled headlamps swivel horizontally according to steering input and yaw rate, illuminating curves before vehicle entry.

- Welcome / Exit Light Animation: OLED and matrix LED modules project brand-specific light signatures, ground projections, and animated sequences for premium user experience.

- Autonomous Vehicle Communication Lighting: Exterior light fields signal vehicle intent (e.g., pedestrian crossing granted, autonomous mode active) in level 3+ self-driving scenarios.

Global Automotive Adaptive Front Lighting System Market: Stats & Facts

U.S. Federal Highway Administration (FHWA)

- Approximately 50% of traffic fatalities occur at night, although only about 25% of travel takes place during nighttime hours.

- The fatal crash rate per mile traveled at night is about three times higher than during the day.

- About 76% of pedestrian fatalities occur during dark conditions.

- Roadway departure crashes are significantly more likely to occur at night than during daylight hours.

- Visibility-related factors contribute to a substantial share of intersection crashes after dark.

National Highway Traffic Safety Administration (NHTSA), U.S. Department of Transportation

- In 2022, the U.S. recorded 42,795 motor vehicle traffic fatalities.

- Nearly half of all fatal crashes occur in dark conditions.

- NHTSA updated Federal Motor Vehicle Safety Standard (FMVSS) No. 108 in 2022 to allow Adaptive Driving Beam (ADB) headlights on U.S. vehicles.

- Headlight-related glare complaints generated over 5,700 public comments in federal regulatory review.

- Visibility limitations are identified as a key factor in nighttime crash severity.

Insurance Institute for Highway Safety (IIHS)

- In 2016, only 1 headlight system out of more than 80 tested received a "Good" rating.

- By 2023–2024 testing cycles, approximately 50% of evaluated headlight systems achieved a "Good" rating.

- Vehicles equipped with "Good"-rated headlights show about 19% fewer nighttime single-vehicle crashes.

- Vehicles with "Good" headlights show approximately 23% fewer nighttime pedestrian crashes.

- More than 80% of vehicles tested before 2016 had inadequate headlight performance ratings.

European Commission – Road Safety Report

- The European Union recorded approximately 20,400 road fatalities in 2023.

- A significant proportion of fatal crashes in the EU occur in low-light or nighttime conditions.

- The EU's General Safety Regulation mandates advanced safety systems in new vehicles starting from 2022 onward.

- Adaptive lighting technologies are permitted under UNECE regulations adopted by the EU.

UNECE (United Nations Economic Commission for Europe)

- UNECE Regulation No. 123 governs Adaptive Front-Lighting Systems (AFS) in participating countries.

- More than 50 countries apply UNECE vehicle lighting regulations.

- UNECE Regulation No. 48 outlines installation requirements for lighting and light-signaling devices.

- ADB systems are legally permitted in UNECE member states under updated lighting regulations.

International Energy Agency (IEA)

- Global electric car sales exceeded 14 million units in 2023.

- Electric vehicles represented about 18% of total global car sales in 2023.

- LED lighting significantly improves energy efficiency compared to halogen systems.

- Vehicle electrification supports increased adoption of energy-efficient lighting technologies such as LED and laser systems.

International Organization of Motor Vehicle Manufacturers (OICA)

- Global motor vehicle production reached approximately 93 million units in 2023.

- Passenger cars account for the majority share of global vehicle production.

- Asia accounts for more than 50% of global vehicle production volume.

- China is the world's largest vehicle producer, manufacturing over 30 million vehicles annually.

Japan Ministry of Land, Infrastructure, Transport and Tourism (MLIT)

- Japan records a significant share of traffic fatalities during nighttime hours.

- Advanced lighting systems are permitted under Japanese vehicle safety standards aligned with UNECE regulations.

UK Department for Transport

- Around 40% of fatal or serious injury collisions occur in the dark.

- Driver surveys indicate that over 90% of motorists report glare from oncoming headlights as a concern.

World Health Organization (WHO)

- Approximately 1.19 million people die globally each year due to road traffic crashes.

- Road traffic injuries are among the leading causes of death globally for people aged 5–29 years.

Global Automotive Adaptive Front Lighting System Market: Market Dynamic

Driving Factors in the Global Automotive Adaptive Front Lighting System Market

Stringent Safety Regulations and NCAP Incentives

The growing global mandate for crash avoidance technologies and pedestrian protection is a major driver for adaptive front lighting adoption. Regulatory frameworks in Europe, Japan, China, and increasingly the U.S. now reward or require glare-free high beam, automatic leveling, and bad-weather light functions. OEMs integrate adaptive systems to achieve 5-star safety ratings and comply with type-approval directives. This allows automakers to reduce liability, increase brand reputation, and unlock access to regulated markets.

Technology Migration and Cost Downscaling

Adaptive front lighting benefits heavily from rapid progress in LED cost reduction, miniaturized ECUs, sensor fusion algorithms, and standardized ADAS interfaces. Advanced systems feature wafer-level optics, single-chip matrix controllers, integrated stepper motors, and lightweight polycarbonate lenses. These innovations enable adaptive technology to cascade from S-Class to Golf-class vehicles. The convergence of front lighting with ADAS camera data and cloud-based traffic mapping further enhances functionality, making adaptive headlamps a democratized safety feature rather than exclusive premium option.

Restraints in the Global Automotive Adaptive Front Lighting System Market

High Bill of Materials in Entry Segments

The significant incremental cost of adaptive front lighting systems, including LED matrices, position sensors, actuators, and validation cycles, limits adoption in A/B-segment vehicles and price-sensitive emerging markets. Many OEMs face feature content trade-offs between lighting and infotainment/ADAS. Additionally, post-crash repair costs for complex headlamp assemblies (often exceeding USD 2,000 for matrix units) create insurance classification friction.

Regulatory and Homologation Fragmentation

Construction regulations, photometric standards, and beam pattern certifications vary widely across UN R149, FMVSS 108, GB 4599 (China), and other regional frameworks, creating engineering complexity in global vehicle platforms. Issues include different color temperature limits, dynamic bending speed restrictions, and ADB masking resolution requirements. Furthermore, retrofitting adaptive lighting in existing legacy architectures often requires full front-end electronic redesign. Variability in grid voltage stability, dirt accumulation assumptions, and headlamp cleaning mandates further limits platform commonality.

Opportunities in the Global Automotive Adaptive Front Lighting System Market

Expansion into Mass-Market and Emerging Regions

Emerging markets represent major growth opportunities due to rapid motorization, localization of LED supply chains, and increasing two-wheeler conflict mitigation programs. Countries in Asia-Pacific, Latin America, and MEA are launching mandatory headlamp performance upgrades and vehicle safety rating programs where adaptive lighting can ensure compliance and differentiation. Local optics manufacturing partnerships, simplified ADB variants, and government fleet procurement contracts can improve accessibility, driving the next wave of market expansion.

Software-Defined Lighting and Function-on-Demand

The integration of lighting functions into centralized vehicle computers not only for beam control but for user-personalized light signatures, FOD (function-on-demand) micro-transactions, and over-the-air upgrades creates new value streams. OEMs can offer adaptive driving beam as a 30-day trial or one-time purchase post-vehicle sale, transforming lighting from fixed BOM component into recurring revenue asset. This transforms lighting systems from passive hardware into intelligent, upgradable platforms that increase vehicle lifetime value.

Trends in the Global Automotive Adaptive Front Lighting System Market

HD Matrix and Micro-Pixel Resolution

The rise of high-definition adaptive lighting systems with 10,000+ individually addressable pixels is gaining traction. These systems enable cinema-grade projection on road surfaces, lane departure warnings, and navigation cues directly projected into driver's field of view. This hybrid illumination-information model elevates headlamps from safety component to communication interface.

LiDAR and Camera Fusion for Predictive Beam Shaping

Centralized fusion of front camera, navigation GPS, and emerging LiDAR data is enabling look-ahead beam shaping adjusting light distribution before the vehicle enters a curve, crests a hill, or encounters intersections. This trend supports scalable deployment of condition-predictive rather than condition-reactive lighting across premium and increasingly mid-segment EVs.

Global Automotive Adaptive Front Lighting System Market: Research Scope and Analysis

By Component Analysis

Electronic Control Units (ECUs) are projected to dominate the Component segment of the Global Automotive Adaptive Front Lighting System Market. This dominance is driven by the fundamental shift from discrete relay-based lighting control to centralized, software-driven light domain controllers. The ECU serves as the intelligence core, processing inputs from multiple sensors including cameras, steering angle sensors, speed sensors, and yaw rate sensors while executing real-time algorithms for beam shaping, cut-off line positioning, and thermal management. As lighting functions multiply matrix pixel control, Adaptive Driving Beam masking, dynamic bending, and predictive light distribution the ECU's role as the integration hub becomes increasingly decisive. The technology for lighting ECUs is also the most rapidly evolving, transitioning from 8-bit to 32-bit multicore architectures with embedded ASIL-B and ASIL-C safety integrity levels. While sensors provide environmental awareness and actuators execute physical movement, the ECU remains the high-value intelligence layer, capturing an increasing share of system bill-of-materials. Its role as the gateway for over-the-air software updates, diagnostic functions, and feature-on-demand activation secures the ECU's leading market position throughout the forecast period.

Sensors and Actuators constitute the essential second and third largest component segments. Front cameras are migrating from mono to stereo setups for improved depth perception and object classification; steering angle and wheel speed sensors are standardizing across all vehicle classes including entry-level segments. Radar sensors are increasingly integrated for predictive adaptive lighting functions in premium platforms. Actuator technology is transitioning from brushed DC motors to precision stepper and brushless DC units for silent, hysteresis-free headlamp leveling and swivel motion with millisecond response times.

By Technology / Light Source Analysis

LED is projected to dominate the Global Automotive Adaptive Front Lighting System Market, fundamentally transforming automotive lighting from consumable bulb to solid-state durable system. Its dominance stems from an unparalleled value proposition: superior energy efficiency achieving 70 percent or greater reduction in power consumption compared to halogen, exceptional design flexibility enabling thin light guides and three-dimensional surface arrays, and continuously declining cost curves driven by manufacturing scale. By integrating advanced chip-on-board architectures, chip-scale packaging, and emerging micro-LED array technologies, these systems deliver adaptive beam patterns, dynamic turn indicator animations, and brand-specific daytime running light signatures with minimal thermal dissipation and packaging constraints. The driving forces behind market leadership are tri-fold: the complete phase-out of halogen in new premium and mid-segment vehicle platforms across Europe, North America, and developed Asia-Pacific markets; the plummeting cost of LED package manufacturing now below USD 0.10 per high-flux emitter; and the growing consumer expectation of premium lighting democratization across mainstream vehicle segments.

As vehicle electrification prioritizes range efficiency and battery conservation, the economic case for LED over legacy technologies becomes irresistible, solidifying these systems as the cornerstone of modern adaptive front lighting architecture.

Xenon and HID constitutes the diminishing second-largest technology segment, gradually phased out in favor of LED in mature markets but retaining substantial installed base for legacy vehicle production and certain emerging market applications where cost sensitivity remains paramount. Halogen persists only in entry-level commercial vehicles, basic fleet specifications, and specific emerging regions with limited lighting regulation enforcement.

By Product Type Analysis

Adaptive Driving Beam is poised to be the largest and most dominant product segment in the Global Automotive Adaptive Front Lighting System Market, driven by powerful global regulatory and safety momentum. The ability to permanently drive with high beam activated while selectively shadowing surrounding vehicles, pedestrians, and cyclists addresses the fundamental driver need maximum nighttime visibility without causing glare to other road users. This functionality, once exclusive to vehicles priced above EUR 80,000, is cascading to mainstream SUVs, crossovers, and hatchbacks through matrix LED implementation and cost-optimized multi-pixel ADB architectures utilizing reduced segment counts. The sector is also acutely affected by Euro NCAP's increasing weighting of lighting performance in overall safety ratings, making ADB a strategic feature for achieving five-star certification. Beyond safety compliance, ADB offers original equipment manufacturers visible technology differentiation in showroom conditions through demonstration of intelligent beam masking and welcome light animations. From premium German sedans to American full-size pickup trucks and Chinese new energy vehicles, the competitive pressure in ADB deployment makes its adoption not merely advantageous but increasingly essential for maintaining brand relevance and perceptual technology leadership.

Matrix and Pixel Lighting ranks as the second-largest product segment, distinguished from base ADB by higher resolution typically exceeding 1,024 individually addressable segments. This enables advanced functions including city intersection illumination, construction zone hazard marking, lane departure warning projection, and brand-specific symbol projection onto road surfaces.

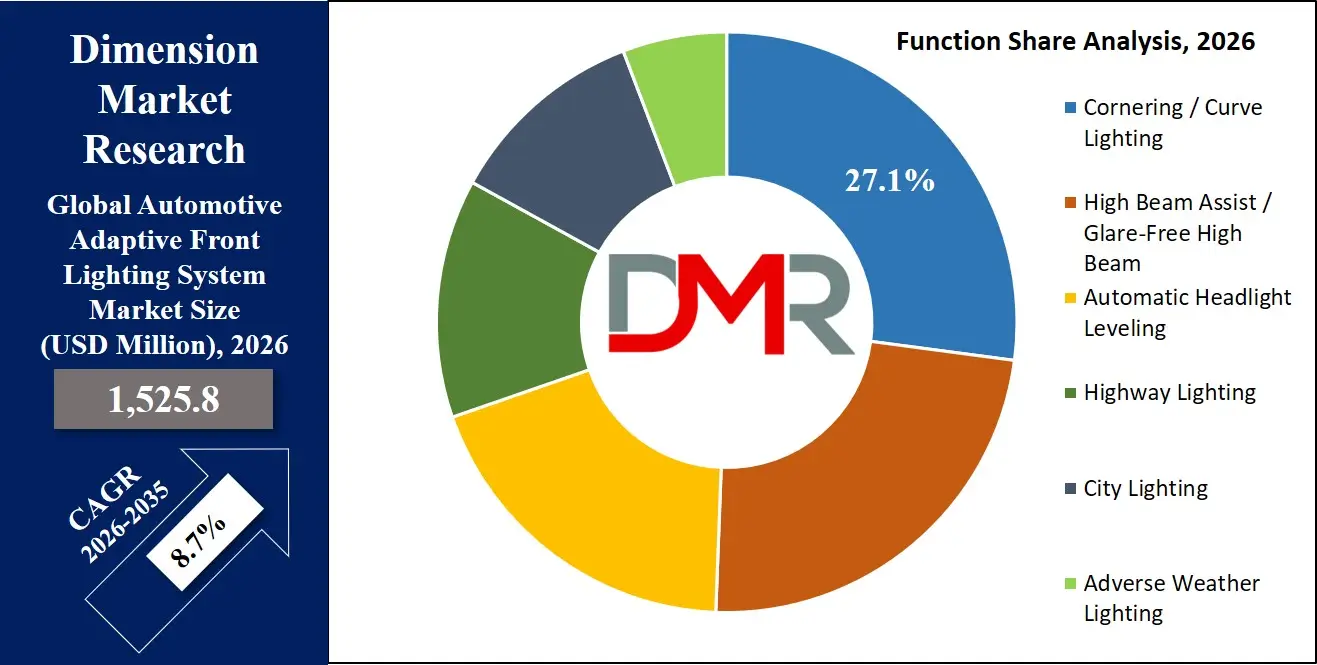

By Function Analysis

High Beam Assist and Glare-Free High Beam is anticipated to dominate the Function segment as the primary utility driver and most consumer-visible benefit of adaptive front lighting systems. These functions deliver quantifiable nighttime crash reduction estimated at up to 35 percent improvement in pedestrian detection distance and are heavily promoted in marketing campaigns as demonstrable safety innovations. Cornering and Curve Lighting remains the established second function, nearly ubiquitous in adaptive systems and increasingly implemented via both swivel actuator and static cornering lamp methods. Automatic Headlight Leveling, mandated in many regions with HID and LED light sources, functions as an invisible but essential enabler for proper beam pattern performance under varying vehicle load conditions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Highway, City, and Adverse Weather Lighting represent differentiated application modes increasingly automated through front camera scene classification the vehicle autonomously recognizes whether it is operating in urban canyon environments, high-speed autobahn conditions, or reduced-visibility rain/fog scenarios and adjusts beam pattern distribution, intensity, and color temperature accordingly. As sensor fusion sophistication increases with neural network-based road understanding, predictive contextual lighting will progressively supersede driver-selected lighting modes.

By Vehicle Type Analysis

Passenger Cars are projected to dominate the Vehicle Type segment, accounting for over 78 percent of global adaptive front lighting system volume. Sports Utility Vehicles, specifically, represent the highest attach rate for premium matrix lighting and Adaptive Driving Beam systems, particularly in North America and China where SUV market share exceeds 45 percent of new vehicle sales. Luxury Vehicles, while contributing lower absolute volume, drive technology introduction and innovation diffusion for laser light sources, high-definition matrix resolution exceeding 10,000 pixels, and digital light processing projection capabilities.

Electric Vehicles represent the highest growth segment: native EV platforms dedicated battery electric vehicle architectures universally specify LED-based adaptive systems to maximize range efficiency via lighting power reduction and align with forward-looking design language emphasizing slim profile illumination. Light Commercial Vehicles and Heavy Commercial Vehicles currently lag in adaptive lighting penetration due to cost sensitivity and fleet purchasing patterns, but are experiencing accelerated adoption due to safety mandates for truck fleet nighttime operations and regulatory emphasis on vulnerable road user detection in urban delivery contexts.

By Sales Channel Analysis

OEM is anticipated to dominate the Global Automotive Adaptive Front Lighting System Market as the exclusive channel for headlamp type-approval, vehicle network integration, and comprehensive warranty coverage. Adaptive front lighting remains primarily factory-fit equipment due to complex calibration requirements involving vehicle-specific bus communication protocols, photometric validation against regional regulatory frameworks, and certification dependencies. The integration of adaptive headlamps with front camera systems, electronic stability control sensors, and navigation data necessitates OEM-level engineering coordination that aftermarket channels cannot replicate. Additionally, the trend toward over-the-air updatable light functions and software-defined vehicle architectures further consolidates OEM control over lighting feature specification, activation, and subscription management. Aftermarket represents a modest but growing segment, primarily focused on premium halogen-to-LED conversion kits for basic lighting improvement, limited adaptive retrofit solutions for older luxury vehicles through specialized integrators, and collision replacement parts that must maintain OEM-specified performance characteristics. The complexity and cost of full adaptive system retrofitting will continue to constrain aftermarket expansion.

The Global Automotive Adaptive Front Lighting System Market Report is segmented on the basis of the following:

By Component

- Electronic Control Unit (ECU)

- Sensors

- Camera

- Radar

- Steering Angle Sensor

- Speed Sensor

- Actuators / Motors

- Light Sources / Modules

By Technology / Light Source

- Halogen

- Xenon / HID (High-Intensity Discharge)

- LED (Light-Emitting Diode)

- OLED (Organic LED)

- Laser

By Product Type

- Static Adaptive Front Lighting

- Dynamic / Bending Light

- Matrix / Pixel Lighting

- Adaptive Driving Beam (ADB)

By Function

- Cornering / Curve Lighting

- High Beam Assist / Glare-Free High Beam

- Automatic Headlight Leveling

- Highway Lighting

- City Lighting

- Adverse Weather Lighting

By Vehicle Type

- Passenger Cars

- Hatchback

- Sedan

- SUV

- Luxury Vehicles

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Electric Vehicles (EVs)

By Sales Channel

- OEM (Original Equipment Manufacturer)

- Aftermarket

Impact of Artificial Intelligence in the Global Automotive Adaptive Front Lighting System Market

- AI for Predictive Beam Shaping: AI analyzes camera, radar, and GPS data to predict road curvature, crests, and intersection entry, enabling proactive light distribution seconds before vehicle reaches the hazard point.

- AI-Driven Traffic Participant Recognition: Neural networks classify oncoming vehicles, preceding vehicles, pedestrians, cyclists, and animals, adjusting mask size, intensity, and beam spread to minimize distraction while maximizing illumination.

- Visual Place Recognition & Light Memory: AI algorithms recognize frequently driven routes (home garage, office parking) and recall user-defined light height, color temperature, and welcome sequences, enabling personalized lighting.

- AI-Based Thermal and Lumen Management: Machine learning models predict LED junction temperature rise under sustained high-output operation, dynamically derating current and adjusting cooling fan curves to maintain optical performance and longevity.

- Fleet Learning for Continuous Optimization: AI systems aggregate edge data from millions of vehicles to continuously improve traffic participant classification models, beam pattern libraries for different geographies, and adverse weather compensation strategies, building a lighting intelligence knowledge base that enhances global fleet safety over time.

Global Automotive Adaptive Front Lighting System Market: Regional Analysis

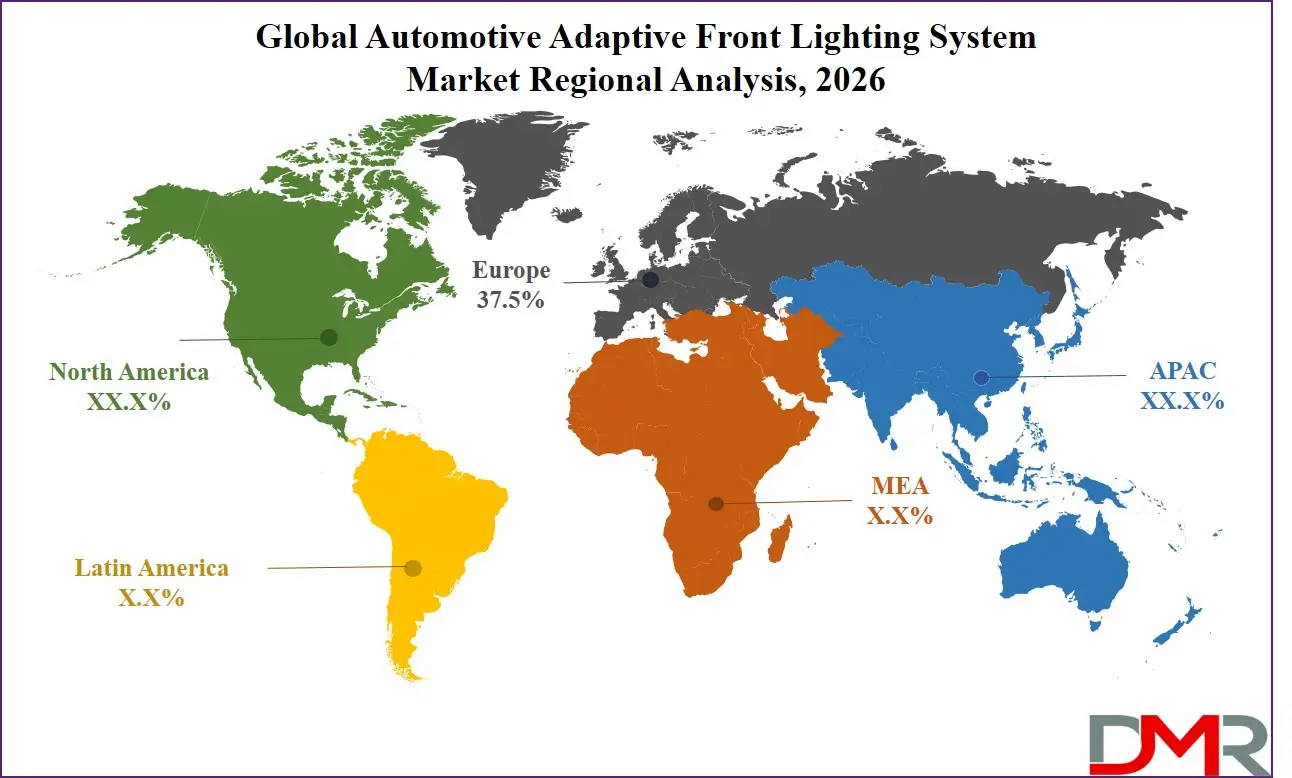

Region with the Largest Revenue Share

Europe is projected to dominate the Global Automotive Adaptive Front Lighting System Market with 37.5% of market share by the end of 2026, owing to a powerful combination of premium OEM concentration (Audi, BMW, Mercedes-Benz, Volkswagen Group), strictest photometric regulations, and Euro NCAP's decisive influence on safety feature adoption. Germany, France, and Italy have rapidly integrated matrix LED and ADB into mainstream vehicle lines, supported by a culture of lighting innovation and high-performance engineering. Major Tier-1 suppliers and automotive lighting specialists are institutionalizing adaptive front lighting as brand-defining technology. The region's stringent CO2 targets, coupled with EV transition, create strong economic case for LED efficiency. Supportive EU research frameworks and harmonized UN R149 type-approval further solidify Europe's leadership position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR and is poised to achieve rapid market share growth due to its massive vehicle production base, aggressive domestic OEM technology upscaling, and catch-up regulatory modernization. Countries like China, India, Japan, South Korea, and Thailand are investing heavily in local lighting R&D and mandating advanced headlamp performance. China's "Intelligent Vehicle Innovation Strategy" and India's Bharat NCAP are creating fertile ground for adaptive lighting adoption. The region's cost sensitivity is being addressed through local LED packaging, domestic ECU manufacturing, and partnerships between global Tier-1s and local automakers. This, combined with the world's largest vehicle production output, positions APAC as the fastest-growing market for automotive adaptive front lighting systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Automotive Adaptive Front Lighting System Market: Competitive Landscape

The Global Automotive Adaptive Front Lighting System Market is moderately consolidated, featuring a mix of global automotive lighting incumbents, electronics system integrators, and optical semiconductor firms. Leading lighting equipment players Koito, Valeo, Marelli Automotive Lighting, Hella, Stanley, and ZKW are leveraging their expertise in optics, thermal management, and mechatronics to develop integrated adaptive headlamp solutions. Pure-play technology specialists such as SL Corporation, Ichikoh, and Varroc are driving market dynamics with cost-competitive matrix LED systems focused on high-volume platforms.

AI and software specialists like NVIDIA (for perception processing), Texas Instruments (for DLP projection control), and Infineon (for power management ICs) play increasingly influential roles as enablers and chipset partners. Semiconductor leaders Osram, Lumileds, and Nichia are critical to LED/laser light source roadmaps. Automotive electronics giants Bosch and Continental supply sensor fusion ECUs and steering angle sensors. Traditional automakers are also increasing in-sourcing of lighting control software, aiming to differentiate via personalized light functions.

Some of the prominent players in the Global Automotive Adaptive Front Lighting System Market are:

- Koito Manufacturing Co., Ltd.

- Valeo SA

- Marelli Automotive Lighting

- Hella GmbH & Co. KGaA

- Stanley Electric Co., Ltd.

- ZKW Group GmbH

- SL Corporation

- Ichikoh Industries, Ltd.

- Varroc Engineering Limited

- Osram Licht AG

- Lumileds Holding B.V.

- Nichia Corporation

- Samsung Electronics (Harman)

- Magna International Inc.

- Continental AG

- Robert Bosch GmbH

- Texas Instruments Incorporated

- Infineon Technologies AG

- NVIDIA Corporation

- Hasco Vision Technology Co., Ltd.

- Other Key Players

Recent Developments in the Global Automotive Adaptive Front Lighting System Market

- November 2025: Valeo introduced its Panamera V3 adaptive headlamp platform, featuring 24,000 individually addressable pixels per module, cloud-connected light functions, and pedestrian intent projection. The system reduces energy consumption by 25% compared to previous generation.

- October 2025: Koito presented its μ-ADB prototype, achieving 1,024 segments in a 30x20mm optical footprint, enabling ultra-slim headlamp styling without compromising ADB performance.

- September 2025: Marelli Automotive Lighting announced a multi-year agreement with a top-5 global automaker to supply its cost-optimized "e-ADB" system for B/C-segment global platforms, signaling commoditization of glare-free high beam.

- August 2025: Osram completed the acquisition of a specialist GaN-on-silicon startup to enhance its front lighting portfolio with programmable beam steering capability, accelerating its roadmap for hybrid illumination-sensing headlamps.

- June 2025: NVIDIA announced a collaboration with a leading Chinese electric vehicle manufacturer to integrate its DRIVE Orin centralized compute with pixel-based lighting control, enabling over-the-air light function upgrades and V2X communication via headlamps.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1,525.8 Mn |

| Forecast Value (2035) |

USD 3,238.5 Mn |

| CAGR (2026–2035) |

8.7% |

| The US Market Size (2026) |

USD 402.8 Mn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Component (Electronic Control Unit (ECU), Sensors, Actuators / Motors, Light Sources / Modules), By Technology / Light Source (Halogen, Xenon / HID (High-Intensity Discharge), LED (Light-Emitting Diode), OLED (Organic LED), Laser), By Product Type (Static Adaptive Front Lighting, Dynamic / Bending Light, Matrix / Pixel Lighting, Adaptive Driving Beam (ADB)), By Function (Cornering / Curve Lighting, High Beam Assist / Glare-Free High Beam, Automatic Headlight Leveling, Highway Lighting, City Lighting, Adverse Weather Lighting), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), Electric Vehicles (EVs)), By Sales Channel (OEM (Original Equipment Manufacturer), Aftermarket) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Koito Manufacturing Co., Ltd.; Valeo SA; Marelli Automotive Lighting; Hella GmbH & Co. KGaA; Stanley Electric Co., Ltd.; ZKW Group GmbH; SL Corporation; Ichikoh Industries, Ltd.; Varroc Engineering Limited; Osram Licht AG; Lumileds Holding B.V.; Nichia Corporation; Samsung Electronics (Harman); Magna International Inc.; Continental AG; Robert Bosch GmbH; Texas Instruments Incorporated; Infineon Technologies AG; NVIDIA Corporation; Hasco Vision Technology Co., Ltd., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Automotive Adaptive Front Lighting System Market?

▾ The Global Automotive Adaptive Front Lighting System Market size is estimated to have a value of USD 1,525.8 million in 2026 and is expected to reach USD 3,238.5 million by the end of 2035.

What is the growth rate in the Global Automotive Adaptive Front Lighting System Market in 2026?

▾ The market is growing at a CAGR of 8.7 percent over the forecasted period of 2026.

What is the size of the US Automotive Adaptive Front Lighting System Market?

▾ The US Automotive Adaptive Front Lighting System Market is projected to be valued at USD 402.8 million in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 816.7 million in 2035 at a CAGR of 8.2%.

Which region accounted for the largest Global Automotive Adaptive Front Lighting System Market?

▾ Europe is expected to have the largest market share in the Global Automotive Adaptive Front Lighting System Market with a share of about 37.5% in 2026.

Who are the key players in the Global Automotive Adaptive Front Lighting System Market?

▾ Some of the major key players in the Global Automotive Adaptive Front Lighting System Market are Koito Manufacturing Co., Ltd., Valeo SA, Marelli Automotive Lighting, Hella GmbH & Co. KGaA, Stanley Electric Co., Ltd., ZKW Group GmbH, and many others.