This growth is fueled by the rising adoption of intelligent automation, AI-driven decision-making, self-learning systems, and next-gen virtual agents across industries such as healthcare, finance, retail, and manufacturing.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Autonomous AI Agents are self-directed intelligent systems capable of perceiving their environment, making decisions, and executing actions without continuous human intervention. These agents leverage a combination of artificial intelligence technologies such as machine learning, reinforcement learning, and natural language processing to adapt, learn from data, and optimize outcomes over time.

Unlike traditional automation tools, autonomous agents are goal-driven, context-aware, and capable of handling complex tasks dynamically across varying scenarios. Whether embedded in virtual environments like digital assistants or deployed in physical systems such as robotics and autonomous vehicles, these agents exhibit human-like reasoning, interaction capabilities, and strategic planning in real-time.

The global Autonomous AI Agents market is witnessing transformative growth, driven by technological advancements and increased enterprise demand for intelligent automation. Businesses across diverse industries such as finance, healthcare, retail, and manufacturing are integrating autonomous agents to streamline workflows, reduce operational costs, and enhance customer engagement. These agents are becoming central to next-generation automation strategies, providing not only task execution but decision intelligence, predictive capabilities, and contextual adaptability. Their ability to operate with minimal human oversight is reshaping organizational models, making them highly valuable in mission-critical applications.

Another key driver of this markets expansion is the convergence of cloud computing, edge AI, and real-time analytics, which enables autonomous agents to function with high scalability and responsiveness. Cloud-native deployment and AI-as-a-Service models are growing in accessibility, especially for small and medium enterprises. Edge-based agents are gaining traction in sectors like logistics and smart cities where real-time decision-making is crucial. The flexibility in deployment and integration has significantly broadened the markets scope, enabling adoption across both virtual ecosystems and embedded environments.

Moreover, the proliferation of large language models and contextual AI has elevated the conversational and analytical capabilities of autonomous agents. These models are enabling more nuanced and human-like interactions, making agents suitable for roles such as customer support, medical diagnostics, legal assistance, and even personalized education. As regulatory frameworks mature and ethical AI practices are enforced, the market is expected to see more responsible innovation, ensuring data privacy, transparency, and accountability in agent-driven systems. This evolution positions autonomous AI agents as a foundational pillar in the global shift toward intelligent and autonomous digital ecosystems.

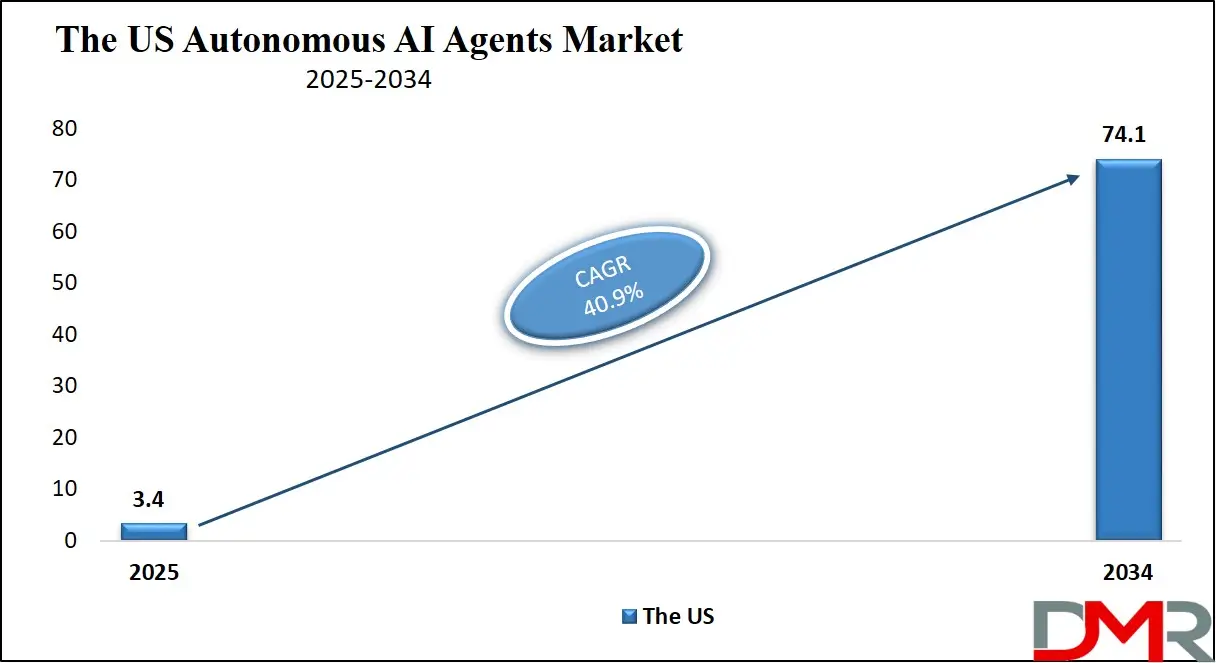

The US Autonomous AI Agents Market

The U.S. Autonomous AI Agents Market size is projected to be valued at USD 3.4 billion in 2025. It is further expected to witness subsequent growth in the upcoming period, holding USD 74.1 billion in 2034 at a CAGR of 40.9%.

The U.S. Autonomous AI Agents market is rapidly evolving, driven by a mature digital ecosystem, high R&D investment, and robust adoption of artificial intelligence technologies across key industries. Organizations in sectors such as healthcare, finance, and defense are deploying self-operating AI systems to enhance operational efficiency, streamline decision-making, and reduce manual intervention in complex workflows. These intelligent agents utilize real-time data processing, predictive analytics, and adaptive learning to make autonomous decisions, enabling businesses to achieve higher precision and agility. The demand for context-aware computing, reinforcement learning models, and human-machine collaboration is propelling innovations that make these agents more intuitive, scalable, and enterprise-ready.

The widespread implementation of intelligent virtual assistants, cognitive automation tools, and autonomous digital agents in U.S. enterprises reflects a shift toward intelligent infrastructure and AI-led business transformation. Federal and state initiatives supporting ethical AI practices, combined with the presence of leading AI research institutions and cloud service providers, are reinforcing the markets momentum. U.S.-based companies are also focusing on enhancing conversational AI, agent collaboration systems, and embedded AI processors to meet the rising need for intelligent autonomy. This environment is fostering a dynamic landscape where self-learning AI systems are becoming central to enterprise automation strategies and the next generation of smart, independent technologies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The European Autonomous AI Agents Market

Europes Autonomous AI Agents market is projected to reach a valuation of approximately

USD 1.8 billion in 2025, reflecting the regions growing investment in artificial intelligence and automation technologies. This steady market share is driven by Europes strong industrial base, particularly in manufacturing, automotive, and financial services sectors, which are adopting autonomous AI agents to enhance operational efficiency, predictive maintenance, and customer engagement.

Additionally, Europes focus on ethical AI development, data privacy, and regulatory frameworks fosters trust and encourages the deployment of AI solutions across various industries. Innovation hubs in countries like Germany, France, and the UK play a significant role in advancing AI research and commercialization, contributing to the regions expanding market footprint.

The European market is expected to experience a compound annual growth rate of around 35.5%, supported by rising demand for cloud-based autonomous AI solutions, edge computing integration, and enhanced machine learning applications. Increasing collaboration between public and private sectors fuels the adoption of autonomous AI agents in smart city projects, healthcare, and retail, driving innovation in context-aware computing and natural language processing technologies. As enterprises seek scalable and efficient AI-driven automation tools, Europes commitment to fostering a robust AI ecosystem positions it as a vital growth region within the global Autonomous AI Agents market landscape.

The Japanese Autonomous AI Agents Market

Japans Autonomous AI Agents market is anticipated to reach approximately USD 0.3 billion in 2025, reflecting the countrys focused investments in AI-driven automation and robotics. Japans strong technological infrastructure, integrated with its leadership in sectors such as manufacturing, healthcare, and consumer electronics, drives the adoption of autonomous AI agents to improve productivity and innovation.

The governments emphasis on smart factory initiatives and Industry 4.0 further accelerates the integration of AI agents for predictive maintenance, quality control, and intelligent supply chain management. This targeted approach supports steady growth despite Japans relatively smaller market size compared to other regions.

The market in Japan is expected to register a robust compound annual growth rate of 42.0%, fueled by advancements in natural language processing, machine learning, and context-aware computing. The widespread implementation of autonomous AI agents in robotics, smart infrastructure, and personalized healthcare solutions positions Japan as a dynamic growth market.

Additionally, collaboration between academic institutions, technology firms, and the government promotes innovation and accelerates the commercialization of AI technologies. This strong growth trajectory highlights Japans strategic role in shaping the future of autonomous AI agents within the Asia-Pacific region and beyond.

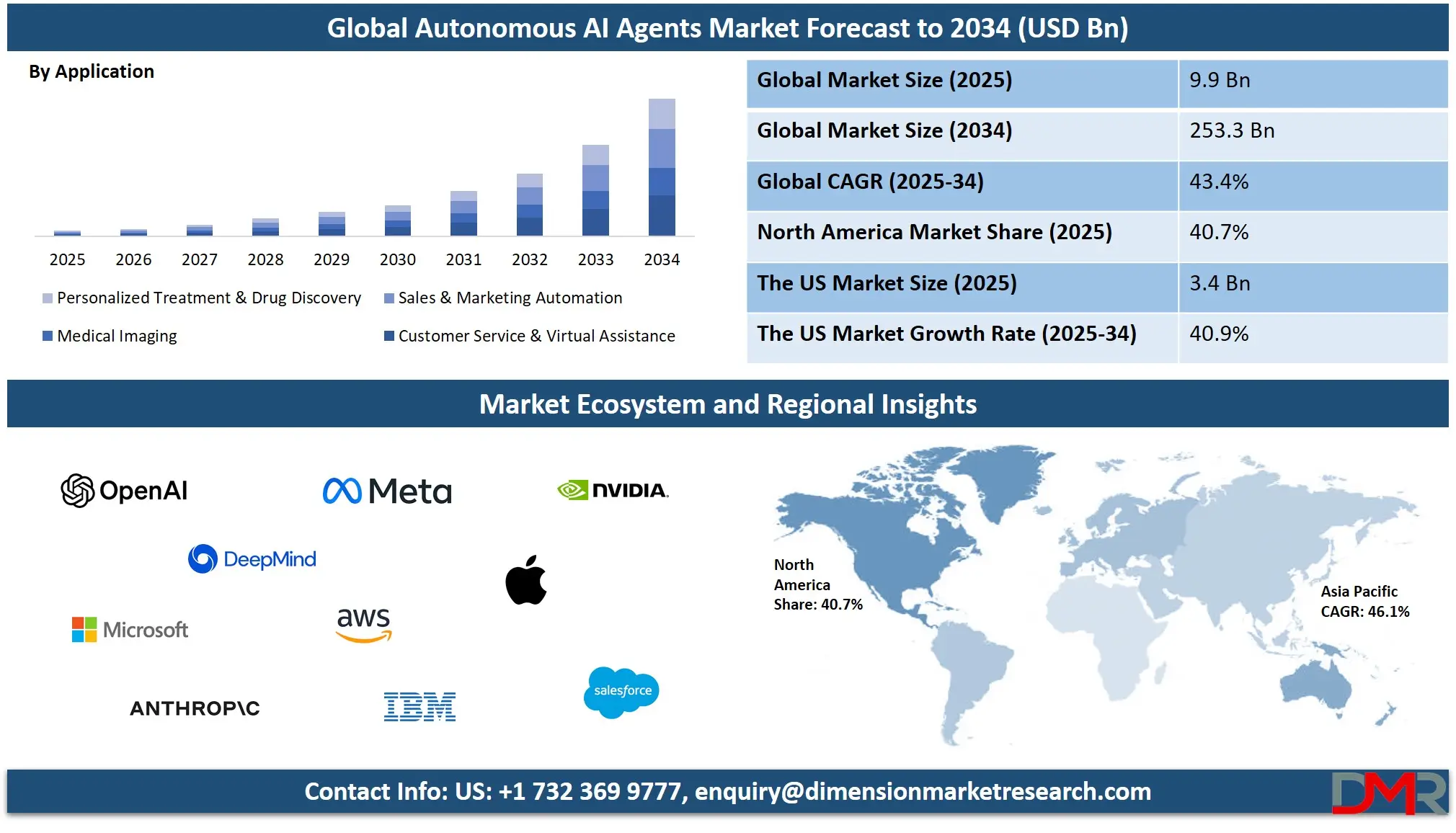

Global Autonomous AI Agents Market: Key Takeaways

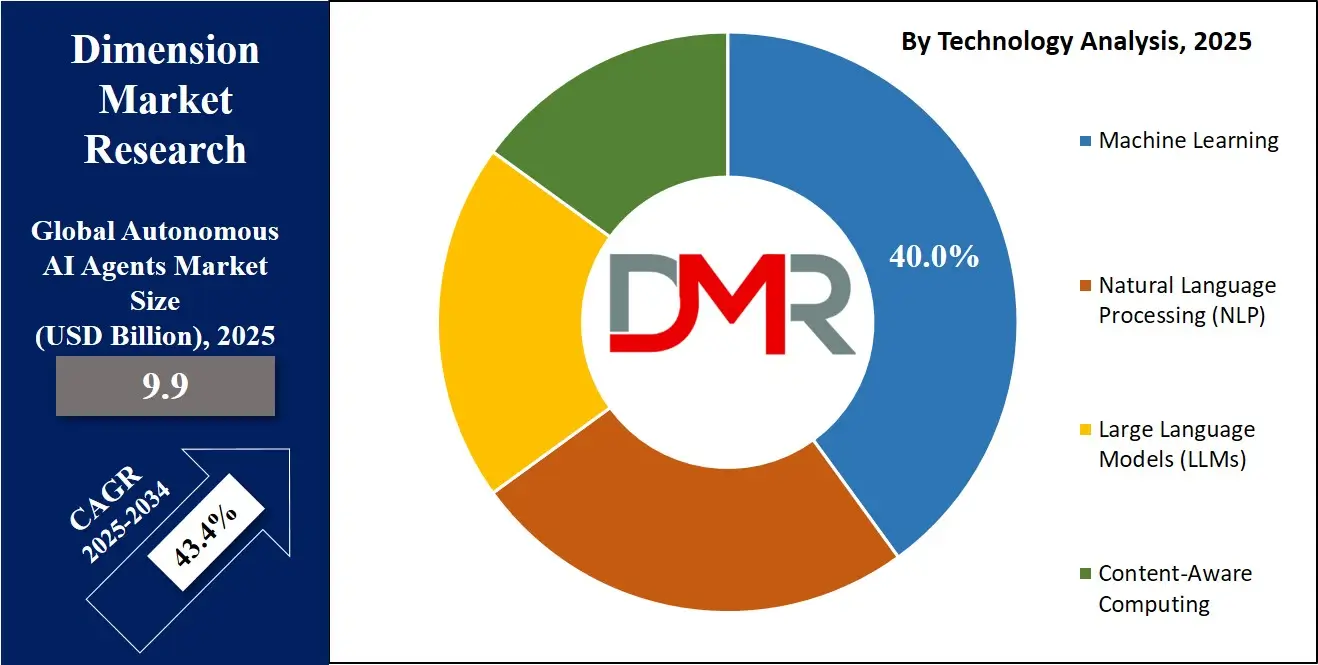

- Market Value: The global autonomous AI agents market size is expected to reach a value of USD 253.3 billion by 2034 from a base value of USD 9.9 billion in 2025 at a CAGR of 43.4%.

- By Component Segment Analysis: Software components are poised to consolidate their dominance in the component segment, capturing 55.7% of the total market share in 2025.

- By Deployment Mode Segment Analysis: Cloud deployment is anticipated to maintain its dominance in the deployment segment, capturing 45.2% of the total market share in 2025.

- By Technology Type Segment Analysis: Machine Learning technologies are expected to maintain their dominance in the technology type segment, capturing 40.9% of the total market share in 2025.

- By Business Model Segment Analysis: Subscription-Based models are expected to maintain their leadership in the business model type segment, capturing 60.1% of the market share.

- By Agent System: Single Agent Systems are poised to consolidate their dominance in the agent system type segment, capturing 65.4% of the market share in 2025.

- By Application Type Segment Analysis: Customer Service & Virtual Assistance applications are expected to consolidate their market position in the application type segment, capturing 30.3% of the total market share in 2025.

- By End-User Industry Analysis: The BFSI industry is anticipated to maintain its dominance in the end-user industry segment, capturing 35.8% of the total market share in 2025.

- Regional Analysis: North America is anticipated to lead the global autonomous AI agents market landscape with 40.7% of total global market revenue in 2025.

- Key Players: Some key players in the global autonomous AI agents market are Perko Inc., OpenAI, Google DeepMind, Microsoft, Anthropic, Meta, Amazon Web Services (AWS), IBM, Nvidia, Apple, Salesforce, Adobe, Baidu, Tencent, Huawei, Oracle, SAP, and Other Key Players.

Global Autonomous AI Agents Market: Use Cases

Autonomous AI Agents in Financial Fraud Detection: In the financial services sector, autonomous AI agents are deployed to detect fraudulent transactions in real-time using a combination of supervised machine learning algorithms, pattern recognition, and anomaly detection techniques. These agents operate continuously and autonomously across vast datasets using GPU-accelerated computing platforms such as Nvidia A100 and custom AI chips for low-latency performance. Equipped with natural language understanding and probabilistic modeling, they can monitor banking activities, flag irregularities, and take preventive actions without human intervention. These agents are integral to risk assessment frameworks, enhancing compliance and supporting real-time fraud prevention at scale.

Intelligent Virtual Healthcare Assistants: In healthcare, autonomous AI agents are revolutionizing patient engagement and diagnostics through intelligent virtual assistants. Powered by large language models like GPT and BERT, these agents interpret patient queries, retrieve medical records, and assist in triage by analyzing symptoms and providing evidence-based suggestions. Leveraging edge AI processors in medical devices and contextual computing frameworks, they ensure real-time interaction with electronic health records (EHRs) and clinical databases. These agents improve healthcare accessibility, reduce administrative burden, and support telehealth services while ensuring HIPAA-compliant data management and secure AI integration.

Smart Supply Chain Optimization: Manufacturers and logistics providers are integrating autonomous AI agents to manage and optimize supply chain operations. These agents use deep reinforcement learning and predictive analytics to forecast demand, track inventory, and autonomously coordinate with suppliers and logistics networks. Deployed on cloud platforms and enhanced by neural processing units (NPUs), these agents offer real-time decision-making capabilities, dynamic scheduling, and cost reduction through route optimization and automated procurement. The combination of IoT sensors, digital twins, and context-aware AI allows these agents to function as real-time orchestrators of complex, global supply chains.

Autonomous AI in Customer Service and Conversational AI: In customer support and service automation, autonomous AI agents are driving personalized user engagement through advanced conversational AI systems. Built using transformer-based language models and natural language generation (NLG) engines, these agents provide instant responses, resolve tickets, and escalate issues when necessary. They are deployed across omnichannel platforms and optimized using AI accelerators and voice synthesis processors for real-time performance. These agents continually learn from user interactions, enabling sentiment analysis, adaptive dialogue management, and proactive issue resolution. This enhances customer satisfaction, reduces operational costs, and transforms the service landscape into a more intelligent and responsive ecosystem.

Global Autonomous AI Agents Market: Stats & Facts

United States — National Institute of Standards and Technology (NIST)

- NIST has developed over 60 AI-related standards globally, including protocols for autonomous agents, to enhance interoperability and security.

- NIST collaborates with over 30 international bodies to align AI safety standards for autonomous systems.

- Research funded by NIST improved machine learning model robustness by 28% in autonomous AI deployments worldwide.

European Union — European Commission (EC)

- The European Commissions Horizon Europe program has allocated €2.5 billion to AI research, with a focus on autonomous agents and ethical AI between 2021-2024.

- Over 120 collaborative AI projects involving autonomous agents are active across EU member states.

- EC reports a 33% increase in AI startups focusing on autonomous agents since 2019, supported by EU innovation funds.

China — Ministry of Science and Technology (MOST)

- Chinas National AI Development Plan has directed USD 5 billion towards autonomous AI agent technologies from 2020 to 2024.

- MOST data indicates over 200 pilot projects deploying autonomous AI agents in smart manufacturing and urban management.

- The governments AI innovation hubs foster the development of over 500 AI startups working on autonomous systems.

Japan — Ministry of Economy, Trade and Industry (METI)

- METI supports more than 80 research initiatives integrating autonomous AI agents in robotics and healthcare sectors.

- Japans AI Strategy Report highlights a 40% increase in AI patents related to autonomous systems from 2018 to 2023.

- Public funding for AI agent R&D increased by 25% annually between 2020 and 2024.

South Korea — Ministry of Science and ICT (MSIT)

- MSIT has invested over USD 1 billion in autonomous AI technologies, focusing on smart cities and automotive applications.

- South Korea hosts 50+ AI testbeds supporting autonomous agent development and deployment.

- National AI strategy projects predict a 38% CAGR for autonomous agent adoption by 2030.

Canada — Innovation, Science and Economic Development Canada (ISED)

- ISED reports that 60% of Canadian AI startups incorporate autonomous agent technologies.

- The government has funded over 100 AI projects involving autonomous agents since 2019.

- Canadas AI research funding increased by 30% in 2023, emphasizing ethical autonomous systems.

United Kingdom — Office for Artificial Intelligence (OAI)

- The UK government allocated £400 million to autonomous AI research between 2021-2024.

- Over 40 autonomous AI agent pilots have been implemented in the UK healthcare and financial sectors.

- OAI reports a 35% year-on-year increase in AI talent focusing on autonomous systems.

Australia — Department of Industry, Science and Resources

- Australia has committed USD 300 million to AI and autonomous agent technologies through its national innovation plan.

- The government supports over 50 AI research collaborations with industry and academia, focusing on autonomous systems.

- AI-driven automation in agriculture, supported by government grants, improved productivity by 20%.

Germany — Federal Ministry for Economic Affairs and Climate Action (BMWK)

- BMWK has funded over 70 projects on autonomous AI agents for smart manufacturing and logistics.

- Public investment in AI increased by 28% annually, emphasizing industrial autonomous systems.

- Germanys AI strategy includes over 100 collaborations with European partners on autonomous agents.

France — National Research Agency (ANR)

- ANR has financed 60+ AI projects focusing on autonomous agents in healthcare and transportation.

- French public sector AI funding increased by 22% from 2019 to 2023, prioritizing autonomous decision-making systems.

- ANR data shows a 30% rise in autonomous AI patent applications over five years.

United Nations — International Telecommunication Union (ITU)

- ITU reports over 100 countries adopting autonomous AI frameworks aligned with global AI ethics guidelines.

- ITU facilitates international cooperation on AI safety standards, impacting autonomous agent deployments worldwide.

- Global AI capacity-building programs supported by ITU have trained 15,000+ professionals in autonomous AI technologies since 2020.

Global Autonomous AI Agents Market: Market Dynamics

Global Autonomous AI Agents Market: Driving Factors

Surge in Enterprise Automation Demand

Organizations across sectors such as finance, healthcare, and manufacturing are rapidly adopting autonomous AI agents to streamline operations and reduce human dependency in decision-making workflows. These agents, powered by machine learning models, intelligent automation, and contextual analytics, are enabling businesses to optimize efficiency, reduce response times, and enhance data-driven strategy execution. The need for self-governing systems capable of autonomous learning and adaptive behavior is fueling massive investments in AI infrastructure, cloud computing, and neural processors.

Advancements in AI Hardware and Infrastructure

The growing availability of high-performance processors like GPUs, TPUs, and edge AI chips is significantly accelerating the deployment of autonomous AI systems. These hardware advancements enable real-time data processing, complex model training, and embedded intelligence in applications such as robotics, autonomous vehicles, and virtual assistants. As AI agents rely on specialized hardware for multitasking and deep contextual reasoning, technological progress in chip design and AI accelerators is becoming a major market driver.

Global Autonomous AI Agents Market: Restraints

Ethical and Regulatory Concerns

The autonomous nature of these AI agents raises questions related to transparency, accountability, and ethical decision-making. Regulatory frameworks around explainable AI, data privacy, and algorithmic fairness are still evolving, particularly in sensitive domains like healthcare and finance. Compliance burdens, liability risks, and the lack of standardized guidelines can hinder deployment and slow innovation in the market.

High Implementation Complexity and Cost

Deploying autonomous agents requires significant investment in infrastructure, skilled personnel, and ongoing model training and optimization. Smaller organizations may face barriers in integrating these systems due to the complexity of custom development, the need for continuous supervision during initial training phases, and the interoperability issues with legacy systems. This cost-intensive nature limits adoption in resource-constrained environments.

Global Autonomous AI Agents Market: Opportunities

Expansion in Edge AI and IoT Ecosystems

As edge computing and IoT networks proliferate, autonomous agents have the opportunity to operate locally with real-time decision-making capabilities. This is especially impactful in industries like manufacturing, smart cities, and logistics, where latency and bandwidth constraints make cloud reliance inefficient. The integration of edge AI agents into physical infrastructure allows for decentralized intelligence, predictive maintenance, and autonomous control systems.

Rising Adoption in Emerging Markets

Emerging economies are accelerating digital transformation initiatives and investing in AI-driven technologies to bridge operational gaps. Governments and enterprises in regions like Southeast Asia, Latin America, and the Middle East are creating favorable environments for the deployment of autonomous AI agents across public services, healthcare delivery, and education. This global expansion presents immense growth potential for vendors and solution providers.

Global Autonomous AI Agents Market: Trends

Integration with Large Language Models (LLMs)

The convergence of autonomous AI agents with LLMs such as GPT, PaLM, and LLaMA is redefining how machines communicate, reason, and interact with users. These agents now exhibit improved language understanding, situational awareness, and multi-turn dialogue management, enabling use cases in personalized education, content generation, and advisory services. The trend toward self-improving agents that leverage LLM capabilities is accelerating across sectors.

Rise of Multi-Agent Collaboration Systems

A growing trend involves the development of systems where multiple autonomous agents collaborate to solve complex problems or coordinate tasks in distributed environments. This is evident in applications like swarm robotics, decentralized finance platforms, and digital twins. These systems rely on distributed learning, inter-agent communication protocols, and shared goal optimization, marking a shift from isolated AI agents to intelligent, coordinated ecosystems.

Global Autonomous AI Agents Market: Research Scope and Analysis

By Component Analysis

In the Autonomous AI Agents market, software components are expected to consolidate their dominance by capturing 55.7% of the total market share in 2025. This growth is fueled by the critical role of software in enabling autonomous decision-making, self-learning, and intelligent task execution.

Software forms the core operational layer of AI agents, encompassing machine learning algorithms, agent orchestration frameworks, large language models, reasoning engines, and contextual awareness modules. With continuous advancements in AI software architecture, such as reinforcement learning, multi-agent coordination, and real-time analytics, developers can create highly adaptable and scalable agents customized to various industries.

Cloud-native AI platforms, APIs for NLP and computer vision, and low-code/no-code environments further accelerate the deployment of autonomous agents. These software solutions are modular, allowing integration with enterprise systems, IoT devices, and real-time monitoring dashboards, which broadens their application scope across sectors such as healthcare, finance, and smart manufacturing.

On the other hand, hardware components, though representing a smaller share of the market, serve as the physical backbone supporting the execution of advanced AI models and real-time processing. This segment includes AI accelerators like GPUs, TPUs, NPUs, edge AI chips, and high-performance servers optimized for deep learning workloads. As autonomous AI agents grow in complexity and scale, there is a rising demand for hardware that can support high-throughput inference, low-latency data exchange, and decentralized deployment in edge environments.

For instance, in autonomous vehicles and robotics, edge computing hardware is essential to enable immediate decision-making without cloud dependence. Additionally, the development of dedicated AI chipsets customized for agent-based processing is driving hardware innovation. These specialized processors reduce energy consumption and improve computation speed, making them indispensable in real-time, resource-constrained applications. Overall, while software dominates the segment by functionality and accessibility, hardware remains critical for delivering the performance and responsiveness required by next-gen autonomous systems.

By Deployment Mode Analysis

In the Autonomous AI Agents market, cloud-based deployment is set to lead the deployment type segment by capturing 55.7% of the total market share in 2025. This dominance is primarily driven by the scalability, flexibility, and cost-efficiency offered by cloud platforms, allowing enterprises to access AI capabilities without heavy upfront infrastructure investment. Cloud environments enable autonomous agents to leverage distributed computing, vast data lakes, and seamless integration with AI services such as model training APIs, natural language processing engines, and real-time analytics tools.

Additionally, cloud service providers like AWS, Microsoft Azure, and Google Cloud are offering pre-trained models and auto-scaling AI frameworks, which accelerate deployment cycles and support rapid experimentation. This model is particularly beneficial for industries with variable workloads or global operations, where centralized cloud access ensures uniform performance and updates across multiple geographies.

On-premise deployment, while gradually becoming less dominant, continues to hold strong relevance in sectors requiring strict data control, low latency, and regulatory compliance. Industries like defense, banking, and healthcare often opt for on-premise solutions to ensure higher security, full data ownership, and offline processing capabilities. These setups use customized AI accelerators, local servers, and private networks to support autonomous agents in mission-critical scenarios.

Despite higher initial costs and maintenance requirements, on-premise deployment is favored in use cases involving sensitive or confidential data, where cloud reliance poses security or sovereignty risks. Furthermore, on-premise deployments allow for more fine-tuned customization and integration with legacy IT systems, ensuring greater continuity and control over agent behavior and performance.

By Technology Analysis

In the Autonomous AI Agents market, machine learning (ML) technologies are projected to remain dominant within the technology type segment, capturing 40.9% of the total market share in 2025. This dominance is driven by MLs foundational role in enabling autonomous agents to learn from data, identify patterns, and make intelligent decisions with minimal human intervention. Machine learning algorithms such as supervised learning, reinforcement learning, and unsupervised clustering are widely used to enhance agent autonomy, adaptability, and context-awareness.

These agents continuously refine their behavior through feedback loops and dynamic environments, which is crucial for applications like robotics, predictive maintenance, and financial modeling. The proliferation of advanced ML frameworks like TensorFlow, PyTorch, and JAX, along with AI-optimized hardware, enables developers to train complex agent models faster and at scale. Moreover, the integration of federated learning and edge ML allows these agents to operate independently in real-time scenarios with high privacy and low latency.

Natural Language Processing (NLP), while not leading in overall market share, plays a pivotal and rapidly growing role in enabling human-AI interaction within autonomous systems. NLP equips agents with the ability to understand, interpret, and respond to human language, making it a key enabler for conversational AI, virtual assistants, and customer service automation.

Through transformer-based architectures like BERT, GPT, and T5, NLP allows agents to handle sentiment analysis, intent recognition, language translation, and contextual dialogue generation. These capabilities are critical in industries such as healthcare, e-commerce, and education, where user interaction and decision-making rely heavily on language comprehension.

As demand rises for explainable and user-friendly AI, the importance of NLP in enhancing natural human-agent communication is growing significantly. With the advancement of large language models and multimodal understanding, NLP-based autonomous agents are evolving beyond basic Q&A functionalities to perform sophisticated tasks like document summarization, negotiation, and advisory services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Business Model Analysis

In the Autonomous AI Agents market, subscription-based business models are expected to maintain their leadership, capturing

60.1% of the market share. This dominance stems from the predictability and steady revenue streams that subscription services provide to both vendors and customers. Enterprises prefer subscription models because they offer scalable access to AI agent platforms, software updates, and ongoing support without requiring large upfront capital expenditures.

Subscription plans often include tiered offerings based on usage, features, and service levels, allowing businesses to select packages that best fit their operational needs and budgets. This model also encourages continuous innovation and improvements from providers, as they are incentivized to regularly enhance AI algorithms, security protocols, and integration capabilities to retain subscribers. The subscription approach aligns well with cloud-based deployments and SaaS platforms, which facilitate seamless, on-demand delivery of autonomous AI solutions across diverse industries.

Conversely, the pay-per-use model is gaining traction as an alternative business approach, especially for organizations with variable or seasonal demand for autonomous AI capabilities. Under this model, customers are billed based on their actual consumption of AI agent resources, such as processing time, API calls, or specific service usage. This flexible pricing structure is attractive to startups and enterprises looking to minimize costs by avoiding long-term commitments and only paying for what they use.

Pay-per-use is particularly beneficial in high-computation scenarios like large-scale data analysis, training complex machine learning models, or sporadic deployment of specialized AI agents for short-term projects. It promotes efficient resource allocation and can encourage broader adoption among companies hesitant to invest heavily up front. Together, subscription and pay-per-use models are shaping the market landscape by catering to diverse customer preferences and fostering greater accessibility to autonomous AI technologies.

By Agent System Analysis

In the Autonomous AI Agents market, Single Agent Systems are expected to dominate the agent system type segment, capturing 65.4% of the market share in 2025. Single-agent systems are designed to operate independently, focusing on specific tasks or objectives within a defined environment. These systems leverage machine learning, decision-making algorithms, and contextual awareness to perform autonomous functions without needing to coordinate with other agents.

Their streamlined architecture makes them highly efficient for applications like virtual assistants, autonomous drones, and robotic process automation, where focused, task-specific intelligence is crucial. The relative simplicity of single-agent systems facilitates faster deployment, easier troubleshooting, and reduced computational overhead, making them attractive for enterprises seeking straightforward AI automation solutions. Moreover, single-agent systems can be optimized with advanced processors and edge computing devices to deliver real-time responsiveness and high accuracy in isolated environments.

On the other hand,

Multi-Agent System (MAS) represents a more complex and collaborative form of autonomous AI, where multiple agents interact, communicate, and coordinate to achieve shared or individual goals. These systems are gaining momentum in areas such as swarm robotics, distributed sensor networks, and decentralized finance, where cooperation among agents can lead to enhanced problem-solving capabilities, scalability, and robustness.

Multi-agent systems utilize communication protocols, consensus algorithms, and game theory to manage interactions and conflicts between agents, enabling sophisticated behaviors like negotiation, task allocation, and collective learning. Although MAS require higher computational resources and intricate design, their ability to handle complex, dynamic environments and perform parallel processing makes them indispensable for applications demanding flexibility and adaptability. As AI research advances, the integration of multi-agent collaboration is expected to grow, complementing single-agent dominance by addressing scenarios where teamwork and distributed intelligence are critical.

By Application Analysis

In the Autonomous AI Agents market, Customer Service and Virtual Assistance applications are projected to solidify their market position by capturing 30.3% of the total market share in 2025. These applications leverage advanced natural language processing, machine learning algorithms, and contextual understanding to provide personalized, real-time support to users across various industries.

Autonomous AI agents in this space can handle tasks such as query resolution, appointment scheduling, troubleshooting, and proactive engagement without human intervention. The integration of conversational AI, sentiment analysis, and voice recognition technologies enables these agents to deliver seamless and human-like interactions, improving customer satisfaction and operational efficiency.

Cloud-based deployments and edge computing further enhance scalability and responsiveness, allowing organizations to offer 24/7 support at reduced costs. This application segment is especially prominent in sectors like retail, banking, and telecommunications, where high volumes of customer interactions demand automated yet intelligent solutions.

Medical Imaging represents another critical application within the Autonomous AI Agents market, focusing on enhancing diagnostic accuracy and efficiency in healthcare. Autonomous agents analyze complex imaging data from modalities such as MRI, CT scans, and X-rays using deep learning, computer vision, and pattern recognition technologies. These agents assist radiologists by detecting anomalies, segmenting tissues, and prioritizing cases based on severity, thereby accelerating diagnosis and improving patient outcomes.

The incorporation of AI accelerators and high-performance computing enables real-time image processing and multi-modal data fusion, which are essential for precise medical assessments. Moreover, these autonomous systems support personalized treatment planning and predictive analytics by correlating imaging findings with patient history and genomic data. As healthcare providers adopt AI-driven workflows, medical imaging applications are becoming pivotal in reducing diagnostic errors, lowering operational costs, and expanding access to quality care.

By End-User Industry Analysis

In the Autonomous AI Agents market, the Banking, Financial Services, and Insurance (BFSI) industry is expected to maintain its dominance, capturing 35.8% of the total market share in 2025. This leadership is driven by the BFSI sector’s strong demand for automation, risk management, fraud detection, and personalized customer experiences.

Autonomous AI agents in BFSI are widely used for tasks such as credit scoring, algorithmic trading, compliance monitoring, and chatbot-enabled customer service. These agents leverage advanced machine learning models, natural language processing, and real-time data analytics to enhance decision-making accuracy and operational efficiency.

The integration of AI accelerators and edge computing ensures faster processing of vast financial datasets while maintaining stringent security and regulatory compliance. Furthermore, autonomous systems enable financial institutions to reduce costs, improve customer engagement, and detect anomalies proactively, making them indispensable for the evolving digital finance landscape.

Healthcare represents another significant end-user segment for autonomous AI agents, with growing adoption driven by the need to improve patient care, diagnostics, and operational workflows. Autonomous agents in healthcare support functions such as medical imaging analysis, patient monitoring, drug discovery, and personalized treatment planning.

These systems utilize deep learning, computer vision, and predictive analytics to interpret complex medical data and provide actionable insights for clinicians. The use of AI-powered autonomous agents facilitates faster diagnosis, reduced human error, and enhanced patient outcomes. Additionally, healthcare providers benefit from AI-enabled workflow automation, which streamlines administrative tasks and resource allocation. As regulatory bodies recognize the potential of AI in healthcare, the sector is witnessing accelerated integration of autonomous systems to meet rising demands for precision medicine and cost-effective care delivery.

The Autonomous AI Agents Market Report is segmented on the basis of the following:

By Component

- Software

- AI Algorithms & Frameworks

- Middleware Platforms

- Analytics & Design Engines

- Hardware

- AI Accelerators

- Edge Devices & Sensors

- Robotics Hardware

- Services

- Integration & Consulting

- Maintenance & Support

- Training & Implementation

By Deployment Mode

- Cloud

-

Public Cloud Platforms

-

Private Cloud Platforms

- Hybrid Cloud Platforms

-

On-Premise

-

Edge

-

Edge Gateways

-

IoT Edge Gateways

- Real-Time Processing Nodes

By Technology

By Business Model

- Subscription-Based

-

Pay-Per-Use

-

Usage-Based Billing

- API Calls/Compute Time Pricing

-

Freemium

-

Free Basic Features

- Premium Upgrades & Add-ons

By Agent System

- Single Agent Systems

-

Virtual Assistants

- Task-Specific Bots

-

Multi-Agent Systems

-

Collaborative Robotics

-

Autonomous Fleets

- Distributed Sensor Networks

By Application

By End-User Industry

- BFSI

-

Healthcare

-

Diagnostic Support

- Remote Patient Monitoring

- Treatment Recommendation Systems

-

Retail & E-Commerce

-

IT & Telecom

-

Network Optimization

-

Predictive Maintenance

- Virtual Network Assistants

Global Autonomous AI Agents Market: Regional Analysis

Region with the Largest Revenue Share

North America is poised to lead the global autonomous AI agents market, capturing 40.7% of the total market revenue in 2025. This dominance is driven by the region’s strong technological infrastructure, significant investments in AI research and development, and the presence of numerous key market players and startups specializing in autonomous AI solutions. The U.S. and Canada benefit from advanced cloud computing capabilities, high adoption of machine learning and natural language processing technologies, and supportive regulatory frameworks that foster innovation.

Additionally, North America’s diverse industry landscape, including finance, healthcare, retail, and defense, actively leverages autonomous AI agents to enhance operational efficiency, customer experience, and decision-making processes. The region’s focus on integrating AI with edge computing and IoT further strengthens its leadership position, enabling real-time autonomous agent deployment across various sectors.

Region with significant growth

The Asia-Pacific region is expected to register the highest compound annual growth rate (CAGR) in the autonomous AI agents market, driven by rapid digital transformation, growing AI adoption across industries, and significant government investments in artificial intelligence and smart technologies. Countries like China, India, Japan, and South Korea are accelerating the integration of autonomous AI agents in sectors such as manufacturing, healthcare, retail, and telecommunications.

The region benefits from a large pool of tech-savvy talent, expanding startup ecosystems, and growing infrastructure for cloud computing and edge AI, which collectively fuel market expansion. Additionally, rising demand for automation to improve productivity, reduce operational costs, and enhance customer engagement is propelling the rapid uptake of AI agent technologies, making Asia-Pacific the fastest-growing market in this space.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Autonomous AI Agents Market: Competitive Landscape

The global autonomous AI agents market features a highly competitive landscape marked by the presence of both established tech giants and innovative startups driving rapid advancements in AI capabilities. Leading companies invest heavily in research and development to enhance machine learning algorithms, natural language processing, and multi-agent coordination, aiming to deliver scalable and adaptable solutions across diverse industries.

Strategic partnerships, mergers, and acquisitions are common as players seek to expand their technology portfolios and geographic reach. Companies focus on developing specialized AI chips, cloud-based platforms, and edge computing solutions to meet the demand for real-time processing and low-latency applications.

The competition also centers on improving user experience through explainable AI, security enhancements, and seamless integration with existing enterprise systems. This dynamic environment fosters continuous innovation, enabling players to capture market share by offering differentiated autonomous AI agents customized to customer-specific needs and emerging use cases globally.

Some of the prominent players in the Global Autonomous AI Agents are:

- OpenAI

- Google DeepMind

- Microsoft

- Anthropic

- Meta

- Amazon Web Services (AWS)

- IBM

- Nvidia

- Apple

- Salesforce

- Adobe

- Baidu

- Tencent

- Huawei

- Oracle

- SAP

- Cohere

- Hugging Face

- Character.AI

- Inflection AI

- Other Key Players

Global Autonomous AI Agents Market: Recent Developments

- March 2025: Google DeepMind acquired Anthropic to strengthen its AI research and autonomous agent capabilities.

- January 2025: Microsoft completed the acquisition of Cohere to enhance its natural language processing and AI agent services.

- November 2024: Nvidia acquired Hugging Face to expand its AI model deployment and autonomous learning technologies.

- September 2024: IBM acquired Character.AI to boost its AI conversational agents and enterprise AI solutions.

- July 2024: Amazon Web Services (AWS) acquired Inflection AI to improve cloud-based autonomous AI agent offerings.

- May 2024: Meta acquired OpenAI’s partner startup to deepen its AI-driven virtual assistant and agent ecosystem.

- March 2024: Oracle acquired Salesforce’s AI division to integrate advanced autonomous agent features into its enterprise cloud solutions.

- January 2024: Baidu acquired a leading Chinese autonomous AI agent startup to accelerate AI adoption in Asia-Pacific.