What is the Autonomous Chemical Laboratory Market Size?

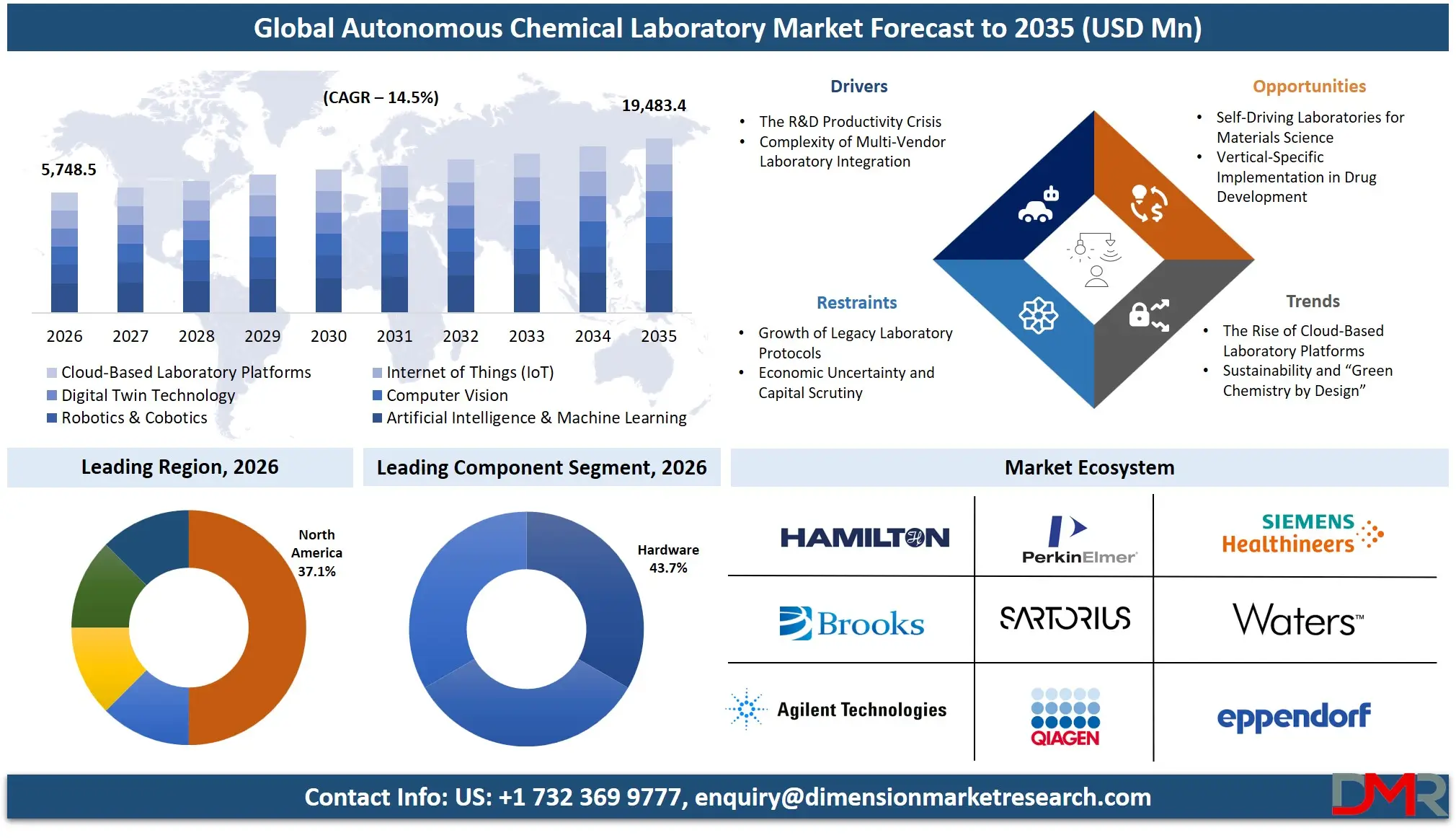

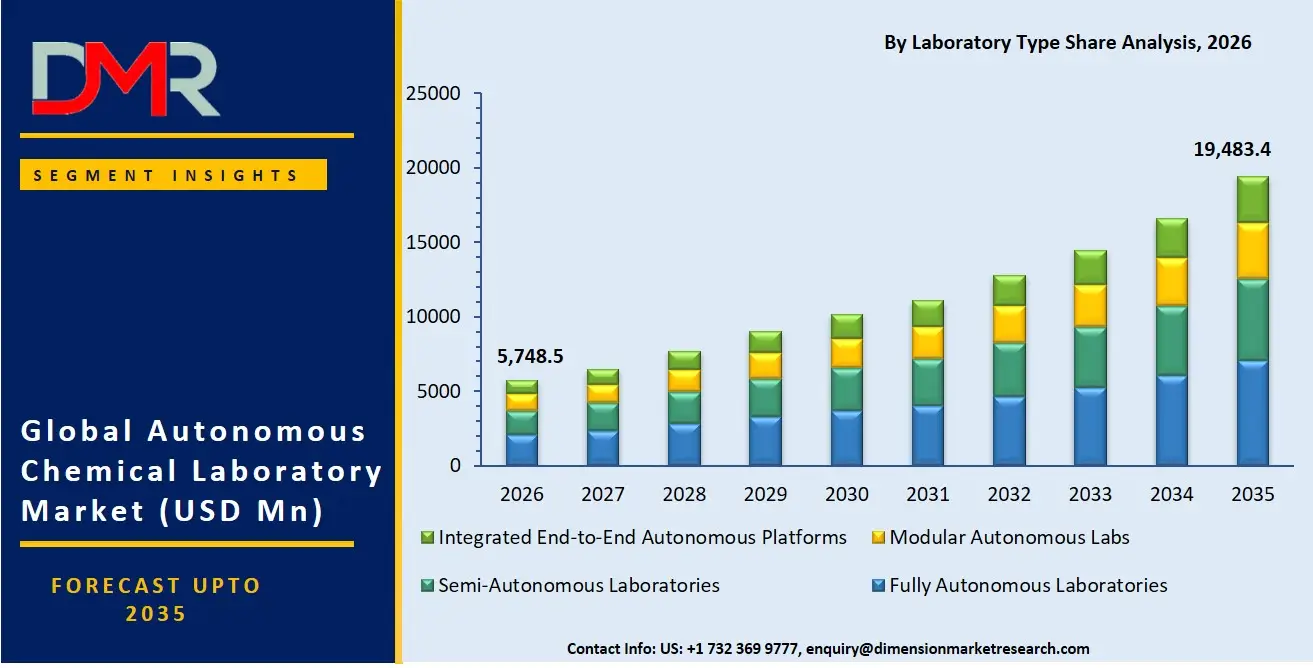

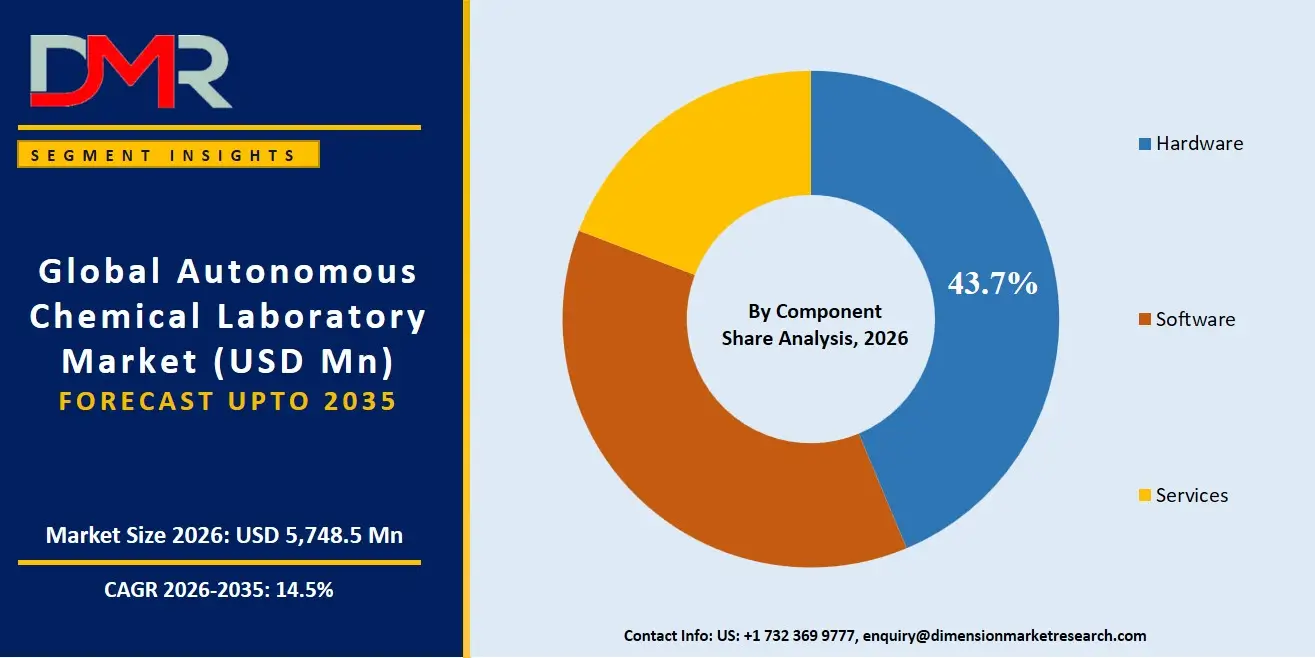

The Global Autonomous Chemical Laboratory Market is expected to reach a value of USD 5,748.5 million in 2026, and it is further anticipated to reach USD 19,483.4 million by 2035, growing at a CAGR of 14.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The autonomous chemical laboratory market has been growing at a high rate with research institutions and chemical enterprises increasing the pace of digital transformation and transitioning out of manual, human-dependent workflows to AI-driven, robotic experimentation.

The market consists of hardware, software, and specialized services which assist organizations in building, integrating, and operating self-driving labs for chemical synthesis, drug discovery, and materials science. The need for integrated autonomous platforms is now emerging due to the demand for faster research cycles, better experimental reproducibility and the need to handle high dimensional chemical information. The most common are pharmaceutical companies and chemical manufacturers, and cloud-based lab platforms are still popular for their scalability and for enabling orchestration of geographically dispersed research. Pharmaceutical, materials science, and specialty chemical companies are important players since they require secure, compliant and continuously operating research ecosystems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

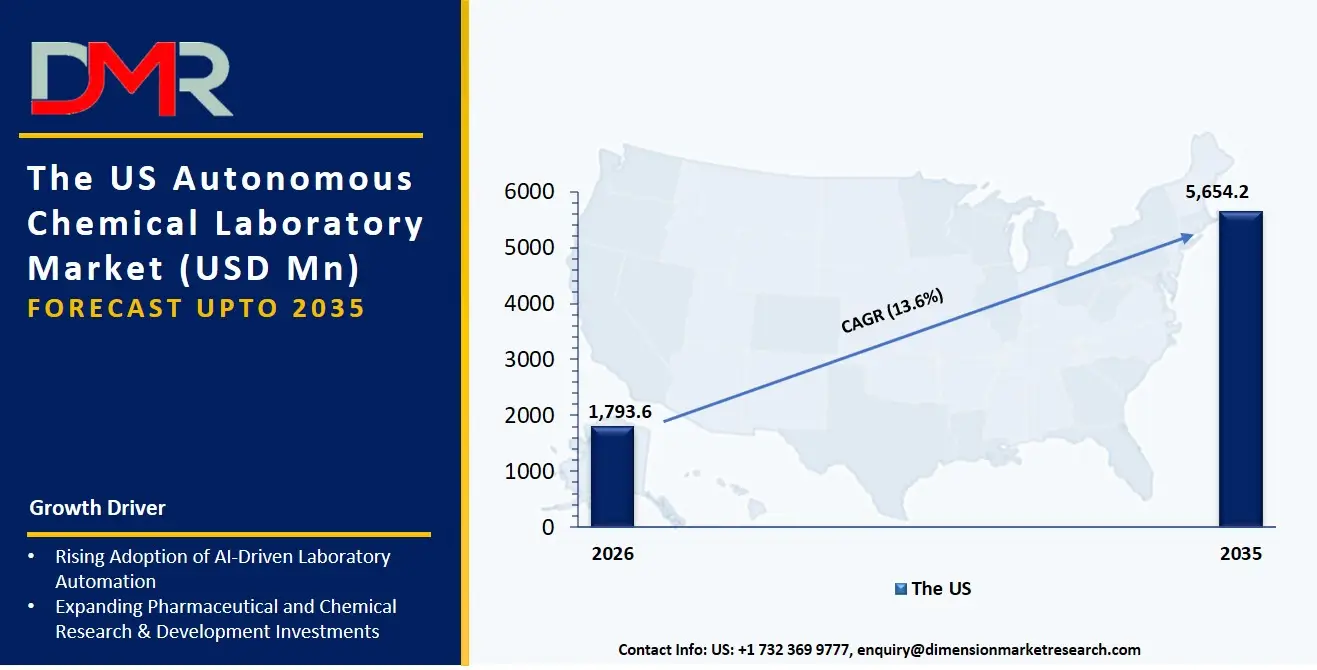

The US Autonomous Chemical Laboratory Market

The US Autonomous Chemical Laboratory Market is projected to reach USD 1,793.6 million in 2026 at a compound annual growth rate of 13.6% over its forecast period, culminating in a value of USD 5,654.2 million by 2035.

The US remains the biggest and most advanced market for autonomous chemical laboratories, with large pharmaceutical firms actively pursuing modernization through research and development and the proliferation of advanced robotics and AI research hubs. The market has been characterized by the high demand for AI and ML software, which are focused on transforming the older trial-and-error chemistry approach into closed-loop experimentation designed with AI. Not only that, but the use of generative AI tools in molecular design is also resulting in a comparable demand for data interpretation and optimization services to manage data governance and reproducibility standards in automated research processes.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Autonomous Chemical Laboratory Market

The Europe Autonomous Chemical Laboratory Market is estimated to be valued at USD 1,670.0 million in 2026 and is further anticipated to reach USD 5,580.0 million by 2035 at a CAGR of 14.3%. Regulatory requirements, such as REACH and changing chemical safety regulations, have a major influence on the European market and so the necessity for high throughput chemical analytical testing and completely auditable autonomous data trails. A parallel development of accelerated growth of integrated end-to-end autonomous platforms is also taking place in the region, as the specialty chemical and agrochemicals industry in Germany and Switzerland seek to reconcile the vision of sustainable chemistry with shortened R&D cycles. In addition, academic and research institutes are challenging service providers to create dedicated digital twin technology implementations to provide experimental predictability and data interoperability across pan-European research ecosystems.

The Japan Autonomous Chemical Laboratory Market

The Japan Autonomous Chemical Laboratory Market is projected to be valued at USD 580.0 million in 2026. It is further expected to witness robust growth, holding USD 1,820.0 million in 2035 at a CAGR of 13.5%. The Japanese market is special, and the corporate efforts towards digital transformation of chemical manufacturing are in response to the falling numbers of Japanese workers and existing legacy systems that are still manually operated in laboratories. A significant amount of the spend is on business transformation consulting and modular deployment services, as large conglomerates move critical quality control processes away from all manual to semi-autonomous, and fully autonomous, processes. There's also a big requirement to be deeply integrated in the local market and to fill the gap between legacy industrial control systems and new IoT capable analytical instruments, creating a niche in computer vision integration for laboratory analytics and process automation.

Key Takeaways

- Market Size & Forecast: The Global Autonomous Chemical Laboratory market is projected to reach USD 5,748.5 million in 2026, expanding dramatically to USD 19,483.4 million by 2035, driven by the confluence of enterprise AI adoption in R&D and the pressing need to modernize aging research infrastructure.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 14.5%, due to the critical scarcity of in-house engineers for AI and robotics and the increasing complexity of handling self-optimising chemical reaction platforms and closed loop experimentation systems.

- Primary Growth Drivers: The primary growth drivers include the growing adoption of automated CapEx-OpEx hybrid models over manual labor-intensive labs, the need for AI and machine learning strategy consultancies to prevent costly experimental dead ends, and the adoption of end-to-end autonomous platforms, which demands specialized software and services capabilities.

- Key Market Trends: The emergence of domain-specific autonomous labs, such as materials science labs and drug discovery labs, is a major trend, while the integration of generative AI in data interpretation and optimization services is expected to automate the remediation of experimental failures, and the adoption of digital twin technology is gaining traction as boards increasingly value the importance of reproducibility and scalability.

- By Deployment Mode Analysis: Cloud-integrated deployment models are expected to dominate enterprise discussions due to data gravity and collaborative needs. As a result, professional services are increasingly being asked to create hybrid architectures that integrate on-premise lab equipment with cloud-based AI innovation engines.

- By End User Analysis: Pharmaceutical companies and chemical manufacturers are the most lucrative end users as they need high throughput and high regulatory compliance. Academic and research institutes are the fastest-growing segment, since the scientific data complexity is demanding that scientists have powerful data interpretation software and automated experimentation platforms.

- Regional Leadership: North America is poised to dominate this market with 37.1% of the market share in 2026 owing to the technological ecosystem in the region, which maximizes the use of this infrastructure and makes it the leader in this market.

What is the Autonomous Chemical Laboratory?

Autonomous Chemical Laboratories are dedicated, integrated chemical laboratory systems that integrate hardware, software and services from various third party experts, systems integrators and consultancies to help organisations automate the entire chemistry research lifecycle. Unlike single purpose software or standalone lab equipments, these systems are related to the how of hands free experiments. These include hardware tools such as robotic arms and liquid handlers for physical execution, software using AI/machine learning to design and plan experiments and services to integrate the whole into a self-driving lab. More than 80% of large pharma R&D budgets are using automation to enable experimental throughput, data governance and reproducibility, thus turning chemical research investments into science rather than data points, and autonomous lab platforms are needed for this.

Use Cases

- Closed-Loop Drug Discovery in Pharma: Pharmaceutical companies employ an entirely autonomous laboratory integrator: an AI designs a new molecule, a robot synthesizes it, and the AI re-designs it, based on the results, without any human involvement.

- Materials Acceleration in Manufacturing: Chemical manufacturers leverage integrated end-to-end autonomous platforms to quickly prototype and test thousands of material formulations, such as advanced polymers or battery materials, to simulate performance prior to physical validation.

- Regulatory Toxicology in Agrochemicals: Agrochemical companies have to deploy architectures to meet strict regulations for the environmental tests conducted on agrochemicals while using cloud-based laboratory platforms with specialized services to ensure audit trails for the preparation of samples and the execution of experiments are immutable and traceable.

- Remote Academic Collaboration: Research institutes implement IoT and hybrid deployment models to remotely link physical laboratory equipment in a central campus with AI software from the cloud for them to submit compounds for synthesis and receive results for data interpretation and optimization.

How AI is Transforming the Autonomous Chemical Laboratory Market

AI is revolutionizing the autonomous chemical laboratory by reframing the way experiments are planned and performed, from human-planned sequential order to an AI-optimized iterative loop. The software component can use AI and machine learning to interpret multi-dimensional experimental data to automatically determine the optimal next experiment, significantly lowering the number of iterations required to optimize the reaction conditions, and saving several months in a project. In the meantime, data interpretation and optimization tools powered by AI enable researchers to manage the experimental direction more effectively by recognizing unusual results, predicting chemical properties, and proposing new synthesis routes to optimize the discovery of molecules.

The same applies to laboratory execution and strategy projects, which are also swirling around AI. In services, intelligent computer vision systems ensure that the robotic experiments are monitored in real time for any anomalies such as precipitates or color changes that may be occurring, alerting the operator to any variation from the standard operating procedure. Beyond this, generative AI tools are augmenting experiment setup, modeling possible synthesis pathways and predicting potential outcomes to provide research teams with a sense of chemical feasibility prior to investing valuable lab resources.

Market Dynamics

Key Drivers in the Global Autonomous Chemical Laboratory Market

The R&D Productivity Crisis

The pharmaceutical and chemical industry is facing a recognized problem of lack of productivity, with the cost of discovering and commercializing a new molecule increasing by a factor of ten and the time required for the process increasing by a factor of two. Today's need for faster, lower cost and reproducible science far exceeds the capabilities of traditional manual science laboratories. This is driving enterprises to invest in self-contained laboratory platforms, instead of just human-led experiment-by-experiment trial-and-error. These systems help in the critical functions such as automated sample preparation, high throughput experiment execution and continuous analytical testing. The use of such systems enables organisations to speed up scientific discoveries and reduce the likelihood of human error and bias that often delays projects.

Complexity of Multi-Vendor Laboratory Integration

Large enterprises are likely to have legacy analytical equipment from various vendors and the challenge of integrating them with new robotic equipment and AI software is enormous. To enable the synch of robotics and cobotics, computer vision inspection, data onboarding from multiple analytical detectors and orchestration of experiments in the cloud with different communication protocols and data standards. Without the help of expert systems integrators, this complexity can lead to inefficiencies, data silos, and security vulnerabilities. Therefore, the demand for dedicated solutions that can help businesses to deploy such integrated end-to-end autonomous platforms within their R&D premises is increasing.

Restraints in the Global Autonomous Chemical Laboratory Market

Inertia of Legacy Laboratory Protocols

In most mature chemical and pharmaceutical companies, there are still well established experimental protocols that were developed, optimized and validated over decades, and represent a wealth of institutional knowledge, but also a barrier to change. However even though an autonomous lab can offer higher efficiency and higher reproducibility, the potential to re-validate automated versions of complex multi-step syntheses or analytical procedures is a risk and cost. The migration of data from paper or static electronic lab notebooks to structured machine-readable ones involves careful planning and expertise in the domain. Organizations are concerned about disruption to the normal process of regulatory filing, tacit human expertise and unknown costs of transition. As a result, this technical debt legacy slows the transition to completely autonomous labs and is likely to stall or fragment wider digital transformation initiatives.

Economic Uncertainty and Capital Scrutiny

The uncertainty in the business environment and unstable economies have left organisations less willing to invest in high CapEx laboratory equipment and longer-term consulting contracts. Despite the fact that R&D transformation is a strategic priority, executives are under pressure to demonstrate the payment of every dollar spent, and the scientific results of those investments. Autonomous lab providers (with a long-term service model, including robotics and modular fully automated components) are subjected to additional scrutiny. Businesses have become accustomed to small projects that deliver quick productivity wins or cost savings and are driven by software. Delays are more likely to be put in place until providers can prove they will receive a near term payday in experimental velocity, such as long-term strategy and full-lab buildouts. This is forcing hardware and software vendors to focus more on performance and results in their offerings.

Growth Opportunities in the Global Autonomous Chemical Laboratory Market

Self-Driving Laboratories for Materials Science

Creating secure, cloud-integrated, AI-driven materials acceleration platforms is one of the major growth opportunities for the autonomous chemical laboratory market, as this helps materials science and clean energy organizations. While numerous companies have turned to exploiting computational chemistry tools, there are now companies that would like to have their own physical autonomous labs that can systematically explore large formulation spaces based on their IP policy. It takes specialized expertise in digital twin technology, high-throughput chemical synthesis, and AI orchestration frameworks to develop these sophisticated settings. Laboratory service providers can help companies to develop these scalable, self-optimizing research ecosystems, which automate the identification of new catalysts, battery materials and polymers. The area has the potential to create high demand for highly specialized hardware, AI software, and integration services.

Vertical-Specific Implementation in Drug Development

Professional services are becoming an increasingly important part of the autonomous lab vendor landscape as new parties are developing solutions tailored to the drug discovery market, requiring both expertise in lab technology and in understanding the process of drug development. Those are drug-discovery-centric robotic platforms, quality control systems that are compliant with GMP, and AI modules for predicting toxicology. The pharmaceutical and contract research organization (CRO) industries have demanding FDA and EMA regulatory requirements and special pharmacokinetic profiling requirements. Thus, they require implementation partners that comprehend autonomous lab technology and the pharmaceutical industry compliance framework. Service providers can enhance their offerings by providing seamless integration of end-to-end platforms with existing electronic lab notebooks, adapting workflows to meet GxP standards, and customizing AI models for specific therapeutic areas.

Trends in the Global Autonomous Chemical Laboratory Market

The Rise of Cloud-Based Laboratory Platforms

Cloud-based laboratory platforms are becoming increasingly adopted in organizations as an alternative to traditional, siloed on-premise data management. Instead of having robots and instruments run solo and teams work independently in various labs across a geopolitical area, enterprises are building centralized cloud portals to create a single control plane for these geographically distributed robotic labs. These platforms allow for remote execution of experiments, centralized data collection, and collaborative training of AI models. In response, independent lab component suppliers are offering expertise in hybrid deployment, data security and workflow automation. For pharmaceutical companies where multiple high throughput screening campaigns are often conducted at the same time across sites around the world, this trend is especially important as it translates into the need for seamless cloud-enabled services.

Sustainability and "Green Chemistry by Design"

Environmental sustainability is also emerging as a key aspect in chemical R&D decisions as companies are under pressure to meet ESG objectives and minimize chemical waste. Businesses are now seeking ways to autonomously pursue lab strategies that could lead to the discovery of more benign methods of synthesis, fewer solvents, and better yields, all while having a lower environmental impact. This has brought about the need for specialized optimization and digital twin services. Professional service providers help organizations to specify AI-controlled experiment execution to explicitly optimize sustainability measures in parallel to functional performance, leading to a virtuous circle of "green chemistry by design" that reduces material cost and environmental footprint.

Research Scope and Analysis

The research scope and analysis of autonomous chemical laboratories covers key segments including hardware, laboratory type, AI & ML technology, cloud deployment, workflow stages, applications, and end users, highlighting strong adoption driven by automation, efficiency, and drug discovery advancements.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

Hardware is projected to be dominated by the component segment as the autonomous chemical laboratories are dependent on cutting-edge robotic infrastructure, automated liquid handling systems, robotic arms, smart sensors, spectroscopy platforms, chromatography instruments, and high throughput screening platforms. These physical systems are the backbone of the operation needed to perform experiments with little or no human involvement. To keep pace with the rising speed of experimentation, reproducibility and the minimization of operational error, while enabling continuous experimentation workflows, pharmaceutical companies, chemical manufacturers and advanced research institutes are investing heavily in laboratory automation hardware. In addition, the quick convergence of precision robotics and AI-powered lab ecosystems is driving further demand for hardware. Furthermore, the cross-over of adoption of modular robotic platforms and automated analytical instruments among drug discovery and materials science applications is leading to hardware leadership, since labs will always choose scalable, high-performance infrastructure that will support fully automated experimentation environments.

By Laboratory Type Analysis

The laboratories type segment is poised to be led by fully autonomous laboratories because of the rising demand for experimental environments that can self-optimize by designing, executing, analyzing, and improving experiments in real time. These laboratories combine robotics, artificial intelligence, machine learning and cloud-based orchestration systems to minimize human intervention and boost research productivity. Fully autonomous platforms are becoming more popular for pharmaceutical and specialty chemical manufacturers, as they enhance the ability to reproduce experiments, accelerate the innovation cycle and lower the cost of operations resulting from labor-intensive workflows. Also, as molecular discovery becomes increasingly complex and the research and development of advanced materials increasingly adapts, closed-loop autonomous systems that continuously experiment and adaptively optimize are increasingly being adopted. Additionally, there is a growing emphasis on next generation autonomous lab infrastructure in scientific research and innovation, funded by government research entities and leading industrial research labs, that enables scalable, high throughput scientific discovery and innovation.

By Technology Analysis

The technology segment is expected to be led by artificial intelligence & machine learning, which is the foundation of intelligence that allows autonomous experimentation, predictive modeling, and adaptive decision-making in chemical labs. The AI algorithms can process vast amounts of experimental data, uncovering chemical trends that might not be apparent to human researchers, and suggest experimental steps and reaction conditions, often requiring little human intervention. By minimizing the need for trial-and-error experimentation, machine learning models also streamline the process of discovering new drugs, developing catalysts, and creating innovative materials. AI technologies are gaining traction in pharmaceuticals and chemical manufacturing for the purposes of boosting lab productivity, precision and reducing research expenses. This is further bolstered by the rising adoption of generative AI, reinforcement learning, and autonomous laboratory software solutions. Furthermore, the use of AI alongside robotics and digital twin systems facilitates ongoing optimization, real-time process control, and autonomous, scalable research operations in various sectors.

By Deployment Mode Analysis

Cloud-based deployment is anticipated to be the dominant mode of deployment in the market due to growing need of autonomous chemical laboratories to have scalable computing infrastructure, remote accessibility, centralized data management, and capabilities for real-time collaboration. Cloud-based laboratory solutions enable ongoing monitoring of robotic workflows, AI-driven experiment orchestration, and easy integration and sharing of analytical data across geographically-distributed research facilities. Cloud-based deployment is popular among pharmaceutical and biotechnology firms as it facilitates quicker computational modelling, efficient data sharing and faster collaboration among research teams. Cloud integration leadership is further bolstered by the increasing use of "digital laboratory" ecosystems and software-as-a-service laboratory platforms. Moreover, cloud deployment allows for low cost of infrastructure maintenance and rapid scaling for high throughput experimentation. Cloud-integrated autonomous laboratories are still in high demand due to the growing trend towards data-driven scientific workflows, predictive analytics and remote lab operation.

By Workflow Stage Analysis

The workflow stage segment is the most influenced by experiment execution are poised to dominate this segment, as this is the key operational process in an autonomous chemical lab, where experiments are actively carried out and managed by robotic systems, AI algorithms and analytical instruments. Autonomous experiment execution makes the process much faster, reproducible, accurate and high throughput than traditional lab work. To speed molecular discovery and optimize reaction pathways, pharmaceutical companies, biotechnology firms, and materials science researchers more and more invest in automated experimentation platforms. The increasing demand for high throughput screening, continuous experimentation workflows further bolsters this segment dominance. AI-powered robotic systems can automatically adjust experimental parameters in real-time, based on the data generated, thus minimizing human intervention and reducing errors. Furthermore, the development of robotic chemistry systems and automated synthesis technologies keep growing the ability for autonomous experiment execution in industrial and academic laboratories worldwide.

By Application Analysis

The drug discovery & development is poised to be segment is the highest dominant application area as the pharmaceutical companies are aggressively implementing autonomous laboratory technology in order to speed up therapeutic identification of novel drugs, optimize the screening of compounds, and shorten drug development timelines. Using autonomous chemical laboratories, researchers can perform continuous high throughput experimentation, AI directed molecular optimisation and can quickly analyse complex biochemical interaction. These functionalities greatly enhance research efficiency, and reduce the time, expense, and danger of conventional drug discovery methods. Further contributing to the adoption in pharmaceutical research settings is the increasing prevalence of chronic diseases, the need for precision medicine as well as increased investment in next generation therapeutics. Moreover, AI-driven autonomous labs can enhance the precision and forecast in preclinical trials. The drug discovery market is still the major application in the world, with robust support from pharmaceutical and biotechnology companies and government-sponsored life science research programs.

By End User Analysis

The end user segment is anticipated to dominate by pharmaceutical firms, which are the biggest adopters of autonomous chemical laboratory technologies for accelerating the drug discovery, molecular synthesis, and clinical research workflow. The pharmaceutical industry is under pressure to shorten research time, cut down on development expenses and boost the success rate of therapeutic innovations. High throughput experimentation, AI-based compound optimisation and automated analytical testing in autonomous laboratories can greatly boost research productivity in pharmaceutical companies. Big pharma is pouring millions of dollars into robotic chemistry platforms, self-driving labs, and cloud-based experimentation platforms to boost competitive advantage and aid precision medicine efforts. Furthermore, the rising need for the development of complex molecules, personalized therapeutics and biologics further heightens the need for independent laboratory facilities. Pharmaceutical companies are continuing to form strategic partnerships with AI technology providers to further cement their segment dominance on a global scale.

The Global Autonomous Chemical Laboratory Market Report is segmented on the basis of the following:

By Component

- Hardware

- Software

- Services

By Laboratory Type

- Fully Autonomous Laboratories

- Semi-Autonomous Laboratories

- Modular Autonomous Labs

- Integrated End-to-End Autonomous Platforms

By Technology

- Artificial Intelligence & Machine Learning

- Robotics & Cobotics

- Computer Vision

- Digital Twin Technology

- Internet of Things (IoT)

- Cloud-Based Laboratory Platforms

By Deployment Mode

- On-Premise

- Cloud-Integrated

- Hybrid Deployment

By Workflow Stage

- Sample Preparation

- Chemical Synthesis

- Experiment Execution

- Analytical Testing

- Data Interpretation & Optimization

- Quality Control

By Application

- Drug Discovery & Development

- Materials Science

- Chemical Manufacturing

- Agrochemical Research

- Specialty Chemical Development

- Academic Research

- Environmental Testing

By End User

- Pharmaceutical Companies

- Chemical Manufacturers

- Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations (CROs)

- Industrial Laboratories

Regional Analysis

Leading Region by Market Share

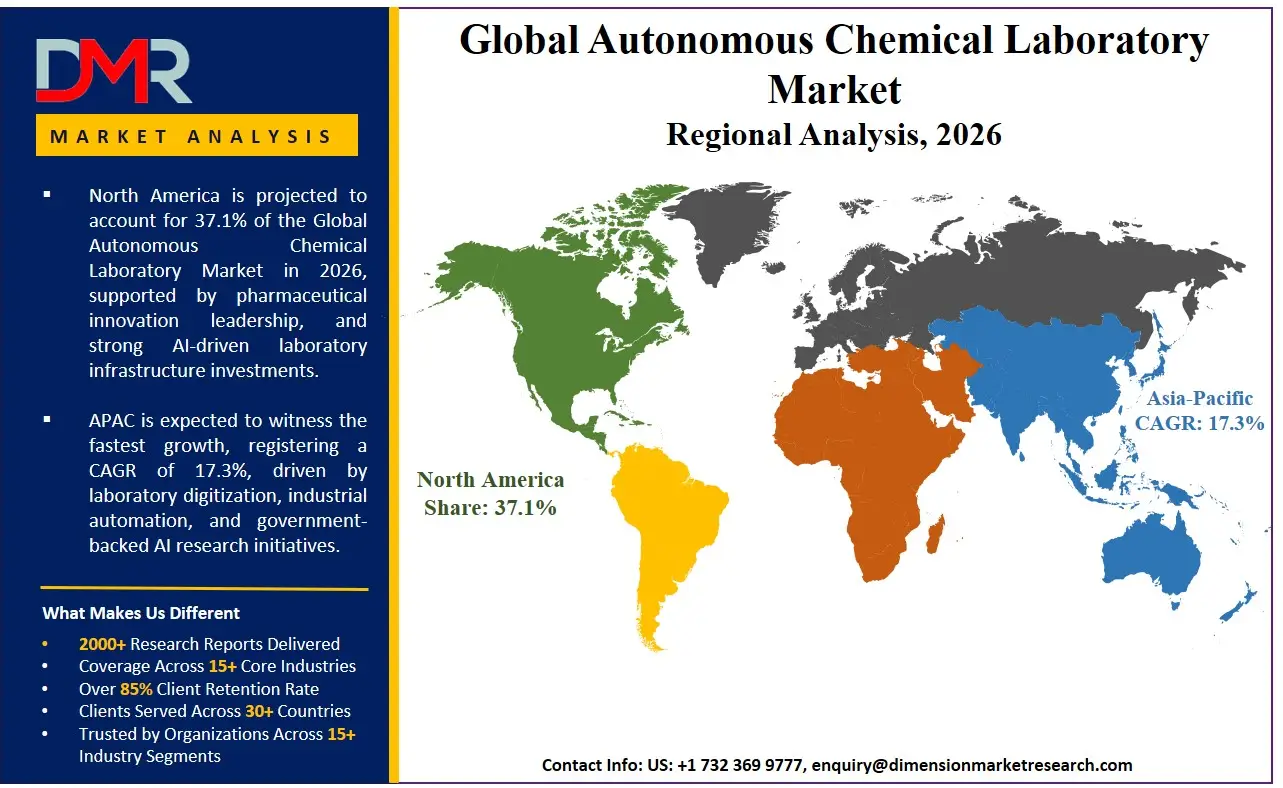

North America is poised to dominate the global autonomous chemical laboratory market as it is projected to hold 37.1% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the autonomous chemical lab market because of the unmatched concentration of top-tier pharmaceutical R&D centers and the aggressive digital transformation agendas of large biotechnology hubs. The area has an established ecosystem of global laboratory hardware manufacturers, specialized AI-driven software startups, and a rich pool of talent in cheminformatics and lab automation engineering. Enterprise investment in drug discovery, advanced materials for defense and energy, and the overall retirement of manual synthesis workflows contribute to the continued demand for integrated autonomous platforms along with continuous data optimization. Moreover, an optimistic venture capital climate persistently finances upcoming AI-native biotech and materials companies that need expert integration services to achieve rapid scientific output and intellectual property security.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding autonomous chemical laboratory market, driven by the government-led sweeping R&D modernization initiatives in China, Japan, South Korea, and Singapore. The fast-paced economic growth, the rise of a domestic innovation economy, and the dynamic expansion of the pharmaceutical and specialty chemical sectors are compelling established conglomerates and Contract Research Organizations to discard unproductive manual infrastructure. Services for modular autonomous laboratory design and implementation are in high demand to help these large organizations head in the direction of high-throughput, AI-driven operating models. There is also a severe lack of qualified laboratory automation talent in the region, and it is necessary to outsource specialized services for hardware integration, software customization, and managed lab operations to cover the skills gap and enable faster ROI on autonomous lab investments.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global autonomous chemical laboratory market has become highly dynamic with a heterogeneous array of multinational laboratory instrument manufacturers, pure-play AI-driven automation software firms, and specialized systems integrators. The key to success will be the profound strategic alliances with leading pharmaceutical and chemical end users because these co-development partnerships open the necessary domain-specific validation and early access to new experimental needs. The movement towards market consolidation is rapidly progressing with the traditional hardware providers acquiring AI and digital twin technology specialists to stay afloat. Proprietary intellectual property, including automated closed-loop experiment execution frameworks and industry-specific AI models for property prediction, is becoming a more important basis of competitive differentiation than just hardware sales or generic software interfaces.

Some of the prominent players in the Global Autonomous Chemical Laboratory Market are:

- Thermo Fisher Scientific

- Agilent Technologies

- Tecan Group

- Hamilton Company

- PerkinElmer

- Danaher Corporation

- Siemens Healthineers

- Sartorius AG

- Waters Corporation

- Qiagen

- Eppendorf

- Brooks Automation

- Biosero

- HighRes Biosolutions

- Opentrons Labworks

- Strateos

- Synthace

- Emerald Cloud Lab

- Automata Labs

- Schrödinger, Inc.

- Other Key Players

Recent Developments

- In February 2026, Bruker Corporation through its divisions Chemspeed and SciY launched an open self-driving laboratory platform integrating AI orchestration, robotics, analytics, and laboratory management software to accelerate autonomous chemical and biomolecular experimentation workflows.

- In March 2026, Ginkgo Bioworks introduced Ginkgo Cloud Lab, a browser-based autonomous laboratory platform powered by robotic infrastructure, AI-driven workflow management, and remote access to more than 70 laboratory instruments for automated biological experimentation.

- In May 2026, Insilico Medicine unveiled LabClaw, an intelligent laboratory autonomy system combining generative AI, automated laboratory hardware, and real-time experimental coordination to advance autonomous drug discovery and chemical research operations.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 5,748.5 Mn |

| Forecast Value (2035) |

USD 19,483.4 Mn |

| CAGR (2026–2035) |

14.5% |

| The US Market Size (2026) |

USD 1,793.6 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Laboratory Type, By Technology, By Deployment Mode, By Workflow Stage, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Autonomous Chemical Laboratory Market?

▾ The Global Autonomous Chemical Laboratory market is poised to be valued at USD 5,748.5 million in 2026 and is projected to reach USD 19,483.4 million by 2035, driven by the universal need for specialized, integrated platforms to accelerate chemical experimentation and materials discovery.

What is the CAGR of the Global Autonomous Chemical Laboratory Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 14.5% from 2026 to 2035, reflecting the accelerating complexity of scientific R&D and the persistent shortage of internal AI and robotics talent within research organizations.

What factors are driving the growth of the Global Autonomous Chemical Laboratory Market?

▾ Key drivers include the R&D productivity crisis, the imperative to modernize legacy manual labs, the management complexity of multi-vendor hardware and software, and the surge in demand for AI-driven data interpretation and optimization amid explosive growth in chemical data.

Which region held the largest share of the Autonomous Chemical Laboratory Market in 2026?

▾ North America is poised to be dominate this market with 37.1% of the market share in 2026, driven by a mature ecosystem of pharmaceutical and biotech R&D and aggressive enterprise investment in integrated end-to-end autonomous platforms and AI-driven drug discovery.

Which region is expected to grow the fastest in the Autonomous Chemical Laboratory Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid R&D digital transformation in China, Japan, and South Korea, where adopting high-throughput autonomous experimentation is critical for transition and growth.

What are the major trends in the Global Autonomous Chemical Laboratory Market?

▾ Major trends include the integration of Generative AI into molecular design, the rise of cloud-based laboratory platforms for global collaboration, the demand for domain-specific autonomous labs, and the focus on sustainability-driven "green chemistry by design."

How is the Global Autonomous Chemical Laboratory Market segmented?

▾ The market is segmented by Component, Laboratory Type, Technology, Deployment Mode, Workflow Stage, Application, and End User.