What is the Autonomous Cloud Management Market Size?

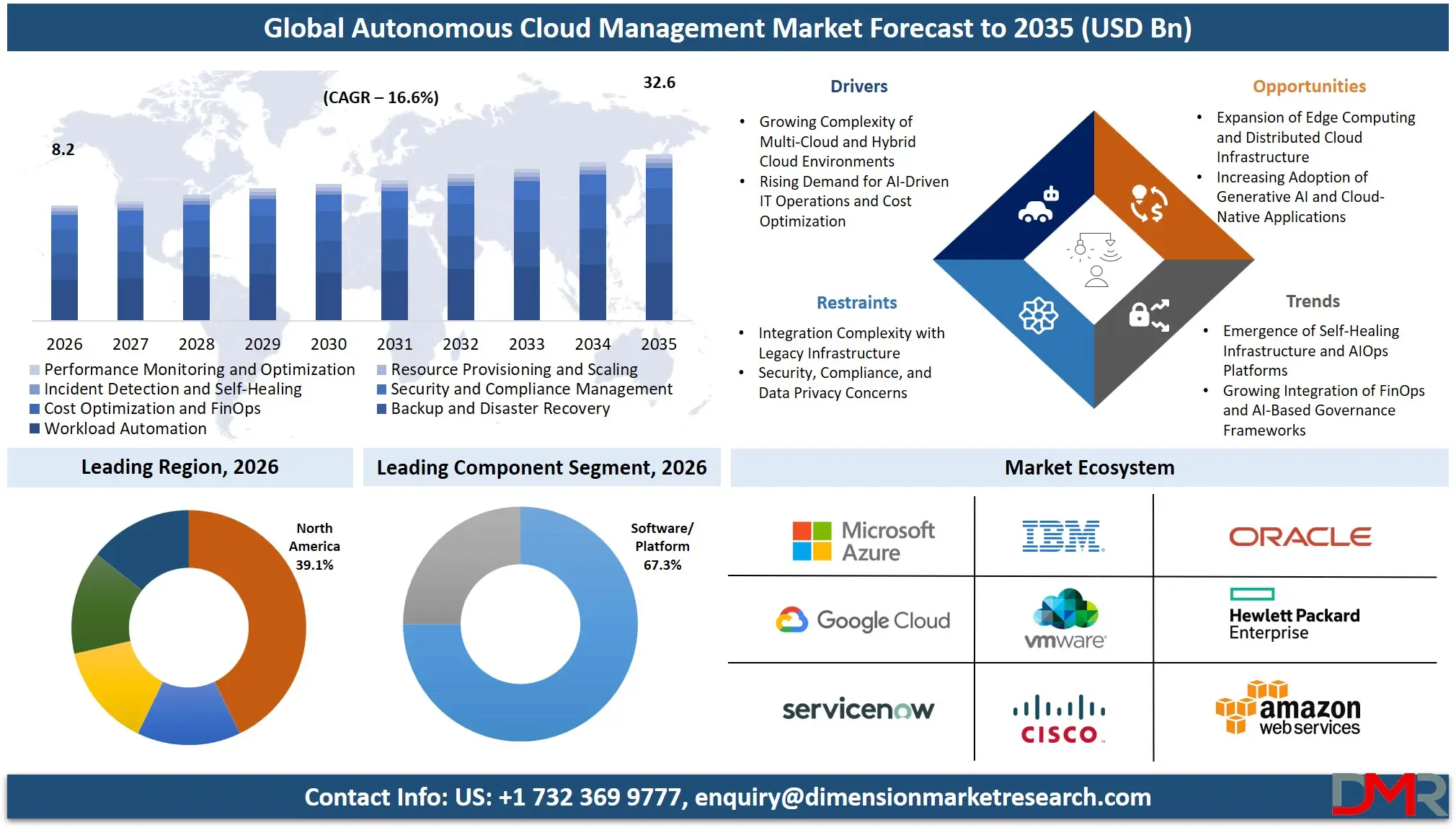

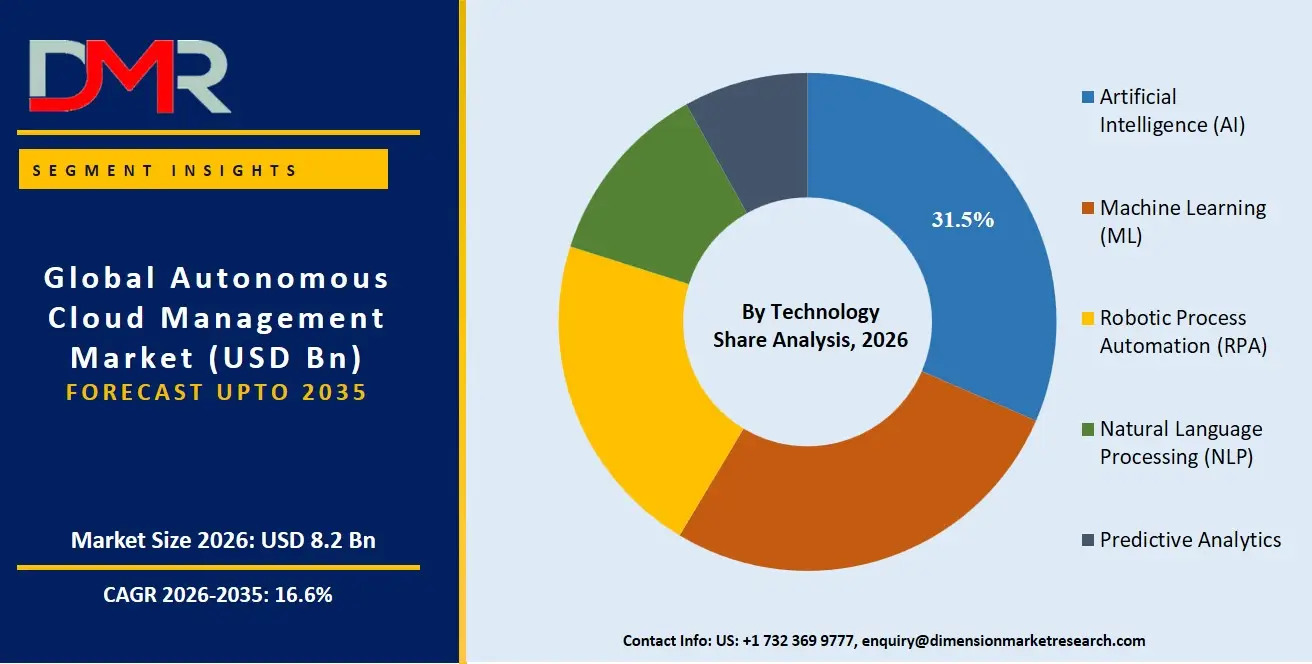

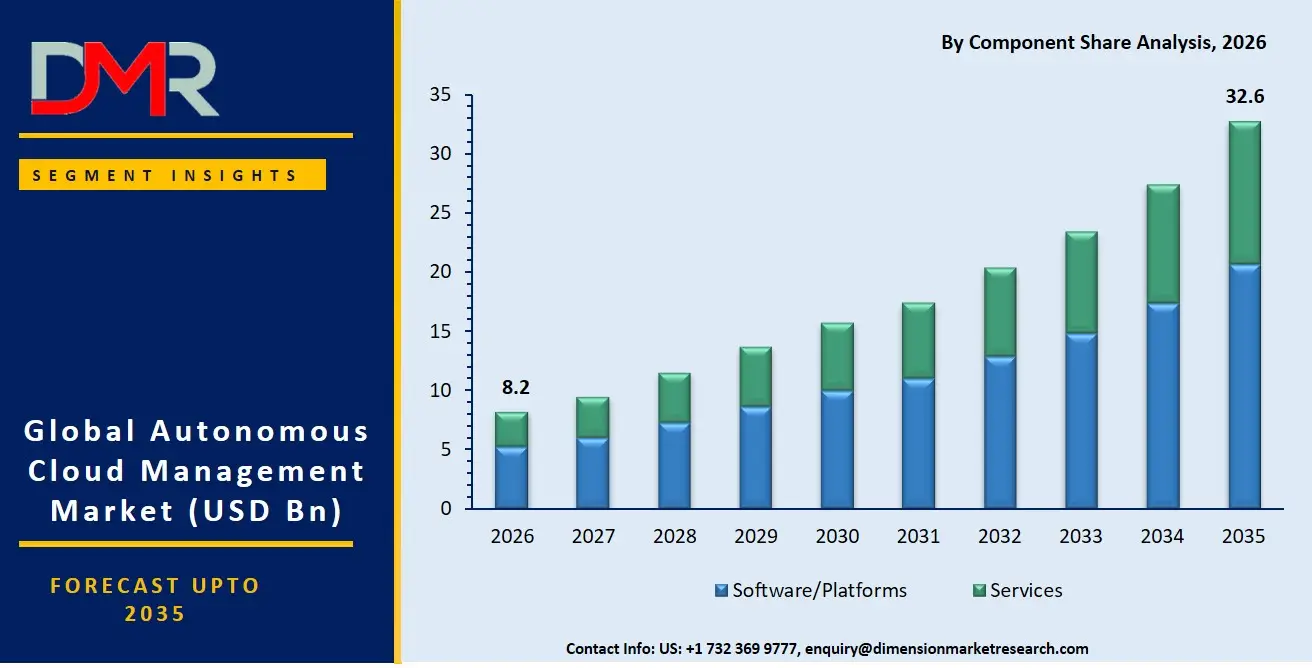

The Global Autonomous Cloud Management Market is expected to reach a value of USD 8.2 billion in 2026, and it is further anticipated to reach USD 32.6 billion by 2035, growing at a CAGR of 16.6% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This market represents a paradigm shift from manual cloud administration to intelligent, self-operating ecosystems. It encompasses AIOps, self-healing infrastructure, and FinOps platforms that leverage artificial intelligence and machine learning to automate routine tasks, predict potential failures, and dynamically optimize resources across hybrid and multi-cloud estates. The core driver is the unmanageable complexity of modern cloud-native architectures, where ephemeral containerized workloads and microservices generate a data deluge beyond human operational capacity. Organizations are adopting these autonomous platforms to enforce governance guardrails, eliminate configuration drift, and transition IT teams from reactive troubleshooting to proactive strategic innovation.

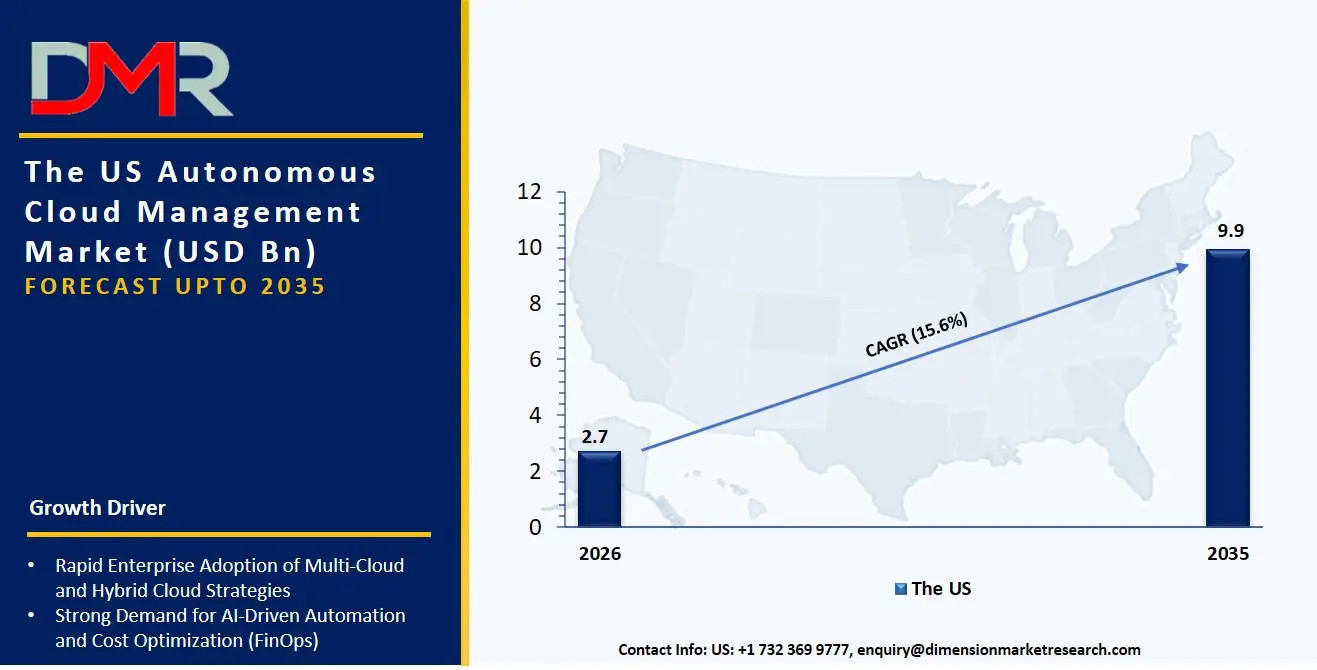

The US Autonomous Cloud Management Market

The US Autonomous Cloud Management Market is projected to reach USD 2.7 billion in 2026 at a compound annual growth rate of 15.6% over its forecast period, culminating in a value of USD 9.9 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States dominates this sector due to its hyperscale data center density and aggressive enterprise adoption of Site Reliability Engineering (SRE) practices. The market is characterized by high demand for AI-Based Cloud Resource Management Platforms that can perform continuous rightsizing of virtual machines and Kubernetes pods. Furthermore, the integration of generative AI co-pilots into cloud operations is creating a parallel surge in demand for Cloud Security and Compliance Management Platforms to autonomously remediate misconfigurations and enforce AI ethics policies across cloud environments.

The Europe Autonomous Cloud Management Market

The Europe Autonomous Cloud Management Market is estimated to be valued at USD 2.3 billion in 2026 and is further anticipated to reach USD 8.9 billion by 2035 at a CAGR of 16.2%. The European market is heavily influenced by stringent regulatory frameworks like GDPR and the EU AI Act, which drive the necessity for autonomous governance and sovereign cloud management. Accelerated growth in Hybrid Cloud Management platforms is occurring as German and French manufacturing firms seek to balance operational technology (OT) security with cloud-based predictive analytics. Initiatives like GAIA-X are compelling vendors to develop autonomous orchestration tools that guarantee data residency and semantic interoperability across federated European cloud ecosystems.

The Japan Autonomous Cloud Management Market

The Japan Autonomous Cloud Management Market is projected to be valued at USD 600.1 million in 2026 at a CAGR of 14.8%. The Japanese market is unique, driven by a corporate imperative to combat a declining workforce through hyper-automation. AIOps platforms and Self-Healing Cloud Infrastructure Platforms constitute a large portion of spending as traditional conglomerates migrate monolithic mainframe applications to the cloud. There is a distinct demand for deep localization to bridge the gap between legacy Electronic Medical Record (EMR) systems and industrial control systems with modern SaaS applications, creating a niche for autonomous workflow automation tools that can perform predictive maintenance without human intervention.

Key Takeaways

- Market Size & Forecast: The Global Autonomous Cloud Management market is projected to reach USD 8.2 billion in 2026, expanding dramatically to USD 32.6 billion by 2035, fueled by the exponential growth of telemetry data that makes manual cloud operations untenable.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 16.6%, driven by a critical shortage of Site Reliability Engineers (SREs) and the escalating complexity of managing distributed tracing and service mesh architectures in cloud-native environments.

- Primary Growth Drivers: Key forces include the transition from static threshold-based alerts to dynamic predictive analytics, the need for Cloud Cost Management and FinOps Platforms to eliminate idle resources and prevent budget overruns, and the integration of Robotic Process Automation (RPA) to close the automation gap between legacy and cloud-native systems.

- Key Market Trends: Major trends include the rise of intent-based orchestration, the use of generative AI for automated runbook generation within AIOps platforms, and the shift toward autonomous security posture management (ASPM) as boards prioritize zero-trust architectures.

- By Cloud Environment Analysis: Hybrid Cloud Management solutions are expected to dominate enterprise discussions due to data gravity and latency requirements. Autonomous platforms are increasingly required to provide federated visibility and unified control across on-premise private clouds and public cloud innovation engines.

- By End User Analysis: BFSI and Healthcare & Life Sciences are the most lucrative verticals due to stringent compliance and uptime requirements. Manufacturing is the fastest-growing sector as Industrial IoT (IIoT) sensor data requires robust Resource Provisioning and Scaling platforms to manage edge-to-cloud data pipelines autonomously.

- Regional Leadership: North America is poised to dominate this market with 39.1% of the market share in 2026 due to its advanced technological ecosystem and early adoption of observability-driven autonomous operations.

What is the Autonomous Cloud Management?

Autonomous Cloud Management refers to the suite of software platforms and services that utilize AI, ML, and advanced analytics to automate the full lifecycle of cloud resource management, including provisioning, scaling, security, and cost optimization, with minimal human intervention. Unlike traditional cloud management tools that rely on reactive manual scripts, these platforms are proactive and intent-driven. This involves Software/Platforms like AIOps to analyze vast streams of telemetry data for anomaly detection, Cloud Automation and Orchestration Platforms to execute complex workflows, and Self-Healing Cloud Infrastructure Platforms to automatically remediate security vulnerabilities or performance bottlenecks. As 90% of organizations operate distributed architectures, autonomous systems are essential for maintaining consistent state enforcement, optimizing spend, and ensuring resilience, turning operational noise into actionable, automated intelligence.

Use Cases

- Autonomous Incident Remediation in Banking: Banking institutions deploy Self-Healing Cloud Infrastructure Platforms to auto-remediate common security misconfigurations in real-time, ensuring zero-touch compliance with PCI DSS standards without interrupting transaction processing.

- Predictive Resource Scaling in E-Commerce: Retail giants use Predictive Analytics and Resource Provisioning and Scaling platforms to anticipate traffic spikes during flash sales, automatically provisioning compute instances seconds before demand hits, thereby eliminating latency and lost revenue.

- Sovereign Compliance Automation in Government: Government agencies leverage Cloud Security and Compliance Management Platforms to autonomously enforce data residency policies, automatically blocking API calls that would inadvertently transfer citizen data across geopolitical borders.

- Intelligent Factory Edge Orchestration: Global manufacturers use AI-Based Cloud Resource Management Platforms to orchestrate containerized analytics workloads across thousands of factory-floor edge nodes, automatically redistributing jobs if a local server fails.

How AI is Transforming the Autonomous Cloud Management Market?

AI is the foundational engine of autonomous cloud management, moving operations beyond simple automation into true cognitive intelligence. In Performance Monitoring and Optimization, AI/ML algorithms continuously learn the unique behavioral patterns of applications to establish dynamic baselines, instantly identifying deviations that signal performance degradation without predefined thresholds. In the FinOps domain, AI-driven Cloud Cost Management and FinOps Platforms ingest complex billing datasets to identify idle storage volumes and zombie instances, automatically scheduling hibernation or rightsizing to align with actual demand.

AI is also revolutionizing security and compliance postures. In autonomous security management, NLP algorithms parse legal text and regulatory documents to translate abstract compliance mandates into specific, enforceable infrastructure-as-code policies, ensuring environments remain continuously compliant with frameworks like SOC 2 and ISO 27001. Furthermore, Generative AI is transforming Support and Maintenance Services by enabling conversational interfaces where operators query system health in natural language and receive not just diagnostic reports, but also generated remediation scripts ready for approval or automatic execution.

Market Dynamics

Key Drivers in the Global Autonomous Cloud Management Market

Growing Complexity of Multi-Cloud and Hybrid Cloud Environments

The rapid adoption of hybrid and multi-cloud architectures has significantly increased infrastructure complexity for enterprises. Organizations are managing workloads across public clouds, private clouds, and edge environments, making manual administration increasingly inefficient. Autonomous cloud management platforms leverage AI, machine learning, and automation to optimize resources, monitor workloads, and ensure seamless operations across diverse environments. Enterprises are increasingly seeking solutions that can reduce operational overhead, enhance scalability, and improve service reliability. As digital transformation accelerates and cloud-native applications proliferate, demand for intelligent cloud management capabilities continues to rise. This growing need to simplify cloud operations and maximize infrastructure efficiency is a major driver supporting market expansion worldwide.

Rising Demand for AI-Driven IT Operations and Cost Optimization

Enterprises are under increasing pressure to optimize cloud spending while maintaining high performance and service availability. AI-powered cloud management solutions enable predictive analytics, anomaly detection, automated remediation, and intelligent workload placement, reducing manual intervention and operational costs. The growing adoption of FinOps practices is encouraging organizations to implement autonomous platforms capable of delivering real-time insights into resource utilization and expenditure. Businesses are also seeking greater operational resilience and faster incident resolution to minimize downtime. With cloud expenditures continuing to rise globally, organizations are prioritizing solutions that enhance efficiency and improve return on investment, making AI-driven operations and cost optimization major growth drivers.

Restraints in the Global Autonomous Cloud Management Market

Integration Complexity with Legacy Infrastructure

Despite the advantages of autonomous cloud management, integrating AI-driven platforms with legacy IT systems remains a major challenge. Many enterprises operate a mix of traditional infrastructure and modern cloud-native environments, creating compatibility issues and operational silos. Migrating workloads and implementing automation frameworks often require significant investments in skilled personnel and customized integration services. Furthermore, inconsistent data structures and fragmented management tools can limit the effectiveness of autonomous operations. Organizations may also face disruptions during implementation, increasing resistance to adoption. These integration complexities can slow deployment timelines and create barriers for enterprises seeking to transition toward fully autonomous cloud management environments.

Security, Compliance, and Data Privacy Concerns

As autonomous cloud management platforms gain greater control over infrastructure operations, concerns regarding cybersecurity, regulatory compliance, and data privacy continue to intensify. Enterprises operating in regulated industries such as banking, healthcare, and government must comply with stringent standards regarding data protection and governance. Automated decision-making processes may introduce risks related to unauthorized access, misconfigurations, or compliance violations. Additionally, organizations remain cautious about relying extensively on AI systems without sufficient transparency and oversight. Variations in regional regulations and increasing cyber threats further complicate cloud governance strategies. These concerns may delay adoption and limit the implementation of fully autonomous cloud management solutions.

Growth Opportunities in the Global Autonomous Cloud Management Market

Expansion of Edge Computing and Distributed Cloud Infrastructure

The growing deployment of edge computing and distributed cloud environments presents substantial opportunities for autonomous cloud management providers. Applications such as Internet of Things (IoT), smart manufacturing, autonomous vehicles, and 5G networks generate vast amounts of data that require intelligent resource allocation and real-time processing. Managing these distributed infrastructures manually is increasingly impractical, creating demand for AI-driven automation and self-healing capabilities. Autonomous cloud platforms can optimize workloads, monitor edge devices, and improve operational efficiency across geographically dispersed environments. As enterprises continue expanding their edge computing capabilities, vendors offering advanced autonomous management solutions are expected to benefit from significant growth opportunities.

Increasing Adoption of Generative AI and Cloud-Native Applications

The rapid emergence of generative AI technologies and cloud-native applications is creating new opportunities for autonomous cloud management platforms. Generative AI workloads require dynamic resource allocation, scalable infrastructure, and continuous performance optimization, making intelligent cloud management essential. Organizations deploying containerized applications, microservices, and Kubernetes environments increasingly need automated orchestration and predictive analytics capabilities. Autonomous cloud solutions can ensure optimal performance, reduce downtime, and enhance infrastructure utilization in highly dynamic environments. Furthermore, enterprises are investing heavily in AI-enabled digital transformation initiatives, creating strong demand for self-managing cloud platforms capable of supporting next-generation workloads and maintaining operational resilience.

Trends in the Global Autonomous Cloud Management Market

Emergence of Self-Healing Infrastructure and AIOps Platforms

One of the most prominent trends in the market is the increasing adoption of self-healing infrastructure supported by AIOps platforms. Organizations are moving beyond traditional monitoring tools toward intelligent systems capable of automatically detecting anomalies, diagnosing issues, and initiating corrective actions without human intervention. These capabilities enhance service availability, minimize downtime, and improve operational efficiency. Vendors are integrating machine learning algorithms and predictive analytics into cloud management solutions to deliver proactive maintenance and autonomous remediation. As enterprises seek higher levels of resilience and operational agility, self-healing architectures are becoming a fundamental component of modern cloud management strategies.

Growing Integration of FinOps and AI-Based Governance Frameworks

Organizations are increasingly integrating FinOps practices with AI-driven governance frameworks to achieve greater visibility and control over cloud expenditures. Autonomous cloud management platforms now provide intelligent cost optimization, policy enforcement, and resource allocation capabilities that align infrastructure spending with business objectives. AI-enabled governance tools help enterprises monitor compliance requirements, optimize workloads, and prevent resource wastage through automated decision-making. Additionally, businesses are emphasizing sustainability and energy efficiency, encouraging vendors to develop cloud management solutions that support environmentally responsible operations. This convergence of FinOps, governance automation, and sustainability initiatives is emerging as a significant trend shaping the future of the autonomous cloud management market.

Research Scope and Analysis

The Global Autonomous Cloud Management Market is segmented by component, cloud environment, enterprise size, technology, application, and end user. Software platforms dominate due to AI-driven automation demand, while hybrid cloud leads deployment. Large enterprises and IT & telecom end users hold major share, driven by complex infrastructure and digital transformation needs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

Software and platforms is projected to dominate the Global Autonomous Cloud Management Market because enterprises increasingly prioritize AI-driven cloud operations, automation, and intelligent resource optimization over standalone services. Organizations are investing heavily in AIOps platforms, cloud orchestration tools, FinOps solutions, and self-healing infrastructure to reduce operational complexity and improve efficiency.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Software platforms provide continuous monitoring, predictive analytics, automated remediation, and governance capabilities that are essential for managing hybrid and multi-cloud environments. Moreover, the growing adoption of cloud-native applications and increasing emphasis on cost optimization have accelerated demand for integrated autonomous management platforms. While services remain important for deployment and support, recurring software subscriptions and platform-based offerings account for the largest share of market revenue.

By Cloud Environment Analysis

Hybrid cloud management is poised to represent the largest segment because enterprises increasingly operate workloads across both private and public cloud environments. Organizations seek flexibility, scalability, regulatory compliance, and data sovereignty while maintaining control over mission-critical applications. Autonomous cloud management platforms are especially valuable in hybrid environments, where managing workloads, security policies, and resource utilization becomes highly complex. AI-powered automation helps organizations optimize performance and maintain operational continuity across diverse infrastructures. Industries such as BFSI, healthcare, and government favor hybrid cloud architectures due to strict compliance requirements. Furthermore, digital transformation initiatives and the need to modernize legacy systems continue to accelerate hybrid cloud adoption, making hybrid cloud management the dominant deployment environment.

By Enterprise Size Analysis

Large enterprises is expected to dominate the market because they operate highly complex IT ecosystems involving multiple cloud providers, thousands of applications, and geographically distributed infrastructure. These organizations require sophisticated autonomous cloud management capabilities to automate operations, optimize costs, improve performance, and enhance cybersecurity. Large enterprises possess the financial resources necessary to invest in advanced AI-driven platforms and managed services. Sectors such as banking, telecommunications, manufacturing, and healthcare increasingly rely on autonomous cloud technologies to support digital transformation initiatives and maintain business continuity. Additionally, the increasing use of generative AI workloads and data-intensive applications has amplified the need for intelligent cloud management solutions, further strengthening large enterprises' leadership in this market.

By Technology Analysis

Artificial Intelligence is expected to dominate the technology segment because AI serves as the foundation of autonomous cloud management systems. AI enables predictive analytics, anomaly detection, automated remediation, capacity forecasting, and intelligent decision-making across cloud environments. Enterprises increasingly deploy AI algorithms to optimize workload allocation, reduce downtime, and enhance infrastructure resilience. AI-driven AIOps platforms help organizations proactively identify issues and minimize manual intervention, thereby improving operational efficiency. Growing investments in generative AI, machine learning, and intelligent automation are also expanding AI applications within cloud management. Since AI powers most self-healing and autonomous operational capabilities, it remains the core enabling technology and commands the largest share of the market.

By Application Analysis

Performance monitoring and optimization is anticipated to be the leading application segment due to the critical need for maintaining application availability, service quality, and infrastructure efficiency. Organizations increasingly rely on AI-driven monitoring tools to detect anomalies, predict failures, and optimize resource utilization in real time. As cloud environments become more distributed and complex, ensuring consistent performance across multiple platforms has become a strategic priority. Autonomous cloud management solutions help reduce downtime, improve user experiences, and maximize return on cloud investments. Enterprises are also focused on controlling latency and ensuring uninterrupted digital services. Consequently, performance monitoring and optimization applications generate the highest demand and account for the largest market share.

By End User Analysis

The Information Technology and Telecommunications sector is expected to dominate the Global Autonomous Cloud Management Market because cloud infrastructure forms the backbone of digital services, software delivery, and communications networks. IT and telecom companies manage extensive multi-cloud environments and process enormous volumes of data, making automation and intelligent resource management essential. Autonomous cloud management solutions help these organizations improve service reliability, optimize infrastructure utilization, and reduce operational expenses. The rapid deployment of 5G networks, edge computing, and AI-driven applications further increases cloud complexity and accelerates the adoption of self-managing systems. Continuous investments in digital transformation and cloud-native technologies position the IT and telecommunications sector as the largest end-user segment.

The Global Autonomous Cloud Management Market Report is segmented on the basis of the following:

By Component

- Software/Platforms

- AI Cloud Operations Platforms (AIOps)

- Autonomous Cloud Optimization Platforms

- AI-Based Cloud Resource Management Platforms

- Cloud Automation and Orchestration Platforms

- Self-Healing Cloud Infrastructure Platforms

- Cloud Cost Management and FinOps Platforms

- Cloud Security and Compliance Management Platforms

- Services

- Consulting Services

- Integration and Deployment Services

- Support and Maintenance Services

- Managed Services

- Training and Education Services

By Cloud Environment

- Hybrid Cloud Management

- Single-Cloud Management

- Multi-Cloud Management

By Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

By Technology

- Artificial Intelligence (AI)

- Machine Learning (ML)

- Robotic Process Automation (RPA)

- Natural Language Processing (NLP)

- Predictive Analytics

By Application

- Performance Monitoring and Optimization

- Resource Provisioning and Scaling

- Incident Detection and Self-Healing

- Security and Compliance Management

- Cost Optimization and FinOps

- Backup and Disaster Recovery

- Workload Automation

By End User

- Information Technology and Telecommunications

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare and Life Sciences

- Retail and E-Commerce

- Manufacturing

- Government and Public Sector

- Media and Entertainment

- Energy and Utilities

- Transportation and Logistics

- Education

- Others

Regional Analysis

Leading Region by Market Share

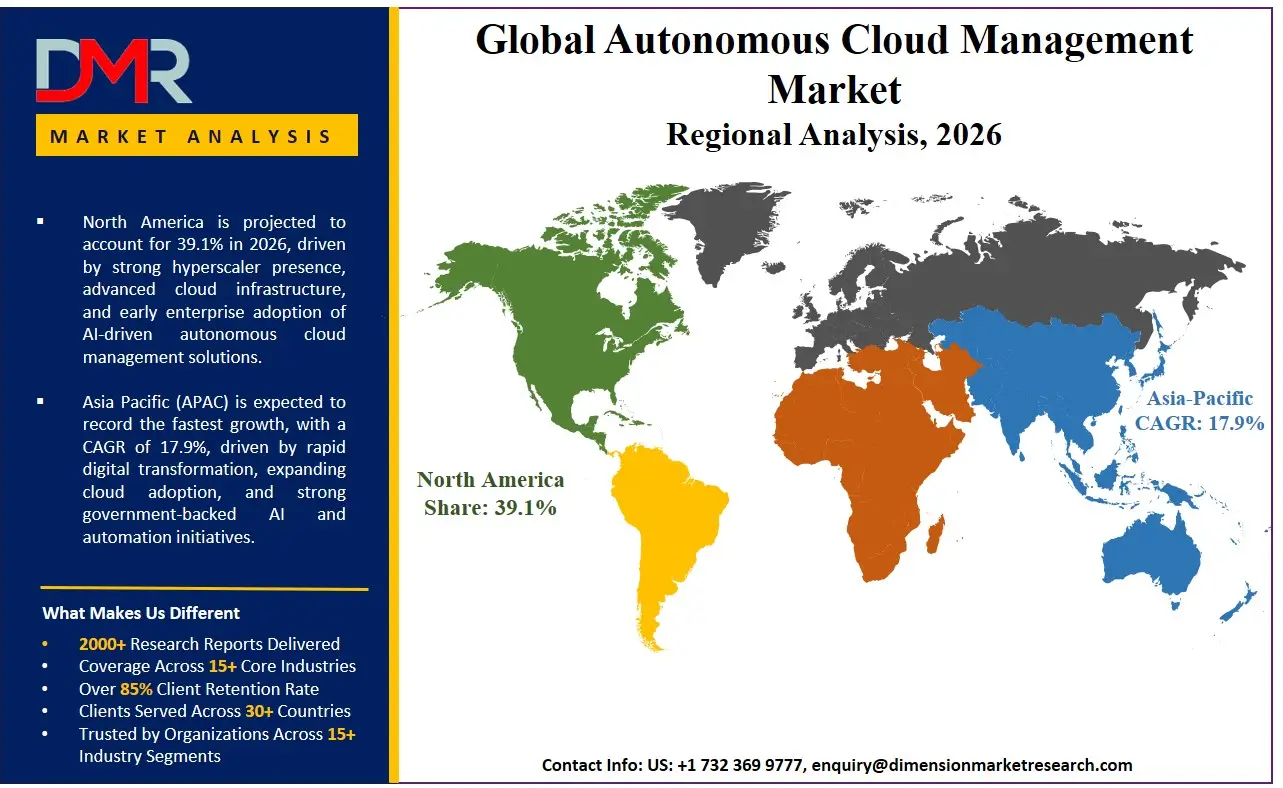

North America is poised to dominate the global autonomous cloud management market, holding a projected 39.1% of the market share by the end of 2026. The United States, which anchors the region, commands the highest share due to an unparalleled concentration of Fortune 500 companies pioneering Site Reliability Engineering (SRE) and GitOps practices. The region possesses a mature ecosystem of platform engineering teams and a deep talent pool of data scientists focused on operational ML. Massive enterprise investment in achieving full-stack observability and the aggressive retirement of manual IT operations frameworks contribute to sustained demand for AIOps and FinOps platforms, alongside autonomous security posture management solutions. Moreover, a high concentration of venture capital continuously funds innovative SaaS startups that require these platforms to achieve exponential growth with lean, fully automated operations teams.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding autonomous cloud management market, driven by accelerated digitalization in India, China, and Southeast Asia, coupled with a strategic need to overcome a shortage of high-cost, senior cloud architects. The rapid economic growth and expansion of the digital economy are compelling large conglomerates and government bodies to bypass traditional IT operations models entirely, "leapfrogging" directly to intent-based autonomous operations. AI-Based Cloud Resource Management Platforms are in high demand to manage the explosive scaling of local e-commerce and fintech platforms. As the volume of operational data produced in this region spirals, autonomous systems become essential not just for efficiency but for the very feasibility of managing these hyperscale digital ecosystems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global autonomous cloud management market is a high-stakes battleground between hyperscaler-native platforms, pure-play AIOps innovators, and Global System Integrators (GSIs). The key to market leadership lies in deep, bi-directional telemetry integrations with AWS, Azure, and GCP APIs to enable real-time closed-loop automation. The market is undergoing rapid consolidation, with traditional IT monitoring vendors acquiring specialized observability and FinOps startups to build comprehensive autonomous portfolios. Competitive differentiation is no longer achieved through data visualization but through the algorithmic quality of unsupervised machine learning models and proprietary pre-trained automation runbooks. The ability to guarantee deterministic outcomes from black-box AI actions what the industry calls "trusted autonomy" is the new battleground for platform engineering and operational technology dominance.

Some of the prominent players in the Global Autonomous Cloud Management Market are:

- Microsoft

- Amazon Web Services (AWS)

- Google Cloud

- IBM

- Oracle

- VMware

- ServiceNow

- Cisco Systems

- Hewlett Packard Enterprise (HPE)

- Nutanix

- HashiCorp

- Apptio (IBM)

- CloudHealth (VMware)

- Turbonomic (IBM)

- Flexera

- Spot by NetApp

- Densify

- Scalr

- Morpheus Data

- CloudBolt Software

- Other Key Players

Recent Developments

- January 2026: Google Cloud announced a major expansion of its AIOps suite within its operations console, introducing a new predictive analytics engine that uses machine learning to forecast cost overruns and performance degradation in GKE (Google Kubernetes Engine) clusters before they occur, enabling autonomous preemptive scaling.

- November 2025: Splunk (now part of Cisco) strengthened its observability collaboration with Microsoft, launching a dedicated Autonomous Security Posture Management (ASPM) solution that uses NLP to interpret new regulatory policies and automatically enforce them across Azure environments for BFSI clients.

- October 2025: ServiceNow acquired a European process mining firm to enhance its Cloud Automation and Orchestration Platforms, specifically to map and automate complex legacy workflows that impede workload migration to sovereign European cloud environments, supporting Government and Public Sector digital transformation mandates.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 8.2 Bn |

| Forecast Value (2035) |

USD 32.6 Bn |

| CAGR (2026–2035) |

16.6% |

| The US Market Size (2026) |

USD 2.7 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Cloud Environment, By Enterprise Size, By Technology, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Autonomous Cloud Management Market?

▾ The Global Autonomous Cloud Management market is poised to be valued at USD 8.2 billion in 2026 and is projected to reach USD 32.6 billion by 2035, driven by the universal need to manage cloud-native complexity with AI-driven software rather than manual human labor.

What is the CAGR of the Global Autonomous Cloud Management Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 16.6% from 2026 to 2035, reflecting the accelerating complexity of microservices architectures and the persistent shortage of Site Reliability Engineers (SREs).

What factors are driving the growth of the Global Autonomous Cloud Management Market?

▾ Key drivers include the overwhelming volume of telemetry data from cloud-native applications, the imperative to eliminate wasteful cloud spending through FinOps, the management complexity of hybrid and multi-cloud deployments, and the demand for self-healing security to address zero-day threats at machine speed.

Which region held the largest share of the Autonomous Cloud Management Market in 2026?

▾ North America is projected to hold a 39.1% market share in 2026, driven by a mature ecosystem of hyperscaler partnerships and aggressive enterprise investment in AIOps and autonomous security orchestration to replace manual NOC/SOC operations.

Which region is expected to grow the fastest in the Autonomous Cloud Management Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid digital transformation in India, China, and Japan, where organizations are leapfrogging traditional IT operations models directly to intent-driven autonomous systems.

What are the major trends in the Global Autonomous Cloud Management Market?

▾ Major trends include the integration of Generative AI co-pilots for natural language operational queries, the rise of intent-based orchestration over declarative IaC, the demand for GreenOps carbon-aware scheduling, and the focus on deterministic self-healing within complex service mesh environments.

Who are the key players in the Global Autonomous Cloud Management Market?

▾ Key players include hyperscaler-native platforms like AWS, Microsoft Azure, and Google Cloud, pure-play observability and AIOps leaders like Dynatrace and Datadog, and IT operations giants like ServiceNow and BMC.

How is the Global Autonomous Cloud Management Market segmented?

▾ The market is segmented by Component, Cloud Environment, Enterprise Size, Technology, Application, and End User.