Market Overview

The Global Autonomous Driving Market size is projected to reach USD 146.3 billion in 2025 and grow at a compound annual growth rate of 33.1% to reach a value of USD 1,921.7 billion in 2034.

The autonomous driving market refers to the evolving segment of mobility where vehicles operate with minimal human input by leveraging technologies like LiDAR, RADAR, cameras, AI, sensor fusion, and real-time connectivity. It spans a range from basic driver assistance features to full vehicle autonomy, transforming how people and goods move across urban and intercity environments.

Growing safety concerns, environmental regulations, and shifts in consumer mobility preferences are accelerating interest in autonomous technologies. Across markets, driver-assistance systems are becoming increasingly common, serving as a bridge toward higher levels of automation. The rise in automation-ready vehicles, supported by expanding infrastructure and awareness, signals that autonomy is no longer a long-term concept but a near-term reality.

Governments and automakers are actively piloting test beds for autonomous vehicles, especially in controlled or mixed-traffic environments. This is supported by broader visions that integrate autonomy within the larger framework of connected, electric, and shared mobility. Collaboration between automotive OEMs, technology companies, and suppliers is further enhancing the pace of innovation, particularly in software and system integration.

While full autonomy remains in early stages, the market is clearly transitioning from assisted to automated mobility. As investment pours into enabling technologies and services, a growing number of applications—from ride-hailing and logistics to personal transport—are adopting autonomy. Despite ongoing challenges like cost, regulation, and infrastructure readiness, the autonomous driving market is set on a strong, multidimensional growth path.

The US Autonomous Driving Market

The US Autonomous Driving Market size is projected to reach USD 48.0 billion in 2025 at a compound annual growth rate of 31.0% over its forecast period.

The U.S. is one of the most advanced markets for autonomous driving, driven by strong technology ecosystems, early adoption, and robust investment from both automotive and tech industries. Federal and state-level pilot programs are supporting real-world testing of autonomous vehicles across urban and suburban environments. Several states have enacted regulations enabling testing and limited deployment, while others are refining policies to keep pace with evolving technology.

The private sector is highly active, with automakers, AI startups, and mobility companies collaborating on driverless systems, especially in ride-hailing and logistics. Consumer awareness of automation is relatively high, though trust and regulatory clarity still pose hurdles. Innovation is focused on software, safety systems, and advanced mapping. While full autonomy remains a future goal, the U.S. continues to lead in foundational R&D, testing, and commercial readiness for autonomous vehicle deployment.

Europe Autonomous Driving Market

Europe Autonomous Driving Market size is projected to reach USD 36.6 billion in 2025 at a compound annual growth rate of 30.5% over its forecast period.

Europe’s autonomous driving market is characterized by a strong regulatory framework, safety-centric innovation, and coordinated efforts among member states to standardize testing and deployment. The region prioritizes environmental goals and road safety, which align with the advancement of driver assistance and autonomous systems. Several countries, including Germany, France, and the Netherlands, have introduced national-level roadmaps and legislation that support testing and controlled use of autonomous vehicles.

Automakers and Tier-1 suppliers in Europe are investing heavily in next-generation mobility platforms, often in partnership with software and AI firms. Urban mobility and public transport integration are key themes, with autonomous shuttles and on-demand services being piloted in smart city initiatives. While regulatory complexity and cross-border differences present challenges, the European market benefits from strong consumer advocacy for safety, data protection, and sustainability. The region is steadily moving toward level 3 and higher systems, with premium vehicle segments and commercial fleet applications leading early deployments.

Japan Autonomous Driving Market

Japan Autonomous Driving Market size is projected to reach USD 7.3 billion in 2025 at a compound annual growth rate of 34.9% over its forecast period.

Japan’s autonomous driving market is shaped by demographic shifts, a mature automotive industry, and strong government involvement in mobility innovation. With an ageing population and shrinking driver base, there is high national interest in deploying autonomous vehicles to support transportation in both urban and rural areas. The government has taken a proactive role by outlining regulatory frameworks, safety standards, and timelines for advancing autonomous capabilities.

Japanese automakers are focusing on integrating semi-autonomous features in consumer vehicles while simultaneously working on full autonomy for mobility services. Consumer trust in technology, particularly in trusted domestic brands, also supports adoption. While cultural conservatism may slow the acceptance of full autonomy, Japan is steadily advancing toward scalable, safe autonomous mobility solutions with a focus on both convenience and societal need..

Autonomous Driving Market: Key Takeaways

- Market Growth: The Autonomous Driving Market size is expected to grow by USD 1,731.8 billion, at a CAGR of 33.1%, during the forecasted period of 2026 to 2034.

- By Vehicle Type: The passenger vehicle segment is anticipated to get the majority share of the Autonomous Driving Market in 2025.

- By Component: The hardware segment is expected to get the largest revenue share in 2025 in the Autonomous Driving Market.

- Regional Insight: North America is expected to hold a 39.0% share of revenue in the Global Autonomous Driving Market in 2025.

- Use Cases: Some of the use cases of Autonomous Driving include transport & logistics, personal use vehicles and more.

Autonomous Driving Market: Use Cases:

- Ride‑Hailing & Mobility Services: Autonomous vehicles can be deployed in ride‑hailing fleets to provide on‑demand transport without human drivers, reducing cost per trip and enabling 24/7 operation.

- Transportation & Logistics: Self‑driving trucks and vans can transport goods with less driver fatigue risk, optimize routing, and operate in platoons or hubs for last‑mile delivery.

- Personal Use Vehicles: Consumer‑owned vehicles equipped with autonomy features (e.g., Level 3/4) allow drivers to relinquish control in certain conditions (e.g., highway cruising), improving comfort and safety.

- Last‑Mile Delivery: Autonomous shuttles, pods or small vehicles can fulfil the “last‑mile” delivery segment in urban/sem i‑urban zones, reducing labour costs and improving delivery efficiency.

Stats & Facts

- According to a report by NITI Aayog, the Indian automotive sector contributes 7.1% of India’s GDP and about 49% of manufacturing GDP, underscoring the strategic importance of mobility technologies.

- The same NITI Aayog report noted that India’s share of global auto‑component trade is only 3%, indicating significant room for growth in higher‑value mobility systems (including autonomous driving) by 2030.

- Per the NITI Aayog “Smart tech, self‑driving and safety features” report, the adoption of Advanced Driver Assistance Systems (ADAS) in new vehicles was 42% in 2020, and is projected to rise to 90% of new vehicle sales by 2030.

- According to JATO Dynamics, ADAS penetration in India reached 8.3% of passenger vehicle wholesales in H1 2025 (up from 6.2% in H1 2024) — a 33% growth.

Market Dynamic

Driving Factors in the Autonomous Driving Market

Safety and regulatory pressure

Rising concerns around road accidents, pedestrian safety and driver fatigue are pushing the adoption of autonomous driving technologies. Governments and OEMs are increasingly mandating ADAS features and preparing for higher levels of automation. For example, the NITI Aayog report forecasts that more than 30% of vehicles could be equipped with some level of autonomous driving capability by 2030. This regulatory and safety imperative creates a compelling driver for investments in sensors, AI algorithms and connected‑vehicle platforms.

Technological advancements and cost reductions

Advances in LiDAR, RADAR, cameras, sensor fusion and AI/machine learning are improving the reliability and capabilities of autonomous driving. At the same time, economies of scale in hardware and modular software platforms are helping reduce costs. This makes autonomous driving features increasingly viable across vehicle segments, not just premium cars. For example, EV platforms, which often integrate connectivity and automation more readily, are spearheading higher ADAS penetration.

Restraints in the Autonomous Driving Market

Infrastructure and real‑world road conditions

In markets such as India, the lack of consistent lane markings, signage, predictable traffic behaviour, and V2X infrastructure pose major barriers to deploying fully autonomous vehicles. Reports point out that over 70% of urban roads lack lane markings and only ~18% of highways have consistent roadside sensors, complicating perception and autonomy.

High development costs and regulatory uncertainty

Developing autonomous driving systems (hardware, sensors, AI, validation) is capital‑intensive. Additionally, regulatory frameworks for liability, standards, data privacy and deployment of autonomous vehicles are still evolving, creating uncertainty for OEMs and tech players. For instance, the NITI Aayog report notes that low R&D spending and weak innovation ecosystem hamper competitiveness in autonomous driving.

Opportunities in the Autonomous Driving Market

Mobility as a Service (MaaS) expansion and robo‑taxis

As urbanization increases and consumers look for cost‑effective mobility solutions, autonomous driving enables the expansion of ride‑hailing fleets, robo‑taxi deployments and shared mobility models. This presents a new business model for OEMs, fleet operators and digital mobility providers.

Logistics and autonomous commercial vehicles

The logistics sector is ripe for disruption via autonomous trucks, vans and urban delivery vehicles. With driver shortages and rising logistics costs, autonomous systems offer opportunities to enhance efficiency, reduce operating costs and improve utilization of assets.

Trends in the Autonomous Driving Market

Shift from hardware to software‑defined vehicles

As autonomous driving matures, the value is moving toward software (AI, sensor fusion, mapping/localization) and recurring services (over‑the‑air updates, fleet management). For instance, the NITI Aayog report forecasts software’s share of vehicle value to double by 2030.

Growing ADAS adoption as precursor to full autonomy

Adoption of Level 1/2 ADAS is accelerating and becoming standard in more vehicle segments. These systems act as stepping‑stones toward higher automation levels.

Impact of Artificial Intelligence in Autonomous Driving Market

- AI enables real‑time perception and decision‑making: Machine learning algorithms analyse sensor data (LiDAR, radar, cameras) to detect, classify and predict traffic participants, enabling automation.

- Sensor fusion and environment modelling: AI integrates inputs from multiple sensors into a unified 3D model of the vehicle’s surroundings, improving reliability in complex scenarios.

- Path planning and control: AI identifies optimal trajectories, manoeuvres and control actions based on dynamic traffic, road conditions and vehicle state.

- Predictive maintenance and fleet intelligence: AI monitors vehicle health, driving patterns and fleet performance, improving uptime and reducing operating cost for autonomous fleets.

- Continuous learning and over‑the‑air updates: AI systems are updated via software releases and fleet‑data feedback loops, enabling incremental improvements in autonomous performance and safety.

Research Scope and Analysis

By Vehicle Type Analysis

In 2025, the Passenger Vehicles segment leads the autonomous driving market with 72.1% share, which is attributed to the widespread ownership of personal vehicles and the increasing integration of advanced driver assistance systems (ADAS) across mid-range and premium models. Automakers are prioritizing autonomous features such as adaptive cruise control, lane keeping, and automatic emergency braking as standard or optional offerings.

Urban consumers, in particular, are looking for greater driving comfort, safety, and convenience—factors that are influencing their preference for vehicles equipped with partial automation. Additionally, the shift toward connected vehicles and software-defined vehicle platforms is more easily implemented in the personal vehicle space, where individual buyers are willing to pay for value-added features. The growing influence of electric vehicles is also contributing to this shift, as many EVs come equipped with the latest semi-autonomous capabilities.

Meanwhile, the Commercial Vehicles segment—including Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs)—is emerging as the fastest-growing category. This growth is being driven by rising logistics demands, growing e-commerce activities, and fleet operators’ increasing interest in automation to reduce operational costs, fuel consumption, and reliance on human drivers. The appeal of autonomous capabilities in long-haul freight and last-mile delivery is accelerating this segment’s development across various markets.

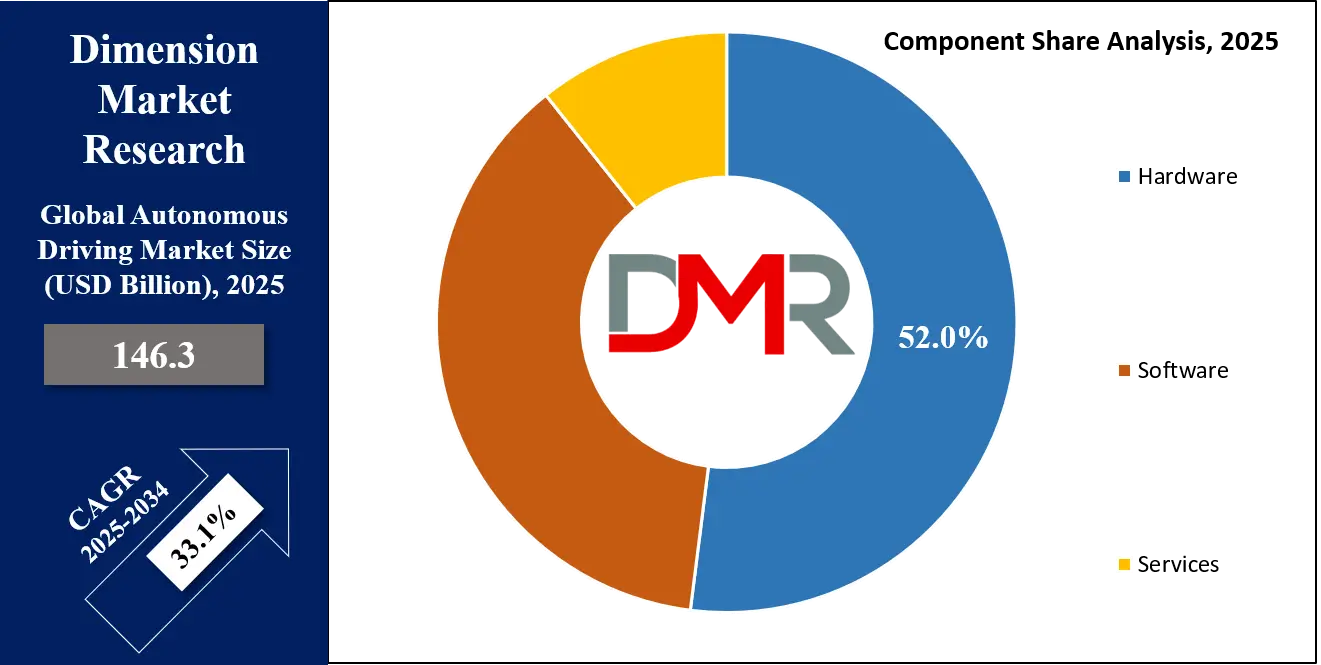

By Component Analysis

Hardware segment remains the largest contributor to the autonomous driving market having 52% of the market share in 2025. Core physical components such as LiDAR, RADAR, ultrasonic sensors, high-resolution cameras, GPS systems, and electronic control units (ECUs) are essential for vehicle perception, environment detection, and navigation. These components serve as the foundational layer of autonomous driving architecture and are required even at the most basic levels of vehicle automation.

As the number of vehicles equipped with automation-ready platforms increases, so does the demand for reliable, high-performance hardware capable of operating under varying road and weather conditions. Manufacturers continue to invest in refining sensor accuracy, reducing size and cost, and integrating systems into streamlined modules to support higher volumes and lower unit costs.

In contrast, the Software segment is emerging as the fastest-growing component category. As the focus shifts from hardware deployment to intelligence and decision-making, software plays a central role in enabling real-time perception, path planning, data fusion, and vehicle control.

Increasing reliance on machine learning algorithms, artificial intelligence, and sensor fusion software is helping vehicles interpret their surroundings more accurately and respond to dynamic traffic scenarios. Automakers and technology firms are now investing in over-the-air updates, software-defined vehicle platforms, and cloud-connected services to enhance performance, personalization, and safety in autonomous driving systems.

By Application Analysis

The Personal Use Vehicles segment is the leading application area in the autonomous driving market with 45% share in 2025. A growing number of individual car buyers are demanding smarter, safer, and more comfortable driving experiences, which is encouraging automakers to integrate semi-autonomous features into personal cars. Many of these vehicles now include technologies such as lane-keeping assist, adaptive cruise control, parking automation, and driver monitoring systems, especially in urban and suburban markets.

Consumers view such features as a blend of luxury and safety, contributing to increased vehicle sales and brand differentiation. Furthermore, vehicle owners are increasingly receptive to driverless technology, particularly in metropolitan areas where traffic congestion and accident risks are higher. This consumer adoption is expected to further solidify the dominance of personal use applications in the market.

Meanwhile, the Transportation & Logistics segment is growing at the fastest rate due to increasing demand for automated freight and delivery systems. Logistics providers are investing in autonomous delivery vans, robotic last-mile delivery units, and driverless freight trucks to improve operational efficiency and meet the demands of faster, round-the-clock services. Autonomous solutions help cut delivery costs, reduce human error, and improve route optimization. The ongoing shortage of skilled drivers is further accelerating adoption in this sector, especially for long-distance and high-frequency transport operations.

The Autonomous Driving Market Report is segmented on the basis of the following:

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Robo-taxis

By Component

- Hardware

- LiDAR

- RADAR

- Cameras

- Ultrasonic Sensors

- GPS/GNSS

- ECUs/Microcontrollers

- Software

- Perception & Sensor Fusion

- Path Planning & Control

- Mapping & Localization

- AI & Machine Learning Algorithms

- Services

By Application

- Ride-Hailing & Mobility Services

- Transportation & Logistics

- Personal Use Vehicles

- Last-Mile Delivery

- Public Transport

Regional Analysis

Leading Region in the Autonomous Driving Market

In 2025, North America holds the largest share in the global autonomous driving market of 39%. This leadership is driven by the presence of advanced automotive manufacturing capabilities, strong regulatory support for testing and deploying autonomous vehicles, and a high level of consumer awareness. Urban centers across the United States and Canada are witnessing widespread pilot programs for autonomous ride-hailing services, robo-taxis, and self-driving delivery vehicles.

The region also benefits from early infrastructure development for intelligent transportation systems, and collaboration between automakers, technology firms, and research institutions. Consumer trust in automation is gradually increasing, aided by favorable laws that encourage safe experimentation and commercial rollout. Public-private partnerships and municipal-level trials are further supporting large-scale adoption.

Fastest Growing Region in the Autonomous Driving Market

Asia-Pacific is emerging as the fastest-growing region for autonomous driving. Rapid urbanisation, increasing traffic congestion, and government-backed investments in smart mobility solutions are contributing to this growth. Countries such as China, India, South Korea, and Japan are witnessing rising deployment of autonomous shuttles, delivery bots, and semi-autonomous vehicles.

The expansion of 5G infrastructure, local production of key components, and high-volume electric vehicle manufacturing are further strengthening the region’s capabilities. Moreover, competitive pricing, large populations, and an openness to mobility innovation make Asia-Pacific a highly dynamic and scalable market for future autonomous systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The autonomous driving market features a broad ecosystem of automotive OEMs, tier‑1 suppliers, sensor and software providers, and mobility‑service players. Partnerships and collaborations between automakers and tech firms (for example between Indian OEMs and global autonomy platforms) are common, enabling shared risk and faster development.

The competitive environment is moderately fragmented with both global giants and regional innovators vying for leadership. The focus is on differentiating via sensor‑stack integration, AI/software capabilities, localization for unique road‑conditions, and scalability of fleet solutions. Many players are also exploring monetization via services, over‑the‑air updates and fleet‑data offerings.

Some of the prominent players in the global Autonomous Driving are:

- Waymo (Alphabet Inc.)

- Cruise (General Motors)

- Tesla, Inc.

- Baidu Apollo

- NVIDIA Corporation

- Mobileye (Intel Corporation)

- Aurora Innovation

- Zoox (Amazon)

- Pony.ai

- WeRide

- Aptiv PLC

- Continental AG

- Magna International Inc.

- ZF Friedrichshafen AG

- Mercedes-Benz Group AG

- Toyota Motor Corporation

- Hyundai Motor Group

- BMW AG

- Volvo Cars

- Ford Motor Company

- Other Key Players

Recent Developments

- In June 2025, PlusAI (formerly Plus Automation Inc.), a company specialising in virtual‑driver software for autonomous trucks, announced that it would merge with Churchill Capital Corp IX via a business‑combination agreement. The merger values the company at a pre‑money equity value of around USD 1.2 billion, and positions PlusAI to scale its factory‑built autonomous truck programs.

- In January 2025, NXP Semiconductors acquired the Austria‑based automotive tech firm TTTech Auto for approximately EUR 625 million. TTTech Auto has expertise in safety‑critical systems and middleware for software‑defined vehicles, marking a significant consolidation in the autonomy/vehicle‑software segment.,

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 146.3 Bn |

| Forecast Value (2034) |

USD 1,921.7 Bn |

| CAGR (2025–2034) |

33.1% |

| The US Market Size (2025) |

USD 48.0 Bn |

| Historical Data |

2019 – 2023 |

| Forecast Data |

2026 – 2034 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Vehicle Type (Passenger Vehicles, Commercial Vehicles, and Robo-taxis), By Component (Hardware, Software, and Services), By Application (Ride-Hailing & Mobility Services, Transportation & Logistics, Personal Use Vehicles, Last-Mile Delivery, and Public Transport) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Waymo, Cruise, Tesla, Inc., Baidu Apollo, NVIDIA Corporation, Mobileye, Aurora Innovation, Zoox , Pony.ai, WeRide, Aptiv PLC, Continental AG, Magna International Inc., ZF Friedrichshafen AG, Mercedes-Benz Group AG, Toyota Motor Corporation, Hyundai Motor Group, BMW AG, Volvo Cars, Ford Motor Company, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

The Global Autonomous Driving Market size is expected to reach a value of USD 146.3 billion in 2025 and is expected to reach USD 1,921.7 billion by the end of 2034.

North America is expected to have the largest market share in the Global Autonomous Driving Market, with a share of about 39.0% in 2025.

The Autonomous Driving Market in the US is expected to reach USD 48.0 billion in 2025.

Some of the major key players in the Global Autonomous Driving Market are Volvo, BMW, Tesla, and others

The market is growing at a CAGR of 33.1 percent over the forecasted period.