What is the Global Autonomous Underwater Vehicle Market Size?

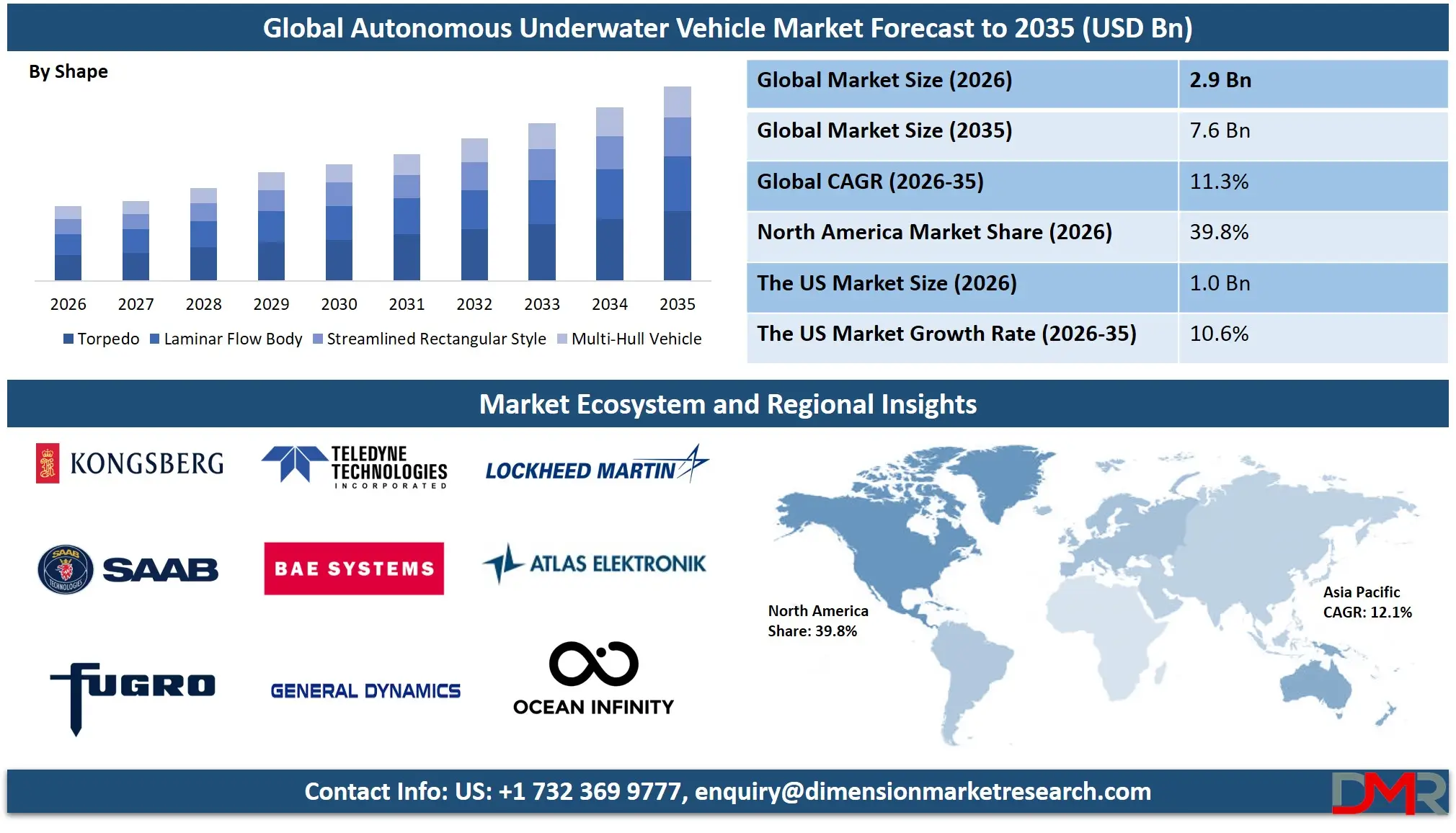

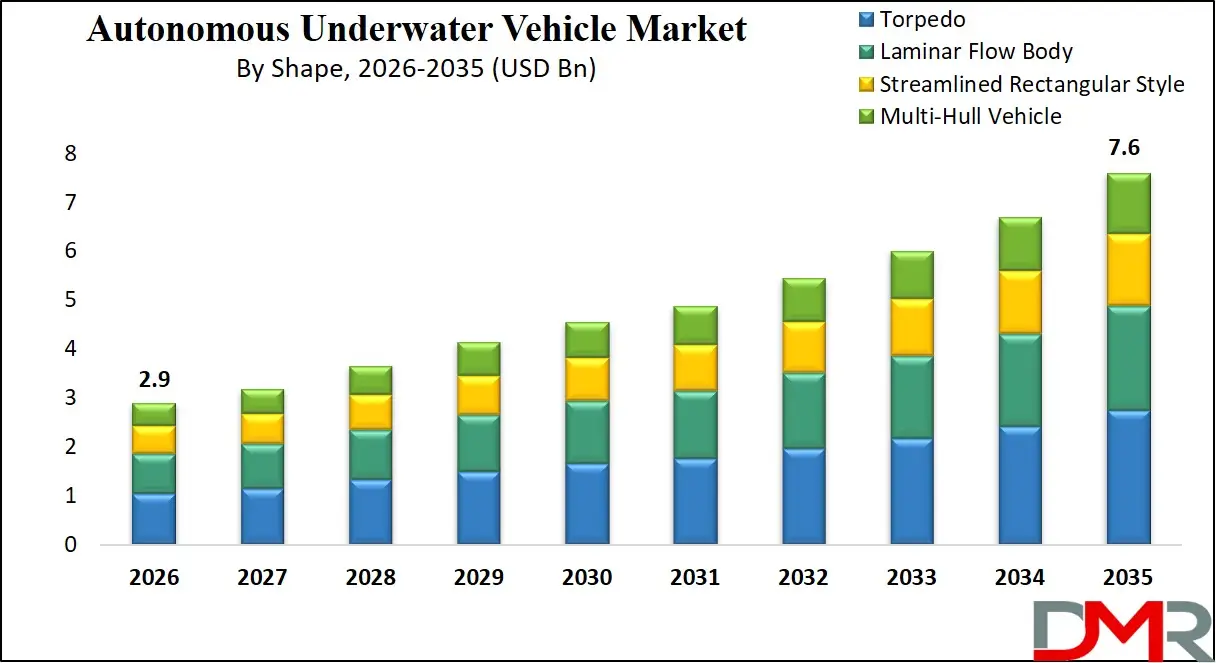

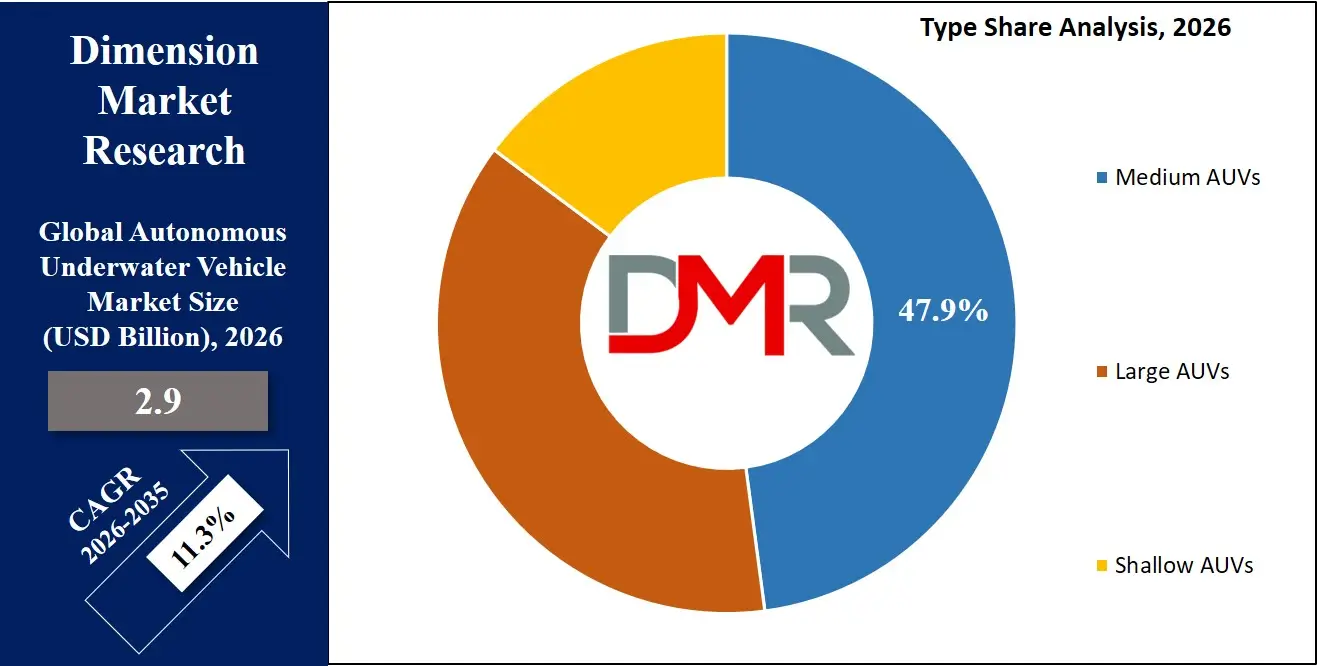

The Global Autonomous Underwater Vehicle Market is projected to reach USD 2.9 billion in 2026 and grow at a compound annual growth rate of 11.3% from there until 2035 to reach a value of USD 7.6 billion.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Autonomous Underwater Vehicle Market is experiencing a strong growth due to the growing demand for efficient, safe, and intelligent underwater operations across the globe. It also includes such modern technologies as AI, sonar imaging, cloud computing, and real-time data analytics applied in the work of AUVs. Modernization is a major investment that governments and other stakeholders in the sector are undertaking to enable efficiency in operations, minimize mission risks, and enhance data accuracy.

The move towards automation, predictive maintenance of subsea assets, and smart payload integration is increasing adoption. Moreover, the need to protect marine ecosystems and the importance of sustainable ocean management are driving digital changes in underwater transport, and autonomous underwater vehicle systems have become an essential part of the future maritime infrastructure on a global scale.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

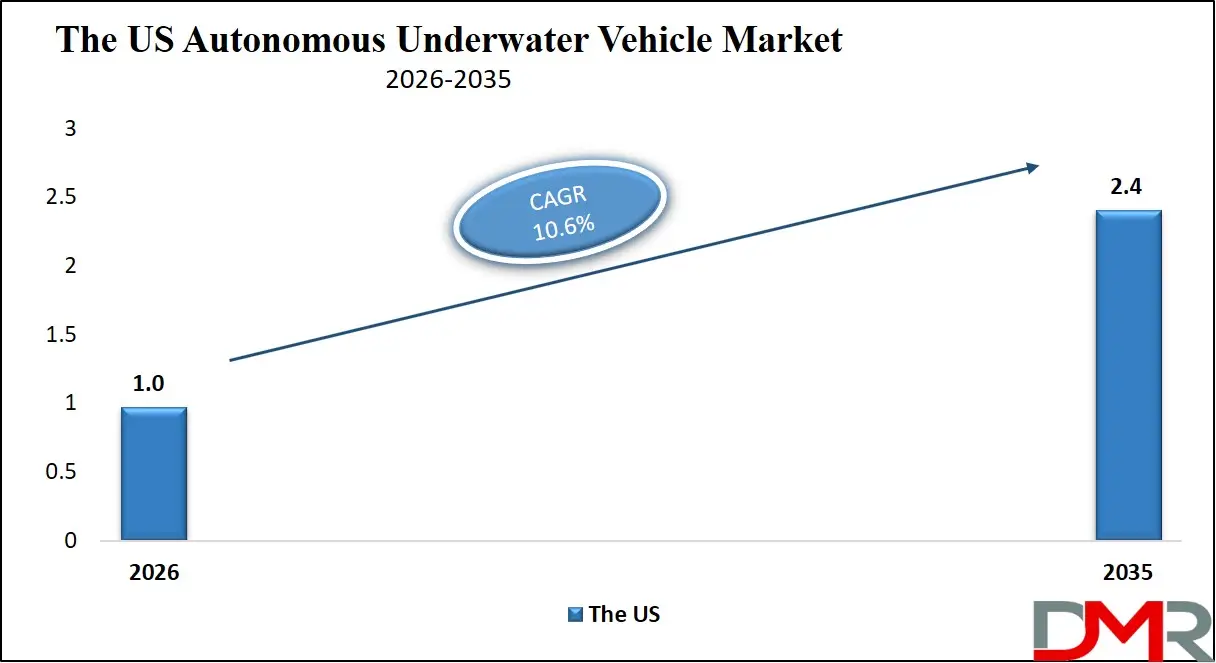

The US Autonomous Underwater Vehicle Market

The US Autonomous Underwater Vehicle Market is projected to reach USD 1.0 billion in 2026 at a compound annual growth rate of 10.6% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US AUV market is motivated by the modernization processes and the necessity to renovate old underwater survey capabilities. There is an increasing investment in smart navigation systems, predictive maintenance based on AI, and sonar-enabled monitoring. The adoption is promoted by government subsidies in terms of defense funding programs. The military & defense segment prevails, and digital tools improve the effectiveness of underwater missions. Major participants are concentrating on innovation and collaborations to increase capacities. The regulatory frameworks that promote maritime safety and efficiency also facilitate the adoption of digital, and the need to have real-time data and automation further determines the growth of markets.

Europe Autonomous Underwater Vehicle Market

The Europe Autonomous Underwater Vehicle Market is estimated to be valued at USD 780.2 million in 2026, witnessing growth at a CAGR of 10.1%, during the forecast period.

Europe is a developed AUV market, which has a strong impact on sustainability objectives and regional policies, including the European Green Deal and marine protection directives. Nations are also working on intelligent underwater systems to minimize ecological disruption and enhance cross-border seabed mapping. Innovation is driven by advanced sonar systems, such as synthetic aperture sonar, and high-endurance AUVs. Adoption is supported by public-private partnerships and harmonization of maritime regulations. Technologies like real-time underwater data transmission and smart payload integration are commonly practiced as research-centric services, and Europe is a frontrunner in terms of the digital transformation of underwater operations.

Japan Autonomous Underwater Vehicle Market

The Japan Autonomous Underwater Vehicle Market is projected to be valued at USD 249.9 million in 2026, progressing at a CAGR of 11.8%, during the period spanning from 2026 to 2035.

The Japanese have a well-developed AUV market backed by good technology and an extensive maritime observation network. Automation, precision, and safety are the priorities in the country and are achieved by AI-driven navigation systems and predictive maintenance solutions for subsea assets. Growth is stimulated by government actions and constant investment in intelligent underwater infrastructure. The high volume of oceanographic research and coastal zone management requires efficient underwater systems for data collection. The difficulties are high implementation costs and system integration, yet the prospects are in exporting the developed autonomous underwater technologies worldwide.

Key Takeaways

- Market Size & Forecast: The Global Autonomous Underwater Vehicle Market size is projected to reach USD 2.9 billion in 2026 and is anticipated to have a value of USD 7.6 billion by 2035.

- Growth Rate & Outlook: The market size is set to grow at a compound annual growth rate of 11.3% during the forecast period of 2026 to 2035.

- Primary Growth Drivers: Some of the major growth drivers in the market include technological advancements in underwater autonomy, government investments in maritime security and ocean exploration, and more.

- Key Market Trends: Some of the major trends in the market are the adoption of AI and data-driven decision making for underwater navigation, the shift toward cloud-based mission planning, and more.

- By Type: The Medium AUVs segment is anticipated to get the majority share of the Autonomous Underwater Vehicle market in 2026.

- By Payload Type: The Sonar Systems segment is expected to get the largest revenue share in 2026 in the Autonomous Underwater Vehicle market.

- By System: The Navigation & Communication System segment is expected to get the largest revenue share in 2026 in the Autonomous Underwater Vehicle market.

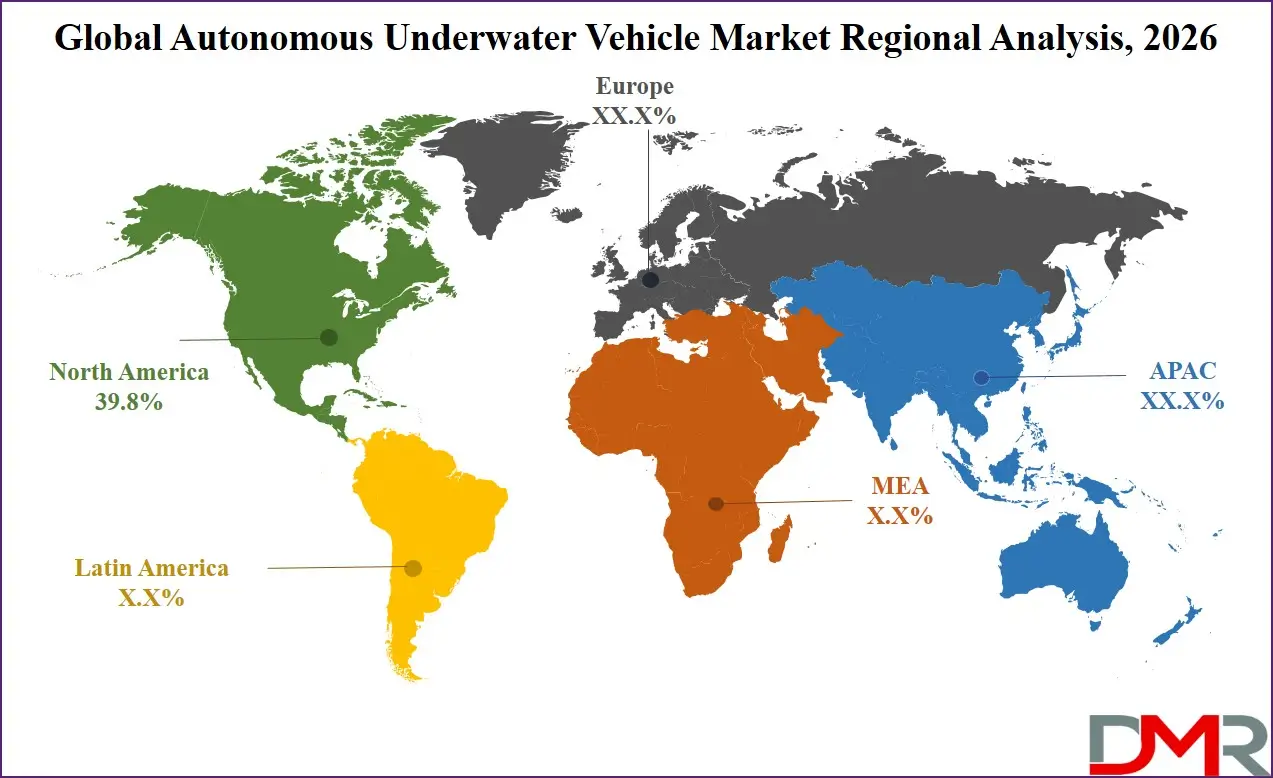

- Regional Leadership: North America is set to lead the Autonomous Underwater Vehicle market with an estimated 39.8% share in 2026.

What is Autonomous Underwater Vehicle?

An autonomous underwater vehicle is a concept of utilizing the latest digital and robotics technologies in underwater systems to streamline subsea operations, improve safety, and data collection for defense, commercial, and research purposes. Such components include smart sonar sensors, automated navigation systems, real-time data analytics, and cloud-based mission planning platforms that facilitate smooth communication between AUVs, surface vessels, and control centers. Autonomous underwater vehicles allow predictive maintenance of subsea infrastructure, effective route planning, and improved asset management. The concept is essential in converting conventional underwater survey methods into intelligent ocean systems, which assist in increasing mission capacity utilization, enhancing reliability, and sustainable marine mobility, as well as offering automation and data-driven decisions in underwater activities.

Use Cases

- Military & Defense Operations: The AUV systems allow automated mine detection, covert surveillance, and efficient underwater reconnaissance, minimizing the risk of human divers and enhancing the efficiency of operations within the naval networks.

- Predictive Maintenance of Underwater Assets: Leaks in underwater pipelines and cables are identified in advance to avoid breakdowns, reduce downtime, limit maintenance costs, and maximize safety.

- Oceanography & Environmental Monitoring: Scientists are able to acquire more accurate data, extended mission durations, and interactivity with real-time water quality sensors, current profiling, and studies of climate change impacts.

- Search & Salvage Operations: New generation sonar and tracking systems maximize the location of wreckage, make recovery operations more efficient, and reduce the time of searching underwater operations.

How AI Is Transforming the Global Autonomous Underwater Vehicle Market

Artificial intelligence is also transforming autonomous underwater vehicle systems, enabling mission planning (predictive), automated obstacle avoidance, and real-time underwater decision-making. Sonar and operational data can be analyzed using AI algorithms to detect any anomaly and optimize performance when it is large enough. This is time-saving, safer, and more efficient.

Moreover, AI enhances the mission performance through offering adaptive navigation, anticipating underwater currents, and intelligent prioritization of payloads. It is also involved in reducing the energy and resource allocation and allowing AUV operators to reduce the cost and environmental footprint and improve the reliability of missions and their operational capacity.

Market Dynamics

Key Drivers of the Global Autonomous Underwater Vehicle Market

Technological Advancements and Automation

The use of AI, advanced sonar, and real-time data analytics are driving the autonomous underwater vehicle market significantly. These technologies enable real time monitoring of the underwater and predictive maintenance and automated mission operations, increasing efficiency and safety. Automation reduces human error, operational costs and maximizes mission capacity. Ongoing navigation system and acoustic communication technology advances lead to improved system reliability, and digital transformation is a necessary part of modern maritime infrastructure development.

Government Investments and Maritime Security Initiatives

The world governments are spending a lot of money in modernizing their naval and ocean observation capabilities, which are also a part of the broader defense and blue economy development programs. Policy support, subsidies, and funding programs are promoting the adoption of AUV technologies. Implementation of measures to protect marine borders and enhance the efficiency of underwater infrastructure inspection is spurring deployment. Such investments provide an attractive atmosphere to the technology providers and system integrators that directly enhances the growth of the market.

Restraints in the Global Autonomous Underwater Vehicle Market

High Capital Investment Requirements

AUV implementation is expensive in terms of initial investment in the hardware, software, and system integration. The process of updating legacy underwater systems can be complicated and expensive, particularly in developing countries. Such cost constraints can cause delays in adoption, especially with smaller research institutes, as the benefit in the long-term operational costs is impeded.

Integration and Interoperability Challenges

AUV systems entail several technologies, which are supposed to seamlessly interact with surface vessels and control centers. The technical challenge of integrating new autonomous solutions with existing maritime infrastructure can take place. The absence of standardized protocols and regional compatibility may be a barrier to adoption. Such difficulties make deployments more expensive and time-consuming, affecting the expansion of the market in general.

Growth Opportunities in the Global Autonomous Underwater Vehicle Market

Expansion in Emerging Economies

To facilitate maritime domain awareness and economic growth, developing countries are investing in underwater exploration capabilities. The areas pose major opportunities for adopting AUVs, since they are not tied to legacy survey technologies. The growing need for efficient ocean monitoring and government incentives provides a good growth opportunity to market participants.

Growth of Blue Economy and Sustainable Ocean Transport

The trend of the blue economy and marine sustainability in the world is also providing AUV systems with new opportunities. AUVs are a crucial part of the future ocean infrastructure by integrating with offshore energy platforms, enabling pipeline inspection, and lowering environmental impact. This is likely to be a long-term demand trend.

Global Autonomous Underwater Vehicle Market Trends

Adoption of AI and Data-Driven Decision Making

The use of AI and analytics in AUV operators is gaining more and more momentum aimed at mission optimization and decision-making. Information-based insights facilitate effective route planning, proactive maintenance of subsea assets, and enhanced data collection. The trend is converting the conventional underwater survey methods into smart, responsive ocean networks.

Shift Toward Cloud-Based Mission Planning

The trend of cloud computing in AUV systems is becoming a fundamental aspect of this sector, allowing the storage of oceanographic data and the availability of mission information on a larger scale and in real-time. Cloud-based solutions facilitate remote mission monitoring, centralized fleet control, and enhanced collaboration. This change increases flexibility in operations and minimizes the cost of infrastructure.

Research Scope and Analysis

By Type Analysis

The Medium AUVs segment is poised to have a market share of about 47.9% in 2026 due to the increasing demand for a flexible payload capacity, endurance, and cost-effectiveness. Medium-sized solutions of interest to defense and research operators include real-time mine countermeasures and oceanography surveys.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The application of AI-based navigation and modular payloads is on the increase, thereby facilitating this segment. In the meantime, the segment of the Large AUVs is the most promising with the growing need for long-range deep-sea operations. Mid-sized AUVs will be right in the middle of the act as the digital transformation of the maritime industry becomes more and more rapid, becoming the key to powering the smart underwater ecosystem.

By Payload Type Analysis

Sonar Systems are expected to dominate with approximately 38.2% market share in the year 2026, owing to their high resolution, affordability, and real-time seabed imaging capabilities. Defense and commercial users are shifting to higher sonar technologies in order to have greater visibility of the underwater environment and improve target recognition. The sonar solutions are adaptable, making it easy to deploy and integrate with other types of AUVs. Cameras can still be used, though, in places where there is visual inspection that is needed. The multi-payload usage with sonar, cameras, and sensors simultaneously has the quickest development, and the mission plans are more flexible to different situations underwater.

By System Analysis

It is expected that the Navigation & Communication System will have the highest share of around 31.5% in 2026, considering its pivotal role in facilitating precise underwater positioning and real-time data transmission. The inertial navigation system and acoustic modem provide continuous flows of positional information, which improve the efficiency and safety of operation. Speed and endurance are calculated by the Propulsion System, and the most common are electric thrusters. The Drive System controls the vehicle dynamics, such as fins and thrust vectoring. The fastest growing area is the Collision Avoidance System, which enhances the power to identify the obstacles and automate the evasive measures by means of forward-looking sonar. The Payload and Imaging System combines cameras, sonars, and sensors to collect mission-specific data. The fusion of navigation and AI is generating smarter AUVs, which results in innovation and expands the technological market.

By Propulsion Analysis

The Electric propulsion segment dominates the AUV market in 2026 due to its quiet operation, high efficiency, and suitability for battery-powered underwater missions. Electric systems are preferred for most defense, research, and commercial applications where stealth and endurance are critical. The Mechanical propulsion segment, including hydraulic and piston-type systems, is used in specialized heavy-duty applications requiring high thrust. The Hybrid segment is the fastest-growing, combining electric efficiency with mechanical power for extended missions and variable speed requirements. Hybrid propulsion enables AUVs to operate in diverse underwater environments, transitioning between energy-saving cruise modes and high-power maneuvering when needed.

By Shape Analysis

The Torpedo shape holds the largest market share in 2026, attributed to its proven hydrodynamic efficiency, low drag, and widespread adoption in military and deep-sea applications. Torpedo-shaped AUVs offer excellent endurance and speed, making them ideal for long-range survey and defense missions. The Laminar Flow Body design, optimized for minimal hydrodynamic resistance, is gaining traction in high-endurance oceanographic missions. Streamlined Rectangular Style AUVs provide greater internal volume for payload integration and are commonly used in shallow-water inspection and mining applications. The Multi-Hull Vehicle segment, though smaller in share, is growing steadily for specialized applications requiring stability, low-speed maneuverability, and surface-switching capabilities such as gliders and hybrid vehicles.

By Application Analysis

Military & Defense in the future is likely to take the lead with an estimated share of 38.4% in 2026, owing to the demand for mine hunting, anti-submarine warfare, and intelligence surveillance reconnaissance operations. Digital solutions enhance mission efficiencies and minimize risks to personnel. The Oil & Gas segment relies heavily on AUVs for pipeline inspection, seabed mapping, and subsea infrastructure monitoring. Oceanography applications include water column profiling, benthic mapping, and climate research. The fastest-growing area is Environmental Monitoring applications driven by the need to have real-time water quality, pollution tracking, and marine protected area surveillance systems. Archaeology & Exploration uses AUVs for shipwreck discovery and underwater heritage documentation. Search & Salvage operations benefit from AUVs in locating downed aircraft, lost cargo, and submerged vessels. With the increasing ocean health concerns and offshore activities, government, defense, and commercial agencies have been spending more on autonomous tools to improve mission success rates and underwater operational efficiency.

By End User Analysis

Defense & Homeland Security represents the largest end-user segment in 2026, accounting for approximately 40 percent of the market, driven by rising naval modernization programs, mine countermeasure requirements, and undersea surveillance needs. Government agencies, including oceanographic institutes and environmental protection bodies, form the second-largest segment, utilizing AUVs for marine research, resource mapping, and regulatory compliance monitoring. Commercial end users, particularly in oil & gas, offshore wind, and subsea cable industries, are adopting AUVs for inspection, maintenance, and repair operations. Research Institutes represent a steadily growing segment, leveraging AUVs for academic and scientific exploration of previously inaccessible underwater environments. Other end users include conservation organizations, museums, and salvage companies. The diversification across end users highlights the broadening adoption of AUV technology beyond traditional defense applications.

The Global Autonomous Underwater Vehicle Market Report is segmented based on the following:

By Type

- Shallow AUVs

- Medium AUVs

- Large AUVs

By Payload Type

- Cameras

- Sensors

- Sonar Systems

- Acoustic Doppler Current Profilers

- Others

By System

- Propulsion System

- Drive System

- Navigation & Communication System

- Collision Avoidance System

- Payload & Imaging System

By Propulsion

- Electric

- Mechanical

- Hybrid

By Shape

- Torpedo

- Laminar Flow Body

- Streamlined Rectangular Style

- Multi-Hull Vehicle

By Application

- Military & Defense

- Oil & Gas

- Oceanography

- Environmental Monitoring

- Archaeology & Exploration

- Search & Salvage

By End User

- Defense & Homeland Security

- Government

- Commercial

- Research Institutes

- Others

Regional Analysis

Leading Region by Market Share

The Global Autonomous Underwater Vehicle market is primarily led by North America, accounting for the largest share of the global market in 2026. The region's dominance is driven by strong defense expenditure, advanced naval modernization programs, and the presence of key technology providers. The widespread adoption of autonomous underwater systems for surveillance, intelligence, and deep-sea exploration further strengthens North America's leading position in the market. Additionally, continuous investments in AI-enabled maritime autonomy and underwater warfare capabilities are further reinforcing regional technological leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is the fastest-growing region, supported by rapid naval modernization programs, increasing investments in maritime security, and expanding offshore energy exploration activities. Countries such as China, India, Japan, and South Korea are actively deploying autonomous underwater technologies to enhance operational efficiency and strengthen ocean surveillance capabilities. Growing emphasis on marine research and indigenous AUV development further accelerates market expansion in the region. Moreover, increasing government initiatives to strengthen territorial waters monitoring and blue economy development are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The autonomous underwater vehicle market is very competitive, with innovation and strategic alliances being the order of the day. In order to achieve a competitive advantage, companies are oriented towards the creation of new advanced technologies, including AI-powered navigation and sonar-enabled imaging systems. There are high barriers to entry because of capital-intensive R&D and technical know-how. Strategic approaches in the market to increase market presence include partnerships, mergers, and long-term contracts with defense and research operators. Moreover, research and development are important factors in staying competitive and meeting the changing needs of the industry.

Some of the prominent players in the Global Autonomous Underwater Vehicle Market are:

- Kongsberg Gruppen ASA

- Teledyne Technologies Incorporated

- Lockheed Martin Corporation

- Saab AB

- BAE Systems plc

- Atlas Elektronik GmbH

- L3Harris Technologies, Inc.

- Fugro N.V.

- General Dynamics Corporation

- The Boeing Company

- Exail Technologies

- Oceaneering International, Inc.

- Sonardyne International Ltd.

- Northrop Grumman Corporation

- Huntington Ingalls Industries

- International Submarine Engineering Ltd.

- Ocean Infinity

- Saipem S.p.A

- Boston Engineering Corporation

- Thales Group

- Other Key Players

Recent Developments

- January 2026: Teledyne Technologies Incorporated confirmed delivery of multiple Gavia AUV systems to defense users, while reporting that its autonomous subsea systems are now deployed across 18 navies and multiple NATO users. The company continues to expand its role as a major supplier of sonar, gliders, and autonomous underwater platforms.

- September 2025: BAE Systems plc announced it is targeting market readiness of its autonomous submarine "Herne" by 2026, developed with Cellula Robotics. The system is designed for mine countermeasures, seabed surveillance, and naval intelligence missions, marking a major step toward operational deployment of combat-capable autonomous underwater systems.

- July 2025: Kongsberg Gruppen ASA began expanding HUGIN AUV production into the United States, responding to rising demand from the U.S. Navy and allied defense programs. The move strengthens supply chain localization and supports increased procurement of autonomous underwater systems for seabed warfare and underwater surveillance missions.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2.9 Bn |

| Forecast Value (2035) |

USD 7.6 Bn |

| CAGR (2026–2035) |

11.3% |

| The US Market Size (2026) |

USD 1.0 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Type (Shallow AUVs, Medium AUVs, Large AUVs), By Payload Type (Cameras, Sensors, Sonar Systems, Acoustic Doppler Current Profilers, Others), By System (Propulsion System, Drive System, Navigation & Communication System, Collision Avoidance System, Payload & Imaging System), By Propulsion (Electric, Mechanical, Hybrid), By Shape (Torpedo, Laminar Flow Body, Streamlined Rectangular Style, Multi-Hull Vehicle), By Application (Military & Defense, Oil & Gas, Oceanography, Environmental Monitoring, Archaeology & Exploration, Search & Salvage), By End User (Defense & Homeland Security, Government, Commercial, Research Institutes, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Autonomous Underwater Vehicle Market?

▾ The Global Autonomous Underwater Vehicle Market size is estimated to have a value of USD 2.9 billion in 2026 and is expected to reach USD 7.6 billion by the end of 2035.

What is the CAGR of the Global Autonomous Underwater Vehicle Market from 2026 to 2035?

▾ The market is growing at a CAGR of 11.3% over the forecasted period.

What factors are driving the growth of the Global Autonomous Underwater Vehicle Market?

▾ Technological advancements in underwater autonomy, government investments in maritime security and ocean exploration, and more are the factors driving the growth of the Autonomous Underwater Vehicle Market.

What are the major trends in the Global Autonomous Underwater Vehicle Market?

▾ Adoption of AI and data-driven decision making for underwater navigation, a shift toward cloud-based mission planning, and more are some of the major trends in the market.

Which region held the largest share of the Global Autonomous Underwater Vehicle Market in 2026?

▾ North America is expected to have the largest market share in the Global Autonomous Underwater Vehicle Market with a share of about 39.8% in 2026.

Which region is expected to grow the fastest in the Global Autonomous Underwater Vehicle Market?

▾ Asia-Pacific is the fastest-growing region in the Autonomous Underwater Vehicle market during the forecast period.

Who are the key players in the Global Autonomous Underwater Vehicle Market?

▾ Some of the major key players in the Global Autonomous Underwater Vehicle Market are Kongsberg Gruppen ASA, Teledyne Technologies Incorporated, Lockheed Martin Corporation, General Dynamics Corporation, Saab AB, and many others.

How is the Global Autonomous Underwater Vehicle Market segmented?

▾ The market is segmented by type, payload type, system, propulsion, shape, application, and end user.