What is the Global Battery Simulation Software Market Size?

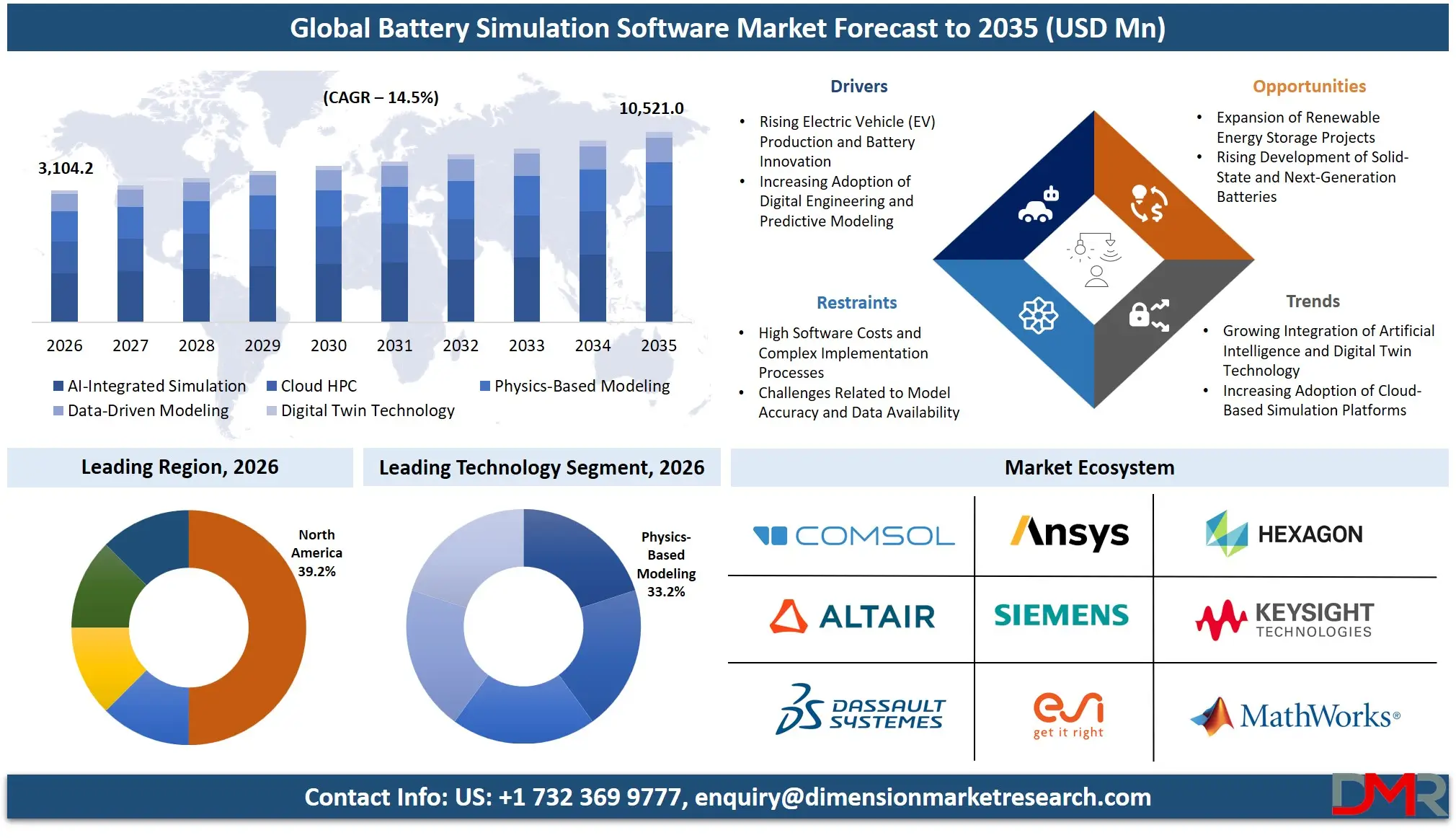

The Global Battery Simulation Software Market is expected to reach a value of USD 3,104.2 million in 2026, and it is further anticipated to reach USD 10,521.0 million by 2035, growing at a CAGR of 14.5% during the forecast period.

ℹ

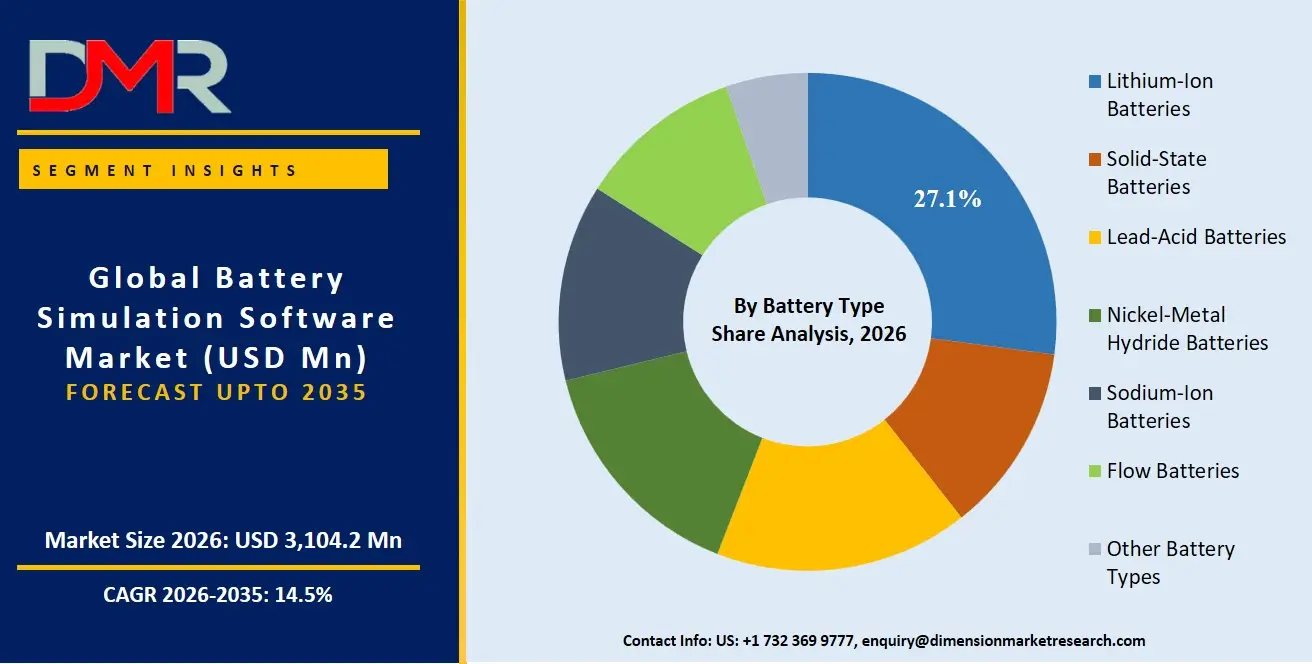

To learn more about this report –

Download Your Free Sample Report Here

The battery simulation software market is experiencing a significant acceleration, driven by the global paradigm shift toward electrification and renewable energy integration. Enterprises and research institutions are rapidly moving away from costly, time-intensive physical prototyping to virtual modeling environments.

The market consists of electrochemical modeling, thermal runaway analysis, structural mechanics, and battery management system (BMS) validation tools that assist engineers in designing safer, denser, and longer-lasting energy storage systems. The increasing demand for faster time-to-market in electric vehicle (EV) production, the complexity of multi-physics interactions within solid-state batteries, and the integration of AI-driven predictive diagnostics are fueling the necessity for specialized digital twin and high-performance computing (HPC) simulation platforms. The automotive & EV and energy storage systems (ESS) sectors are the most prolific adopters, with lithium-ion simulation remaining dominant due to its established supply chain, while solid-state battery modeling is emerging as a critical growth frontier.

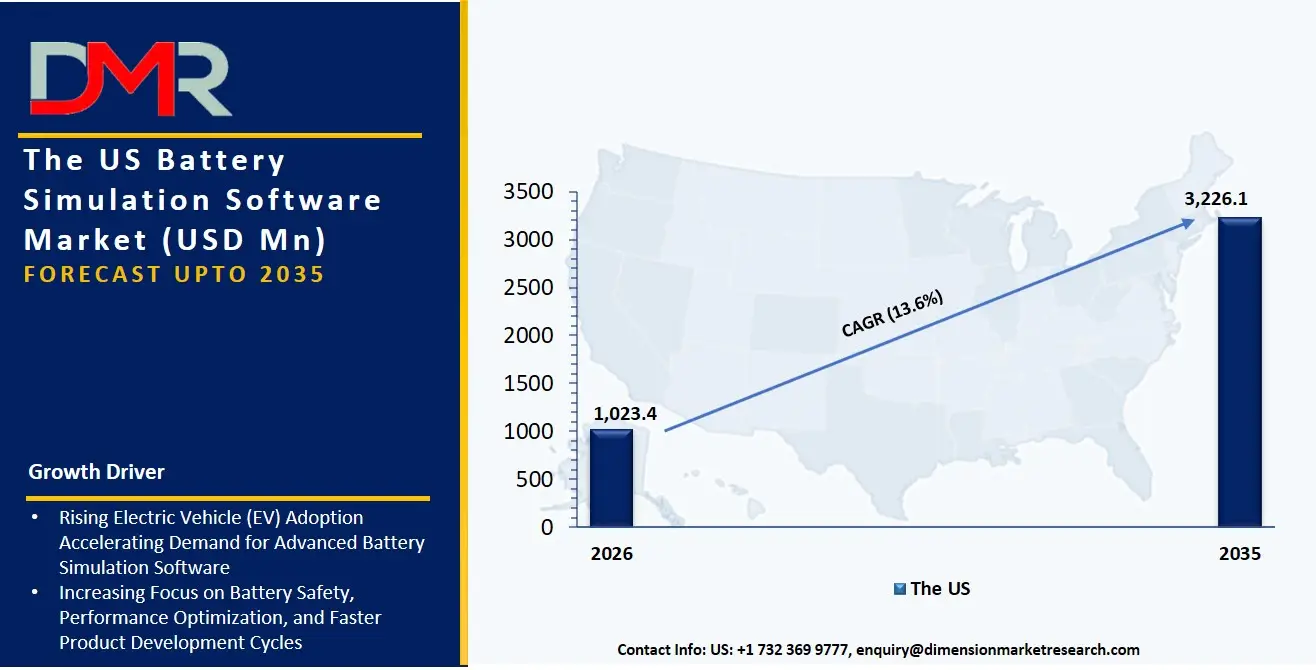

The US Battery Simulation Software Market

The US Battery Simulation Software Market is projected to reach USD 1,023.4 million in 2026, growing at a CAGR of 13.6% to culminate in a value of USD 3,226.1 million by 2035. The US maintains its position as the most mature and technologically advanced market, underpinned by aggressive federal funding for domestic battery manufacturing and the rapid electrification strategies of Detroit's automotive giants. The market is characterized by a high demand for multiphysics and electrochemical simulation tools, as organizations prioritize the reduction of thermal runaway risks in next-generation EV battery packs. Furthermore, the establishment of gigafactory production lines is generating substantial demand for manufacturing process simulation and digital twin technology to optimize electrode drying, formation, and aging cycles before physical commissioning.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Battery Simulation Software Market

The European battery simulation market is estimated to be valued at USD 895.6 million in 2026, advancing to USD 2,958.4 million by 2035 at a CAGR of 14.2%. The European ecosystem is deeply influenced by stringent regulatory frameworks like the EU Battery Regulation and the digital battery passport mandate, which require meticulous lifecycle analysis and carbon footprint tracking. This drives the need for physics-based degradation modeling and lifecycle simulation tools. The region is also witnessing accelerated growth in mechanical and structural simulation services, as manufacturers in Germany and the Nordics seek to optimize crash safety and structural integrity of battery enclosures without adding excessive weight. Additionally, pan-European consortiums focused on sovereign cell development are compelling software vendors to create highly accurate data-driven models that ensure interoperability and performance traceability across the continent's evolving battery value chain.

The Japan Battery Simulation Software Market

The Japan Battery Simulation Software Market is projected to be valued at USD 312.8 million in 2026, reaching USD 1,019.5 million by 2035, growing at a CAGR of 14.0%. The Japanese market is unique, driven by a corporate-wide strategic imperative to leapfrog current lithium-ion limitations through the rapid commercialization of solid-state and sulfide-based electrolyte batteries. Material informatics and AI-integrated simulation tools constitute a large portion of R&D spending, enabling conglomerates to virtually screen thousands of electrolyte-cathode combinations without physical synthesis. There is also a strong requirement for high-fidelity thermal simulation to bridge the gap between lab-scale coin cells and commercial-scale prismatic or pouch modules, forming a niche in multiphysics coupling and extreme-fast-charging degradation analysis.

Key Takeaways

- Market Size & Forecast: The Global Battery Simulation Software market is projected to reach USD 3,104.2 million in 2026, expanding to USD 10,521.0 million by 2035, fueled by the dual engines of EV mass adoption and the mandatory transition from physical prototyping to virtual validation.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 14.5%, propelled by a critical shortage of electrochemical engineers and the escalating complexity of managing multi-scale, multi-dimensional physics models that span from molecular dynamics to system-level thermal management.

- Primary Growth Drivers: Key forces include the reduction of costly "design-test-fail" physical testing cycles, the necessity for battery management systems (BMS) simulation to ensure functional safety and state-of-health (SoH) accuracy, and the integration of digital twins requiring specialized lifecycle & degradation analysis skills.

- Key Market Trends: Major trends include the rise of AI-driven "inverse design" to autonomously discover next-gen electrode materials, the use of cloud HPC to solve complex computational fluid dynamics (CFD) cooling problems for DC fast charging, and the shift toward safety & failure analysis as boards prioritize preventing thermal runaway field failures.

- By Simulation Type Analysis: Electrochemical simulation is expected to dominate fundamental R&D, but multiphysics simulation is growing fastest as enterprises realize that thermal, electrical, and mechanical degradation are inextricably linked within a sealed cell environment. Professional simulation tools are increasingly required to couple Newman-based pseudo-2D models with 3D thermal models seamlessly.

- By End-Use Industry Analysis: Automotive & Electric Vehicles and Energy Storage Systems (ESS) are the most lucrative verticals due to scale and safety-critical requirements. Consumer electronics remains a steady demand driver, while aerospace & defense is an emerging high-value sector demanding exotic high-power and low-weight custom chemistry simulations.

- Regional Leadership: North America is poised to dominate this market with a 39.2% market share in 2026, driven by a robust venture capital ecosystem funding battery-tech startups and a dense concentration of cloud HPC infrastructure that accelerates simulation throughput.

What is the Battery Simulation Software Market?

Battery Simulation Software comprises the specialized computational modeling and virtual testing platforms offered by third-party developers, academic licenses, and engineering consultancies to assist organizations across the full battery innovation lifecycle. These services, distinct from physical materials or cell manufacturing, relate to the how of battery engineering. This involves cell simulation to design novel active materials and electrolytes at the atomistic level, multiphysics modeling to couple heat generation, mechanical stress, and lithium-plating phenomena, and testing & validation tools to replace hardware-in-the-loop testing with software-in-the-loop for BMS algorithms. With 90% of battery developers utilizing a combination of commercial and bespoke simulation codes, professional-grade software is essential to achieve accurate state-of-charge (SoC) estimation, longevity prediction, and safety compliance, translating raw computational power into tangible improvements in energy density and cycle life rather than just raw data.

Use Cases

- Virtual Material Screening for Solid-State Electrolytes: Automotive OEMs utilize cell simulation and AI-integrated simulation platforms to virtually screen thousands of solid electrolyte candidate materials, narrowing down synthesis to a handful of top performers, drastically cutting the R&D timeline for anodeless architectures.

- Grid-Scale Thermal Runaway Propagation: Utility-scale ESS integrators use computational fluid dynamics (CFD) and thermal simulation tools to model catastrophic thermal runaway propagation across thousands of cells within a container, designing passive propagation resistance (PPR) barriers to meet NFPA safety standards without destructive live-testing.

- BMS Functional Safety (FuSa) Validation: Semiconductor and Tier-1 suppliers use testing & validation tools and hardware-in-the-loop emulation to inject thousands of fault conditions into a virtual BMS, validating firmware responses to over-voltage, under-temperature, and short-circuit events for ISO 26262 ASIL-D compliance.

- Fast-Charge Electrode Architecture Optimization: Consumer electronics manufacturers employ multiphysics and electrochemical simulation to optimize the porosity, tortuosity, and particle size distribution of graphite anodes, enabling 10-minute fast-charge capabilities without lithium plating that would degrade cycle life.

How AI is Transforming the Battery Simulation Software Market?

AI is revolutionizing battery simulation by transforming the speed of materials discovery and the accuracy of predictive maintenance. In cell simulation, AI-integrated surrogate models are replacing traditional first-principles calculations, allowing researchers to screen massive chemical spaces for optimal ionic conductivity properties millions of times faster than density functional theory (DFT). Meanwhile, AI-driven features in digital twin technology allow grid operators to predict the remaining useful life (RUL) of BESS assets with high precision by fusing real-time operational data with physics-informed neural networks, directly informing warranty reserves and energy trading strategies.

Business strategy and manufacturing are now deeply intertwined with AI. In the application of manufacturing process simulation, intelligent computer vision and data-driven models are being used to detect micron-level coating defects during electrode wetting and drying in real-time, automatically feeding back process parameters to ensure uniform quality. Moreover, generative AI copilots are beginning to augment simulation platforms, allowing engineers to query failure root causes via natural language prompts rather than manually sifting through terabytes of transient simulation output data.

Market Dynamics

Key Drivers in the Global Battery Simulation Software Market

Rising Electric Vehicle (EV) Production and Battery Innovation

The rapid expansion of the global electric vehicle industry is one of the primary drivers of the battery simulation software market. Automotive manufacturers are increasingly investing in advanced battery technologies to improve driving range, charging speed, safety, and energy efficiency. Battery simulation software enables companies to test and optimize battery performance digitally before physical production, significantly reducing development costs and time-to-market. Governments across North America, Europe, and Asia-Pacific are also introducing stricter emission regulations and incentives for EV adoption, accelerating battery research and development activities. Additionally, rising investments in lithium-ion, solid-state, and sodium-ion battery technologies are increasing the need for accurate electrochemical and thermal simulation tools, strengthening the market demand for advanced battery simulation platforms globally.

Increasing Adoption of Digital Engineering and Predictive Modeling

The growing adoption of digital engineering technologies across battery manufacturing and energy storage industries is significantly driving the battery simulation software market. Companies are increasingly using predictive modeling, AI-based analytics, and digital twin technologies to improve battery reliability, reduce prototype failures, and accelerate innovation cycles. Simulation software helps manufacturers evaluate battery behavior under various operating conditions, enabling faster design optimization and improved safety compliance. The rising complexity of modern battery systems, especially in EVs and renewable energy storage applications, further increases the need for advanced simulation capabilities. In addition, manufacturers are focusing on reducing operational costs and minimizing material waste through virtual testing environments. This shift toward data-driven battery development continues supporting strong demand for battery simulation software solutions worldwide.

Restraints in the Global Battery Simulation Software Market

High Software Costs and Complex Implementation Processes

One of the major restraints affecting the global battery simulation software market is the high cost associated with advanced simulation platforms and their implementation. Comprehensive battery simulation tools often require substantial investments in software licenses, high-performance computing infrastructure, and technical expertise, making adoption difficult for small and medium-sized enterprises. In addition, integrating simulation software into existing engineering workflows can be complex and time-consuming. Companies frequently require skilled professionals with expertise in electrochemistry, thermal analysis, and multiphysics modeling to operate these platforms effectively. Training costs and limited availability of experienced simulation engineers can further slow adoption. These financial and operational challenges may limit market penetration, particularly in developing economies and among smaller battery manufacturers with constrained budgets.

Challenges Related to Model Accuracy and Data Availability

Battery simulation software relies heavily on accurate material properties, electrochemical data, and real-world operating conditions to generate reliable results. However, obtaining high-quality and standardized battery performance data remains a significant challenge for many manufacturers and research organizations. Variations in battery chemistry, manufacturing methods, and environmental conditions can reduce the accuracy of simulation models, affecting predictive reliability. In addition, next-generation battery technologies such as solid-state and sodium-ion batteries often lack sufficient historical data for advanced modeling. This creates difficulties in validating simulation outcomes and increases uncertainty during product development. Continuous updates, calibration requirements, and complex multiphysics interactions also add to modeling challenges, potentially limiting confidence in simulation-driven decision-making across the battery industry.

Growth Opportunities in the Global Battery Simulation Software Market

Expansion of Renewable Energy Storage Projects

The increasing deployment of renewable energy systems worldwide is creating major growth opportunities for the battery simulation software market. Solar and wind energy projects require efficient battery energy storage systems to manage power fluctuations and improve grid stability. Battery simulation software helps energy companies optimize storage system design, thermal management, charging cycles, and long-term battery performance. Governments and utility providers are investing heavily in grid-scale energy storage projects to support clean energy transitions and carbon reduction goals. This growing demand for advanced battery technologies is encouraging the adoption of simulation platforms capable of improving operational efficiency and reducing maintenance costs. Additionally, rising investments in smart grids and distributed energy systems are expected to create long-term opportunities for battery simulation software providers globally.

Rising Development of Solid-State and Next-Generation Batteries

The growing focus on next-generation battery technologies presents a strong growth opportunity for the battery simulation software market. Companies and research institutions are investing significantly in solid-state, sodium-ion, lithium-sulfur, and other advanced battery chemistries to achieve higher energy density, faster charging, and improved safety. These emerging battery technologies require extensive virtual testing and predictive modeling due to their complex electrochemical behavior and limited commercialization history. Simulation software plays a critical role in accelerating research, reducing development costs, and minimizing physical prototyping requirements. In addition, increasing competition among automotive OEMs and battery manufacturers to commercialize innovative battery technologies is driving demand for highly accurate multiphysics and AI-driven simulation platforms, creating substantial growth potential for software providers in the coming years.

Trends in the Global Battery Simulation Software Market

Growing Integration of Artificial Intelligence and Digital Twin Technology

A major trend shaping the global battery simulation software market is the increasing integration of artificial intelligence and digital twin technologies into simulation platforms. AI-driven simulation tools enable faster data analysis, predictive maintenance, and automated optimization of battery performance under different operating conditions. Digital twin technology allows manufacturers to create real-time virtual replicas of battery systems, improving monitoring, lifecycle analysis, and operational efficiency. These technologies help companies reduce testing time, improve battery reliability, and accelerate innovation in electric vehicles and energy storage applications. In addition, AI-powered simulation solutions can process large datasets more efficiently, enabling more accurate predictions related to degradation, thermal behavior, and charging performance. This technological advancement is transforming battery development and manufacturing processes globally.

Increasing Adoption of Cloud-Based Simulation Platforms

The battery simulation software market is experiencing a strong trend toward cloud-based deployment models as companies seek scalable and cost-efficient engineering solutions. Cloud-based simulation platforms provide remote accessibility, faster collaboration, and high-performance computing capabilities without requiring large on-premises infrastructure investments. Battery manufacturers, automotive OEMs, and research organizations are increasingly using cloud environments to conduct complex electrochemical and thermal simulations more efficiently. This trend is particularly beneficial for global development teams working across multiple locations. In addition, cloud-based platforms support easier software updates, data sharing, and integration with AI and machine learning tools. As battery systems become more complex and simulation workloads increase, the demand for flexible and scalable cloud-based battery simulation solutions is expected to grow significantly worldwide.

Research Scope and Analysis

The analysis of the Agentic AI in Pharmaceutical Market highlights dominance across key segments including drug discovery, cloud deployment, large pharmaceutical end-users, and sales optimization. Growth is driven by automation efficiency in early-stage research, scalable cloud infrastructure, and strong ROI from commercialization and market research applications.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Software Type Analysis

Cell simulation is projected to dominate the battery simulation software market because battery manufacturers and EV developers heavily rely on cell-level modeling to optimize energy density, charging efficiency, thermal stability, and battery lifespan before physical prototyping. Cell simulation software helps companies reduce development costs and accelerate commercialization by predicting electrochemical behavior under different operating conditions. The increasing demand for high-performance lithium-ion and next-generation solid-state batteries further strengthens the importance of cell simulation tools. Automotive OEMs, battery startups, and research institutions are investing significantly in advanced cell modeling platforms to improve battery safety and efficiency. In addition, the growing complexity of EV battery architectures and rising focus on fast-charging technologies continue supporting the dominance of cell simulation solutions across the global market.

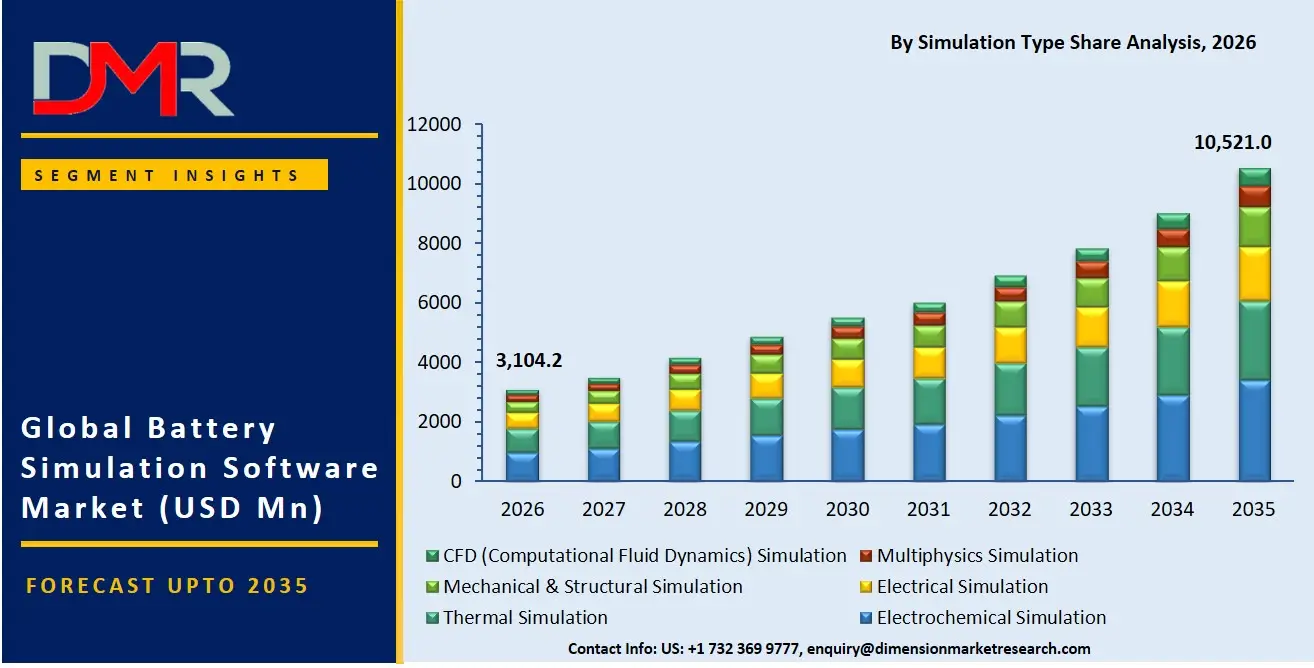

By Simulation Type Analysis

Electrochemical simulation is poised to dominate the battery simulation software market due to its critical role in analyzing battery chemistry, ion transport behavior, degradation mechanisms, and overall cell performance. Manufacturers increasingly depend on electrochemical modeling to shorten development cycles and reduce costly experimental testing.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The technology enables engineers to optimize battery materials, charging efficiency, cycle life, and energy density for electric vehicles, consumer electronics, and energy storage systems. Growing investments in next-generation battery technologies such as solid-state and sodium-ion batteries are further driving demand for electrochemical simulation platforms. Additionally, stricter safety standards and increasing pressure to improve battery reliability encourage companies to adopt advanced electrochemical simulation tools that provide accurate predictive analysis and enhance product innovation across multiple industries.

By Battery Type Analysis

Lithium-ion batteries is anticipated to dominate the battery simulation software market because they remain the most widely used battery technology across electric vehicles, consumer electronics, industrial equipment, and energy storage systems. The rapid global expansion of EV production and renewable energy storage projects has significantly increased demand for simulation tools specifically designed for lithium-ion battery optimization. Manufacturers use simulation software to improve battery safety, thermal management, charging speed, cycle life, and energy density while minimizing development costs and physical testing requirements. In addition, continuous advancements in lithium-ion chemistries, including LFP and NMC batteries, are creating strong demand for accurate modeling and predictive analysis solutions. The widespread commercialization and technological maturity of lithium-ion batteries continue reinforcing their dominant market position globally.

By Technology Analysis

Physics-based modeling is projected to dominate the battery simulation software market because it provides highly accurate analysis of electrochemical, thermal, and mechanical battery behavior using scientifically validated principles. Automotive manufacturers, battery developers, and research organizations rely on physics-based models to predict battery performance, degradation, safety risks, and charging characteristics under various operating conditions. This modeling approach helps reduce dependence on physical prototypes, lowering development costs and accelerating product innovation. The growing complexity of advanced battery systems, especially for electric vehicles and grid-scale energy storage, further strengthens the adoption of physics-based simulation platforms. In addition, the technology supports integration with multiphysics and digital twin solutions, enabling comprehensive battery optimization. Its reliability and precision continue making physics-based modeling the preferred technology across the global market.

By Application Analysis

Battery design and development is expected to dominate the battery simulation software market because manufacturers increasingly prioritize faster innovation cycles, cost reduction, and performance optimization in battery production. Simulation software enables engineers to evaluate battery architecture, material selection, thermal behavior, and charging efficiency before physical prototyping, significantly reducing research and development expenses. The rapid growth of electric vehicles and renewable energy storage systems has intensified demand for advanced battery designs with higher energy density, longer lifespan, and improved safety. Companies are therefore investing heavily in digital engineering and predictive simulation technologies to accelerate commercialization timelines. In addition, rising competition among battery manufacturers and stricter regulatory requirements for battery performance and safety continue driving strong adoption of simulation solutions in battery design and development applications globally.

By End-Use Industry Analysis

Automotive and electric vehicles is projected to dominate the battery simulation software market due to the rapid global transition toward electrified transportation and increasing investments in EV battery innovation. Automakers and battery manufacturers rely heavily on simulation software to optimize battery performance, thermal management, charging efficiency, safety, and lifecycle durability while reducing physical testing costs. The growing demand for long-range electric vehicles and fast-charging technologies is further accelerating the adoption of advanced battery simulation platforms. Government regulations supporting emission reduction and clean transportation are also encouraging large-scale EV production, particularly in North America, Europe, and Asia-Pacific. Additionally, intense competition among automotive OEMs to develop next-generation battery technologies and improve vehicle efficiency continues strengthening the dominance of the automotive and EV segment in the global market.

The Global Battery Simulation Software Market Report is segmented on the basis of the following:

By Software Type

- Cell Simulation

- Battery Management Systems (BMS)

- Testing & Validation Tools

By Simulation Type

- Electrochemical Simulation

- Thermal Simulation

- Electrical Simulation

- Mechanical & Structural Simulation

- Multiphysics Simulation

- CFD (Computational Fluid Dynamics) Simulation

By Battery Type

- Lithium-Ion Batteries

- Solid-State Batteries

- Lead-Acid Batteries

- Nickel-Metal Hydride Batteries

- Sodium-Ion Batteries

- Flow Batteries

- Other Battery Types

By Technology

- AI-Integrated Simulation

- Cloud HPC

- Physics-Based Modeling

- Data-Driven Modeling

- Digital Twin Technology

By Application

- Battery Design & Development

- Battery Performance Optimization

- Battery Thermal Management

- Battery Lifecycle & Degradation Analysis

- Charging & Discharging Analysis

- Safety & Failure Analysis

- Manufacturing Process Simulation

- Digital Twin & Predictive Modeling

By End-Use Industry

- Automotive & Electric Vehicles

- Energy Storage Systems (ESS)

- Consumer Electronics

- Aerospace & Defense

- Industrial Equipment

- Marine

- Healthcare & Medical Devices

- Telecommunications

- Research & Academia

- Other End-Use Industry

Regional Analysis

Leading Region by Market Share

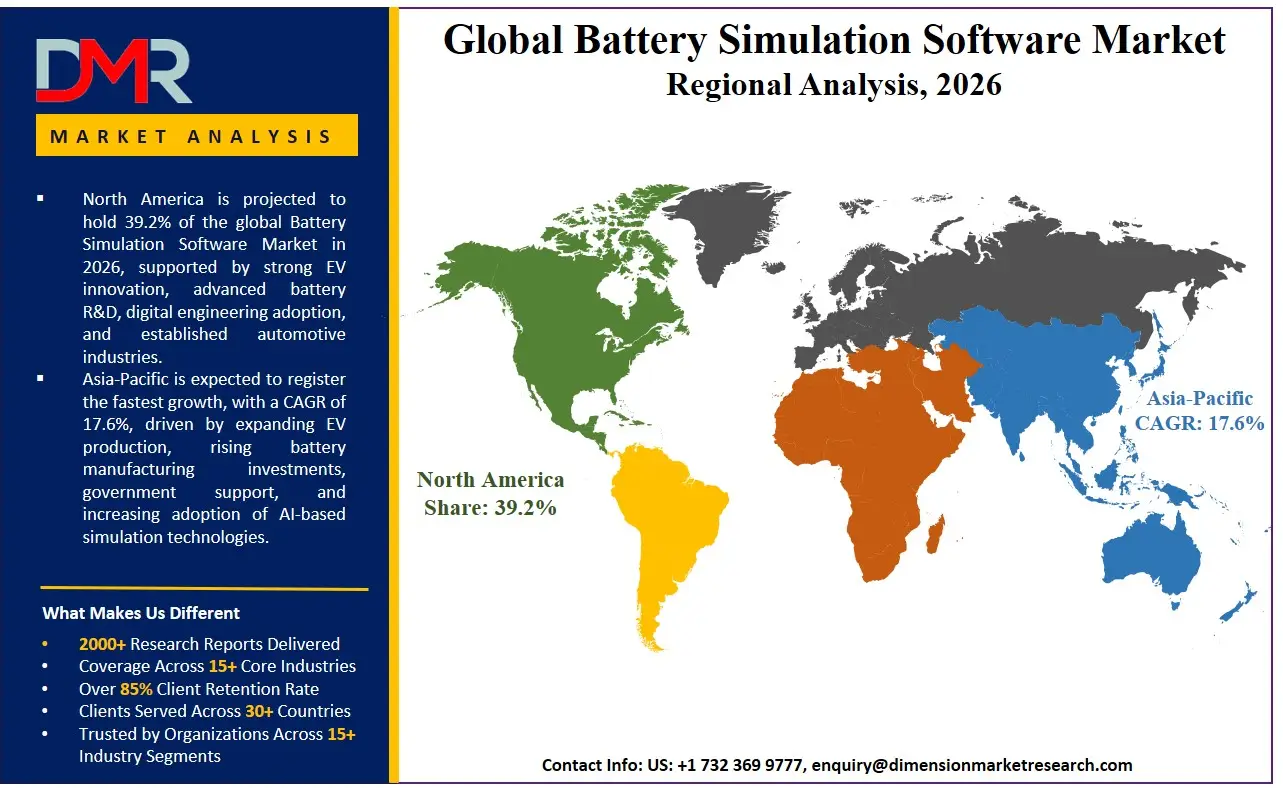

North America is poised to dominate the global battery simulation software market, holding a projected 39.2% of the market share by the end of 2026. The United States, which serves as the epicenter of this dominance, commands the highest share due to an unmatched concentration of cloud hyper-scalers providing high-performance computing (HPC) cycles and the aggressive electrification agendas of Detroit-based automakers alongside a vibrant start-up culture in Silicon Valley focused on solid-state and silicon anode breakthroughs. The region possesses a deeply established ecosystem of national laboratories offering open-source physics-based solvers, major commercial ISVs (Independent Software Vendors), and a rich talent pool of computational electrochemists. Massive federal investment in domestic battery gigafactories through the Bipartisan Infrastructure Law contributes to sustained demand for manufacturing process simulation and virtual formation optimization, while a buoyant venture capital climate continuously funds novel AI-native simulation entrants requiring expert validation tools.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding battery simulation market, driven by the entire continental-scale consolidation of the lithium-ion supply chain, from precursor cathode active material (pCAM) processing to final pack integration in China, South Korea, and Japan. The blistering pace of production capacity expansion and the race to commercialize cobalt-free and high-voltage mid-nickel chemistries are compelling global battery giants and state-backed entities to discard legacy trial-and-error methods. Digital twin and multiphysics simulation are in high demand to help these massive organizations reduce scrap rates in electrode coating and optimize formation protocols. There is also a severe lack of highly experienced R&D engineers relative to the scale of capacity expansion, making it necessary to embed AI-integrated simulation into workflows to automate DoE (Design of Experiments) strategies, bridging the skills gap and enabling faster throughput on next-generation sodium-ion and LMFP (lithium manganese iron phosphate) product portfolios.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global battery simulation software market has become highly dynamic with a heterogeneous array of multinational CAE (Computer-Aided Engineering) giants, specialized electrochemistry software firms, and the cloud platform divisions of major hyperscalers. The key to success will be the profound strategic alliances with major cell manufacturers, automotive OEMs, and national research consortia because they will open the necessary co-development opportunities and early access to the material property databases for next-generation chemistries. The movement towards market consolidation is rapidly progressing with traditional system-level simulation companies acquiring specialized physics-based electrochemical and atomistic-scale modeling boutiques to stay competitive. Proprietary intellectual property, including automated parameter identification frameworks, AI-driven surrogate model generators, and application-specific digital twin accelerators, is becoming a more important basis of competitive differentiation than just generic meshing or solver speed approaches.

Some of the prominent players in the Global Battery Simulation Software Market are:

- Ansys

- COMSOL

- Siemens Digital Industries Software

- Dassault Systèmes

- Altair Engineering

- AVL List GmbH

- ESI Group

- MathWorks

- PTC

- Hexagon AB

- Keysight Technologies

- Gamma Technologies

- Cadence Design Systems

- Synopsys

- dSPACE

- AutoLion

- Battery Design Studio

- Maplesoft

- Duality AI

- Bosch Engineering

- Other Key Players

Recent Developments

- January 2026: Ansys announced a major expansion of its AI-integrated simulation and digital twin platform portfolio to support Automotive & Electric Vehicles and Energy Storage Systems customers with predictive maintenance, virtual sensing, and advanced Safety & Failure Analysis capabilities.

- November 2025: Dassault Systèmes expanded its partnership with a European automotive consortium and introduced advanced Multiphysics Simulation and Lifecycle & Degradation Analysis solutions to help gigafactory operators comply with EU Battery Regulation digital passport requirements.

- October 2025: Altair Engineering acquired a European computational electrochemistry company to strengthen its Cell Simulation and Manufacturing Process Simulation capabilities for solid-state battery manufacturing and aerospace battery research initiatives.

- August 2025: Siemens Digital Industries Software launched a cloud-based battery engineering platform integrating electrochemical, thermal, and electrical simulation technologies to accelerate EV battery development and improve battery lifecycle optimization for global automotive manufacturers.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 3,104.2 Mn |

| Forecast Value (2035) |

USD 10,521.0 Mn |

| CAGR (2026–2035) |

14.5% |

| The US Market Size (2026) |

USD 1,023.4 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Software Type, By Simulation Type, By Battery Type, By Technology, By Application, and By End-Use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Battery Simulation Software Market?

▾ The Global Battery Simulation Software market is poised to be valued at USD 3,104.2 million in 2026 and is projected to reach USD 10,521.0 million by 2035, driven by the universal need for specialized digital tools in electrochemical design, thermal safety, and lifecycle management.

What is the CAGR of the Global Battery Simulation Software Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 14.5% from 2026 to 2035, reflecting the accelerating complexity of next-generation battery chemistries and the persistent shortage of internal multiphysics engineering talent.

What factors are driving the growth of the Global Battery Simulation Software Market?

▾ Key drivers include the global electrochemical engineering skills gap, the imperative to virtually validate solid-state designs, the management complexity of coupled electrochemical-thermal-structural interactions, and the surge in demand for Lifecycle & Degradation Analysis amid evolving battery passport legislation.

Which region held the largest share of the Battery Simulation Software Market in 2026?

▾ North America, specifically the United States, is projected to hold a 39.2% market share in 2026, driven by a mature national lab ecosystem and aggressive enterprise investment in Cell Simulation and AI-driven predictive modeling capabilities.

Which region is expected to grow the fastest in the Battery Simulation Software Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid manufacturing digitalization in China, Japan, and South Korea, where Manufacturing Process Simulation is critical for transitioning gigafactories to high-yield solid-state and sodium-ion operations.

What are the major trends in the Global Battery Simulation Software Market?

▾ Major trends include the integration of Generative AI into materials discovery workflows, the rise of cloud-HPC and simulation-as-a-service, the demand for chemistry-specific modeling tools, and the focus on Digital Twin & Predictive Modeling within complex fleet-wide battery management environments.

Who are the key players in the Global Battery Simulation Software Market?

▾ Key players include Global leaders like ANSYS, Dassault Systèmes, and Siemens Digital Industries Software, as well as specialized electrochemistry software firms like COMSOL and Gamma Technologies, alongside cloud-native simulation platforms like SimScale and Rescale.

How is the Global Battery Simulation Software Market segmented?

▾ The market is segmented by Software Type, Simulation Type, Battery Type, Technology, Application, and End-Use Industry.