What is the Bio-based Epoxy Resin Market Size?

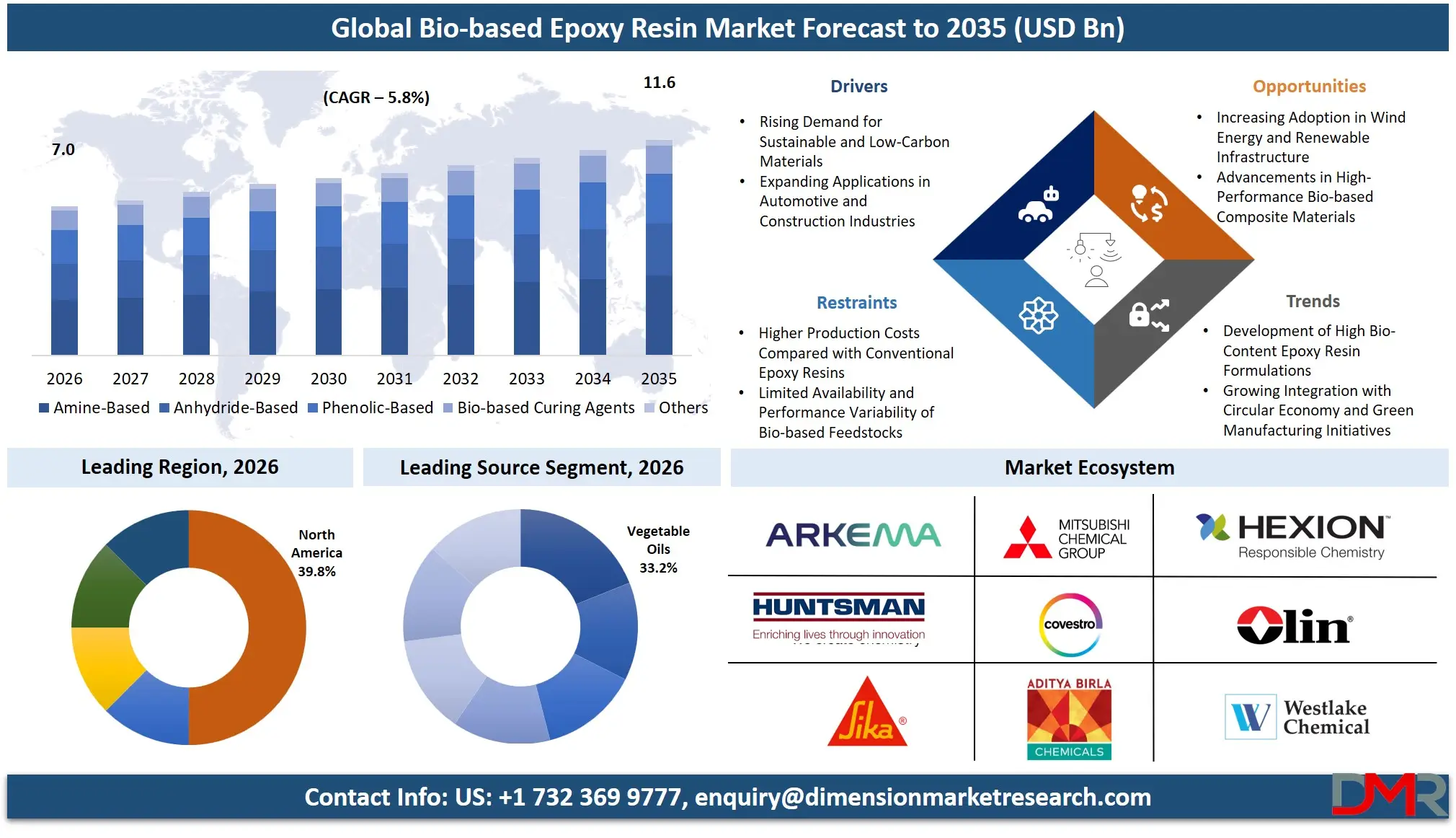

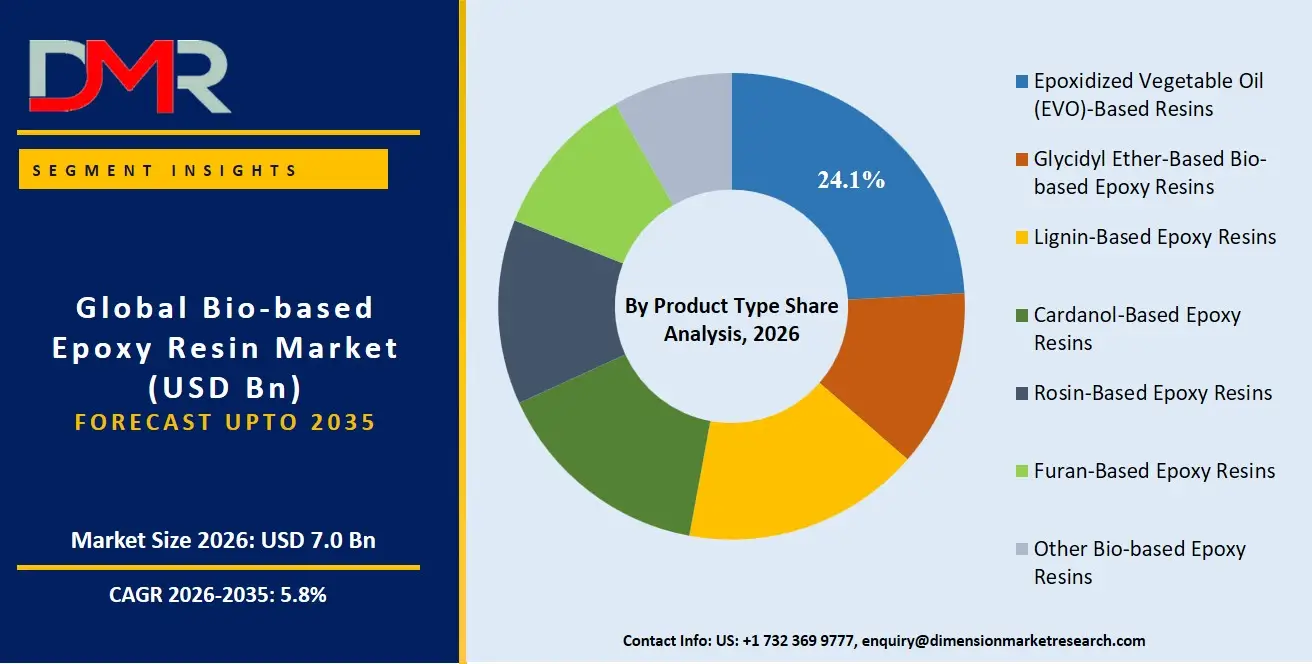

The Global Bio-based Epoxy Resin Market is expected to reach a value of USD 7.0 billion in 2026, and it is further anticipated to reach USD 11.6 billion by 2035, growing at a CAGR of 5.8% during the forecast period. The bio-based epoxy resin market has been growing at a steady rate as industries intensify their sustainability mandates and transition away from petroleum-derived, bisphenol A (BPA)-based epoxy thermosets.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market consists of resins formulated with renewable carbon content from sources like vegetable oils, lignin, cardanol, and rosin, which assist formulators in reducing carbon footprint and volatile organic compound (VOC) emissions. The increasing demand to achieve circular economy goals, lower toxicity profiles, and de-risk supply chains from petrochemical feedstock volatility is driving the necessity of these specialized green polymers. The coatings, adhesives, and composites sectors are the most frequent adopters, with epoxidized vegetable oil (EVO)-based resins remaining the most popular because of their processability and cost-to-performance balance. The building & construction, automotive, and electronics industries are key players as they need durable, thermally stable, and environmentally compliant material ecosystems.

The US Bio-based Epoxy Resin Market

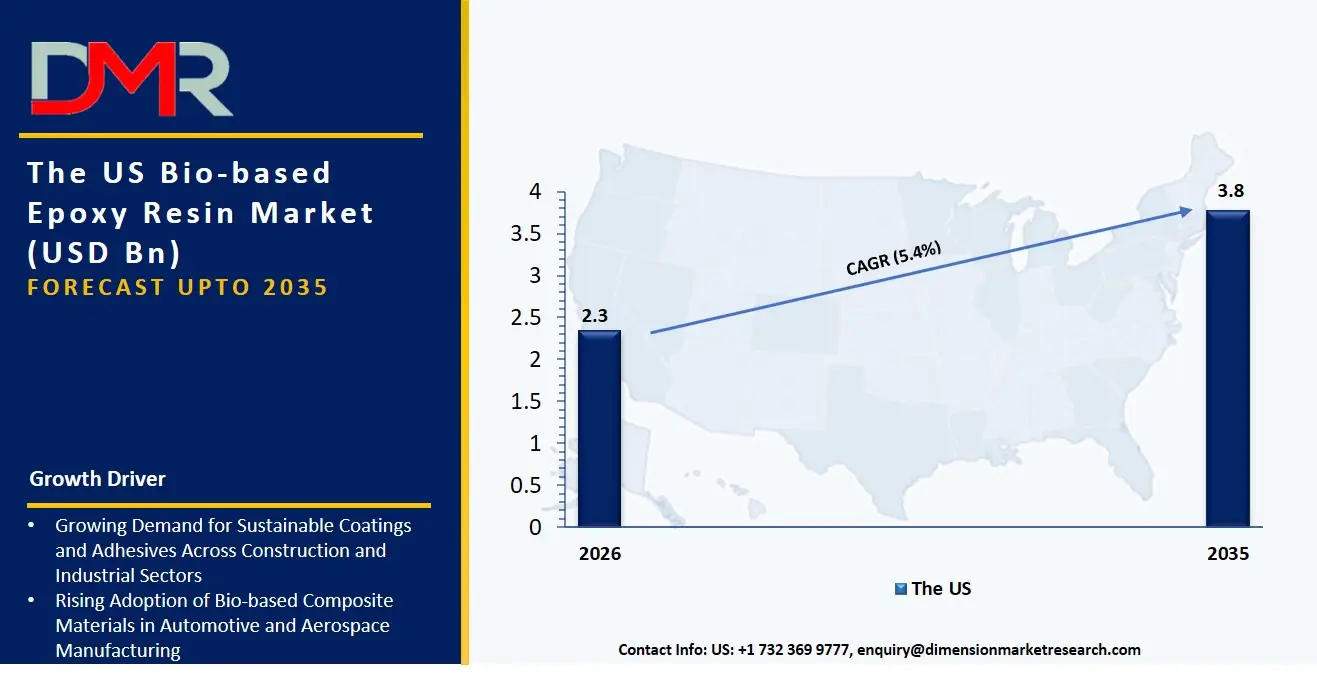

The US Bio-based Epoxy Resin Market is projected to reach USD 2.3 billion in 2026 at a compound annual growth rate of 5.4% over its forecast period, culminating in a value of USD 3.8 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US continues to be the largest and most mature market for bio-based epoxy resins due to the proactive sustainability goals of Fortune 500 material science companies and stringent Environmental Protection Agency (EPA) regulations on hazardous air pollutants. The market has been typified by high demand for epoxidized soybean oil (ESBO)-based resins, whereby domestic soybean abundance provides a cost-competitive, renewable building block to replace dioctyl phthalate plasticizers and conventional epoxy novolacs. Besides, the implementation of high-solids, low-VOC bio-based coatings in architectural and automotive refinish applications is producing a similar need in amine-based and anhydride-based curing agent systems to ensure rapid ambient curing and superior chemical resistance.

The Europe Bio-based Epoxy Resin Market

The Europe Bio-based Epoxy Resin Market is estimated to be valued at USD 2.0 billion in 2026 and is further anticipated to reach USD 3.2 billion by 2035 at a CAGR of 5.3%. The regulatory frameworks including REACH and the EU's Circular Economy Action Plan have a significant impact on the European market and drive the need to substitute Substances of Very High Concern (SVHC) like BPA with cardanol-based and lignin-based epoxy resins. Accelerated growth of natural fiber-reinforced composites is also being experienced in the region as automotive OEMs in Germany and France are trying to strike a balance between lightweight structural performance and end-of-life vehicle (ELV) recyclability. In addition, efforts in eco-labeling are challenging resin manufacturers to create dedicated bio-based powder coatings and floor coatings that provide verified bio-content and low indoor air emissions across European building ecosystems.

The Japan Bio-based Epoxy Resin Market

The Japan Bio-based Epoxy Resin Market is projected to be valued at USD 457.2 million in 2026 at a CAGR of 5.1%. The Japanese market is unique, with a corporate drive toward carbon neutrality in response to government mandates and highly engineered legacy material performance standards. Rosin-based epoxy resins and high-purity glycidyl ether-based bio-based epoxy resins make up a large part of the spending as electronics conglomerates qualify bio-based alternatives for printed circuit boards (PCBs) and encapsulation applications. There is also a strong need to integrate deeply in the local manufacturing ecosystem to bridge the performance gaps between traditional phenol novolac hardeners and novel bio-based curing agents derived from terpenes, which forms a niche in high-thermal reliability and dielectric property optimization.

Key Takeaways

- Market Size & Forecast: The Global Bio-based Epoxy Resin market is projected to reach USD 7.0 billion in 2026, expanding steadily to USD 11.6 billion by 2035, fueled by the dual drivers of net-zero carbon commitments and the mandatory replacement of bisphenol A (BPA) in food-contact and consumer goods applications.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 5.8%, driven by a critical shortage of high-purity bio-based epichlorohydrin and the escalating complexity of formulating thermosets with equivalent glass transition temperatures (Tg) and mechanical strength to their petrochemical counterparts.

- Primary Growth Drivers: Key forces include the widespread migration from petroleum-derived epichlorohydrin to plant-based alternatives, the need for life cycle assessment (LCA) consulting to validate environmental product declarations (EPDs), and the integration of bio-resins into existing composite manufacturing lines requiring tailored rheology and cure kinetics.

- Key Market Trends: Major trends include the rise of industry-specific bio-formulations (e.g., marine antifouling coatings, lightweight automotive structural adhesives), the use of AI-powered tools within resin synthesis to predict optimal fatty acid epoxidation pathways, and the shift toward bio-based content verification as corporate boards prioritize Scope 3 emission reductions.

- By Product Type Analysis: Epoxidized Vegetable Oil (EVO)-Based Resins, led by ESBO and ELO, are expected to dominate due to global agricultural commodity availability and established epoxidation chemistry. Professional material development is increasingly required to blend these with glycidyl ether-based resins to achieve the desired balance of crosslink density, hydrophobicity, and impact strength.

- By End User Analysis: Building & Construction and Automotive are the most lucrative verticals due to stringent VOC regulations and light-weighting needs. Electrical & Electronics is the fastest-growing sector as halogen-free, bio-based laminates require robust dielectric performance and flame-retardant synergy for PCB substrates.

- Regional Leadership: North America is poised to dominate this market with 39.8% of the market share in 2026 due to its well-developed agricultural feedstock infrastructure and advanced material science ecosystem that utilizes this bio-based supply chain to its fullest.

What is the Bio-based Epoxy Resin?

Bio-based Epoxy Resins are specialized thermosetting polymers formulated with renewable carbon feedstocks offered by resin manufacturers, formulators, and technology licensors to assist industries through the entire material substitution lifecycle. These materials, unlike conventional petroleum-based epoxy (the familiar two-part liquid systems), are related to the source of the carbon building blocks. This involves Epoxidized Vegetable Oils to provide plasticizing and reactive diluent functions, Glycidyl Ether-Based Bio-epoxies to replicate the performance of bisphenol A diglycidyl ether (BADGE), and Lignin-Based Epoxy Resins to impart rigidity and thermal stability from biomass waste streams. With 85% of global epoxy demand requiring BPA reduction or elimination pathways, bio-based resins are needed to achieve comparable adhesion, chemical resistance, and modulus, making green chemistry investments translate into tangible competitive differentiation, as opposed to just incremental sustainability marketing.

Use Cases

- Heavy-Duty Marine Coatings: Shipbuilders and dry-dock operators employ cardanol-based epoxy resins and phenalkamine curing agents to create high-solids, low-temperature cure anticorrosive coatings that bond to marginally prepared steel and provide long-term fouling and seawater immersion protection.

- Lightweight Automotive E-coat Substitutes: Automotive manufacturers use ESBO and ELO-based cationic resins in electrodeposition (e-coat) to replace lead-containing, high-VOC primers, enabling a lower bake temperature and improved edge coverage on lightweight alloys and composite body panels.

- Sustainable Printed Circuit Boards (PCBs): Electronics OEMs qualify lignin-based and furan-based epoxy laminates to produce halogen-free, high-Tg printed circuit boards, achieving UL 94 V-0 flame retardancy through inherent char-forming chemistry rather than toxic brominated additives.

- Natural Fiber Composite Automotive Interiors: Tier-1 automotive suppliers use bio-based epoxy resin systems with flax, hemp, or kenaf fiber preforms to compression-mold lightweight, impact-resistant interior door panels and trunk liners that reduce vehicle weight and improve acoustic damping.

How AI is Transforming the Bio-based Epoxy Resin Market?

AI is changing the bio-based epoxy resin landscape by accelerating the discovery of novel renewable monomers and optimizing thermoset performance. In product type innovation, AI-based molecular dynamics simulations have the potential to automatically predict the glass transition temperature, viscosity, and modulus of epoxidized vegetable oil blends with novel bio-based curing agents, greatly minimizing the number of physical synthesis trials and development timelines, and project risk. Meanwhile, AI-powered features in chemical informatics allow formulators to better design epoxy-amine networks by predicting stoichiometric ratios, gel times, and exothermic profiles, suggesting novel anhydride or phenolic hardener combinations to optimize manufacturing throughput and minimize cure cycle energy consumption.

Governance and material compliance projects are also revolving around AI. In the area of regulatory consulting, intelligent compliance-monitoring algorithms are used to continuously screen global chemical inventories to identify emerging restrictions on bio-phenol derivatives and keep formulations aligned with frameworks like TSCA and REACH. Moreover, generative AI assistants are complementing life cycle assessment (LCA) consulting by simulating cradle-to-gate carbon footprints of different bio-sourcing pathways (e.g., soybean oil vs. castor oil) to give stakeholders a visualization of environmental impact reductions before committing to agricultural supply chain investments.

Market Dynamics

Key Drivers in the Global Bio-based Epoxy Resin Market

Rising Demand for Sustainable and Low-Carbon Materials

Growing environmental awareness and stringent regulations aimed at reducing carbon emissions are driving demand for bio-based epoxy resins worldwide. Manufacturers across automotive, construction, electronics, and marine industries are increasingly replacing petroleum-based resins with renewable alternatives to achieve sustainability goals. Bio-based epoxy resins offer lower environmental impact while maintaining excellent mechanical strength, chemical resistance, and durability. Government incentives supporting bio-based chemicals, expanding circular economy initiatives, and corporate commitments toward carbon neutrality further accelerate market adoption. Continuous advancements in bio-based feedstocks and resin technologies are improving product performance, enabling broader commercialization across high-performance industrial applications and supporting long-term market growth globally.

Expanding Applications in Automotive and Construction Industries

Rapid growth in the automotive and construction sectors is significantly boosting demand for bio-based epoxy resins. Automakers increasingly utilize lightweight, sustainable materials to improve fuel efficiency and reduce vehicle emissions, while construction companies adopt environmentally friendly coatings, adhesives, flooring systems, and composites to meet green building standards. Bio-based epoxy resins provide superior adhesion, corrosion resistance, and mechanical performance suitable for demanding structural applications. Rising investments in infrastructure development, electric vehicles, and sustainable construction projects further strengthen market demand. Continuous innovation in resin formulations and manufacturing processes enables wider industrial acceptance and supports sustained expansion across multiple end-use sectors.

Restraints in the Global Bio-based Epoxy Resin Market

Higher Production Costs Compared with Conventional Epoxy Resins

Bio-based epoxy resins generally involve higher production costs due to expensive renewable feedstocks, complex processing technologies, and relatively limited manufacturing scale. Specialized extraction, purification, and chemical modification processes increase production expenses compared with conventional petroleum-derived epoxy resins. These higher costs often discourage adoption among price-sensitive industries, particularly where sustainability regulations are less stringent. Limited economies of scale and fluctuating agricultural feedstock prices further affect commercial competitiveness. Although technological advancements continue reducing manufacturing costs, price disparities remain a major challenge limiting broader industrial adoption, especially in cost-driven applications requiring large-volume resin consumption.

Limited Availability and Performance Variability of Bio-based Feedstocks

The performance and supply of bio-based epoxy resins depend heavily on renewable raw materials such as vegetable oils, lignin, and cardanol, whose availability can fluctuate due to seasonal agricultural production and climate conditions. Variations in feedstock composition may influence resin quality, curing behavior, and final product performance, creating challenges for manufacturers seeking consistent material properties. Supply chain disruptions and competition for agricultural resources may also increase raw material costs. While research continues improving feedstock standardization and processing efficiency, maintaining consistent quality and stable supply remains a significant restraint affecting wider commercialization.

Growth Opportunities in the Global Bio-based Epoxy Resin Market

Increasing Adoption in Wind Energy and Renewable Infrastructure

The global expansion of renewable energy projects presents significant growth opportunities for bio-based epoxy resins. Wind turbine manufacturers increasingly seek sustainable composite materials for blades and structural components without compromising mechanical performance. Bio-based epoxy resins provide excellent strength, durability, and fatigue resistance while supporting environmental sustainability objectives. Rising investments in offshore and onshore wind farms, government renewable energy targets, and decarbonization initiatives continue expanding demand. Continuous improvements in composite manufacturing technologies and bio-based resin formulations further enhance performance, positioning renewable energy infrastructure as an important long-term growth opportunity for the global market.

Advancements in High-Performance Bio-based Composite Materials

Continuous innovation in bio-based composite technologies is creating new commercial opportunities across aerospace, automotive, marine, and industrial manufacturing sectors. Researchers are developing advanced epoxy formulations with improved thermal stability, mechanical strength, impact resistance, and chemical durability to match or exceed conventional petroleum-based alternatives. Integration with natural fibers and carbon fiber composites further expands application potential in lightweight structural components. Growing investments in sustainable advanced materials, increased research collaborations, and expanding commercialization of high-performance bio-composites are expected to accelerate global demand while supporting broader industrial adoption over the coming years.

Trends in the Global Bio-based Epoxy Resin Market

Development of High Bio-Content Epoxy Resin Formulations

A key trend shaping the global bio-based epoxy resin market is the development of formulations with significantly higher renewable content while maintaining high mechanical and thermal performance. Manufacturers are utilizing lignin, cardanol, vegetable oils, and other renewable feedstocks to reduce reliance on fossil-based chemicals. Advances in polymer chemistry are improving curing efficiency, durability, and compatibility with existing manufacturing processes. These innovations help industries meet sustainability targets without sacrificing product quality. Increasing environmental regulations and customer preference for renewable materials continue encouraging commercialization of high bio-content epoxy resins across numerous industrial applications worldwide.

Growing Integration with Circular Economy and Green Manufacturing Initiatives

Bio-based epoxy resin manufacturers are increasingly aligning product development with circular economy principles by utilizing renewable resources, reducing production emissions, and improving recyclability. Companies are investing in sustainable manufacturing technologies, waste reduction strategies, and environmentally responsible supply chains to meet evolving regulatory and customer requirements. Green certification programs and lifecycle assessment practices are becoming more important in product development and procurement decisions. Collaboration among chemical producers, research institutions, and end-use industries continues accelerating innovation. This strong industry-wide focus on sustainability is reinforcing bio-based epoxy resins as a preferred material for future high-performance industrial applications.

Research Scope and Analysis

The Global Bio-based Epoxy Resin Market is segmented by product type, source, curing agent, application, and end user. It covers epoxidized vegetable oil and other bio-based resin types, renewable feedstocks, diverse curing technologies, applications spanning coatings, adhesives, composites, electronics, construction, automotive, aerospace, and marine, while analyzing demand across major industrial end-use sectors worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Type Analysis

Epoxidized Vegetable Oil (EVO)-based resins is projected to dominate the global bio-based epoxy resin market due to their high bio-based content, commercial availability, cost-effectiveness, and broad industrial acceptance. Epoxidized soybean oil (ESBO) is the leading product because of abundant soybean production and established processing infrastructure. These resins offer excellent flexibility, chemical resistance, and compatibility with conventional epoxy formulations, making them suitable for coatings, adhesives, composites, and plasticizers. Increasing environmental regulations encouraging renewable raw materials and reduced dependence on petroleum-derived chemicals further strengthen demand. Continuous product innovation and expanding applications in automotive, construction, and consumer products continue reinforcing EVO-based resins as the largest product category worldwide.

By Source Analysis

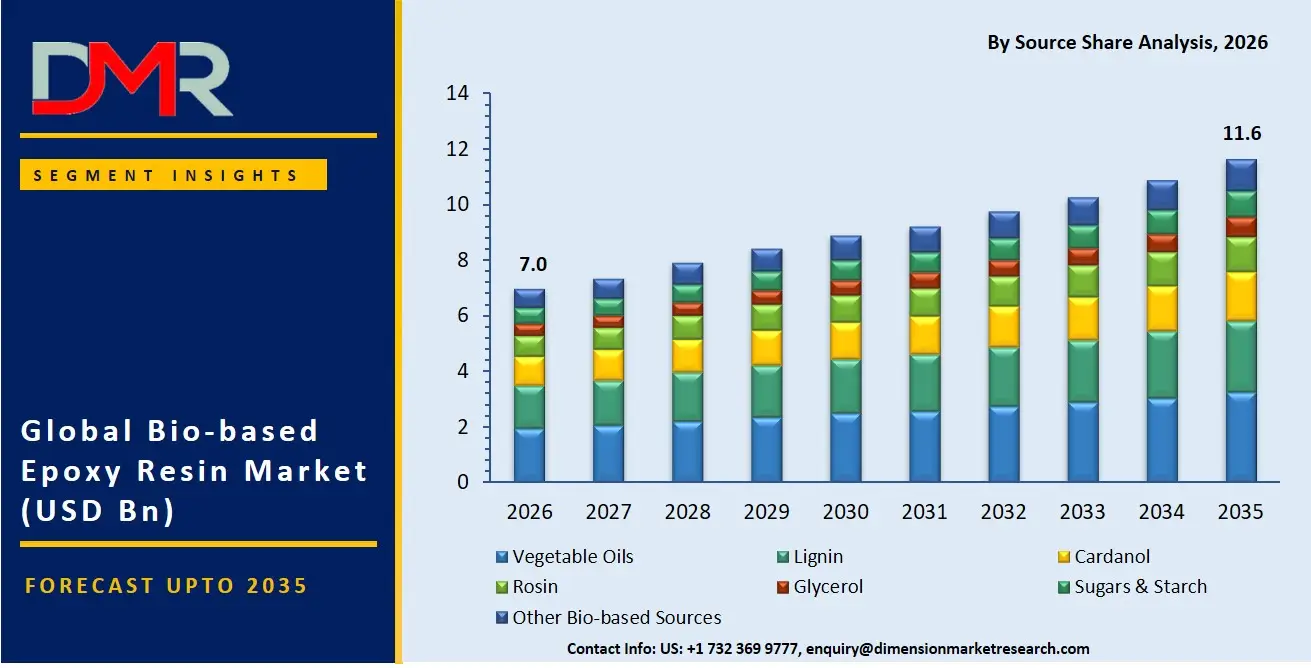

Vegetable oils is expected to represent the dominant source segment owing to their renewable availability, affordability, and well-developed global supply chains. Soybean, linseed, castor, sunflower, and other vegetable oils provide sustainable feedstocks for manufacturing high-performance bio-based epoxy resins.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

These oils possess favorable chemical structures that enable efficient epoxidation while delivering excellent mechanical and chemical properties. Strong agricultural production, particularly in North America, Europe, and Asia-Pacific, ensures consistent raw material availability. Increasing government support for bio-based chemicals, rising sustainability initiatives, and continuous improvements in vegetable oil processing technologies have further expanded their industrial utilization, making vegetable oils the primary feedstock across global bio-based epoxy resin production.

By Curing Agent Analysis

Amine-based curing agents is poised to dominate the market because they provide superior curing efficiency, excellent adhesion, high mechanical strength, and outstanding chemical resistance across numerous industrial applications. They are widely compatible with bio-based epoxy formulations and offer reliable performance under varying environmental conditions. Manufacturers prefer amine curing systems for coatings, adhesives, composites, electrical insulation, and construction materials due to their proven commercial performance and relatively simple processing. Ongoing development of low-emission and partially bio-based amine curing technologies further supports market expansion. Their versatility, established industrial acceptance, and ability to meet demanding application requirements continue maintaining their leading position in the global market.

By Application Analysis

Coatings is poised to constitute the largest application segment because bio-based epoxy resins deliver exceptional corrosion resistance, durability, adhesion, and chemical protection for industrial and commercial surfaces. They are extensively used in automotive, marine, construction, infrastructure, and protective coating applications where environmental compliance and long service life are critical. Increasing demand for low-VOC and sustainable coating solutions has accelerated the replacement of conventional petroleum-based systems. Continuous investments in green building projects, industrial maintenance, and infrastructure development further stimulate demand. Technological advancements improving coating performance while increasing renewable content continue strengthening coatings as the dominant application segment globally.

By End User Analysis

Building and construction is projected to dominate the end-user segment owing to extensive consumption of bio-based epoxy resins in protective coatings, flooring systems, structural adhesives, repair materials, sealants, and composite construction products. Rising global infrastructure investments, sustainable building initiatives, and stricter environmental regulations encourage the adoption of renewable materials with lower carbon footprints. Bio-based epoxy resins provide excellent durability, mechanical strength, moisture resistance, and long-term structural performance, making them suitable for demanding construction environments. Increasing renovation activities, green certification programs, and demand for environmentally friendly construction materials continue driving widespread adoption, securing the building and construction sector's leading market position.

The Global Bio-based Epoxy Resin Market Report is segmented on the basis of the following:

By Product Type

- Epoxidized Vegetable Oil (EVO)-Based Resins

- Epoxidized Soybean Oil (ESBO)

- Epoxidized Linseed Oil (ELO)

- Epoxidized Castor Oil (ECO)

- Other Vegetable Oil-Based Resins

- Glycidyl Ether-Based Bio-based Epoxy Resins

- Lignin-Based Epoxy Resins

- Cardanol-Based Epoxy Resins

- Rosin-Based Epoxy Resins

- Furan-Based Epoxy Resins

- Other Bio-based Epoxy Resins

By Source

- Vegetable Oils

- Lignin

- Cardanol

- Rosin

- Glycerol

- Sugars & Starch

- Other Bio-based Sources

By Curing Agent

- Amine-Based

- Anhydride-Based

- Phenolic-Based

- Bio-based Curing Agents

- Others

By Application

- Coatings

- Industrial Coatings

- Protective Coatings

- Marine Coatings

- Automotive Coatings

- Architectural Coatings

- Powder Coatings

- Floor Coatings

- Adhesives & Sealants

- Structural Adhesives

- Construction Adhesives

- Industrial Sealants

- Composites

- Fiber-Reinforced Composites

- Natural Fiber Composites

- Carbon Fiber Composites

- Electrical & Electronics

- Printed Circuit Boards (PCBs)

- Encapsulation & Potting Compounds

- Electrical Insulation

- Wind Energy Components

- Wind Turbine Blades

- Nacelle Components

- Construction Materials

- Concrete Repair Systems

- Flooring Systems

- Structural Grouts

- Automotive Components

- Interior Components

- Exterior Components

- Lightweight Structural Parts

- Aerospace Components

- Structural Composites

- Interior Components

- Adhesive Bonding Systems

- Marine Applications

- Boat Hulls

- Deck Coatings

- Corrosion Protection Systems

- 3D Printing

- Functional Prototypes

- End-Use Parts

- Others

By End User

- Building & Construction

- Automotive

- Aerospace & Defense

- Electrical & Electronics

- Marine

- Energy & Power

- Consumer Goods

- Industrial Manufacturing

- Packaging

- Others

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

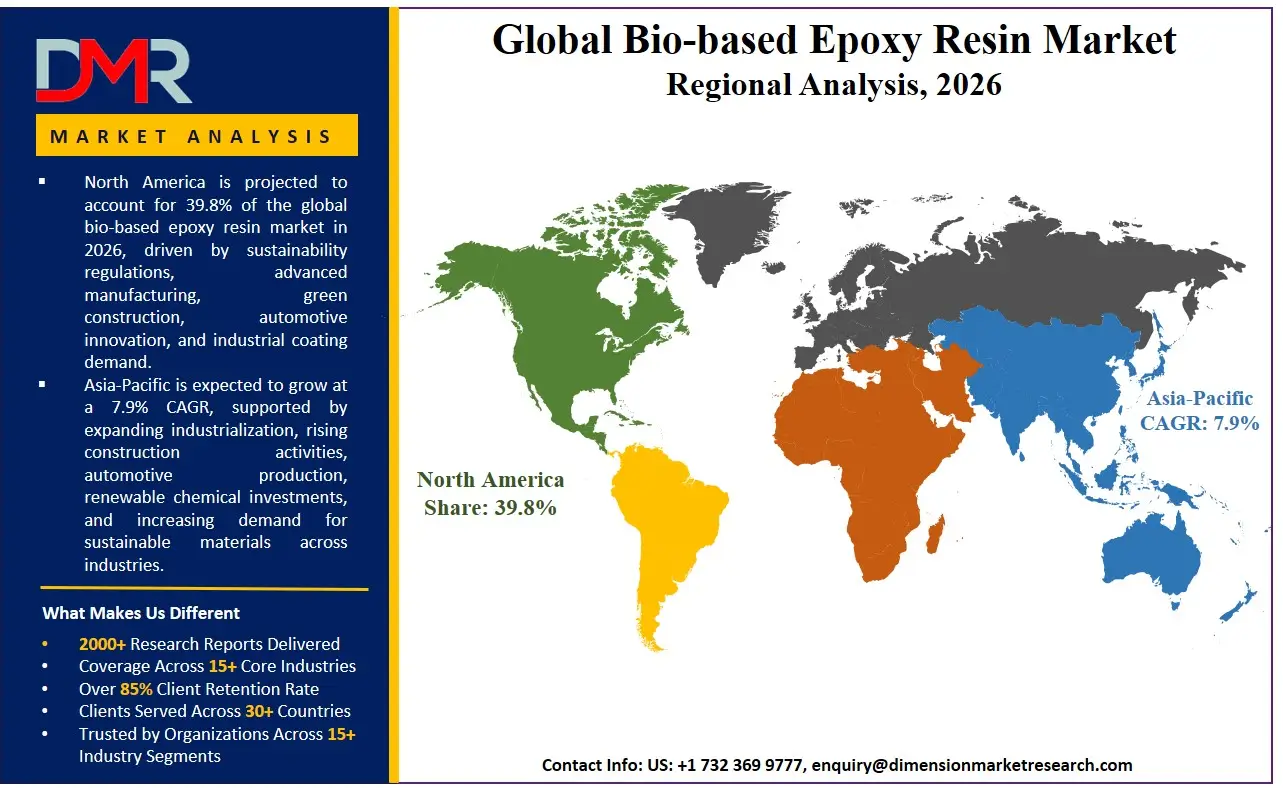

North America is poised to dominate the global bio-based epoxy resin market as it is projected to hold 39.8% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the bio-based epoxy resin market because of the unmatched concentration of soybean farming, integrated biorefinery assets, and the aggressive sustainability procurement mandates of the Fortune 500 building and automotive material specifiers. The area has an established ecosystem of global resin manufacturers, specialty chemical formulators, and a rich pool of material science talent and application development engineers. Enterprise investment in LEED-certified buildings, electric vehicle light-weighting, and the overall retirement of BPA-based can and coil coatings contribute to the continued demand for ESBO and cardanol-based epoxy resins along with high-performance bio-amine curing agents. Moreover, an optimistic green chemistry venture capital climate persistently finances upcoming bio-resin start-ups that need strategic partnerships to achieve expedited scale-up and regulatory clearance for food-contact and sensitive application indirect exposure.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding bio-based epoxy resin market, driven by the government-led sweeping green manufacturing initiatives in China, India, Japan, and Southeast Asia. The fast-paced industrialization, the rise of a middle-income population, and the dynamic expansion of electronics and construction sectors are compelling regional conglomerates and state-owned enterprises to discard hazardous BPA and VOC-emitting material inventories. Technology licensing and co-development partnerships are in high demand to help these large organizations head in the direction of indigenous, bio-based thermoset production. There is also a severe lack of qualified polymer formulation talent in the region, and it is necessary to outsource application testing, pilot-scale trial management, and curing agent optimization to cover the technical skills gap and enable faster material qualification cycles.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global bio-based epoxy resin market has become highly dynamic with a heterogeneous array of multinational petrochemical giants diversifying into renewables, specialty bio-polymer start-ups with proprietary monomer technology, and agricultural processors forward-integrating into chemicals. The key to success will be profound strategic feedstock alliances with integrated soybean crushers, cashew nut shell liquid (CNSL) processors, or kraft lignin producers because they will open the necessary cost-advantaged raw material positions and early access to new high-purity bio-refinery streams. The movement towards market consolidation is rapidly progressing with the traditional petrochemical epoxy producers acquiring novel glycidylation and epoxidation technology patents from university spin-offs to stay afloat. Proprietary intellectual property, including novel enzymatic epoxidation methods and bio-based epoxy-amine adduct dispersion technology, is becoming a more important basis of competitive differentiation than just generic sourcing of commodity ESBO or trading bio-content percentage certifications.

Some of the prominent players in the Global Bio-based Epoxy Resin Market are:

- Olin Corporation

- Hexion Inc.

- Westlake Corporation

- Covestro AG

- Arkema S.A.

- BASF SE

- Sika AG

- Huntsman Corporation

- Aditya Birla Chemicals

- Atul Ltd.

- Nagase & Co., Ltd.

- Mitsubishi Chemical Group Corporation

- SABIC

- Cardolite Corporation

- EcoPoxy Inc.

- Entropy Resins, Inc.

- Sicomin Epoxy Systems

- Bitrez Ltd.

- Greenpoxy

- Resoltech

- Other Key Players

Recent Developments

- September 2025: Huntsman Corporation launched a new range of ARALDITE® epoxy adhesives designed to be safer and more sustainable, including BPA-free and non-CMR formulations for industrial bonding, composites, and electronics applications.

- February 2025: Entropy Resins, Inc. introduced BIOinfusion™, a high bio-content epoxy infusion resin developed for composite manufacturing in marine, automotive, aerospace, sporting goods, and industrial applications, offering improved processing efficiency and mechanical performance.

- November 2025: Huntsman Corporation highlighted continued innovation in sustainable polymer technologies and advanced material solutions during its third-quarter 2025 results, reinforcing its strategic focus on high-performance epoxy systems and specialty materials.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 7.0 Bn |

| Forecast Value (2035) |

USD 11.6 Bn |

| CAGR (2026–2035) |

5.8% |

| The US Market Size (2026) |

USD 2.3 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product Type, By Source, By Curing Agent, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Bio-based Epoxy Resin Market?

▾ The Global Bio-based Epoxy Resin market is poised to be valued at USD 7.0 billion in 2026 and is projected to reach USD 11.6 billion by 2035, driven by the universal need for BPA-free, low-VOC materials in protective coatings, lightweight composites, and electronic encapsulation.

What is the CAGR of the Global Bio-based Epoxy Resin Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 5.8% from 2026 to 2035, reflecting the accelerating complexity of replacing petroleum-derived epoxy monomers and the persistent innovation in bio-based curing agent stoichiometry and network morphology.

What factors are driving the growth of the Global Bio-based Epoxy Resin Market?

▾ Key drivers include the global mandate to eliminate Bisphenol A (BPA) from consumer and industrial goods, the imperative to reduce Scope 3 carbon emissions through renewable feedstocks, the performance convergence of EVO-based systems with petrochemical benchmarks, and the surge in demand for sustainable marine and protective coatings amid evolving eco-label regulations.

Which region held the largest share of the Bio-based Epoxy Resin Market in 2026?

▾ North America is poised to hold a 39.8% market share in 2026, driven by a mature agricultural feedstock ecosystem and aggressive enterprise investment in ESBO-based plasticizers, lignin-based construction materials, and bio-composite automotive components.

Which region is expected to grow the fastest in the Bio-based Epoxy Resin Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid green manufacturing transformation in China, India, and Japan, where cardanol-based and furan-based epoxy resins are critical for transitioning large electronics and construction conglomerates to halogen-free, bio-based material platforms.

What are the major trends in the Global Bio-based Epoxy Resin Market?

▾ Major trends include the integration of AI-driven molecular design into bio-resin development workflows, the rise of non-leachable ESBO plasticizers and GreenOps consulting, the demand for application-specific bio-formulations, and the focus on UV-stable lignin-based powder coatings for exterior architectural durability.

Who are the key players in the Global Bio-based Epoxy Resin Market?

▾ Key players include integrated material science companies like Huntsman and Olin, bio-specialty leaders like Cardolite and Nagase ChemteX, and purpose-driven green chemistry disruptors like Entropy Resins and EcoPoxy, alongside forward-integrating agricultural processors.

How is the Global Bio-based Epoxy Resin Market segmented?

▾ The market is segmented by Product Type, Source, Curing Agent, Application, and End User.