What is the Biodegradable Polymers Market Size?

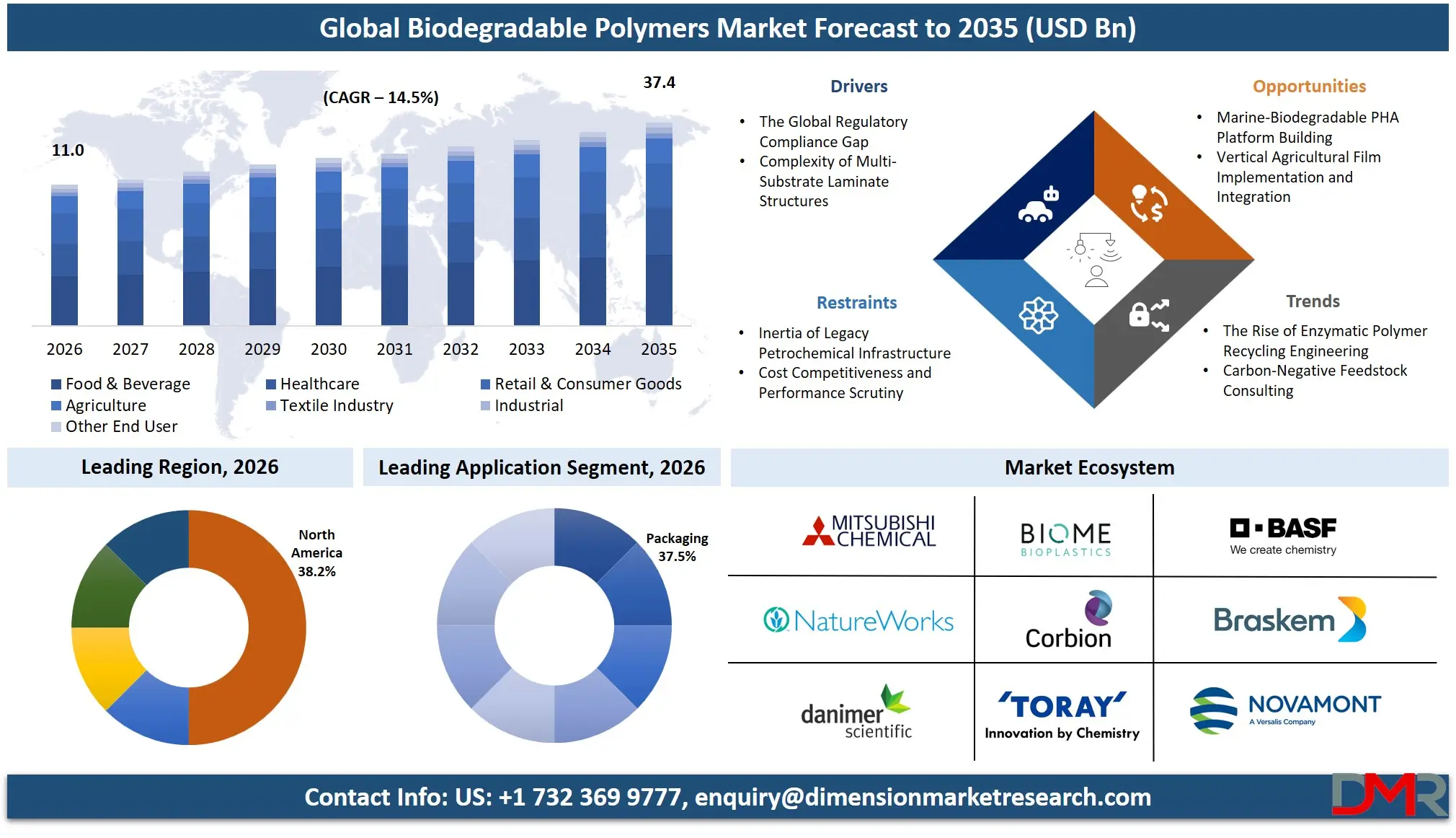

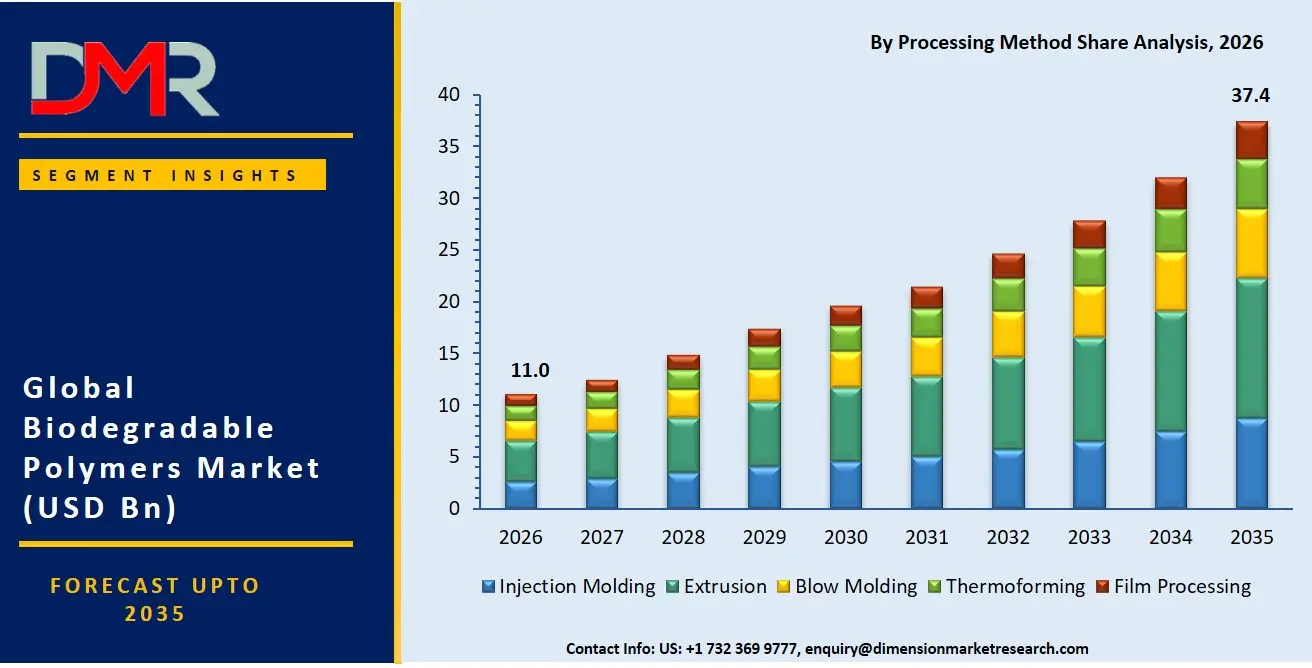

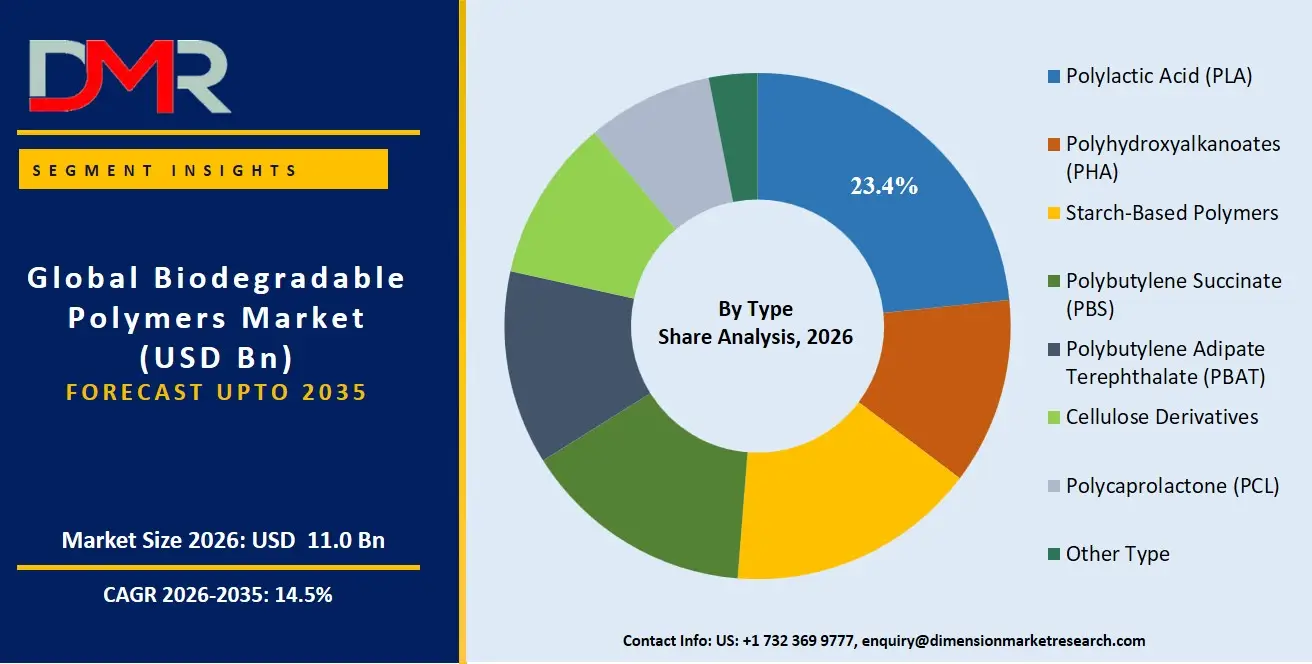

The Global Biodegradable Polymers Market is expected to reach a value of USD 11.0 billion in 2026, and it is further anticipated to reach USD 37.4 billion by 2035, growing at a CAGR of 14.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The biodegradable polymers market has been expanding rapidly as enterprises and consumers have accelerated the process of transitioning toward sustainability and stop using legacy petrochemical-based plastics and use bio-based, compostable ones. The market can be segmented into PLA, PHA, starch-based polymers, PBS, PBAT, and cellulose derivatives, which help industries implement circular economy principles in their packaging, agriculture, and consumer goods.

Reducing waste from packaging, single-use plastic elimination policies and industrial composting facilities are creating a growing need for innovative material science solutions. Packaging is the most common use, with the still most popular polymers being made from PLA and starch due to their processability and cost efficiency. The food & beverage, healthcare, and retail & consumer goods industries are key players as they need food-contact safe, biocompatible, and end-of-life compostable material ecosystems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Biodegradable Polymers Market

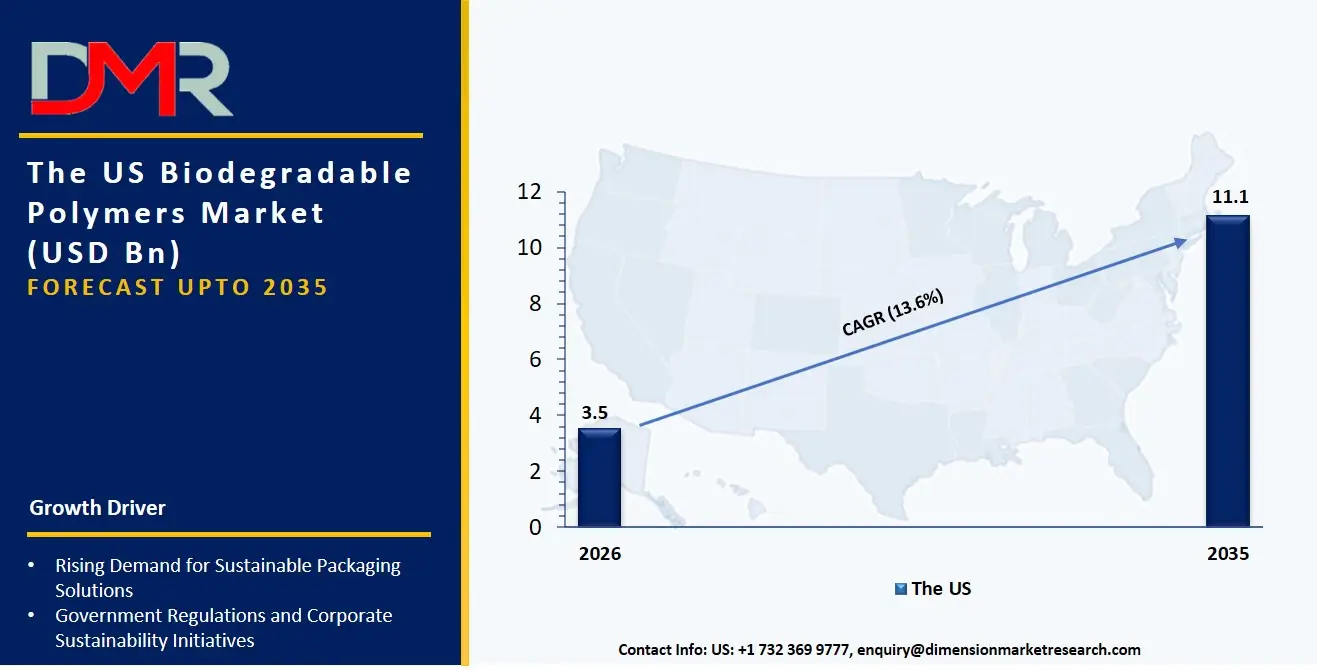

The US Biodegradable Polymers Market is projected to reach USD 3.5 billion in 2026 at a compound annual growth rate of 13.6% over its forecast period, culminating in a value of USD 11.1 billion by 2035.

The US continues to be the largest and most developed market in biodegradable polymers due to the active sustainable packaging commitments of Fortune 500 companies and the growing patchwork of state-level single-use plastic bans. The market has been typified by high demand for film processing services, whereby organizations are aimed at converting rigid packaging formats into flexible, compostable structures. In addition, advanced composting infrastructure is creating a parallel demand for PHA and PBS grades to mandate end-of-life performance and biodegrability ethics in various disposal media.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Biodegradable Polymers Market

The Europe Biodegradable Polymers Market is estimated to be valued at USD 3.2 billion in 2026 and is further anticipated to reach USD 10.4 billion by 2035 at a CAGR of 14.0%. The regulatory frameworks including the EU single-use plastics directive and the upcoming packaging and packaging waste regulation (PPWR) have a significant impact on the european market and drive the need to employ home-compostable and industrially compostable polymer solutions. Accelerated growth of extrusion-based processing is also being experienced in the region as the agriculture and horticulture sector in Italy and France is trying to strike a balance in soil health with biodegradable mulch films. Moreover, concepts like the circular bio-economy strategies are putting pressure on the material suppliers to develop specific bio-based PBAT and cellulose derivatives that will supply specific disintegration profiles and interoperability in European organized organic waste collection systems.

The Japan Biodegradable Polymers Market

The Japan Biodegradable Polymers Market is projected to be valued at USD 450.3 million in 2026. It is further expected to witness robust growth, a CAGR of 13.3%. The Japanese market is more distinctive, as companies are pushing to achieve a circular economy due to rigorous waste management laws and dwindling landfill sites. Cellulose derivatives and injection molding applications make up a large part of the spending as large conglomerates migrate cosmetic and consumer electronics packaging off petroleum-based plastics to bio-based alternatives. Another marketable niche is in-depth penetration into the local market to fill the gap between the legacy polymer conversion equipment and new bio-polyester grades for thermoforming and film processing of PLA and PBS blends.

Key Takeaways

- Market Size & Forecast: The Global Biodegradable Polymers market is projected to reach USD 11.0 billion in 2026, expanding dramatically to USD 37.4 billion by 2035, backed by the global plastic pollution treaties and the necessary pace of packaging modernization for sustainability standards.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 14.5%, due to an urgent need for material alternatives that are not fossil fuel-based and as a result of the growing complexity of end-of-life biodegradation and certification requirements.

- Primary Growth Drivers: Key drivers are the broad transition from traditional single-use plastics to compostable packaging models, material consulting to prevent accusations of greenwashing, and bio-refinery pipelines that require specialized production scale-up for PLA and PHA.

- Key Market Trends: Key Market Trends include the growing availability of application-specific grades of polymer, the rise of AI-driven tools for extrusion and injection molding to automatically correct rheological issues, and the shift towards certified home-compostable cellulose derivatives, as consumers seek to use the composting system in their own backyards.

- By Application Analysis: Packaging is forecast to be the dominate this segment as material demand as food safety and regulatory requirements drive growth. Seamless laminate structures are increasingly being demanded that join paper-based substrates with high barrier bio-polyester coatings, and biodegradable polymers are playing an important role in the construction of these structures.

- By End-Use Industry Analysis: Food & Beverage and Healthcare are projected to dominate this segment owing to the strict compliance and biocompatibility requirements of food. The fastest-growing sector is agriculture where strong soil-degradable starch-based and PBAT architectures are necessary due to the use of controlled-release mulch films.

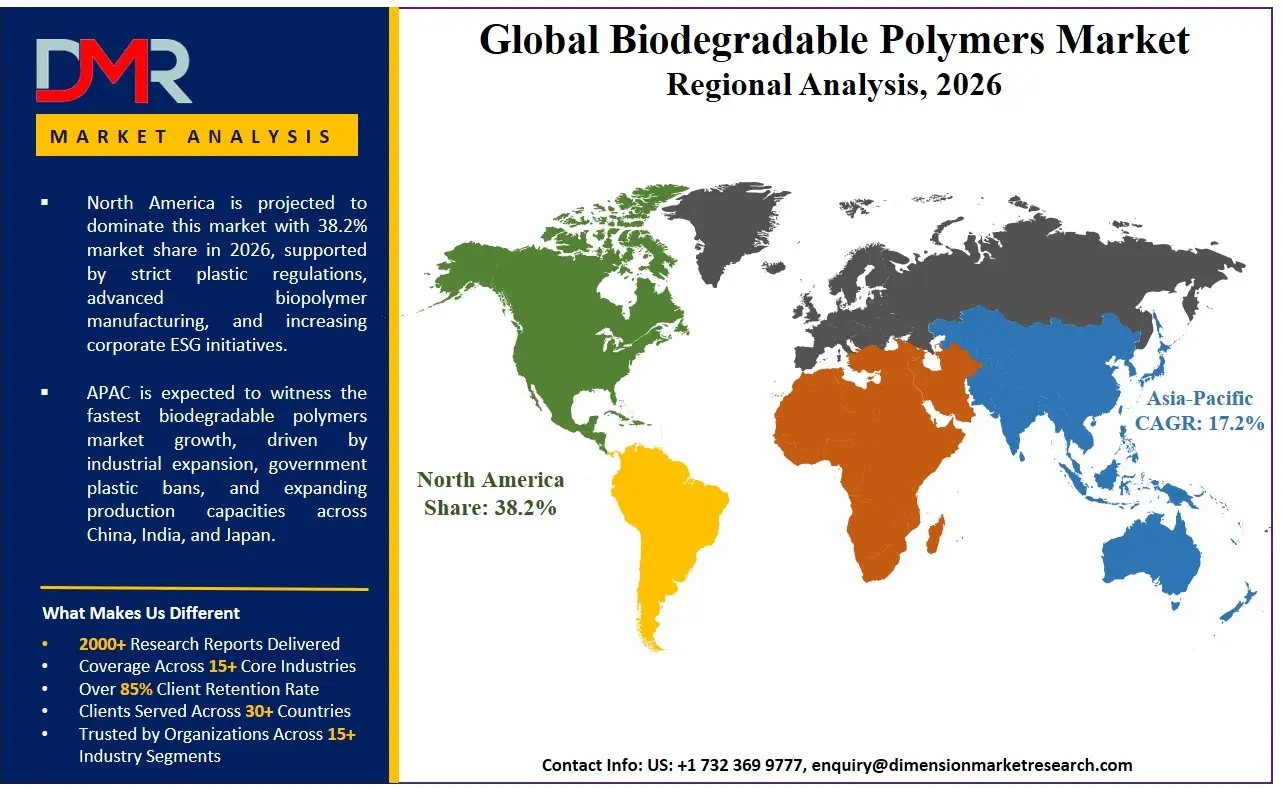

- Regional Leadership: North America is poised to dominate this market with 38.2% of the market share in 2026 due to its well-developed bio-economy infrastructure that utilizes this industrial base to its fullest and makes it a leader in this market.

What is the Biodegradable Polymers?

Biodegradable Polymers are the polymeric materials which are offered by third party compounders, resin producers, and material integrators, that help organizations switch to plastics which are not persistent. These materials, unlike conventional plastic consumption (the commodity polymer itself) are related to the end-of-life of material use. These include PLA to achieve low carbon footprint; rigid packaging roadmap; PHA, PBAT and flexible films physically decomposed without ecotoxicity; PBS and polymers based on starch are developed to be able to integrate the disposable items into microbial digestion environments. With over 90% of organizations running sustainability-targeted packaging programs, biodegradable polymers are needed to achieve waste reduction, carbon neutrality, and material circularity, making plastic investments translate into tangible environmental responsibility, as opposed to linear landfill accumulation.

Use Cases

- Rigid Food Packaging Modernization in Food & Beverage: Food brands are seeking PLA and thermoforming conversion services for redesigning their rigid PET containers into clear, compostable clamshells using high purity lactides, with real-time shelf-life extension and compatibility with organic waste streams.

- Compostable Device Readiness in Healthcare: Hospital networks incorporate services such as PHA and injection molding to convert single-use surgical devices to a medical-grade biodegradable polymer that is safe for composting and prepare the hospital waste estate for diversion from incineration to industrial composting.

- Soil-Biodegradable Navigation in Agriculture: In Agriculture, Government agricultural bodies employ PBAT extrusion services to release mulch films that meet strict soil ecotoxicity regulations, ensuring that no microplastic will build up in the farmland, but with the use of scalable in-soil biodegradation.

- Cellulose Textile Fiber Integration: The global textile sector employs cellulose derivatives and fiber spinning methods to combine nature-based fibers with synthetic biodegradable coating systems, and delivers durable clothing that is completely biodegradable in marine settings.

How AI is Transforming the Biodegradable Polymers Market?

Plastic manufacturing companies are implementing PLA based thermoforming conversion services to replace traditional PET rigid packaging with transparent, compostable clamshell packaging, offering better shelf-life performance and then incorporating the packaging into organic waste management systems. In healthcare, hospital networks are moving towards PHA based injection-molded single-use surgical devices, which are composed of a range of biocompatible biodegradable polymers, with the result that healthcare waste streams can be diverted from incineration to an industrial composting infrastructure. In the field of agriculture, government bodies and agriculture institutions are implementing PBAT based extrusion technology for soil-biodegradable mulch films that meet the strict soil ecotoxicity regulations and do not cause a long-term build-up of micro-plastics in soil, while allowing for a scalable degradation in soil. In the meantime, the textile industry is combining cellulose derivatives, as well as advanced fiber spinning techniques and biodegradable coating systems to create durable garments that are able to perform their intended function during use and fully biodegradable at the end of use, even in marine settings.

Market Dynamics

Key Drivers in the Global Biodegradable Polymers Market

The Global Regulatory Compliance Gap

Global organisations are struggling to find material formulations with updated knowledge of the changing compostable packaging regulations such as the PPWR, certain state-specific plastic bans and the EPR. The compliant polymers are in demand at a faster pace than the number of certified grades available, which has led to a structural shortage in the supply market. This is driving an increasing number of firms to shift specialty compounders and material science experts to their outsourcing partners, rather than relying on internal polymer synthesis. These companies help with critical steps such as application-specific grading, certification testing and sourcing sustainable feedstocks. Outsourcing such functions allows organizations to speed up sustainable packaging transformation initiatives and minimize the chances of delays due to insufficient in-house material science knowledge.

Complexity of Multi-Substrate Laminate Structures

Enterprises of significant size are also likely to have multiple types of packaging, most notably rigid packaging, pouches and films, to provide functional barrier performance. However, handling a portfolio of multi-substrate biodegradable packaging materials is extremely complex. Multiple material interfaces with different polymer chemistries and standards must be coordinated in terms of mechanical strength, moisture vapor transmission, oxygen barriers and end-of-life disintegration. Without the help of material scientists, this complexity can lead to suboptimal performance, shelf-life issues, and compliance violations. Consequently, there is an increasing demand for special blending and multi-layer extrusion services to help enterprises function in such environments.

Restraints in the Global Biodegradable Polymers Market

Inertia of Legacy Petrochemical Infrastructure

Most polymer producers still run on petrochemical synthesis systems that were developed over a long history, and have become highly optimized for specific olefin-based production. These legacy cracking and polymerization assets are a significant obstacle to change, despite biodegradable polymers potentially delivering more environmental compliance. Re-tooling large polymerization reactors, complex downstream extrusion lines and highly integrated feedstock supply chains can be expensive and risk prone for bio-based monomers. Material changes that require cross over multiple product grades require a significant amount of planning, purification, and certifications. The organizations worry about production disruption, off-spec material and stranded capital costs during the transition. As a result, petrochemical debt is limiting the uptake of biodegradable polymers and often gets in the way of more significant sustainability transformation projects.

Cost Competitiveness and Performance Scrutiny

The volatile fossil fuels market and the less predictable yields from bio-feedstocks have made it more difficult for organisations to invest in sustainable options that are more expensive. Although biodegradability will remain a key criterion, procurement executives are under pressure to prove every dollar added and prove measurable cost-neutral performance. Bio-polyesters, such as PHA and PCL, will be more likely to be under closer scrutiny because of their higher capital costs and the longer certification time. Short, drop-in compatible applications, such as PLA blends for fruit packaging, which yield fast environmental claims or cost-level with legacy logistics, have been adopted by businesses. Long-term high performance and durability application initiatives are more likely to be postponed until near-term equivalence with conventional plastic durability is proven. This change is compelling the polymer compounders to be more cost-driven and performance-oriented.

Growth Opportunities in the Global Biodegradable Polymers Market

Marine-Biodegradable PHA Platform Building

Another big opportunity in the biodegradable polymers market will be helping organizations to engineer safe environments for the oceans using PHA. Many companies have experimented with using PLA for packaging, but they would like their own custom PHA platforms that fit their own end-of-life situations, marine biodegradation needs, and organic recycling processes. Bacterial fermentation, co-polymer blending, and scale-up downstream processing are specialized skills required for the development of these technologically complex biopolymer settings. Material suppliers can support brands to create buildable, custom PHA ecosystems to help flexible packaging, consumer good and single use food serviceware. The region could develop high demand for very specialized compounding and application development services.

Vertical Agricultural Film Implementation and Integration

As agricultural organisations develop region-specific soil conditions, the requirement to combine material science skills and know-how with the knowledge of specific farming practices is fueling the development of customised polymer solutions. These include planting tubes made of starch, soil-biodegradable PBAT mulch films, and PCL controlled release matrices. Farmers and farm managers in the agriculture and horticulture industries must follow strict soil health standards and local climate requirements. For this reason, they need implementation partners who understand the polymer chemistry and agricultural compliance frameworks. To provide added value, it is recommended that material suppliers develop customized PBAT compositions in conjunction with cultivation systems, according to the requirements of organic farming, and develop in-soil disintegration rates.

Trends in the Global Biodegradable Polymers Market

The Rise of Enzymatic Polymer Recycling Engineering

Platform engineering for biodegradation is being widely used in material science as a substitute for conventional and passive composting environment. Enterprises are developing masterbatches with enzymes and/or triggers that provide a self-destructing packaging profile to brands instead of relying on the unpredictable microbial environment to do it. On these platforms, polymer chain scission can be precisely controlled and biomass can be supplied to the soil that is ready to be used as a soil amendment. In response to this, the suppliers of biodegradable polymers are offering the knowledge of enzyme-polymer compatibility, designing industrial composting systems, and developing triggered reaction kinetics.

Carbon-Negative Feedstock Consulting

The issue of sustainability in carbon accounting is also becoming important in the polymer field, where companies are facing pressure to reach 'net-zero' goals and reduce scope 3 emissions. Today, bio-polymer strategies are of interest for businesses because they can potentially increase biodegradability and reduce end-of-life CH4, and sequester carbon during the bio-polymer growth phase. This has brought about the need to have carbon-farming and sustainable feedstock consulting services. Material providers support organizations in optimizing land use, optimizing the molecular-weight of the materials, providing algae-based PHA, and scope 3 reduction by sequestering carbon from biogenic cycles.

Research Scope and Analysis

The biodegradable polymers market is witnessing strong growth driven by rising demand for sustainable packaging, increasing adoption of PLA materials, expanding extrusion processing applications, and growing usage across the food & beverage industry amid stricter environmental regulations worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Type Analysis

Polylactic Acid (PLA) is poised to dominate the type segment due to its strong commercial availability, compostability, and wide adoption across packaging, textiles, and food service applications. PLA is extensively derived from renewable resources such as corn starch and sugarcane, making it highly attractive for manufacturers seeking sustainable material alternatives. Its compatibility with existing plastic processing technologies, including injection molding and film extrusion, further supports large-scale industrial usage. Growing regulatory pressure against petroleum-based plastics in North America and Europe has accelerated PLA demand in consumer packaging and disposable products.

By Processing Method Analysis

Extrusion are anticipated to dominate the processing method segment because it is the most widely used and cost-efficient manufacturing technique for biodegradable polymer products. The method supports high-volume production of films, sheets, coatings, pipes, and packaging materials, making it essential for commercial-scale applications. Rising demand for biodegradable flexible packaging, agricultural mulch films, and compostable carry bags has significantly increased extrusion usage worldwide. The process offers operational efficiency, reduced material wastage, and compatibility with various biodegradable polymers such as PLA, PBAT, and starch blends. Manufacturers also prefer extrusion because it enables continuous processing with lower production costs and consistent product quality.

By Application Analysis

Packaging is projected to dominate the application segment owing to the massive global demand for sustainable alternatives to conventional plastic packaging. Biodegradable polymers are increasingly utilized in food containers, compostable bags, films, bottles, and disposable packaging products due to rising environmental concerns and stringent government regulations on single-use plastics. The food and beverage industry remains a major consumer because biodegradable materials help companies achieve sustainability goals while maintaining product safety and shelf-life performance.

By End-Use Industry Analysis

Food & Beverage are anticipated to dominates the end-use industry segment because the sector represents the largest consumer of biodegradable packaging materials globally. Increasing regulations restricting conventional plastic usage in food packaging, cutlery, takeaway containers, and beverage applications are driving substantial adoption of biodegradable polymers. Food manufacturers and restaurant chains are prioritizing compostable and bio-based materials to strengthen sustainability commitments and improve brand image among environmentally conscious consumers. The industry also benefits from the rising popularity of organic foods, eco-friendly packaging standards, and circular economy initiatives.

The Global Biodegradable Polymers Market Report is segmented on the basis of the following:

By Type

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Starch-Based Polymers

- Polybutylene Succinate (PBS)

- Polybutylene Adipate Terephthalate (PBAT)

- Cellulose Derivatives

- Polycaprolactone (PCL)

- Other Type

By Processing Method

- Injection Molding

- Extrusion

- Blow Molding

- Thermoforming

- Film Processing

By Application

- Packaging

- Agriculture & Horticulture

- Consumer Goods

- Textile

- Healthcare & Medical

- Automotive

- Electronics

- Other Application

By End-Use Industry

- Food & Beverage

- Healthcare

- Retail & Consumer Goods

- Agriculture

- Textile Industry

- Industrial

- Other End User

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global biodegradable polymers market as it is projected to hold 38.2% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the biodegradable polymers market because of the unmatched concentration of biopolymer production facilities and the aggressive sustainable packaging agendas of Fortune 500 consumer packaged goods companies. The area has an established ecosystem of global resin compounders, boutique material science firms, and a rich pool of polymer chemists and application engineers. Moreover, an optimistic venture capital climate persistently finances upcoming PHA and algae-based material enterprises that need expert material processing services to achieve rapid scale-up and certification compliance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding biodegradable polymers market, driven by the government-led sweeping single-use plastic bans and sustainability initiatives in India, China, Japan, and Southeast Asia. The fast-paced economic growth, the rise of a consuming-class population, and the dynamic expansion of the e-commerce economy is compelling established resin producers and consumer brands to discard persistent plastic infrastructure. PLA and starch-blend compounding is in high demand to help these large organizations head in the direction of bio-based, circular material operating models. There is also a severe lack of qualified biopolymer processing talent in the region, and it is necessary to outsource material development services to implement, certify, and provide quality assurance for biodegradable applications to cover the skills gap and enable faster investments in home-compostable and soil-biodegradable projects.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global biodegradable polymers market has become highly dynamic with a heterogeneous array of multinational chemical corporations, specialized bio-polymer divisions of large agricultural processors, and niche material science start-ups. The key to success will be the profound strategic alliances with food & beverage brands, packaging converters, and organic waste management facilities because they will open the necessary co-investment opportunities and early access to the new composting certification standards. The movement towards market consolidation is rapidly progressing with the traditional petrochemical conglomerates acquiring PHA fermentation and PLA production specialized boutiques to stay afloat.

Some of the prominent players in the Global Biodegradable Polymers Market are:

- BASF SE

- NatureWorks LLC

- Novamont S.p.A.

- TotalEnergies Corbion PLA

- Mitsubishi Chemical Group Corporation

- Corbion N.V.

- Danimer Scientific

- Biome Bioplastics Limited

- Braskem S.A.

- Toray Industries, Inc.

- FKuR Kunststoff GmbH

- Plantic Technologies Limited

- CJ CheilJedang Corporation

- PTT MCC Biochem Co., Ltd.

- Kaneka Corporation

- Eastman Chemical Company

- Arkema S.A.

- Tianan Biologic Material Co., Ltd.

- Green Dot Bioplastics

- Teijin Limited

- Other Key Players

Recent Developments

- January 2026: NatureWorks declared it will make a major expansion of its Ingeo PLA production facility, a manufacturing initiative to assist clients in Healthcare and Food & Beverage to create proprietary high-heat PLA grades through lactide purification and expertise in thermoforming and film processing.

- November 2025: Danimer Scientific strengthened its collaboration with a major QSR chain and introduced a specific application based on PHA extrusion and coating designed to support compostable cold cup and straw manufacturing and keeping in compliance with proposed international single-use plastic regulations.

- October 2025: BASF acquired a European seaweed-based polymer start-up to further its PBAT and cellulose derivatives blending solutions for thin-film mulch applications, to support the complicated requirements of agriculture and horticulture sector customers in soil biodegradability.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 11.0 Bn |

| Forecast Value (2035) |

USD 37.4 Bn |

| CAGR (2026–2035) |

14.5% |

| The US Market Size (2026) |

USD 3.5 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Type, By Processing Method, By Application, and By End-Use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Biodegradable Polymers Market?

▾ The Global Biodegradable Polymers market is poised to be valued at USD 11.0 billion in 2026 and is projected to reach USD 37.4 billion by 2035, driven by the universal need for specialized material solutions in sustainable packaging, compostable consumer goods, and agricultural films.

What is the CAGR of the Global Biodegradable Polymers Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 14.5% from 2026 to 2035, reflecting the accelerating complexity of plastic replacement mandates and the persistent shortage of industrial-scale polymerization capacity.

What factors are driving the growth of the Global Biodegradable Polymers Market?

▾ Key drivers include the global regulatory push against single-use plastics, the imperative to find end-of-life solutions for flexible packaging, the material certification complexity of multi-substrate applications, and the surge in demand for soil-biodegradable polymers amid evolving extended producer responsibility laws.

Which region held the largest share of the Biodegradable Polymers Market in 2026?

▾ North America is poised to dominate this market with 38.2% of the market share in 2026, driven by a mature bio-refinery ecosystem and aggressive brand investment in PLA and PHA-based material capabilities.

Which region is expected to grow the fastest in the Biodegradable Polymers Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid plastic regulation enforcement in India, China, and Japan, where starch-based and PBAT material consulting is critical for transitioning large consumer goods conglomerates to certified compostable operations.

What are the major trends in the Global Biodegradable Polymers Market?

▾ Major trends include the integration of enzymatic degradation triggers into polymer formulations, the rise of carbon-negative feedstock consulting, the demand for application-specific PHA grades, and the focus on blending optimization within complex biopolymer conversion environments.

Who are the key players in the Global Biodegradable Polymers Market?

▾ Key players include large-scale PLA producers like NatureWorks and TotalEnergies Corbion, PHA pioneers like Danimer Scientific and Kaneka, as well as the material science divisions of chemical conglomerates like BASF and Mitsubishi Chemical Group, alongside specialized pure-play compounders.

How is the Global Biodegradable Polymers Market segmented?

▾ The market is segmented by By Type, Processing Method, Application, and End-Use Industry.