What is the Global Biofoundry Market Size?

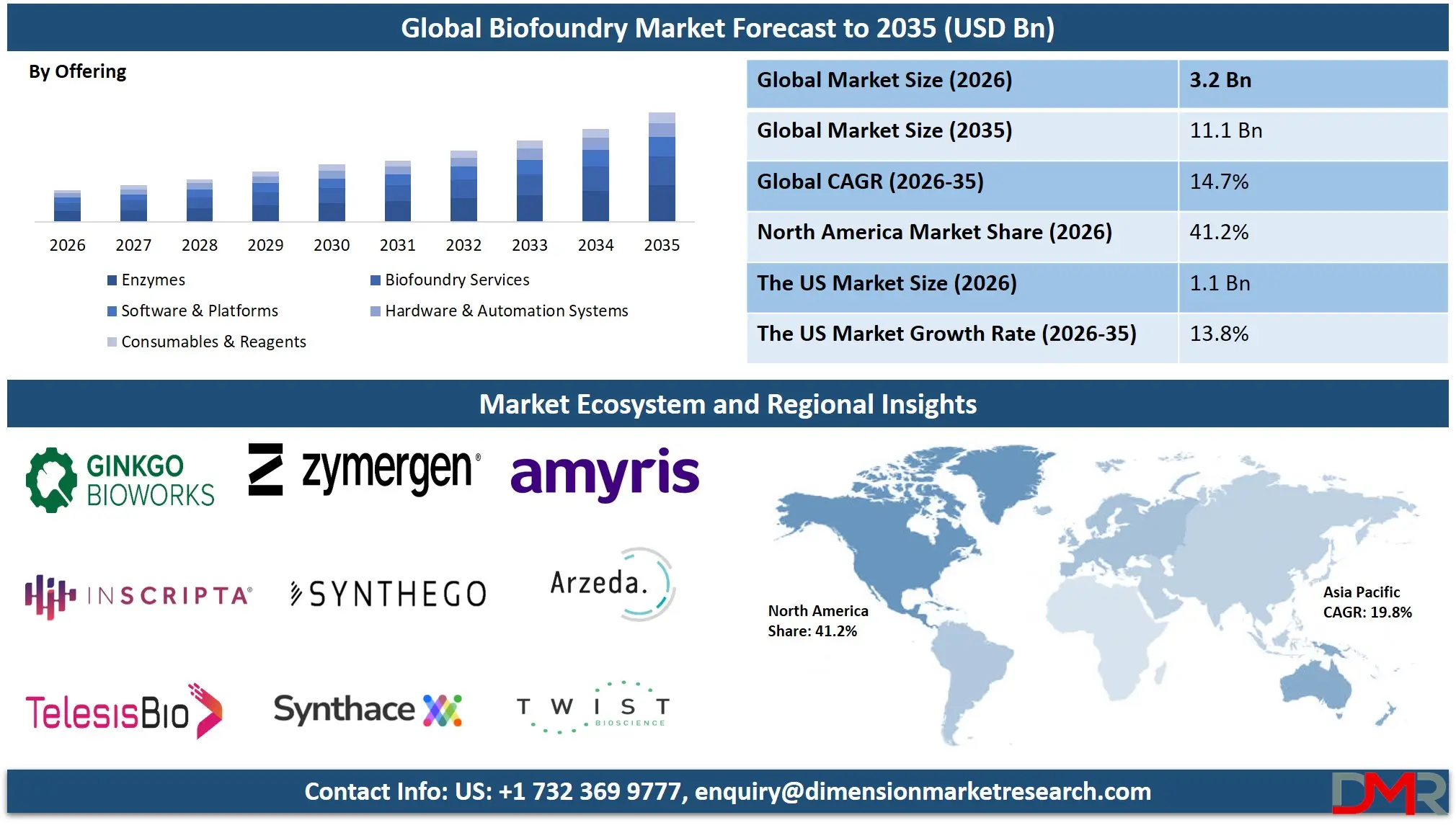

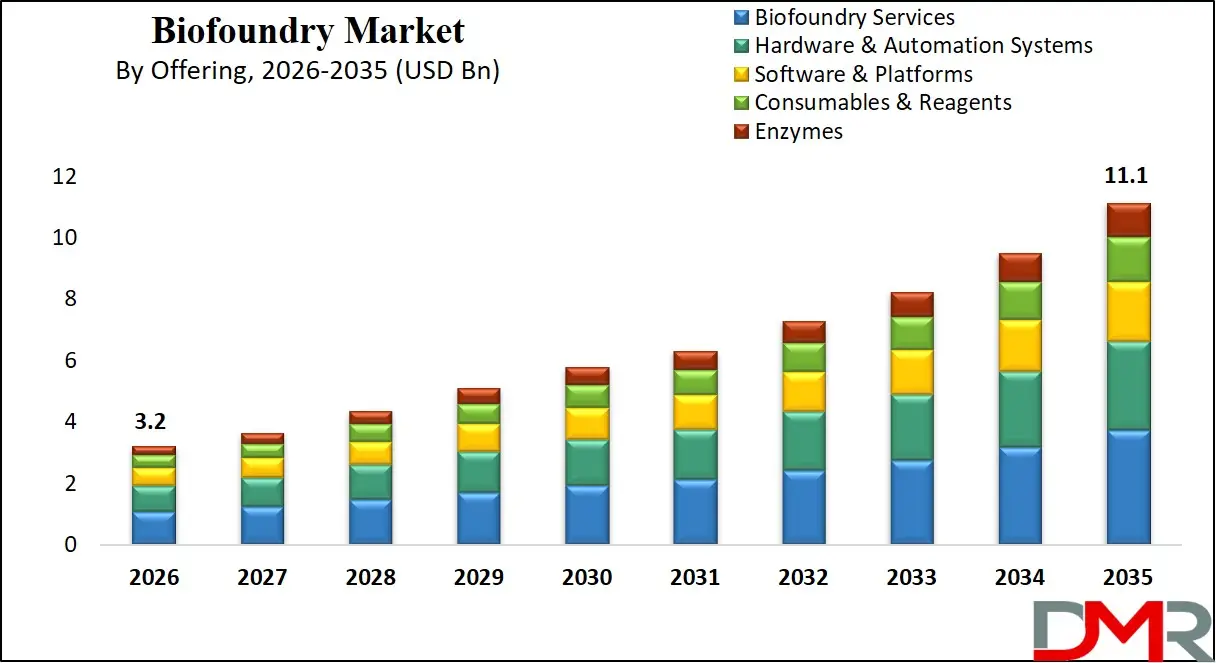

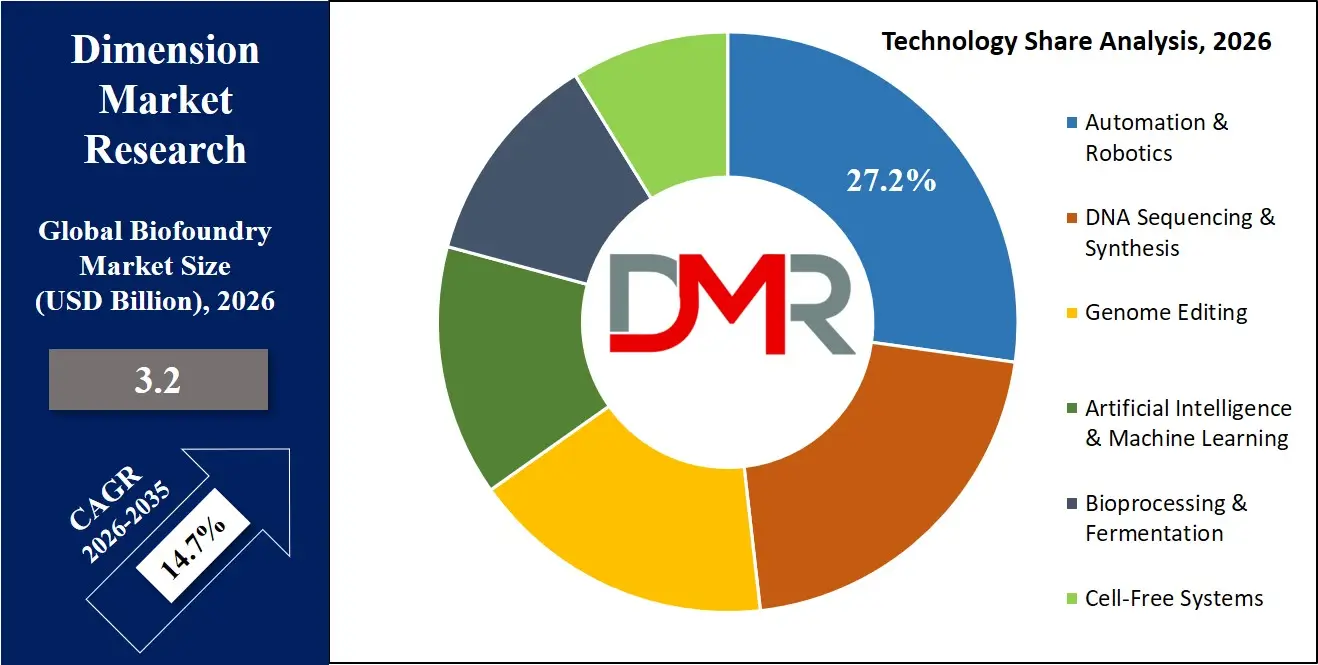

The Global Biofoundry Market size is estimated at USD 3.2 billion in 2026 and is projected to reach USD 11.1 billion by 2035, growing at a CAGR of 14.7% during the forecast period, driven by AI-enabled engineering, automation, and integrated DBTL workflows in synthetic biology.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The growth of the biofoundry industry can be attributed to an increase in machine learning techniques for strain optimization and microbial cell engineering, government mandates that minimize the likelihood of failure of the bioprocesses and shorten the timeline for the development of biologics, and higher investment in automated synthetic biology programs by private companies and governments. Additional factors driving the growth include breakthroughs in real-time fermentation tracking technologies, metabolic modeling and prediction, automated DNA synthesis, and high-throughput screening, among other developments in interoperability systems which facilitate biofoundry integration in biomanufacturing operations.

Digital modernization in pharma and industrial biotech companies has helped optimize strain design and improve process outcomes, including reduced time to production. Automation of the workflows, predictive processes, and artificial intelligence-enabled design-build-test systems have accelerated adoption, and bioeconomy national strategies have supported sustainability in biomanufacturing.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Biofoundry Market

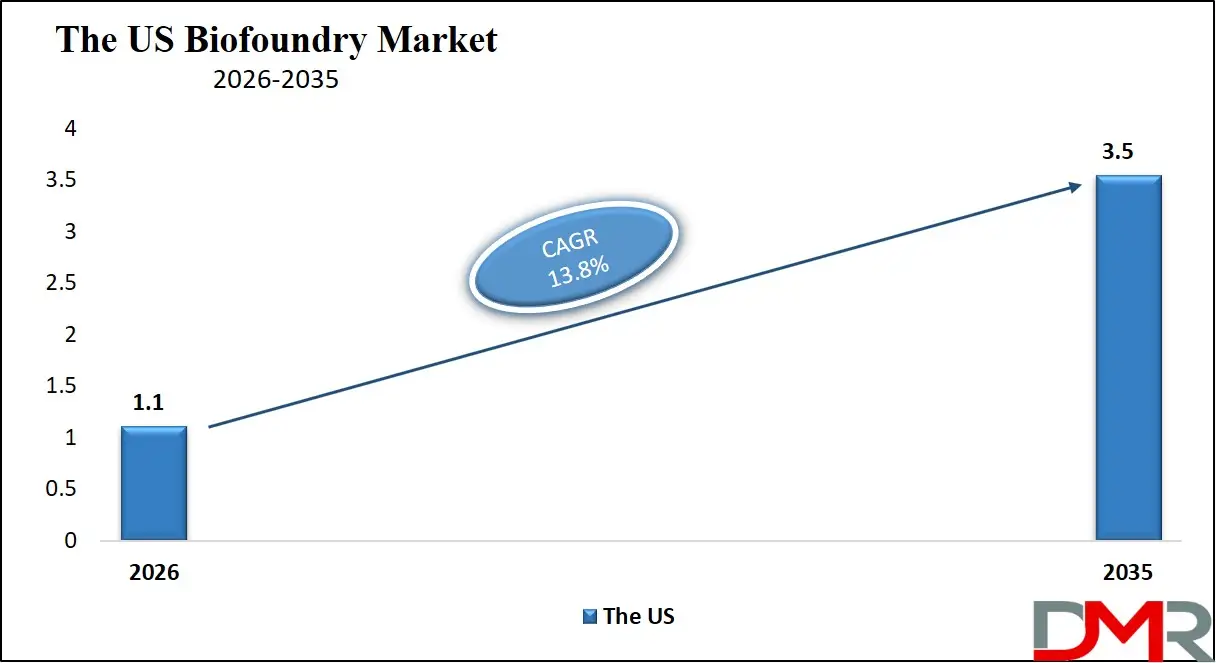

The US Biofoundry Market is estimated to grow to USD 1.1 billion in 2026 with a compound annual growth rate of 13.8% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US market is defined by the existence of significant federal funding schemes like the National Biofoundry Initiative, the NIIMBL-based biopharmaceutical manufacturing centers, the FDA-involved AI/ML-enabled bioprocess control pathway to gene therapy and vaccine production, all of which will help the development of the necessity of AI-driven strain engineering, real-time bioprocess telemetry of automated bioreactors and robotic workcells, and predictive biofoundry software, automated biofoundry hardware systems remain to be more rapidly adopted in the region, and the US needs highly developed interoperability frameworks, integration of real-world evidence using electronic lab notebooks (ELNs), and verifiable biofoundry AI assurance. Also, service providers are being pressured by initiatives like the 21st Century Cures Act and national AI in biomanufacturing strategies to create dedicated integration and deployment services to guarantee data interoperability, security, and compliance across a variety of pharma R&D departments and academic research centers.

Europe Biofoundry Market

The Europe Biofoundry Market is estimated to be valued at USD 859.9 million in 2026, witnessing growth at a CAGR of 13.6%, during the forecast period.

The biofoundry market is mature in Europe, and it has a strong effect on the regulatory specifications and the regional policies including the EU Bioeconomy Strategy, the European Biomanufacturing Pilot Lines, and national digital biotech programs (e.g., the France-Biofoundry and the German Bioökonomie 2030 strategy). Another area that countries are working towards is smart biofoundry modularization in order to align research and production workload demands and interoperability of cross-border bioprocess data supply chains. It is driven by advanced technologies, such as real-time genome design engines and high-reliability metabolic flux scoring systems with an inbuilt predictive algorithm on the development of engineered cell lines. Adoption is facilitated by the use of public-private partnerships and harmonization of biofoundry standards. Technologies like real-time computational workload balancing and smart contract-based data sharing are commonly practiced as research-centric programs, and Europe is a frontrunner in terms of the digital transformation of safe and efficient biofoundry-enabled biomanufacturing.

Japan Biofoundry Market

The Japan Biofoundry Market is projected to be valued at USD 220.1 million in 2026, progressing at a CAGR of 17.2%, during the period spanning from 2026 to 2035.

Japan boasts a mature biofoundry market supported by high-performance automated DNA assembly systems, diagnostic fermentation integration technology, and a wide network of robotic bioprocessing AI innovations. Automation, precision, and process integrity are the priorities in the country and are achieved by predictive metabolic progression models and intelligent process management systems for industrial fermentation. Growth is stimulated by government actions under the Society 5.0 initiative and constant investment in digital biomanufacturing infrastructure. The high volume of biopharma R&D, industrial strain development for enzymes and biofuels, and biofoundry lab automation requires efficient AI for real-time evidence-based inference. The difficulties are high validation costs for new biofoundry automation architectures and integration with legacy bioprocessing systems, yet the prospects are in exporting developed biofoundry technologies to Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Biofoundry Market is estimated to be valued at USD 3.2 billion in 2026 and is expected to grow to USD 11.1 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 14.7% in the forecast period.

- Primary Growth Drivers: Technological progress in machine learning-based engineering of microbial strains for therapeutics and chemicals; regulatory requirements for faster bioprocess development and reduced failure rates; and clinical/industrial deployment of intelligent biofoundry platforms are some of the key drivers of growth in the market.

- Key Market Trends: The use of predictive metabolic outcome monitoring, real-time bioprocess optimization, and transition to cloud-based biofoundry telemetry and fleet management systems are some of the primary market trends.

- By Offering: The Software & Platforms segment is anticipated to get the majority share of the biofoundry market in 2026.

- By Technology: The Artificial Intelligence & Machine Learning segment is expected to occupy the largest revenue share in 2026 in the biofoundry market.

- By Application: The Healthcare segment (specifically Drug Discovery) is expected to get the largest revenue share in 2026 in the biofoundry market.

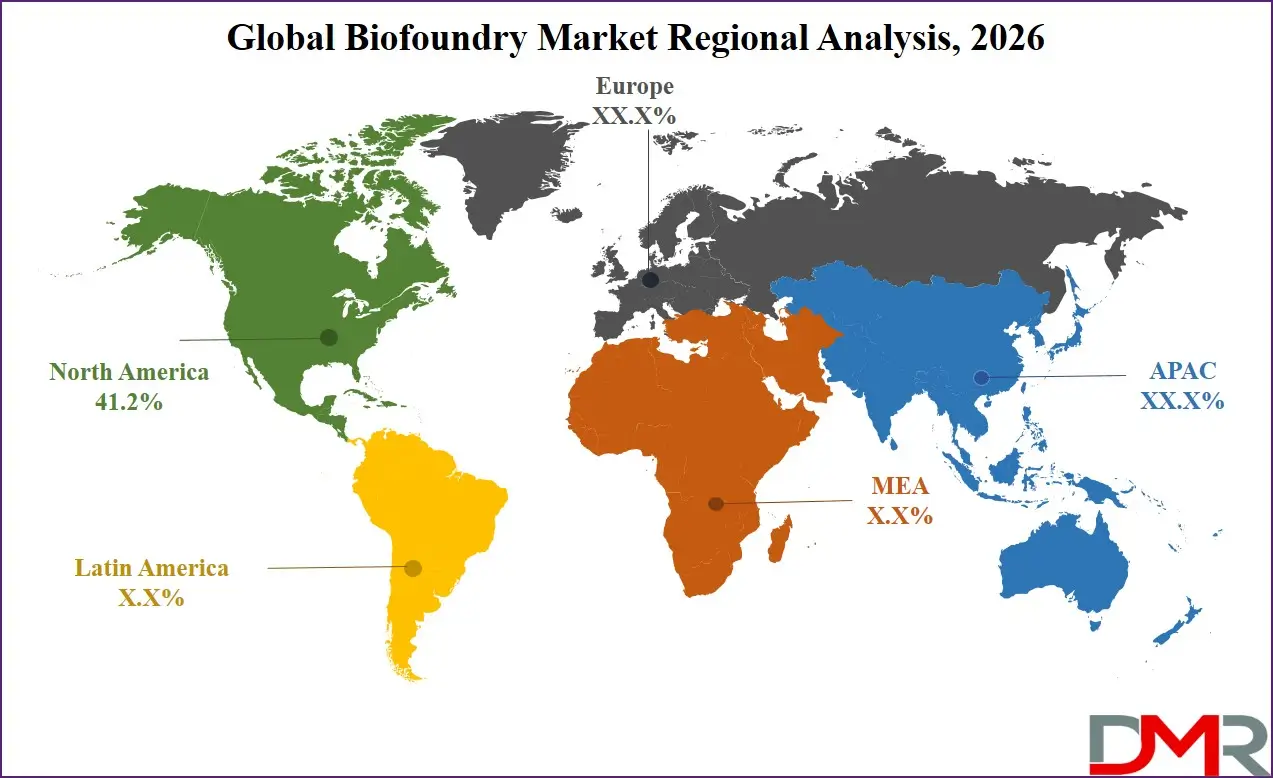

- Regional Leadership: North America is predicted to dominate the market with an estimated 41.2% share in 2026, with high biotech R&D spend and biofoundry technology investment.

What is Biofoundry?

Biofoundry refers to an integrated, automated platform that combines robotics, artificial intelligence, and high-throughput biological engineering tools to execute the design-build-test-learn (DBTL) cycle for engineered biological systems. These systems use automated liquid handling, DNA synthesis and assembly, bioreactors, and analytical technologies to enable rapid strain engineering, improved design accuracy, and accelerated prototyping and scale-up of bioprocesses. Biofoundries are increasingly used in industrial biotechnology and pharmaceutical R&D to enhance process efficiency, support personalized medicine development, and advance the production of bio-based chemicals and therapeutics.

Use Cases

- Strain Engineering for Biologics: Biofoundries are capable of designing high-throughput genetic construct designs in real-time to discover an optimal production strain in monoclonal antibodies and gene therapies with latency on the order of weeks, and saving orders of magnitude over time compared with manually screening microbial libraries.

- Metabolic Pathway Optimization: Long-term fermentation and flux data, such as cumulative yields and byproduct accumulation, are modeled to give process adjustment recommendations and keep safely managing production runs without interruption to ensure bioprocess stability and manufacturing confidence.

- Fermentation Monitoring & Control: Industrial deployments are employing machine learning and bioreactor analytics to perform on-device real-time yield prediction, process anomaly detection, and automated feed adjustment with quantifiable and proven accuracy.

- Population Health & Government Programs: More efficient biofoundries contribute to the success of biopharma innovation, rare disease therapeutic development, and smart bioprocess surveillance, facilitate national bioeconomy adoption, contribute to deployment reliability, and help implement policies, such as the biofoundry governance policy and biomanufacturing standards.

How AI Is Transforming the Global Biofoundry Market?

Artificial intelligence is revolutionizing the field of biofoundry, allowing predictive modeling of the likelihood of metabolic pathway success, automatic detection of anomalies in fermentation data patterns, and optimization of strain design parameters in a pathway-specific scenario. Bioreactor-generated telemetry and metabolomics data can be processed using AI algorithms to identify any degradation or performance drift and optimize production outcomes at scale. This saves time, is verifiable and cheaper than manual data analysis.

Moreover, AI enhances bioprocess assurance through offering adaptive computational event-based scheduling, anticipating workflow threats to design accuracy, and intelligent prioritization of biofoundry module health monitoring. It is also involved in reducing the cost of baseline testing and ongoing performance tracking, allowing biomanufacturing IT operators to reduce the cost and physical footprint of on-prem test campaigns and improve the reliability of biofoundry workloads and their financial returns.

Market Dynamics

Key Drivers of the Global Biofoundry Market

Rapid developments in Machine Learning and Real-Time Bioprocess Inference

The market is being pushed by a fast uptake of AI-driven strain and bioprocess optimization, high-efficiency bioprocess data processing, API-based interoperability with ELNs and laboratory information management systems (LIMS), and real-time telemetry analytics from bioreactors. These technologies enable monitoring of the performance of biofoundry systems in real-time, identify process anomalies early, predict metabolic flux rates, and simplify the process of experimental validation. Consequently, operational uptime and R&D efficiency are highly enhanced while minimizing the costs of manual data analysis. The growth of machine learning models for pathway design, in particular, is also accelerating the need for intelligent biofoundry automation, as biomanufacturing operators are increasingly adopting automation and workflow optimization based on bioprocess data.

Growing Focus on Bioprocess Regulation and Sustainable Biomanufacturing

The world is increasingly focused on bioprocess safety and quality, with governments and regulatory bodies introducing biomanufacturing efficiency frameworks, such as the EU Bioeconomy Strategy provisions and the US FDA's Advanced Manufacturing Technologies framework for biologics and cell therapies. These structures are driving demand for efficient biofoundry automation capable of supporting real-time process monitoring and continuous learning. In parallel, global initiatives promoting biomanufacturing standardization and workforce development are encouraging the adoption of evidence-based biofoundry architectures. The increasing focus on transparency in bioprocess design and reduction in production failure rates is also enhancing the necessity of reliable and scalable biofoundry automation in both public and private biomanufacturing systems.

Restraints in the Global Biofoundry Market

High Costs of Integration and Process Validation

Biofoundry platforms are expensive and time-intensive to implement, need to be heavily tested in production settings, and process logic reliability is tested, and long-term performance evaluation of new components is needed. Also, regulatory limitations and data privacy regulations (e.g., GDPR for biosensor data, trade secret protections) add to the complexity and cost of deployment. These aspects pose barriers to entry, lengthen deployment, and raise initial capital investments.

Limited Standardization Across Bioprocess Data and Workflows

The industry continues to rely on multiple biofoundry automation architectures, including robotics-based, AI-based for process optimization, and computer vision-based for colony picking. However, the lack of standardized bioprocess data interfaces beyond platforms like SiLA for lab automation and Allotrope for analytical data remains a key challenge. Biofoundry lacks universal plug-and-play standards compared to traditional bioprocess modules, making integration complex and limiting interoperability of biofoundry models across different R&D and production systems.

Growth Opportunities in the Global Biofoundry Market

Expansion of Emerging Biomanufacturing Programs

Developing biomanufacturing markets such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are investing in digital bioeconomy infrastructure and advanced biofoundry capabilities. These regions present strong growth potential due to increasing demand for automated strain development, fermentation monitoring, and remote bioprocess consultation applications. With limited legacy bioprocessing infrastructure, they provide opportunities for the deployment of modern biofoundry automation optimized for R&D and manufacturing environments.

Rising Demand for Cloud-Based Biofoundry Deployment

The increased requirement for advanced biofoundry automation is being generated by the growth of remote R&D collaboration, distributed biomanufacturing, and real-time bioprocess control applications. These technologies play a vital role in virtual biofoundry platforms, remote production clinics, and biotech innovation hubs. With the rising importance of sub-hour process latency as a major production concern, cloud-based biofoundry inference capabilities are likely to be fundamental to future biomanufacturing and biotech IT infrastructure.

Global Biofoundry Market Trends

Predictive Metabolic Outcome Monitoring and Computational Analytics

Biofoundry platforms are being monitored and process logic anomalies are detected in real time, and prediction override patterns are predicted using on-system learning. The use of digital twin models of metabolic flux and machine learning algorithms is enhancing bioprocess workflow scheduling, system lifespan, and deployment reliability. This shift is transforming biofoundry management from manual data review to a fully automated, continuously optimized system monitoring.

Cloud-Based Telemetry and Fleet Management Systems

Cloud computing and digital twin technologies are taking centre stage in the operations of biofoundry clusters. These platforms enable real-time storage and analysis of bioprocess performance data, centralized fleet management of automated work cells, and remote monitoring of biofoundry module health. Cloud-based systems enhance transparency, lower on-prem infrastructure expenses, and provide quicker responses to workflow changes across R&D sites, as experienced by operators of large biofoundry networks.

Research Scope and Analysis

By Component Analysis

The Software & Platforms segment is expected to remain the largest in 2026, accounting for about 34.8% of the global biofoundry market, driven by its dominant use in large-scale metabolic pathway design, seamless LIMS workflow integration, and flexibility across diverse R&D frameworks where real-time bioprocess data access and software ecosystem maturity are essential. Meanwhile, the Hardware & Automation Systems segment is witnessing strong growth, driven by rising demand for automated liquid handlers, robotic colony pickers, and AI-powered bioreactors in R&D and production settings where real-time data capture and process reproducibility are critical. Adoption is further supported by workflow optimization, real-time efficiency improvements, and modular configurations that integrate multiple process logic types for improved workflow flexibility and operator satisfaction.

By Technology Analysis

The Automation & Robotics segment is expected to account for 27.2% share in 2026, as biofoundries heavily rely on robotic workcells for DNA assembly, colony picking, and high-throughput screening. The segment is further supported by increasing deployment of automated liquid handling systems, AI-enabled bioreactors, and integrated workflow platforms that enhance process reproducibility and operational efficiency across synthetic biology and biomanufacturing applications. It is also among the fastest-growing segments in the biofoundry market, driven by rapid adoption of fully automated DBTL workflows and scalable laboratory automation infrastructure.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Application Analysis

The Healthcare segment (specifically Drug Discovery) is expected to dominate with around 44.2% market share in 2026, driven by the critical need for rapid and accurate engineering of therapeutic proteins, monoclonal antibodies, and cell/gene therapies in pharma R&D. Biofoundries support drug discovery scenarios due to their ability to rapidly prototype production strains, delivering rapid turnaround times while maintaining process data within R&D systems. The Industrial Biotechnology segment (specifically Bio-based Chemicals), while smaller, is witnessing strong growth, driven by smaller biotech firms and industrial labs where lower upfront costs and integration with existing fermentation infrastructure are required. The Food Technology segment (specifically Engineered Proteins), with AI-powered strain engineering for alternative proteins, has the fastest development.

By End-User Industry Analysis

The Pharmaceutical & Biotechnology Companies segment represents the largest end-user in 2026, accounting for 48.7% share, driven by complex R&D environments requiring real-time strain design and bioprocess optimization for biologics, vaccines, and gene therapies. Academic & Research Institutes form the second-largest segment, utilizing biofoundries for fundamental synthetic biology research and pathway discovery. The fastest-growing area is Government & Public Research Institutions, adopting biofoundry infrastructure for national bioeconomy initiatives and biosecurity applications. Contract Development & Manufacturing Organizations (CDMOs) are emerging for biofoundry-assisted process development and scale-up.

The Global Biofoundry Market Report is segmented based on the following:

By Offering

- Enzymes

- Biofoundry Services

- Software & Platforms

- Hardware & Automation Systems

- Consumables & Reagents

By Technology

- DNA Sequencing & Synthesis

- Genome Editing (CRISPR/Cas)

- Automation & Robotics

- Artificial Intelligence & Machine Learning

- Cell-Free Systems

- Bioprocessing & Fermentation

By Application

- Healthcare

- Drug Discovery

- Vaccines

- Personalized Medicine

- Industrial Biotechnology

- Bio-based Chemicals

- Biofuels

- Bioplastics

- Agriculture

- Environment

- Bioremediation

- Carbon-negative Solutions

- Food Technology

- Synthetic Food

- Engineered Proteins

By End-User Industry

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Development & Manufacturing Organizations (CDMOs)

- Contract Research Organizations (CROs)

- Government & Public Research Institutions

Regional Analysis

Leading Region in the Biofoundry Market

It is projected that North America will take the lead in the global biofoundry market (by value), covering a market share of about 41.2% in the year 2026. The region's dominance is driven by strong biotech R&D workload cadence (US-based National Biofoundry Initiative and NIIMBL programs), high software and automation prices relative to other regions, a mature laboratory IT supply chain for advanced interoperability and high-speed data exchange, and the presence of key biofoundry vendors and synthetic biology labs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The widespread adoption of advanced machine learning and robotics-based biofoundry automation for drug discovery, industrial biotechnology, and biomanufacturing further strengthens North America's leading position in the market. Additionally, continuous investments in AI-enabled process logic monitoring and interoperability capabilities are further reinforcing regional technological leadership.

Fastest-Growing Region in the Biofoundry Market

Asia-Pacific is the fastest-growing region, supported by strong digital biomanufacturing deployment targets (China, India, Japan), increasing bioprocess sovereignty initiatives, rising investments in domestic biofoundry capabilities, and growing adoption of automated strain engineering systems. The region benefits from well-established instrumentation manufacturing capacity for automated workcells, increasing commercial participation, and alignment with national bioeconomy roadmaps. Countries across the region are actively deploying biofoundries to enhance R&D productivity-per-dollar and strengthen biomanufacturing infrastructure. Growing emphasis on biofoundry R&D and structured process logic development further accelerates market expansion in the region. Moreover, increasing government support and commercial biotech commitments are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The biofoundry market is highly competitive, with innovation and strategic alliances shaping the competitive environment. In order to achieve a competitive advantage, companies and research labs are focused on the development of advanced automation architectures (e.g., AI-based pathway design, robotics for high-throughput screening, and machine learning for bioprocess optimization), AI-powered bioprocess telemetry, and digital twin-enabled process monitoring platforms. There are high barriers to entry due to capital-intensive process validation infrastructure, specialized synthetic biology expertise, and the need for mature software ecosystems and biomanufacturing regulatory and procurement compliance.

Strategic approaches in the market to increase market presence include partnerships with pharma companies and biomanufacturing centers, mergers between automation solution providers and system integrators, and long-term support contracts with R&D labs and academic institutions. Moreover, research and development in interoperability frameworks and scalable software architectures are important factors in maintaining competitiveness and addressing the evolving needs of the synthetic biology community.

Some of the prominent players in the Global Biofoundry Market are:

- Ginkgo Bioworks Holdings, Inc.

- Zymergen Inc.

- Amyris, Inc.

- Inscripta, Inc.

- Synthego Corporation

- Arzeda Corporation

- Evonetix Limited

- DNA Script SAS

- Telesis Bio Inc.

- Strateos Inc.

- Synthace Limited

- LabGenius Ltd.

- TeselaGen Biotechnology, Inc.

- Automata Technologies Limited

- Benchling, Inc.

- Twist Bioscience Corporation

- GenScript Biotech Corporation

- Thermo Fisher Scientific Inc.

- Agilent Technologies, Inc.

- Novonesis Group

- Other Key Players

Recent Developments

- February 2026: Ginkgo Bioworks Holdings, Inc. expanded its AI-driven synthetic biology ecosystem through continued integration of automation and AI-based strain design platforms, strengthening its positioning as a leading "biological foundry-as-a-service" provider and accelerating partnerships across industrial biotech and pharmaceuticals.

- July 2025: Thermo Fisher Scientific Inc. expanded the US manufacturing footprint by acquiring sterile fill-finish plant from Sanofi, enhancing biologics production capabilities supporting synthetic biology workflows.

- May 2025: Twist Bioscience and Ginkgo updated their DNA supply agreement (3-year, USD 15M structure), strengthening long-DNA synthesis licensing and expanding flexible DNA procurement for synthetic biology workflows.

- April 2025: GenScript expanded its global gene synthesis, protein engineering, and CRISPR tool offerings, strengthening its role as a major upstream supplier for synthetic biology and biofoundry workflows.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 3.2 Bn |

| Forecast Value (2035) |

USD 11.1 Bn |

| CAGR (2026–2035) |

14.7% |

| The US Market Size (2026) |

USD 1.1 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Offering (Enzymes, Biofoundry Services, Software & Platforms, Hardware & Automation Systems, Consumables & Reagents), By Technology (DNA Sequencing & Synthesis, Genome Editing (CRISPR/Cas), Automation & Robotics, Artificial Intelligence & Machine Learning, Cell-Free Systems, Bioprocessing & Fermentation), By Application (Healthcare, Industrial Biotechnology, Agriculture, Environment, Food Technology), By End-User Industry (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Contract Development & Manufacturing Organizations, Contract Research Organizations, Government & Public Research Institutions) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Biofoundry Market?

▾ The Global Biofoundry Market size is estimated to have a value of USD 3.2 billion in 2026 and is expected to reach USD 11.1 billion by the end of 2035.

What is the CAGR of the Global Biofoundry Market from 2026 to 2035?

▾ The market is growing at a CAGR of 14.7% over the forecasted period.

What factors are driving the growth of the Global Biofoundry Market?

▾ The market is driven by advances in machine learning-based strain and pathway engineering and real-time bioprocess data generation, regulatory pressure to accelerate bioprocess development and reduce production failure rates, and increasing government investment in national bioeconomy infrastructure.

What are the major trends in the Global Biofoundry Market?

▾ The key market trends include the adoption of predictive metabolic outcome monitoring and real-time bioprocess control, along with a growing shift toward cloud-based biofoundry platforms and telemetry-enabled workflow management systems.

Which region held the largest share of the Global Biofoundry Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 41.2%.

Which region is expected to grow the fastest in the Global Biofoundry Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Biofoundry Market?

▾ Some of the major key players in the Global Biofoundry Market are Ginkgo Bioworks Holdings, Inc., Twist Bioscience Corporation, Amyris, Inc., Synthace Limited, Thermo Fisher Scientific, and many others.

How is the Global Biofoundry Market segmented?

▾ The market is segmented by offering, technology, application, and end-user industry.