Market Snapshot

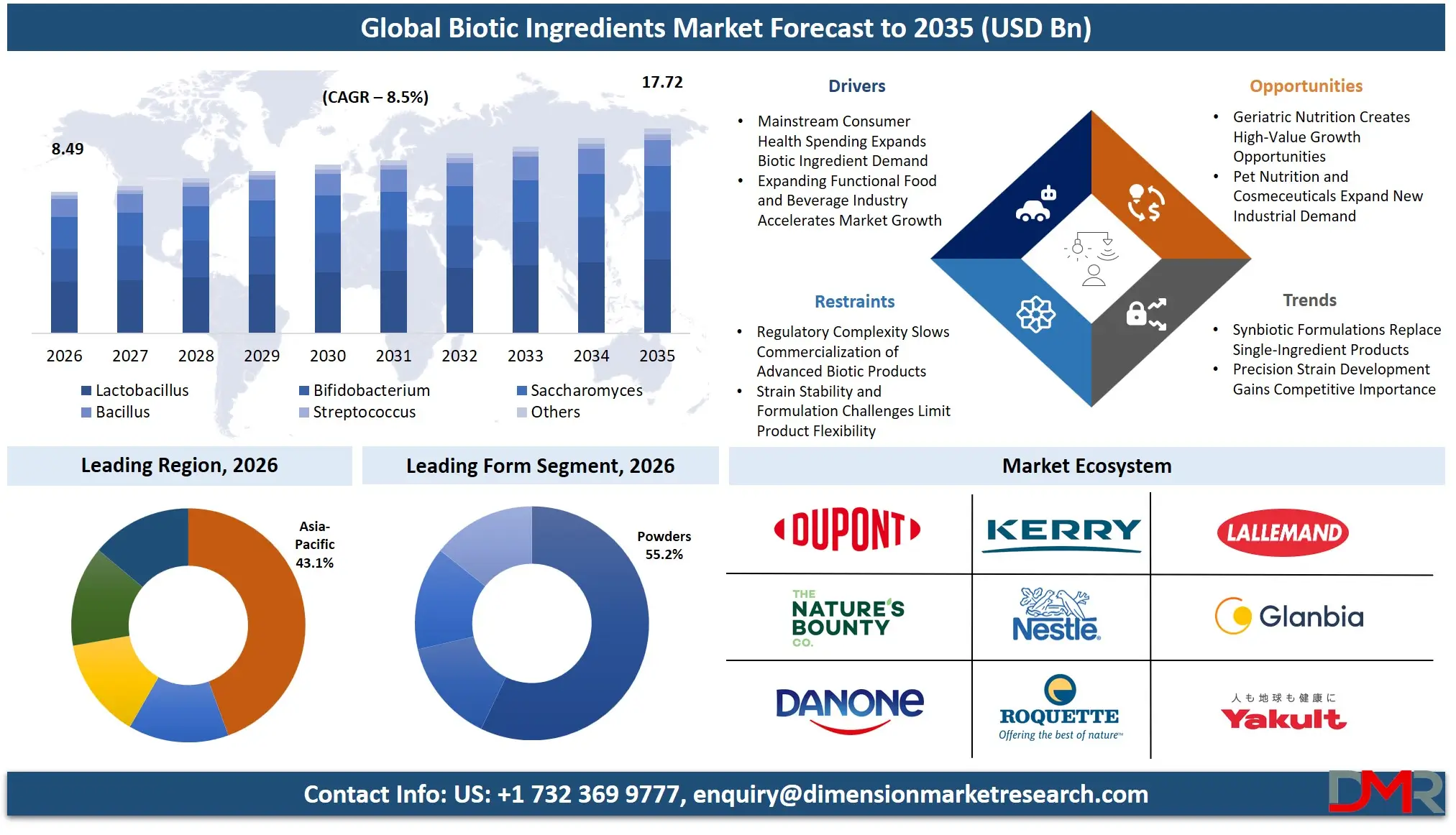

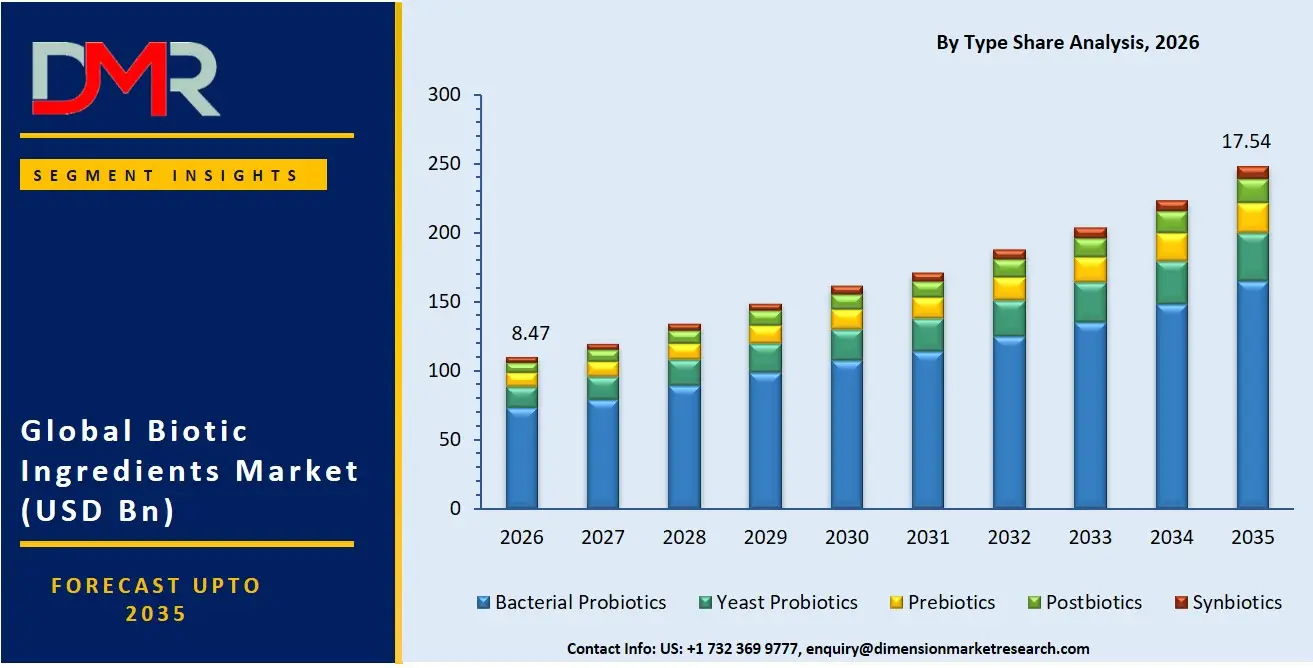

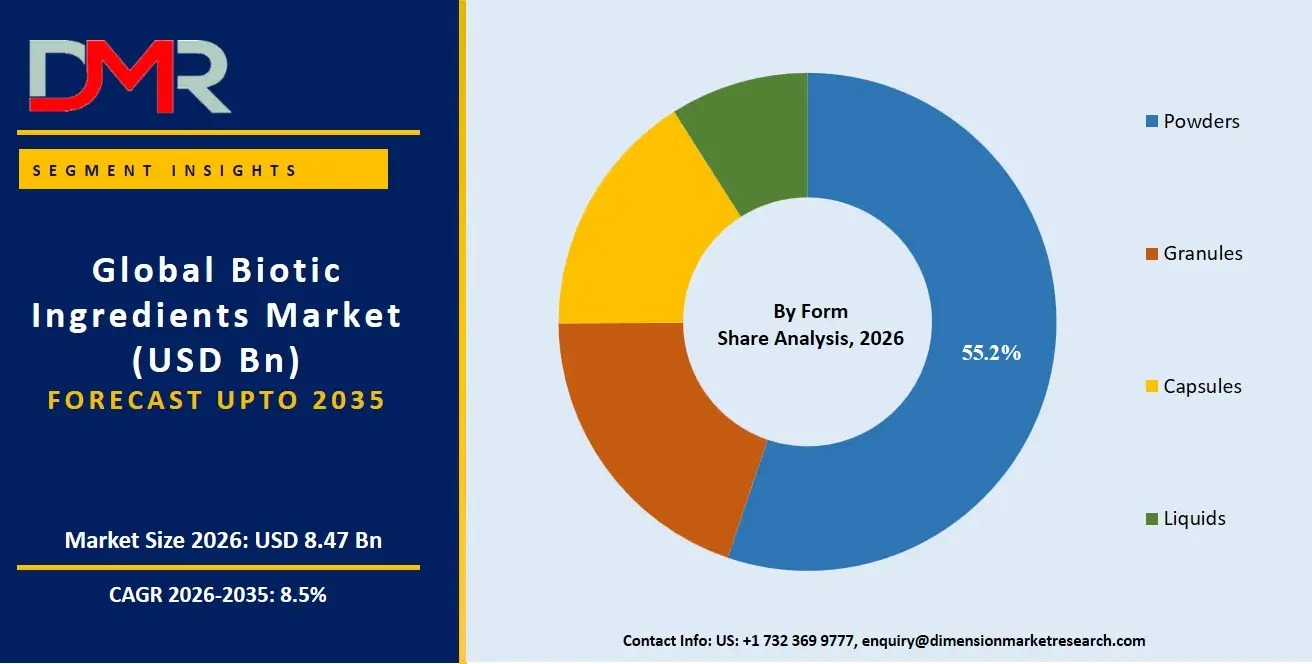

- The market size is USD 7.81 Billion in 2025, reached USD 8.47 Billion in 2026, and is projected to hit USD 17.54 Billion by 2035 at a CAGR of 8.5%.

- Bacterial Probiotics held the dominant type segment with a 66.3% revenue share in 2026.

- Powders led the By Form segment with a 55.2% revenue share in 2026.

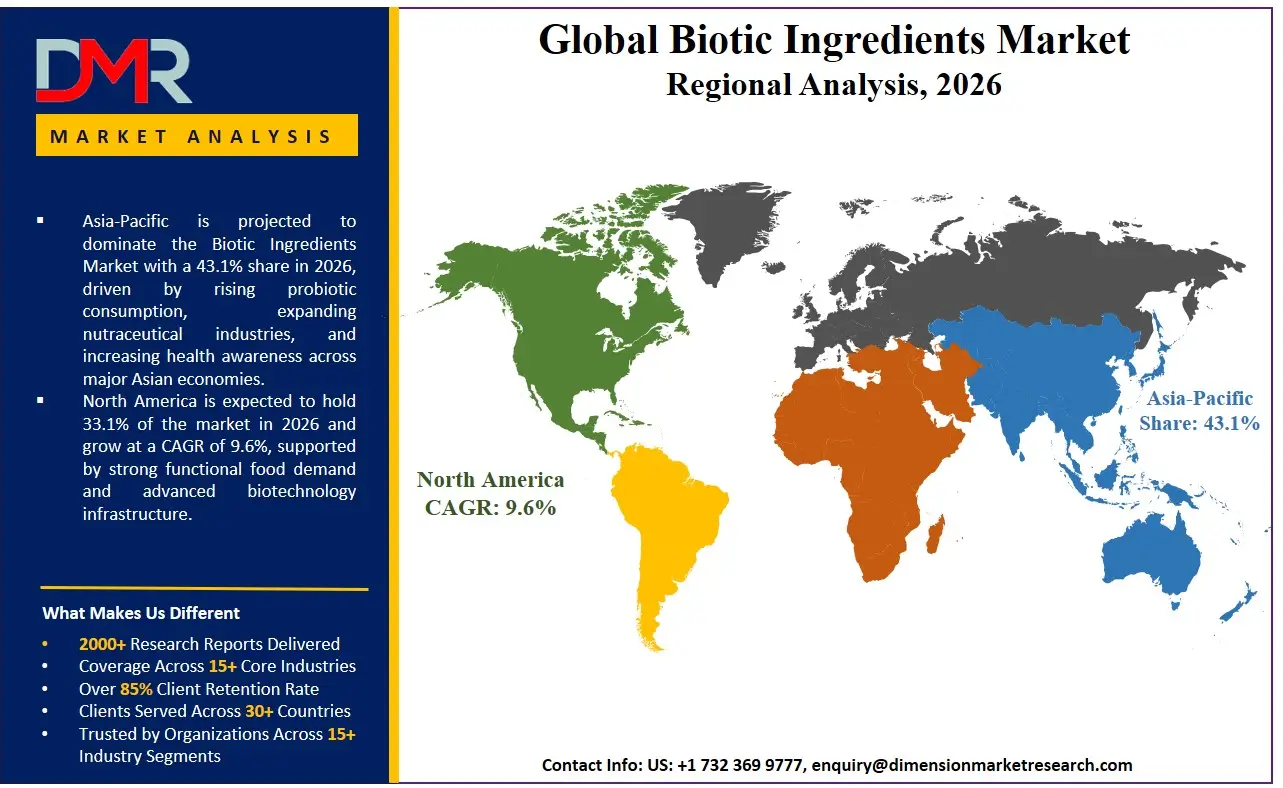

- Asia-Pacific held the dominant regional position in 2026.

- Key applications include Functional Food and Beverages, Dietary Supplements, Infant Nutrition, Medical Food, Pharmaceuticals, and Personal Care and Beauty Products.

Market Overview

The global biotic ingredients market covers the production and commercial supply of bacterial probiotics, yeast probiotics, prebiotics, and postbiotics used across functional food and beverage, dietary supplement, infant nutrition, medical food, pharmaceutical, and personal care applications. The market spans fermentation, encapsulation, drying and stabilization, centrifugation and filtration, and cell disruption manufacturing technologies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market excludes finished consumer products, branded supplement retail, and pharmaceutical drug formulations where the biotic ingredient is not the primary commercial unit. As reported by Frontiers in Immunology, 84.1% of 1,306 adult respondents believed biotic ingredients actively support digestion and gastrointestinal health, confirming that consumer pull is now broad enough to sustain ingredient demand across mainstream categories.

Biotic ingredients are no longer confined to digestive health supplements. Formulators now source these inputs for immune health, brain health, metabolic health, beauty-from-within, sports nutrition, and women's health applications. Personal care and cosmeceutical channels have emerged as credible industrial buyers, widening the total addressable market beyond traditional food and pharma procurement. This application expansion directly increases the number of B2B contract cycles per ingredient strain, giving suppliers with multi-application strain libraries a structural revenue advantage over single-category specialists.

Market Size and Forecast

The Global Biotic Ingredients Market size is estimated at USD 8.47 Billion in 2026 from USD 7.81 Billion in 2025, and is projected to reach USD 17.54 Billion by 2035, exhibiting a CAGR of 8.5% during the forecast period.

The forecast rests on three structural forces: widening health benefit adoption across non-digestive categories, accelerating B2B ingredient supply expansion by major biosolution companies, and rising consumer health awareness converting casual buyers into habitual users. Novonesis reported 8.0% organic growth in its Food and Health division in FY2025, confirming that leading suppliers are already capturing this trajectory ahead of full forecast-period volume.

Kirin Holdings recorded total annual net sales of 23.0 billion yen from its LC-Plasma postbiotic ingredient segment in FY2024, a 10.0% increase year-on-year as reported by Kirin Holdings on February 14, 2025, showing that postbiotic-specific revenue lines are growing independently of broader segment performance.

Consistent international volume expansion by ingredient manufacturers signals that overseas demand is absorbing new supply without pricing pressure, which supports the durability of the 8.5% growth rate through 2035. Manufacturers already operating at global distribution scale are better positioned to capture incremental procedure volume from new application channels than single-market players building international distribution from scratch.

Type Analysis

Bacterial Probiotics led the By Type segment with a 66.3% revenue share in 2026.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Bacterial probiotics dominate because they offer superior strain diversity, the deepest clinical validation across human health applications, and compatibility with food, supplement, and pharmaceutical manufacturing formats. The 66.3% share reflects years of clinical dossier investment that gives bacterial probiotic suppliers a procurement advantage no yeast or postbiotic format has yet displaced. Ingredient buyers selecting strains for product formulation overwhelmingly default to bacterial formats because regulatory approval precedents, safety data, and consumer recognition all concentrate in this sub-segment.

Postbiotics represent the fastest-moving sub-segment structurally. Kirin Holdings generated over 28.0 billion yen from its LC-Plasma postbiotic series in FY2025, confirming that shelf-stable inactivated preparations are converting from a niche science concept into a scalable commercial category. Yeast probiotics compete on fermentation resilience and heat stability but face formulation flexibility limitations compared to bacterial formats. Prebiotics are seeing renewed commercial interest as suppliers advance compound synbiotic products, repositioning prebiotics from standalone ingredients into foundational components of combination formats.

Form Analysis

With a 55.2% share in 2026, Powders outpaced all other form categories in the By Form segment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Powders dominate because they offer the lowest processing friction for bulk B2B ingredient blending, the longest shelf life across ambient storage conditions, and the best cost efficiency in large-scale food and supplement manufacturing. For formulators producing functional foods and infant nutrition products, powders remove the compatibility constraints that capsule or liquid formats impose on high-temperature or high-moisture production environments. The 55.2% share reflects the reality that most B2B volume moves through powder formats before any downstream consumer product format decision is made.

Capsules hold ground in pharmaceutical and clinical nutrition channels where precise dosing and gut-targeted delivery are required. Liquids serve ready-to-drink functional beverage formats, a channel that major food multinationals are entering through acquisition rather than organic development. Granules address niche pediatric and elderly nutrition applications where swallowability and dispersibility are primary formulation requirements. Suppliers capable of offering multi-format strain delivery will capture a wider range of B2B contracts than those committed to a single production format.

Application Analysis

Functional Food and Beverages captured the leading position across By Application categories in 2026.

Functional food and beverages represent the highest-volume application channel because they combine mass-market distribution reach with the lowest regulatory barrier among all biotic application categories. Ingredient buyers in this channel prioritize heat stability, taste neutrality, and shelf-life compatibility, which favors both powder formats and postbiotic preparations that survive processing conditions that destroy live bacterial strains. The scale of this channel creates the largest absolute B2B ingredient procurement volumes in the market.

Dietary supplements hold the second position and offer ingredient suppliers the highest margin per unit because clinical claim differentiation commands premium pricing. Infant nutrition is the most tightly regulated application category and therefore the most defensible once a supplier achieves approval. Personal care and beauty products represent the fastest-growing non-food application, as South Korean cosmetics producers integrate shelf-stable postbiotic preparations into anti-inflammatory dermo-cosmetics, creating an industrial buyer segment that did not exist at commercial scale three years prior.

Regional Analysis

Asia-Pacific held the dominant regional position in 2026, anchored by Japan, China, South Korea, and India.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia-Pacific leads because a deeply embedded fermented food culture normalizes biotic ingredient consumption across demographics, giving ingredient suppliers a consumer base with established purchasing habits rather than one requiring behavioral conversion. Japan alone illustrates this concentration: over 70.0% of 635 respondents in a Kirin Holdings survey reported increased awareness of daily health management throughout the year, confirming that Japanese consumers actively track and act on health ingredient information at a rate that far exceeds comparable metrics in other regions.

South Korean cosmetics producers are simultaneously scaling postbiotic dermo-cosmetic lines, adding a manufacturing pull that reinforces Asia-Pacific's supply and demand leadership. Japan's domestic postbiotic beverage market expanded at approximately 40.0% year-on-year in 2025 within the chilled beverage category alone, a growth rate that no other regional market is currently matching in this specific format.

North America is the most commercially active region outside Asia-Pacific, anchored by major acquisition activity in the functional beverage channel and the NIH's allocation of USD 215.0 million to the Human Microbiome Project, as reported by ACS Biomaterials, signaling long-term institutional commitment to microbiome science that will translate into commercial ingredient demand. Europe holds strategic importance through regulatory standard-setting, where cross-regional harmonization efforts will affect market entry timelines globally.

The UK's retail grocery market, valued at USD 342.0 Billion, confirms its relevance as a premium biotic food ingredient destination market. The Middle East is an early-awareness market where a Saudi Arabia survey found 51.8% of adults still rate their probiotic knowledge as low, representing a consumer education gap that patient early-entry brands can convert into first-mover loyalty before the category matures.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Consumer Behavior and Corporate Capital Accelerate Category Expansion

More than half of global consumers now actively choose biotic ingredients to improve health outcomes, according to 2026 functional food consumption data. As reported by Frontiers in Immunology, 72.5% of 1,306 surveyed adults associated regular prebiotic or probiotic use with immune system support, confirming that health benefit awareness extends well beyond digestive claims and into categories that command premium formulation budgets.

Novonesis registered 12.0% organic sales growth across emerging markets for its biosolutions portfolio in FY2024, as reported by Novonesis on February 26, 2025, showing that international volume expansion is outpacing mature market growth rates and broadening the commercial base for ingredient suppliers with global distribution.

Corporate acquisition activity confirms that this behavior shift is attracting capital at a scale that validates the long-term commercial thesis. PepsiCo acquired prebiotic soda brand Poppi for USD 1.95 Billion in 2025, signaling that multinationals now treat gut health consumer demand as a core beverage channel strategy rather than a niche premium play.

Danone's acquisition of The Akkermansia Company the same year shows that food majors are racing to secure next-generation microbiome assets before independent innovators scale them independently. Both moves compress the window for mid-tier ingredient suppliers to build brand equity with consumer-facing partners before the largest buyers lock in exclusive supply agreements.

Regulatory Burden and Strain Complexity Slow New Category Commercialization

Psychobiotic products targeting mental health face the most acute commercial barriers. Regulatory bodies require rigorous randomized placebo-controlled trial protocols before approving mental health efficacy claims, slowing the product pipeline for brain health biotics and forcing smaller companies to either partner with clinical research organizations or exit the segment entirely. This clinical bar concentrates brain health biotic development among well-capitalized suppliers and structurally limits how quickly the mental health application category can expand.

Yeast biotics face a separate constraint. Microbial stability and strain diversity limitations restrict formulation flexibility compared to bacterial formats. Suppliers relying on yeast-based platforms must invest in strain development programs to close this gap or accept a secondary market position in categories where bacterial probiotics already hold established clinical precedent and formulary preference.

Geriatric, Pet, and Cosmeceutical Segments Open New Revenue Streams

Lallemand Health Solutions launched its Cerenity probiotic blend targeting the gut-muscle axis for healthy aging in 2025, marking a deliberate pivot toward clinical geriatric nutrition. Aging populations in developed markets combine high purchasing power with growing preventive health spending, and early movers with validated strain data will command premium B2B pricing before the segment attracts larger competitor attention. Probi launched specialized probiotic varieties for pet digestive and oral health in 2025, tapping the companion animal humanization trend that mirrors human supplement premiumization in both willingness to pay and purchase frequency.

Cosmeceutical biotics represent a third parallel opportunity. South Korean producers integrating shelf-stable postbiotic preparations into dermo-cosmetics have created a new industrial buyer segment that now competes with food and pharma channels for the same ingredient supply. Suppliers that secure supply agreements across all three emerging verticals before any single one reaches mainstream adoption will build a diversified revenue base that is far more resilient to single-category demand fluctuations.

Market Trends

Synbiotic Combinations and Precision Strains Replace Single-Ingredient Formats

The market is moving from single-strain or single-category products toward compound biotic formats with defined clinical outcomes. Probi and Clasado launched commercial synbiotic formulas combining Bimuno GOS prebiotic with Defendum probiotics in 2024, signaling that ingredient suppliers now compete on combined efficacy data rather than individual strain performance alone.

PharmExtracta's targeted Colipral and Brevicillin bacterial strain drops for ulcerative colitis and pediatric applications, unveiled at CPHI 2025, confirm that precision strain positioning is becoming the primary B2B differentiation strategy. Early movers who build clinical dossiers for specific condition-linked formulations will secure supply agreements before the broader market standardizes around these formats and price competition intensifies.

Market Competition Overview

The global biotic ingredients market is moderately consolidated at the top, with a small group of large biosolution and specialty ingredient companies holding disproportionate share through proprietary strain libraries, clinical data portfolios, and global manufacturing infrastructure.

The January 2024 merger of Novozymes and Chr. Hansen into Novonesis, valued at USD 12.3 Billion, created the single largest biotic ingredient entity and reset competitive benchmarks for strain breadth and R&D capacity. Novonesis reported 5.0% organic sales growth within its Human Health biotic segment in FY2024, as reported by Novonesis on February 26, 2025, confirming that the combined entity is already converting scale into commercial momentum rather than absorbing integration disruption.

Below the top tier, mid-sized players are pursuing clinical differentiation and channel-specific partnerships to hold position. The emergence of pet health, geriatric nutrition, and cosmeceutical biotics as distinct commercial verticals creates sub-market structures where specialized entrants can build leadership positions before larger players redirect resources there. Companies without published multicenter clinical data face structural disadvantages in B2B procurement processes that increasingly require peer-reviewed performance validation before granting supplier access to formulation programs.

Company Profiles

Novonesis, formed through the completion of the Novozymes and Chr. Hansen merger, holds the strongest market position by strain library depth and global distribution reach. The combined entity brings together Chr. Hansen's human health probiotic strain library and Novozymes' biosolution scale, creating a supplier with unmatched clinical documentation depth.

As reported by Novonesis on February 25, 2026, the company delivered 7.0% broad-based organic sales growth in FY2025 with an adjusted EBITDA margin of 37.1%, confirming that integration is delivering financial performance without margin dilution. Its 2030 penetration target for the EUR 13 billion probiotic supplement market gives it the clearest long-range commercial roadmap of any player in this space.

dsm-firmenich competes through regulatory-first market entry and clinical application breadth across synbiotics, HMO prebiotics, and condition-specific formulations. The company revealed a clinically backed synbiotic capsule for IBS relief in July 2025, adding a condition-specific product to a portfolio already spanning metabolic and infant nutrition categories.

A USD 10 million facility modernization at its Schenectady site, completed in March 2026, reflects deliberate investment in precision delivery technology that positions the company to serve pharmaceutical and clinical nutrition channels requiring guaranteed bioavailability standards. Securing regulatory clearance in high-growth emerging markets before competitors gives dsm-firmenich a first-mover advantage in markets where ingredient approval timelines are long and distributor relationships are difficult to replicate quickly.

Key Players

- Novozymes (Chr. Hansen)

- dsm-firmenich (Koninklijke DSM N.V.)

- Lallemand Inc.

- Yakult Honsha Co., Ltd.

- Morinaga Milk Industry Co., Ltd.

- Probi AB

- Kerry Group PLC

- BioGaia AB

- OptiBiotix Health PLC

- FrieslandCampina Ingredients

- Beneo GmbH

- BASF SE

Supply Chain and Value Chain Analysis

The biotic ingredients value chain begins with microbial strain sourcing and fermentation, where the largest share of proprietary value is created. Companies with proprietary strain libraries and fermentation process expertise control the most defensible position in the chain. Downstream, value shifts to encapsulation and stabilization technology, which determines shelf life, bioavailability, and end-use format compatibility. Encapsulation capability is increasingly a B2B contract differentiator, as formulators in pharmaceutical and infant nutrition channels require guaranteed viable cell counts through packaging and distribution.

The biggest supply chain risk sits at the strain stability and cold-chain interface. Live bacterial formats require controlled temperature logistics that add cost and complexity across long international shipping routes. Kirin Holdings' overseas LC-Plasma volume growth of more than 200.0% year-on-year in FY2024, as reported by Kirin Holdings on February 14, 2025, reflects precisely how shelf-stable postbiotic formats remove logistical friction and unlock distribution scale in markets where cold-chain infrastructure is unreliable or prohibitively expensive. Postbiotics and heat-stable inactivated preparations are accelerating commercially in part because they solve a supply chain problem that live bacterial formats have not resolved.

Regulatory Landscape

Regulatory frameworks for biotic ingredients vary significantly by region and application channel, creating uneven market access timelines for suppliers. In India, dsm-firmenich secured approval for its GLYCARE 2FL HMO prebiotic ingredient in March 2025, confirming that human milk oligosaccharide ingredients are entering regulatory clearance in high-growth emerging markets. This approval matters commercially because India's infant nutrition sector represents one of the largest volume opportunities for HMO ingredients outside Europe and North America. Suppliers without proactive regulatory submissions in these markets face multi-year delays while approved competitors build distributor relationships and brand equity.

Regulatory bodies continue to enforce randomized placebo-controlled trial requirements before approving mental health efficacy claims for psychobiotics and brain health products, creating a high clinical bar that favors well-capitalized suppliers and limits smaller innovators from commercializing in this sub-category without partnership support.

At the international coordination level, the International Probiotics Association and Complementary Medicines Australia signed a regulatory memorandum of understanding in February 2026, signaling a push toward cross-border standard harmonization that will affect how probiotic health claims are substantiated and approved across member markets.

Investment and White Space Analysis

Capital is concentrating around two poles: large-scale consolidation at the top and clinical specialization in emerging sub-categories. Novonesis publicly targeted the EUR 13 billion probiotic supplement market as its 2030 penetration goal in February 2026, signaling where institutional investment within the sector is directed over the next five years. The clearest white space sits in geriatric nutrition, companion animal health, and cosmeceutical biotics, where all three verticals are commercially active but not yet dominated by any single supplier.

Regions with high growth potential and low current penetration represent the most accessible near-term entry points. A Saudi Arabia survey finding that 51.8% of surveyed adults report low probiotic awareness points to a consumer education gap that patient brand investors can convert into durable market share ahead of the category maturing. Lallemand's Innov'Biome Challenge open innovation funding scheme signals that even established mid-tier players recognize they cannot develop next-generation postbiotic and probiotic microorganisms internally at the pace Biotic Ingredients Market now requires, opening partnership and licensing opportunities for specialized innovators who lack distribution scale but hold proprietary strain assets.

Key Market Segments

By Type

- Bacterial Probiotics

- Yeast Probiotics

- Prebiotics

- Postbiotics

- Synbiotics

By Form

- Powders

- Granules

- Capsules

- Liquids

By Application

- Functional Food and Beverages

- Dietary Supplements

- Infant Nutrition

- Medical Food

- Pharmaceuticals

- Personal Care and Beauty Products

By Health Benefit

- Gut/Digestive Health

- Immune Health

- Brain Health

- Metabolic Health

- Beauty-from-Within

- Sports Nutrition

- Women's Health

By Manufacturing Technology

- Fermentation

- Centrifugation and Filtration

- Drying and Stabilization

- Encapsulation and Protection

- Inactivation and Cell Disruption

By Ingredient/Formulation

- Lactobacillus crispatus Ferment

- Lactobacillus Ferment

- Bifidobacterium Ferment Lysate

- Lactococcus Ferment Lysate

- Maltodextrin and Lactobacillus Ferment

- Other Fermented Biotic Ingredients

Recent Developments

- May 2026, ADM published optimized clinical documentation for postbiotic applications targeting women's health across specific life stages, advancing its positioning in the specialized women's nutrition ingredient segment.

- April 2026, PrecisionBiotics and Biocodex renewed their global probiotic expansion partnership, reinforcing combined distribution reach across key international markets and extending their joint commercial agreement.

- February 2026, International Probiotics Association and Complementary Medicines Australia. Regulatory MoU. The two organizations signed a memorandum of understanding to advance cross-border probiotic standard harmonization, with direct implications for health claim substantiation timelines across member markets.

- In September 2025, Kerry Group isolated and commercially launched human milk probiotic strains LC40 and BfM26 specifically for early-life nutrition applications, targeting the infant nutrition channel with clinically characterized strains.

- April 2025, DSM-Firmenich introduced a 3-month synbiotic supplementation protocol targeting chronic fatigue syndrome, adding a condition-specific clinical application to its growing portfolio of precision biotic formulations.

- January 2025, Debut launched BeautyORB, an AI-powered biotech innovation engine for skin-microbiome ingredient discovery, signaling that artificial intelligence tools are entering the biotic ingredient development pipeline at the earliest discovery stage.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 7.81 Billion |

| Market Value (2026) |

USD 8.47 Billion |

| Forecast Revenue (2035) |

USD 17.54 Billion |

| CAGR (2026–2035) |

8.5% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 – 2024 |

| Forecast Period |

2026 – 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Type (Bacterial Probiotics, Yeast Probiotics, Prebiotics, Postbiotics), By Form (Powders, Granules, Capsules, Liquids), By Application (Functional Food and Beverages, Dietary Supplements, Infant Nutrition, Medical Food, Pharmaceuticals, Personal Care and Beauty Products), By Health Benefit (Gut/Digestive Health, Immune Health, Brain Health, Metabolic Health, Beauty-from-within, Sports Nutrition, Women's Health), By Manufacturing Technology (Fermentation, Centrifugation and Filtration, Drying and Stabilization, Encapsulation and Protection, Inactivation and Cell Disruption), By Target Skin Microbiota (Lactobacillus crispatus Ferment, Maltodextrin and Lactobacillus Ferment) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

Novozymes (Chr. Hansen), dsm-firmenich (Koninklijke DSM N.V.), Lallemand Inc., Yakult Honsha Co. Ltd., Morinaga Milk Industry Co. Ltd., Probi AB, Kerry Group PLC, BioGaia AB, OptiBiotix Health PLC, FrieslandCampina Ingredients, Beneo GmbH, BASF SE |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF). |

Frequently Asked Questions

What is the biggest investment opportunity in the biotic ingredients market?

▾ The clearest near-term opportunity sits at the intersection of geriatric nutrition and postbiotic ingredient supply, where no single supplier currently dominates. The Middle East represents the highest-return geographic entry point, where the majority of surveyed adults still report low probiotic awareness and no established brand holds category leadership. Patient brand investors entering these markets now face minimal competitive pressure from established players.

Who are the top companies in the biotic ingredients market?

▾ Novonesis, formed through the merger of Novozymes and Chr. Hansen, holds the strongest combined position by strain library depth and global manufacturing scale. dsm-firmenich ranks alongside it through regulatory-first market entry and clinical application breadth across synbiotics, HMO prebiotics, and condition-specific formulations targeting IBS, metabolic health, and infant nutrition.

Which segment is growing fastest in Biotic Ingredients Market and why?

▾ PostbioticPostbiotics represent the fastest-moving type segment because shelf-stable inactivated formats remove cold-chain dependency, which accelerates international distribution and widens the addressable channel set beyond refrigerated retail. Bacterial Probiotics retain the dominant 66.3% revenue share in 2025 by breadth of clinical validation, but postbiotics are closing the gap fastest in overseas and cosmeceutical channels.s represent the fastest-moving type segment. Kirin Holdings generated over 28.0 billion from its LC-Plasma postbiotic series in FY2025, with overseas volume growing more than 200.0% year-on-year in FY2024. Their shelf-stable inactivated format removes cold-chain dependency, which accelerates international distribution and widens the addressable channel set beyond refrigerated retail.

Which region is growing fastest in Biotic Ingredients Market and why?

▾ Asia-Pacific leads both current volume and growth trajectory. South Korea's cosmeceutical biotic integration and India's newly opened HMO regulatory pathway add structural demand that no other region currently matches in breadth. Japan's domestic postbiotic beverage channel growth and China's expanding functional food market reinforce Asia-Pacific's position as the primary near-term volume driver.

What is the biggest challenge holding Biotic Ingredients Market back?

▾ Clinical validation requirements for psychobiotics and brain health claims remain the most binding commercial constraint. Randomized placebo-controlled trial protocols create multi-year development timelines that smaller innovators cannot fund independently, concentrating brain health biotic development among a handful of well-capitalized suppliers and slowing the mental health application segment's expansion relative to its addressable consumer demand.