Market Overview

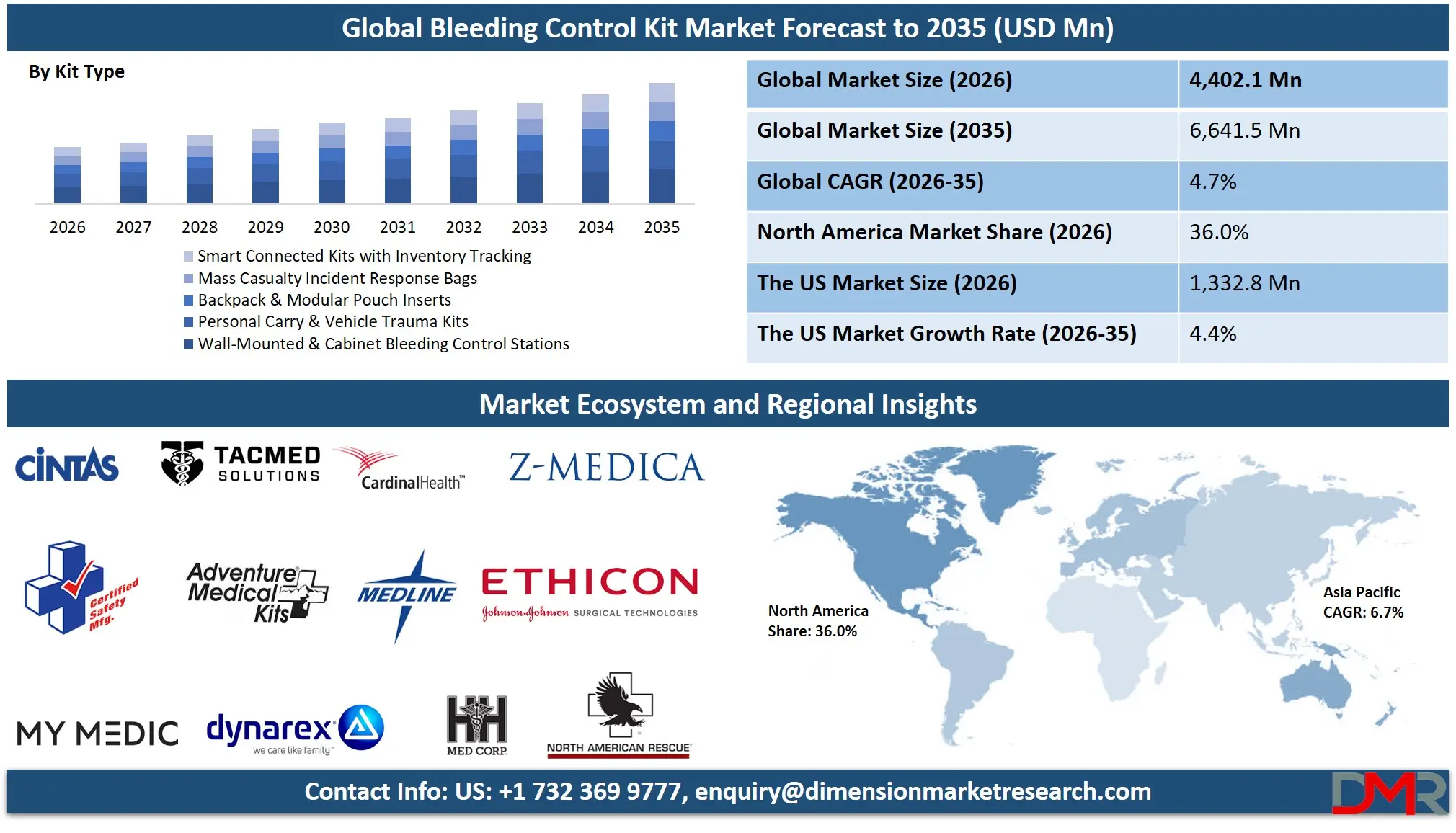

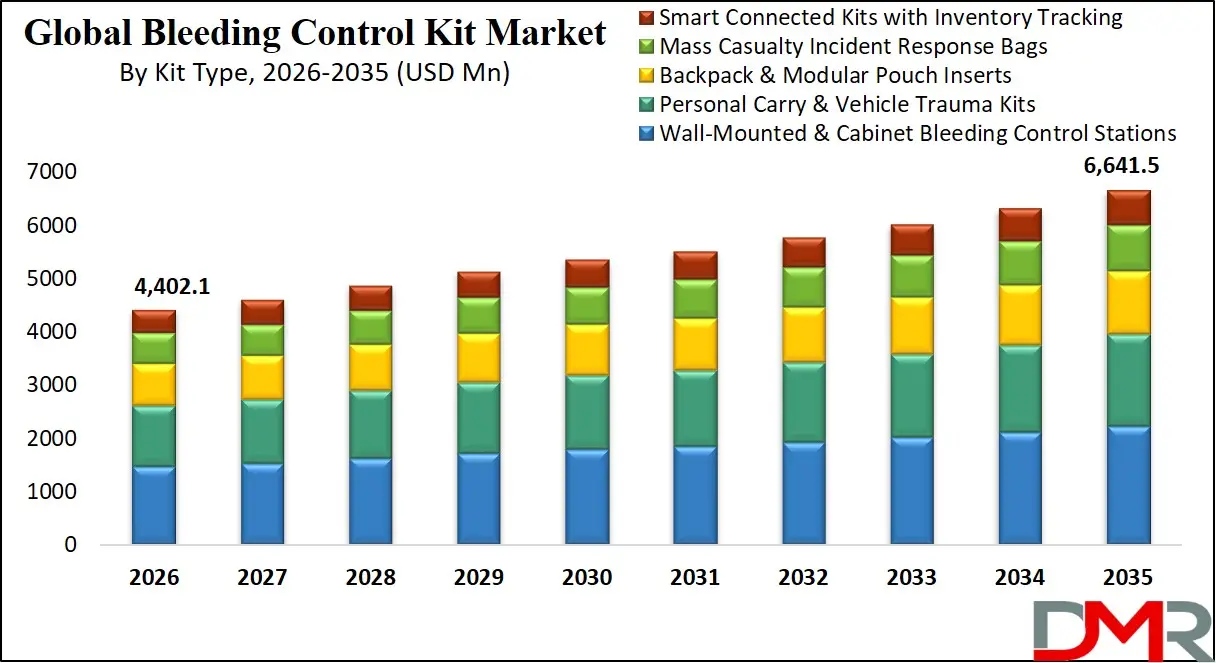

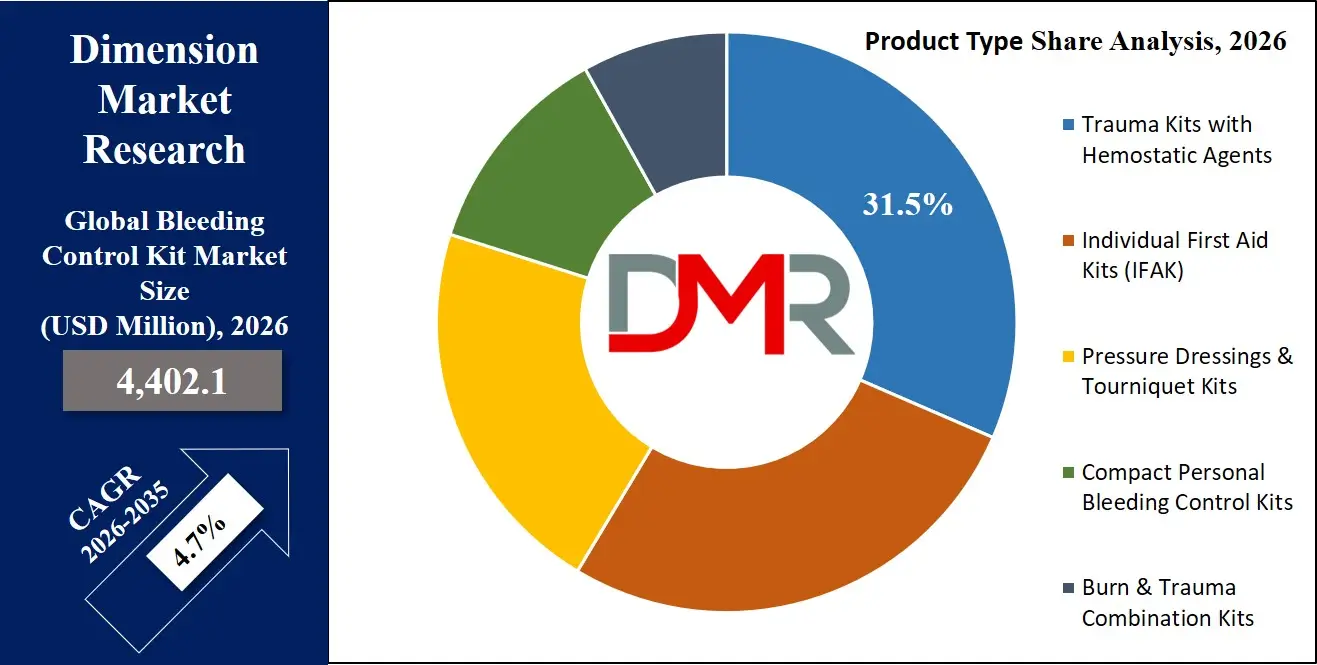

The Global Bleeding Control Kit Market is estimated to be valued at USD 4,402.1 million in 2026 and is projected to witness strong expansion over the forecast period. Growing at a compound annual growth rate (CAGR) of 4.7% from 2026 to 2035, the market is anticipated to reach approximately USD 6,641.5 million by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This growth reflects increasing demand for trauma care solutions, rising awareness regarding emergency preparedness, expanding adoption of public access bleeding control programs, and greater deployment of first-aid and hemorrhage control kits across hospitals, law enforcement agencies, military units, corporate facilities, educational institutions, and public spaces. The market expansion is further supported by advancements in hemostatic agents, tourniquets, and compression bandages, along with strengthening regulations promoting workplace and community safety initiatives worldwide.

Bleeding control kits enable rapid, effective hemorrhage management through intuitive component organization, military-grade hemostatic agents, windlass tourniquets, and compressed gauze engineered for deep wound packing. These solutions address critical pre-hospital care gaps related to emergency response times, bystander intervention capability, and preventable trauma deaths, supporting healthcare systems and public safety initiatives in reducing mortality from hemorrhagic injuries.

Technological advancements, including smart tourniquets with pressure sensors, RFID-enabled inventory tracking, extended shelf-life hemostatic formulations, vacuum-sealed compact packaging, and app-integrated instructional QR codes, are transforming the market into a scalable and highly accessible ecosystem. Integration of biocompatible hemostatic agents derived from chitosan and kaolin, alongside freeze-dried plasma components for advanced military and civilian use, is reshaping survivability outcomes in both tactical and austere environments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government mandates requiring bleeding control kits in federal buildings, K-12 schools, stadiums, and mass transit systems under initiatives like the Stop the Bleed campaign further accelerate global adoption. However, barriers such as lack of standardized training requirements, limited public awareness in developing regions, product expiration management challenges, and regulatory variability for hemostatic agents remain. Despite these limitations, the convergence of portable medical technology, public health policy, and community resilience programming positions bleeding control kits as a cornerstone of global civilian and tactical trauma response through 2035.

The US Bleeding Control Kit Market

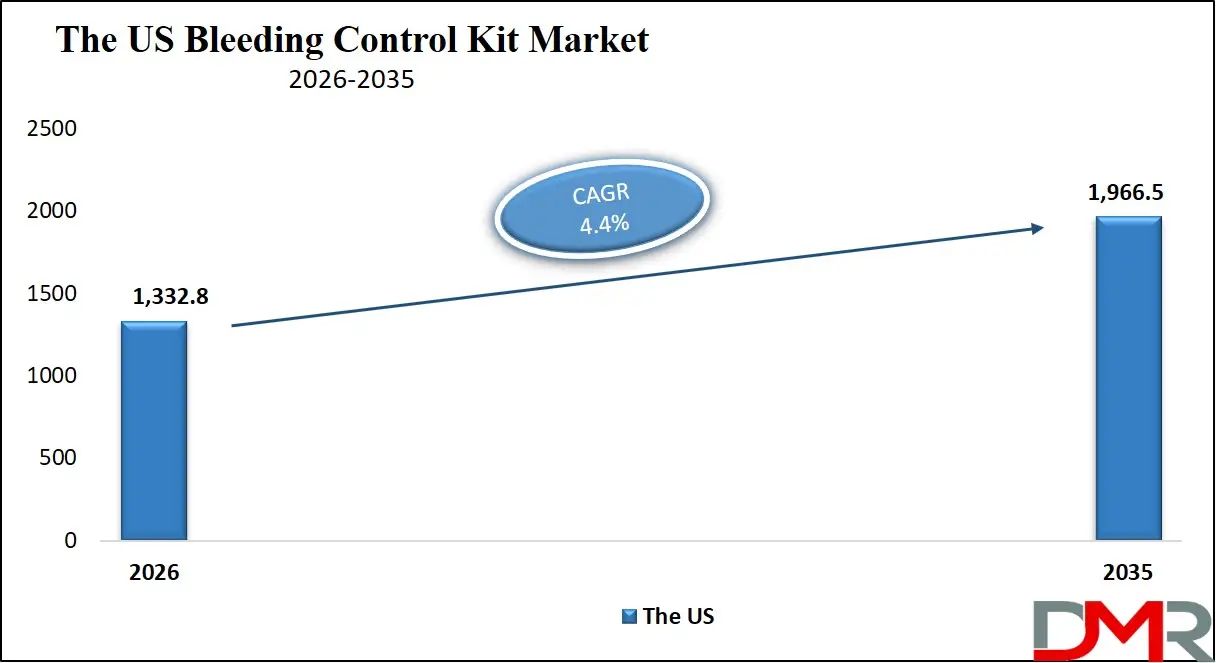

The U.S. Bleeding Control Kit Market is projected to reach USD 1,332.8 million in 2026 and grow at a CAGR of 4.4%, reaching USD 1,966.5 million by 2035. The U.S. leads global adoption due to its mature Stop the Bleed training infrastructure, robust school security funding, high rates of civilian firearm injury incidents, and strong emphasis on workplace safety compliance.

The national expansion of bleeding control cabinet installations in airports, corporate campuses, houses of worship, and sports venues, coupled with growing institutional demand from law enforcement and first responder agencies, fuels sustained market growth. Major distributors such as North American Rescue, H&H Medical, and Z-Medica are scaling production and innovating next-generation intuitive kit designs optimized for layperson use.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. federal support through Department of Homeland Security grants, CDC public health preparedness funding, and state-level school safety mandates encourages institutional procurement. Partnerships between medical device manufacturers and organizations like the American College of Surgeons continue to advance public education and kit accessibility.

The rapid rise of personalized compact kits for vehicle, backpack, and home use, integration with workplace emergency action plans, and development of connected tourniquets with real-time application feedback continues to redefine the U.S. public safety landscape, positioning the country as the global benchmark for civilian bleeding control readiness.

The Europe Bleeding Control Kit Market

The Europe Bleeding Control Kit Market is projected to be valued at approximately USD 1,232.6 million in 2026 and is projected to reach around USD 1,859.6 million by 2035, growing at a CAGR of about 4.7% from 2026 to 2035. Europe's leadership is anchored by strengthening civil protection mechanisms, increasing counter-terrorism preparedness, and harmonized medical device regulations across member states.

Countries such as Germany, the U.K., France, Italy, and Spain are widely adopting public access bleeding control programs, driven by elevated threat environments, mass transit security upgrades, and EU initiatives like rescEU stockpiling of medical countermeasures. The U.K.'s National Health Service trauma network integration and Germany's civil defense restructuring are particularly active in deploying bleeding control assets in high-density public areas.

Europe's aging volunteer emergency responder workforce, demand for standardized trauma training, and emphasis on interoperable medical equipment across borders further drive adoption. Funding through Horizon Europe resilience research and national interior ministry security contracts supports R&D in extended-duration hemostatic agents, compact deployable kits, and multilingual instructional interfaces.

Urban security upgrades in Paris metro stations, Berlin transport hubs, and London public squares increasingly deploy wall-mounted hemorrhage control cabinets, RFID-tracked inventory systems, and training manikins co-located with kit installations. With robust procurement frameworks, integration into workplace health and safety directives, and emphasis on community first responder empowerment, Europe remains one of the most advanced regions in public access bleeding control penetration.

The Japan Bleeding Control Kit Market

The Japan Bleeding Control Kit Market is anticipated to be valued at approximately USD 352.2 million in 2026 and is expected to attain nearly USD 531.3 million by 2035, expanding at a CAGR of about 4.7% during the forecast period. Japan's high prevalence of natural disasters including earthquakes and tsunamis, combined with an aging population vulnerable to traumatic falls, drives strong demand for distributed bleeding control assets in community disaster preparedness stockpiles.

The Fire and Disaster Management Agency (FDMA) actively supports civilian hemorrhage control training and equipment placement through national resilience planning, prefectural disaster medical stockpiles, and integration into school and senior care facility safety protocols. Japan's leadership in compact, lightweight emergency kit design and high-efficiency packaging accelerates innovation in ultra-portable bleeding control solutions suitable for residential units, small retail businesses, and personal disaster bags.

Japan's concept of "Community-Based Integrated Care Systems", supported by municipal governments and volunteer fire corps, integrates bleeding control assets into neighborhood emergency response hubs. Compact kits are being deployed in Tokyo metropolitan government buildings, Osaka train stations, and regional disaster evacuation centers. Japan's cultural emphasis on collective preparedness and meticulous emergency organization, combined with demographic urgency, positions the country as a high-growth innovator in civilian accessible hemorrhage control.

Global Bleeding Control Kit Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Bleeding Control Kit Market is expected to be valued at USD 4,402.1 million in 2026 and is projected to reach USD 6,641.5 million by 2035, showcasing rapid expansion supported by rising public safety investments and trauma preparedness awareness.

- High CAGR Driven by Civilian Access Programs: The market is expected to grow at an impressive CAGR of 4.7% from 2026 to 2035, fueled by accelerating Stop the Bleed style campaign rollouts, school security mandates, workplace safety modernization, and increasing frequency of natural disasters and mass casualty incidents worldwide.

- Strong Growth Trajectory in the United States: The U.S. Bleeding Control Kit Market stands at USD 1,332.8 million in 2026 and is projected to reach USD 1,966.5 million by 2035, expanding at a CAGR of 4.4% due to robust federal and state preparedness funding, high institutional adoption rates, and advanced medical device innovation.

- North America Maintains Regional Dominance: North America is expected to capture approximately 36.0% of the global market share in 2026, supported by mature emergency medical services infrastructure, significant public-private partnership investment, and early adoption of smart connected bleeding control technologies.

- Rapid Advancement in Bleeding Control Technologies: Innovations including pressure-indicating tourniquets, hemostatic gauze with extended shelf stability, integrated instructional augmented reality applications, and cloud-based cabinet inventory management are significantly accelerating accessibility, compliance, and survivability outcomes.

- Growing Mass Casualty Threats Boost Adoption: Rising global incidence of active shooter events, vehicular attacks, natural disasters, and industrial accidents, coupled with widening emergency response gaps in rural and underserved areas, is driving sustained demand for intuitive, immediate-use hemorrhage intervention solutions.

Global Bleeding Control Kit Market: Use Cases

- K-12 School Emergency Preparedness: Wall-mounted bleeding control cabinets installed in hallways and cafeterias enable staff and resource officers to access tourniquets and wound packing supplies within critical seconds during campus emergencies.

- Mass Transit & Transportation Hubs: RFID-inventoried kits positioned in airport terminals, subway stations, and railway concourses provide commuters and security personnel immediate hemorrhage intervention tools prior to EMS arrival.

- Workplace & Industrial Safety Compliance: Bleeding control stations integrated into OSHA-driven first aid programs in manufacturing plants, warehouses, and corporate offices address laceration and amputation risks from heavy machinery.

- Law Enforcement & Tactical Operations: Compact personal trauma kits worn on duty belts and vehicle-stocked response bags equip officers with immediate care capabilities for self-aid or partner rescue in ballistic and edged weapon environments.

- Outdoor Recreation & Remote Wilderness: Ultra-lightweight, weather-sealed bleeding control kits designed for backcountry hiking, climbing expeditions, and hunting trips provide essential hemorrhage management in prolonged evacuation scenarios.

Global Bleeding Control Kit Market: Stats & Facts

U.S. Centers for Disease Control and Prevention (CDC)

- In 2023, over 227,000 deaths in the U.S. were caused by unintentional injuries.

- Injury is the leading cause of death for individuals aged 1–44 years in the U.S.

- There were approximately 43 million emergency department visits due to injuries in a recent reporting year.

- About 26 million emergency visits annually are due to unintentional injuries.

- The U.S. injury death rate is approximately 89 deaths per 100,000 population.

- Firearm-related deaths exceeded 46,000 annually, many involving severe bleeding.

- Motor vehicle crashes account for over 40,000 deaths annually in the U.S.

- Falls result in more than 3 million emergency department visits annually among older adults.

- Traumatic injuries contribute significantly to premature mortality and disability nationwide.

World Health Organization (WHO)

- Injuries cause approximately 4.4 million deaths globally every year.

- Road traffic injuries account for about 1.2–1.3 million deaths annually worldwide.

- Injuries represent nearly 8% of all global deaths.

- Violence contributes to roughly 1.25 million deaths annually.

- Injuries are among the top five causes of death for people aged 5–29 years globally.

- Postpartum hemorrhage causes approximately 70,000 maternal deaths annually worldwide.

- Trauma accounts for nearly 9% of global mortality.

- Injuries contribute to around 10% of years lived with disability globally.

American College of Surgeons (ACS) – Stop the Bleed Initiative

- More than 5 million individuals worldwide have received Stop the Bleed training.

- At least 14 U.S. states have enacted legislation supporting bleeding control kits and training.

- Research analysis of homicide cases showed that approximately 1–2% of deaths might have been preventable with rapid hemorrhage control.

- A significant portion of penetrating trauma victims have extremity injuries where tourniquet use could be lifesaving.

National Institutes of Health (NIH) / National Library of Medicine (Government Research Data)

- Hemorrhage is responsible for approximately 30–40% of trauma-related deaths.

- Up to 50% of trauma deaths from bleeding occur before hospital arrival.

- Severe trauma leads to over 5 million deaths globally each year.

- Hemorrhage is the leading preventable cause of death after traumatic injury.

- Around 70% of deaths within the first 24 hours of trauma are linked to uncontrolled bleeding.

National Highway Traffic Safety Administration (NHTSA)

- Motor vehicle crashes result in over 2.6 million injuries annually in the U.S.

- Traffic crashes remain a leading cause of traumatic hemorrhage-related emergency cases.

Global Bleeding Control Kit Market: Market Dynamic

Driving Factors in the Global Bleeding Control Kit Market

Mass Casualty Preparedness Imperative

The rising frequency and severity of mass casualty incidents including active shooter events, vehicular terror attacks, and natural disasters represent a primary driver for bleeding control kit adoption. Governments, school districts, and private venue operators are increasingly mandated to deploy immediate hemorrhage intervention assets as a component of layered security and resilience planning. The public expectation of survivability through bystander intervention has elevated bleeding control kits from niche medical products to essential civic infrastructure, accelerating institutional procurement cycles.

Technology Innovation and Accessibility

Bleeding control kit innovation has shifted decisively toward layperson usability and extended field durability. Advancements in hemostatic agent carrier materials, compact windlass mechanisms, puncture-resistant packaging, and integrated visual/audio instructions lower the barrier to effective use by untrained bystanders. Smart tourniquets with embedded application timing sensors and cloud-connected cabinet inventory systems enable real-time readiness monitoring. The convergence of biomaterials engineering, intuitive industrial design, and digital health connectivity makes bleeding control more accessible and reliable than ever before.

Restraints in the Global Bleeding Control Kit Market

Training Gaps and Psychological Barriers

Even when kits are ubiquitously available, lack of hands-on training and psychological hesitation during actual emergencies significantly limit real-world effectiveness. Many bystanders, despite public awareness campaigns, remain unwilling or unable to apply tourniquets or pack wounds under extreme stress. This training deficit is particularly acute in developing regions and rural communities without sustained Stop the Bleed program penetration, creating a critical gap between equipment availability and lifesaving outcomes.

Expiration Management and Lifecycle Costs

Bleeding control kit components, particularly hemostatic gauze and sterile dressings, carry finite shelf lives requiring systematic inspection, rotation, and replacement. Large-scale deployments across hundreds of school or transit locations present substantial logistical burdens for facility managers unprepared for medical asset lifecycle management. The recurring cost of replenishment, combined with initial procurement expense, can deter sustained adoption among budget-constrained public agencies and smaller private entities.

Opportunities in the Global Bleeding Control Kit Market

Expansion into Emerging Economy Public Health Infrastructure

Rapidly urbanizing regions across Southeast Asia, Latin America, and Sub-Saharan Africa represent major growth frontiers as governments upgrade emergency medical response capacity and workplace safety regulations. Partnerships with international NGOs, disaster relief organizations, and development banks can accelerate kit distribution alongside first responder training programs. Localized manufacturing and ultra-low-cost compact kit variants tailored to regional threat profiles and purchasing power constraints can unlock massive volume-driven expansion.

Smart Kit Ecosystems and Predictive Resupply

Integration of IoT sensors, RFID item-level tracking, and cloud-based inventory platforms creates recurring revenue opportunities through automated resupply subscriptions and predictive analytics for kit placement optimization. Data generated from kit utilization patterns, even in training contexts, can inform public health authorities on emerging injury trends and geographic response gaps. This transforms bleeding control kits from static consumables into intelligent nodes within broader community resilience data networks.

Trends in the Global Bleeding Control Kit Market

Hybrid Military-Civilian Technology Transfer

Advanced hemostatic agents, junctional wound devices, and intraosseous access tools developed for battlefield use are rapidly migrating into civilian trauma protocols and commercial kit configurations. This accelerated transfer pathway, enabled by collaborative research between defense medical agencies and commercial manufacturers, places once-restricted technologies into the hands of civilian first responders and educated laypersons, significantly elevating pre-hospital care capabilities.

Customization and Demographic-Specific Kits

Market segmentation is deepening with kits specifically engineered for pediatric settings, geriatric care facilities, wilderness expeditions, and marine environments. Demographic-specific component selection, packaging ergonomics, and instructional design improve usability and clinical appropriateness across diverse user populations. This trend reflects maturation beyond one-size-fits-all configurations toward precision public health deployment of hemorrhage control assets.

Global Bleeding Control Kit Market: Research Scope and Analysis

By Product Type Analysis

Trauma Kits with Hemostatic Agents are projected to dominate the Product Type segment of the Global Bleeding Control Kit Market. This dominance is driven by the clinical superiority of advanced hemostatic dressings infused with kaolin or chitosan over conventional gauze in controlling severe, life-threatening hemorrhage. Military combat casualty care data demonstrating dramatically improved survival rates with hemostatic agent use has accelerated adoption across civilian tactical medicine, law enforcement, and high-risk industrial sectors. These kits, while priced at a premium, are increasingly specified in institutional procurement tenders and grant-funded public safety deployments where efficacy outweighs unit cost considerations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

While Pressure Dressings & Tourniquet Kits represent the historical backbone of extremity hemorrhage control and remain widely distributed, their relative share is moderating as comprehensive trauma kits incorporating multiple intervention modalities become the institutional standard. Individual First Aid Kits or IFAKs, originating from military individual gear, have successfully crossed over into civilian personal carry, vehicle, and workplace markets, yet remain smaller in average unit value compared to institutional-grade trauma kits. Compact Personal Bleeding Control Kits represent the fastest-growing consumer segment, driven by parental anxiety, outdoor recreation demand, and concealed carriers seeking everyday carry medical capability. However, the institutional procurement volumes and higher price points of hemostatic agent-enhanced trauma kits secure their leading revenue position throughout the forecast period.

By Kit Type Analysis

Wall-Mounted & Cabinet Bleeding Control Stations are projected to dominate the global market, fundamentally transforming hemorrhage response from a specialized medical intervention into ubiquitously accessible public safety infrastructure. Their dominance stems from an unparalleled value proposition for high-occupancy, high-traffic environments such as schools, airports, stadiums, corporate campuses, and government buildings. By positioning bleeding control assets visibly and immediately adjacent to potential incident zones, these stations reduce time-to-treatment from minutes to seconds, directly addressing the survivability window for exsanguinating hemorrhage. The driving forces behind their market leadership are tri-fold: accelerating legislative mandates requiring kit placement in public facilities, growing awareness that bystanders will not search for medical supplies, and the declining cost premium of purpose-designed cabinetry with integrated alarm and inventory tracking capabilities. As public venues compete to demonstrate safety stewardship, the economic and reputational case for permanent, visible kit installations becomes compelling, solidifying these systems as the cornerstone of civilian bleeding control infrastructure.

Personal Carry & Vehicle Trauma Kits form the crucial and substantial second-largest segment, effectively bridging the gap between fixed installation and individual mobility. These systems, typically compact soft packs or pouches designed for glove compartments, backpacks, and duty belts, cater to security-conscious citizens, outdoor professionals, law enforcement officers, and parents. Their strength lies in immediate personal accessibility, ensuring the individual has hemorrhage control capability irrespective of whether fixed cabinets are present. By empowering the individual rather than relying solely on facility infrastructure, this segment addresses the reality that trauma can occur anywhere, from remote trailheads to unsecured retail environments. This balance of portability and preparedness makes personal kits the primary entry point for first-time buyers and sustained consumer market growth. As such, personal carry configurations will remain indispensable, meeting the nuanced needs of a mobile society where trauma does not confine itself to locations with pre-installed equipment.

By Application Analysis

Civilian Public Access & Workplace Safety is poised to be the largest and most dominant application segment for bleeding control kits, driven by powerful global regulatory and societal trends. The relentless expansion of active assailant preparedness programs in K-12 schools and university campuses creates a perfect use case: predictable high-occupancy facilities with demonstrated vulnerability. This institutionalization of medical readiness is where bleeding control kit adoption scales exponentially, ensuring standardized equipment across thousands of geographically dispersed sites. The segment is also acutely reinforced by OSHA-driven workplace first aid modernization, evolving beyond basic bandaging to include severe hemorrhage response capability in manufacturing, logistics, and corporate environments. Beyond compliance, employers recognize bleeding control kits as tangible evidence of workforce safety commitment, directly impacting employee retention and liability reduction. From district-wide school implementations to Fortune 500 headquarters installations, the operational and reputational pressures in civilian public access make bleeding control kit adoption not merely advisable but increasingly mandated by insurers and regulators.

Law Enforcement & Military Tactical Application ranks as the second-largest application segment, fueled by its own distinct procurement imperatives. Tactical operators require compact, ruggedized, intuitively organized trauma kits capable of immediate self-application or buddy care under fire. The precision and reliability requirements of hemostatic agents and tourniquets designed for ballistic and blast injuries directly address survivability in high-threat environments. Furthermore, the scale of federal defense and homeland security budgets justifies premium component selection and continuous product iteration based on battlefield after-action reporting. While more constrained in total unit volume compared to civilian mass deployment, the high per-kit value, recurring individual issue to personnel, and sustained global counterterrorism and peacekeeping commitments secure the tactical segment's role as an enduring, high-margin market pillar.

By End User Analysis

Government & Public Works Agencies are anticipated to dominate the market as the primary drivers and beneficiaries of bleeding control kit integration. These entities possess the legislative authority to mandate kit placement, the budgetary scale to execute nationwide procurement programs, and the jurisdictional responsibility for public safety outcomes. For them, adoption is a strategic imperative to demonstrate proactive threat mitigation, satisfy constituent expectations for security, and reduce the mortality burden on emergency medical systems. Federal, state, and municipal agencies serve as essential anchor customers for manufacturers, providing predictable, high-volume demand signals that justify production scaling. Their focus on standardization, interoperability, and auditable deployment records aligns perfectly with the maturation of connected cabinet technologies and centralized inventory management platforms. This control over public safety asset distribution enhances their overall emergency preparedness posture and crisis response credibility.

Institutional End Users including School Districts, Transportation Authorities, and Private Venue Operators represent the vital second-largest end-user segment, for whom bleeding control adoption is a strategic response to acute vulnerability perception. Confronted with heightened threat warnings, media scrutiny following high-profile incidents, and stakeholder demands for visible security enhancements, these entities are turning to comprehensive bleeding control programs to differentiate their safety posture and fulfill duty of care obligations. For them, a turnkey solution encompassing equipment, cabinet hardware, staff training, and replenishment contracts represents an administratively manageable path to preparedness. Adoption in this segment is often accelerated following proximate incidents or via parent advocacy groups demanding action. By mastering bleeding control readiness, these institutions future-proof their reputations, transitioning from passive facility managers to active community resilience contributors.

The Global Bleeding Control Kit Market Report is segmented on the basis of the following:

By Product Type

- Trauma Kits with Hemostatic Agents

- Individual First Aid Kits (IFAK)

- Pressure Dressings & Tourniquet Kits

- Compact Personal Bleeding Control Kits

- Burn & Trauma Combination Kits

By Kit Type

- Wall-Mounted & Cabinet Bleeding Control Stations

- Personal Carry & Vehicle Trauma Kits

- Backpack & Modular Pouch Inserts

- Mass Casualty Incident Response Bags

- Smart Connected Kits with Inventory Tracking

By Application

- Civilian Public Access & Workplace Safety

- Law Enforcement & Military Tactical

- Wilderness & Remote Expedition

- Sports & Athletic Training Facilities

- Residential & Home Preparedness

By End User

- Government & Public Works Agencies

- Institutional End Users (Schools, Transit, Venues)

- Industrial & Corporate Enterprises

- Law Enforcement & Defense Agencies

- Individual Consumers & Outdoor Enthusiasts

Impact of Artificial Intelligence in the Global Bleeding Control Kit Market

- AI for Kit Placement Optimization: AI models analyze historical crime data, incident density mapping, and foot traffic patterns to recommend optimal positioning of wall-mounted bleeding control cabinets, maximizing accessibility and projected utilization rates across municipalities and large campuses.

- AI-Driven Training & Augmented Reality Instruction: Computer vision and AR applications guide laypersons through tourniquet application and wound packing sequences using smartphone cameras, providing real-time feedback on technique accuracy and compression adequacy without requiring live instructors.

- Predictive Inventory & Expiration Management: AI algorithms predict consumption rates, forecast resupply needs, and optimize expiration rotation schedules across distributed cabinet networks, reducing waste and ensuring continuous readiness across thousands of installation sites.

- Smart Tourniquet Application Analytics: Embedded sensors capture tourniquet application time, pressure metrics, and environmental conditions during both training and actual use, feeding aggregated data to device manufacturers for continuous design improvement and clinical protocol refinement.

- Incident Forensics and Response Reconstruction: AI-enabled analysis of utilization data from connected kits deployed at actual trauma events provides emergency medical directors with detailed response timelines and intervention sequence reconstruction, informing future training priorities and equipment modifications.

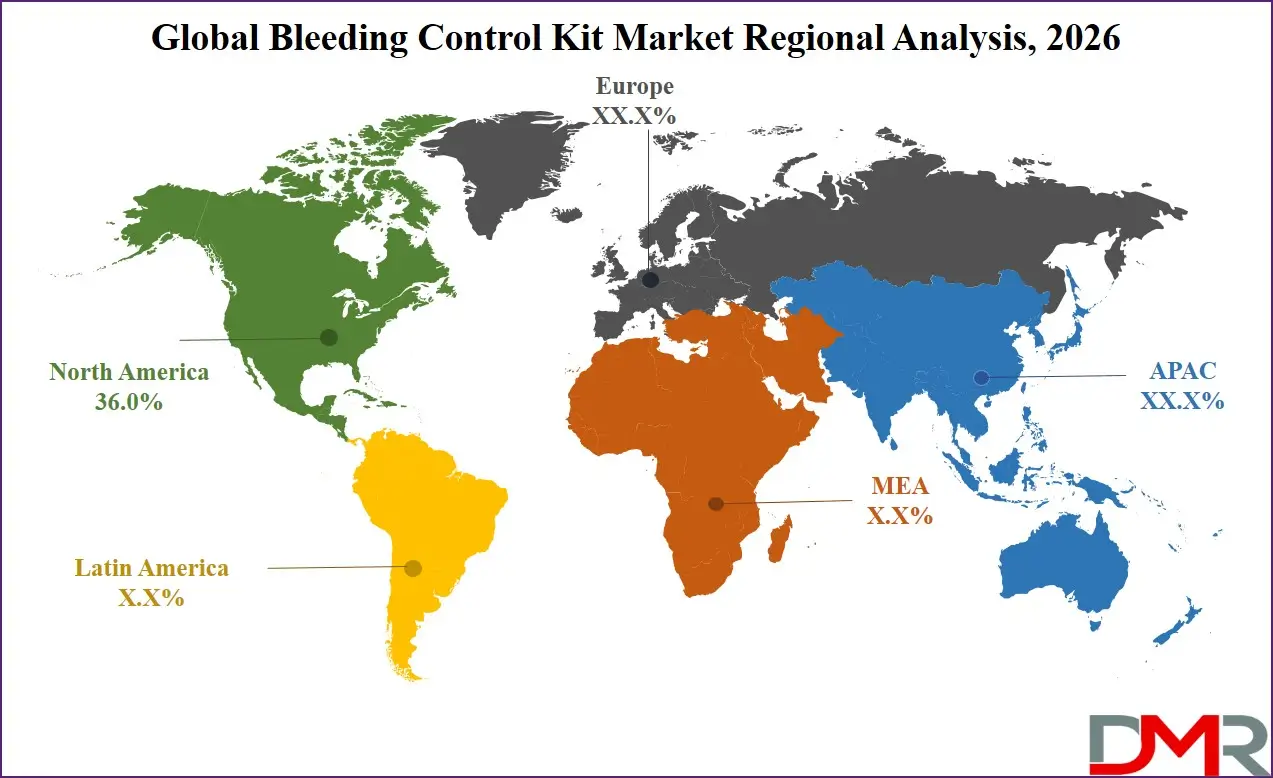

Global Bleeding Control Kit Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to dominate the Global Bleeding Control Kit Market with 36.0% of market share by the end of 2026, owing to a powerful combination of high threat awareness, mature Stop the Bleed program infrastructure, robust federal and state preparedness funding, and the presence of dominant medical device innovators. The United States and Canada have rapidly integrated bleeding control assets into school security protocols, workplace safety frameworks, and public venue resilience planning. Major distributors and manufacturers are scaling production capacity and distribution networks to meet sustained institutional and consumer demand.

The region's active shooter preparedness imperative, coupled with elevated civilian firearm injury rates and expansive wilderness recreation, creates a durable multi-channel demand environment. Supportive federal grant programs and gradual liability-driven adoption in corporate sectors further solidify North America's leadership position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR and is poised to achieve rapid market share growth due to its massive population density, accelerating disaster resilience investments, and emerging workplace safety regulatory frameworks. Countries like China, India, Japan, and Australia are investing heavily in public access defibrillation and bleeding control co-deployment strategies. China's Healthy China 2030 initiative and India's National Disaster Management Authority guidelines are creating fertile ground for government and institutional adoption. The region's cost sensitivity is being addressed through domestic manufacturing partnerships, NGO-facilitated donation programs, and scaled basic kit configurations optimized for mass distribution. This, combined with immense urbanization-driven infrastructure development and natural disaster exposure, positions APAC as the fastest-growing market for bleeding control systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Bleeding Control Kit Market: Competitive Landscape

The Global Bleeding Control Kit Market is moderately consolidated, featuring a mix of established medical device manufacturers, specialized tactical medical suppliers, and consumer first aid brands expanding into trauma preparedness. Leading medical equipment players Johnson & Johnson, 3M, and Cardinal Health are leveraging their vast distribution networks and healthcare provider relationships to capture institutional market share. Pure-play tactical medical innovators such as North American Rescue, H&H Medical, and TacMed Solutions are driving market dynamics with mission-driven product development focused on combat casualty care standards.

Consumer lifestyle and outdoor brands like Adventure Medical Kits and MyMedic play increasingly influential roles in expanding the personal carry and vehicle kit segments through direct-to-consumer marketing and influencer partnerships. Traditional first aid kit manufacturers are also entering the space through strategic acquisitions and white-label partnerships, aiming to capture bleeding control-specific procurement contracts.

Some of the prominent players in the Global Bleeding Control Kit Market are:

- North American Rescue

- H&H Medical Corporation

- Z-Medica Corporation

- Johnson & Johnson (Ethicon)

- 3M Company

- Cardinal Health, Inc.

- Medline Industries, LP

- Dynarex Corporation

- TacMed Solutions

- Adventure Medical Kits

- MyMedic

- Certified Safety Manufacturing

- Cintas Corporation

- Stryker Corporation (Physio-Control)

- Teleflex Incorporated

- SAM Medical Products

- First Care Products

- REV MEDX, Inc.

- Rescue Essentials

- NAR Summit

- Other Key Players

Recent Developments in the Global Bleeding Control Kit Market

- November 2025: Z-Medica announced FDA 510(k) clearance for its QuikClot Control+ XR extended-residence hemostatic dressing, featuring improved clot adhesion and 36-month shelf stability, significantly reducing replacement cycle costs for institutional customers.

- October 2025: North American Rescue unveiled NAR Shield, an IoT-enabled bleeding control cabinet system with real-time RFID inventory tracking, automated resupply ordering, and remote tamper/status alerting for large-scale school and transit authority deployments.

- September 2025: 3M completed the acquisition of a leading specialist in compact hemostatic dressing and pressure bandage technologies, strengthening its acute wound care portfolio and public safety market access.

- August 2025: H&H Medical secured a multi-year framework agreement to supply standardized bleeding control kits for civilian crisis response stockpiles across multiple NATO member nations, marking significant transatlantic market expansion.

- July 2025: The American College of Surgeons announced that Stop the Bleed training courses have now reached over 4 million cumulative participants globally, driving sustained demand for practice tourniquets and institutional kit procurement.

- June 2025: MyMedic announced a national retail placement agreement with a major U.S. big-box chain for its compact personal bleeding control kits, signaling mainstream consumer market maturation and accessibility expansion.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 4,402.1 Mn |

| Forecast Value (2035) |

USD 6,641.5 Mn |

| CAGR (2026–2035) |

4.7% |

| The US Market Size (2026) |

USD 1,332.8 Mn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Trauma Kits with Hemostatic Agents, Individual First Aid Kits (IFAK), Pressure Dressings & Tourniquet Kits, Compact Personal Bleeding Control Kits, Burn & Trauma Combination Kits), By Kit Type (Wall-Mounted & Cabinet Bleeding Control Stations, Personal Carry & Vehicle Trauma Kits, Backpack & Modular Pouch Inserts, Mass Casualty Incident Response Bags, Smart Connected Kits with Inventory Tracking), By Application (Civilian Public Access & Workplace Safety, Law Enforcement & Military Tactical, Wilderness & Remote Expedition, Sports & Athletic Training Facilities, Residential & Home Preparedness), By End User (Government & Public Works Agencies, Institutional End Users (Schools, Transit, Venues), Industrial & Corporate Enterprises, Law Enforcement & Defense Agencies, Individual Consumers & Outdoor Enthusiasts) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

North American Rescue, H&H Medical Corporation, Z-Medica Corporation, Johnson & Johnson (Ethicon), 3M Company, Cardinal Health, Inc., Medline Industries, LP, Dynarex Corporation, TacMed Solutions, Adventure Medical Kits, MyMedic, Certified Safety Manufacturing, Cintas Corporation, Stryker Corporation (Physio-Control), Teleflex Incorporated, SAM Medical Products, First Care Products, REV MEDX, Inc., Rescue Essentials, NAR Summit, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Bleeding Control Kit Market?

▾ The Global Bleeding Control Kit Market size is estimated to have a value of USD 4,402.1 million in 2026 and is expected to reach USD 6,641.5 million by the end of 2035.

What is the growth rate in the Global Bleeding Control Kit Market in 2026?

▾ The market is growing at a CAGR of 4.7 percent over the forecasted period of 2026-2035.

What is the size of the US Bleeding Control Kit Market?

▾ The US Bleeding Control Kit Market is projected to be valued at USD 1,332.8 million in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 1,966.5 million in 2035 at a CAGR of 4.4%.

Which region accounted for the largest Global Bleeding Control Kit Market?

▾ North America is expected to have the largest market share in the Global Bleeding Control Kit Market with a share of about 36.0% in 2026.

Who are the key players in the Global Bleeding Control Kit Market?

▾ Some of the major key players in the Global Bleeding Control Kit Market are North American Rescue, H&H Medical Corporation, Z-Medica Corporation, Johnson & Johnson, 3M Company, Cardinal Health, Inc., and many others.