Market Overview

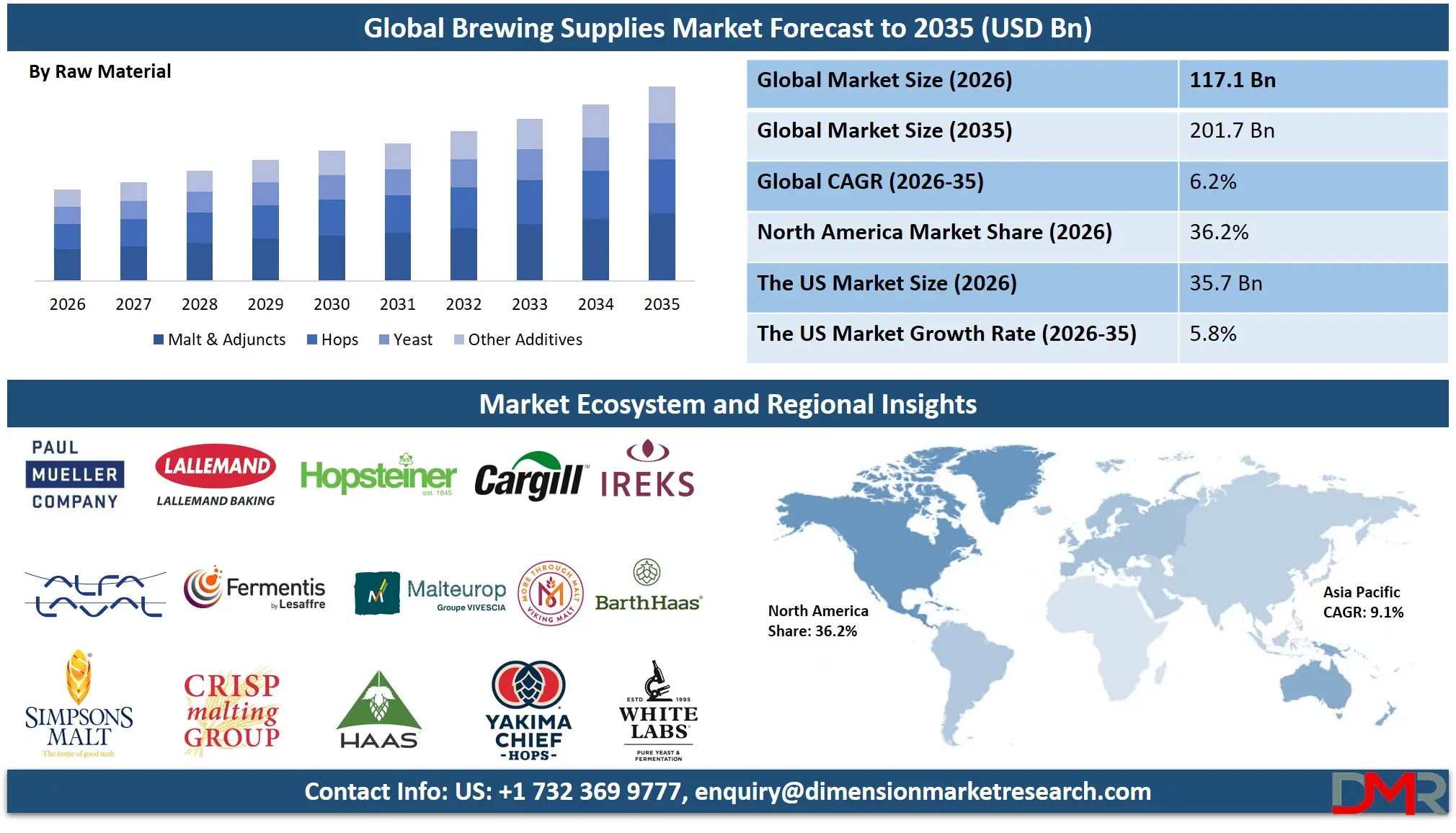

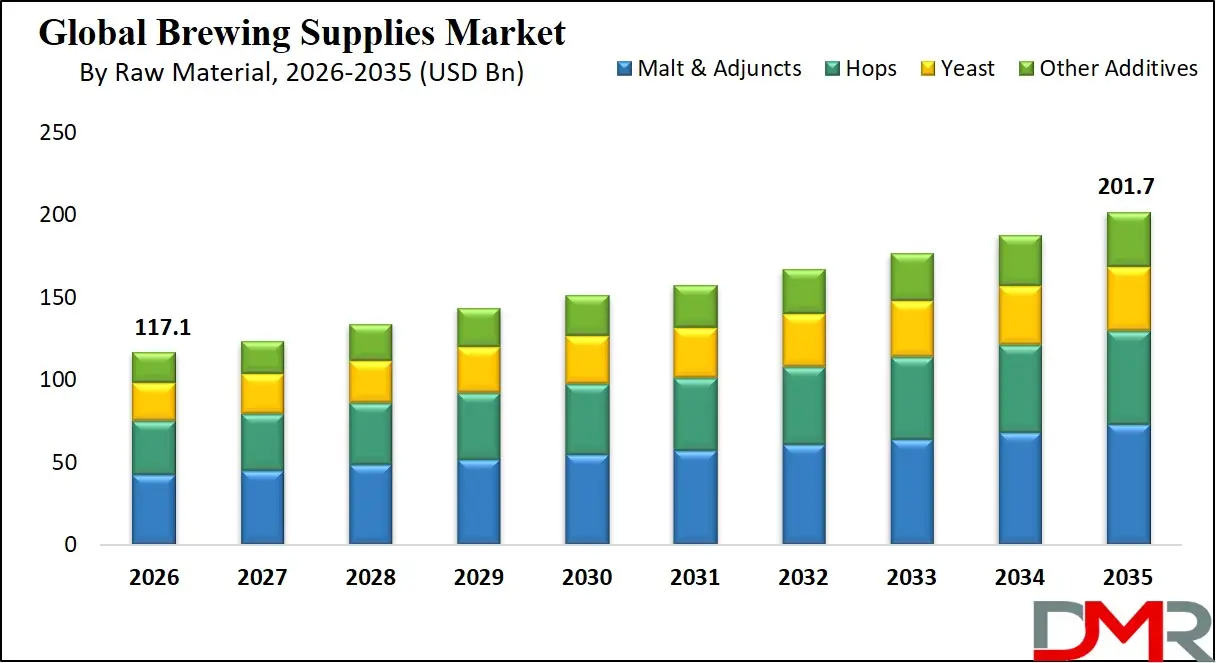

The Global Brewing Supplies Market is set for substantial expansion, reaching an estimated USD 117.1 billion in 2026 and projected to grow at a strong CAGR of 6.2% from 2026 to 2035, to the market value of USD 201.7 billion by 2035. This robust growth trajectory is fueled by the accelerating adoption of automated brewing technologies, specialty malt and hop varieties, advanced fermentation systems, and integrated quality control platforms across the brewing industry.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Rising consumer demand for craft beers, premium lagers, non-alcoholic brews, and experimental flavor profiles is compelling breweries to implement advanced brewing equipment, ingredient sourcing frameworks, and quality assurance protocols. The rapid expansion of microbreweries, brewpubs, craft brewing collectives, contract brewing operations, and home brewing communities is significantly increasing demand for reliable brewing supply chains.

Additionally, growing regulatory compliance requirements related to food safety standards, alcohol production licensing, sustainability mandates, and ingredient traceability are further accelerating market adoption. Breweries are increasingly integrating automated mash tuns, precision fermentation vessels, centrifuge systems, kegging lines, and AI-driven quality monitoring solutions to enhance production efficiency and prevent batch inconsistencies.

Cloud-based brewery management systems, IoT-enabled equipment monitoring, and scalable ingredient procurement platforms are enabling enterprises and small-scale brewers to implement cost-effective and globally accessible brewing solutions. As artisanal food movements dominate consumer preferences and craft beer penetration continues to rise worldwide, the Brewing Supplies Market is expected to witness sustained double-digit growth through 2035, driven by product innovation and premiumization initiatives.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government initiatives promoting local agricultural sourcing, craft beverage tourism, and export facilitation further accelerate global adoption. However, barriers such as fluctuating raw material prices (barley, hops), supply chain disruptions, reliance on agricultural yield quality, and the rising complexity of flavor customization remain. Despite these limitations, the convergence of agricultural science, brewing technology, and automated production systems positions brewing supplies as a central pillar of global beverage innovation through 2035.

The US Brewing Supplies Market

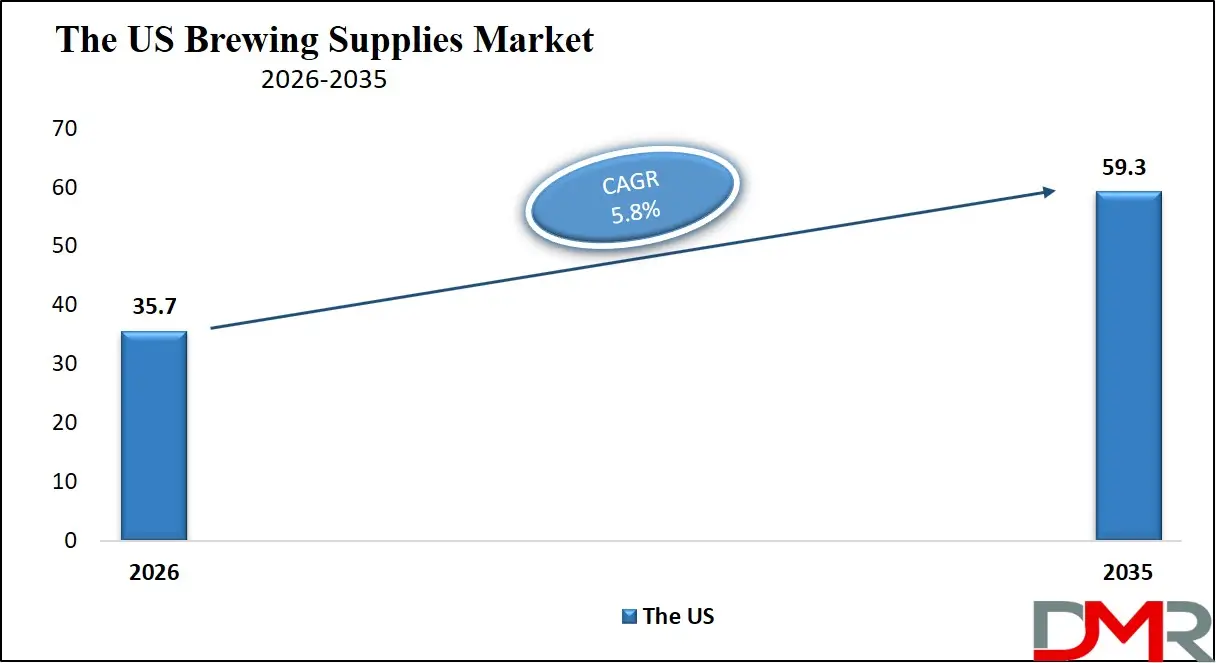

The U.S. Brewing Supplies Market is projected to reach USD 35.7 billion in 2026 and grow at a CAGR of 5.8%, reaching USD 59.3 billion by 2035. The U.S. leads global adoption due to its mature craft beer ecosystem, high per capita consumption of specialty brews, and a strong network of brewing equipment manufacturers and ingredient suppliers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The proliferation of microbreweries and taprooms across all 50 states, coupled with consumers' expectation of variety and authenticity, fuels demand for diverse malt profiles, experimental hop varieties, and specialized yeast strains. Major brewing equipment suppliers, ingredient distributors, and craft brewery collectives are integrating advanced supply chain solutions to mitigate risks during seasonal ingredient shortages and production scale-ups.

U.S. regulatory support for small brewery excise tax reductions, alongside frameworks like the Craft Beverage Modernization Act, encourages investment in brewing infrastructure. The market is witnessing a shift toward direct-to-consumer ingredient sales and real-time inventory management, reducing reliance on traditional three-tier distribution systems and enhancing the brewer experience. The rise of hazy IPAs and pastry stouts as high-profile style trends has further intensified the focus on specialized ingredient sourcing, positioning the U.S. as a critical innovator in this space.

The Europe Brewing Supplies Market

The Europe Brewing Supplies Market is projected to be valued at approximately USD 29.2 billion in 2026 and is projected to reach around USD 47.4 billion by 2035, growing at a CAGR of about 5.5% from 2026 to 2035. Europe's leadership is anchored by its centuries-old brewing tradition, particularly in Germany, Belgium, the Czech Republic, and the U.K., combined with modern regulatory frameworks like the EU's Common Agricultural Policy supporting hop and barley cultivation.

Countries such as Germany, Belgium, the U.K., and Italy are widely adopting advanced brewing supplies, driven by a high emphasis on purity laws (Reinheitsgebot), protected geographical indications, and artisanal production methods. The U.K.'s expanding craft ale sector and the EU's evolving organic certification frameworks further necessitate robust ingredient traceability and quality assurance mechanisms across brewing operations.

Europe's high density of brewpubs, strong beer tourism, and a mature malting industry drive the demand for premium, consistent brewing supplies. Funding and support for agricultural innovation encourage cross-border ingredient collaboration and the standardization of quality metrics across member states. With a sophisticated consumer base and a regulatory landscape that prioritizes tradition and authenticity, Europe remains a highly advanced and essential region for brewing supplies.

The Japan Brewing Supplies Market

The Japan Brewing Supplies Market is anticipated to be valued at approximately USD 5.8 billion in 2026 and is expected to attain nearly USD 8.7 billion by 2035, expanding at a CAGR of about 4.5% during the forecast period. Japan's aging population and a government push for regional revitalization through "craft brewery tourism" initiatives are driving the adoption of specialized brewing equipment and ingredients, making quality supplies a cornerstone of beverage diversification.

The Ministry of Agriculture, Forestry and Fisheries (MAFF) actively supports the development of local ingredient sourcing, promoting the use of domestic barley, hops, and unique yeast strains for sake-influenced beers. Japan's leadership in precision fermentation technology and high sanitation standards provides a robust foundation for advanced brewing methods, including automated quality control and small-batch experimentation.

Japan's concept of "monozukuri" (craftsmanship), driven by major beverage conglomerates and regional cooperatives, integrates brewing excellence into everything from limited-edition seasonal releases to mainstream beer offerings. Companies are deploying advanced brewing supplies to combat flavor standardization and ensure the integrity of craft production in Tokyo's bustling craft beer scene and regional agricultural initiatives. Japan's cultural emphasis on precision and quality positions it as a high-growth, quality-focused market for brewing solutions.

Global Brewing Supplies Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Brewing Supplies Market is expected to be valued at USD 117.1 billion in 2026 and is projected to reach USD 201.7 billion by 2035, showcasing rapid expansion supported by rising demand for craft beer diversity and production efficiency.

- High CAGR Driven by Craft Brewing Adoption: The market is expected to grow at an impressive CAGR of 6.2% from 2026 to 2035, fueled by accelerating craft brewery openings, automated equipment integration, and increasing consumer preference for premium alcoholic beverages worldwide.

- Strong Growth Trajectory in the United States: The U.S. Brewing Supplies Market stands at USD 35.7 billion in 2026 and is projected to reach USD 59.3 billion by 2035, expanding at a CAGR of 5.8% due to high craft beer consumption and strong manufacturing infrastructure.

- Regional Dominance: North America is expected to capture approximately 36.2% of the global market share in 2026, supported by a mature craft brewing ecosystem, robust distribution networks, and high consumer spending on premium beverages.

- Rapid Advancement in Brewing Technologies: Innovations including AI-driven fermentation monitoring, automated cleaning-in-place (CIP) systems, precision hop dosing equipment, and blockchain-based ingredient traceability are significantly enhancing efficiency, consistency, and quality of brewing operations.

- Growing Craft Beer Movement Boosts Adoption: Rising global incidents of flavor commoditization and mass-market saturation, coupled with the need for distinctive product offerings, is driving sustained demand for specialized, high-quality brewing supplies.

Global Brewing Supplies Market: Use Cases

- Microbrewery Equipment Procurement: Craft breweries source complete turnkey brewing systems including mash tuns, boil kettles, fermenters, and bright tanks to establish new production facilities.

- Specialty Ingredient Sourcing: Brewers procure unique hop varieties (Citra, Mosaic, Galaxy), specialty malts, and experimental yeast strains to create seasonal and limited-edition beer releases.

- Quality Control Implementation: Production facilities implement laboratory equipment for measuring IBU (bitterness), ABV (alcohol content), and microbiological stability to ensure batch consistency.

- Packaging Line Integration: Breweries invest in canning lines, bottling equipment, and kegging systems to expand distribution channels and retail presence.

- Home Brewing Supply Retail: Retailers provide starter kits, ingredient bundles, and educational resources to the growing community of home-based craft beer enthusiasts.

Global Brewing Supplies Market: Stats & Facts

Brewers Association (U.S.)

- The U.S. had 9,761 operating breweries in 2023.

- Of these, 9,456 were craft breweries.

- Craft breweries produced 24.6 million barrels of beer in 2023.

- Craft beer accounted for 13.3% of total U.S. beer volume.

- Craft beer represented 24.7% of the total U.S. beer retail dollar sales.

- The U.S. craft brewing industry contributed over USD 77 billion to the U.S. economy.

- The craft brewing industry supported 460,000+ jobs in the U.S.

- 495 new breweries opened in 2023, while 418 closed.

Alcohol and Tobacco Tax and Trade Bureau (TTB), U.S. Department of the Treasury

- Total U.S. beer production exceeded 180 million barrels in 2023.

- The U.S. had over 14,000 active brewery permits issued.

- Small brewers (under 2 million barrels annually) account for over 98% of U.S. breweries.

- Beer removals for consumption are reported monthly across all U.S. states.

National Beer Wholesalers Association (U.S.)

- The U.S. beer industry shipped approximately 192 million barrels in 2023.

- That volume equals more than 6 billion gallons of beer.

- The beer distribution sector supports 135,000 direct jobs in the U.S.

Eurostat (European Union Statistical Office)

- The EU produced 32.7 billion litres of alcoholic beer in 2024.

- An additional 2 billion litres of non-alcoholic beer (<0.5% alcohol) were produced in 2024.

- Germany produced 7.2 billion litres of beer in 2024 (largest in EU).

- Spain produced 4.0 billion litres of beer in 2024.

- Poland produced 3.4 billion litres in 2024.

- The Netherlands exported 1.5 billion litres of beer in 2024.

- EU barley production reached 49 million tonnes in 2024.

- The EU harvested barley across 10.3 million hectares.

Food and Agriculture Organization (FAO), United Nations

- Global barley production exceeded 150 million tonnes annually in recent years.

- Europe accounts for roughly 60% of global barley exports.

- Global hop production exceeds 110,000 tonnes annually.

- Germany and the United States are the top global hop producers.

- Barley yields globally average around 3 tonnes per hectare.

U.S. Department of Agriculture (USDA)

- The U.S. produces over 2 million acres of barley annually.

- Washington state accounts for over 70% of U.S. hop production.

- U.S. hop production exceeded 100 million pounds annually in recent years.

- U.S. barley production exceeds 3 million metric tons annually.

- The U.S. is among the top three global barley exporters.

The Brewers of Europe (Industry Association – based on official EU data)

- Europe has more than 10,000 active breweries.

- The European beer sector supports over 2 million jobs directly and indirectly.

- Beer production in Europe accounts for roughly one quarter of global beer output.

Japan National Tax Agency

- Japan has over 500 licensed breweries.

- Annual beer and beer-like beverage production in Japan exceeds 4 billion litres.

Global Brewing Supplies Market: Market Dynamic

Driving Factors in the Global Brewing Supplies Market

Escalating Consumer Demand for Craft and Specialty Beers

The growing global preference for artisanal, flavorful, and locally-produced beer is a major driver for brewing supplies. Consumers increasingly seek out hazy IPAs, pastry stouts, sour ales, and experimental brews that require specialized ingredients and equipment. Brewing supply systems that provide diverse malt profiles, unique hop varieties, and proprietary yeast strains enable breweries to differentiate their offerings. This allows businesses to capture premium pricing and build brand loyalty, especially in competitive markets like North America and Europe.

Technological Advancements in Brewing Equipment

Brewing supplies benefit heavily from innovations in automation, energy efficiency, and quality control. Modern brewhouses equipped with programmable logic controllers (PLCs), automated cleaning systems, and real-time monitoring sensors reduce labor costs and improve batch consistency. The ability to integrate these systems with inventory management and recipe formulation software provides an auditable trail and helps meet food safety standards, avoiding costly recalls and production inefficiencies associated with manual processes.

Restraints in the Global Brewing Supplies Market

Volatile Raw Material Prices and Supply Chain Uncertainty

The significant challenge of sourcing consistent quality barley, hops, and yeast creates friction in brewing operations. Achieving stable pricing and reliable availability requires long-term agricultural contracts, which can be disrupted by climate events, trade disputes, or pest/disease outbreaks. In many regions, crop failures or logistical delays can lead to ingredient shortages or price spikes, negatively impacting production planning and forcing breweries to reformulate recipes or absorb margin compression.

Regulatory and Tax Compliance Complexity

Alcohol production regulations impose strict rules on licensing, excise tax collection, labeling, and distribution. Navigating varying state and federal requirements, obtaining formula approvals, and managing three-tier system compliance create significant operational and legal complexity for breweries and their suppliers. Varying interpretations of "craft brewer" definitions and tax reduction eligibility across jurisdictions make it difficult to build a single, universal supply chain strategy.

Opportunities in the Global Brewing Supplies Market

Expansion into Emerging Beverage Markets

Emerging markets in Asia-Pacific, Africa, and Latin America represent major growth opportunities due to rising disposable incomes, westernization of drinking habits, and increasing craft brewery openings. Countries like China, Vietnam, Nigeria, and Brazil are seeing a surge in premium beer consumption and microbrewery concepts, creating massive demand for brewing equipment and ingredients. Localized distribution partnerships, equipment financing programs, and educational initiatives can improve accessibility, driving the next wave of market expansion.

Sustainability-Driven Ingredient Sourcing

The integration of organic farming practices, regenerative agriculture, and local ingredient procurement creates new value streams. Breweries can differentiate through "farm-to-glass" storytelling, carbon-neutral production claims, and support for regional farmers. This transforms brewing supplies from commodity inputs into marketing assets that appeal to environmentally conscious consumers and command premium pricing.

Trends in the Global Brewing Supplies Market

Automated and Smart Brewing Systems

The rise of fully automated brewhouses with remote monitoring capabilities is gaining significant traction. This trend leverages IoT sensors and cloud-based software to provide real-time data on fermentation progress, energy consumption, and equipment maintenance needs. These systems are far more efficient than traditional manual brewing and are becoming the gold standard for both new craft entrants and established regional breweries seeking modernization.

Direct-to-Consumer Ingredient Sales

E-commerce platforms are enabling ingredient suppliers to bypass traditional distribution channels and sell directly to home brewers and small commercial brewers. This ensures higher margins for suppliers and fresher ingredients for brewers. This trend supports the rapidly growing home brewing community and nano-brewery segment, ensuring reliable access to specialty products everywhere.

Global Brewing Supplies Market: Research Scope and Analysis

By Raw Material Analysis

The Malt & Adjuncts segment is projected to dominate the Global Brewing Supplies Market, accounting for the largest revenue share compared to hops, yeast, and other additives. This dominance is primarily driven by the fact that malted barley forms the fundamental backbone of nearly all beer styles, constituting the largest portion of the grain bill. Breweries across all scales from macro to micro require a constant, high-volume supply of base malts like two-row and pilsner.

Modern brewing, however, demands more than just base malt. The segment's value is enhanced by a vast array of specialty malts (such as caramel, roasted, and smoked malts) that provide the color, flavor, and body characteristics for diverse styles from stouts to IPAs. Furthermore, the use of unmalted adjuncts like corn, rice, and oats is significant in both macro lagers (for lightness) and craft hazy IPAs (for mouthfeel), adding another layer to the segment's breadth.

While hops, particularly high-value aroma varieties, command high prices per pound and are critical for craft beer differentiation, their overall volume and cost contribution to a batch of beer is typically lower than malt. The continuous, high-volume demand for malt and adjuncts from every brewery worldwide ensures this segment's revenue leadership. As global beer production volumes remain stable and the trend for specialty ingredients grows, the Malt & Adjuncts segment is expected to maintain its dominant position.

By Scale of Operation Analysis

The Micro Scale (3-15 BBL) segment is expected to dominate the market by number of units and contribute significantly to overall equipment and consumables revenue. This scale represents the sweet spot for the vast majority of new craft breweries and brewpubs opening globally. These operations are large enough to be commercially viable and supply a busy taproom and local distribution, yet small enough to remain agile and experimental.

The sheer number of breweries operating at this scale numbering in the tens of thousands worldwide creates massive cumulative demand. They require complete brewhouse systems, multiple fermenters, and consistent resupply of raw materials. Their growth trajectory often involves adding more fermenters or slightly expanding, generating ongoing equipment sales.

While Industrial Scale (100+ BBL) operations account for the vast majority of global beer volume and thus massive raw material consumption, the number of these facilities is far smaller. The Micro Scale segment, due to its high population, constant need for diverse supplies, and central role in the craft beer movement, continues to lead in terms of market dynamism and is a primary growth driver for suppliers focused on the craft sector. Its dominance is projected to continue as the craft beer culture globalizes.

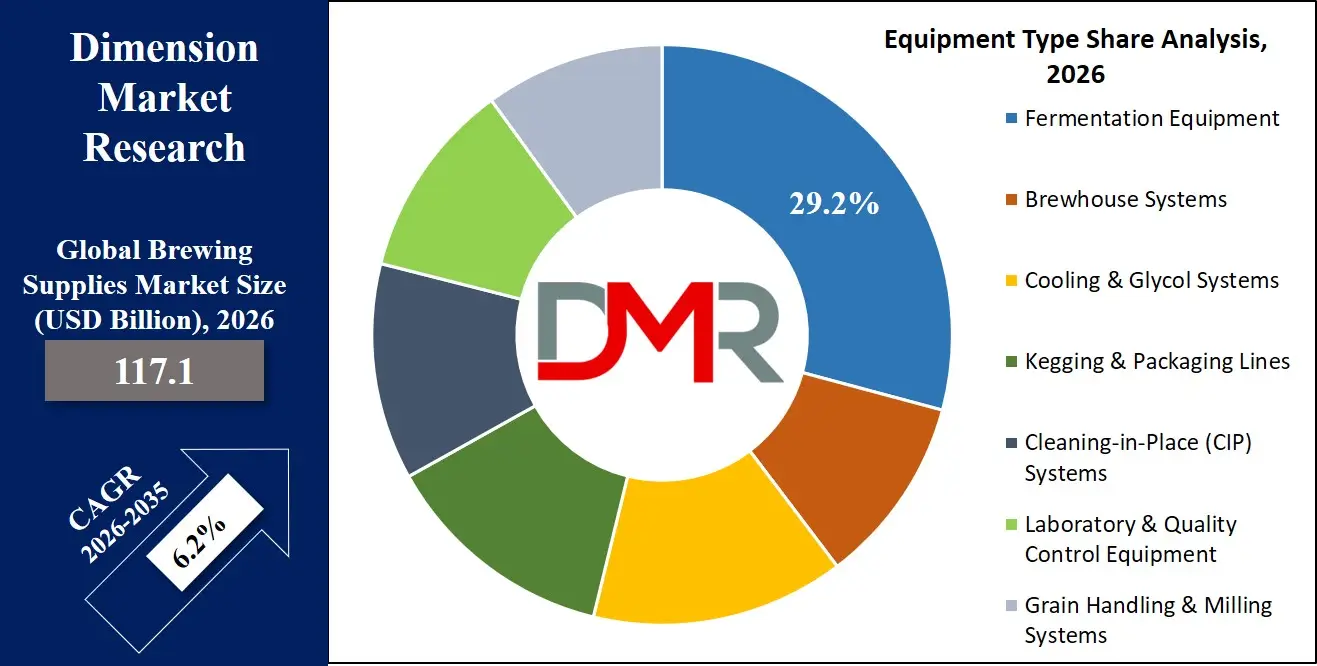

By Equipment Type Analysis

The Fermentation Equipment segment is anticipated to dominate the equipment market. This is because fermentation vessels including fermenters, unitanks (for both fermentation and conditioning), and bright beer tanks are required in a much higher quantity per brewery than any other single piece of major equipment. While a brewery typically has one brewhouse, it will have a fleet of fermenters to allow for continuous production, multiple beer styles, and proper aging cycles.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The demand for this equipment is driven by both new brewery openings (requiring a full tank farm) and expansion at existing breweries (adding more tanks to increase capacity). Furthermore, technological advancements in tank design, such as highly efficient cooling jackets, variable speed pressure control, and conical shapes for optimal yeast harvesting, encourage upgrades. The robust stainless steel construction, insulation, and complex cooling systems make these tanks a significant capital investment, contributing to the segment's high revenue. As global beer production and the number of breweries grow, the need for more fermentation capacity ensures this segment's continued dominance.

By Brewing Process Analysis

Automated/Industrial Brewing is projected to generate the largest revenue share within the process segment due to its application in producing the vast majority of the world's beer volume by macro breweries and large regional players. These processes rely on highly sophisticated, fully automated systems designed for maximum efficiency, consistency, and throughput. The equipment and control systems required are immensely capital-intensive, involving large-scale brewhouses, high-speed packaging lines, and centralized automation software.

However, the Craft Brewing segment is a critical and fast-growing counterpoint. It emphasizes flexibility, traditional methods, and manual control to produce small-batch, high-flavor beers. This segment drives demand for a different set of supplies, including specialized, often experimental, ingredients and versatile, high-quality equipment from brewhouse manufacturers catering to the craft market. While Automated/Industrial leads in revenue from large-scale equipment sales, Craft Brewing drives innovation and demand for premium raw materials, making both processes vital to the overall market dynamics.

By Distribution Channel Analysis

Distributors/Wholesalers is expected to dominate the distribution channel segment. This is due to the established nature of the three-tier system (producer-distributor-retailer) in many mature markets like the U.S., and the logistical efficiency they provide. Distributors aggregate products from hundreds of suppliers from massive maltsters and hop merchants to specialty equipment makers and provide warehousing, sales representation, and just-in-time delivery to thousands of breweries.

For a brewery, relying on a distributor simplifies procurement, allowing them to order a wide range of supplies from a single source. For smaller suppliers, distributors provide immediate access to a broad customer base without the need to build a direct sales force. While Direct-to-Brewery sales are growing, particularly for large, custom equipment orders and contract ingredient purchases, and Online/E-commerce is booming for the homebrew and nano segment, the comprehensive logistical network and consolidated purchasing power of traditional distributors/wholesalers secure their dominant revenue position.

By End-User Analysis

Microbreweries & Brewpubs is projected to be the dominant end-user segment in terms of overall market engagement and demand diversity. This segment comprises the largest number of active business entities in the brewing industry. Their business model, which often combines a production facility with a taproom or restaurant, creates robust and consistent demand across all supply categories.

They require a steady stream of raw materials (malt, hops, yeast) to keep their tanks full. They need equipment for their initial setup and subsequent expansion (brewhouses, fermenters, kegs). They invest in cleaning supplies and often basic lab equipment for quality control. Their numbers continue to grow globally, and their need for a diverse and reliable supply chain makes them the core customer base for a vast network of distributors and suppliers. While Macro Breweries purchase larger volumes of specific commodities, the sheer number, growth rate, and diverse needs of Microbreweries & Brewpubs make them the dominant end-user segment.

The Global Brewing Supplies Market Report is segmented on the basis of the following:

By Raw Material

- Malt & Adjuncts

- Base Malts

- Specialty Malts

- Unmalted Grains (Corn, Rice, Oats)

- Hops

- Bittering Hops

- Aroma Hops

- Dual-Purpose Hops

- Hop Pellets/Extracts

- Yeast

- Ale Yeast

- Lager Yeast

- Wild/Brettanomyces Yeast

- Other Additives

By Scale of Operation

- Nano Scale (Up to 3 BBL)

- Micro Scale (3-15 BBL)

- Regional Scale (15-100 BBL)

- Industrial Scale (100+ BBL)

By Equipment Type

- Fermentation Equipment

- Fermenters

- Unitanks

- Bright Beer Tanks

- Brewhouse Systems

- Mash Tuns

- Lauter Tuns

- Brew Kettles

- Whirlpool Tanks

- Cooling & Glycol Systems

- Kegging & Packaging Lines

- Cleaning-in-Place (CIP) Systems

- Laboratory & Quality Control Equipment

- Grain Handling & Milling Systems

By Brewing Process

- Traditional Brewing

- Craft Brewing

- Automated/Industrial Brewing

- Nano Brewing

- Smart Brewing Systems

- Home Brewing Kits

- Commercial Brewing Systems

By Distribution Channel

- Direct-to-Brewery

- Distributors/Wholesalers

- Retail (Homebrew Shops)

- Online/E-commerce Platforms

By End-User

- Microbreweries & Brewpubs

- Regional Breweries

- Macro Breweries

- Contract Brewing Companies

- Home Brewers

- Restaurants & Bars

Impact of Artificial Intelligence in the Global Brewing Supplies Market

- AI for Recipe Development and Flavor Prediction: AI algorithms analyze vast datasets of ingredient profiles (malt, hop, yeast characteristics) and consumer preference data to suggest novel and optimized beer recipes, predicting final flavor profiles with high accuracy.

- AI-Driven Quality Control and Anomaly Detection: AI-powered vision systems monitor packaging lines for defects (e.g., incorrect fill levels, label flaws). In the brewhouse, AI analyzes sensor data to detect subtle deviations in temperature, pressure, or flow that could indicate a quality issue before it affects the final product.

- Predictive Maintenance for Brewery Equipment: AI analyzes real-time data from sensors on brewhouse systems, pumps, and packaging lines to predict when equipment is likely to fail. This allows breweries to perform maintenance proactively, minimizing costly downtime and ensuring consistent production.

- Supply Chain Optimization and Yield Forecasting: AI models analyze weather patterns, geopolitical factors, and market trends to predict the yield and price volatility of key agricultural ingredients like hops and barley. This enables breweries and suppliers to make more informed purchasing and risk-management decisions.

- Personalized Consumer Engagement: E-commerce platforms and brewery apps use AI to recommend beers to consumers based on their past purchases and reviews. This data on consumer preferences can be fed back to breweries, guiding decisions on which beer styles and ingredient profiles to develop next.

Global Brewing Supplies Market: Regional Analysis

Region with the Largest Revenue Share

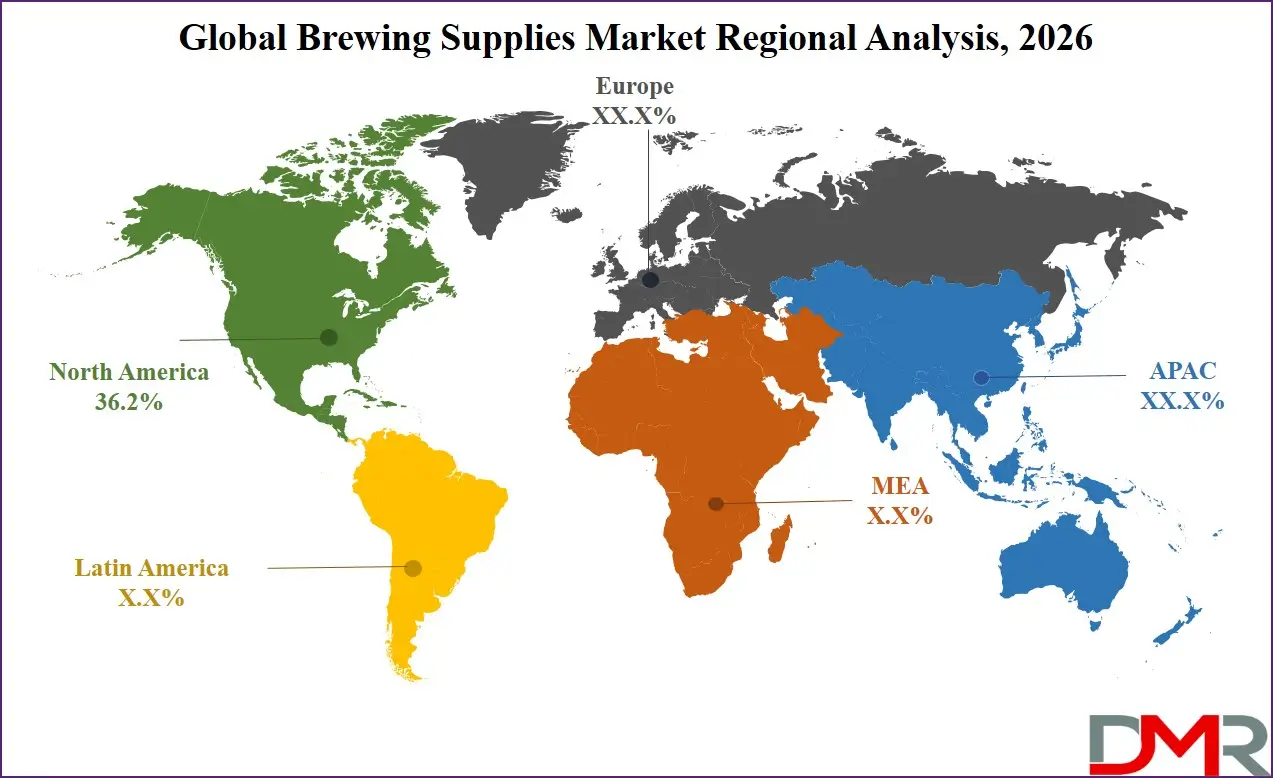

North America is projected to dominate the regional segment with the highest market share as it is anticipated to hold a 36.2% of the total market revenue by the end of 2026, due to the unparalleled number of craft breweries, a highly mature and efficient distribution network, and high per-capita consumption of premium beer. The region is home to world-leading hop growers (U.S.), major maltsters, and numerous innovative equipment manufacturers, driving the entire supply chain. Strong consumer culture around craft beer and homebrewing further strengthens demand.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States, in particular, accounts for the largest share within North America due to its sheer market size and the "hub-and-spoke" model of its brewing supply industry. Although Asia Pacific is often the fastest-growing region, North America continues to hold a leading revenue share due to the high value of its premium-focused market and the established nature of its supply infrastructure.

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR and is poised to achieve rapid market share growth due to its massive and growing beer consumption, a rapidly emerging craft beer scene in countries like China, Japan, South Korea, Vietnam, and Thailand, and increasing local production of raw materials and equipment. Government support for agricultural diversification and the food & beverage industry in nations like India and China are creating fertile ground for local supply chain development. The region's growing middle class, with rising disposable income and exposure to global beer styles, is driving demand for both international and domestically produced premium supplies. This, combined with an immense volume of new breweries and increasing modernization of existing industrial facilities, positions APAC as the fastest-growing market for brewing supplies.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Brewing Supplies Market: Competitive Landscape

The Global Brewing Supplies Market is moderately consolidated, featuring a mix of global agricultural giants, specialized ingredient merchants, and regional equipment manufacturers. Leading players like Malteurop Group (part of InVivo), Boortmalt, and Cargill, Incorporated leverage their vast agricultural networks and scale to dominate the global malt supply chain. Hop merchants and processors such as John I. Haas, Inc. (a subsidiary of S.S. Steiner, Inc.) and BarthHaas are driving market dynamics with proprietary hop varieties and advanced hop product formats.

Specialized equipment manufacturers like GEA Group, Alfa Laval, and Criveller Group play a crucial role in supplying technology for brewhouses, fermentation, and packaging to breweries of all sizes. Pure-play ingredient innovators, including Lallemand Inc. (for yeast and bacteria) and White Labs, are critical for providing the biological diversity that defines craft beer.

Regional distributors and homebrew supply retailers form a vital link in the chain, connecting global suppliers with local breweries and homebrewers. These players often act as brand ambassadors and technical consultants for the products they sell, fostering deep relationships within their communities.

Some of the prominent players in the Global Brewing Supplies Market are:

- Malteurop Group (Groupe InVivo)

- Boortmalt NV

- Cargill, Incorporated

- Rahr Corporation

- Viking Malt

- IREKS GmbH

- Simpsons Malt Limited

- Crisp Malting Group

- John I. Haas, Inc. (S.S. Steiner, Inc.)

- BarthHaas GmbH & Co. KG

- Yakima Chief Hops

- Hopsteiner (Steiner Brewing)

- Lallemand Inc. (Lallemand Brewing)

- Fermentis (Lesaffre)

- White Labs

- GEA Group AG

- Alfa Laval AB

- Paul Mueller Company

- Criveller Group

- Specific Mechanical Systems

- Portland Kettle Works

- Ss Brewtech

- MoreBeer!

- Northern Brewer

- Other Key Players

Recent Developments in the Global Brewing Supplies Market

- November 2025: Yakima Chief Hops released its first-ever "Virtual Hop" variety, developed through machine learning to predict flavor profiles, allowing brewers to pre-order crops years in advance based on digital sensory data.

- October 2025: GEA Group unveiled its new "Brewery 4.0" automation suite at drinktec 2025, featuring AI-driven control loops that self-optimize brewhouse efficiency in real-time, reducing energy consumption by up to 15%.

- September 2025: Lallemand Brewing announced a strategic partnership with a leading genomics firm to develop a range of non-GMO hybrid yeast strains specifically optimized for producing hop-forward, non-alcoholic beers.

- August 2025: Boortmalt completed the acquisition of a major malting facility in Zambia, significantly expanding its footprint in the rapidly growing African beer market and securing local barley supply chains.

- July 2025: A consortium of German hop growers received a government grant to develop precision agriculture techniques using drone surveillance and AI to detect fungal diseases in hop fields earlier and more accurately than the human eye.

- June 2025: MoreBeer! opened its largest distribution hub to date in Austin, Texas, featuring automated picking and packing systems to handle the surge in online orders for homebrew and nano-brewery equipment and ingredients across the Southern U.S.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 117.1 Bn |

| Forecast Value (2035) |

USD 201.7 Bn |

| CAGR (2026–2035) |

6.2% |

| The US Market Size (2026) |

USD 35.7 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Raw Material (Malt & Adjuncts, Hops, Yeast, Other Additives), By Scale of Operation (Nano Scale (Up to 3 BBL), Micro Scale (3-15 BBL), Regional Scale (15-100 BBL), Industrial Scale (100+ BBL)), By Equipment Type (Fermentation Equipment, Brewhouse Systems, Cooling & Glycol Systems, Kegging & Packaging Lines, Cleaning-in-Place (CIP) Systems, Laboratory & Quality Control Equipment, Grain Handling & Milling Systems), By Brewing Process (Traditional Brewing, Craft Brewing, Automated/Industrial Brewing, Nano Brewing, Smart Brewing Systems, Home Brewing Kits, Commercial Brewing Systems), By Distribution Channel (Direct-to-Brewery, Distributors/Wholesalers, Retail (Homebrew Shops), Online/E-commerce Platforms), and By End-User (Microbreweries & Brewpubs, Regional Breweries, Macro Breweries, Contract Brewing Companies, Home Brewers, Restaurants & Bars) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Malteurop Group (Groupe InVivo), Boortmalt NV, Cargill, Incorporated, Rahr Corporation, Viking Malt, IREKS GmbH, Simpsons Malt Limited, Crisp Malting Group, John I. Haas, Inc. (S.S. Steiner, Inc.), BarthHaas GmbH & Co. KG, Yakima Chief Hops, Hopsteiner (Steiner Brewing), Lallemand Inc. (Lallemand Brewing), Fermentis (Lesaffre), White Labs, GEA Group AG, Alfa Laval AB, Paul Mueller Company, Criveller Group, Specific Mechanical Systems, Portland Kettle Works, Ss Brewtech, MoreBeer!, Northern Brewer, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Brewing Supplies Market?

▾ The Global Brewing Supplies Market size is estimated to have a value of USD 117.1 billion in 2026 and is expected to reach USD 34.8 billion by the end of 2035.

What is the growth rate in the Global Brewing Supplies Market?

▾ The market is growing at a CAGR of 7.2 percent over the forecasted period of 2026-2035.

What is the size of the US Brewing Supplies Market?

▾ The US Brewing Supplies Market is projected to be valued at USD 5.2 billion in 2026. It is expected to witness subsequent growth as it holds USD 9.3 billion in 2035 at a CAGR of 6.5%.

Which region accounted for the largest Global Brewing Supplies Market?

▾ North America is expected to have one of the largest market shares in the Global Brewing Supplies Market, alongside Europe, driven by its high concentration of craft breweries and mature supply chain.

Who are the key players in the Global Brewing Supplies Market?

▾ Some of the major key players in the Global Brewing Supplies Market are Malteurop Group, Boortmalt, Cargill, Inc., John I. Haas, Inc., BarthHaas, GEA Group, Lallemand Inc., and many others.