What is the Carbon Accounting Software Market Size?

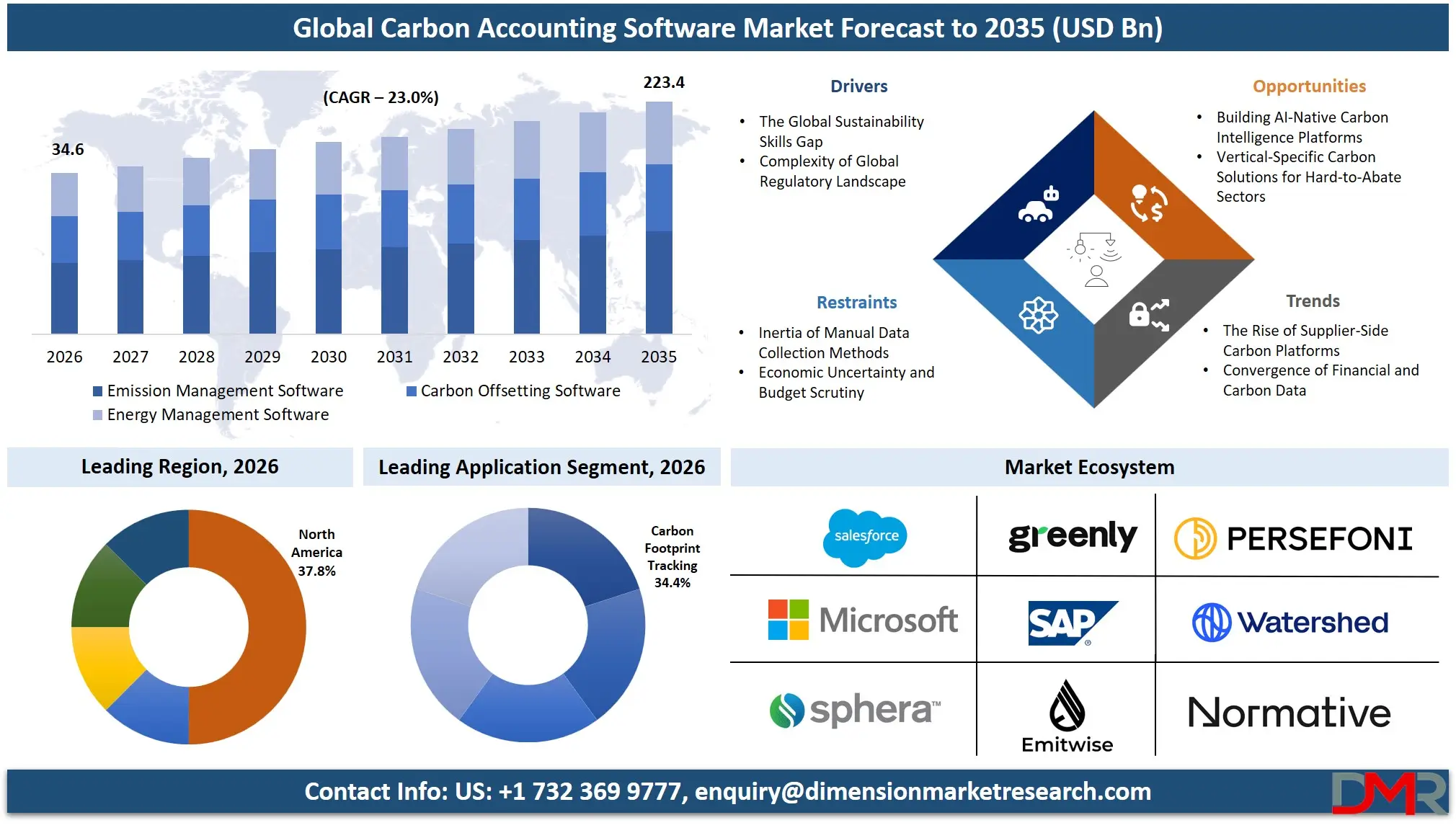

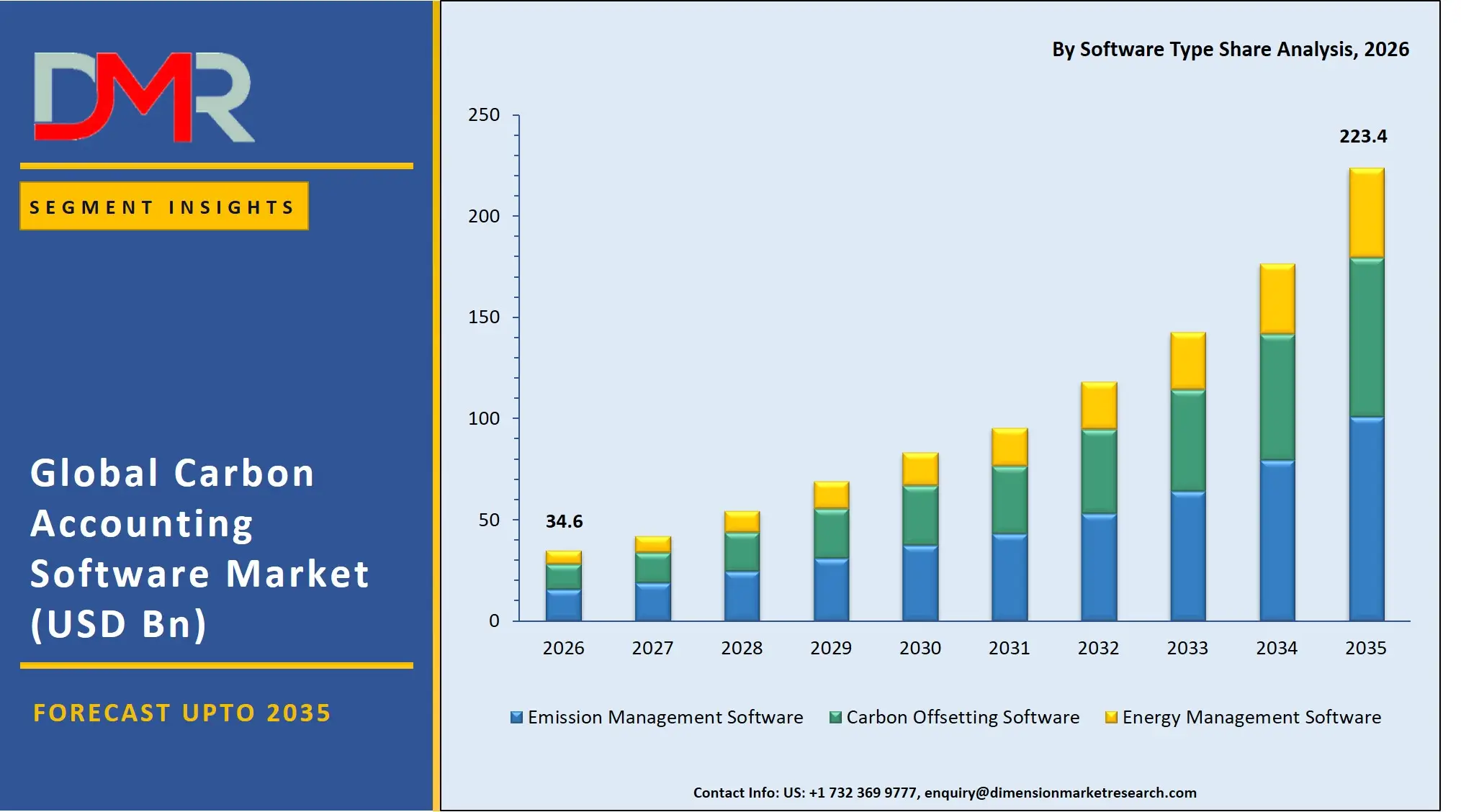

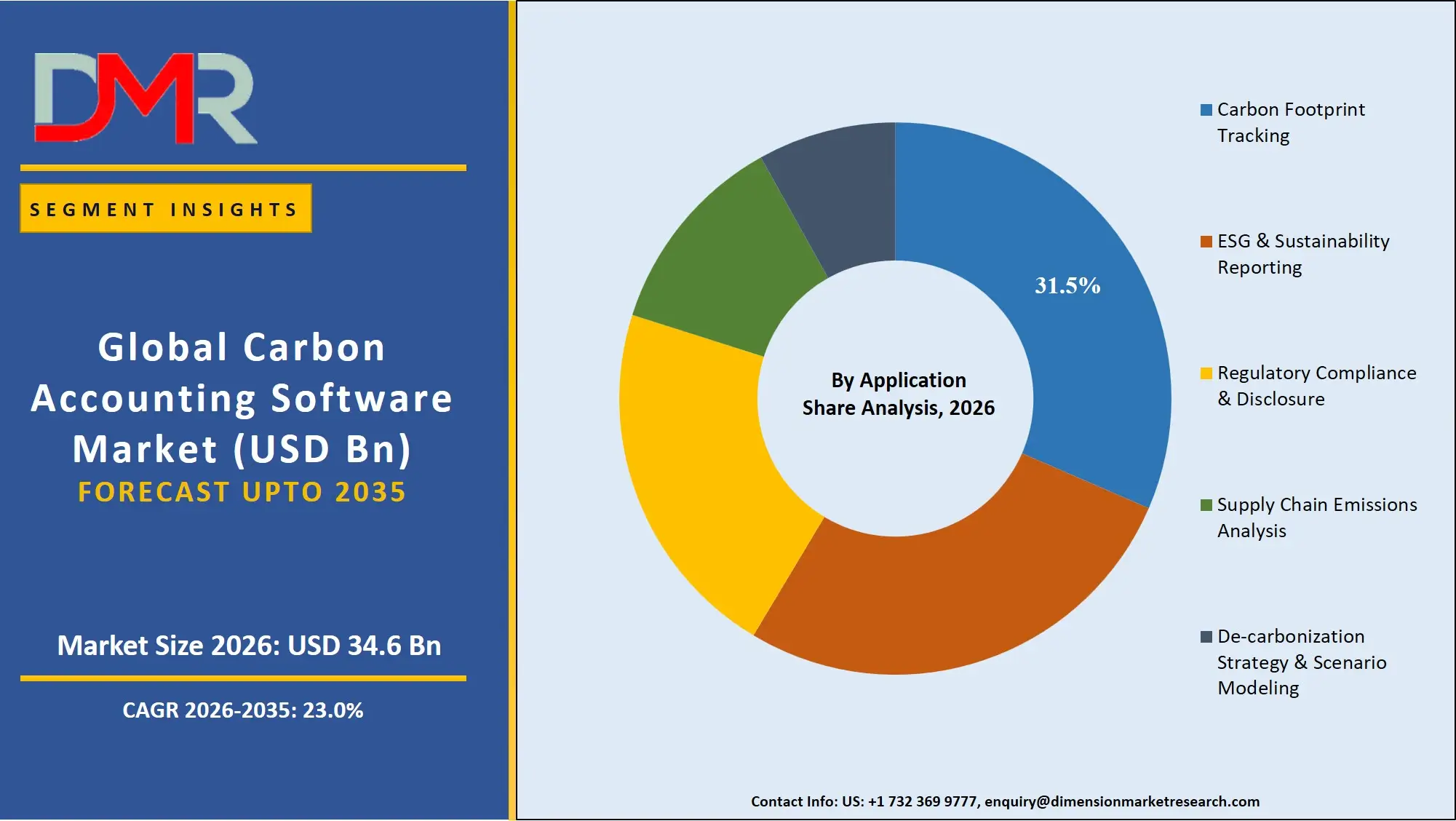

The Global Carbon Accounting Software Market is expected to reach a value of USD 34.6 billion in 2026, and it is further anticipated to reach USD 223.4 billion by 2035, growing at a CAGR of 23.0% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Carbon accounting software solutions have been expanding at an exponential pace as companies are under greater pressure from regulators, investors, and consumers to quantify, report and mitigate their greenhouse gas (GHG) footprints.

The market includes software platforms that can automatically calculate Scope 1, 2, and 3 emissions, that manage carbon credit portfolios, and that model de-carbonization strategies to support organizations in their journey to become "net zero". Specialized carbon accounting platforms are vital as the disclosure requirements become more complex, supply chain emissions are required to be analysed and AI is now being used to help with predictive energy analytics. Cloud-based deployment is most popular, as is the use by large enterprises, which are more likely to deploy the service as it is scalable and can aggregate data from all geographically distributed operations. The energy & utilities, manufacturing, transportation & logistics, and chemicals sectors are critical as they have the most stringent regulatory standards and require a carbon data ecosystem that is auditable, highly available, and accessible.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

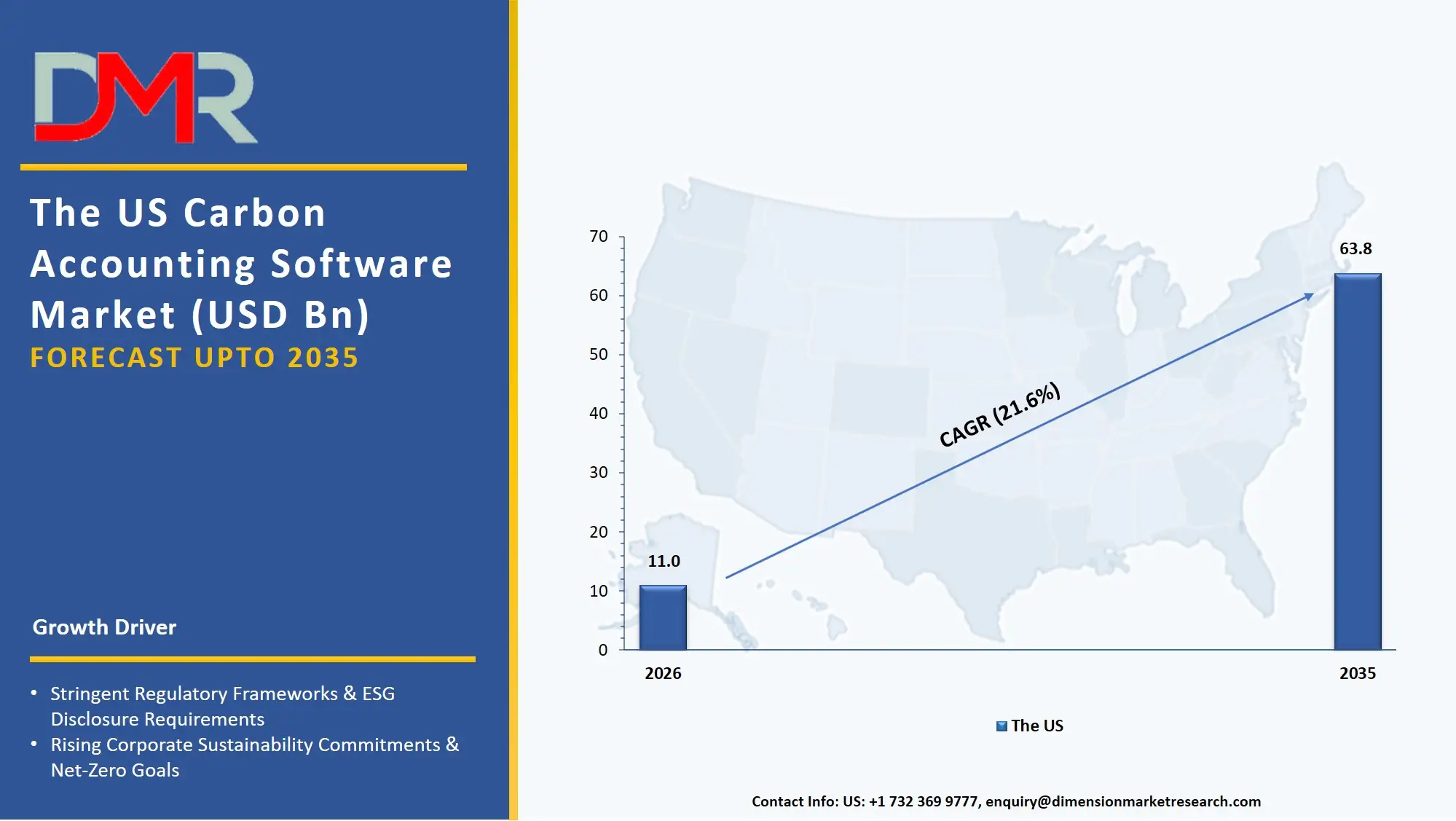

The US Carbon Accounting Software Market

The US Carbon Accounting Software Market is projected to reach USD 11.0 billion in 2026 at a compound annual growth rate of 21.6% over its forecast period, culminating in a value of USD 63.8 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Carbon accounting software is the most developed and biggest market in the U.S. because of the proactive climate disclosure rules proposed by the SEC and the proliferation of voluntary carbon markets. The market has been typified by high demand for Emission Management Software, whereby organizations are aimed at moving from manual spreadsheet-based calculations to automated, audit-ready carbon footprint calculation & reporting. Moreover, the use of Generative AI in carbon data analysis is creating a similar requirement in Regulatory Compliance Management software to ensure regulatory disclosures are accurate, and compliant with new frameworks such as the GHG Protocol.

The Europe Carbon Accounting Software Market

The Europe Carbon Accounting Software Market is estimated to be valued at USD 10.0 billion in 2026 and is further anticipated to reach USD 61.2 billion by 2035 at a CAGR of 22.2%. ESG & Sustainability Reporting and Carbon Offsetting Software has a great influence on the European market as a result of the regulatory frameworks that are present, such as the EU's Corporate Sustainability Reporting Directive (CSRD) and European Green Deal. Accelerated growth of Supply Chain Emissions Analysis solutions is also being experienced in the region as automotive and manufacturing industries in Germany and France are trying to strike a balance in operational technology (OT) security with cloud-based carbon data analytics. In addition, efforts to implement carbon border adjustment mechanisms (CBAM) are challenging software providers to create dedicated Carbon Footprint Tracking features to provide data residency and interoperability across European supply chain ecosystems.

The Japan Carbon Accounting Software Market

The Japan Carbon Accounting Software Market is projected to be valued at USD 3.8 billion in 2026. It is further expected to witness robust growth, holding USD 22.6 billion in 2035 at a CAGR of 21.9%. The Japanese market is special, as the climate neutrality strategy is driven by the corporate desire to reduce carbon emissions to zero by 2050, which comes in the background of international trade pressures and aging energy infrastructure. De-carbonization Strategy & Scenario Modeling and Energy Management Software make up a large part of the spending as large conglomerates model the transition of mission-critical manufacturing off fossil fuels to renewable energy sources. The Energy Consumption Analytics and Efficiency Optimization niche is also growing in demand, as deep local market integration is required to connect legacy industrial control systems with modern platforms running in the cloud and managing carbon accounting.

Key Takeaways

- Market Size & Forecast: The Global Carbon Accounting Software market is projected to reach USD 34.6 billion in 2026, expanding dramatically to USD 223.4 billion by 2035, owing to the two primary growth drivers the mandatory climate disclosure regulation and the mandatory modernization of enterprise ESG data infrastructure.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 23.0%, due to the critical shortage of in-house sustainability experts and the rapidly increasing complexity of handling Scope 3 emissions data and dealing with voluntary carbon markets.

- Primary Growth Drivers: Many organizations are shifting from manual reporting to a centralized, automated Carbon footprint calculation & reporting system, needing de-carbonization Strategy & Scenario Modeling to inform capital allocation, and needing to integrate supply chain data, which demands specialized supply chain emissions analysis capabilities.

- Key Market Trends: Major trends include the rise of industry-specific carbon accounting solutions, the use of AI-powered tools within Emission Tracking & Monitoring to auto-remediate data gaps, and the shift toward Carbon Credit Management as boards prioritize credible offsetting strategies for hard-to-abate emissions.

- By Software Type Analysis: Emission Management Software is poised to dominates the software type segment as accurate carbon tracking, regulatory compliance, and ESG reporting requirements are growing. Organizations are increasingly turning to these platforms for automated emissions monitoring, audit-ready reporting, and transparency in their Scope 1, 2 and 3 emission management activities globally.

- By Deployment Mode Analysis: Cloud-based deployment dominates the carbon accounting software market owing to its scalability, flexibility, and real-time data accessibility. Organizations increasingly prefer cloud solutions for centralized emissions tracking, seamless enterprise integration, regulatory updates, and cost-effective subscription models supporting global carbon management operations.

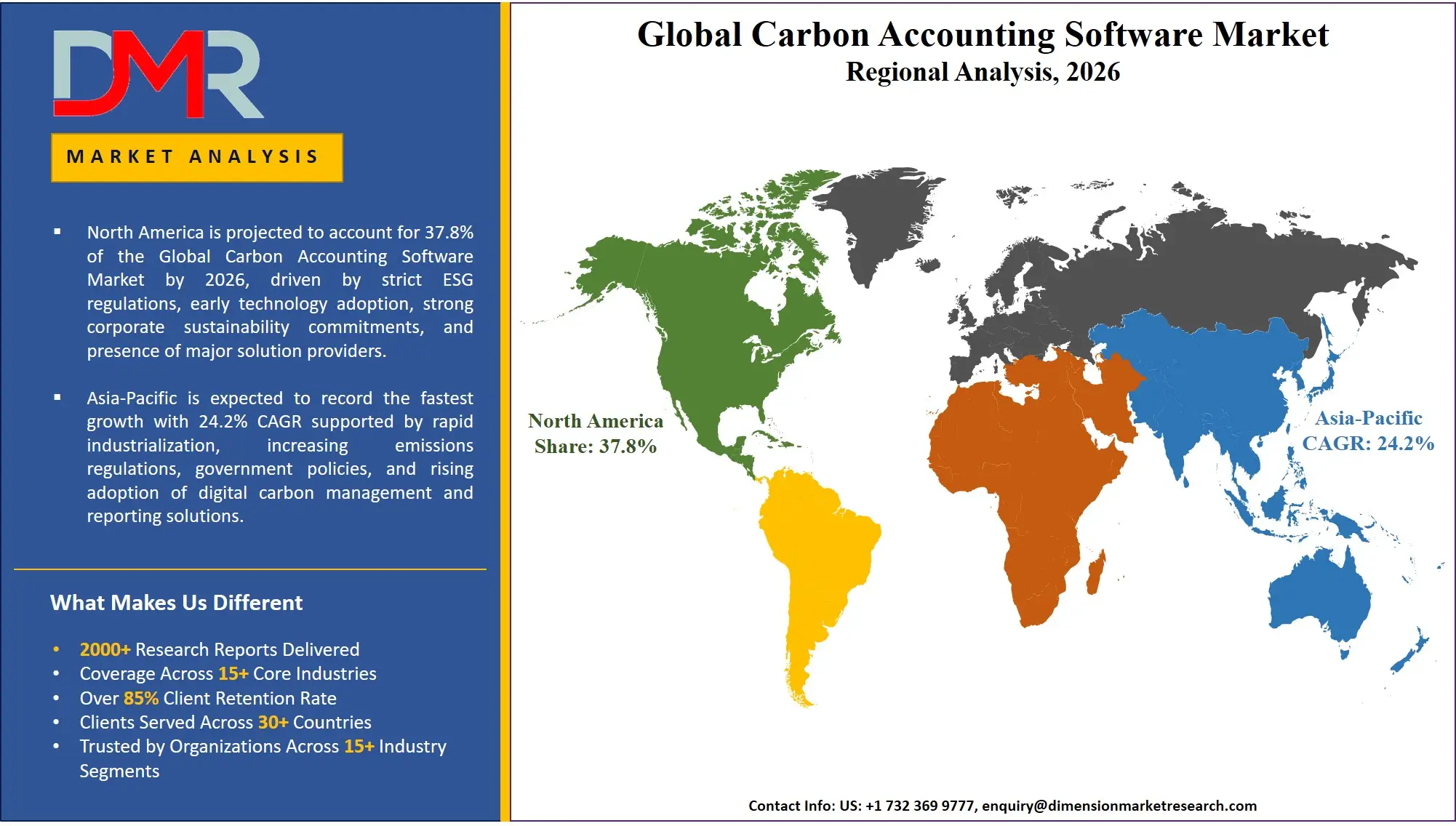

- Regional Leadership: North America is poised to dominate this market with 37.8% of the market share in 2026 due to its well-developed climate tech ecosystem that utilizes this infrastructure to its fullest and makes it a leader in this market.

What is the Carbon Accounting Software?

Carbon Accounting Software comprises specialized digital platforms that are offered by third-party vendors, climate tech specialists, and enterprise software giants to assist organizations in measuring, managing, and reporting their greenhouse gas (GHG) inventory throughout the entire carbon lifecycle. These services, unlike generic environmental reporting tools, are related to the precision and auditability of carbon data. This involves Emission Management Software to establish a verifiable GHG footprint, Carbon Offsetting Software to physically curate and retire verified carbon credits, and Energy Management Software to ensure operational energy use is continuously optimized against carbon reduction targets. With thousands of companies setting Science Based Targets initiative (SBTi) goals, carbon accounting software is needed to achieve granular data governance, a defensible audit posture, and scenario forecasting, making net-zero investments translate into tangible decarbonization outcomes, as opposed to mere compliance exercises.

Use Cases

- Streamlined Regulatory Compliance in Energy & Utilities: Utility operators hire Emission Management Software to automate the calculation of Scope 1 emissions from power generation assets, transforming flue gas sensor data into regulatory-grade reports for EPA and EU ETS compliance.

- Supply Chain Decarbonization in Automotive: Automotive manufacturers use Supply Chain Emissions Analysis platforms to gather primary emissions data from thousands of tier-1 and tier-2 suppliers and categorize spending-based and activity-based Scope 3 emissions to identify actionable reduction hotspots.

- Carbon Credit Portfolio Management in Finance: Financial institutions use Carbon Offsetting Software to screen, purchase, and track the retirement of verified carbon credits from afforestation and direct air capture projects, ensuring claims of portfolio carbon neutrality are substantiated and transparent.

- Renewable Energy Integration in Manufacturing: Global manufacturers use Energy Management Software to integrate factory floor power purchase agreement (PPA) data with production output, creating a real-time view of the percentage of renewable energy powering their operations to validate green product claims.

How AI is Transforming the Carbon Accounting Software Market?

AI is changing the carbon accounting software market by accelerating the process of emissions data ingestion, as well as enhancing the credibility of climate disclosures. In Emission Management Software, AI-based spend classification tools have the potential to automatically transform millions of lines of procurement data into Scope 3 emission estimates, greatly minimizing the amount of manual mapping work and reporting timelines, and project risk. Meanwhile, AI-powered features in Energy Management Software allow businesses to better control energy consumption by detecting anomalies in usage, predicting future demand profiles, and suggesting measures like load shifting to capitalize on periods of high renewable energy availability on the grid.

Corporate strategy and audit readiness projects are also revolving around AI. In the area of Regulatory Compliance & Disclosure, intelligent compliance-monitoring agents are used to continuously check draft sustainability reports and identify inconsistencies, narrative gaps, and alignment breaches with frameworks like ISSB and ESRS. Moreover, generative AI assistants are complementing De-carbonization Strategy & Scenario Modeling by simulating the carbon impact of capital allocation decisions and modelling future business portfolios to give stakeholders a visualization of the transition pathway before committing financial resources.

Market Dynamics

Key Drivers in the Global Carbon Accounting Software Market

The Global Sustainability Skills Gap

Global organizations are grappling to acquire skilled professionals who have the knowledge of GHG Protocol scoping, lifecycle assessment, carbon market mechanisms, and climate risk quantification. The skills are in demand at a faster pace than the number of trained talents which has led to a structural shortage in the labor market. This is leading to a trend of enterprises deploying automated carbon accounting software platforms rather than depending solely on in-house sustainability teams and consultants. These platforms assist in essential processes like Carbon Footprint Calculation & Reporting, Emission Tracking & Monitoring, and automated disclosures that are continuously provided. Deploying such software allows organizations to accelerate net-zero initiatives and minimize the chances of errors due to insufficient in-house carbon expertise.

Complexity of Global Regulatory Landscape

Enterprises of considerable size tend to have operations across several jurisdictions, primarily the EU, the US, and the UK, each with distinct climate disclosure mandates including CSRD, SEC rules, and TCFD. Nonetheless, managing compliance across a fragmented regulatory environment is very complicated. Organizations need to align data collection methods, materiality thresholds, and reporting templates on multiple platforms using various protocols and definitions. This complexity may cause inefficiencies, disclosure gaps, and reputational risk without the guidance of a unified platform. Thus, there is a growing need for Regulatory Compliance Management software that can assist enterprises to operate in such a dynamic policy environment.

Restraints in the Global Carbon Accounting Software Market

Growth of Manual Data Collection Methods

Most businesses still run sustainability reporting on old systems that were developed over a long history, primarily relying on disconnected spreadsheets, emails, and manual surveys. These outdated processes are a significant obstacle to change, despite carbon accounting software delivering more accuracy and auditability. It can be costly and resource-intensive to migrate complex, highly customized spreadsheet-based models to a centralized software platform. Gathering primary data across thousands of facilities and suppliers necessitates a lot of planning, stakeholder engagement, and validation. The organizations are afraid of business disruption, data loss, and unforeseen implementation costs in the transition. Consequently, data inertia decelerates the adoption of automated carbon accounting and tends to delay or even block larger-scale digital transformation of the ESG function.

Economic Uncertainty and Budget Scrutiny

Unstable economies and unpredictable business environments have caused organizations to be more hesitant to spend on new software initiatives. Even though sustainability is still a strategic priority, executives are being pressurized to justify every technology investment and provide a measurable return on investment. The subscription fees and long-term engagement models of Carbon Offsetting Software and advanced Energy Management Software providers are more likely to come under increased scrutiny. Businesses have shifted to platforms that deliver quick operational benefits or immediate cost reductions through efficiency optimization. Long-term strategy and net-zero planning initiatives are more likely to be delayed until the providers can demonstrate a near-term payoff in reduced energy spend or lowered carbon tax liability. This change is compelling the carbon accounting software vendors to be more performance-driven and results-oriented.

Growth Opportunities in the Global Carbon Accounting Software Market

Building AI-Native Carbon Intelligence Platforms

One of the significant growth opportunities in the carbon accounting software market is building secure, AI-native platforms that not only report on past emissions but predict future carbon trajectories. A lot of companies have started with basic carbon footprint tracking tools, but now they desire sophisticated predictive capabilities that align with their own financial planning and compliance requirements. The development of these advanced settings involves specialized skills in Data Engineering, Life Cycle Assessment databases, and AI orchestration frameworks. Carbon accounting software vendors are able to assist enterprises to build scalable, automated analytics ecosystems that support dynamic scenario modelling, supply chain optimization, and automated audit trails. The area has the potential to create high demand for highly specialized De-carbonization Strategy & Scenario Modeling capabilities.

Vertical-Specific Carbon Solutions for Hard-to-Abate Sectors

The need to integrate both technical carbon calculation skills and understanding of particular industrial processes is driving the growth of software as regulators and investors focus on hard-to-abate sectors. These are solutions specific to the chemicals industry (tracking process emissions), food & beverages (linking farm-level data), and construction & infrastructure (calculating embodied carbon). Companies within the chemicals and construction sectors are required to adhere to stringent physical climate risk and material measurement standards. Thus, they require software partners that comprehend carbon science and the industry's specific production processes. To add value, carbon accounting software providers can consider integrating vertical-specific emission factor databases with existing ERP systems, aligning with industry protocols, and tailoring workflows.

Trends in the Global Carbon Accounting Software Market

The Rise of Supplier-Side Carbon Platforms

Supplier-centric carbon management is becoming increasingly adopted as an alternative to traditional, buyer-driven Scope 3 data collection. Large enterprises are providing their SME suppliers with dedicated carbon accounting portals, rather than requesting data through one-off surveys, with infrastructure, calculation, and benchmarking running on a shared platform. These platforms enable the ease of carbon data sharing, validation of claims, and automated credit allocation. To counter this, carbon accounting software vendors are providing expertise in platform design, supply chain data interoperability, and SME user experience.

Convergence of Financial and Carbon Data

Environmental sustainability is also emerging as a key aspect in financial decisions as companies are under pressure to link executive compensation to ESG metrics and assess climate-related financial risks. Businesses are now interested in carbon accounting platforms that help produce investor-grade disclosures as well as production optimization and cost reduction. This has brought about the need for Integrated Financial and Carbon Reporting services. Software providers assist organizations in selecting investment scenarios with the lowest marginal abatement cost, optimizing resources through energy efficiency analytics, and reducing waste by underutilized assets.

Research Scope and Analysis

Research Scope and Analysis focuses on key segmentation of the carbon accounting software market, highlighting dominance of emission management software, cloud deployment, large enterprises, ESG reporting applications, and the energy and utilities sector due to regulatory pressure and sustainability needs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Software Type Analysis

Emission Management Software is poised to dominate the software type segment as it forms the foundation of carbon accounting practices. Organizations prioritize accurate measurement, monitoring, and reporting of Scope 1, 2, and 3 emissions to meet regulatory and investor expectations. These platforms provide end-to-end capabilities, including automated data collection, real-time emission tracking, audit-ready reporting, and compliance alignment with global standards. As regulatory pressure intensifies and ESG disclosures become mandatory, enterprises increasingly rely on emission management solutions as their primary tool. Compared to carbon offsetting and energy management tools, emission management software delivers direct value in compliance and transparency, making it the most widely adopted and essential category across industries and enterprise sizes globally.

By Deployment Mode Analysis

Cloud-based deployment is expected to dominate the carbon accounting software market due to its scalability, flexibility, and cost-effectiveness. Organizations prefer cloud platforms because they enable real-time data access, seamless integration with enterprise systems, and centralized emissions tracking across global operations. These solutions support continuous updates to reflect evolving regulatory frameworks, reducing the burden of manual upgrades. Additionally, cloud-based tools facilitate collaboration across departments and geographies, which is critical for managing Scope 3 emissions. Subscription-based pricing models further enhance affordability, especially for SMEs. As digital transformation accelerates and remote accessibility becomes essential, cloud deployment continues to outperform on-premises and hybrid models, positioning itself as the preferred infrastructure for modern carbon management systems.

By Enterprise Size Analysis

Large enterprises is anticipated to dominate this segment due to their complex operational structures, extensive supply chains, and higher regulatory exposure. These organizations face stringent ESG disclosure requirements and are often under pressure from investors and stakeholders to demonstrate measurable sustainability progress. As a result, they invest significantly in advanced carbon accounting platforms capable of handling large-scale, multi-location data. Large enterprises also have the financial resources and technical capabilities to implement integrated software solutions across departments. Their early adoption of net-zero commitments further drives demand for sophisticated analytics, reporting, and scenario modeling tools. While SMEs are increasingly adopting such solutions, large enterprises remain the primary contributors to market revenue and innovation adoption.

By Application Analysis

ESG and sustainability reporting is poised to dominate the application segment as organizations prioritize transparent communication of their environmental impact. Increasing regulatory mandates, investor scrutiny, and stakeholder expectations have made standardized ESG disclosures a business necessity. Carbon accounting software plays a critical role in generating accurate, audit-ready reports aligned with frameworks such as GHG Protocol and other global standards. Companies use these platforms to consolidate emissions data, track performance against sustainability goals, and ensure compliance with disclosure requirements. Compared to other applications, ESG reporting directly influences corporate reputation, investment decisions, and regulatory compliance. This makes it the most critical and widely adopted use case, driving consistent demand across industries worldwide.

By Vertical Analysis

The energy and utilities sector is expected to dominate the vertical segment due to its inherently high carbon footprint and strict regulatory oversight. Companies in this sector are major contributors to global emissions and are therefore subject to rigorous monitoring, reporting, and reduction mandates. Carbon accounting software is essential for tracking emissions across generation, transmission, and distribution operations. Additionally, the transition toward renewable energy and decarbonization strategies requires advanced analytics and scenario modeling capabilities. These organizations also lead in adopting digital tools to optimize energy efficiency and manage carbon costs. While other sectors are increasing adoption, the scale, complexity, and regulatory pressure within energy and utilities ensure its continued dominance in the market.

The Global Carbon Accounting Software Market Report is segmented on the basis of the following:

By Software Type

- Emission Management Software

- Carbon footprint calculation & reporting

- Emission tracking & monitoring

- Regulatory compliance management

- Carbon Offsetting Software

- Carbon credit management

- Offset project tracking & verification

- Energy Management Software

- Energy consumption analytics

- Renewable energy integration

- Efficiency optimization

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Application

- Carbon Footprint Tracking

- ESG & Sustainability Reporting

- Regulatory Compliance & Disclosure

- Supply Chain Emissions Analysis

- De-carbonization Strategy & Scenario Modeling

By Vertical

- Energy & Utilities

- IT & Telecom

- Healthcare

- Transportation & Logistics

- Retail & Consumer Goods

- Construction & Infrastructure

- Food & Beverages

- Chemicals

- Manufacturing

- Others

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global carbon accounting software market as it is projected to hold 37.8% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the carbon accounting software market because of the unmatched concentration of climate tech innovation hubs and the aggressive net-zero agendas of the Fortune 500 companies. The area has an established ecosystem of global system integrators, boutique climate consultancies, and rich pool of talent in carbon accounting and data science. Enterprise investment in artificial intelligence, advanced analytics, and the overall retirement of manual data collection methods contribute to the continued demand for emission management software and the continuous optimization of energy efficiency. Moreover, an optimistic venture capital climate persistently finances upcoming carbon accounting startups that need to achieve expeditious development and data security compliance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding carbon accounting software market, driven by government-led sweeping net-zero commitments in India, China, Japan, and Southeast Asia. The fast-paced economic growth, the rise of a climate-conscious middle-income population, and the dynamic expansion of corporate ESG reporting is compelling established conglomerates and state-owned enterprises to discard unproductive manual data-gathering methods. De-carbonization Strategy & Scenario Modeling is in high demand to help these large organizations head in the direction of Paris-aligned operating models. There is also a severe lack of qualified carbon accounting talent in the region, and it is necessary to deploy automated software platforms to calculate, track, and report emissions to cover the skills gap and enable faster progress on validated climate targets.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global carbon accounting software market has become highly dynamic with a heterogeneous array of multinational enterprise software giants, sustainability divisions of the large ratings agencies, and niche climate-native platform providers. The key to success will be profound strategic alliances with ESG assurance firms, data brokers, and ERP providers like SAP and Microsoft because they will open the necessary co-selling opportunities and early access to new data connectivity capabilities. The movement towards market consolidation is rapidly progressing with traditional financial accounting software companies acquiring carbon data engineering and supply chain analytics specialized boutiques to stay afloat. Proprietary intellectual property, including automated emission factor engines and industry-specific data models for Scope 3, is becoming a more important basis of competitive differentiation than just generic reporting templates or generic user interfaces.

Some of the prominent players in the Global Carbon Accounting Software Market are:

- IBM

- Microsoft

- Salesforce

- Persefoni

- Watershed

- Sweep

- Greenly

- SAP

- Sphera

- Normative

- Emitwise

- Plan A

- Planetly

- Carbon Analytics

- Net0

- CarbonetiX

- Evalue8

- Carbonbase

- The Carbon Accounting Company

- Pangolin Associates

- Other Key Players

Recent Developments

- January 2026: Salesforce declared it will integrate a major expansion of its Net Zero Cloud with AI-driven Carbon Footprint Calculation & Reporting capabilities, a software initiative to assist clients in Manufacturing and Transportation & Logistics to automate Scope 3 data ingestion and categorize supplier emissions.

- November 2025: IBM strengthened its collaboration with Microsoft and introduced a specific software module combining Regulatory Compliance Management and ESG & Sustainability Reporting aimed at helping Chemicals and Energy clients move compliance workflows to the cloud and keep in line with evolving EU CSRD requirements.

- October 2025: Persefoni purchased a European carbon credit verification platform to further its Carbon Credit Management and Offset Project Tracking & Verification solutions for voluntary carbon markets, supporting the complicated requirements of Financial Services and corporate buyers in generating credible net-zero claims.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 34.6 Bn |

| Forecast Value (2035) |

USD 223.4 Bn |

| CAGR (2026–2035) |

23.0% |

| The US Market Size (2026) |

USD 11.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Software Type, By Deployment Mode, By Enterprise Size, By Application, and By Vertical |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Carbon Accounting Software Market?

▾ The Global Carbon Accounting Software market is poised to be valued at USD 34.6 billion in 2026 and is projected to reach USD 223.4 billion by 2035, driven by the universal need for specialized platforms in emissions measurement, regulatory reporting, and AI-driven de-carbonization strategy.

What is the CAGR of the Global Carbon Accounting Software Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 23.0% from 2026 to 2035, reflecting the accelerating complexity of global climate disclosure regulations and the persistent shortage of internal sustainability expertise.

What factors are driving the growth of the Global Carbon Accounting Software Market?

▾ Key drivers include the global sustainability skills gap, the imperative to automate legacy manual reporting methods, the management complexity of multi-tier Scope 3 data, and the surge in demand for Regulatory Compliance Management amid evolving climate disclosure mandates.

Which region held the largest share of the Carbon Accounting Software Market in 2026?

▾ North America, specifically the United States, held 37.8% of the market share in 2026, driven by a mature climate technology ecosystem and aggressive enterprise investment in Carbon Footprint Calculation & Reporting and AI-driven emissions analytics.

Which region is expected to grow the fastest in the Carbon Accounting Software Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid net-zero commitments in India, China, and Japan, where De-carbonization Strategy & Scenario Modeling is critical for transitioning large conglomerates to Paris-aligned operations.

What are the major trends in the Global Carbon Accounting Software Market?

▾ Major trends include the integration of Generative AI into carbon data workflows, the rise of supplier-side Scope 3 platforms, the convergence of financial and carbon data, and the focus on Energy Consumption Analytics within complex manufacturing environments.

Who are the key players in the Global Carbon Accounting Software Market?

▾ Key players include enterprise software giants like Salesforce, SAP, and Microsoft, as well as climate-native platforms like Persefoni, Watershed, and Sphera, alongside established ESG reporting platforms like Workiva.

How is the Global Carbon Accounting Software Market segmented?

▾ The market is segmented by Software Type, Deployment Mode, By Enterprise Size, By Application, and By Vertical.