Market Snapshot

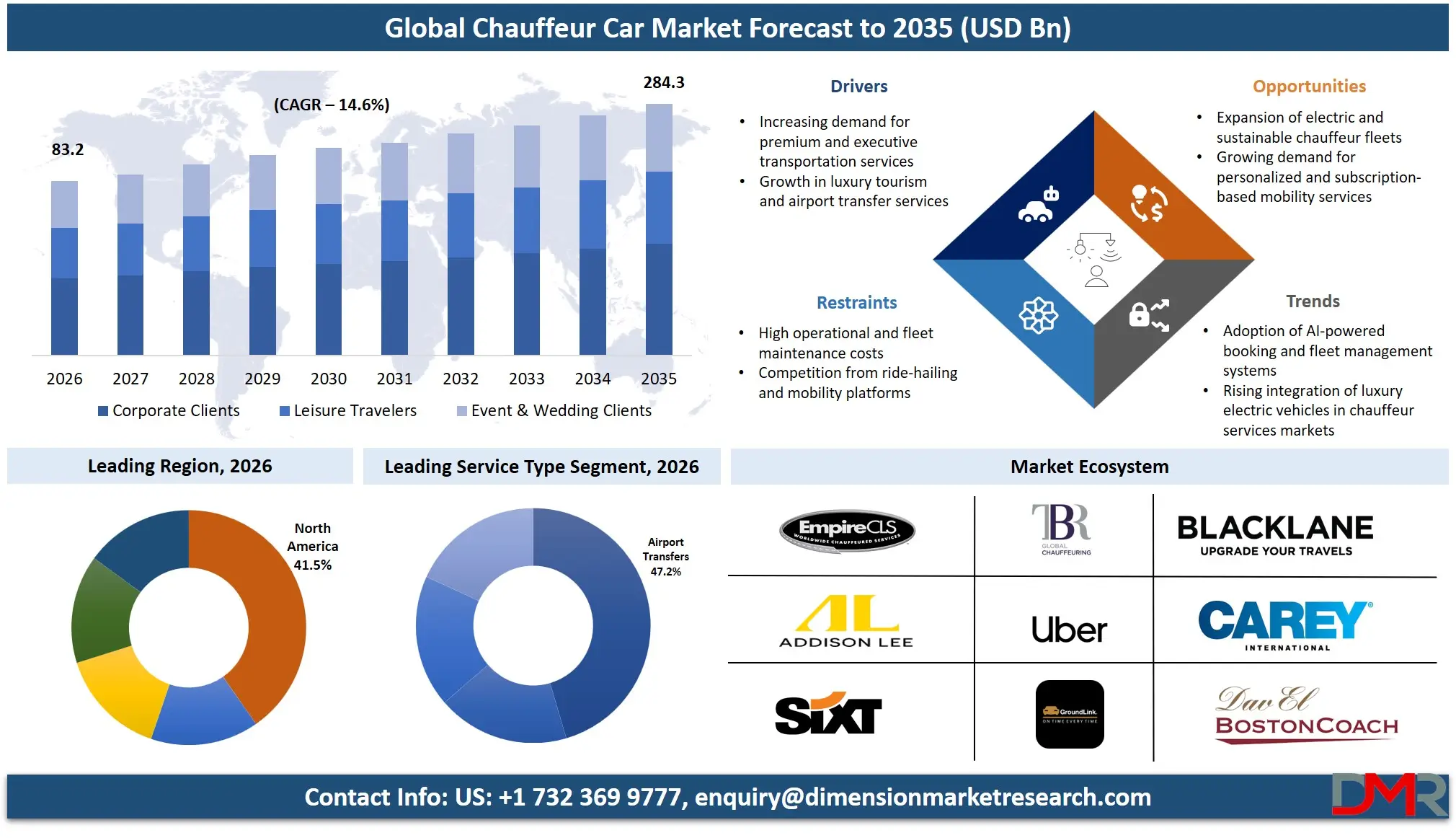

- The Global Chauffeur Car Market is set to be valued at USD 83.2 Billion in 2026 and is forecast to reach USD 284.3 Billion by 2035, at a CAGR of 14.6% from 2026 to 2035.

- By Vehicle Type, Luxury Cars hold the leading position with a 44.5% revenue share in 2026.

- By Customer Type, Corporate Clients dominate with a 54.1% revenue share in 2026.

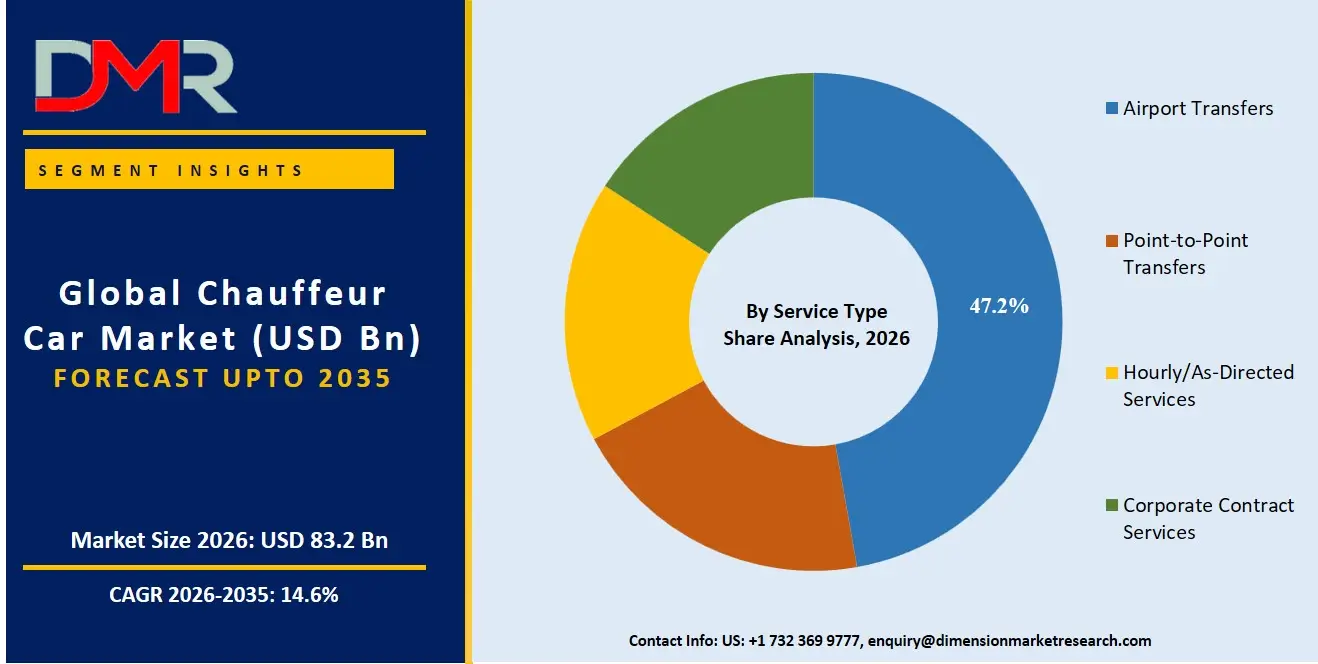

- By Service Type, Airport Transfers lead with a 47.2% revenue share in 2026.

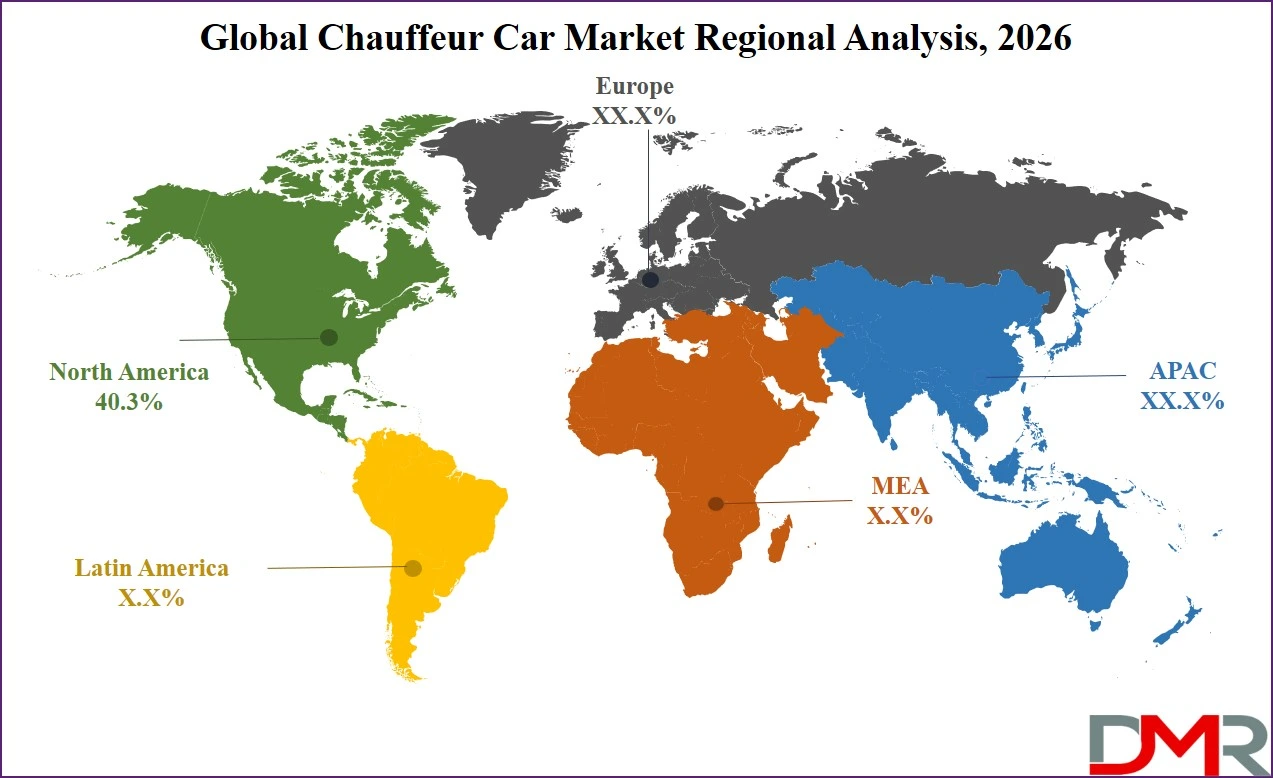

- North America is the leading region, accounting for 41.5% of global revenue in 2026.

- Uber's premium tier (Black/Comfort/SUV) recorded annualized gross bookings exceeding USD 10 Billion with 35% year-on-year growth in 2024, signaling the scale of premium ground transport demand.

- Uber agreed to acquire Blacklane in March 2026, with Blacklane operating across more than 500 cities in over 60 countries at the time of the deal.

- Lyft acquired TBR Global Chauffeuring in October 2025 for £83 million (~USD 110 million), reflecting active consolidation among major mobility platforms.

Market Overview

Global Chauffeur Car Market size is expected to be worth around USD 284.3 Billion by 2035 from USD 83.2 Billion in 2026, growing at a CAGR of 14.6% during the forecast period 2026 to 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The chauffeur car market covers professionally driven, pre-booked ground transportation services delivered through licensed operators. This includes airport transfers, point-to-point rides, hourly-directed services, and corporate contract bookings. The market does not include standard ride-hailing, taxis, or self-drive rentals. This distinction matters because chauffeur services carry a fundamentally different cost and service structure than mass-market mobility.

The market spans five vehicle categories luxury cars, SUVs, vans, limousines, and executive cars and serves three primary customer groups: corporate clients, leisure travelers, and event or wedding clients. Corporate clients alone account for 54.1% of revenue, confirming that the market's financial backbone is business travel, not consumer leisure. This concentration creates predictable, contract-based revenue streams that reduce volatility for operators.

Airport transfers lead by service type with a 47.2% share, which reflects a structural link between premium ground transport and premium aviation. The Air India–Avis India partnership, which offers up to 20% discounts on chauffeur-driven cars across 17 Indian cities, and Etihad Airways' reinstatement of complimentary global chauffeur service for first-class passengers from August 1, 2025, both confirm that airlines are actively using chauffeur access as a premium differentiator. For chauffeur operators, airline partnerships are now a distribution channel, not just a referral source.

North America holds 41.5% of global revenue, though not the fastest-growing region. Operators already present in North America must defend share rather than rely on market expansion alone.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Platform consolidation is reshaping the competitive structure faster than organic fleet growth. Uber announced an agreement to acquire Blacklane in March 2026 a platform operating across more than 500 cities and 60+ countries to power Uber Elite, its new chauffeur-style tier above Uber Black. Lyft acquired TBR Global Chauffeuring in October 2025 for £83 million. These moves signal that technology platforms have identified chauffeur services as the premium layer missing from their existing offerings.

Market Size and Forecast

The Global Chauffeur Car Market stands at USD 83.2 Billion in 2026, according to DMR. This baseline reflects a market that has moved well beyond niche executive transport into a structured commercial sector with defined segments, regional hierarchies, and institutional investment. A market of this size commands serious strategic attention from both operators and investors.

The market is forecast to reach USD 284.3 Billion by 2035, implying a CAGR of 14.6% over the 2026–2035 forecast period. This pace of expansion is steep and reflects a market where demand is being unlocked at multiple layers simultaneously corporate contract consolidation, airline bundling, sovereign capital inflows, and platform-led premiumization. Each of these operates on a different timeline, which gives the forecast structural depth rather than dependence on a single variable.

A downside scenario emerges if cross-border licensing friction slows operator expansion and if corporate travel budgets tighten under macroeconomic pressure. The Katara Limousine case requiring a phased multi-year market entry with limited UAE remote operations in 2024, full UAE expansion only by end-2025, and Saudi Arabia active operations only from Q4 2025 shows that regulatory timelines directly compress revenue-generating windows. For any operator targeting multi-country buildout, regulatory drag is a real constraint on CAGR realization.

Market Dynamics

Platform-Led Premiumization and Airline Integration Are Redirecting Corporate Travel Spend Into Structured Chauffeur Channels

Airline-chauffeur bundling reinforces this channel. Air India and Avis India now offer chauffeur-driven cars at up to 20% discounts across 17 Indian cities, per Air India's press release. Etihad Airways extended complimentary chauffeur service globally to all first-class passengers from August 1, 2025, expanding from previously UAE-only coverage. These integrations embed chauffeur access into the premium aviation booking journey, capturing passengers before they reach the ground transport decision independently.

Fragmented Licensing Regimes and Urban Safety Gaps Constrain Operator Scalability Across Key Growth Markets

The practical implication is that operators with geographically concentrated licenses cannot respond to demand spikes in adjacent markets without absorbing multi-year regulatory lead times. For global platforms attempting rapid multi-country rollouts, this friction is a meaningful constraint on the speed at which market share can be captured. Regulatory readiness must be treated as a strategic investment, not a back-office function.

Consolidation Activity and India's Premium Fleet Expansion Open Structural Entry Points for Operators and Capital Allocators

However, consolidation at the platform level simultaneously opens white space at the regional and specialist level. Katara Limousine's deployment of a coordinated 20+ luxury vehicle fleet for a VVIP delegation in Riyadh in January 2026 demonstrates that high-margin government and protocol transport remains a niche where specialist operators hold a structural advantage over generalist platforms. This segment is underserved by technology-first players and offers premium pricing with lower price sensitivity.

Market Trends

Invitation-Only Service Tiers, Corporate Funnel Integration, and Gender-Specific Offerings Are Redefining How Chauffeur Services Compete for Share

Uber launched Uber Elite in March 2026 as an invitation-only chauffeur tier above Uber Black, featuring commercially licensed chauffeurs, luxury vehicles under three years old, in-terminal Meet and Greet airport pickup, and 24/7 support, per Uber Newsroom. The initial rollout targeted Los Angeles and San Francisco, with New York City expansion planned. This tiering strategy tells operators that exclusivity not just quality is becoming a product feature in itself.

Vehicle Type Analysis

Luxury Cars dominate with 44.5% due to corporate client preference for premium sedans.

In 2026, Luxury Cars held a dominant market position in the By Vehicle Type segment of the Chauffeur Car Market, with a 44.5% share. Luxury sedans remain the default vehicle class for corporate airport transfers and executive point-to-point journeys. Their combination of cabin privacy, brand signaling, and driver professionalism makes them the lowest-risk choice for corporate travel managers specifying fleet standards in contract agreements.

Vans serve airport group transfers and event transportation where passenger volume exceeds sedan capacity. This sub-segment captures incremental revenue per booking by consolidating multiple passengers into a single dispatch. For operators managing corporate accounts, van capacity reduces per-seat costs and improves fleet utilization during peak transfer windows.

Limousines remain concentrated in event, wedding, and ceremonial transport. Their share of the overall vehicle mix is structurally constrained by limited use cases and higher operating costs relative to revenue frequency. However, limousines carry premium per-trip pricing that supports strong margin contribution for operators with event-focused client bases.

Executive Cars occupy the segment between standard luxury sedans and full limousines, serving senior corporate travelers who require comfort and discretion without the visual prominence of a limousine. This category benefits directly from the airline-chauffeur bundling trend, as first-class and business-class passengers represent the core demographic for executive car deployment.

Customer Type Analysis

Corporate Clients dominate with 54.1% due to high-frequency contract-based booking volumes.

In 2026, Corporate Clients held a dominant market position in the By Customer Type segment of the Chauffeur Car Market, with a 54.1% share. Corporate accounts generate predictable, recurring revenue through annual contracts and travel management company integrations. This structural predictability allows operators to optimize fleet deployment and driver scheduling with a level of efficiency that event-driven or leisure bookings cannot support.

Event and Wedding Clients form the most price-inelastic sub-segment in the customer mix. Bookings in this category are low in frequency but high in per-transaction value, with significant vehicle and service customization involved. For operators, event clients require dedicated fleet capacity and scheduling infrastructure that cannot be easily shared with corporate contract operations, making this sub-segment operationally distinct.

Service Type Analysis

Airport Transfers dominate with 47.2% due to scheduled flight integration and predictable dispatch windows.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In 2026, Airport Transfers held a dominant market position in the By Service Type segment of the Chauffeur Car Market, with a 47.2% share. The structural link between premium aviation and premium ground transport is well-established. Uber Elite's in-terminal Meet and Greet airport pickup, launched in March 2026 per Uber Newsroom, is a direct response to this demand pattern. Flight-tracking integration and fixed pickup windows make airport transfers the most operationally predictable service type, supporting high fleet utilization.

Hourly and As-Directed Services carry the highest per-trip revenue potential because the meter runs on time rather than distance. Corporate clients and VVIP travelers who require a vehicle to remain on standby throughout a full business day generate significantly more revenue per booking than fixed-route transfers. This service type is where operator relationships and driver quality matter most, as extended engagements expose any service inconsistency.

Booking Channel Analysis

Offline and Traditional Booking retains relevance for high-value corporate contract renewals, government protocol arrangements, and VVIP engagements where personal account management is expected. Katara Limousine's coordinated VVIP fleet deployment in Riyadh in January 2026 reflects a relationship-led booking process that digital self-serve platforms are not yet equipped to replicate at this level of customization.

Mobile App-Based Booking is the channel where platform operators hold a structural advantage over independent operators. Uber's existing base of 171 million Monthly Active Platform Consumers as of Q4 2024, per Uber Investor Relations, creates a pre-installed distribution channel for Uber Elite and Uber Black that standalone chauffeur operators cannot replicate without equivalent app penetration.

Key Market Segments

By Vehicle Type

- Luxury Cars

- SUVs

- Vans

- Limousines

- Executive Cars

By Customer Type

- Corporate Clients

- Leisure Travelers

- Event & Wedding Clients

By Service Type

- Airport Transfers

- Point-to-Point Transfers

- Hourly/As-Directed Services

- Corporate Contract Services

By Booking Channel

- Online Booking Platforms

- Offline/Traditional Booking

- Mobile App-Based Booking

Regional Analysis

North America Dominates the Chauffeur Car Market with a Market Share of 41.5%

North America holds 41.5% of global chauffeur car revenue in 2026, as the region's dominance reflects deep corporate travel infrastructure, high per-trip pricing, and the presence of major platform operators. Uber Elite's launch in Los Angeles and San Francisco in March 2026 confirms that North America remains the primary testing ground for premium tier innovation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia Pacific Chauffeur Car Market Trends

Asia Pacific presents the widest range of market maturity within a single region. Australia's chauffeur car market is valued at USD 239.3 million in 2026, forecast to reach USD 737.8 million by 2035 at a CAGR of 11.9%. Taiwan's market is valued at USD 76.4 million in 2026, projected to reach USD 232.7 million by 2035 at a CAGR of 11.8%. India's premium segment is the highest-velocity opportunity in the region, as the Air India–Avis India partnership, covering chauffeur services across 17 Indian cities, embeds premium ground transport directly into airline distribution for the first time at this scale.

Denmark Chauffeur Car Market Trends

Denmark's Chauffeur Car Market is valued at USD 103.12 million in 2026, forecast to reach USD 355.5 million by 2035 at a CAGR of 13.2%. Denmark's CAGR of 13.2% is notably high for a mature Western European economy of its size. This trajectory reflects demand from a concentrated high-income corporate base, strong business travel activity relative to GDP, and premium service expectations that support above-average per-trip pricing. For operators, Denmark represents a high-margin, lower-volume market where service quality commands pricing power.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The Global Chauffeur Car Market is transitioning from a fragmented operator landscape toward a two-tier structure. A small group of technology-enabled platforms with global or multi-regional reach is pulling away from the long tail of city-specific and specialist operators. This bifurcation is being driven by acquisition activity, platform capital, and the distribution advantages that app-based booking confers at scale. Operators without technology infrastructure or institutional backing face compression on both pricing and customer acquisition.

However, regional specialist operators retain structural advantages in high-margin niches that platform generalists have not yet fully penetrated. VVIP protocol transport, government delegation movements, and event-specific fleet deployments require relationship-led account management and operational precision that technology platforms have not yet replicated at the same quality level. Operators who concentrate on these verticals and invest in service differentiation can sustain premium pricing and margin even as platform competition intensifies in the broader market.

Company Profiles

Uber Technologies Inc. enters the chauffeur segment not as a traditional operator but as a platform deploying its 171 million Monthly Active Platform Consumers and USD 54.1 Billion Q4 2025 Gross Bookings base as distribution infrastructure. Also, in March 2026 launch of Uber Elite, an invitation-only tier above Uber Black featuring commercially licensed chauffeurs and luxury vehicles under three years old combined with the Blacklane acquisition, signals a deliberate move to own the premium ground transport stack from booking to execution.

Carey International positions itself as a specialist in corporate and government ground transport with a managed services model that prioritizes compliance, duty of care, and global account management over consumer-facing app adoption. This approach serves multinational corporations and government clients whose procurement requirements favor structured contracts over platform-based bookings. Carey's strategic positioning becomes more defensible as platform operators commoditize the consumer-facing premium tier while corporate procurement standards remain relationship-dependent.

Key Players

- Blacklane

- Carey International

- Addison Lee

- EmpireCLS Worldwide Chauffeured Services

- Dav El | BostonCoach

- GroundLink

- TBR Global Chauffeuring

- SIXT

- Uber Technologies

- Lyft

- Limos.com

- GetTransfer

- Gett

- Wheely

- Europcar Mobility Group

- Mears Transportation Group

- Chauffeur Privé

- A1A Airport & Limousine Service

- Allied Limousine International

- Global Limousines

Supply Chain and Value Chain Analysis

The chauffeur car value chain runs from vehicle manufacturing and fleet acquisition through operator infrastructure, driver engagement, and booking technology, to the end customer experience at point of dispatch and journey completion. The most capital-intensive stage is fleet ownership and maintenance, which requires continuous reinvestment to meet the vehicle-age and brand standards that premium clients expect. Addison Lee's investment of over £30 million in vehicle upgrades in a single financial year, per its own reporting, illustrates the recurrent capital commitment that fleet-based operators carry.

Airline partnerships represent an emerging distribution layer that bypasses traditional booking channels entirely. Air India's partnership with Avis India delivering chauffeur-driven cars at up to 20% discounts across 17 cities, per Air India's and Etihad Airways' extension of global chauffeur service to all first-class passengers from August 1, 2025, demonstrate that airlines are inserting themselves as demand aggregators between premium travelers and ground operators. For chauffeur operators, securing airline distribution partnerships is now a supply chain decision as much as a sales activity, since it determines access to the highest-value customer segment at the point of flight booking.

Regulatory Landscape

The GCC regulatory environment requires operators to demonstrate physical presence, licensed local partnerships, and fleet registration within each jurisdiction before commercial dispatch begins. Katara Limousine's structured phased entry across UAE and Saudi Arabia illustrates that even operators with established credentials in neighboring markets cannot transfer operating licenses across borders. This creates a meaningful barrier that protects incumbents and raises the cost of entry for new regional competitors.

Autonomous vehicle deployment is entering the regulatory agenda for chauffeur-adjacent platforms. Stellantis and Bolt announced a partnership in December 2025 to deploy autonomous vehicles including the eK0 medium van and STLA Small platforms into Bolt's ride-hailing network across European countries, with trials beginning in 2026. Also, European regulators will need to establish clear frameworks for commercially licensed autonomous vehicles operating in shared urban transport, and the outcome of these trials will set precedents for how autonomous technology integrates with chauffeur service licensing standards.

Recent Developments

- March 30, 2026 — Uber Technologies announced an agreement to acquire Berlin-based global chauffeur platform Blacklane, which operates across more than 500 cities in over 60 countries, to expand into luxury and executive travel and power its newly launched Uber Elite service.

- October 15, 2025 — Lyft acquired Glasgow-based TBR Global Chauffeuring for £83 million (~USD 110 million) in cash plus contingent consideration to strengthen its premium ground transportation offering.

- December 8, 2025: Stellantis and Bolt announced a partnership to deploy autonomous vehicles including the eK0 medium van and STLA Small platforms into Bolt's ride-hailing network across European countries, with trials beginning in 2026.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 83.2 Billion |

| Forecast Revenue (2035) |

USD 284.3 Billion |

| CAGR (2026–2035) |

14.6% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020–2024 |

| Forecast Period |

2026–2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Vehicle Type (Luxury Cars, SUVs, Vans, Limousines, Executive Cars); By Customer Type (Corporate Clients, Leisure Travelers, Event & Wedding Clients); By Service Type (Airport Transfers, Point-to-Point Transfers, Hourly/As-Directed Services, Corporate Contract Services); By Booking Channel (Online Booking Platforms, Offline/Traditional Booking, Mobile App-Based Booking) |

| Regional Analysis |

North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape |

Blacklane, Addison Lee, Sixt Limousine Service (Sixt SE), Carey International, EmpireCLS Worldwide Chauffeured Services, BostonCoach, TBR Global Chauffeuring, Uber Technologies Inc. |

| Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options |

Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions

What is the current size of the Global Chauffeur Car Market?

▾ The Global Chauffeur Car Market is valued at USD 83.2 Billion in 2026, according to DMR. This reflects a market that spans corporate contract services, airport transfers, leisure, and event transport across all major global regions.

What is the forecast growth rate of the Chauffeur Car Market?

▾ The market is forecast to reach USD 284.3 billion by 2035, growing at a CAGR of 14.6% over the 2026–2035 period. This trajectory is supported by platform consolidation, airline-chauffeur bundling, and sovereign capital investment in premium mobility infrastructure.

Which vehicle type segment leads the Chauffeur Car Market?

▾ Luxury Cars lead the By Vehicle Type segment with a 44.5% revenue share in 2026. Their dominance reflects the preference of corporate clients and premium aviation passengers for sedan-class vehicles that combine cabin privacy with brand-appropriate presentation.

Which customer type generates the most revenue in this market?

▾ Corporate Clients account for 54.1% of market revenue in 2026, making them the largest and most structurally important customer group. Corporate accounts generate predictable, contract-based booking volumes that support efficient fleet deployment and driver scheduling.

Which service type holds the largest share in the Chauffeur Car Market?

▾ Airport Transfers lead the By Service Type segment with a 47.2% revenue share in 2026. The structural link between premium aviation and premium ground transport reinforced by airline chauffeur partnerships and flight-tracking-enabled dispatch makes this the most operationally predictable and consistently utilized service category.

Which region dominates the Global Chauffeur Car Market?

▾ North America leads with a 41.5% revenue share in 2026, as the region benefits from deep corporate travel infrastructure, high per-trip pricing, and the presence of major platform operators actively investing in premium tier development.

Which region offers the fastest growth opportunity in this market?

▾ Asia Pacific particularly offers the most defined high-growth opportunity

Who are the leading companies in the Chauffeur Car Market?

▾ Key players include Blacklane, Addison Lee, Sixt Limousine Service (Sixt SE), Carey International, EmpireCLS Worldwide Chauffeured Services, BostonCoach, TBR Global Chauffeuring, and Uber Technologies Inc. Blacklane was acquired by Uber in March 2026 for a reported €900 million, while Addison Lee was acquired by ComfortDelGro in October 2024.

What are the biggest drivers of growth in the Chauffeur Car Market?

▾ Airline-chauffeur integration through Air India's partnership with Avis India across 17 cities and Etihad Airways' global first-class chauffeur rollout from August 1, 2025 is embedding chauffeur access directly into premium aviation booking journeys.