What is the Global Chemical Waste-to-Feedstock Market Size?

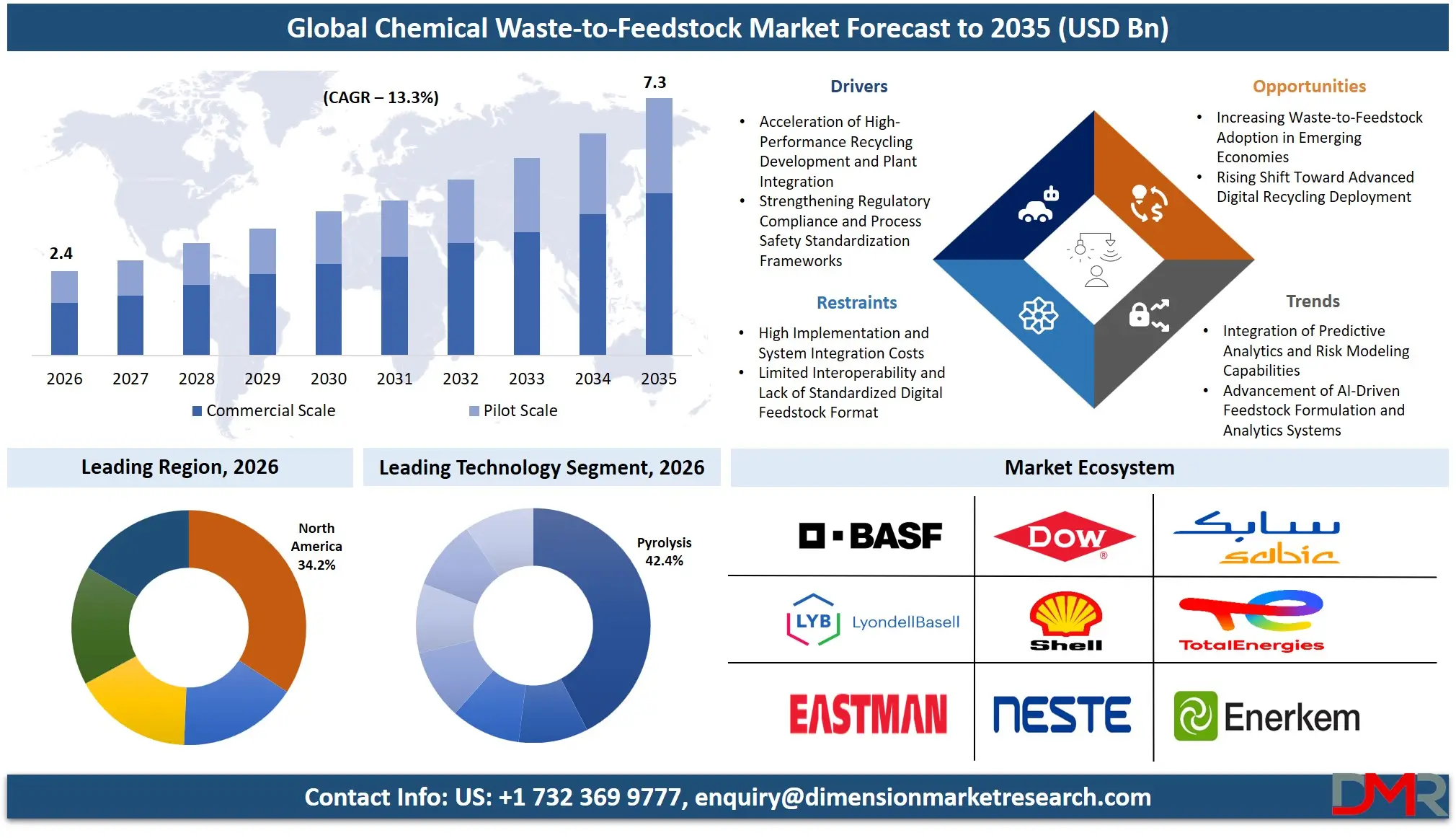

The Global Chemical Waste-to-Feedstock Market size is estimated at USD 2.4 billion in 2026 and is projected to reach USD 7.3 billion by 2035, exhibiting a CAGR of 13.3% during the forecast period, driven by the rising use of real-time feedstock quality monitoring and automated process validation, decentralized chemical recycling deployment patterns in modular plant architectures, and connected digital governance and compliance management systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global chemical waste-to-feedstock market is expanding because of increasing use of high-fidelity reactor compatibility testing and impurity profiling in detecting and analyzing anomalous catalytic activity patterns, increasing regulatory mandates, which reduce the chance of thermal runaway during chemical recycling operations and speed up compliance audits for new processing plants, and more funding in automating privacy-preserving feedstock logging.

Some other reasons for expansion in this market include new technologies in runtime process stability management, catalyst fouling prediction through behavior analytics, automated solvent-based feedstock handling, high-volume process data platforms, and improved cross-supplier feedstock-sharing rules. The digital shift in specialty chemical recycling and batch processing has been helpful in speeding up product development and making sensitive process transaction management easier. This includes halogenated solvent analytics research. In addition, government plans focusing on preventing industrial accidents and the secure chemical materials economy have ensured steady research in waste-to-feedstock systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

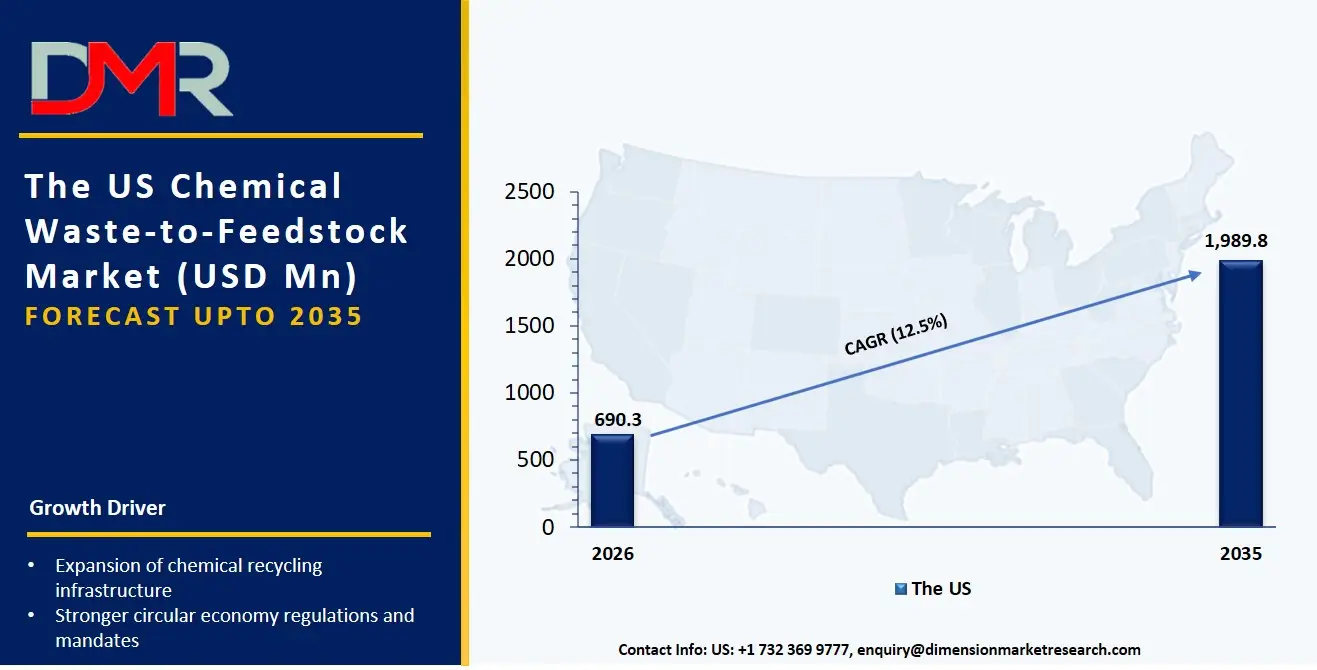

The US Chemical Waste-to-Feedstock Market

The US Chemical Waste-to-Feedstock Market is estimated to grow to USD 690.3 million in 2026 with a compound annual growth rate of 12.5% during the forecast period.

The US market is shaped by major federal and state-level programs promoting fire-resistant process architectures, secure digital adoption supported by DOE and NIST, and DOD-led chemical modernization initiatives. These programs encourage the use of high-purity solvent processing, real-time impurity-in-solution protection, and predictive compliance software for waste processing. Automated process safety platforms are being rapidly adopted, and the US continues to invest in better data sharing between R&D labs, encrypted feedstock audit systems, and reliable thermal runaway detection tools for waste-to-feedstock platforms. Service providers are also influenced by laws like EPA RCRA, OSHA PSM, and national digital chemical strategies to offer services that ensure process safety, rule-following, and smooth integration across hybrid and modular plant environments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Chemical Waste-to-Feedstock Market

The European Chemical Waste-to-Feedstock Market is estimated to be valued at USD 792.0 million in 2026, witnessing growth at a CAGR of 11.9%, during the forecast period.

Europe's chemical waste-to-feedstock market is well-established, shaped by EU-wide policies such as the Circular Economy Action Plan, the Waste Framework Directive, and national policies to support sustainable digital markets (e.g., Germany's chemical recycling digital plans and France's national plastic waste strategies). Countries are also making process safety management more flexible to align plant operators and customer demands and enable the sharing of anonymized feedstock data across borders. The market grows due to new tools like software for real-time viscosity validation and risk scoring systems for process thermal stability. Use is made easier by teamwork between public and private groups and shared digital safety rules. Manufacturers have access to technologies such as sulfide-based solid process fine-tuning, solvent interaction modeling, and secure process audit logging, and Europe is at the forefront of the digitisation of safe and efficient chemical recycling operations.

Japan Chemical Waste-to-Feedstock Market

The Japan Chemical Waste-to-Feedstock Market is projected to be valued at USD 136.8 million in 2026, progressing at a CAGR of 10.7%, during the period spanning from 2026 to 2035.

Japan's chemical waste-to-feedstock market is well developed, with high-purity halogenated solvent data platforms, connected secure process blending management systems, and a wide array of process aging simulation software tools. National focus on automation, efficiency, and process integrity is delivered via catalytic activity models and smart process protection. Growth opportunities are helped by government measures under the Green Growth Strategy by Japan's Ministry of Economy, Trade and Industry (METI), and continued investment in chemical recycling cloud modernization. AI-driven process research, multi-party analytics for application-specific feedstock data sharing, and virtualized process safe environments all need effective waste-to-feedstock software to keep pace with high-voltage chemical recycling. Higher costs for validating new waste-to-feedstock systems and connecting them with older infrastructure are significant, but there are opportunities for the export of Japanese chemical recycling technologies to the Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Chemical Waste-to-Feedstock Market is estimated to be valued at USD 2.4 billion in 2026 and is expected to grow to USD 7.3 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 13.3% in the forecast period.

- Primary Growth Drivers: The availability of new recycling technologies that use real-time degradation detection, the need to speed up compliance results and improve success rates of feedstock data sharing, and more government investment in a national secure chemical material infrastructure are key growth drivers.

- Key Market Trends: The real-time profiling of process thermal stability risks, halogenated solvent handling, and the shift to AI-driven feedstock formulation platforms and automated digital asset inventory management are key market trends.

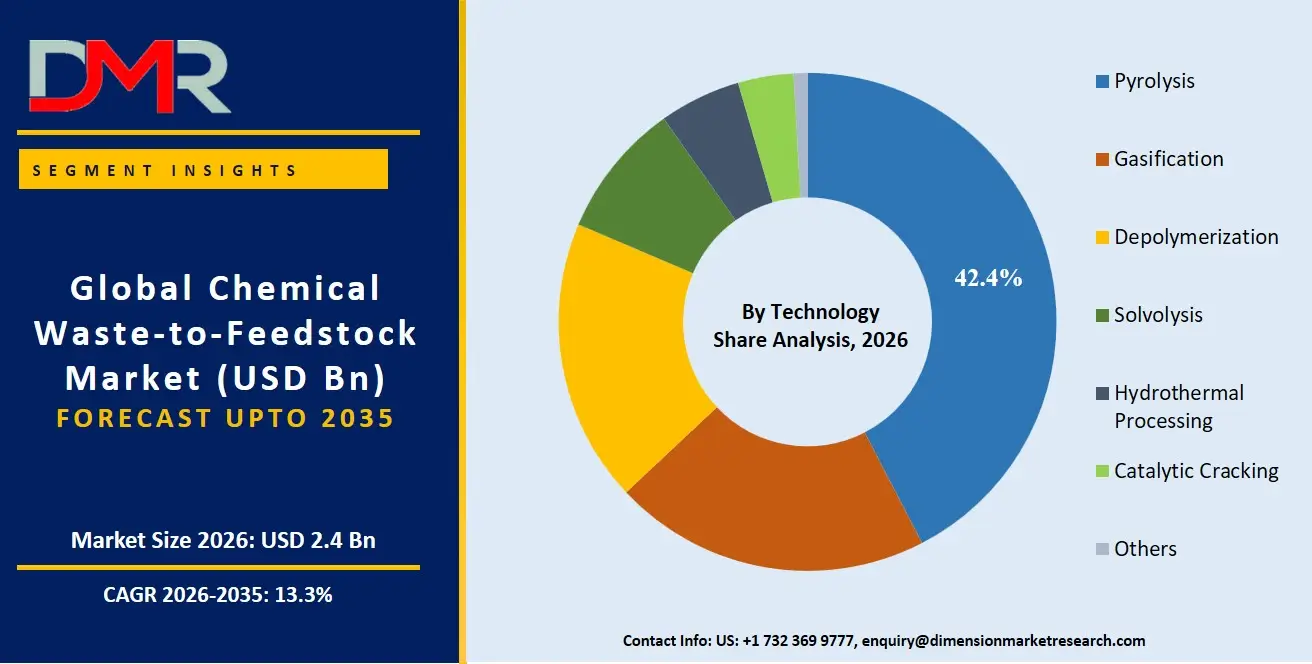

- By Technology: The Pyrolysis segment is expected to take the largest revenue share in the global chemical waste-to-feedstock market in 2026.

- By Waste Type: Plastic Waste is expected to take the largest revenue share in 2026 in the chemical waste-to-feedstock market.

- By End-Use Industry: The Chemicals & Petrochemicals segment is estimated to take the lead in 2026 with the largest share in the chemical waste-to-feedstock market.

- Regional Leadership: North America is estimated to take the lead in 2026 with 34.2% share in the chemical waste-to-feedstock market.

What is Chemical Waste-to-Feedstock?

Chemical Waste-to-Feedstock refers to a combination of thermo-chemical and real-time monitoring technologies that provide waste processors, plant operators, and compliance entities with enhanced capabilities beyond basic waste management, including helping to protect process formulations during recycling, preventing thermal runaway via solvent engineering, and enabling secure multi-party feedstock analytics. They include simulation & modeling software, asset performance management platforms, process optimization tools, and visualization systems. These platforms use modern systems such as real-time viscosity validation, digital asset inventory management software, and remote process advisory to manage, verify, and track sensitive process events and results. To improve chemical safety outcomes, manage process variability and application-specific programs, and expand protection into customized digital coverage to support individual plant designs and promote the development of safe recycled feedstocks.

Use Cases

- Market Stability for Daily Operations: Chemical waste-to-feedstock platforms can provide market-balancing benefits through software (encrypted feedstock analytics, attestation) and control systems to reduce thermal runaway risk and support settlement of safe process transactions in minutes, compared to days that it would take with only manual process handling.

- Long-Term Sensitive Chemical Asset Management: Long-term data on ongoing process stability issues, including catalytic activity intermittency, chemical waste price spikes, or process degradation, are studied to better understand market performance and to help plan long-term software-based chemical recycling care.

- Workload Load Balancing: Process safety is handled through waste-to-feedstock platforms and smart software in modular plant and corporate settings to support market capacity balance for high-volume chemical recycling workloads.

- Government & Regulated Programs: Faster waste-to-feedstock software development helps data innovation and development of targeted safe recycling programs; government programs, through smart monitoring of national chemical material data, advance national chemical protection strategies and help the adoption of operational standards.

How AI Is Transforming the Global Chemical Waste-to-Feedstock Market?

Artificial intelligence (AI) is being used progressively more often in chemical waste-to-feedstock platforms to improve feedstock demand forecasting, find safety quality trends in catalytic activity patterns, and automatically spot unusual degradation patterns in chemical recycling data. It also allows faster process thermal verification because it can handle digital feedstock submissions on a large scale. Encrypted process audit logs are easier to study and help registries find integration issues, reduce mistakes, and improve the overall accuracy of process certification. This has resulted in operations being cost-effective, quicker, and more efficient than the old manual review method.

AI is also strengthening research and development by improving process risk assessment and enabling more accurate capacity planning for waste processing. It helps chemical recyclers predict how many safe process batches will be needed, find possible catalytic activity delays, and monitor the performance of process safety networks more effectively. In addition, automation of routine process compliance checks and performance tracking is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is leading to better financial results and more stable operations across the chemical waste-to-feedstock production chain.

Market Dynamics

Key Drivers of the Global Chemical Waste-to-Feedstock Market

Acceleration of High-Performance Recycling Development and Plant Integration

The market is growing with the rise of advanced digital formulations for chemical recycling plants, better management of sensitive chemical waste streams, and a closer connection between process performance monitoring and secure plant integration. Chemical waste-to-feedstock platforms provide real-time data that allows monitoring of catalytic activity, helping to spot degradation early, and checking process safety performance much faster. This has improved operational efficiency and reduced human errors and production costs. At the same time, demand for more automated research and development is being helped by more activity in predictive analytics for the assessment of individual process risks, as chemical science further digitizes waste formulation and material processing tasks.

Strengthening Regulatory Compliance and Process Safety Standardization Frameworks

There is increasing emphasis on chemical safety, feedstock purity, and rule-following within the chemical waste-to-feedstock system. Rules and frameworks such as the EU Circular Economy Action Plan, EPA RCRA, and chemical material modernization efforts in key markets are encouraging better waste handling practices and more structured chemical recycling safety processes. These advances are supporting the need for systems that can offer steady monitoring of sensitive chemical materials and standardized reporting. At the same time, active work to improve the sharing of process performance data and reduce verification issues is strengthening the need for more effective management systems in both government and private market participants.

Restraints in the Global Chemical Waste-to-Feedstock Market

High Implementation and System Integration Costs

The rollout of chemical waste-to-feedstock systems remains costly, requiring significant investment in simulation software, catalytic activity validation technologies, system integration, testing, and alignment with existing waste processing workflows. In addition, following environmental regulations such as the EU Waste Framework Directive and other regional laws adds to setup complexity. These factors increase upfront costs and can limit adoption, especially among smaller waste processors and new companies entering the market.

Limited Interoperability and Lack of Standardized Digital Feedstock Format

There is still fragmentation in the market in terms of digital feedstock formats and data handling procedures. Although some areas have put in place organized digital management systems, many waste processing plants continue to work with both legacy process control and modern automated simulation systems. Lack of standardized process thermal stability protocols limits the ability to share process performance data between chemical recyclers and digital platform suppliers and results in inefficiencies in production, deployment, and system integration.

Growth Opportunities in the Global Chemical Waste-to-Feedstock Market

Increasing Waste-to-Feedstock Adoption in Emerging Economies

Newly developing economies such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are slowly building their chemical recycling and waste-to-feedstock systems. These regions have long-term growth possibilities, with more people adopting advanced recycling, and with more companies becoming aware of chemical safety programs and slowly modernizing digital production infrastructure. These markets have few older waste processing systems and can be used with new, technology-driven waste-to-feedstock platforms that can grow over time.

Rising Shift Toward Advanced Digital Recycling Deployment

The move to safer chemical recycling systems, decentralized production networks, and real-time process performance checks is creating the adoption of advanced waste-to-feedstock systems. These systems allow centralized process data access, better coordination between chemical recyclers and market participants, and faster digital asset inventory management. Advanced digital setups are increasingly becoming a trend among modern recycling providers as operational efficiency becomes one of the competitive factors.

Global Chemical Waste-to-Feedstock Market Trends

Integration of Predictive Analytics and Risk Modeling Capabilities

Chemical waste-to-feedstock platforms are gradually adding data-driven technology to find process degradation trends and improve accuracy in digital asset inventory management. These systems allow chemical recyclers and plant operators to study their process units' catalytic activity behavior better, simplify the management of their digital portfolios, and improve their overall process performance. This move is slowly turning the industry more proactive and data-driven in chemical safety instead of being purely reactive in market operations.

Advancement of AI-Driven Feedstock Formulation and Analytics Systems

The use of AI-based feedstock formulation systems is currently becoming a basic part of today's chemical recycling operations. These systems allow real-time process stability monitoring, centralized digital asset administration, and better network coordination among market participants. Advanced waste-to-feedstock platforms are improving the efficiency and responsiveness of platform providers that operate in different regions by reducing dependence on manual formulation processes and allowing operations to grow more easily.

Research Scope and Analysis

The global chemical waste-to-feedstock market is witnessing strong growth driven by rising adoption of advanced recycling technologies, batch process optimization, and increasing demand for high-safety and high-efficiency chemical recycling processes. The market is segmented based on technology, waste type, feedstock type, scale of operation, and end-use industry.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Technology Analysis

The Pyrolysis segment is likely to continue dominating the market in 2026, accounting for approximately 38.5% of the global chemical waste-to-feedstock market share. This is due to its key role in enabling high-fidelity thermal decomposition, a wide operating parameter range, and long-term process stability, and its usefulness in various waste settings where operational efficiency is needed. Within Pyrolysis, the Fast Pyrolysis sub-segment holds the largest share, driven by high deployment volumes, automated demand for stable feedstock chemistry, and compliance requirements. The Gasification segment is driven by its key role in enabling syngas production, with Plasma Gasification leading, followed by Conventional Gasification. Depolymerization is the fastest-growing segment, supported by increasing PET and polyamide recycling mandates.

By Waste Type Analysis

The Plastic Waste segment is likely to continue holding the lead in 2026, accounting for approximately 44.2% of the global chemical waste-to-feedstock market share, driven by strong demand for circular polymer solutions, regulatory bans on landfilling, and flexible processing across technologies. This segment reflects the continued shift toward agile and data-driven chemical recycling operations. The Municipal Solid Waste (MSW) segment is the second-largest and fastest-growing, supported by urban waste management challenges and government incentives for waste diversion. Industrial Chemical Waste remains a mature segment focused on hazardous waste streams where data sovereignty and safety are critical.

By Feedstock Type Analysis

The Pyrolysis Oil segment is expected to dominate with around 31.7% market share in 2026, driven by its irreplaceable role as an intermediate feedstock for new polymers and fuels, enabling real-time quality control and contamination identification. Pyrolysis oil supports customized downstream processing plans because it can offer multiple levels of parameter tuning, capacity amounts, and yearly stability plans, delivering fast results while keeping process data within secure registry systems. The Syngas segment is the second-largest, driven by demand for hydrogen and methanol production. The Recycled Monomers segment is the fastest-growing within Feedstock Type, witnessing strong growth with increasing needs for closed-loop PET and polyamide recycling.

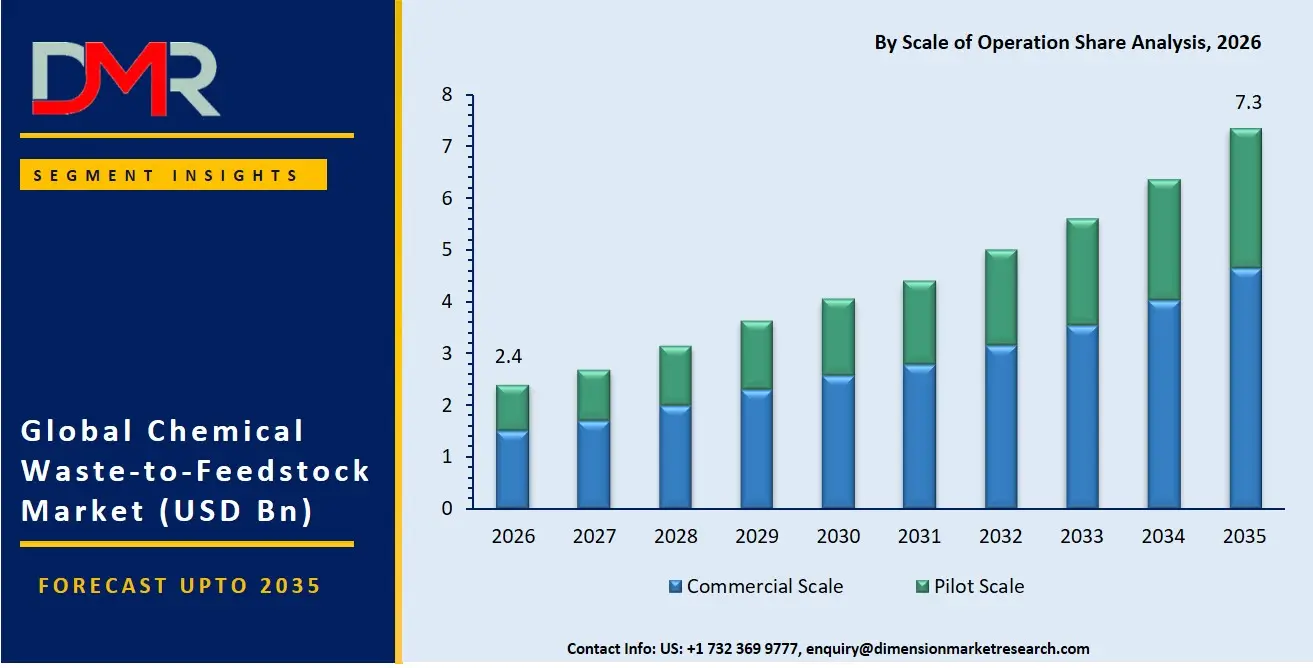

By Scale of Operation Analysis

The Commercial Scale segment is the largest in 2026, accounting for 71.8% share, driven by the need for enterprise-wide digital transformation, multi-plant standardization, and significant capital budgets. Large-scale facilities are adopting digital twin platforms to optimize global production networks and ensure operational excellence. The Pilot Scale segment is the fastest-growing, supported by R&D grants, technology validation requirements, and lower entry costs for emerging recycling technologies.

By End-Use Industry Analysis

The Chemicals & Petrochemicals segment is the largest end-use industry in 2026, accounting for approximately 35.6% share, driven by the need for consistent recycled feedstock quality, yield optimization, and cracker unit performance. This segment reflects the continued shift toward digitalization of large-scale continuous processes. The Packaging segment is the second-largest and fastest-growing, supported by brand owner commitments to recycled content, high-mix low-volume production, and traceability requirements. Energy & Fuels and Automotive represent specialized segments with dedicated waste-to-feedstock requirements for regulatory compliance and quality assurance.

The Global Chemical Waste-to-Feedstock Market Report is segmented based on the following:

By Technology

- Pyrolysis

- Fast Pyrolysis

- Catalytic Pyrolysis

- Gasification

- Plasma Gasification

- Conventional Gasification

- Depolymerization

- PET Depolymerization

- Polyamide Depolymerization

- Solvolysis

- Hydrothermal Processing

- Catalytic Cracking

- Others

By Waste Type

- Plastic Waste

- Municipal Solid Waste (MSW)

- Industrial Chemical Waste

- Biomass Waste

- Agricultural Waste

- Electronic Waste

- Others

By Feedstock Type

- Pyrolysis Oil

- Syngas

- Recycled Monomers

- Recycled Polymers

- Hydrogen

- Methanol & Ethanol

- Others

By Scale of Operation

- Commercial Scale

- Pilot Scale

By End-Use Industry

- Chemicals & Petrochemicals

- Packaging

- Energy & Fuels

- Automotive

- Consumer Goods

- Textiles

- Construction

- Others

Regional Analysis

Largest Region in the Chemical Waste-to-Feedstock Market

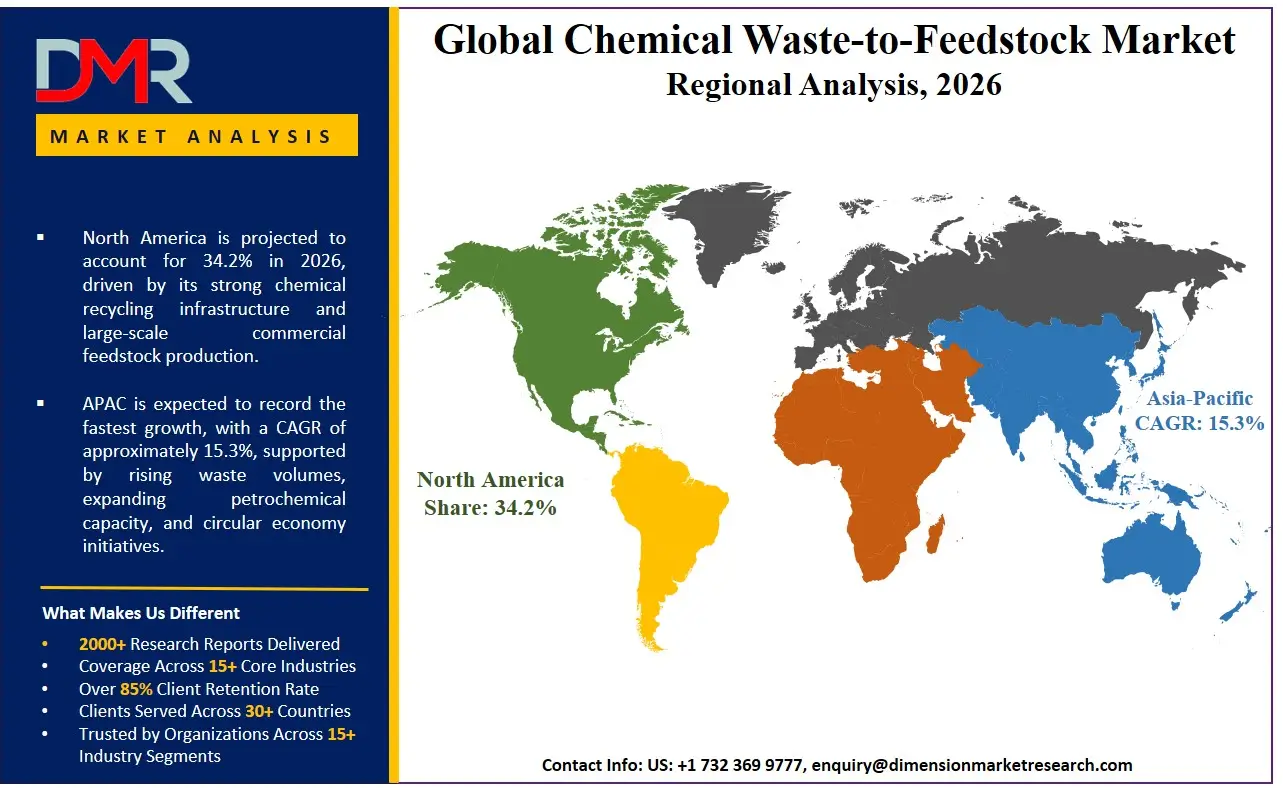

It is projected that North America will take the lead in the global chemical waste-to-feedstock market, covering a market share of about 34.2% in the year 2026. The region's dominance is driven by the presence of major chemical recycling technology vendors, strong regulatory frameworks such as EPA RCRA and state-level chemical recycling mandates, and early adoption of AI-driven simulation and predictive maintenance technologies across plastic and industrial waste sectors. North America benefits from significant investment in chemical recycling plant digitalization, the highest concentration of brownfield modernization projects in the US Gulf Coast, and strong government support through DOE funding for industrial decarbonization. The region is also home to major waste processors and engineering firms, enabling rapid deployment of plant-wide digital twins. Additionally, ongoing investments in workforce training using AR/VR and operator training simulators further strengthen North America's leading position. The widespread adoption of advanced digital twins for plastic waste processing, feedstock optimization, and chemical recycling batch manufacturing continues to reinforce the region's market leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Chemical Waste-to-Feedstock Market

Asia-Pacific is the fastest-growing region, supported by aggressive domestic chemical recycling expansion in China and India, substantial government funding for smart factory and Industry 4.0 initiatives, and increasing investments in greenfield waste-to-feedstock complexes that integrate digital twins from the initial design phase. The region is witnessing rapid growth in modular plant construction, driving demand for cloud-based simulation and process optimization software. Asia-Pacific is also at the forefront of AI-driven process deployment in high-growth sectors like battery recycling and electronic waste. The region benefits from lower labor costs, driving faster ROI on automation, along with rising corporate commitments to operational excellence and safety compliance. Growing focus on plastic traceability for export markets further accelerates market expansion. Moreover, increasing environmental regulations and the need to reduce industrial accidents in rapidly industrializing economies are expected to keep Asia-Pacific's growth momentum as the highest CAGR region during the forecast period.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The chemical waste-to-feedstock market is highly competitive, with new ideas and strategic partnerships shaping the competitive environment. To gain an advantage, companies and providers are focused on developing better digital platforms (such as AI-powered process simulation, automated thermal stability detection systems, and software development kits for process safety management), smart catalytic activity analytics, and cloud-based process degradation monitoring. There are high barriers to entering the market due to the large amount of money needed for regulatory approval, specialized process chemistry knowledge, and the need for mature software systems and rule-following.

Strategic approaches to increase market presence include partnerships with chemical recycling research groups and digital registries, mergers between software providers and waste processors, and long-term support contracts with customers and government institutions. Additionally, research and development in digital feedstock-sharing rules and flexible simulation designs are important for staying competitive and meeting the changing needs of the chemical waste-to-feedstock community.

Some of the prominent players in the Global Chemical Waste-to-Feedstock Market are:

- BASF SE

- Dow Inc.

- Saudi Basic Industries Corporation (SABIC)

- LyondellBasell Industries N.V.

- Shell plc

- TotalEnergies SE

- Exxon Mobil Corporation

- Eastman Chemical Company

- Covestro AG

- Neste Oyj

- Agilyx ASA

- Plastic Energy Limited

- Loop Industries, Inc.

- Brightmark LLC

- Enerkem Inc.

- Carbios SA

- Mura Technology Limited

- PureCycle Technologies, Inc.

- INEOS Group Holdings S.A.

- Versalis S.p.A.

- Other Key Players

Recent Developments

- April 2026: BASF SE partnered with TSR Group to strengthen electric vehicle battery recycling operations across Europe, including black mass processing, battery dismantling, and circular raw material recovery to expand its chemical recycling and circular feedstock network in the region.

- March 2026: Neste Oyj commissioned the world's largest upgrading facility for liquefied waste plastic at its Porvoo refinery in Finland, with annual processing capacity of up to 150,000 tons of liquefied waste plastic to produce high-quality petrochemical feedstock for the plastics and chemicals industry.

- October 2025: PureCycle Technologies, Inc. expanded commercial production capacity at its recycled polypropylene operations and strengthened supply agreements with packaging and consumer goods companies to accelerate adoption of recycled resin feedstocks across North America.

- September 2025: Eastman Chemical Company advanced construction activities at its molecular recycling facility in France aimed at converting difficult-to-recycle polyester waste into virgin-quality chemical feedstocks, supporting large-scale circular materials production in Europe.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2.4 Bn |

| Forecast Value (2035) |

USD 7.3 Bn |

| CAGR (2026–2035) |

13.3% |

| The US Market Size (2026) |

USD 690.3 Mn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Technology, By Waste Type, By Feedstock Type, By Scale of Operation, By End-Use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Chemical Waste-to-Feedstock Market?

▾ The Global Chemical Waste-to-Feedstock Market is estimated to be valued at USD 2.4 billion in 2026 and is expected to reach USD 7.3 billion by the end of 2035.

What is the CAGR of the Global Chemical Waste-to-Feedstock Market from 2026 to 2035?

▾ The market is growing at a CAGR of 13.3% over the forecasted period.

What factors are driving the growth of the Global Chemical Waste-to-Feedstock Market?

▾ The market is driven by advances in real-time process degradation detection and automated safety enforcement, regulatory pressure to speed up chemical recycling compliance results and reduce thermal runaway mistakes, and increased government investment in national safe chemical material infrastructure.

What are the major trends in the Global Chemical Waste-to-Feedstock Market?

▾ The key market trends include the adoption of real-time process thermal stability tracking and halogenated solvent analysis, along with a growing shift toward AI-driven feedstock formulation platforms and data-enabled digital asset inventory management systems.

Which region held the largest share of the Global Chemical Waste-to-Feedstock Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 34.2%.

Which region is expected to grow the fastest in the Global Chemical Waste-to-Feedstock Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Chemical Waste-to-Feedstock Market?

▾ Some of the major key players in the Global Chemical Waste-to-Feedstock Market are BASF SE, Dow Inc., Saudi Basic Industries Corporation (SABIC), LyondellBasell Industries N.V., TotalEnergies SE, Exxon Mobil Corporation, and many others.

How is the Global Chemical Waste-to-Feedstock Market segmented?

▾ The market is segmented by technology, waste type, feedstock type, scale of operation, and end-use industry.