Market Snapshot

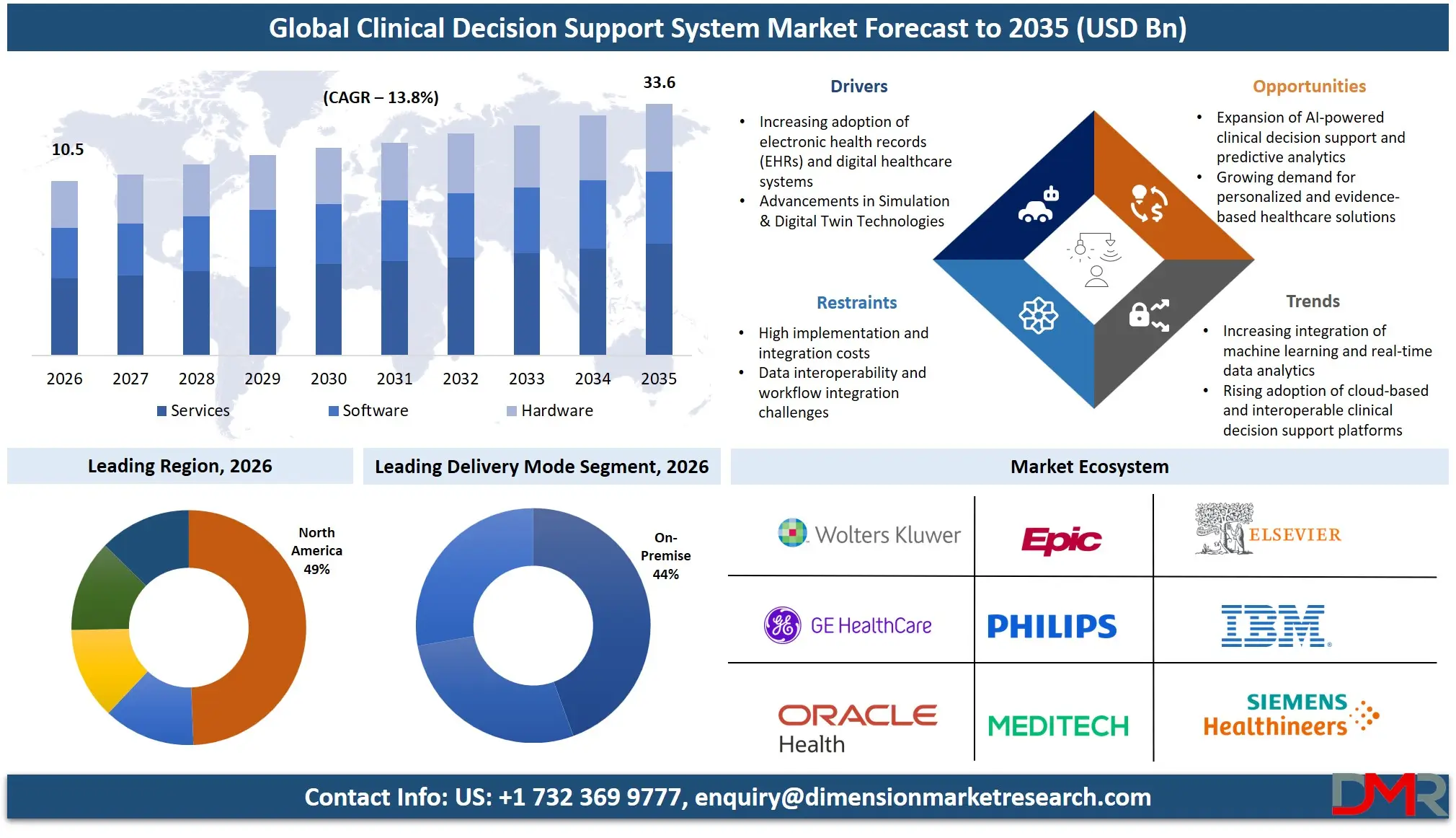

- The global Clinical Decision Support System Market is valued at USD 9.2 Billion in 2025, reached USD 10.5 Billion in 2026, and is projected to hit USD 33.6 Billion by 2035 at a CAGR of 13.8%.

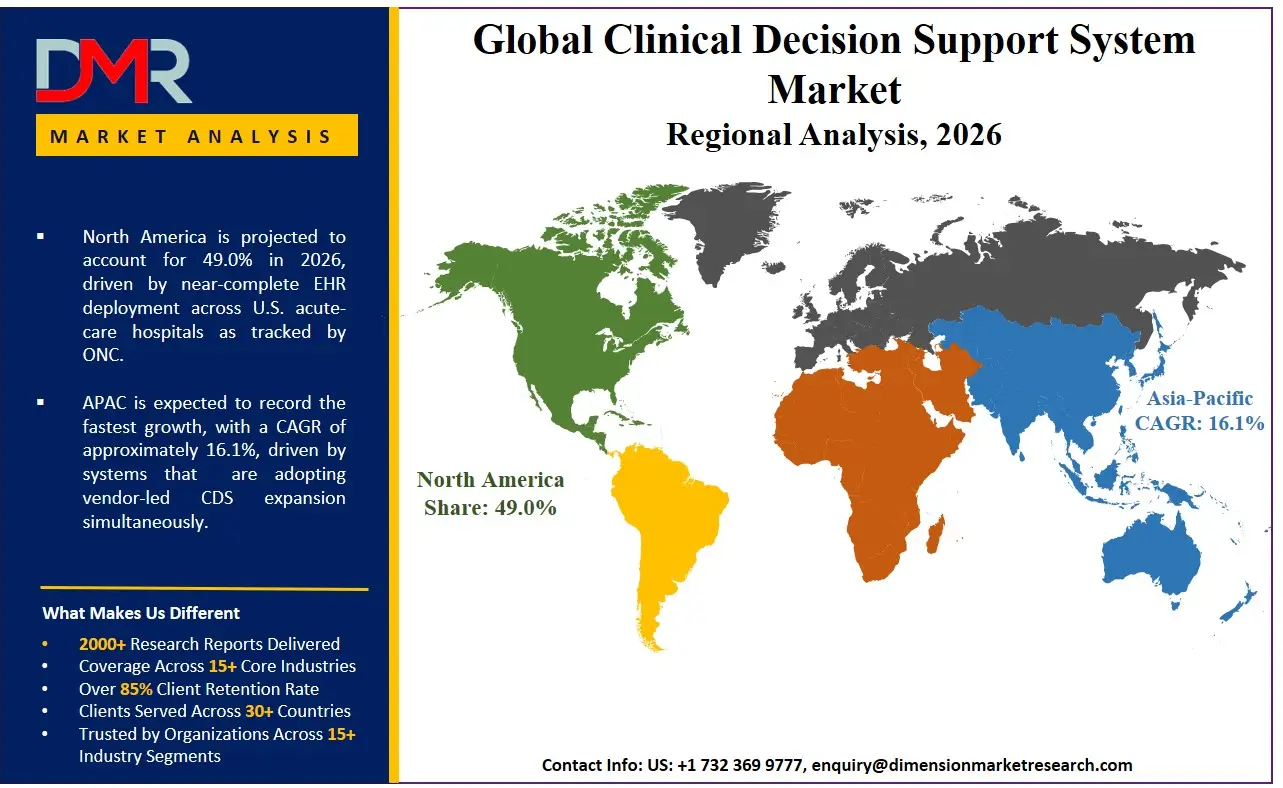

- North America holds the dominant regional position with a 49.0% revenue share in 2026, anchored by the United States at USD 3.6 Billion.

- Standalone CDSS leads the By Product segment with a 32.3% revenue share in 2026.

- Drug Allergy Alerts leads the By Application segment with a 28.5% revenue share in 2026.

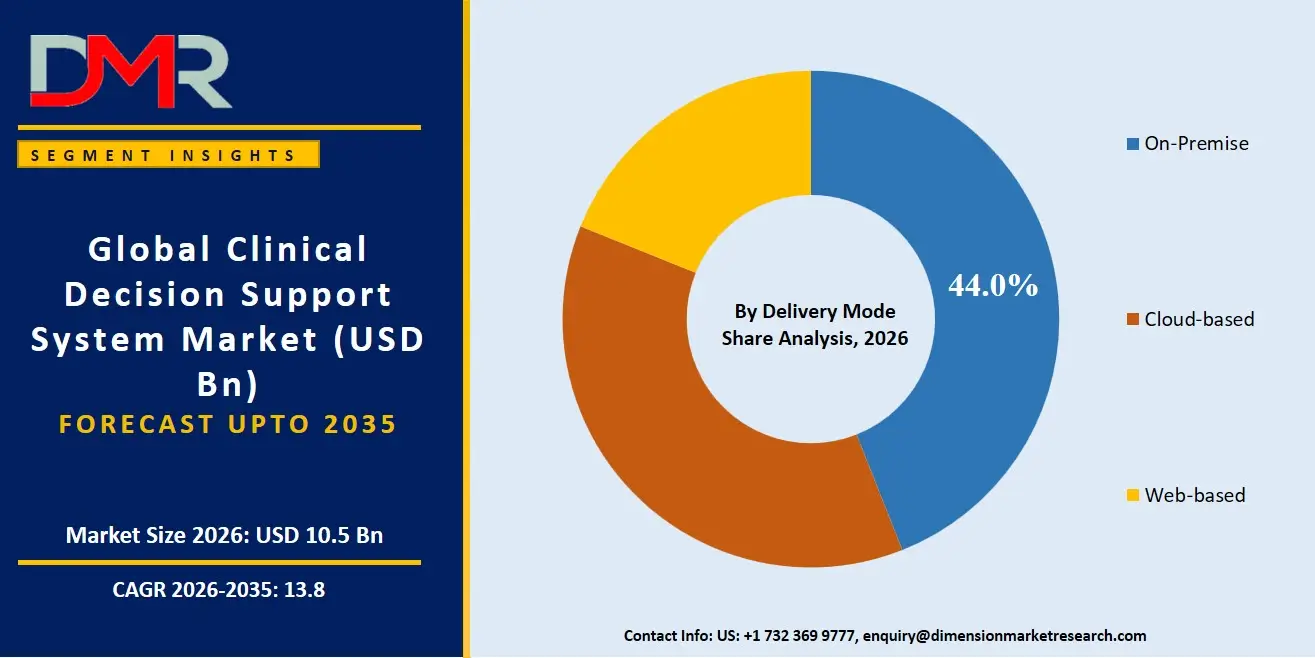

- On-premise Systems lead the By Delivery Mode segment with a 44.0% revenue share in 2026.

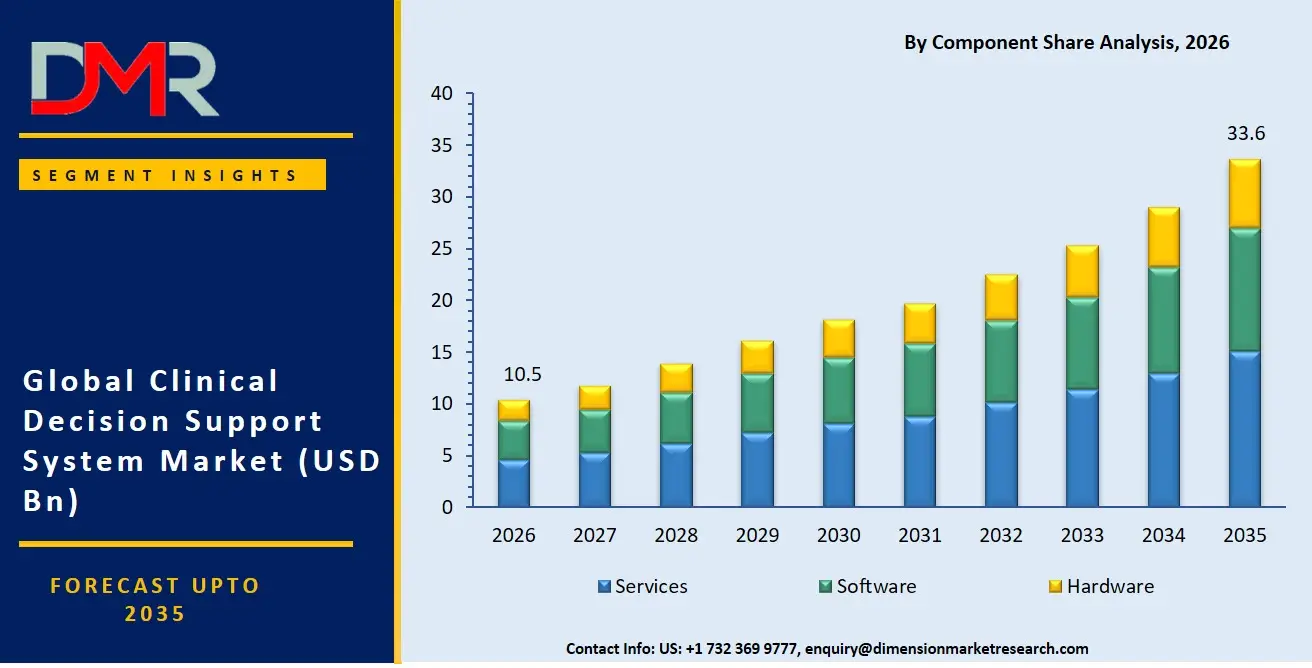

- Services lead the By Component segment with a 44.6% revenue share in 2026.

- The U.S. CDSS market is projected to reach USD 9.8 Billion by 2035 at a CAGR of 11.3%.

- As per the AMA 2026 Physician Survey, 81% of U.S. physicians now use AI in their practice, more than double the 38% recorded in 2023.

Market Overview

The Clinical Decision Support System market encompasses software, hardware, and services that help clinicians make evidence-based decisions at the point of care. CDSS tools include drug allergy alert engines, drug-drug interaction checkers, clinical reminder systems, dosing calculators, guideline-driven care pathways, and predictive analytics platforms. Purely administrative clinical tools that do not support diagnostic or therapeutic decisions sit outside this scope. The boundary drawn here separates workflow automation from active clinical intelligence.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

As tracked by the ONC in 2024, nearly all U.S. acute-care hospitals had deployed certified EHRs by late 2024. A near-complete EHR base makes CDSS deployment technically feasible at scale across the entire U.S. health system. Based on data from the AMA 2026 Physician Survey, 76% of physicians confirmed that AI tools improve their ability to care for patients. Only 18% of physicians currently use AI for assistive diagnosis, compared to 28% using it for administrative documentation. This gap tells vendors that workflow-adjacent CDS tools carry lower sales resistance than full diagnostic decision engines, a commercially meaningful distinction for product roadmap decisions.

The U.S. represents the single largest national market, valued at USD 3.6 billion in 2026. North America, as a region, commands 49.0% of global revenue. This concentration reflects the depth of U.S. hospital digitization and the regulatory activity that directly shapes vendor strategy and procurement cycles worldwide. FDA's revised CDS Software Guidance issued on January 6, 2026, reduced regulatory ambiguity for a category of generative AI tools, unlocking product investment that vendors had held pending classification clarity.

Market Size and Forecast

The Global Clinical Decision Support System Market size is estimated at USD 10.5 Billion in 2026 from USD 9.2 Billion in 2025, and is projected to reach USD 33.6 Billion by 2035, exhibiting a CAGR of 13.8% during the forecast period.

A CAGR of 13.8% reflects a market where two structural forces are compounding simultaneously. Near-complete EHR deployment across U.S. acute-care hospitals creates the data substrate that CDS engines require to function. FDA's January 2026 revised guidance reduced the regulatory ambiguity that had previously placed vendor roadmaps on hold. Both conditions were absent or incomplete in prior forecast periods. Their simultaneous presence materially raises the probability that the base forecast is achievable without extraordinary policy or technology tailwinds.

The U.S. market will reach USD 9.8 Billion by 2035 at a CAGR of 11.3%. The gap between the global CAGR of 13.8% and the U.S. rate of 11.3% confirms that non-U.S. markets will drive a disproportionate share of new market value through 2035. Regions with lower current CDSS penetration carry higher absolute growth potential precisely because their installed base is smallest today.

Under an upside scenario, accelerated FDA clearance of predictive CDS tools following eCART's June 2024 510(k) clearance could establish a template for faster clinical AI commercialization and push adoption above forecast levels. A downside scenario centers on persistent regulatory ambiguity for image-analyzing, IVD-analyzing, and signal-analyzing CDS tools. If FDA classification disputes increase among high-value clinical vertical vendors, both tool immaturity and regulatory uncertainty barriers compound, suppressing adoption below the base case.

Market Dynamics

FDA Regulatory Clarity and Rising Clinician AI Acceptance Accelerate CDSS Procurement

As reported by the AMA 2026 Physician Survey, 81% of U.S. physicians now use AI in practice, more than double the 38% who did so in 2023. Clinician acceptance has crossed a threshold that now directly supports institutional willingness to fund CDSS procurement. Vendors no longer face the adoption resistance that characterized the 2021 to 2023 period. The commercial lever in Clinical Decision Support System has shifted from clinician education to procurement execution.

AgileMD's eCART Clinical Deterioration Suite received FDA 510(k) clearance in June 2024 for inpatient risk prediction covering sepsis, heart failure, and COPD. This clearance establishes a replicable regulatory template that other predictive CDS vendors can follow with reduced uncertainty. Each new cleared-device precedent shortens the effective regulatory runway for subsequent applicants in the same clinical category, compressing time-to-market for the next wave of AI-driven CDS tools.

Regulatory Device Classification and Clinician Behavioral Barriers Slow Vendor Roadmaps

FDA's 2026 guidance reaffirmed that image-analyzing, IVD-analyzing, and signal-analyzing CDS software remains a regulated medical device regardless of meeting all other non-device criteria. Vendors building CDSS for radiology, pathology, and physiologic monitoring face the full device regulatory pathway before commercialization. These are three of the highest-value clinical verticals in CDSS. The compliance overhead in each directly limits product velocity and raises the capital requirement for market entry.

Data published in npj Digital Medicine in 2025, from a survey of 43 U.S. health systems, found 77% cite immature AI tools as the top adoption barrier, 47% cite financial concerns, and 40% cite regulatory uncertainty. Low clinician buy-in and tool immaturity create procurement friction that slows market realization independently. Together they create a compounding barrier. Organizations may accept a single constraint but two simultaneous barriers routinely defer purchasing decisions into the next budget cycle.

FDA Enforcement Discretion, AHRQ Funding, and Cleared Predictive CDS Open New Revenue Channels

FDA's 2026 guidance permits a single clinically appropriate CDS recommendation to qualify as non-device under enforcement discretion, as reported by Covington and Burling in January 2026. This opens a low-oversight regulatory lane suited specifically to generative AI CDS tools. Vendors who design single-recommendation outputs can now reach U.S. hospitals faster and at lower compliance cost than those building multi-output diagnostic engines. The enforcement discretion lane is not a loophole. It is a deliberate policy mechanism that FDA created to accelerate a defined category of clinical AI deployment.

AHRQ's CDSiC program, which marked 20 years of CDS investment in 2024, actively funds shareable, standards-based patient-centered CDS tools that incorporate patient-specific data, as documented in the 2024-2025 CDSiC Annual Report. This sustained public funding creates a procurement-ready buyer segment for vendors building patient-centered CDS products. Organizations already aligned with AHRQ's standards framework enter the procurement process institutionally prepared, which shortens vendor sales cycles and reduces the competitive field to compliant vendors only.

Market Trends

Directive CDS Architecture, EHR-Native Integration, and Algorithm Transparency Are Becoming Baseline Procurement Requirements

FDA's 2026 CDS guidance is shifting product design industry-wide toward single-recommendation directive outputs and away from multi-option alert menus. As reported by the AMA 2026 Physician Survey, 85% of physicians want direct control over AI adoption decisions in their practice. Vendors that redesign their user experience around directive, single-recommendation architectures gain both a regulatory compliance advantage and a usability edge simultaneously. Clinicians respond measurably better to specific recommendations than to lists of possibilities that require additional decision-making at an already cognitively loaded moment.

ML-enhanced CDS platforms deployed native EHR connectors for Epic and Oracle Health between 2024 and 2026. Vendors that secured EHR-native integration contracts during this window now hold structural switching-cost advantages over later entrants who must compete on capability alone. EHR integration depth has become the primary retention mechanism in enterprise CDSS sales cycles, not feature differentiation.

Transparency is becoming a non-negotiable product requirement across every buyer segment. FDA's 2026 guidance mandates disclosure of data inputs, underlying logic, and recommendation generation methods in vendor labeling. Vendors who embed transparency documentation into product development from the design phase rather than retrofitting it post-launch will face lower regulatory friction and faster institutional acceptance. Buyers who lack governance confidence in a CDS tool's algorithm provenance now have the regulatory standing to reject procurement, making transparency a commercial prerequisite rather than a differentiating feature.

Product Analysis

Standalone CDSS leads the segment with a 32.3% share, reflecting a market where deployment flexibility and independence from existing EHR or CPOE infrastructure make this configuration the preferred entry point for smaller facilities and specialty clinics. Organizations that need decision support without a full-platform overhaul choose standalone systems because they reduce implementation risk and compress deployment timelines. No dependency on a third-party EHR vendor's release schedule means faster go-live and lower integration cost.

Integrated CPOE with CDSS embeds clinical alerts directly into physician ordering workflows, intercepting potential drug errors at the moment of prescribing and holding strong adoption in acute-care settings where order volume and medication complexity are highest. Integrated EHR with CDSS leverages patient record data to generate context-aware recommendations at the point of care, facing a penetration opportunity rather than an infrastructure barrier given near-complete U.S. EHR deployment. Integrated CDSS with CPOE and EHR represents the most comprehensive configuration available, connecting prescribing, records, and decision logic into a single clinical intelligence layer, with adoption concentrated in large health systems with mature IT governance structures capable of managing the higher implementation complexity this architecture requires.

Application Analysis

Drug Allergy Alerts accounts for 28.5% of the segment, driven by direct patient safety and institutional liability requirements that make allergy alerting operationally mandatory. Hospitals face direct liability exposure without it. Non-discretionary procurement status sustains this segment's share regardless of broader technology investment cycles or budget constraint periods that affect other CDS application categories.

Drug-Drug Interactions detection is permanently embedded across clinical settings because polypharmacy rates in aging populations make DDI checks a daily necessity rather than an optional safety layer. Clinical Reminders reduce clinician cognitive load while tying preventive care adherence directly to payer reimbursement quality metrics, making them a financially strategic tool for health systems. As reported by AHRQ's CDSiC 2024-2025 Annual Report, Clinical Guidelines are moving from static reference tools toward dynamic AI-enhanced protocol engines through the active development of shareable, standards-based guidelines incorporating patient-specific data. Drug Dosing Support prevents the most common preventable adverse drug events in hospitals and carries high institutional ROI as a standard inclusion in any CDSS procurement package alongside allergy and interaction alerting.

Delivery Mode Analysis

With a 44.0% share, On-premise Systems hold the dominant position due to data security mandates and legacy IT infrastructure investment accumulated over decades. Large hospitals and health systems operating under strict HIPAA compliance and data sovereignty requirements retain on-premise deployments to maintain direct control over sensitive patient data. This share reflects an installed base built over decades of capital investment, not a technology preference for legacy architecture over cloud alternatives.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Cloud-based Systems are gaining procurement traction among mid-size and community health organizations with limited in-house IT infrastructure, as cloud delivery reduces upfront capital expenditure and accelerates compliance update deployment timelines. Web-based Systems serve ambulatory care, telehealth, and multi-site group practices where browser-accessible CDS eliminates device dependency and supports rapid rollout, though latency and offline access limitations constrain their viability in high-acuity inpatient environments where real-time decisioning determines clinical outcomes.

Component Analysis

Services captures 44.6% of segment demand, as CDSS deployment requires clinical workflow mapping, staff training, ongoing system configuration, and post-go-live support that are continuous requirements rather than one-time costs. As reported by Wolters Kluwer's results covering 9M 2025, Clinical Solutions delivered 7% organic growth driven by CDS renewals, confirming that software retention rates are a reliable leading performance indicator for the services revenue stream that follows every deployment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Software constitutes the core intellectual property layer and the highest-margin revenue stream for vendors operating subscription-based cloud-deployed CDS platforms. Hardware forms the smallest component of CDSS revenue, covering point-of-care terminals, server infrastructure, and bedside display units in settings where digital infrastructure is not yet fully embedded. As cloud deployment expands and hospital IT infrastructure matures, hardware dependency in CDS delivery will continue declining as a revenue contributor across the forecast period.

Key Market Segments

By Product

- Standalone CDSS

- Integrated CPOE with CDSS

- Integrated EHR with CDSS

- Integrated CDSS with CPOE and EHR

By Application

- Drug Allergy Alerts

- Drug-Drug Interactions

- Clinical Reminders

- Clinical Guidelines

- Drug Dosing Support

By Delivery Mode

- On-premise Systems

- Cloud-based Systems

- Web-based Systems

By Component

- Services

- Software

- Hardware

Regional Analysis

North America held a dominant position in 2026 with a 49.0% revenue share of the global Clinical Decision Support System Market, anchored by the United States at USD 3.6 Billion. Near-complete EHR deployment across U.S. acute-care hospitals creates the data infrastructure that CDS engines depend on, while active FDA regulatory output continues to define global product standards. No other region currently matches this combination of infrastructure depth, regulatory clarity, and procurement scale. North America's structural lead is not closing over the forecast period. The gap between the U.S. CAGR of 11.3% and the global CAGR of 13.8% confirms that growth is accelerating faster elsewhere, but North America retains the largest absolute revenue base throughout.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia Pacific is the most commercially active expansion target among non-U.S. regions, with enterprise CDS vendor coverage now reaching over 200 hospitals across Australia, New Zealand, Singapore, Taiwan, and Hong Kong following Wolters Kluwer's APAC launch in September 2025. Europe represents the second-largest regional market, with the AI-enhanced UpToDate Enterprise Edition already in early release at 40 of the largest EMEA health systems as of June 2025, signaling that enterprise CDS vendors are investing in European infrastructure expansion in parallel with their North American operations.

Latin America remains an emerging-stage market where EHR penetration lags North America and Europe, representing a future-cycle opportunity that vendors should build channel partnerships in before infrastructure-led adoption accelerates. The Middle East and Africa CDSS market is at an early but structurally active stage, with international vendors forming regional distribution and implementation partnerships as a commercially rational entry strategy for a market with limited infrastructure depth.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The global CDSS market is moderately consolidated at the enterprise tier, with a small number of large health IT platform vendors holding dominant install-base positions across acute-care hospitals. The market is simultaneously fragmented at the application layer, where point-solution vendors compete across specific clinical use cases including sepsis prediction, drug safety, and diagnostic AI. Platform vendors with deep EHR integrations hold the structural advantage. Vendors that control the EHR-CDS integration layer effectively set the default clinical intelligence standard for their entire client base and generate renewal-driven revenue that point-solution competitors cannot structurally replicate.

Wolters Kluwer launched UpToDate Expert AI in September 2025, a generative AI CDS tool extending its portfolio across UpToDate, Lexidrug, Patient Engagement, and Digital Architect product lines, demonstrated in Epic workflows and with Microsoft Dragon Copilot at HLTH 2025. Vendors that have launched evidence-grounded, citation-transparent generative AI CDS tools are differentiating on clinician trust and institutional governance alignment rather than feature parity. The next competitive battleground is not capability but the provenance and transparency of the clinical intelligence layer.

KLAS rankings are emerging as a decisive procurement signal in health system sales cycles. Third-party validation directly influences purchasing decisions at large health systems, creating a competitive disadvantage for vendors without strong KLAS positioning that cannot be overcome by sales effort alone. The cleared-device predictive CDS sub-market is establishing itself as a distinct competitive arena, where regulatory clearance depth functions as the primary barrier to entry and the primary signal of clinical credibility for buyers evaluating inpatient risk prediction tools.

Company Profiles

McKesson Corporation operates as a broad-based health IT and pharmaceutical distribution platform, with CDS embedded within its clinical workflow infrastructure. Distribution scale gives McKesson a procurement channel that pure-play CDS vendors cannot replicate, as its relationships with pharmacies, hospitals, and payers provide pre-existing access to the buyer tier. CDS is not McKesson's core revenue driver, which means product investment depth in CDSS may lag dedicated clinical AI vendors who allocate their full R&D budget to decision support capability development over the forecast period.

Wolters Kluwer N.V. has built the most documented commercial CDS performance record in the market. Clinical Solutions delivered 8% organic growth in 9M 2024 and 7% in 9M 2025, driven by UpToDate CDS renewals, as reported by Wolters Kluwer. FY2024 Health division organic revenue growth reached 6% within total group revenues of €5,916 million. The 2026 Best in KLAS ranking for the second consecutive year confirms that renewal-led growth and clinical trust are compounding into a defensible competitive position that new entrants with superior technology cannot displace quickly without equivalent institutional relationships.

Key Players

- McKesson Corporation

- Oracle (Cerner)

- Koninklijke Philips N.V.

- Wolters Kluwer N.V.

- Siemens Healthineers AG

- Allscripts Healthcare, LLC

- athenahealth, Inc.

- NextGen Healthcare Inc.

- IBM Corporation

- Agfa-Gevaert Group

- Becton, Dickinson and Company

- GE HealthCare

- Nordic

- Cabot Technology Solutions

- BeeKeeperAI

- EBSCO Industries, Inc.

- Epic Systems Corporation

Supply Chain and Value Chain Analysis

The CDSS value chain begins with clinical evidence and patient data as the two foundational raw inputs. Vendors that control proprietary evidence content, including continuously updated drug databases and evidence-based clinical guidelines, hold a structural upstream advantage that pure-algorithm competitors cannot easily replicate. As cited in Lancet Digital Health in 2026, only two inpatient risk-prediction CDS tools, eCART and PeraTrend, had achieved FDA clearance by that date. The scarcity of cleared AI models confirms that model validation is the highest-leverage activity in the CDSS value chain. A cleared AI model carries commercial value that vastly exceeds its development cost, making regulatory clearance the single most defensible asset a CDS vendor can hold.

EHR and CPOE integration functions as the critical distribution bottleneck. A CDSS product without a native connector to Epic or Oracle Health faces adoption barriers at the point of sale that no marketing investment can overcome. UpToDate Expert AI was demonstrated in Epic workflows and with Microsoft Dragon Copilot at HLTH 2025, confirming integration depth as a direct revenue lever rather than a technical prerequisite. Post-deployment services form the final stage and represent the largest component revenue category at 44.6%. Ongoing configuration, regulatory compliance updates, clinician training, and integration support are continuous requirements. Vendors that build strong post-sale service teams create recurring revenue streams and high switching costs simultaneously, making services both a margin source and the primary customer retention mechanism in Clinical Decision Support System.

Regulatory Landscape

The U.S. FDA issued its revised Clinical Decision Support Software Guidance on January 6, 2026, superseding the 2022 version. The update refined the four criteria under Section 520(o)(1)(E) of the FD&C Act that determine whether a CDSS product qualifies as a non-device. Failure on any single criterion automatically classifies the software as a regulated medical device. This binary outcome directly shapes vendor product architecture decisions, making the four-criteria test the most operationally significant compliance checkpoint in the entire CDSS regulatory framework.

The 2026 guidance introduced a meaningful opening for generative AI tools. FDA now permits a single clinically appropriate CDS output to qualify as non-device under enforcement discretion, as reported by Covington and Burling in January 2026. Prenosis's Sepsis ImmunoScore became the first AI/ML CDS for sepsis to receive FDA marketing authorization via the De Novo pathway in April 2024, establishing a replicable regulatory template for AI-driven predictive CDS tools seeking cleared-device status. As reported by Innolitics, 38 manufacturers secured two or more 510(k) AI/ML clearances in 2024, confirming that the cleared supplier pool is selective and that repeat-clearance firms hold structural procurement advantages over first-time filers.

Section 520(o)(1)(E) carve-outs remain firm for high-value clinical verticals. FDA's 2026 guidance reaffirmed that image-analyzing, IVD-analyzing, and signal-analyzing CDS software remains a regulated medical device regardless of meeting all other non-device criteria. Vendors building CDSS for radiology, pathology, and physiologic monitoring face the full device regulatory pathway before commercialization. Real-time, emergent, or highly automated CDS tools carry the heaviest regulatory overhead, meaning the products most needed clinically in fast-moving care environments face the highest compliance barrier under the current framework.

AHRQ's regulatory and funding posture shapes the CDSS landscape as a parallel channel to the FDA device pathway. As reported by AHRQ's CDSiC 2024-2025 Annual Report, the agency actively funds shareable, standards-based patient-centered CDS tools incorporating patient-specific data, sustaining a publicly funded procurement pipeline for compliant vendors. This sustained public investment creates a buyer segment that enters procurement institutionally prepared, distinct from the FDA device pathway but equally significant in shaping clinical adoption norms across U.S. health systems.

Investment and White Space Analysis

Active investment is flowing into FDA-cleared predictive CDS as a distinct commercial category with validated clinical volume. Cytovale's IntelliSep, an FDA-cleared sepsis CDS tool, evaluated over 15,000 patients in 2024 alone, confirming that cleared predictive CDS can achieve material clinical scale within its first full year of deployment. This adoption figure validates the investment case for cleared-device CDS as a high-conviction thesis rather than an early-stage research bet. Vendors pursuing 510(k) clearance or De Novo authorization for predictive CDS tools now enter a market where commercial precedents exist and buyer procurement criteria are established.

Generative AI CDS operating within FDA's new enforcement discretion lane represents the second primary investment destination. The single-recommendation output pathway creates a commercially viable, low-oversight route to U.S. hospitals for vendors building evidence-grounded AI tools. Early movers who deploy FDA-aligned generative AI CDS in 2026 will establish renewal-based revenue positions before the competitive set matures. Patient-centered CDS is an underserved segment with structured public funding support through AHRQ's CDSiC program. Vendors aligned with AHRQ's standards reach an institutionally prepared buyer segment that pure-platform vendors have not addressed at scale, creating a defined white space with a procurement-ready customer base already in place.

Non-U.S. markets represent the largest structural growth gap relative to North America's 49.0% revenue concentration. Asia Pacific, where enterprise CDS coverage now extends across more than 200 hospitals, represents the highest-return geographic white space for vendors with scalable international delivery models. The clinical documentation and ambient AI segment is the fastest-emerging investment adjacency. Findings from a 2025 survey of 43 U.S. health systems show 53% reported high success with AI for clinical documentation, the highest success rate of any clinical AI use case surveyed. Vendors that position ambient documentation tools as a gateway product into structured CDSS access a high-success, low-resistance adoption pathway and can expand into higher-complexity CDS applications within the same customer relationship.

Recent Developments

- May 2026: Wolters Kluwer formed a partnership with Guardia Systems and Lebanese Hospital Geitaoui-UMC to advance Medi-Span medication decision support across the Levant region, marking a regional distribution entry strategy for the Middle East market.

- November 5, 2025: Wolters Kluwer reported Clinical Solutions delivered 7% organic revenue growth in 9M 2025, driven by UpToDate CDS renewals, with full-year FY2025 Health division revenues growing 5% organically.

- September 23, 2025: Wolters Kluwer Health demonstrated UpToDate Expert AI in Epic workflows and with Microsoft Dragon Copilot at HLTH 2025, confirming native EHR integration as the primary commercialization channel for generative AI CDS tools.

- February 26, 2025: Wolters Kluwer reported FY2024 Health division organic revenue growth of 6% within total group revenues of €5,916 million, with Clinical Solutions delivering 8% organic growth in 9M 2024 led by UpToDate CDS renewals.

- January 9, 2025: Cytovale reported its FDA-cleared IntelliSep sepsis-risk CDS solution evaluated over 15,000 patients in 2024, confirming commercial-scale adoption of a cleared predictive CDS product within its first full year of deployment.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 9.2 Billion |

| Market Value (2026) |

USD 10.5 Billion |

| Forecast Revenue (2035) |

USD 33.6 Billion |

| CAGR (2026 to 2035) |

13.8% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Product (Standalone CDSS, Integrated CPOE with CDSS, Integrated EHR with CDSS, Integrated CDSS with CPOE and EHR), By Application (Drug Allergy Alerts, Drug-Drug Interactions, Clinical Reminders, Clinical Guidelines, Drug Dosing Support), By Delivery Mode (On-premise Systems, Cloud-based Systems, Web-based Systems), By Component (Services, Software, Hardware) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

McKesson Corporation, Oracle (Cerner), Koninklijke Philips N.V., Wolters Kluwer N.V., Siemens Healthineers AG, Allscripts Healthcare LLC, athenahealth Inc., NextGen Healthcare Inc., IBM Corporation, Agfa-Gevaert Group, Becton Dickinson and Company, GE HealthCare, Nordic, Cabot Technology Solutions, BeeKeeperAI, EBSCO Industries Inc., Epic Systems Corporation |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the biggest investment opportunity in Clinical Decision Support System?

▾ The market expands from USD 9.2 Billion in 2025 to USD 33.6 Billion by 2035. The clearest white space lies in FDA-cleared predictive CDS tools, generative AI CDS operating under FDA's enforcement discretion lane, and patient-centered CDS aligned with AHRQ standards. All three address regulation-created gaps that current market offerings do not fully cover at commercial scale.

Who are the top companies in Clinical Decision Support System?

▾ Key players include McKesson Corporation, Oracle (Cerner), Wolters Kluwer N.V., Koninklijke Philips N.V., Siemens Healthineers AG, Epic Systems Corporation, GE HealthCare, IBM Corporation, and others. Wolters Kluwer's UpToDate was ranked #1 by KLAS for the second consecutive year in the 2026 Best in KLAS report, reflecting the commercial value of renewal-led CDS relationships with large health systems.

Which segment is growing fastest in Clinical Decision Support System Market and why?

▾ Cloud-based Systems within the By Delivery Mode segment are positioned for the fastest adoption trajectory, as mid-size and community health organizations replace on-premise deployments to reduce capital expenditure and accelerate regulatory compliance update cycles. AI-driven predictive CDS within the By Application segment is the fastest-emerging clinical category, with FDA-cleared inpatient risk prediction tools now demonstrating commercial-scale deployment in their first full year of market availability.

Which region is growing fastest in Clinical Decision Support System Market and why?

▾ Asia Pacific is the fastest-expanding regional block, driven by enterprise CDS vendor coverage now reaching over 200 hospitals across Australia, New Zealand, Singapore, Taiwan, and Hong Kong. The gap between the global CAGR of 13.8% and the U.S. CAGR of 11.3% confirms that non-U.S. markets including Asia Pacific are absorbing a disproportionate share of new market value through 2035.

What is the biggest challenge holding Clinical Decision Support System back?

▾ Regulatory device classification for image-analyzing, IVD-analyzing, and signal-analyzing CDS tools is the most structurally limiting constraint, requiring full 510(k) or De Novo compliance in three of the highest-value clinical verticals regardless of other non-device criteria. Findings from a 2025 survey of 43 U.S. health systems show 77% cite immature AI tools as the top adoption barrier, confirming that regulatory burden and tool immaturity compound each other to suppress procurement velocity across the market.