What is the CO₂ Mineralisation Chemical Market Size?

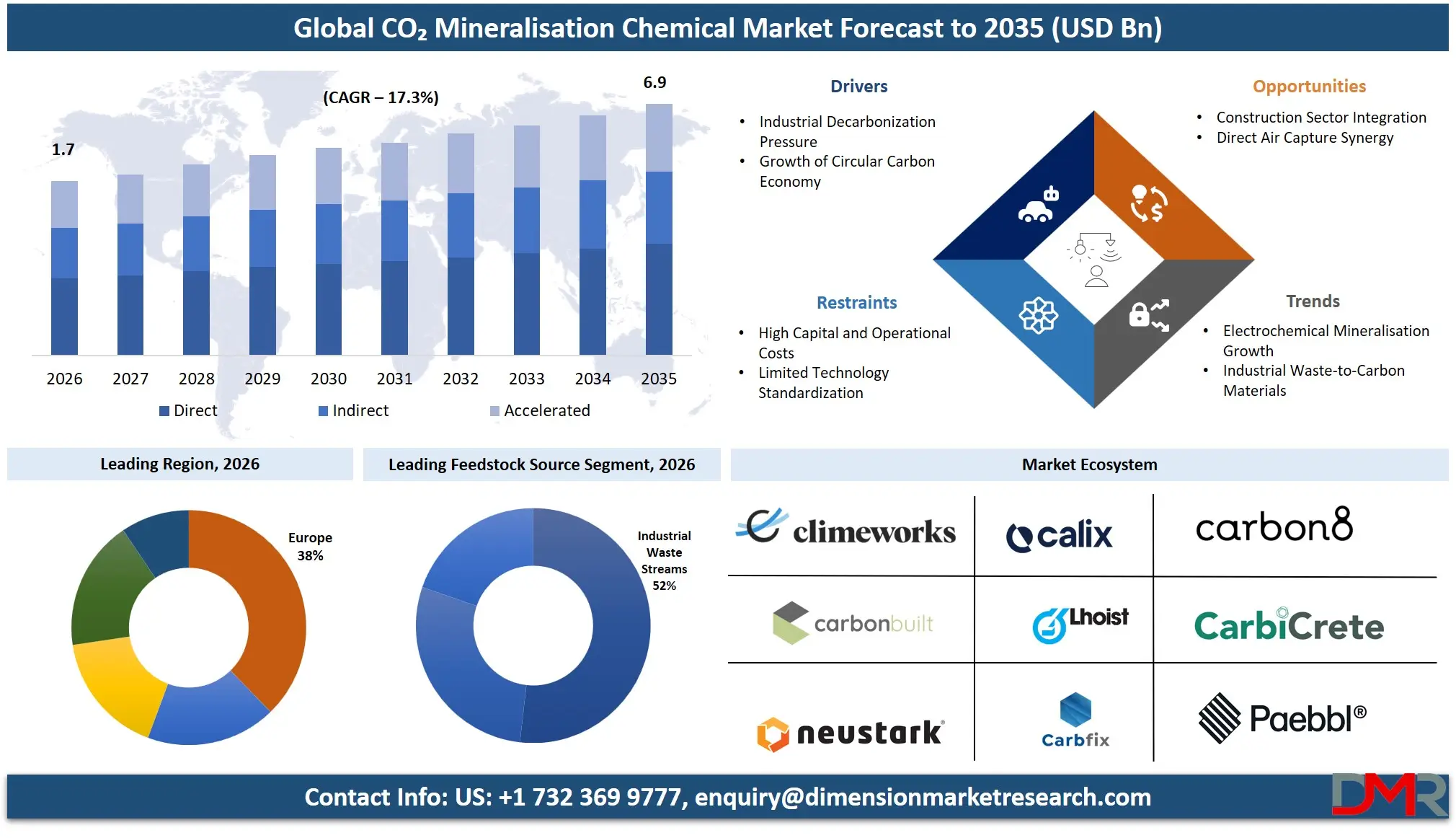

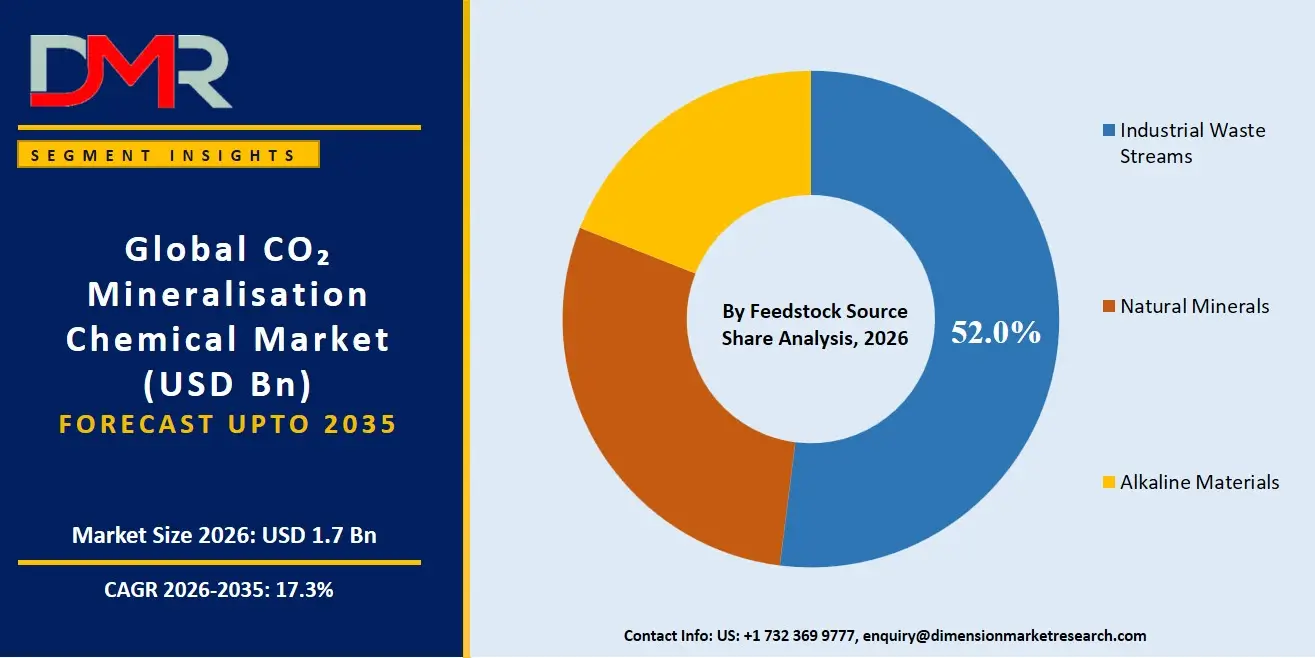

The CO₂ Mineralisation Chemical Market size is expected to be USD 1.7 billion in 2026 and increase at a compound annual growth rate of 17.3% to USD 6.9 billion in 2035 due to growing global demand for industrial sectors such as cement, steel, and chemicals.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The CO2 Mineralisation Chemical Market can be defined as an industry that encompasses all processes, products, equipment, etc., involved in chemically reacting captured CO2 with bases like calcium, magnesium salts, etc., in order to convert CO2 into stable carbonate minerals. This is considered a critical part of CCUS technology due to its ability to mineralize CO2 and permanently store it in solid mineral form thereby preventing emissions into the atmosphere. Increasing commitments to reduce carbon footprint and growing regulatory pressures have led to higher demand. Electrochemical mineralisation, waste-based CO2 utilization, and integration into the cement/construction sector are recent trends.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

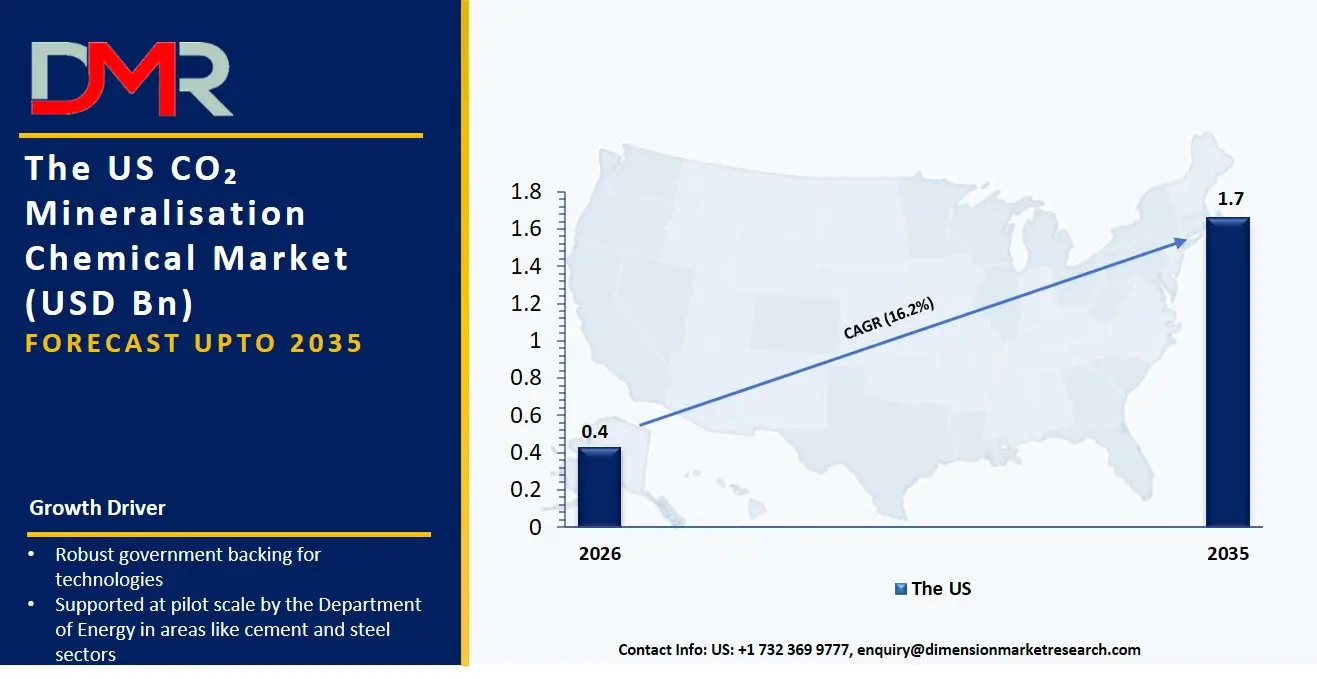

The US CO₂ Mineralisation Chemical Market

The US CO₂ Mineralisation Chemical Market size is estimated to be USD 400 million in 2026 and is expected to increase at a CAGR of 16.2% over the forecast period.

In the United States, there is robust government backing for technologies like the Inflation Reduction Act (IRA), which provides incentives for carbon capture and utilization initiatives via tax breaks. Mineralisation technologies are being supported at pilot scale by the Department of Energy in areas like cement and steel sectors. Some of the notable centers for innovations in mineralisation are California and Texas because of the higher emissions of industries in those areas. There are private players who are investing in the development of large-scale mineralisation techniques that work with DAC systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe CO₂ Mineralisation Chemical Market

The Europe CO₂ Mineralisation Chemical Market size is estimated to be USD 646 million in 2026 and is expected to increase at a CAGR of 16.0% over the forecast period.

The most prominent region in this context is Europe, with climate-friendly policies implemented through the European Green Deal and the net-zero emissions by 2050 goal. Investments in carbon utilisation technology are significant among countries such as Germany, Netherlands, and Norway. EU Emissions Trading System (ETS) adds cost pressure on industrial polluters, promoting the use of mineralisation solutions. Research funding in Horizon Europe promotes developments in CO₂ conversion into useful materials. The main application sectors of this technology are cement production and construction. The rise of carbon-negative construction materials is expected to be rapid.

Japan CO₂ Mineralisation Chemical Market

The market size of Japan CO₂ Mineralisation Chemical will be USD 85 million in 2026 and at a CAGR of 18.1% in the forecast period.

Japan is promoting mineralisation of CO2 with assistance from government schemes facilitated by METI. Japan's efforts concentrate on decarbonization of its industries, especially steel, cement, and chemicals. Due to low opportunities for geological storage, mineralisation has become extremely attractive. Japanese companies have been developing small-scale and energy-efficient solutions that can be deployed in urban industrial complexes. Increasing integration with hydrogen production and circular economy strategies is another important feature of Japan's mineralisation activities. However, mineralisation faces such obstacles as high operating expenses and insufficient minerals domestically.

Key Takeaways

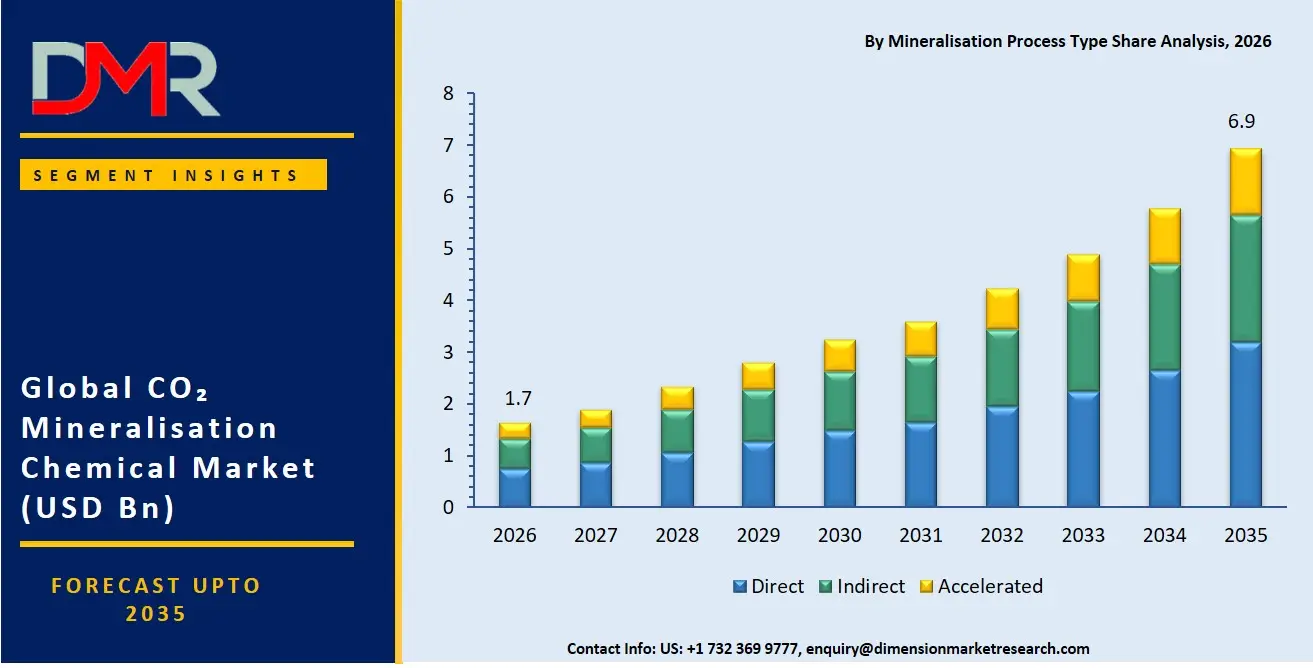

- Market Size & Forecast: The CO₂ Mineralisation Chemical Market size is projected to reach USD 1.7 billion in 2026 and is anticipated to have a value of USD 6.9 billion in 2035.

- Growth Rate & Outlook: The CO₂ Mineralisation Chemical Market size is set to grow at a compound annual growth rate of 17.3% during the forecast period of 2026 to 2035.

- Primary Growth Drivers: Some of the major growth drivers in the market include Demand for CO2 Mineralisation Chemicals, and more.

- Key Market Trends: Some of the major trends in the market are Electrochemical Mineralisation Growth, and more.

- By Mineralisation Process Type: The direct segment is anticipated to get the majority share of the CO₂ Mineralisation Chemical market in 2026.

- By Feedstock Source: Industrial Waste Streams is expected to get the largest revenue share in 2026 in the CO₂ Mineralisation Chemical market.

- By Product Type: The carbonate material segment is expected to get the largest revenue share in 2026 in the CO₂ Mineralisation Chemical market.

- Regional Leadership: Europe is set to lead the CO₂ Mineralisation Chemical market with an estimated 38.0% share in 2026.

What is the CO₂ Mineralisation Chemical?

CO₂ Mineralisation Chemical pertains to chemicals and chemical processes that enable the transformation of CO₂ gas into chemically stable carbonate salts by reactions with metal oxides/hydroxides or alkaline industrial effluents. Through this process, CO₂ is stored in a permanent solid state, making it non-emittable back into the environment. This technique is commonly employed in carbon capture and utilization systems, improving the quality of building materials, and treating industrial waste. The method is becoming increasingly significant because of its sustainability, safety, and efficiency relative to geological storage methods. Some of the notable changes being experienced include low-energy catalysis, industrial symbiosis, and circular economy models.

Use Cases

- Decarbonization of Cement and Concrete: The application of CO2 mineralization chemicals includes the injection of captured CO2 into cement and concrete mixes. This leads to the creation of stable calcium carbonates. It improves the quality of material and reduces the carbon emission intensity of the material. This leads to the creation of carbon-neutral or low-carbon building materials.

- Valorization of Industrial Waste: The steel slag, fly ash, and mine tailings are processed using CO2 mineralization chemicals, leading to the creation of stable carbonates. It helps reduce the stockpile of industrial waste and creates useful construction materials.

- Carbon Dioxide Mineralization during Direct Air Capture: Carbon dioxide present in the air is captured through the application of mineralization chemicals that include catalysts and alkaline chemicals. It leads to the creation of technology that provides permanent carbon storage. It is gaining popularity for its use in DAC plants.

- Production of Carbonate Chemicals: The process of chemical conversion uses CO2 mineralization chemicals to convert carbon dioxide to carbonate compounds like calcium and magnesium carbonates. These carbonates are used for plastic, paper, paint, and filling industries.

How AI Is Transforming the CO₂ Mineralisation Chemical Market

The use of AI technology makes the optimization of process efficiency in CO₂ mineralization possible because it facilitates the monitoring of efficiency of reactions and the rate of materials conversion in real time. Through machine learning algorithms, the choice of optimal combinations of feedstocks can be achieved, leading to increased output and lower energy expenditure.

In addition, AI facilitates material discovery by allowing for simulations of catalysts and pathways for quicker conversion of CO₂. It also contributes to more efficient industrial integration of the processes through improved logistics.

Market Dynamic

Driving Factors in the CO₂ Mineralisation Chemical Market

Demand for CO2 Mineralisation Chemicals

The growing global demand for industrial sectors such as cement, steel, and chemicals is one of the key factors behind the rising popularity of CO₂ mineralisation chemicals. It is difficult for heavy industries to minimize their carbon emissions using renewable energy sources. Carbon mineralisation can offer a sustainable method of storing CO₂ according to the net-zero mission. ESG principles, carbon pricing frameworks, and compliance necessitate companies to adopt carbon-negative technologies. In addition, industries generate extra revenue through carbonate production.

Restraints in the CO₂ Mineralisation Chemical Market

Expensive Capital and Operating Costs

Another constraint that hinders the application of CO2 mineralization technologies is the costly capital cost involved in chemical systems involving CO2 mineralization. The expensive operating cost involved in such technologies is another hindrance since it involves energy-consuming activities, which consume a lot of materials. This technology cannot be used by small and medium-sized companies. The non-standardized facilities also pose challenges in scaling up the technology.

Opportunities in the CO₂ Mineralisation Chemical Market

Integration into Construction Industry

There is much potential for minerals derived from CO₂ in the construction industry, which includes the manufacturing of carbon-negative cements and building materials. Urbanization and infrastructure development in developing countries have resulted in the creation of an increased demand for environmentally sustainable building materials. Moreover, many governments are requiring green construction codes to be followed in their cities. There are thus many benefits to combining mineralisation with cement production.

Trends in the CO₂ Mineralisation Chemical Market

Electrochemical Mineralisation Growth

Electrochemical CO₂ mineralisation has become an important technological trend where the process of converting CO₂ into carbonate minerals through electrochemical reactions powered by electricity is done. The technology fits well with renewable energy usage and the decarbonization of power grids. Academia and start-ups are investing their efforts in enhancing catalyst effectiveness and the speed of reactions.

Research Scope and Analysis

CO₂ Mineralisation Chemicals Market Analysis provides an assessment of leading process technologies, raw material suppliers, types of products, sources of CO₂, and industries driving market growth. It covers various aspects such as regional dynamics, industry implementation, technology developments, sustainability measures, and regulations that can impact future market requirements.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Mineralisation Process Type Analysis

Direct mineralization accounts for the largest market share, projected at 46%, owing to the ease with which it can be employed and its effectiveness and consistency in capturing carbon dioxide emissions from industries like cement kilns and steel furnaces. In-situ and aqueous carbonation systems are extensively used in the building industry, providing advantages in terms of durability as well as carbon dioxide sequestration. Indirect mineralization has emerged as a popular approach for its superior performance in dealing with heterogeneous materials, particularly industrial waste materials that need to undergo multiple processing steps. Accelerated mineralization technologies, encompassing electrochemical and catalytic methods, constitute the fastest-growing area of mineralization because of their energy efficiency and quick carbon dioxide conversion capabilities. Pilot projects involving pressure carbonation and advanced catalysts have demonstrated enormous growth potential in this regard.

By Feedstock Source Analysis

The industrial waste stream will dominate the market share with around 52% in 2026 owing to the ready availability of steel slag, fly ash, cement kiln dust, and mine waste. These sources of raw material serve two purposes - first, they represent inexpensive options for manufacturers and second, these minerals help companies achieve their circular economy goals by tackling the problem of waste disposal. Naturally occurring minerals, such as olivine, serpentine, and basalt, have been widely adopted for large-scale storage because of their excellent carbon binding capability; however, the cost of extracting and transporting these minerals renders them economically impractical. The most promising category is that of alkaline minerals, which includes magnesite-based materials owing to their fast reaction kinetics and higher reactivity.

By Product Type Analysis

Products made from carbonates have gained prominence with an estimated market share of 49% in 2026, mainly because of the growing demand for calcium carbonate and PCC. Carbonate-based construction materials, such as carbonated aggregates and carbon-negative cement, have risen in popularity since more constructions now meet the requirements of green buildings according to government regulations. The specialty mineral product segment is expected to record the highest growth rate due to the new uses of nanocarbonates and carbonate chemicals for industries in paints and composites. Including mineralization in conventional production systems ensures economic benefits, low emission levels, and creation of carbon-negative products, making it economically viable for consumers.

By CO2 Source Analysis

Industrial emissions will continue to lead, contributing around 58% by 2026, through cement, steel, and chemical manufacturing plants because the emission is large enough to allow easy mineralization immediately. Energy and process industries, such as hydrogen and ammonia industries as well as power generation facilities, will also grow gradually as providers of CO₂ emission. Captured carbon source will be the most rapidly growing component because of increased demand in negative emission efforts, carbon credits, and climate-oriented investments. Adoption of mineralization systems with DAC enables industries to comply with their carbon reduction objectives and obtain stable carbonate products. The growing use of CO₂ capture technology and innovative mineralization systems can make CO₂ input source diverse in the coming years.

By End Use Industry Analysis

Construction & Infrastructure dominates as the largest end-user segment and accounts for about 44% market share in 2026. Growth in this end-user segment stems from growing need for carbon-negative cements, concretes, and carbonated aggregates. Chemical industry is second, using mineralisation to produce industrial carbonates, and specialty chemicals. Mining and metal industries have been showing increasing interest in mineralisation technology to manage tailings and wastes, and turning environmental hazards to valuable materials that can be used again. Industries like paper, plastics, and agricultural are other emerging markets. Fastest growth in any segment comes from construction industry owing to rapid urbanization and development of infrastructures in addition to green building regulations.

The CO₂ Mineralisation Chemical Market Report is segmented on the basis of the following:

By Mineralisation Process Type

- Direct Mineralisation

- In-situ mineral carbonation

- Ex-situ mineral carbonation

- Gas-solid carbonation

- Aqueous carbonation

- Indirect Mineralisation

- Multi-step carbonation

- Acid extraction-based process

- Alkali extraction-based process

- pH swing carbonation

- Accelerated Mineralisation

- Pressure-enhanced carbonation

- Catalyst-assisted carbonation

- Electrochemical mineralisation

By Feedstock Source

- Natural Minerals

- Olivine

- Serpentine

- Basalt

- Wollastonite

- Industrial Waste Streams

- Steel slag

- Fly ash

- Cement kiln dust

- Mining tailings

- Red mud

- Alkaline Materials

- Calcium-based feedstocks

- Magnesium-based feedstocks

- Industrial brines

By Product Type

- Carbonate Materials

- Calcium carbonate

- Magnesium carbonate

- Precipitated calcium carbonate (PCC)

- Construction Products

- Carbonated aggregates

- Carbon-negative cementitious materials

- Concrete additives

- Specialty Mineral Products

- Mineral fillers

- Nano-carbonates

- Industrial carbonate chemicals

By CO₂ Source

- Industrial Emissions

- Cement plants

- Steel plants

- Chemical facilities

- Refineries

- Energy & Process Industries

- Power generation facilities

- Hydrogen production

- Ammonia production

- Captured Carbon Sources

- Direct Air Capture (DAC)

- Bio-based CO₂

By End-use Industry

- Construction & Infrastructure

- Cement & concrete

- Green building materials

- Carbon-negative construction products

- Chemical Industry

- Specialty chemicals

- Industrial fillers

- Carbonate compounds

- Mining & Metals

- Tailings management

- Waste mineralisation

- Other Industries

- Paper & pulp

- Plastics & polymers

- Agriculture

Regional Analysis

Leading Region in the CO₂ Mineralisation Chemical Market

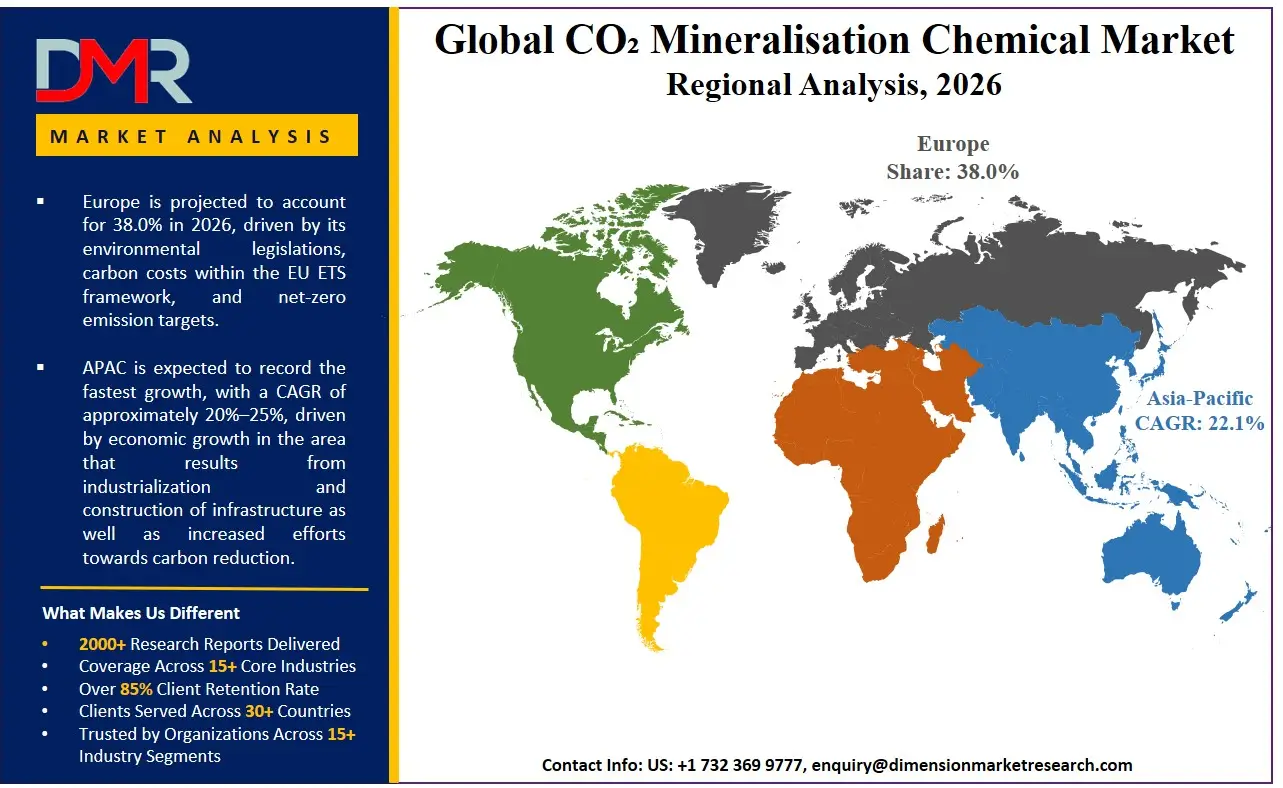

Europe is expected to hold a dominant position with a market share of 38% in 2026 owing to environmental legislations, carbon costs within the EU ETS framework, and net-zero emission targets. Policies associated with the European Green Deal encourage mineralisation of carbon dioxide through technology development, thus fostering investments in clean technology. Research infrastructure, innovation initiatives from Horizon Europe programs, and collaboration with industrial partners are some of the factors that offer a conducive environment for the development of the technology. Adoption of the technology will be limited to industries related to construction, particularly Germany, the Netherlands, and Nordic nations. High compliance costs with regulations will drive the growth of the industry.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the CO₂ Mineralisation Chemical Market

Asia Pacific Region is considered the fastest-growing area because of the economic growth in the area that results from industrialization and construction of infrastructure as well as increased efforts towards carbon reduction. Countries such as China, Japan, South Korea, and India are spending much on the research on carbon capture and mineralization. This area has been selected as one that produces high amounts of cement, steel, and chemicals, hence making it suitable for CO2 mineralization initiatives. Clean energy projects from government initiatives within this area will increase its adoption rate.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

Innovation drives competition in the CO₂ mineralization chemicals industry, which is characterized by the efficiency of technology used, cost-effectiveness, and scalability of operations. Organizations are taking advantage of their relationships with the cement, steel, and chemical industries to embed carbon utilization technology into the manufacturing process itself. Research and development spending is directed at catalyst technology, reactor engineering, and electrochemical mineralization to minimize energy costs and optimize conversion efficiency. The high level of capital intensity and complex nature of technology involved make entry barriers quite high. As a result, competition is restricted to organizations that have substantial financial resources at their disposal.

Some of the prominent players in the global CO₂ Mineralisation Chemical are:

- CarbonCure Technologies

- Carbfix

- Blue Planet Systems Corporation

- Mineral Carbonation International (MCi)

- Solidia Technologies

- Carbon Upcycling Technologies

- neustark

- CarbiCrete

- CarbonBuilt

- Heidelberg Materials

- Calix Limited

- Carbon Free

- Paebbl

- Carbon8 Systems

- Climeworks

- Heirloom Carbon Technologies

- Lhoist Group

- Green Minerals AS

- Deep Sky

- Fortera

- Other Key Players

Recent Developments

- In May 2026, Caravel Bio, a US-based biotech startup, claims to have made substantial progress regarding enzyme stability for carbon capture applications, which could help reduce the overall cost of the technology. The biotech firm has managed to improve enzyme stability by 12 times in just six months through its protein engineering platform. Caravel Bio is also working with Shell GameChanger, which is helping it assess the commercial viability of the technology amid the high operational costs related to scaling up the process of carbon capture.

- In December 2025, The Holcim company has collaborated with 44.01 in implementing an innovative pilot project in the Fujairah region, which will involve both direct capture of CO₂ emissions at cement plants and the subsequent mineralization process, thus becoming a pioneering venture for the entire cement industry globally. The project is targeted at capturing about 5 tons of CO₂ on a daily basis and injecting it into subsurface rocks for long-term storage purposes. As part of the UAE's Net Zero 2050 strategy, the project will be implemented with the assistance of the Fujairah Natural Resources Corporation along with NT Energies.

- In July 2025, The partnership between Resonac Corporation and Tohoku University in exploring sustainable raw material sources for silicon carbide (SiC) power semiconductors has made significant progress. From 2024 onwards, Resonac Corporation and Tohoku University have engaged in research related to the use of silicon sludge obtained from wafer production along with CO2 as feedstocks for growing SiC single crystals. After successfully completing the basic research stage, both entities have now moved forward with their full-scale research toward practical implementation.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.7 Bn |

| Forecast Value (2035) |

USD 6.9 Bn |

| CAGR (2026–2035) |

17.3% |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Mineralisation Process Type, By Feedstock Source, By Product Type, By CO₂ Source, By End-use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the CO2 Mineralisation Chemical Market?

▾ The CO2 Mineralisation Chemical Market size is expected to reach USD 1.7 billion by 2026 and is projected to reach USD 6.9 billion by the end of 2035.

What is the CAGR of the CO2 Mineralisation Chemical Market from 2026 to 2035?

▾ The market is growing at a CAGR of 17.3 percent over the forecasted period.

What factors are driving the growth of the CO2 Mineralisation Chemical Market?

▾ Demand for CO2 Mineralisation Chemicals, and more are the factors driving the growth of the CO2 Mineralisation Chemical Market.

What are the major trends in the CO2 Mineralisation Chemical Market?

▾ Electrochemical Mineralisation Growth, and more are some of the major trends in the market.

Who are the key players in the CO2 Mineralisation Chemical Market?

▾ Some of the key players in the CO2 Mineralisation Chemical Market include Carbfix, Paebell, Carbon Free, and more.

How is the CO2 Mineralisation Chemical Market segmented?

▾ The CO2 Mineralisation Chemical Market is segmented by mineralisation process type, feedstock source, product type, co2 source, end-use industry.

Which region held the largest share of the CO2 Mineralisation Chemical Market in 2026?

▾ Europe is set to lead the CO2 Mineralisation Chemical market with an estimated 38.0% share in 2026.

Which region is expected to grow the fastest in the CO2 Mineralisation Chemical Market?

▾ Asia Pacific is the fastest-growing region in the CO2 Mineralisation Chemical market during the forecast period.