Market Overview

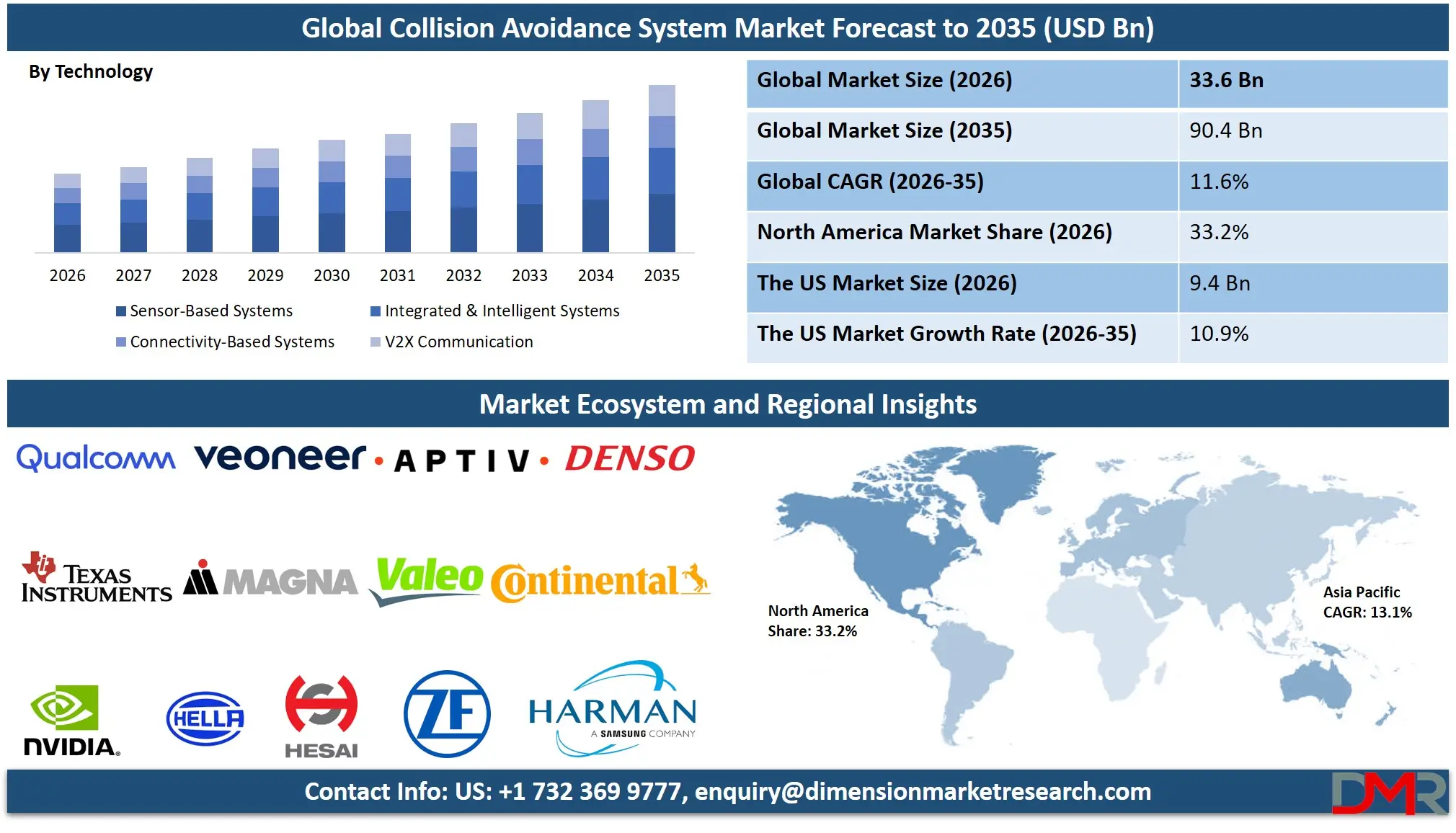

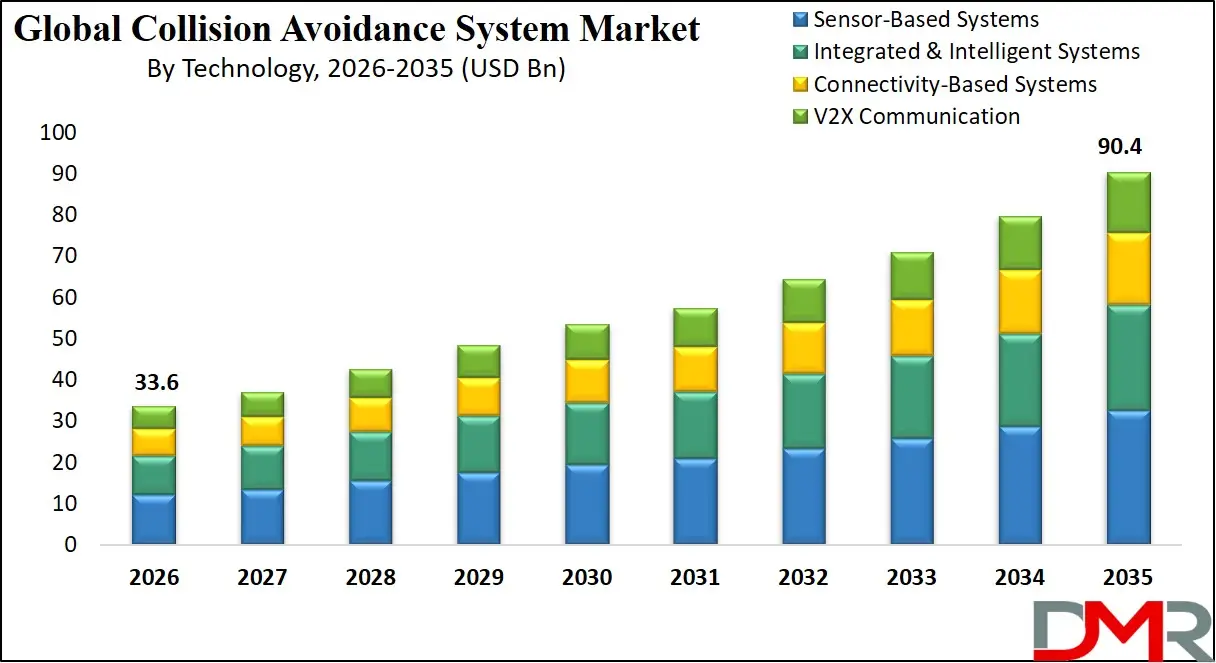

The Global Collision Avoidance System (CAS) Market is estimated to reach USD 33.6 billion in 2026 and is projected to expand at a compound annual growth rate (CAGR) of 11.6% from 2026 to 2035, ultimately reaching USD 90.4 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This strong growth trajectory is driven by the increasing integration of Advanced Driver Assistance Systems (ADAS), rising adoption of autonomous and semi-autonomous vehicles, and stringent vehicle safety regulations across major automotive markets. The demand for technologies such as Adaptive Cruise Control (ACC), Autonomous Emergency Braking (AEB), Forward Collision Warning (FCW), Lane Keeping Assist (LKA), and Blind Spot Detection (BSD) continues to accelerate across passenger and commercial vehicle segments.

Rapid advancements in radar sensors, LiDAR systems, camera-based vision technology, ultrasonic sensors, and sensor fusion platforms are enhancing real-time object detection, obstacle avoidance, and predictive safety capabilities. Additionally, the integration of Artificial Intelligence (AI), machine learning algorithms, and V2X (Vehicle-to-Everything) communication systems is strengthening collision mitigation accuracy and vehicle situational awareness.

Growth is further supported by expanding electric vehicle (EV) penetration, increasing fleet safety investments, and government mandates for mandatory safety features in regions such as North America, Europe, and Asia Pacific. The evolution toward SAE Level 3–Level 5 autonomous driving is also expected to significantly boost demand for high-performance collision avoidance architectures.

Technological advancements, including 4D imaging radar, solid-state LiDAR, thermal imaging cameras, V2X communication, cloud-based hazard mapping, and edge AI processing, are transforming the market into a highly sophisticated and integrated safety ecosystem. Integration of deep learning algorithms for pedestrian and cyclist recognition, adaptive behavior prediction, and sensor fusion architectures is reshaping automotive safety standards globally.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government initiatives promoting Vision Zero road safety policies, mandatory NCAP safety ratings, and smart city infrastructure investments further accelerate global adoption. However, barriers such as high system costs, integration complexity with legacy vehicles, varying regulatory standards across regions, and cybersecurity vulnerabilities remain. Despite these limitations, the convergence of sensor technology, AI, and connected mobility positions collision avoidance systems as a cornerstone of global automotive safety transformation through 2035.

The US Collision Avoidance System Market

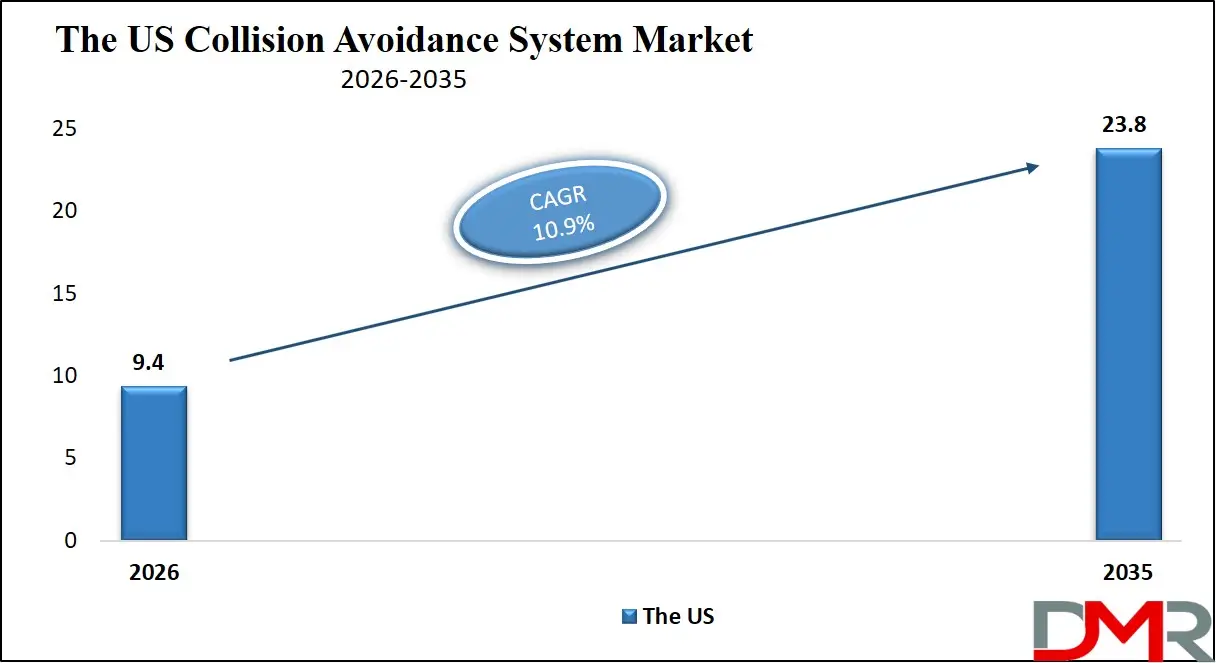

The U.S. Collision Avoidance System Market is projected to reach USD 9.4 billion in 2026 and grow at a CAGR of 10.9%, reaching USD 23.8 billion by 2035. The U.S. leads global adoption due to its advanced automotive technology ecosystem, high vehicle ownership rates, stringent safety regulations, and strong consumer awareness of advanced safety features.

The National Highway Traffic Safety Administration (NHTSA) has been progressively mandating collision avoidance technologies, including automatic emergency braking as a standard feature in new vehicles, fueling widespread OEM adoption. Major automakers such as Ford, General Motors, and Tesla are integrating increasingly sophisticated sensor suites and AI-based predictive algorithms across their vehicle lineups.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. regulatory support through the Infrastructure Investment and Jobs Act, which includes funding for connected vehicle infrastructure and V2X deployment, encourages investment in next-generation collision prevention technologies. Training programs and partnerships with automotive technical schools are emerging to develop expertise in calibration and maintenance of advanced sensor systems, ensuring proper functionality throughout vehicle lifetime.

The rapid rise of over-the-air (OTA) update capabilities, real-time cloud-based hazard alerting, and integration with smart city traffic infrastructure continues to redefine the U.S. automotive safety landscape, positioning the country as a global leader in collision avoidance technology deployment.

The Europe Collision Avoidance System Market

The Europe Collision Avoidance System Market is projected to be valued at approximately USD 9.2 billion in 2026 and is projected to reach around USD 23.5 billion by 2035, growing at a CAGR of about 11.0% from 2026 to 2035. Europe's leadership is anchored by strong regulatory frameworks including Euro NCAP safety ratings, General Safety Regulation mandates, and rigorous type-approval requirements.

Countries such as Germany, France, the U.K., Sweden, and Italy are widely adopting collision avoidance technologies, driven by stringent safety standards, high consumer expectations for vehicle safety, and government-backed initiatives like the EU's Vision Zero road safety program. The German automotive industry, with premium manufacturers like Mercedes-Benz, BMW, and Volkswagen Group, is particularly active in developing and deploying advanced sensor fusion and AI-based safety systems.

Europe's dense urban environments, high highway speeds, and focus on pedestrian and cyclist protection further drive adoption of sophisticated detection algorithms. Funding through Horizon Europe and national automotive innovation funds supports R&D in next-generation sensor technology, V2X communication, and predictive threat modeling.

New vehicle models increasingly feature integrated safety suites combining multiple sensor modalities, cloud-connected hazard databases, and over-the-air updatable safety algorithms. With strong technical standards, emphasis on occupant and vulnerable road user protection, and leadership in autonomous vehicle development, Europe remains one of the most advanced regions in collision avoidance system penetration.

The Japan Collision Avoidance System Market

The Japan Collision Avoidance System Market is anticipated to be valued at approximately USD 3.1 billion in 2026 and is expected to attain nearly USD 8.4 billion by 2035, expanding at a CAGR of about 11.7% during the forecast period. Japan's aging population, high traffic density, and strong government commitment to traffic fatality reduction drive demand for advanced collision avoidance technologies.

The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) actively supports safety technology adoption through regulatory incentives, public awareness campaigns, and integration of advanced driver assistance systems into public transportation fleets. Japan's leadership in sensor miniaturization, camera technology, and robotics accelerates innovation in compact, high-performance collision avoidance systems suitable for the country's diverse vehicle segments.

Japan's concept of "Society 5.0" applied to mobility, driven by companies like Toyota, Honda, and Denso, integrates AI, connected vehicle technology, and sensor fusion into seamless safety ecosystems. Collision avoidance systems are being deployed across Tokyo's dense urban traffic networks, highway systems, and aging driver populations. Japan's cultural emphasis on technological precision and safety excellence, combined with automotive innovation, positions the country as a high-growth market for advanced collision prevention technologies.

Global Collision Avoidance System Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Collision Avoidance System Market is expected to be valued at USD 33.6 billion in 2026 and is projected to reach USD 90.4 billion by 2035, showcasing rapid expansion supported by rising safety mandates and consumer demand for crash prevention technologies.

- High CAGR Driven by Safety Technology Adoption: The market is expected to grow at an impressive CAGR of 11.6% from 2026 to 2035, fueled by accelerating sensor integration, AI-driven threat prediction, cloud-based hazard mapping, and increasing vehicle electrification and autonomy worldwide.

- Strong Growth Trajectory in the United States: The U.S. Collision Avoidance System Market stands at USD 9.4 billion in 2026 and is projected to reach USD 23.8 billion by 2035, expanding at a CAGR of 10.9% due to robust regulatory mandates, high consumer awareness, and advanced technology adoption.

- North America Maintains Regional Dominance: North America is expected to capture approximately 31.5% of the global market share in 2026, supported by mature automotive safety infrastructure, significant R&D investment, and stringent NCAP safety rating requirements.

- Rapid Advancement in Collision Avoidance Technologies: Innovations including 4D imaging radar, solid-state LiDAR, AI-based object classification, sensor fusion architectures, and V2X communication are significantly enhancing detection range, accuracy, and reliability of collision prevention systems.

- Growing Safety Regulations Boost Adoption: Rising global implementation of mandatory safety ratings, pedestrian protection standards, and autonomous emergency braking requirements is driving sustained demand for comprehensive collision avoidance solutions.

Global Collision Avoidance System Market: Use Cases

- Highway Automated Emergency Braking: Systems detect imminent rear-end collisions and automatically apply brakes to mitigate or avoid impact, significantly reducing highway accident severity.

- Urban Pedestrian and Cyclist Detection: Advanced sensor fusion identifies vulnerable road users in complex urban environments, providing warnings and automated braking to prevent collisions.

- Intersection Collision Avoidance: Vehicle-to-everything (V2X) communication and 360-degree sensing detect crossing traffic and pedestrians at intersections, alerting drivers or automatically intervening.

- Lane Change Assistance and Blind Spot Monitoring: Radar and camera systems monitor adjacent lanes, providing alerts or steering intervention to prevent side-swipe collisions during lane changes.

- Fleet Safety Management: Commercial fleets utilize telematics-integrated collision avoidance data to monitor driver behavior, reduce accident rates, and optimize vehicle safety protocols.

Global Collision Avoidance System Market: Stats & Facts

National Highway Traffic Safety Administration (NHTSA) – United States

- 42,795 people were killed in U.S. motor vehicle crashes in 2022.

- Over 2.38 million people were injured in motor vehicle crashes in 2022.

- Approximately 94% of serious crashes are attributed to human error.

- Rear-end crashes account for nearly 29% of all crashes in the U.S.

- In 2023, NHTSA proposed making Automatic Emergency Braking (AEB) mandatory on all light vehicles.

- By 2029, all new passenger vehicles in the U.S. must include AEB under finalized federal rule.

- Heavy vehicles (>10,000 lbs) are involved in over 400,000 police-reported crashes annually.

- Around 5,000 fatalities annually involve large trucks.

Insurance Institute for Highway Safety (IIHS) – United States

- Front crash prevention systems reduce rear-end crashes by approximately 50%.

- Vehicles equipped with AEB show a 13% reduction in pedestrian crashes.

- Lane Departure Warning reduces single-vehicle, sideswipe, and head-on crashes by 11%.

- Blind Spot Monitoring reduces lane-change crashes by 14%.

- Rear Automatic Braking reduces backing crashes by up to 78%.

- By 2023, over 90% of new passenger vehicles sold in the U.S. were equipped with standard AEB.

European Commission – European Union

- Road crashes cause approximately 20,600 deaths annually in the EU (2022 data).

- The EU aims to reduce road deaths by 50% by 2030 under its Road Safety Policy Framework.

- From July 2022, all new vehicle models in the EU must include Advanced Emergency Braking systems.

- From July 2024, all newly registered vehicles in the EU must include Intelligent Speed Assistance and lane-keeping technologies.

- The EU estimates that new vehicle safety measures could save over 25,000 lives by 2038.

World Health Organization (WHO)

- Road traffic injuries cause approximately 1.19 million deaths globally each year.

- Road traffic injuries are the leading cause of death for children and young adults aged 5–29 years.

- Between 20–50 million people suffer non-fatal injuries annually from road crashes.

- More than 90% of road traffic deaths occur in low- and middle-income countries.

United Nations (UN) – Decade of Action for Road Safety

- The UN targets a 50% reduction in global road traffic deaths and injuries by 2030.

- The first Decade of Action for Road Safety aimed to save 5 million lives globally.

U.S. Department of Transportation (USDOT)

- Vehicle-to-Everything (V2X) technology could address up to 80% of unimpaired crash scenarios.

- The Connected Vehicle Pilot Deployment Program includes over 10,000 equipped vehicles across test sites.

International Civil Aviation Organization (ICAO)

- Airborne Collision Avoidance Systems (ACAS) are mandated on aircraft above 5,700 kg or carrying more than 19 passengers.

- Since implementation of TCAS/ACAS, mid-air collision risks have reduced significantly, contributing to a global accident rate below 2 accidents per million departures.

Global Collision Avoidance System Market: Market Dynamic

Driving Factors in the Global Collision Avoidance System Market

Stringent Government Safety Regulations

Mandatory safety requirements implemented by regulatory bodies worldwide represent the primary driver for collision avoidance system adoption. Regulations including the EU's General Safety Regulation, which mandates advanced emergency braking and lane keeping systems for all new vehicles, NHTSA's automatic emergency braking commitment from major automakers, and NCAP rating systems that incentivize higher safety specifications create non-negotiable demand. These regulatory frameworks ensure that collision avoidance technologies transition from optional luxuries to essential vehicle components, fundamentally reshaping automotive manufacturing requirements and creating sustained market growth.

Technology Innovation and Integration

Collision avoidance benefits heavily from rapid progress in sensor technology, AI processing, sensor fusion algorithms, and connectivity. Advanced systems feature 4D imaging radar with elevation detection, solid-state LiDAR with enhanced resolution, thermal cameras for night vision, and V2X communication for beyond-line-of-sight threat detection. These innovations enable vehicles to detect and respond to hazards with unprecedented speed and accuracy, operate in diverse environmental conditions, and predict complex traffic scenarios. The convergence of sensor technology with cloud-based hazard databases and edge AI processing further enhances detection capabilities, making collision avoidance systems increasingly sophisticated and reliable.

Restraints in the Global Collision Avoidance System Market

High System Costs and Integration Complexity

The significant cost of advanced sensor suites, processing hardware, and software development limits adoption in entry-level vehicle segments and price-sensitive emerging markets. Multi-sensor fusion systems incorporating radar, LiDAR, and high-resolution cameras can add thousands of dollars to vehicle costs. Additionally, integration complexity with existing vehicle architectures, calibration requirements, and the need for specialized technical expertise for maintenance and repair create adoption friction, particularly for smaller automakers and aftermarket applications.

Regulatory and Technical Standardization Challenges

Collision avoidance regulations, testing protocols, and performance standards vary significantly across regions, creating complexity for global automakers seeking unified system designs. Issues include divergent requirements for pedestrian detection, varying false-positive tolerance levels, and inconsistent testing methodologies. Furthermore, environmental conditions such as heavy rain, snow, fog, or direct sunlight can affect sensor performance, creating reliability concerns. Achieving robust performance across all operating conditions while maintaining regulatory compliance across multiple jurisdictions remains a significant technical and commercial challenge.

Opportunities in the Global Collision Avoidance System Market

Expansion into Emerging Vehicle Segments and Markets

Emerging markets represent major growth opportunities due to rapid motorization, increasing middle-class populations, and gradual implementation of safety regulations. Countries in Asia-Pacific, Latin America, Africa, and the Middle East are experiencing rising vehicle sales and growing awareness of automotive safety. Two-wheelers, commercial vehicles, and entry-level passenger cars in these regions present substantial untapped potential for cost-optimized collision avoidance solutions. Local manufacturing partnerships, modular system designs, and regulatory technical assistance programs can improve accessibility, driving the next wave of market expansion.

AI-Driven Predictive Threat Modeling and Behavior Prediction

The integration of AI not only for object detection but for predictive threat modeling, trajectory prediction, and scenario-based risk assessment creates new safety capabilities. AI can analyze historical accident data, real-time traffic patterns, and individual driver behavior to anticipate potential collision scenarios before they develop. This transforms collision avoidance from reactive intervention to proactive threat prevention. Integration with cloud-based mapping and real-time traffic data enables predictive hazard alerting for upcoming road conditions, intersections, and high-risk zones.

Trends in the Global Collision Avoidance System Market

Sensor Fusion and Redundancy Architectures

The trend toward combining multiple sensor modalities—radar, LiDAR, cameras, ultrasonic—in redundant, complementary configurations is accelerating. Sensor fusion architectures leverage the strengths of each technology while compensating for individual limitations, providing robust detection across all environmental conditions and scenarios. This approach supports higher levels of automation and ensures fail-safe operation through sensor redundancy, becoming the standard approach for premium vehicles and gradually penetrating mass-market segments.

V2X Communication Integration

Vehicle-to-everything (V2X) communication, including vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I), is emerging as a complementary technology to onboard sensors. V2X enables detection of hazards beyond line-of-sight, such as approaching emergency vehicles, traffic signal violations, or hidden intersection threats. Integration of V2X data with onboard sensor inputs creates a comprehensive safety picture, significantly expanding the effective range and predictive capability of collision avoidance systems. Government investment in connected infrastructure accelerates this trend.

Global Collision Avoidance System Market: Research Scope and Analysis

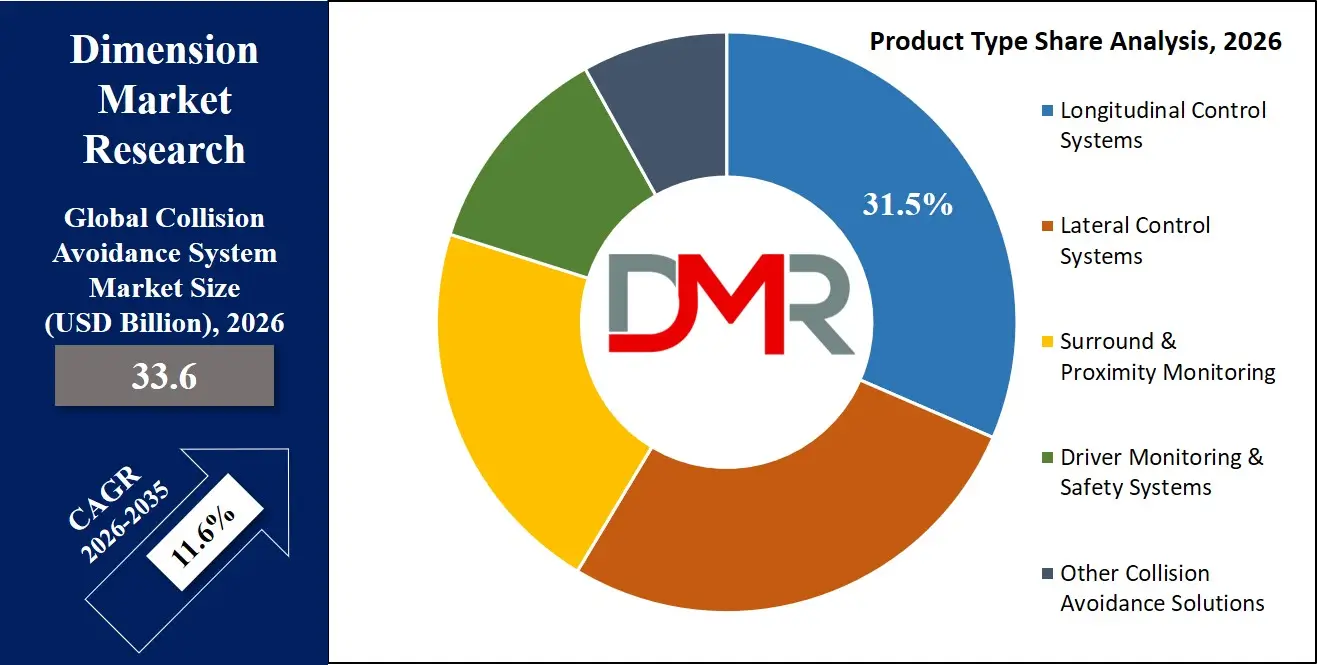

By Product Type Analysis

Within the product type segmentation, Longitudinal Control Systems dominate the global Collision Avoidance System market. These systems include Adaptive Cruise Control (ACC), Autonomous Emergency Braking (AEB), and Forward Collision Warning (FCW). Their dominance is primarily driven by regulatory mandates in major automotive markets such as the United States and the European Union, where AEB has become either mandatory or standard across most new vehicles. Longitudinal systems directly address rear-end collisions, which represent one of the most frequent accident types worldwide. Their proven effectiveness in reducing crash severity and fatalities makes them a regulatory and consumer priority.

Lateral Control Systems, including Lane Departure Warning (LDW) and Lane Keeping Assist (LKA), represent the second-largest segment. Their adoption has accelerated due to highway safety concerns and the growing penetration of Level 2 semi-autonomous driving technologies. These systems enhance vehicle stability and reduce unintended lane departures, particularly during high-speed driving.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Surround & Proximity Monitoring Systems, such as Blind Spot Detection and Parking Assistance, have high penetration rates, especially in mid-range and premium vehicles. However, their revenue contribution is slightly lower due to relatively lower system complexity compared to radar-based longitudinal control.

Driver Monitoring Systems (DMS) are the fastest-growing subsegment, supported by new European regulations mandating driver attention monitoring. Other advanced solutions such as intersection assist and emergency steering remain niche but are expanding alongside autonomous vehicle development.

Overall, longitudinal systems maintain the largest market share due to mandatory adoption and high safety impact.

By Technology Analysis

In terms of technology, Sensor-Based Systems dominate the Collision Avoidance System market, particularly radar and camera technologies. Radar sensors are widely adopted because they provide reliable object detection across various weather conditions and offer cost-effective scalability for mass-market vehicles. Cameras complement radar by enabling lane detection, traffic sign recognition, and object classification. Together, radar and camera systems form the backbone of modern Advanced Driver Assistance Systems (ADAS).

Integrated & Intelligent Systems (Sensor Fusion) represent the fastest-growing segment. Automakers increasingly combine radar, camera, ultrasonic, and sometimes LiDAR data into centralized processing units to improve detection accuracy and reduce false positives. Sensor fusion is particularly critical for Level 2+ and Level 3 automation, where higher reliability standards are required.

Learning-Based Processing Systems, driven by artificial intelligence and machine learning algorithms, are gaining traction. These systems enhance real-time decision-making, predictive collision detection, and adaptive driving behavior. However, AI functions are typically layered on top of existing sensor platforms rather than acting as standalone solutions.

Connectivity-Based Systems, including V2X communication, remain in early-stage commercialization. While pilot programs in North America, Europe, and Asia demonstrate strong safety potential, infrastructure deployment and standardization challenges limit widespread adoption.

Currently, radar and camera-based systems dominate revenue share due to cost efficiency and regulatory acceptance, while sensor fusion and AI-based processing are expected to shape long-term market expansion.

By Vehicle Type Analysis

Passenger Vehicles are poised to be the largest and most dominant vehicle type segment for collision avoidance systems, driven by powerful global consumer trends and regulatory mandates. The sheer volume of passenger vehicle production—exceeding 60 million units annually—creates the largest addressable market. Consumer demand for safety features, reflected in purchasing decisions and willingness to pay for advanced driver assistance packages, drives automaker investment. The segment is also the primary focus of regulatory mandates, including AEB requirements and NCAP rating systems that incentivize comprehensive safety suites. From entry-level compacts to luxury sedans, the economic and regulatory pressures in passenger vehicle manufacturing make the adoption of collision avoidance systems not merely advantageous but increasingly essential for market competitiveness.

Commercial Vehicles rank as the second-largest vehicle type segment, fueled by distinct operational and safety requirements. Trucks, buses, and vans face unique challenges including longer stopping distances, larger blind spots, and higher accident severity. Fleet operators recognize collision avoidance systems as investments that reduce accident costs, lower insurance premiums, and protect valuable assets and drivers. Regulatory pressure, including specific mandates for commercial vehicle safety systems in various regions, further drives adoption. While lower in unit volume than passenger vehicles, the higher system content per vehicle and strong ROI proposition for fleet operators secure commercial vehicles as a significant market segment.

By Autonomy Level Analysis

The Collision Avoidance System market is currently dominated by Level 1 (Driver Assistance) and Level 2 (Partial Automation) vehicles. These levels include features such as Adaptive Cruise Control, Lane Keeping Assist, and Automatic Emergency Braking. Most new vehicles sold globally fall within these categories, making them the primary revenue drivers.

Level 1 systems provide single-function assistance, such as steering or acceleration support, while Level 2 combines multiple systems to offer partial automation under driver supervision. Increasing consumer demand for convenience and safety has significantly accelerated Level 2 penetration, particularly in North America, Europe, China, Japan, and South Korea.

Level 0 vehicles, lacking automation features, are steadily declining in developed markets due to mandatory safety requirements. Level 3 (Conditional Automation) is emerging in premium vehicle segments but faces regulatory and liability challenges that slow broader deployment.

Level 4 and Level 5 automation, which represent high and full automation respectively, remain limited to pilot programs and specific use cases such as robo-taxis and controlled environments. These levels require highly advanced sensor fusion, LiDAR, AI computing platforms, and redundancy systems, resulting in high costs. Currently, Level 1 and Level 2 dominate due to affordability, scalability, and regulatory support, while higher autonomy levels represent long-term growth potential rather than present market dominance.

By Sales Channel Analysis

The OEM (Original Equipment Manufacturer) segment dominates the Collision Avoidance System market. Most collision avoidance technologies require deep integration with vehicle electronic control units (ECUs), braking systems, steering modules, and onboard software platforms. Factory installation ensures proper calibration, compliance with safety standards, and seamless integration with vehicle architecture.

Regulatory mandates further strengthen OEM dominance. In the U.S. and EU, safety features such as AEB and lane-keeping systems are required in new vehicles, making OEM installation compulsory. Additionally, consumers increasingly expect advanced safety features as standard equipment rather than optional add-ons.

The Aftermarket segment remains comparatively smaller but serves important roles in retrofitting older vehicles and upgrading commercial fleets. Emerging economies with slower vehicle turnover rates demonstrate higher aftermarket potential. However, technical limitations and calibration challenges restrict widespread retrofit of complex radar- and camera-based systems.

OEM channels also benefit from partnerships between automakers and Tier-1 suppliers, ensuring cost optimization and large-scale deployment. As vehicles become increasingly software-defined, integrated safety platforms are more difficult to replicate through aftermarket installations.

Overall, OEM installations dominate revenue share due to regulatory mandates, technological complexity, and integration requirements, while aftermarket growth remains supplementary.

By End User Analysis

Automotive OEMs are anticipated to dominate the market as the primary integrators and beneficiaries of collision avoidance technology. These entities possess the engineering capability for system integration, the production scale to achieve cost efficiencies, and the regulatory compliance responsibilities that mandate safety technology adoption. For them, collision avoidance systems represent both compliance requirements and competitive differentiation opportunities. Premium OEMs leverage advanced safety suites as key selling propositions, while volume manufacturers focus on cost-optimized compliance with regulatory minimums. OEMs serve as crucial partners for technology suppliers, co-developing integrated solutions and establishing the specifications that define market standards.

Aftermarket and Fleet Operators represent the vital second-largest end-user segment, for whom collision avoidance adoption is a strategic investment in safety and operational efficiency. Fleet operators face direct costs from accidents including vehicle repair, downtime, insurance premiums, and liability. For them, retrofitting collision avoidance systems to existing vehicles represents a tangible investment with measurable ROI through accident reduction. Commercial fleets, government vehicle fleets, and public transportation authorities increasingly mandate collision avoidance technology through procurement specifications. Aftermarket system providers serve this segment with retrofit solutions that bring advanced safety capabilities to vehicles not originally equipped, extending the addressable market beyond new vehicle production.

The Global Collision Avoidance System Market Report is segmented on the basis of the following:

By Product Type

- Longitudinal Control Systems

- Adaptive Cruise Control (ACC)

- Autonomous Emergency Braking (AEB)

- Forward Collision Warning (FCW)

- Pedestrian & Cyclist Detection Systems

- Lateral Control Systems

- Lane Departure Warning System (LDWS)

- Lane Keeping Assist (LKA)

- Lane Centering Assist

- Surround & Proximity Monitoring

- Blind Spot Detection (BSD)

- Rear Cross Traffic Alert (RCTA)

- Front & Rear Parking Sensors

- 360° Surround View Camera Systems

- Automated Parking Assistance

- Driver Monitoring & Safety Systems

- Driver Monitoring Systems (DMS)

- Driver Drowsiness Detection

- Attention & Distraction Monitoring

- Other Collision Avoidance Solutions

By Technology

- Sensor-Based Systems

- Radar

- LiDAR

- Camera

- Ultrasonic

- Fusion (Multi-Sensor)

- Infrared/Thermal Imaging

- Integrated & Intelligent Systems

- Sensor Fusion (Multi-Sensor Integration)

- Artificial Intelligence & Machine Learning-Based Processing

- Connectivity-Based Systems

- V2X Communication

By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Electric Vehicles

- Two-Wheelers

- Autonomous Vehicles

By Autonomy Level

- Level 0 (No Automation)

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

By Sales Channel

By End User Industry

- Automotive

- Aviation

- Marine & Shipping

- Railways

- Industrial / Warehousing & Logistics

- Other End-Use Areas

Impact of Artificial Intelligence in the Global Collision Avoidance System Market

- AI for Object Detection and Classification: AI analyzes sensor data to identify and classify objects including vehicles, pedestrians, cyclists, animals, and obstacles with high accuracy, continuously improving through deep learning on massive datasets.

- AI-Driven Threat Prediction and Trajectory Analysis: AI algorithms predict the future paths of detected objects based on current motion, historical patterns, and contextual cues, enabling anticipation of potential collision scenarios before they develop.

- Sensor Fusion and Environmental Modeling: AI integrates data from multiple sensor modalities into a cohesive environmental model, compensating for individual sensor limitations and providing comprehensive situational awareness.

- Edge AI for Real-Time Decision Making: On-vehicle AI processors enable real-time collision threat assessment and intervention decisions without cloud latency, ensuring instantaneous response to imminent crash scenarios.

- Learning from Fleet Data: AI systems aggregate anonymized data across vehicle fleets to continuously improve detection algorithms, identify emerging risk patterns, and enhance predictive capabilities through collective learning.

- Driver Behavior Monitoring and Personalization: AI analyzes driver attention, reaction patterns, and typical behavior to customize warning timing and intervention thresholds, reducing nuisance alerts while maintaining safety.

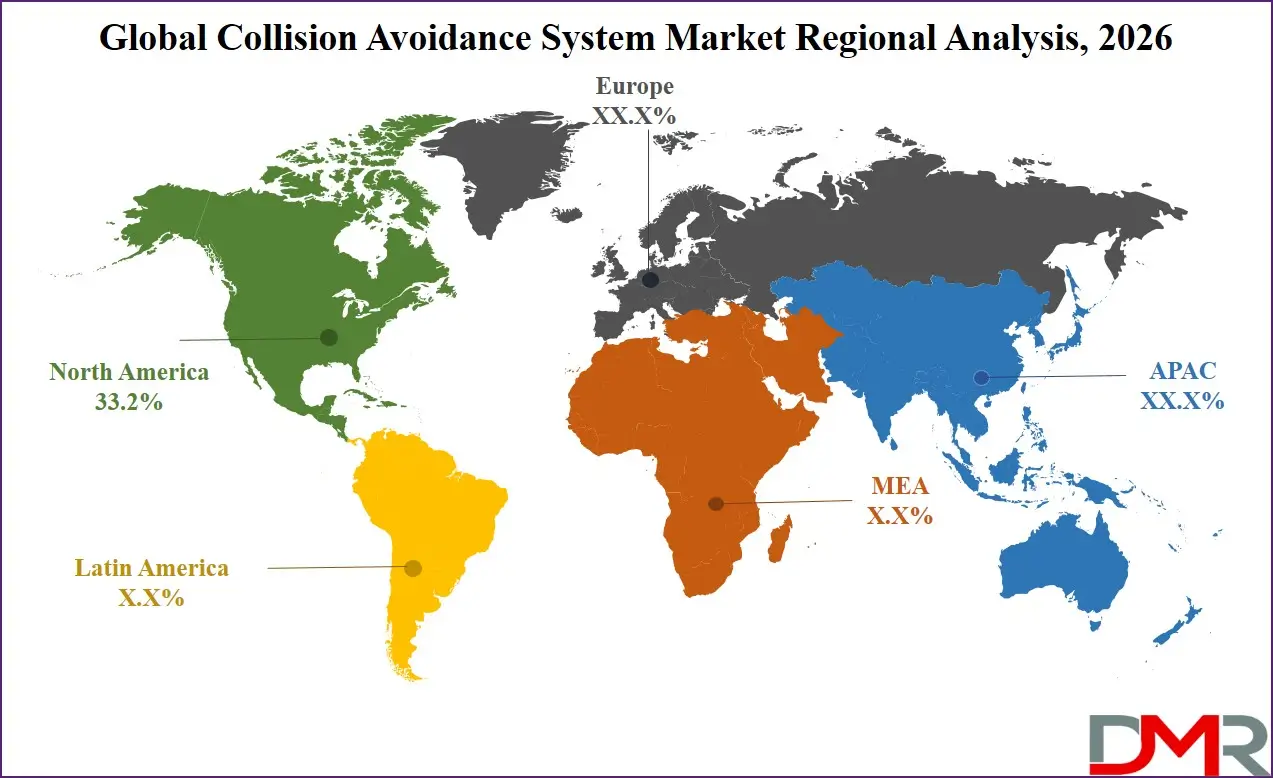

Global Collision Avoidance System Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to dominate the Global Collision Avoidance System Market with 31.5% of market share by the end of 2026, due to its strong regulatory environment, high adoption of advanced vehicle safety technologies, and the presence of leading automotive and semiconductor companies. The United States has implemented stringent safety regulations through federal agencies that mandate features such as Automatic Emergency Braking (AEB) and other advanced driver assistance systems (ADAS) in new vehicles, accelerating large-scale OEM integration. Consumers in the region demonstrate high awareness of vehicle safety ratings, which encourages automakers to equip even mid-range models with adaptive cruise control, lane-keeping assist, blind spot detection, and forward collision warning systems. Additionally, North America has one of the highest vehicle ownership rates globally, along with strong demand for SUVs, pickup trucks, and premium vehicles that typically incorporate advanced safety technologies as standard features.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The region also benefits from a robust technology ecosystem, with major semiconductor and AI companies supporting innovation in radar, sensor fusion, and autonomous driving platforms. Furthermore, North America leads in autonomous vehicle testing and pilot deployments, which require sophisticated collision avoidance architectures. These combined factors—regulatory mandates, consumer demand, high vehicle production value, and technological leadership—position North America as the dominant regional market in the global Collision Avoidance System industry.

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR and is poised to achieve rapid market share growth due to its massive vehicle production volumes, expanding middle-class vehicle ownership, and gradual implementation of safety regulations. Countries including China, India, Japan, South Korea, and ASEAN nations are experiencing rapid motorization and rising consumer expectations for vehicle safety. China's leadership in electric vehicle adoption and autonomous driving development, India's Bharat NCAP implementation, and Japan's advanced automotive technology sector are creating fertile ground for adoption. The region's cost sensitivity is being addressed through local sensor manufacturing, modular system designs, and partnerships between global technology suppliers and domestic automakers. This, combined with immense vehicle production volumes and improving regulatory frameworks, positions APAC as the fastest-growing market for collision avoidance systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Collision Avoidance System Market: Competitive Landscape

The Global Collision Avoidance System Market is moderately consolidated, featuring a mix of established automotive Tier 1 suppliers, specialized sensor technology companies, semiconductor firms, and software developers. Leading Tier 1 suppliers including Bosch, Continental, Denso, ZF Friedrichshafen, and Aptiv dominate system integration and OEM supply relationships, leveraging their deep automotive expertise and manufacturing scale. Sensor technology specialists such as Valeo, Hella, Magna, and Veoneer drive innovation in radar, camera, and LiDAR technologies.

Semiconductor and computing platform providers including NVIDIA, Intel (Mobileye), Qualcomm, Texas Instruments, and Infineon play increasingly influential roles, supplying the processing power and AI capabilities essential for advanced collision avoidance. LiDAR specialists including Luminar, Velodyne, Innoviz, Hesai, and Ouster are driving cost reduction and performance improvement in critical sensing technology.

Software and AI specialists including Mobileye (Intel), NVIDIA, Waymo, and Tesla (in-house development) are pushing the boundaries of perception algorithms and predictive modeling. Traditional automotive suppliers are acquiring or partnering with technology startups to accelerate development and maintain competitive positioning.

Some of the prominent players in the Global Collision Avoidance System Market are:

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- Valeo SA

- Magna International Inc.

- Hella GmbH & Co. KGaA

- Veoneer AB

- Mobileye (Intel Corporation)

- NVIDIA Corporation

- Qualcomm Technologies, Inc.

- Texas Instruments Incorporated

- Infineon Technologies AG

- Luminar Technologies

- Velodyne Lidar, Inc.

- Innoviz Technologies

- Hesai Group

- Ouster, Inc.

- Analog Devices, Inc.

- NXP Semiconductors

- Renesas Electronics Corporation

- Samsung Electronics (Harman International)

- Panasonic Corporation

- Other Key Players

Recent Developments in the Global Collision Avoidance System Market

- November 2025: Mobileye introduced its 4D imaging radar technology at CES 2026, featuring high-resolution point clouds and elevation detection capable of operating independently without LiDAR, significantly reducing system costs while maintaining safety performance.

- October 2025: Bosch announced a strategic partnership with a leading electric vehicle manufacturer to develop and supply comprehensive collision avoidance systems incorporating radar, camera, and software for next-generation EV platforms.

- September 2025: Continental completed the acquisition of a specialist AI software firm to enhance its collision avoidance systems' predictive capabilities, enabling earlier detection and more accurate trajectory prediction in complex scenarios.

- August 2025: The European Union published final regulations under the General Safety Regulation requiring all new passenger and commercial vehicles to be equipped with advanced emergency braking, lane keeping, and driver monitoring systems, effective 2027.

- July 2025: Qualcomm announced that BMW will utilize its Snapdragon Ride vision system-on-chip across multiple vehicle lines, enabling centralized processing of camera-based collision avoidance features.

- June 2025: Luminar announced an expanded partnership with Mercedes-Benz to supply its Iris LiDAR units for the automaker's next-generation vehicle platform, supporting advanced highway autonomous driving capabilities.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 33.6 Bn |

| Forecast Value (2035) |

USD 90.4 Bn |

| CAGR (2026–2035) |

11.6% |

| The US Market Size (2026) |

USD 9.4 Bn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Longitudinal Control Systems, Lateral Control Systems, Surround & Proximity Monitoring, Driver Monitoring & Safety Systems, and Other Collision Avoidance Solutions), By Technology (Sensor-Based Systems, Integrated & Intelligent Systems, Connectivity-Based Systems, and V2X Communication), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles, Two-Wheelers, and Autonomous Vehicles), By Autonomy Level (Level 0 (No Automation), Level 1 (Driver Assistance), Level 2 (Partial Automation), Level 3 (Conditional Automation), Level 4 (High Automation), and Level 5 (Full Automation)), By Sales Channel (OEM, and Aftermarket), By End User Industry (Automotive, Aviation, Marine & Shipping, Railways, Industrial / Warehousing & Logistics, Other end-use areas) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, Aptiv PLC, Valeo SA, Magna International Inc., Hella GmbH & Co. KGaA, Veoneer AB, Mobileye (Intel Corporation), NVIDIA Corporation, Qualcomm Technologies, Inc., Texas Instruments Incorporated, Infineon Technologies AG, Luminar Technologies, Velodyne Lidar, Inc., Innoviz Technologies, Hesai Group, Ouster, Inc., Analog Devices, Inc., NXP Semiconductors, Renesas Electronics Corporation, Samsung Electronics (Harman International), Panasonic Corporation, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Collision Avoidance System Market?

▾ The Global Collision Avoidance System Market size is estimated to have a value of USD 33.6 billion in 2026 and is expected to reach USD 90.4 billion by the end of 2035.

What is the growth rate in the Global Collision Avoidance System Market?

▾ The market is growing at a CAGR of 11.6 percent over the forecasted period of 2026 to 2035.

What is the size of the US Collision Avoidance System Market?

▾ The US Collision Avoidance System Market is projected to be valued at USD 9.4 billion in 2026. It is expected to witness subsequent growth in the upcoming period as it reaches USD 23.8 billion in 2035 at a CAGR of 10.9%.

Which region accounted for the largest Global Collision Avoidance System Market?

▾ North America is expected to have the largest market share in the Global Collision Avoidance System Market with a share of about 33.2% in 2026.

Who are the key players in the Global Collision Avoidance System Market?

▾ Some of the major key players in the Global Collision Avoidance System Market are Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, Aptiv PLC, Valeo SA, Mobileye (Intel Corporation), NVIDIA Corporation, and many others.