AI integration, in particular, is helping increase adenoma detection rates while decreasing missed lesions and leading to more efficient colorectal screenings. Furthermore, outpatient and ambulatory care settings that offer cost-effective and convenient solutions for patients is expanding the market footprint further.

However, several challenges still exist for colonoscopy adoption across regions: high costs associated with procedures in areas with underdeveloped healthcare infrastructure hinder access and cause patient discomfort during preparation; inconsistent reimbursement environments across regions also act as obstacles to widespread acceptance of colonoscopie.

Leading players in the colonoscopy market have focused their innovation efforts and strategic partnerships on meeting market challenges while capitalizing on growth opportunities.

Healthcare systems continue to prioritize preventive care while technological improvements enhance both accuracy and accessibility of colonoscopie procedures, driving sustained market expansion. Demographic shifts, rising cancer detection demand and technological breakthroughs will play key roles in shaping its future development.

Key Takeaways

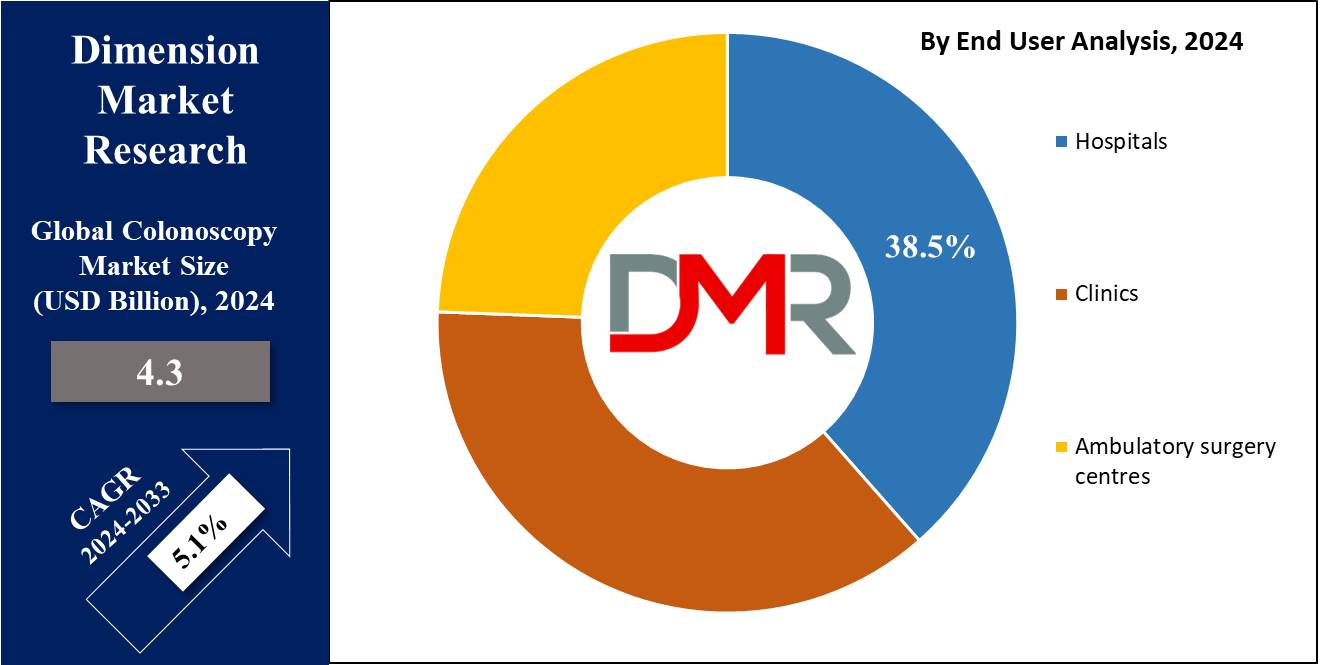

- The global colonoscopy market is expected to grow from USD 4.3 billion in 2024 to USD 6.8 billion by 2033, with a CAGR of 5.1%, indicating robust long-term demand.

- Colonoscope visualization systems dominated the product type segment in 2023, holding over 72.5% market share, driven by their critical role in imaging quality.

- Colorectal cancer Lynch syndrome was the leading application segment in 2023, reflecting the importance of colonoscopy in high-risk genetic groups.

- Ambulatory Surgery Centers (ASCs) accounted for more than 38.5% of the end-user segment in 2023, highlighting their growing role in delivering cost-effective, outpatient colonoscopy procedures.

- North America led the global colonoscopy market in 2023 with a 38.2% share, driven by advanced healthcare infrastructure and widespread screening initiatives.

Use Cases

- Aviation: E-fuels reduce emissions in aviation by acting as drop-in replacements for jet fuel and helping airlines meet net-zero targets without engine modifications.

- Shipping: E-fuels such as eMethanol and eDiesel enable sustainable shipping by cutting emissions while using existing engines and infrastructure.

- Industrial Heating: Hydrogen-based e-fuels power high temperature industrial processes while decreasing carbon emissions across steel and chemical production industries.

- Heavy-Duty Transport: E-fuels offer long-haul trucks an alternative fuel that lowers emissions without necessitating new infrastructure investments.

- Remote Power Generation: E-fuels offer remote areas a reliable power solution by storing renewable energy sources while decreasing fossil fuel use.

Driving Factors

Rising Incidence of Colorectal Cancer Fuels Increase in Demand for Colonoscopy Procedures

Colorectal cancer remains one of the primary drivers behind colonoscopy's market growth. Colorectal cancer ranks third most frequently among worldwide cancer diagnoses with approximately 1.9 million new cases and 940,000 deaths reported annually, according to World Health Organization estimates. As early detection awareness rises, colonoscopy remains an ideal way of diagnosing and preventing colorectal cancer, offering direct visualisation of colonic tissue as well as removal of precancerous polyps. Increased cancer screening programs across developed nations has further expanded adoption of colonoscopy as an indispensable way of combatting mortality from colorectal cancer mortality reduction strategy.

Aging Population Drives Uptick in Colonoscopy Procedures

An increasingly aged global population is driving the colonoscopy market forward, creating more demand for preventive and diagnostic procedures such as colonoscopy. Individuals aged 50 or above have increased risks for colorectal cancer and other GI disorders that necessitate preventive screening measures like colonoscopy. By 2050 it's anticipated that over two billion will have reached 60 years old, up from one billion today; colonoscopy plays an instrumental part in providing comprehensive screening programs to address age-related health concerns; its projected increase will inevitably contributes to continued demand within healthcare systems over decades to meet rising geriatric populations resulting in demand.

Technological Advancements Advance Diagnostic Precision and Market Expansion.

Technological developments play a pivotal role in improving colonoscopy procedures. HD imaging systems combined with

artificial intelligence-assisted colonoscopies are significantly increasing adenoma detection rates while decreasing missed lesions. Studies have demonstrated that AI-assisted colonoscopies can increase adenoma detection rates by 14.4%, leading to more precise diagnoses and better patient outcomes. Minimally invasive techniques have revolutionized patient comfort and recovery times, making colonoscopy procedures even more attractive to potential candidates. Not only have these technological developments enhanced diagnostic precision; they've also expanded market reach by making colonoscopies more cost-efficient across varying healthcare environments.

Growth Opportunities

Expanding into Emerging Markets May Present Significant Growth Potential

2023 should see significant gains to the global colonoscopy market from expanding healthcare infrastructure and government initiatives in emerging markets, particularly Asia-Pacific, Latin America, and parts of Africa. As healthcare systems modernize and dedicate more resources towards preventive care initiatives such as colorectal cancer detection screening programs; demand for colonoscopie procedures will likely surge considerably as availability of funding grows alongside greater awareness regarding its benefits - creating significant opportunity for market players who seek expansion into these developing regions.

AI Integration Enhances Diagnostic Accuracy and Efficiency

Artificial Intelligence (AI)-driven polyp detection tools could transform colonoscopy procedures globally in 2023 and beyond, revolutionising patient outcomes as well as efficiency of procedures. As AI technologies advance and gain regulatory approvals, healthcare providers will adopt these tools to expand screening capacities - propelling market expansion forward.

Disposable Colonoscopes Cut Risk and Drive Adoption

Disposable colonoscopes represent an innovative step toward infection control in environments with inadequate or inconsistent sterilization processes, eliminating cross-contamination between patients - an increasingly significant consideration in hospitals and clinics prioritizing infection prevention measures. With disposable scopes gaining ground across developed and emerging markets alike - especially regions with greater infection concerns - disposable scopes could drive procedure volumes up, creating growth opportunities for manufacturers.

Key Trends

Capsule Endoscopy Has Gained Staggering Adoption

2023 is projected to see capsule endoscopy become a dominant trend in colonoscopy market due to its minimally-invasive approach compared with traditional colonoscopy procedures. Capsule endoscopy utilizes an ingestible camera that captures images of the digestive tract for detection and analysis, providing patients with more comfortable options for colorectal abnormalities detection and removal. While capsule endoscopy cannot replace colonoscopy for biopsy or polyp removal procedures, its rapid rise as diagnostic tool represents shift toward patient-friendly screening technologies.

Outpatient and Ambulatory Settings Improve Accessibility while Reducing Costs

2023 will see an increasing shift toward colonoscopy procedures being completed at outpatient and ambulatory care centers due to their cost-effectiveness and convenience, offering shorter procedure times and lower facility costs than traditional hospital environments. Outpatient/ambulatory centers have increasingly become popular as regular procedures can be completed more efficiently with this trend set to persist as healthcare systems seek to optimize resource allocation while improving patient experiences.

Personalised Screening Gaining Momentum for Targeted Preventive Care

Personalized screening programs are revolutionizing colorectal cancer prevention landscape. Starting in 2023, more emphasis will be put on tailoring screening programs based on an individual's genetics, family history and lifestyle risks to maximize early detection rates while optimizing resource use - reflecting an increasing shift toward precision medicine as an overall trend that could shape future colorectal screening protocols.

Restraining Factors

High process costs limit accessibility and hinder market expansion

One of the key impediments to widespread colonoscopy adoption is its high cost. In low and middle income countries, colonoscopie may be prohibitively expensive without adequate healthcare coverage for patients without access.

As an example, in the U.S. the cost of colonoscopies can range anywhere from $1,000 to $3000 depending on insurance coverage, hospital setting and procedural needs - often leading to reduced access for underserved populations as well as contributing to inequities in colorectal cancer screening rates.

Financial burden associated with colonoscopy procedures remains an arduous barrier in regions with higher out-of-pocket expenses and limited insurance reimbursement, thus hampering colonoscopy market expansion potential. While healthcare systems strive to lower healthcare costs worldwide, this remains one of the major roadblocks to increasing colonoscopy adoption.

Substantial Patient Participation Impeded By Invasive Procedure

Colonoscopy's invasive nature presents another significant hurdle to market expansion, with patients reluctant to undergo its discomfort both during preparation phase and test itself, leading to lower compliance rates among asymptomatic populations where preventative screenings are vitally important. Studies demonstrate this effect: an American Cancer Society report revealed that 40% of adults eligible for colorectal cancer screening avoid colonoscopy due to its intrusiveness and discomfort of procedure.

Research Scope and Analysis

By Product Type

Colonoscope visualization systems were the clear market leaders among Product Type systems within the colonoscopy market in 2023, holding more than

72.5% market share. Widely recognized for providing high-quality imaging during colonoscopie procedures, these systems have seen widespread adoption across hospitals and outpatient centers alike. Their rising preference among healthcare facilities, coupled with technological innovations like higher image resolutions and real-time video processing has solidified their leadership role within this competitive industry.

Capsule endoscopy has emerged as an emerging less-invasive alternative to colonoscopy and is quickly gaining ground as an emerging segment. Although currently holding only a smaller market share compared to traditional colonoscopes, its adoption is increasing thanks to patient preference for less invasive diagnostic options and technological developments; consequently, capsule endoscopy's growth should significantly accelerate over the forecast period due to technological innovations and rising patient interest in minimally invasive procedures.

Deliberate use of disposable colonoscopes has seen widespread adoption within healthcare settings with stringent infection control protocols, particularly among developed markets with rising health awareness of infection prevention concerns. Disposable scopes offer reduced cross-contamination risks making them attractive options across both developed and emerging markets; though their current market penetration remains lower; their increasing use should fuel growth within this segment in coming years.

Outpatient and ambulatory care settings should also experience significant growth in colonoscopy procedures due to increased demand for cost-effective and convenient options. As healthcare systems prioritize efficiency and patient experience, these settings could gain more share in procedure volumes.

By Application

Colorectal cancer Lynch syndrome was the dominant Application segment within the colonoscopy market in 2023, accounting for an overwhelming portion of its market. This market segment's dominance can be explained by its high prevalence - Lynch syndrome being an inherited genetic condition which significantly raises colorectal cancer risks; regular colonoscopy screening for individuals diagnosed with this syndrome being essential preventive measure and thus contributing to its strong demand. As awareness regarding potential genetic predispositions to colorectal cancer increases, so will its dominating position within its respective market position within colonoscopies market position!

Polyps or colorectal cancer represents another significant part of the market, as colonoscopy has long been considered an industry standard method for detecting and removing polyps and their development into cancerous tumors. With colorectal cancer being one of the world's most frequently occurring and lethal cancers, routine colonoscopies for at-risk populations has become an integral component of preventive healthcare services - further contributing to its expansion.

As ulcerative colitis and Crohn's disease become more prevalent, colonoscopy has become an essential diagnostic and monitoring tool in their care, often necessitating regular colonoscopic inspection to track disease progress or detect early symptoms of dysplasia or cancer; further fueling market expansion within this segment.

The others category - which encompasses various gastrointestinal disorders requiring colonoscopic evaluation - also contributes to market expansion; although, their share remains much smaller compared to that of major segments. Overall, colonoscopy's widespread utility across many GI conditions demonstrates its vast application landscape.

By End Users

Ambulatory Surgery Centers (ASCs) were the market leaders among End Users for colonoscopy procedures in 2023, accounting for more than 38.5% of total market share in this segment of End Users of colonoscopy market. Their growth can be attributed to increasing consumer demand for cost-effective and convenient colonoscopie procedures at ASCs; with faster turnaround times and lower costs as compared with hospital settings making ASCs attractive options for routine screenings as well as elective procedures like colonoscopy screenings making ASCs more than dominant market players in terms of market position compared with traditional hospital settings resulting in ASC's prominent market position.

Hospitals remain an essential end user in the colonoscopy market, particularly for more complex procedures requiring advanced

medical support or when immediate follow up is essential. They frequently manage patients who pose higher medical risks, including those suffering from comorbidities or severe digestive conditions, thus increasing hospital profits over time. Even as more procedures take place outside hospitals' sphere of influence due to outpatient settings' increasing popularity and shifting some procedural volumes away from hospitals' traditional dominance in healthcare delivery - hospitals remain critical players regardless, particularly in regions without established ambulatory infrastructure as well as cases requiring immediate follow up treatments immediately afterwards.

Clinics represent a smaller but rapidly expanding segment within the end user landscape. Offering easy accessibility for patients requiring regular screenings or follow-up colonoscopies, clinics often operate more locally compared to larger healthcare facilities. Their role within the market continues to expand as more individuals look for convenient care in cities and suburbs where specialist services exist outside major hospital networks.

The Colonoscopy Market Report is segmented based on the following:

By Product Type

- Colonoscope visualization systems

- Others

By Application

- Colorectal cancer lynch syndrome

- Ulcerative colitis

- Crohn's Disease

- Polyps or colorectal cancer

- Others

By End Users

- Hospitals

- Clinics

- Ambulatory surgery centres

Regional Analysis

North America held the highest market share for global colonoscopy sales, at 38.2% in 2023. North American colonoscopie sales are driven by factors including high prevalence rates of colorectal cancer as well as established healthcare infrastructure; strong government support for cancer screening programs, AI assisted colonoscopies adoption rates and growing elderly populations requiring routine screenings further propel this region's dominance of global market.

Europe lags close behind, driven by robust healthcare systems and mandatory colorectal cancer screening programs in several European nations - Germany, France and U.K. for instance - which emphasize preventive healthcare along with increasing awareness about early cancer detection to increase demand for colonoscopies. Meanwhile in 2023 Europe is also benefiting from adopting advanced imaging systems and minimally invasive techniques which is further increasing their market share.

Asia-Pacific region is witnessing rapid expansion in colonoscopy market growth due to expanding healthcare infrastructure, rising disposable incomes and an increase in awareness regarding colorectal cancer prevention. China, Japan and India lead this market; Japan being especially notable due to their high adoption of advanced endoscopic technologies. Asia's increasing burden of colorectal cancer should spur significant development over the forecast period.

Latin America and Middle East/Africa markets experience slower but steady market expansion as these regions face healthcare access and infrastructure difficulties, but rising government initiatives to enhance cancer screening programs as well as growing investments are creating growth opportunities particularly within urban centers of these regions.

By Region

North America

Europe

- Germany

- U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

Medtronic remains a top player in the global colonoscopy market in 2023, capitalizing on their strong standing within medical devices industry and advanced colonoscopy technologies such as AI-assisted visualization systems and minimally invasive tools, to remain at the forefront of innovation within colonoscopy procedures. Their focus on increasing diagnostic accuracy and procedural efficiency matches with overall trend of artificial intelligence integration into colonoscopy procedures; Medtronic can capture significant market share both developed and emerging markets by expanding product portfolio and entering strategic partnerships thereby strengthening position within colonoscopy market

Olympus Corporation remains an impressive force in the global colonoscopy market, maintaining their dominance through an expansive offering of endoscopic solutions. They are best-known for their HD imaging systems and advanced endoscopes - widely utilized across hospitals and ambulatory surgery centers worldwide - while in 2023 Olympus will further innovate into AI enhanced colonoscopy to increase detection rates while improving patient outcomes. Olympus boasts strong global distribution channels along with decades of excellence in endoscopy to keep driving adoption of cutting edge technologies into healthcare markets worldwide.

Fujifilm Holdings has established itself in the colonoscopy market through their cutting-edge endoscopic systems and imaging technologies, particularly their focus on high resolution imaging and minimally invasive procedures. Their emphasis on research and development has produced continuous enhancements to product offerings - particularly diagnostic accuracy - over the years, and with AI solutions being introduced as colonoscopy procedures this year (2023), further cements Fujifilm as one of the premier competitors delivering on today's demand for precision in colorectal cancer screening and diagnosis.

Some of the prominent players in the Global Colonoscopy Market are:

- Medtronic

- Boston Scientific

- Avantis Medical Systems

- KARL STORZ

- Endomed Systems

- NA-MED

- Fujifilm Holdings

- Olympus Corporation

- HOYA Group

- Getinge Group

Recent developments

- Reese Pharmaceutical unveiled ColoTest in February 2024 - an innovative fecal immunochemical test (FIT) used for colorectal cancer screening that provides noninvasive early cancer detection by collecting stool samples at home and sending them directly to lab analysis for analysis. ColoTest seeks to increase screening compliance among those who may avoid traditional colonoscopy procedures while meeting an increasing demand for easy, cost-effective solutions that promote preventive screening solutions.

- In November 2023, Guardant Health in collaboration with Samsung Medical Center announced, through Shield, an advanced blood-based colorectal cancer test for South Koreans to use. Shield provides noninvasive detection of colorectal biomarkers without needing stool samples and colonoscopies - thus increasing screening rates as an accessible early detection solution, particularly among individuals reluctant to undergo traditional screening methods.

Report Details

| Report Characteristics |

| Market Size (2024) |

USD 4.3 Bn |

| Forecast Value (2033) |

USD 6.8 Bn |

| CAGR (2024-2033) |

5.1% |

| Historical Data |

2018 – 2023 |

| Forecast Data |

2025 – 2033 |

| Base Year |

2023 |

| Estimate Year |

2024 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type(Colonoscope visualization systems, Others), By Application(Colorectal cancer lynch syndrome, Ulcerative colitis, Crohn's Disease, Polyps or colorectal cancer, Others), By End Users(Hospitals, Clinics, Ambulatory surgery centres) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA

|

| Prominent Players |

Medtronic, Boston Scientific, Avantis Medical Systems, KARL STORZ, Endomed Systems, NA-MED, Fujifilm Holdings, Olympus Corporation, HOYA Group, Getinge Group |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |