Market Overview

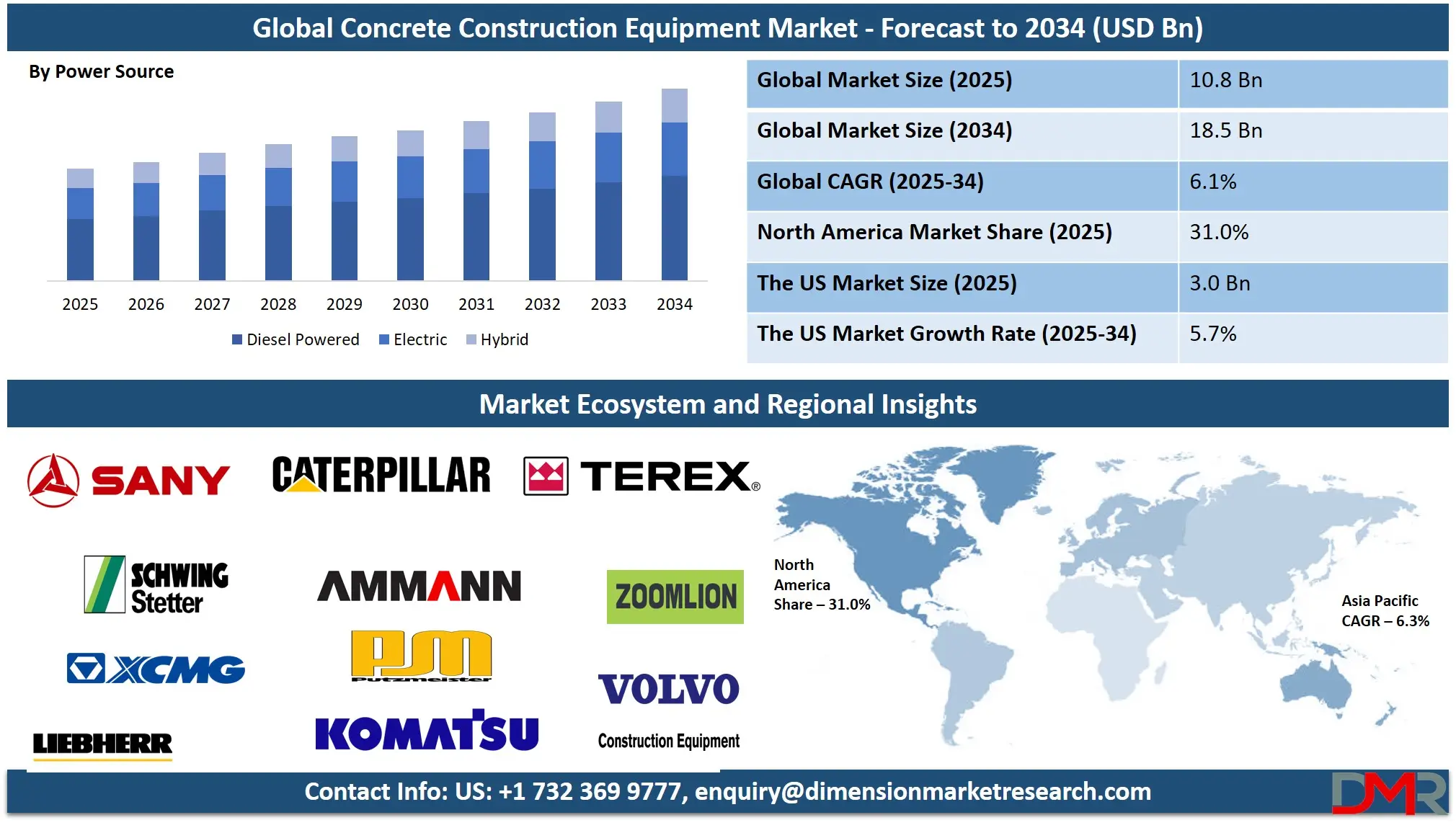

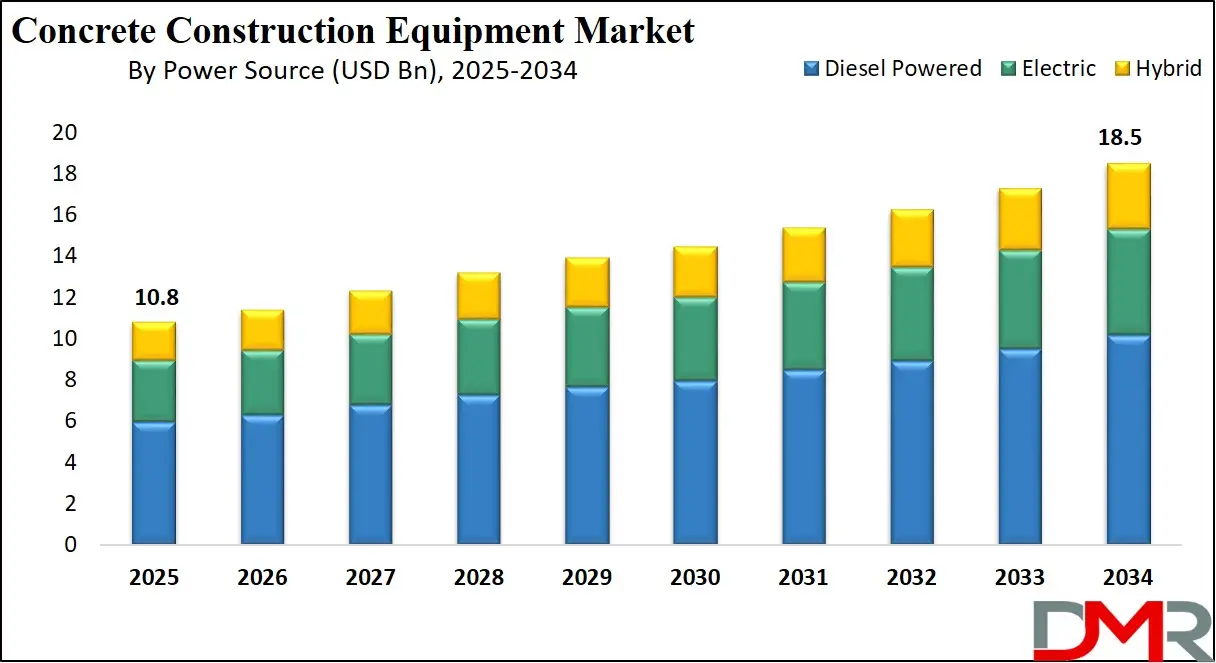

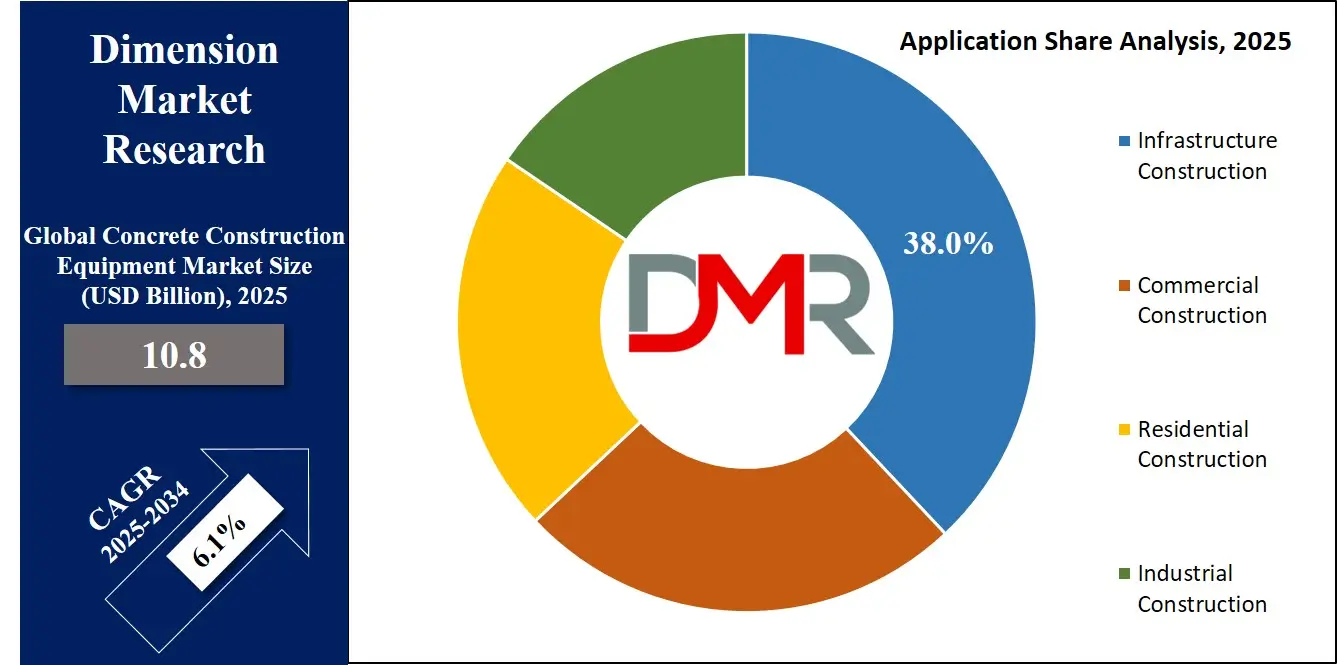

The Global Concrete Construction Equipment Market size is projected to reach USD 10.8 billion in 2025 and grow at a compound annual growth rate of 6.1% to reach a value of USD 18.5 billion in 2034.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Concrete construction equipment refers to the machinery and tools used for mixing, transporting, placing, compacting, finishing, cutting, and drilling concrete across construction projects. This market includes batch mixers, transit mixers, pumps, vibrators, screeds, saws, and drilling machines powered by diesel, electric, or hybrid systems. These solutions are essential for ensuring structural strength, precision, and efficiency in residential, commercial, industrial, and infrastructure construction. The market plays a crucial role in facilitating large-scale urban development and the expansion of modern infrastructure worldwide.

Concrete construction equipment holds strong importance within the global construction and infrastructure ecosystem due to its direct impact on project timelines, quality, and labor productivity. Rising investments in smart cities, transport infrastructure, and housing projects have increased demand for advanced and automated equipment. Equipment manufacturers are mainly focusing on durability, fuel efficiency, and compliance with environmental norms to support sustainable construction practices.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Ongoing shifts toward mechanized construction, electrification of equipment, and digital integration are influencing market growth. Contractors are prioritizing high-capacity, low-emission, and mobile equipment to manage labor shortages and reduce operating costs. Emerging economies are witnessing increased adoption as governments prioritize infrastructure modernization and urban resilience programs.

The US Concrete Construction Equipment Market

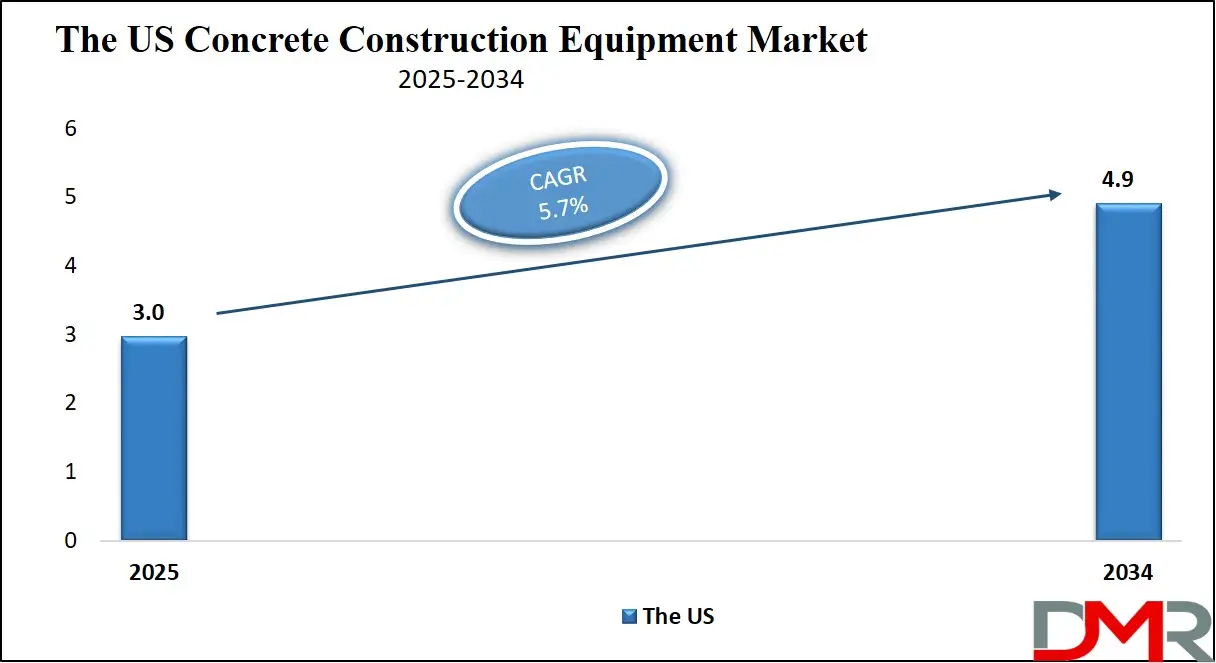

The US Concrete Construction Equipment Market size is projected to reach USD 3.0 billion in 2025 at a compound annual growth rate of 5.7% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US market is driven by strong infrastructure spending, highway rehabilitation programs, and commercial construction activity. Federal initiatives supporting transportation upgrades and public infrastructure renewal are encouraging contractors to invest in advanced concrete equipment. High labor costs are accelerating demand for automated and high-efficiency machinery. The presence of established equipment manufacturers, widespread rental models, and strict safety regulations further support market growth. Adoption of electric and hybrid equipment is increasing as emission standards tighten and sustainability goals gain prominence across states.

Europe Concrete Construction Equipment Market

Europe Concrete Construction Equipment Market size is projected to reach USD 2.2 billion in 2025 at a compound annual growth rate of 6.0% over its forecast period.

Strict environmental regulations and sustainability-driven construction policies influence Europe’s market. Initiatives such as the European Green Deal are pushing contractors toward low-emission and electric concrete equipment. Renovation of aging infrastructure, renewable energy projects, and urban redevelopment are key demand drivers. Countries such as Germany, France, and the UK lead in technology adoption, while Eastern Europe is witnessing growing demand due to industrial expansion. Equipment standardization and safety compliance play a major role in shaping purchasing decisions.

Japan Concrete Construction Equipment Market

Japan Concrete Construction Equipment Market size is projected to reach USD 756 million in 2025 at a compound annual growth rate of 5.6% over its forecast period.

Japan’s market is shaped by advanced construction technologies, seismic-resistant infrastructure requirements, and continuous urban redevelopment. Government-backed infrastructure maintenance programs and disaster-resilient construction initiatives support equipment demand. High automation levels, compact equipment designs, and precision-focused machinery are widely adopted due to limited space and skilled labor constraints. Aging infrastructure renewal and smart construction initiatives are creating opportunities, while high equipment costs and strict quality standards remain notable challenges for new entrants.

Concrete Construction Equipment Market: Key Takeaways

- Market Growth: The Concrete Construction Equipment Market size is expected to grow by USD 7.1 billion, at a CAGR of 6.1%, during the forecasted period of 2026 to 2034.

- By Power Source: The Diesel powered segment is anticipated to get the majority share of the Concrete Construction Equipment Market in 2025.

- By Application: The infrastructure construction segment is expected to get the largest revenue share in 2025 in the Concrete Construction Equipment Market.

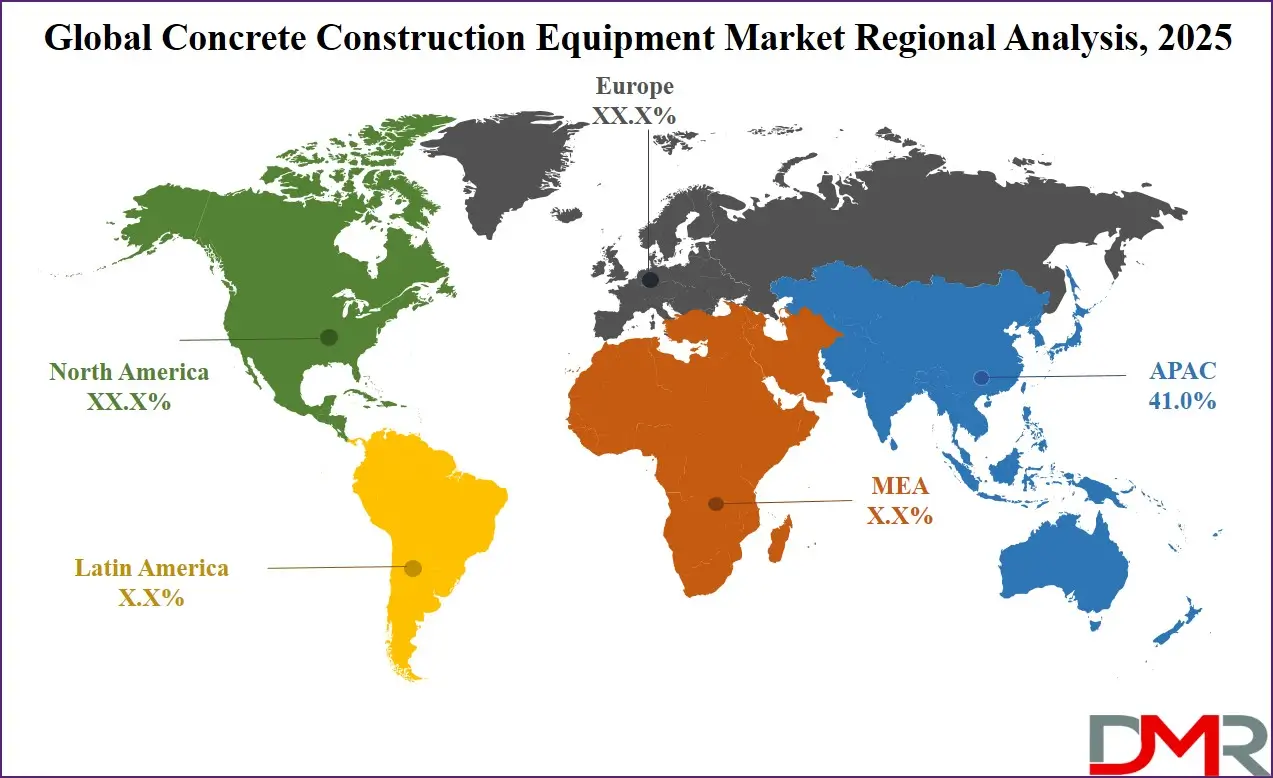

- Regional Insight: Asia Pacific is expected to hold a 41.0% share of revenue in the Global Concrete Construction Equipment Market in 2025.

- Use Cases: Some of the use cases of Concrete Construction Equipment include commercial building, residential construction, and more.

Concrete Construction Equipment Market: Use Cases:

- Residential Construction: Used for small- to mid-scale mixing, placing, and finishing to ensure structural integrity and faster project completion.

- Commercial Buildings: Enables high-volume concrete handling for offices, malls, and high-rise developments with precision and efficiency.

- Infrastructure Projects: Essential for roads, bridges, tunnels, and dams requiring continuous concrete placement and compaction.

- Industrial Facilities: Supports heavy-duty concrete work in factories, power plants, and logistics hubs demanding high load-bearing structures.

Stats & Facts

- US Department of Transportation reported over USD 75 billion allocated to concrete-intensive infrastructure projects in 2024.

- US Census Bureau recorded a 6.2% rise in construction spending involving concrete structures in 2024.

- European Commission stated that 37% of infrastructure funding in 2025 targets sustainable construction materials.

- Eurostat reported a 5.4% increase in construction equipment investments across EU nations in 2024.

- Japan Ministry of Land, Infrastructure, Transport and Tourism allocated over JPY 6 trillion (USD 38 billion) for infrastructure maintenance in 2025.

- World Bank indicated that emerging economies increased infrastructure investment by 8% in 2024.

- International Energy Agency noted a 12% rise in electric construction equipment adoption globally in 2025.

- US Environmental Protection Agency reported tightening emission standards for diesel construction equipment in 2024.

- OECD highlighted that urban infrastructure demand grew by 7% globally in 2025.

- European Investment Bank confirmed increased financing for low-emission construction machinery in 2024.

- Statistics Canada observed steady growth in concrete-intensive housing projects in 2025.

- Asian Development Bank reported increased infrastructure lending for transport and water projects in 2024.

Market Dynamic

Driving Factors in the Concrete Construction Equipment Market

Infrastructure Expansion

Large-scale infrastructure development is a major growth driver as governments invest in roads, bridges, airports, and public utilities. Concrete remains the preferred material for durability and load-bearing capacity, increasing reliance on specialized equipment. Public–private partnerships and stimulus programs are accelerating project execution timelines, pushing contractors to adopt high-capacity and automated equipment. Urbanization and population growth further intensify infrastructure needs, making concrete construction equipment essential for meeting modern engineering and safety standards.

Technological Advancements

Innovation in automation, telematics, and electric power systems is transforming equipment efficiency and usability. Smart controls improve accuracy in mixing and placing, reducing material waste. Hybrid and electric equipment lower fuel consumption and emissions, aligning with regulatory requirements. These advancements enhance productivity, reduce downtime, and lower long-term operational costs, making advanced machinery attractive to contractors and rental providers.

Restraints in the Concrete Construction Equipment Market

High Capital Investment

Concrete construction equipment involves high upfront costs, particularly for automated and eco-friendly machinery. Small and mid-sized contractors often struggle to justify large investments due to budget constraints. Maintenance expenses, spare parts costs, and skilled operator requirements further increase ownership costs, limiting adoption in cost-sensitive markets and slowing replacement cycles.

Regulatory and Operational Challenges

Compliance with varying emission, safety, and noise regulations across regions complicates equipment deployment. Contractors operating in multiple markets face higher compliance costs. Limited charging infrastructure for electric equipment and inconsistent fuel quality in developing regions also hinder smooth operations, affecting market penetration.

Opportunities in the Concrete Construction Equipment Market

Growth in Rental Models

The expansion of equipment rental services presents strong opportunities by lowering entry barriers for contractors. Rental models enable access to advanced equipment without high capital expenditure. Growing preference for flexible project-based equipment usage is driving demand for rental-friendly, durable machines.

Emerging Market Infrastructure

Developing regions are increasing investments in transport, housing, and industrial infrastructure. Government-backed urban development programs and foreign investment inflows create untapped demand for concrete equipment. Localization of manufacturing and financing support further enhances growth potential.

Trends in the Concrete Construction Equipment Market

Electrification of Equipment

Electric and hybrid concrete equipment is gaining traction due to emission regulations and fuel cost volatility. Manufacturers are focusing on battery efficiency and charging solutions. This trend supports sustainable construction goals and reduces operational noise, particularly in urban projects.

Digital Integration

Telematics, remote monitoring, and predictive maintenance are increasingly integrated into equipment. These features improve fleet management, reduce downtime, and enhance project planning accuracy, making digital-enabled machinery more attractive to contractors.

Impact of Artificial Intelligence in Concrete Construction Equipment Market

- Predictive Maintenance: AI analyzes equipment data to prevent breakdowns and reduce downtime.

- Quality Control: AI systems ensure accurate mixing ratios and placement consistency.

- Fleet Optimization: Intelligent scheduling improves equipment utilization rates.

- Autonomous Operations: AI supports semi-autonomous concrete placement and finishing.

- Cost Optimization: AI-driven insights reduce fuel and maintenance expenses.

- Safety Monitoring: AI detects operational risks and improves job-site safety.

Research Scope and Analysis

By Equipment Type Analysis

Concrete mixing equipment accounts for approximately 32% of the Concrete Construction Equipment market in 2025, making it the leading equipment type segment. Its dominance is attributed to its indispensable role across residential, commercial, industrial, and infrastructure construction projects. Batch mixers and transit mixers are extensively used to ensure uniform concrete quality, consistency, and large-volume output. Infrastructure megaprojects and high-rise commercial developments rely heavily on high-capacity and automated mixing solutions to meet tight construction schedules. Continuous innovation in automation, digital controls, and fuel-efficient designs has further strengthened adoption, allowing contractors to reduce material wastage, enhance productivity, and maintain compliance with quality and safety standards.

Concrete cutting and drilling equipment is emerging as one of the fastest-expanding segments, driven by increasing renovation, retrofitting, and infrastructure maintenance activities. While holding a smaller share than mixing equipment in 2025, demand is rising steadily as aging buildings, bridges, and transport infrastructure require precision cutting, drilling, and modification. These tools are essential for expansion projects, utility installations, and structural upgrades without compromising safety or integrity. Advancements in diamond cutting technology, electric-powered saws, and low-noise drilling solutions are improving efficiency and usability, especially in urban environments. Growing focus on refurbishment rather than new construction in developed regions is further accelerating segment growth.

By Power Source Analysis

Diesel-powered equipment represents nearly 54% of the market share in 2025, maintaining its leadership due to reliability, high torque output, and suitability for heavy-duty operations. These machines are widely preferred for large infrastructure projects, remote construction sites, and continuous operations where access to electric charging infrastructure is limited. Diesel equipment offers consistent performance under harsh conditions and supports high-load applications such as concrete mixing, pumping, and compaction. Despite rising environmental concerns, ongoing improvements in fuel efficiency and emission control technologies help sustain demand. Contractors continue to rely on diesel-powered solutions for their durability, operational flexibility, and proven performance in large-scale construction projects.

Electric-powered concrete construction equipment is the fastest-growing power source segment, driven by tightening emission regulations and increasing sustainability commitments. Although its 2025 market share remains lower than diesel, adoption is accelerating rapidly, particularly in urban and indoor construction environments. Electric equipment offers lower operating costs, reduced noise levels, and zero on-site emissions, making it ideal for residential and commercial projects in densely populated areas. Advancements in battery technology, charging infrastructure, and energy efficiency are enhancing performance and runtime. Government incentives and green construction initiatives are further supporting growth, positioning electric equipment as a key contributor to the market’s future transformation.

By Mobility Analysis

Mobile equipment holds approximately 61% of the Concrete Construction Equipment market share in 2025, making it the dominant mobility segment. Its leadership is driven by flexibility, ease of transportation, and adaptability across multiple job sites. Mobile mixers, pumps, and finishing equipment are widely used in infrastructure, residential, and commercial projects where frequent relocation is required. Contractors prefer mobile solutions to optimize project timelines, reduce logistical complexity, and improve on-site efficiency. The growing trend toward modular and fast-paced construction further supports demand. Continuous enhancements in maneuverability, fuel efficiency, and compact designs are reinforcing the strong position of mobile equipment across diverse construction applications.

Stationary equipment is witnessing steady growth, particularly in large batching plants, precast facilities, and industrial construction projects that require continuous and high-volume concrete output. While its 2025 market share is lower than mobile equipment, stationary solutions offer superior stability, precision, and long-term operational efficiency. These systems are commonly used in infrastructure hubs, industrial complexes, and ready-mix concrete plants where mobility is less critical. Increasing investments in industrial infrastructure and centralized concrete production facilities are supporting demand. Technological advancements in automation and process control are further improving productivity, making stationary equipment an attractive option for large-scale, long-duration construction operations.

By Application Analysis

Infrastructure construction accounts for nearly 38% of the total market share in 2025, making it the leading application segment. This dominance is supported by substantial government investments in roads, highways, bridges, tunnels, dams, and public transport systems. Concrete construction equipment is essential for handling large volumes, continuous placement, and structural reinforcement required in such projects. National infrastructure development programs, public–private partnerships, and urban connectivity initiatives are sustaining strong demand. The long lifecycle and durability requirements of infrastructure assets further increase reliance on advanced concrete machinery, positioning this segment as a consistent revenue generator within the overall market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Residential construction is one of the fastest-growing application segments, fueled by rising housing demand, urban expansion, and population growth. Although its 2025 market share is lower than infrastructure, increased investments in affordable housing, high-rise apartments, and residential complexes are driving equipment adoption. Compact and mobile concrete equipment is particularly favored for residential projects due to space constraints and shorter project timelines. Government housing schemes and private real estate development are accelerating construction activity, especially in emerging economies. This segment benefits from the growing need for efficient, cost-effective equipment that supports rapid construction while maintaining quality and safety standards.

By End User Analysis

Construction contractors represent approximately 46% of the market share in 2025, making them the dominant end-user group. Contractors utilize concrete construction equipment across a wide range of residential, commercial, industrial, and infrastructure projects. Their dominance is driven by direct involvement in execution, scheduling, and quality control of construction activities. Large contractors often invest in advanced, high-capacity machinery to improve productivity and reduce project timelines, while smaller firms increasingly rely on rental models. The need to meet strict deadlines, safety regulations, and performance standards ensures consistent demand from this segment across all major construction markets.

Rental equipment providers are experiencing rapid growth as contractors seek to minimize capital expenditure and maintain operational flexibility. Although their 2025 market share remains lower than direct contractor ownership, demand is increasing steadily across regions. Rental providers offer access to advanced and specialized equipment without long-term financial commitments, making them attractive to small and mid-sized contractors. Short-term projects, maintenance work, and seasonal demand further support rental adoption. Expansion of rental fleets, improved maintenance services, and flexible pricing models are strengthening this segment’s role, positioning it as a key growth driver in the evolving construction ecosystem.

By Sales Channel Analysis

Dealer and distributor networks account for approximately 49% of total sales in 2025, making them the leading sales channel in the market. Their dominance is supported by localized market knowledge, strong after-sales service capabilities, and established relationships with contractors. Dealers provide critical services such as maintenance support, spare parts availability, operator training, and financing assistance. This channel is particularly important in emerging markets where direct manufacturer presence is limited. The ability to offer customized solutions and responsive technical support strengthens customer trust and long-term engagement, reinforcing the importance of dealer and distributor networks across regions.

Equipment rental is the fastest-growing sales channel, driven by shifting contractor preferences toward flexible and cost-efficient procurement models. While its 2025 share is lower than traditional dealer networks, growth is accelerating due to rising project-based construction and budget constraints. Rental channels allow users to access modern, well-maintained equipment without ownership risks. Increasing urban construction, short-duration projects, and technological complexity are boosting rental demand. The expansion of organized rental firms and digital booking platforms is further enhancing accessibility, making equipment rental an increasingly influential channel within the Concrete Construction Equipment market.

The Concrete Construction Equipment Market Report is segmented on the basis of the following:

By Equipment Type

- Concrete Mixing Equipment

- Batch Mixers

- Transit Mixers

- Concrete Placing Equipment

- Concrete Pumps

- Concrete Buckets

- Concrete Compaction Equipment

- Concrete Finishing Equipment

- Concrete Cutting & Drilling Equipment

- Concrete Saws

- Core Drilling Machines

By Power Source

- Diesel-Powered

- Electric

- Hybrid

By Mobility

- Mobile Equipment

- Stationary Equipment

By Application

- Residential Construction

- Commercial Construction

- Infrastructure Construction

- Roads & Highways

- Bridges

- Tunnels

- Dams

- Industrial Construction

By End User

- Construction Contractors

- Infrastructure Development Companies

- Ready-Mix Concrete (RMC) Producers

- Rental Equipment Providers

By Sales Channel

- Direct Sales

- Dealer & Distributor Network

- Equipment Rental

Regional Analysis

Leading Region in the Concrete Construction Equipment Market

Asia-Pacific accounts for approximately 41% of the Concrete Construction Equipment market share in 2025, making it the leading regional market globally. This dominance is driven by massive infrastructure development, rapid urbanization, and sustained government investments across major economies such as China, India, and Southeast Asian countries. Large-scale projects involving highways, railways, bridges, ports, and housing developments are creating strong and consistent demand for concrete construction equipment. Industrial expansion, growth in manufacturing hubs, and rising population density further support construction activity. Favorable government policies, public–private partnerships, and increasing adoption of mechanized construction methods continue to reinforce Asia-Pacific’s leadership position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Concrete Construction Equipment Market

The Middle East & Africa region is emerging as the fastest-growing market for concrete construction equipment, supported by rapid infrastructure expansion and rising foreign investments. Governments across the region are investing heavily in smart city initiatives, transport networks, energy facilities, and large-scale urban developments. Mega projects related to airports, metro systems, highways, and industrial zones are significantly boosting demand for advanced concrete equipment. Economic diversification efforts, particularly in Gulf countries, are accelerating construction activity beyond oil and gas. Additionally, improved access to financing and increasing participation of international contractors are creating strong growth momentum across the region.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The Concrete Construction Equipment market is highly competitive, with participants focusing on product innovation, rental partnerships, and regional expansion to strengthen their presence. Companies emphasize fuel efficiency, automation, electrification, and digital features to improve productivity and meet regulatory requirements. After-sales services such as maintenance support and spare parts availability are critical for customer retention. High entry barriers exist due to capital-intensive manufacturing and strict compliance standards. Strategic collaborations with contractors, infrastructure developers, and equipment rental providers are widely adopted to enhance market reach and sustain long-term competitiveness.

Some of the prominent players in the global Concrete Construction Equipment are:

- SANY Group

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- XCMG Group

- Liebherr Group

- Caterpillar Inc.

- Putzmeister Holding GmbH

- Schwing Stetter / Schwing GmbH

- Terex Corporation

- Volvo Construction Equipment / Volvo CE

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- Doosan Infracore Co., Ltd.

- Atlas Copco AB

- Ammann Group

- CON-E-CO

- Elkon

- Fangyuan Machinery

- Lintec

- McCrory Engineering

- Meka Concrete Plants

- Other Key Players

Recent Developments

- In January 2026, CASE Construction Equipment launched its BS CEV Stage V-compliant construction equipment range in Gurgaon, reinforcing its commitment to delivering sustainable, future-ready solutions for the Indian construction industry.The equipment was showcased at CASE NCR Store, a pre-existing dealership catering to customers across Gurgaon and the wider NCR region, in the presence of Puneet Vidyarthi, Head of Brand Marketing, CASE Construction Equipment, APAC & India. The event witnessed participation from over 150+ customers.

- In June 2025, Putzmeister launched its latest product BSA 1405 D Classic - Stationary Concrete Pump through an on-ground customer engagement campaign, the “Putzmeister Concrete Dastak Roadshow”. The BSA 1405 D Classic- Performance Simplified, represents the newest addition to Putzmeister’s strong product portfolio, designed to perform reliably in demanding site conditions with simple, user-friendly controls and low maintenance needs. Also customized for residential buildings, mid-rise projects, bridges, and long-distance pumping applications, this pump delivers powerful performance with practical ease.

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 10.8 Bn |

| Forecast Value (2034) |

USD 18.5 Bn |

| CAGR (2025–2034) |

6.1% |

| The US Market Size (2025) |

USD 3.0 Bn |

| Historical Data |

2019 – 2024 |

| Forecast Data |

2026 – 2034 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Equipment Type (Concrete Mixing Equipment, Concrete Placing Equipment, Concrete Compaction Equipment, Concrete Finishing Equipment, Concrete Cutting & Drilling Equipment), By Power Source (Diesel-Powered, Electric, Hybrid), By Mobility (Mobile Equipment, Stationary Equipment), By Application (Residential Construction, Commercial Construction, Infrastructure Construction, Industrial Construction), By End User (Construction Contractors, Infrastructure Development Companies, Ready-Mix Concrete (RMC) Producers, Rental Equipment Providers), By Sales Channel (Direct Sales, Dealer & Distributor Network, Equipment Rental) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

SANY Group, Zoomlion Heavy Industry Science & Technology Co., Ltd., XCMG Group, Liebherr Group, Caterpillar Inc., Putzmeister Holding GmbH, Schwing Stetter / Schwing GmbH, Terex Corporation, Volvo Construction Equipment / Volvo CE, Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Doosan Infracore Co., Ltd., Atlas Copco AB, Ammann Group, CON-E-CO, Elkon, Fangyuan Machinery, Lintec, McCrory Engineering, Meka Concrete Plants, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Concrete Construction Equipment Market?

▾ The Global Concrete Construction Equipment Market size is expected to reach USD 10.8 billion by 2025 and is projected to reach USD 18.5 billion by the end of 2034.

Which region accounted for the largest Global Concrete Construction Equipment Market?

▾ Asia Pacific is expected to have the largest market share in the Global Concrete Construction Equipment Market, with a share of about 41.0% in 2025.

How big is the Concrete Construction Equipment Market in the US?

▾ The US Concrete Construction Equipment market is expected to reach USD 3.0 billion by 2025.

Who are the key players in the Concrete Construction Equipment Market?

▾ Some of the major key players in the Global Concrete Construction Equipment Market include Caterpillar, SANY, XCMG Group and others

What is the growth rate in the Global Concrete Construction Equipment Market?

▾ The market is growing at a CAGR of 6.1 percent over the forecasted period.