What is the Congestive Heart Failure Drugs Market Size?

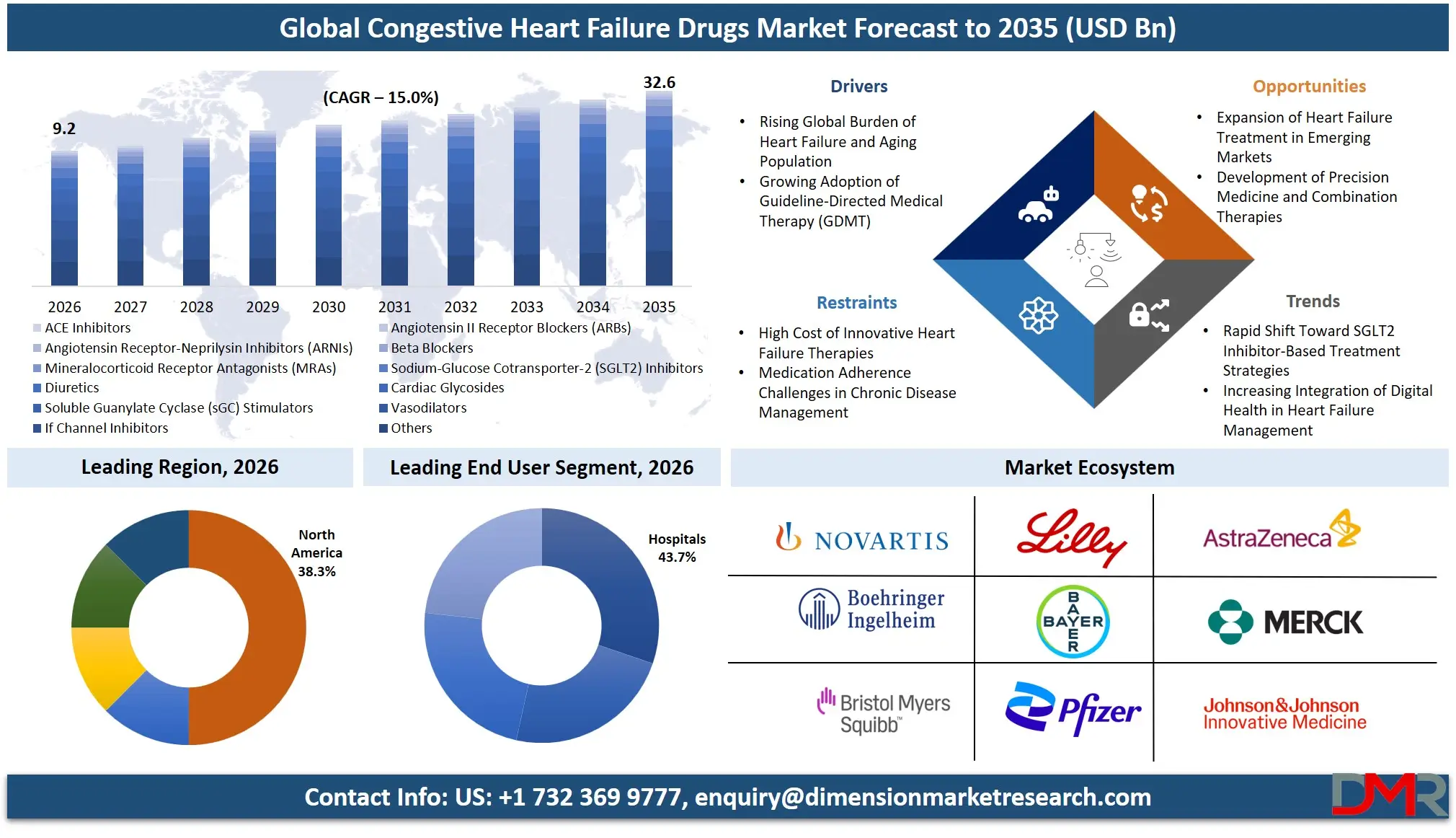

The Global Congestive Heart Failure Drugs Market is expected to reach a value of USD 9.2 billion in 2026, and it is further anticipated to reach USD 32.6 billion by 2035, growing at a CAGR of 15.0% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The congestive heart failure (CHF) drugs market is experiencing robust growth, propelled by a deepening understanding of the disease's pathophysiology and a paradigm shift toward multi-drug, guideline-directed medical therapy (GDMT). The market comprises a sophisticated armamentarium of drug classes from foundational ACE inhibitors and beta blockers to novel entrants like ARNIs and SGLT2 inhibitors designed to manage the hemodynamic and neurohormonal imbalances of heart failure. The rising global prevalence of cardiovascular diseases, an aging population, and an increasing demand for therapies that improve survival and quality of life for both HFrEF and HFpEF patients are driving the need for advanced pharmacological solutions. Hospital pharmacies remain the primary distribution channel, while specialty cardiac clinics are emerging as critical points of care for therapy initiation and titration.

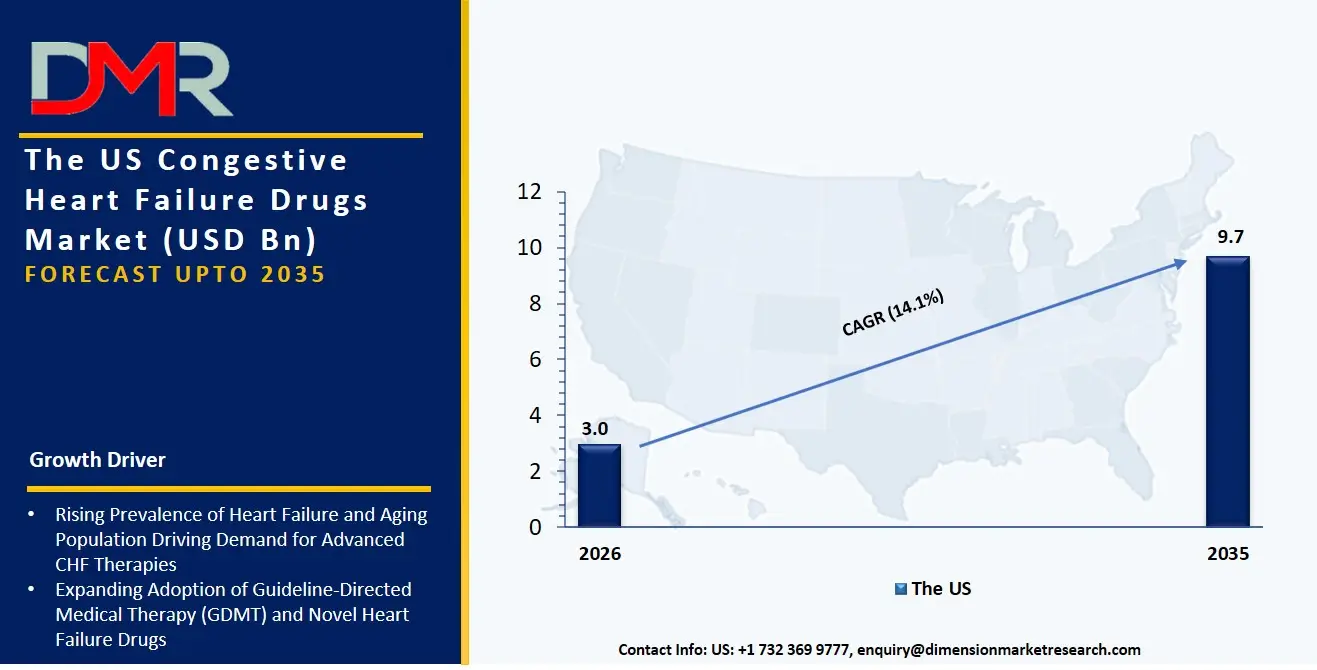

The US Congestive Heart Failure Drugs Market

The US Congestive Heart Failure Drugs Market is projected to reach USD 3.0 billion in 2026 at a compound annual growth rate of 14.1% over its forecast period, culminating in a value of USD 9.7 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US remains the largest and most sophisticated market for CHF drugs, driven by a high burden of heart failure, favorable reimbursement frameworks for novel branded therapies, and the aggressive adoption of updated clinical guidelines by cardiologists. The market has been typified by rapid uptake of SGLT2 Inhibitors and ARNIs, with organizations focused on transitioning patients from older generic regimens to these higher-efficacy, patented therapies. Besides, the implementation of pharmacogenomic tools in clinical workflows is producing a similar need for targeted therapies, underpinning a new era of precision medicine within heart failure management.

The Europe Congestive Heart Failure Drugs Market

The Europe Congestive Heart Failure Drugs Market is estimated to be valued at USD 2.7 billion in 2026 and is further anticipated to reach USD 9.0 billion by 2035 at a CAGR of 14.3%. The regulatory frameworks, including stringent health technology assessments (HTAs) by bodies like NICE and HAS, have a significant impact on the European market and drive the need for robust cost-effectiveness data for premium-priced ARNIs and sGC Stimulators. Accelerated uptake of SGLT2 Inhibitors is also being experienced in the region as healthcare systems in Germany and France seek to reduce hospitalizations for HFpEF, a patient segment with historically limited treatment options. In addition, national heart failure registries are challenging pharmaceutical companies to deliver comprehensive real-world evidence on long-term safety and efficacy across diverse European populations.

The Japan Congestive Heart Failure Drugs Market

The Japan Congestive Heart Failure Drugs Market is projected to be valued at USD 548.3 million at a CAGR of 13.7%. The Japanese market is unique, with a national healthcare policy driving early treatment intervention in response to a super-aging society and a soaring prevalence of hypertension-related heart failure with preserved ejection fraction (HFpEF). SGLT2 Inhibitors and ARBs make up a large part of the prescription volume as cardiologists manage a delicate balance of cardio-renal protection in elderly patients with multiple comorbidities. There is also a strong need for deep market localization to bridge the gap between globally developed clinical trial data and the specific genetic and dietary profiles of Japanese patients, forming a niche in post-marketing surveillance and outcomes research.

Key Takeaways

- Market Size & Forecast: The Global Congestive Heart Failure Drugs market is projected to reach USD 9.2 billion in 2026, expanding dramatically to USD 32.6 billion by 2035, fueled by the dual drivers of an aging global demographic and the clinical imperative to implement lifesaving quadruple therapy at scale.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 15.0%, driven by a critical expansion of treatment guidelines to include SGLT2 inhibitors for HFpEF and the escalating need for therapies that reduce both cardiovascular mortality and recurrent hospitalization.

- Primary Growth Drivers: Key forces include the widespread pharmacological shift from symptomatic management (diuretics) to disease-modifying therapy (ARNIs, SGLT2 inhibitors), the need for combination polypill strategies to avoid therapeutic inertia, and the integration of NT-proBNP biomarkers driving earlier diagnosis and treatment initiation.

- Key Market Trends: Major trends include the rise of cardio-renal-metabolic disease management as a unified treatment paradigm, the use of AI-powered tools within clinical trials to identify responder phenotypes for novel sGC Stimulators, and the shift toward value-based contracting as payers prioritize demonstrable reductions in hospitalizations.

- By Drug Class Analysis: ARNIs and SGLT2 Inhibitors are expected to dominate market value growth due to strong evidence of mortality benefit. Their use is increasingly required to build a foundational GDMT backbone that redefines heart failure as a manageable chronic condition rather than a terminal one.

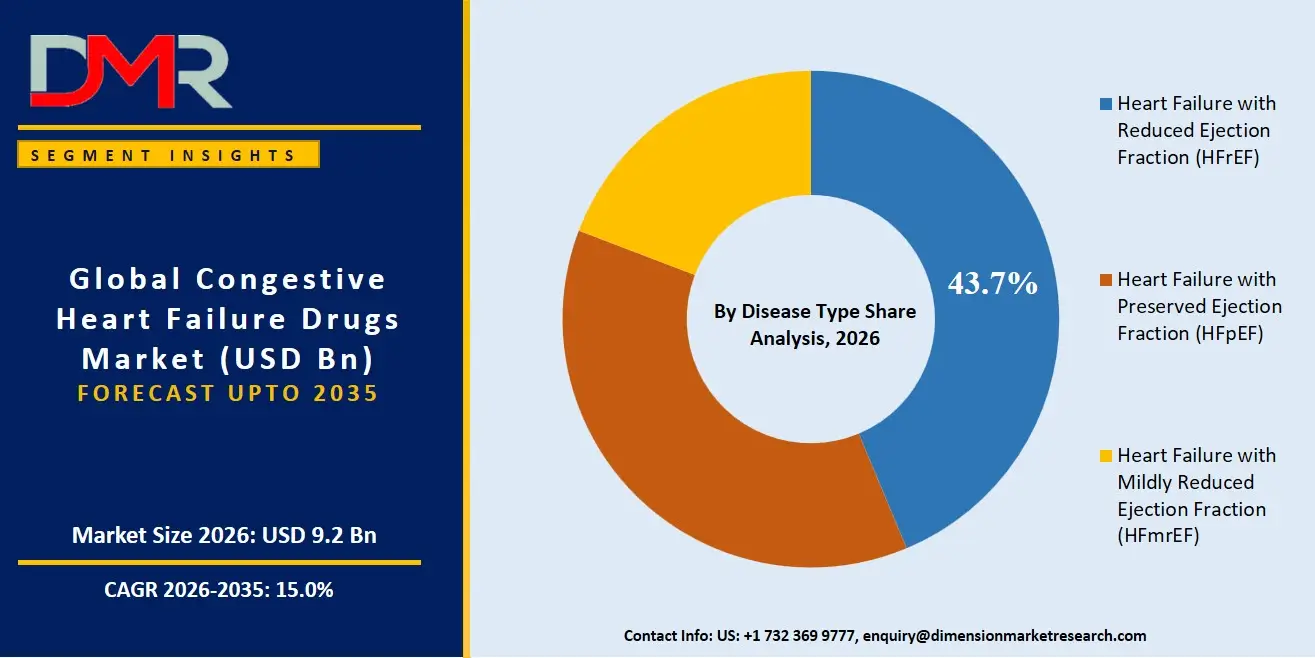

- By Disease Type Analysis: HFrEF historically commands the largest market share due to a well-established therapeutic arsenal. However, HFpEF is the fastest-growing segment as SGLT2 inhibitors and novel mineralocorticoid receptor antagonists provide the first clear pharmacologic strategies for this under-served population.

- Regional Leadership: North America is poised to dominate this market with 38.3% of the market share in 2026 due to its conducive regulatory environment for novel drug approvals and a healthcare infrastructure that rapidly operationalizes clinical trial findings into routine practice.

What is the Congestive Heart Failure Drugs?

Congestive Heart Failure Drugs are the specialized pharmacological agents prescribed to combat the complex neurohormonal cascade and hemodynamic overload that characterize a failing heart. These drugs, unlike mechanical devices or surgical interventions, are the frontline defense for chronic management. This involves ACE Inhibitors, ARBs, and ARNIs to counteract maladaptive vasoconstriction, Beta Blockers and If Channel Inhibitors to control heart rate and myocardial oxygen demand, and Mineralocorticoid Receptor Antagonists (MRAs) and Diuretics to manage fluid volume overload. With 64 million people affected by heart failure globally, these drug classes are needed to achieve guideline-directed targets, maintain euvolemia, and improve functional capacity, making pharmacotherapy the cornerstone of transforming a high-mortality condition into a chronically manageable disease.

Use Cases

- Quadruple Therapy Initiation in HFrEF: Cardiologists employ an aggressive combination of an ARNI, a Beta Blocker, an MRA, and an SGLT2 Inhibitor rapidly after a new heart failure diagnosis, titrating doses over weeks to achieve the target regimen that maximally reduces the risk of sudden cardiac death.

- Decongestion in Acute Decompensated Heart Failure: Hospitalists use intravenous Loop Diuretics as first-line agents to achieve rapid decongestion in patients with acute fluid overload, with subsequent transition to oral combination diuretic therapy for maintenance.

- Managing HFpEF with Co-morbid Diabetes: Primary care physicians and endocrinologists initiate SGLT2 Inhibitors for patients with preserved ejection fraction and diabetes, leveraging the drug's dual mechanism to control glycemic status and reduce heart failure hospitalization risk.

- Advanced Therapy for Worsening Chronic Heart Failure: Specialty heart failure clinics prescribe oral sGC Stimulators in combination with standard GDMT for high-risk patients with recent hospitalizations, aiming to improve outcomes through a novel nitric oxide pathway.

How AI is Transforming the Congestive Heart Failure Drugs Market?

AI is changing the congestive heart failure drugs landscape by accelerating the discovery of novel therapeutic targets and de-risking clinical trials. In drug development, AI-based molecular simulation tools have the potential to automatically screen billions of compounds against neurohormonal targets like the angiotensin receptor or neprilysin enzyme, greatly minimizing the preclinical timeline and identifying candidates with superior binding affinity. Meanwhile, AI-powered imaging analysis allows for the deep phenotyping of HFpEF patients, enabling sponsors to enrich trial populations with the specific cardiac and metabolic profiles most likely to respond to experimental sGC Stimulators or MRAs.

Clinical practice and market access are also revolving around AI. In the area of real-world evidence generation, intelligent analytics platforms are used to continuously mine electronic health records to identify optimal titration sequences for ARNIs and forecast patient adherence to life-long beta blocker therapy, keeping health systems aligned with quality metrics. Moreover, generative AI models are complementing physician decision-making by simulating patient-specific hemodynamic responses to a combination of Vasodilators and Diuretics, giving clinicians a visualization of therapeutic effect before committing to a complex polypharmacy regimen.

Market Dynamics

Key Drivers in the Global Congestive Heart Failure Drugs Market

Rising Global Burden of Heart Failure and Aging Population

The increasing prevalence of congestive heart failure, driven by aging populations, hypertension, diabetes, obesity, and coronary artery disease, is a major growth driver for the market. Older adults are particularly susceptible to heart failure, leading to rising demand for long-term pharmacological management. Improved diagnostic capabilities and greater disease awareness enable earlier diagnosis and treatment initiation. Governments and healthcare organizations are investing in cardiovascular disease prevention and management programs, further supporting prescription volumes. As life expectancy continues to rise worldwide, the number of patients requiring chronic heart failure medications is expected to increase substantially, fueling sustained market expansion.

Growing Adoption of Guideline-Directed Medical Therapy (GDMT)

The widespread adoption of guideline-directed medical therapy has significantly transformed congestive heart failure treatment. Clinical guidelines now recommend combination therapy involving SGLT2 inhibitors, ARNIs, beta blockers, and mineralocorticoid receptor antagonists to improve survival and reduce hospitalizations. Continuous publication of positive clinical trial results has strengthened physician confidence in these therapies. Expanding reimbursement coverage, increasing availability of innovative drugs, and improved physician education have accelerated treatment uptake across developed and emerging markets. The shift toward evidence-based, multidrug treatment strategies continues to increase prescription rates and improve long-term patient outcomes, supporting robust growth of the global market.

Restraints in the Global Congestive Heart Failure Drugs Market

High Cost of Innovative Heart Failure Therapies

Although advanced heart failure therapies offer superior clinical outcomes, their relatively high prices remain a significant market restraint. Newer drug classes such as ARNIs and SGLT2 inhibitors often impose higher treatment costs than conventional therapies, limiting affordability in low- and middle-income countries. Inadequate insurance coverage and reimbursement restrictions can further reduce patient access. Many patients require lifelong multidrug therapy, increasing overall healthcare expenditure. These financial barriers may delay treatment initiation or reduce adherence, particularly in resource-constrained healthcare systems, ultimately limiting the widespread adoption of premium heart failure medications.

Medication Adherence Challenges in Chronic Disease Management

Congestive heart failure requires lifelong treatment involving multiple medications with different dosing schedules, creating challenges for patient adherence. Elderly patients often experience polypharmacy because of multiple chronic conditions, increasing the risk of missed doses and treatment discontinuation. Adverse drug effects, complex medication regimens, and limited patient education further contribute to poor compliance. Reduced adherence can lead to disease progression, recurrent hospitalizations, and increased healthcare costs. Despite improvements in treatment guidelines, maintaining consistent long-term medication use remains a significant challenge that can limit therapeutic effectiveness and market growth.

Growth Opportunities in the Global Congestive Heart Failure Drugs Market

Expansion of Heart Failure Treatment in Emerging Markets

Emerging economies present significant opportunities for congestive heart failure drug manufacturers due to improving healthcare infrastructure and expanding access to cardiovascular care. Governments are investing in healthcare modernization, insurance coverage, and chronic disease management programs that improve patient access to advanced medications. Increasing urbanization and changing lifestyles have contributed to a growing burden of cardiovascular diseases, creating substantial unmet treatment needs. Pharmaceutical companies are expanding their regional presence through partnerships, local manufacturing, and affordable product offerings. These developments are expected to accelerate market penetration and long-term revenue growth across developing countries.

Development of Precision Medicine and Combination Therapies

Advancements in precision medicine are creating new opportunities for personalized heart failure treatment. Biomarker-based patient stratification, genetic research, and digital health technologies enable physicians to tailor therapies according to disease characteristics and patient risk profiles. Pharmaceutical companies are also developing novel fixed-dose combination therapies that improve medication adherence and simplify treatment regimens. Continued investment in clinical research is expanding therapeutic options for heart failure with preserved and mildly reduced ejection fraction, addressing previously underserved patient populations. These innovations are expected to broaden treatment possibilities and stimulate future market expansion.

Trends in the Global Congestive Heart Failure Drugs Market

Rapid Shift Toward SGLT2 Inhibitor-Based Treatment Strategies

SGLT2 inhibitors have rapidly become one of the most important therapeutic classes in heart failure management following strong evidence demonstrating reductions in cardiovascular mortality and hospitalization. Their clinical benefits extend beyond diabetic patients, resulting in broader prescribing across multiple heart failure populations. Healthcare providers increasingly incorporate these medicines into first-line treatment strategies alongside established therapies. Pharmaceutical companies continue expanding clinical indications and conducting additional research to strengthen their market position. This shift toward SGLT2 inhibitor-centered treatment protocols is reshaping prescribing patterns and influencing future product development across the global market.

Increasing Integration of Digital Health in Heart Failure Management

Digital health technologies are increasingly supporting congestive heart failure treatment through remote patient monitoring, connected medical devices, wearable sensors, and telemedicine platforms. These technologies enable continuous monitoring of patient health, allowing earlier detection of disease worsening and timely medication adjustments. Improved patient engagement and adherence through digital applications contribute to better clinical outcomes while reducing hospital readmissions. Healthcare providers are increasingly integrating digital monitoring with pharmacological therapy as part of comprehensive heart failure management programs. This trend is enhancing treatment efficiency and creating opportunities for value-based cardiovascular care worldwide.

Research Scope and Analysis

The Global Congestive Heart Failure Drugs Market is segmented by Drug Class, Disease Type, Route of Administration, Distribution Channel, and End User. Drug class leads the analysis with therapies including SGLT2 inhibitors, ARNIs, beta blockers, and ACE inhibitors, while disease-specific treatment approaches, oral formulations, hospital pharmacies, and hospitals collectively define market demand and therapeutic adoption worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Drug Class Analysis

SGLT2 inhibitors is projected to dominate the global congestive heart failure drugs market due to their transformative clinical benefits across a broad spectrum of heart failure patients. Originally developed for diabetes management, these drugs have demonstrated significant reductions in cardiovascular death, hospitalization, and disease progression in both diabetic and non-diabetic patients. Their inclusion as first-line guideline-directed medical therapy (GDMT) by leading cardiovascular societies has accelerated physician adoption worldwide. Strong clinical evidence from large-scale trials, expanding regulatory approvals, and increasing reimbursement support have further strengthened market leadership. Growing awareness of their renal protective effects and favorable long-term outcomes continues to drive demand, making SGLT2 inhibitors the fastest-growing and largest revenue-generating drug class.

By Disease Type Analysis

Heart Failure with Reduced Ejection Fraction (HFrEF) is anticipated to represent the dominant disease segment because it has the most established treatment guidelines and the widest availability of evidence-based pharmacological therapies. Patients with HFrEF benefit from multiple approved drug classes, including ARNIs, beta blockers, MRAs, ACE inhibitors, and SGLT2 inhibitors, resulting in higher prescription volumes than other heart failure types. Extensive clinical research, standardized diagnosis, and continuous monitoring have encouraged earlier intervention and combination therapy. Higher hospitalization rates and disease burden further increase medication utilization. Ongoing improvements in survival rates through comprehensive drug therapy continue to reinforce HFrEF as the largest contributor to the congestive heart failure drugs market.

By Route of Administration Analysis

The oral route is projected to dominate the congestive heart failure drugs market because most long-term heart failure therapies are formulated as tablets or capsules for daily administration. Oral medications provide superior convenience, improved patient compliance, and lower healthcare costs compared to injectable therapies. Widely prescribed drug classes, including SGLT2 inhibitors, beta blockers, ACE inhibitors, ARBs, MRAs, and ARNIs, are primarily available in oral formulations, supporting chronic disease management outside hospital settings. Increasing preference for home-based treatment and outpatient care further boosts oral drug utilization. Continuous development of fixed-dose combinations and once-daily formulations also enhances adherence, making oral administration the preferred and largest route globally.

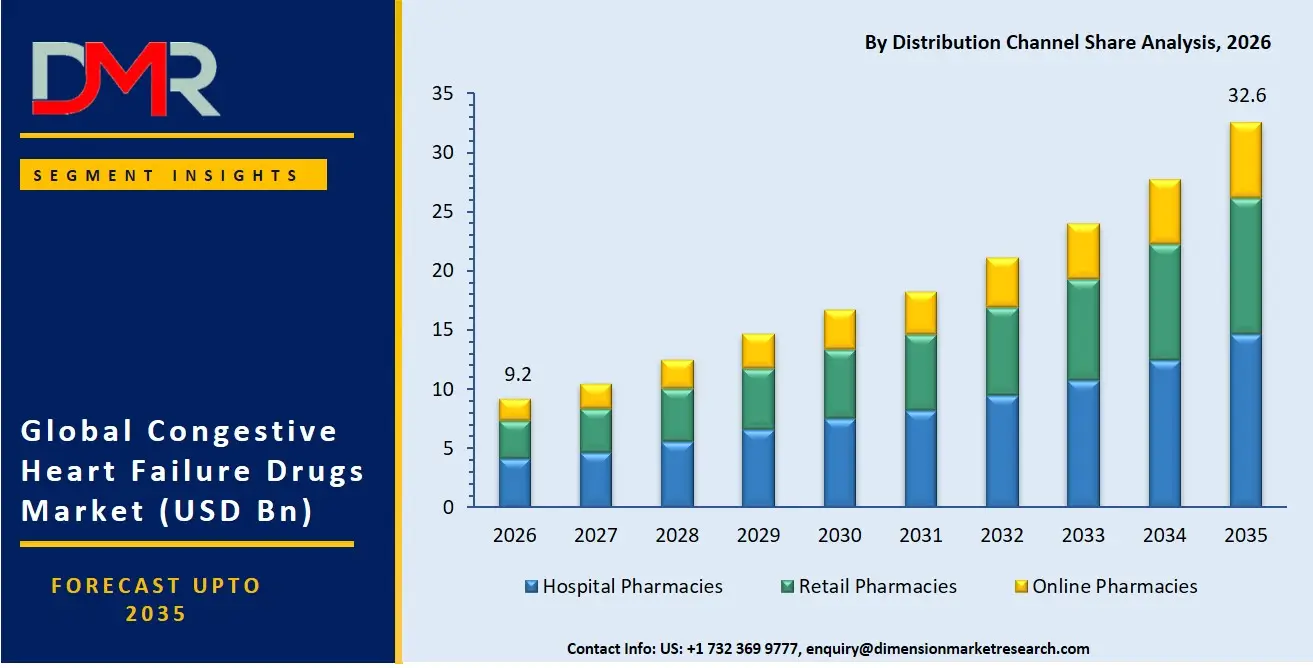

By Distribution Channel Analysis

Hospital pharmacies is anticipated to dominate the distribution channel segment because congestive heart failure patients frequently require hospitalization for diagnosis, acute exacerbations, medication optimization, and ongoing cardiovascular management. Hospitals serve as the primary point for initiating advanced therapies, adjusting dosages, and monitoring treatment response under specialist supervision.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Newly approved heart failure medications are often introduced through hospital settings before transitioning to community care. Strong procurement systems, availability of multidisciplinary cardiac teams, and high patient inflow further strengthen hospital pharmacy sales. Increasing admissions related to aging populations and cardiovascular diseases continue to support the leadership of hospital pharmacies in global heart failure drug distribution.

By End User Analysis

Hospitals is poised to dominate the end-user segment because they remain the primary healthcare setting for diagnosing, treating, and managing congestive heart failure across all disease stages. Patients experiencing acute decompensated heart failure often require emergency care, intensive monitoring, and specialist cardiology services available only in hospitals. These facilities also manage complex cases requiring combination drug therapy, intravenous medications, and continuous clinical assessment. The presence of experienced cardiologists, advanced diagnostic infrastructure, and comprehensive treatment protocols contributes to higher prescription volumes. Growing hospitalization rates among elderly patients and increasing adoption of guideline-directed medical therapy continue to position hospitals as the leading end users in this market.

The Global Congestive Heart Failure Drugs Market Report is segmented on the basis of the following:

By Drug Class

- ACE Inhibitors

- Angiotensin II Receptor Blockers (ARBs)

- Angiotensin Receptor-Neprilysin Inhibitors (ARNIs)

- Beta Blockers

- Mineralocorticoid Receptor Antagonists (MRAs)

- Sodium-Glucose Cotransporter-2 (SGLT2) Inhibitors

- Diuretics

- Loop Diuretics

- Thiazide Diuretics

- Potassium-Sparing Diuretics

- Cardiac Glycosides

- Soluble Guanylate Cyclase (sGC) Stimulators

- Vasodilators

- If Channel Inhibitors

- Others

By Disease Type

- Heart Failure with Reduced Ejection Fraction (HFrEF)

- Heart Failure with Preserved Ejection Fraction (HFpEF)

- Heart Failure with Mildly Reduced Ejection Fraction (HFmrEF)

By Route of Administration

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By End User

- Hospitals

- Specialty Cardiac Clinics

- Ambulatory Surgical Centers (ASCs)

- Home Healthcare Settings

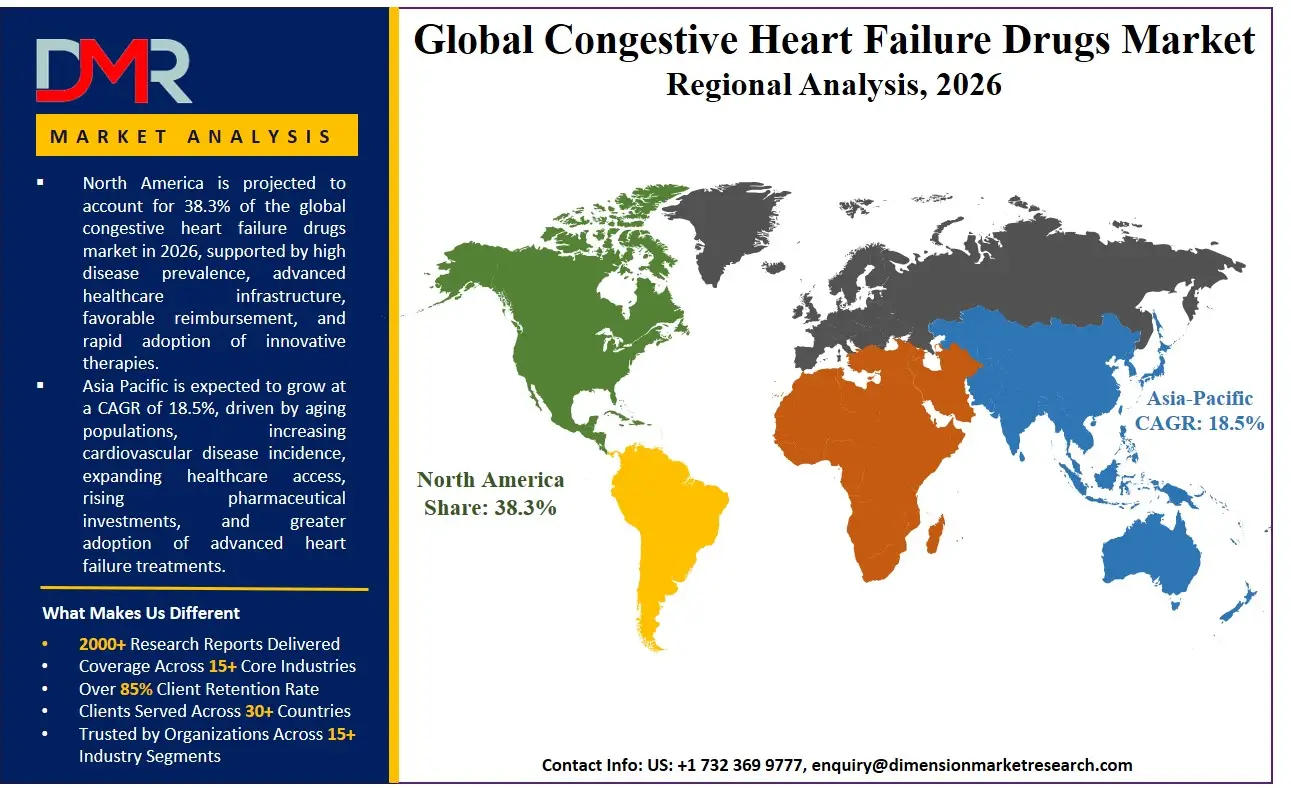

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

North America is poised to dominate the global CHF drugs market as it is projected to hold 38.3% of the market share by the end of 2026. The United States, which dominates North America, has the highest share due to the unmatched concentration of a cardiology specialty ecosystem that rapidly translates landmark clinical trials into practice. The region benefits from premium pricing of patented ARNIs and SGLT2 inhibitors without direct price controls at launch, an aggressive medical education environment, and a high prevalence of heart failure risk factors like obesity and diabetes. Enterprise-level investment in cardio-renal clinical trials and the broad adoption of quadruple therapy in both academic and community settings contribute to the continued demand for high-cost, disease-modifying agents. Moreover, a favorable venture capital climate persistently finances novel biotechs developing next-generation sGC stimulators and gene therapies, ensuring a robust pipeline of premium-priced innovations.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding CHF drugs market, driven by the staggering rise in hypertension and diabetes, which is fueling a cardiovascular disease epidemic across India, China, and Southeast Asia. The fast-paced epidemiological transition and urbanization are compelling governments and hospital networks to adopt global GDMT standards to combat rising premature mortality. Market access consulting and physician education are in high demand to help these large health systems transition from older, generic monotherapies to branded ARNI and SGLT2 Inhibitor combination approaches. There is also a severe lack of specialized heart failure clinics in the region, necessitating innovative distribution models through hospital and retail pharmacies to bridge the rural-urban healthcare gap and enable faster patient access to novel therapies.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the global CHF drugs market is defined by fierce innovation among pharmaceutical giants racing to establish new standards in cardio-renal-metabolic care. Dominant players like Novartis, AstraZeneca, Boehringer Ingelheim, and Bayer leverage deep cardiology franchises, with success hinging on lifecycle management and expanding indications for blockbuster ARNIs and SGLT2 inhibitors into HFpEF and chronic kidney disease. The movement toward market consolidation is progressing as large-cap pharma acquires biotechs with novel mechanisms like sGC stimulation and myosin activation. Proprietary fixed-dose combinations and companion digital adherence platforms are becoming critical differentiators rather than just molecular novelty alone. Patent cliffs for foundational therapies are simultaneously intensifying generic pressure, forcing innovators to pivot toward next-generation precision targets.

Some of the prominent players in the Global Congestive Heart Failure Drugs Market are:

- Novartis AG

- AstraZeneca PLC

- Bayer AG

- Boehringer Ingelheim International GmbH

- Eli Lilly and Company

- Merck & Co., Inc.

- Pfizer Inc.

- Bristol Myers Squibb

- Johnson & Johnson (Janssen Pharmaceuticals)

- Amgen Inc.

- Abbott Laboratories

- Sanofi S.A.

- Otsuka Pharmaceutical Co., Ltd.

- Daiichi Sankyo Company, Limited

- Viatris Inc.

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Lupin Limited

- Zydus Lifesciences Limited

- Other Key Players

Recent Developments

- In June 2026, AstraZeneca PLC announced positive Phase III trial results demonstrating that dapagliflozin significantly reduced the risk of recurrent heart failure hospitalization and cardiovascular death in patients with chronic heart failure, supporting expanded clinical adoption.

- In April 2026, Novartis AG received regulatory approval in multiple international markets for an expanded indication of sacubitril/valsartan, allowing its use across a broader spectrum of chronic heart failure patients based on updated clinical evidence.

- In February 2026, Bayer AG initiated a global Phase III clinical study evaluating a next-generation cardiovascular therapy designed to improve outcomes in patients with heart failure and chronic kidney disease.

- In January 2026, Boehringer Ingelheim International GmbH expanded its strategic collaboration with Eli Lilly and Company to support additional clinical research evaluating empagliflozin across multiple heart failure populations, including earlier-stage disease.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 9.2 Bn |

| Forecast Value (2035) |

USD 32.6 Bn |

| CAGR (2026–2035) |

15.0% |

| The US Market Size (2026) |

USD 3.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Drug Class, By Disease Type, By Route of Administration, By Distribution Channel, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Congestive Heart Failure Drugs Market?

▾ The Global Congestive Heart Failure Drugs Market is poised to be valued at USD 9.2 billion in 2026 and is projected to reach USD 32.6 billion by 2035, driven by the universal adoption of guideline-directed medical therapy and the launch of novel drug classes for previously untreatable heart failure phenotypes.

What is the CAGR of the Congestive Heart Failure Drugs Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 15.0% from 2026 to 2035, reflecting the expanding therapeutic indications for SGLT2 inhibitors and ARNIs, and the persistent clinical need to reduce heart failure hospitalizations and cardiovascular mortality globally.

What factors are driving the growth of the Congestive Heart Failure Drugs Market?

▾ Key drivers include the aging global population with rising cardiovascular comorbidities, the paradigm shift to quadruple therapy for HFrEF, the landmark expansion of SGLT2 inhibitors into the previously untreatable HFpEF population, and the clinical imperative to overcome therapeutic inertia through novel fixed-dose combinations.

What are the major trends in the Congestive Heart Failure Drugs Market?

▾ Major trends include the convergence of cardio-renal-metabolic drug management, the integration of digital therapeutics to boost pharmaco-adherence, the rise of fixed-dose polypill combinations to simplify complex regimens, and the use of AI-driven real-world evidence to support value-based contracting and payer negotiations.

Which region held the largest share of the Congestive Heart Failure Drugs Market in 2026?

▾ North America is poised to hold a 38.3% market share in 2026, driven by rapid clinical guideline implementation, a favorable pricing environment for novel patented drugs, and aggressive adoption of ARNIs and SGLT2 inhibitors within both hospital and specialty cardiology settings.

Which region is expected to grow the fastest in the Congestive Heart Failure Drugs Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by the escalating prevalence of hypertension and diabetes in India, China, and Southeast Asia, where improving diagnosis rates and expanding healthcare access are critical for transitioning patients from older generic therapies to modern disease-modifying drug classes.

Who are the key players in the Congestive Heart Failure Drugs Market?

▾ Key players include Novartis (Entresto), AstraZeneca (Farxiga), Boehringer Ingelheim/Lilly (Jardiance), Bayer (Verquvo), Merck, Pfizer, and Cytokinetics, alongside generic manufacturers and emerging biotechs focused on next-generation myosin activators and novel sGC stimulators.

How is the Congestive Heart Failure Drugs Market segmented?

▾ The market is segmented by Drug Class, Disease Type, Route of Administration, Distribution Channel, and End User.