Market Overview

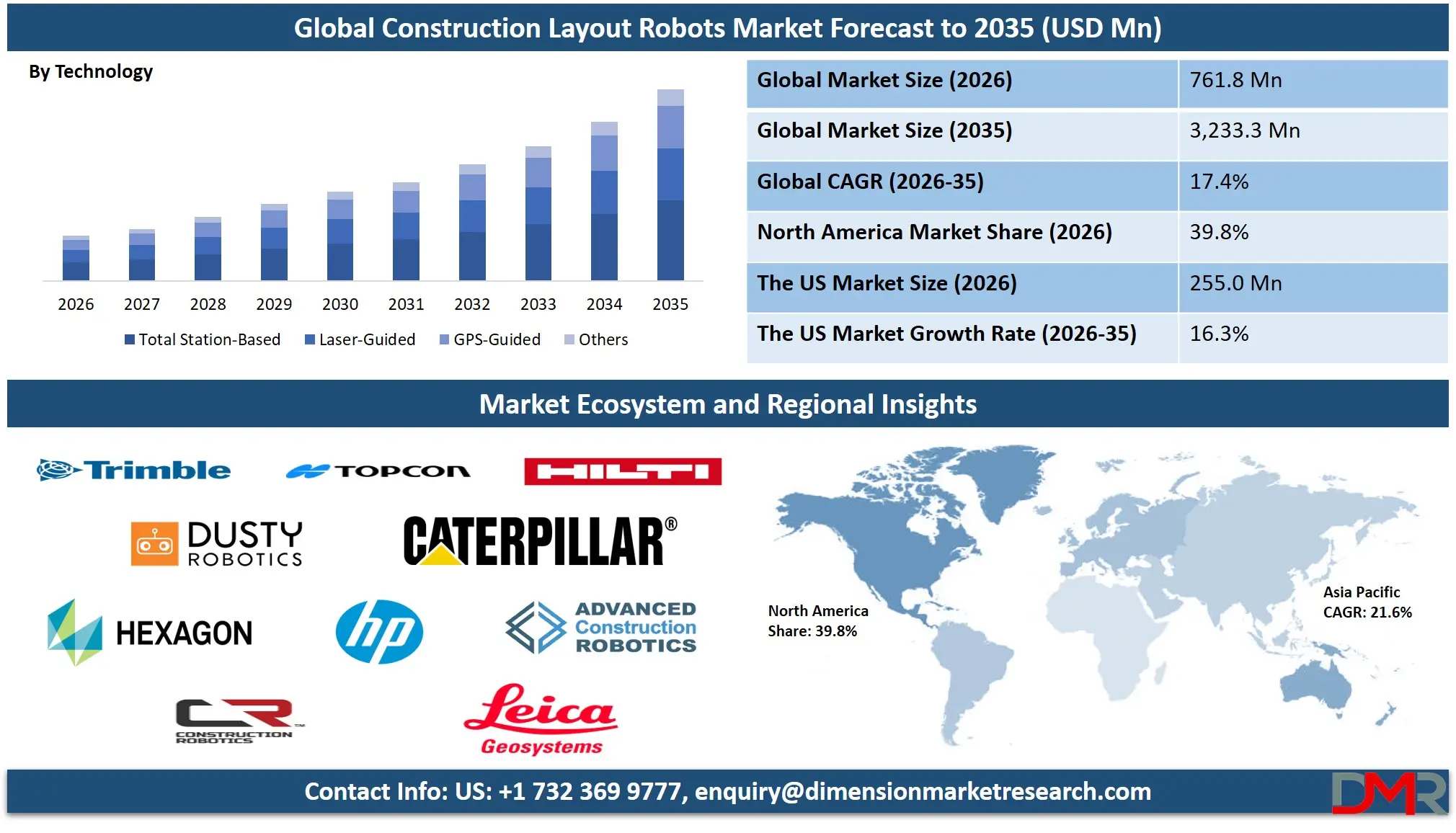

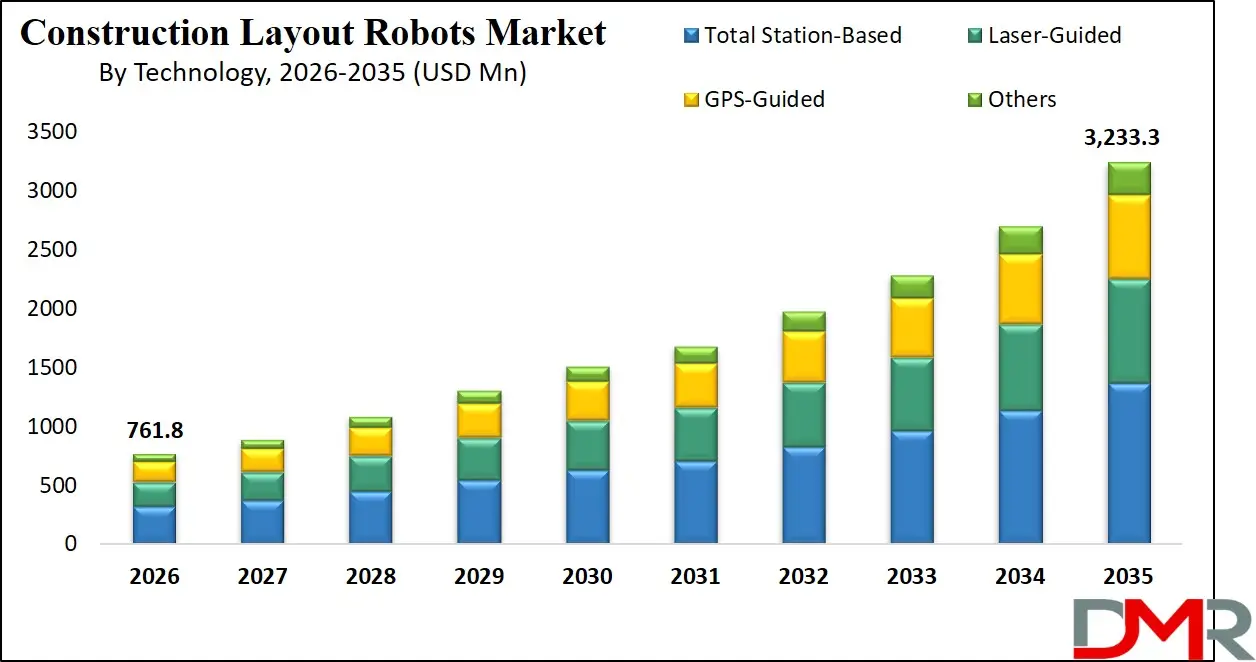

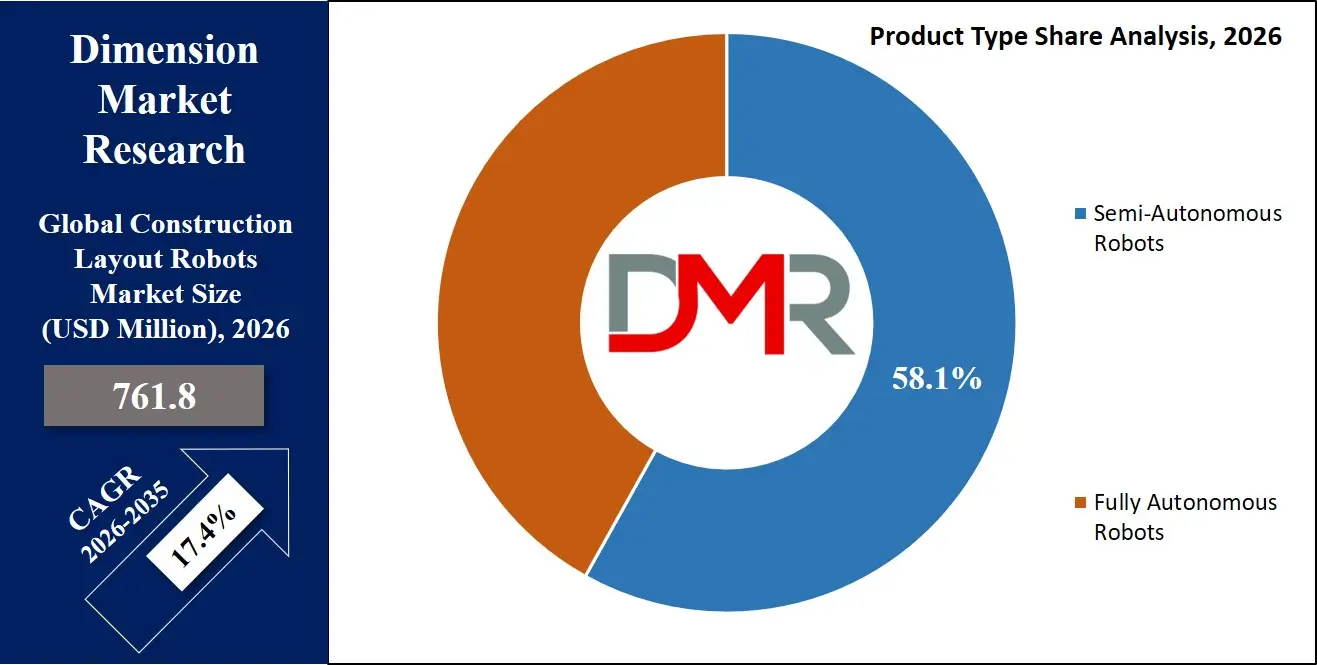

The Global Construction Layout Robots Market is projected to reach USD 761.8 million in 2026 and grow at a compound annual growth rate of 17.4% from there until 2035 to reach a value of USD 3,233.3 million.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

A construction layout robot serves as a precision positioning and marking system within modern construction sites. It facilitates the accurate translation of digital building information modeling (BIM) data into physical layout points on floors, walls, and ceilings by automating the measurement and marking process. This enables real-time quality control, reduced rework, and enhanced labor productivity, improving project schedule certainty and profitability. By eliminating manual tape measurement and chalk line methods, construction layout robots are foundational to the transition toward fully digital, data-driven, and automated construction workflows.

The global construction layout robots market encompasses the worldwide industry providing hardware, software, and services that enable automated positioning, layout marking, and quality verification across commercial, residential, industrial, and infrastructure projects. This market includes a range of providers from specialized construction robotics startups to established surveying instrument manufacturers and diversified automation solution vendors. Growth is fueled by global investments in construction productivity enhancement, the persistent shortage of skilled labor, and increasing project complexity demanding millimeter-level accuracy. The expansion of prefabrication and modular construction techniques further propels demand for precise digital-to-physical layout solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market is also being shaped by technological advancements in robotic navigation, sensor fusion, and cloud connectivity. Modern layout robots are evolving into autonomous field-to-BIM feedback systems capable of real-time as-built verification and deviation reporting. Simultaneously, the increasing focus on construction safety and quality assurance is driving the adoption of robotic systems that remove workers from hazardous marking tasks, positioning them as essential components for both operational excellence and modern construction site management.

The US Construction Layout Robots Market

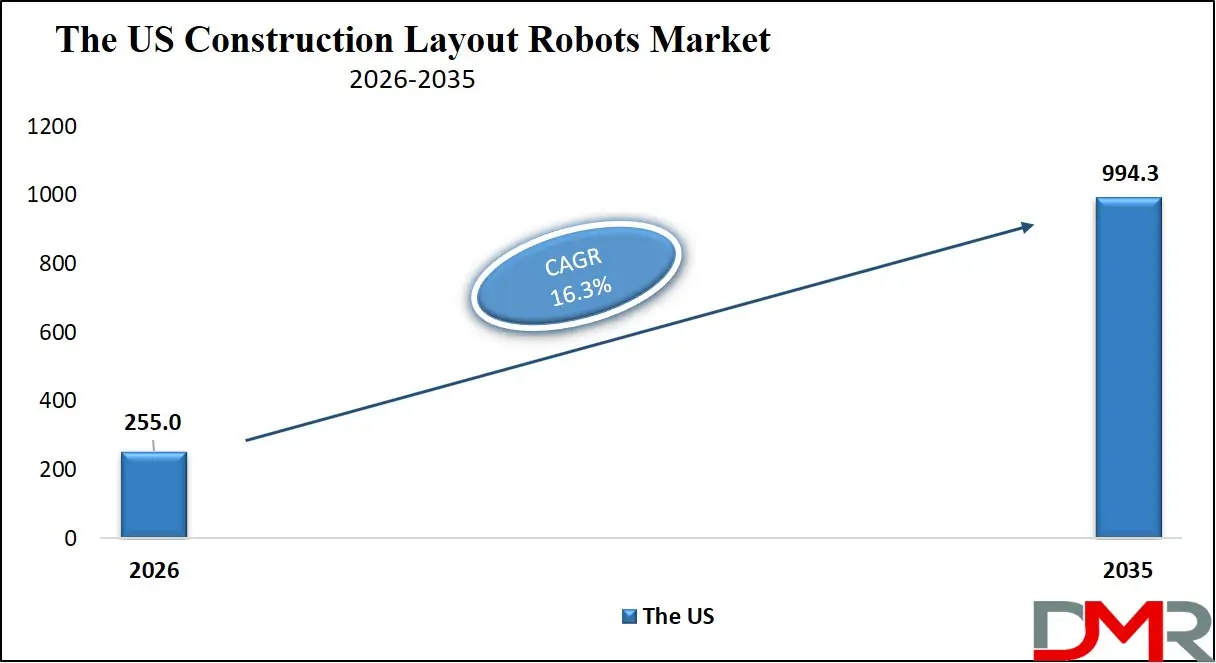

The US Construction Layout Robots Market is projected to reach USD 255.0 million in 2026 and grow at a CAGR of 16.3%, reaching USD 994.3 million by 2035. The U.S. leads global adoption due to its mature commercial construction sector, an acute and worsening skilled labor shortage with over 400,000 unfilled craft positions nationally, and intensifying owner demand for schedule certainty, rework reduction, and verifiable quality documentation.

The pressing need to maximize field productivity in critical building segments like large-scale commercial office towers, complex healthcare facilities, hyperscale data centers, and advanced manufacturing plants fuels demand for robotic layout solutions. Major general contractors including Turner Construction, DPR Construction, Clark Group, and Swinerton are integrating semi-autonomous robotic total stations and fully autonomous layout printers into standard project workflows. Concrete subcontractors and MEP trades have emerged as particularly enthusiastic adopters, using robotic systems to place embeds, set anchor bolts, and mark overhead MEP rough-in points with millimeter precision.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. federal infrastructure investment under the Infrastructure Investment and Jobs Act, which allocates billions for transportation, water, and energy projects, is expanding adoption into the civil construction segment. Equipment rental giants including United Rentals and Sunbelt Rentals have significantly expanded their layout robot fleets, offering daily, weekly, and monthly rental options that lower adoption barriers for small to mid-sized contractors. Training partnerships between equipment manufacturers, rental houses, and community colleges are emerging to develop operator expertise and address the industry's fear of technological obsolescence. The rapid maturation of robotics-as-service commercial models and cloud-based layout data management platforms continues to redefine the U.S. construction technology landscape, positioning the country as the global epicenter of construction robotics adoption and innovation.

The Europe Construction Layout Robots Market

The Europe Construction Layout Robots Market is estimated to be valued at USD 182.8 million in 2026 and is further anticipated to reach USD 783.7 million by 2035 at a CAGR of 17.9%. Europe's leadership is supported by the region's leadership in digital construction adoption, ambitious productivity improvement targets, and stringent building quality and sustainability regulations. Countries such as Germany, the UK, France, and the Nordic nations are at the forefront of construction robotics deployment, driven by high labor costs, advanced BIM mandates, and strong government support for construction technology innovation.

Countries including Germany, the United Kingdom, France, the Nordic nations, and Italy are at the forefront of layout robot deployment. Germany's Mittelstand of specialized engineering and construction firms is actively developing and deploying robotic total station solutions integrated with proprietary BIM workflows. The United Kingdom's BIM mandate for all government-funded projects has created a fertile environment for digital-to-field technologies. Nordic contractors, facing extreme labor costs and short construction seasons, have embraced autonomous layout systems to maximize productivity during limited weather windows.

Funding through Horizon Europe and national digital construction programs supports research and development in autonomous navigation, sensor fusion for harsh job site conditions, and interoperability between layout robots and emerging digital twin platforms. European contractors are increasingly specifying robotic layout as a standard requirement on large commercial and infrastructure tenders. The retrofit of existing contractor workflows with robotic layout solutions represents a significant and growing market segment. With strong technical standards, emphasis on circular economy principles in building lifecycle management, and contractor desperation for labor productivity solutions, Europe remains one of the most advanced and fastest-growing regions for construction layout robot penetration.

The Japan Construction Layout Robots Market

The Japan Construction Layout Robots Market is projected to be valued at USD 45.7 million in 2026. It is further expected to witness subsequent growth in the upcoming period, holding USD 212.0 million in 2035 at a CAGR of 18.4%.

Japan's construction market faces an existential demographic crisis, with the construction workforce having declined by approximately 30% since 2000 and projections indicating an additional 20% reduction by 2040. This severe and accelerating labor shortage, combined with Japan's cultural emphasis on exceptional construction quality and precision, creates uniquely compelling drivers for layout robot adoption.

The Ministry of Land, Infrastructure, Transport and Tourism actively champions construction robotics through its i-Construction initiative, which provides subsidies for small and medium-sized contractors adopting automated layout and surveying technologies. Major general contractors including Obayashi Corporation, Shimizu Corporation, Kajima Corporation, and Takenaka Corporation are investing heavily in developing and deploying robotic layout systems tailored to the unique constraints of dense Japanese urban construction sites, where space is limited and precision is paramount.

Japan's leadership in robotics, precision sensors, and compact automation accelerates domestic innovation in miniaturized, highly accurate layout robots suitable for tight floor plates and restricted site access. The government's Society 5.0 strategic framework, which envisions the seamless integration of cyber and physical systems, directly supports the convergence of BIM, IoT sensors, and construction robotics. Layout robots are increasingly deployed in high-rise residential towers, semiconductor fabrication facilities requiring vibration-sensitive precision, and regional infrastructure rehabilitation projects. Japan's zero-defect construction culture and willingness to invest in automation solutions with clear long-term paybacks position the country as a high-growth innovation hub for construction layout robotics, with numerous domestic startups receiving substantial corporate and venture investment.

Global Construction Layout Robots Market: Key Takeaways

- Robust Global Market Growth Driven by Labor Crisis: The Global Construction Layout Robots Market is expected to be valued at USD 761.8 million in 2026 and is projected to reach USD 3,233.3 million by 2035, showcasing rapid expansion supported by the construction industry's unprecedented and worsening skilled labor shortage, particularly in layout and surveying trades where the average worker age exceeds 48 years.

- North America Maintains Regional Dominance: North America is expected to capture approximately 39.8% of global market share in 2026, anchored by acute labor shortages, early and widespread adoption by large general contractors, a sophisticated equipment rental infrastructure, and the world's highest concentration of venture capital investment in construction robotics startups.

- Asia-Pacific Delivers Decisive Growth Engine: Asia-Pacific holds the highest regional CAGR, driven by China's state-mandated construction digitalization, India's National Infrastructure Pipeline requiring productivity-enhancing technologies, and Japan's demographic emergency compelling rapid construction automation adoption across all sectors.

- Semi-Autonomous Robots Dominate, Fully Autonomous Accelerates: Semi-autonomous layout robots currently hold the largest installed base, representing 58.1% of market share in 2026, due to accessible capital requirements and intuitive operation by existing field personnel. Fully autonomous systems represent the fastest-growing product segment as large contractors seek to eliminate labor dependencies entirely on mega-projects.

- Commercial Construction Remains Anchor Application: Commercial construction maintains dominant application share, driven by demanding tolerance requirements for curtain wall and MEP systems, compressed project schedules, and the substantial rework savings achievable through digital layout workflows in office towers, healthcare facilities, and data centers.

- Rental and Subscription Models Democratize Market Access: The rapid proliferation of equipment rental partnerships and robotics-as-service commercial models is fundamentally transforming market dynamics, significantly lowering entry barriers for the vast middle market of small to mid-sized contractors and creating predictable recurring revenue streams for vendors.

Global Construction Layout Robots Market: Use Cases

- Commercial Core and Shell Layout: General contractors deploy robotic total stations and autonomous layout printers to establish column grids, wall lines, elevation benchmarks, and curtain wall embeds across large floor plates in office towers, healthcare facilities, hotels, and data centers. These systems enable simultaneous work by multiple trades with verified positional accuracy, eliminating cumulative measurement errors that cascade through subsequent construction phases and cause costly field modifications.

- MEP Rough-In Positioning: Mechanical, electrical, and plumbing subcontractors utilize laser-guided and total station-based layout robots to mark embed locations, sleeve penetrations, equipment set points, and overhead suspension points with millimeter precision. Accurate MEP layout reduces destructive conflicts between trades, minimizes costly post-pour core drilling, and accelerates rough-in cycles on fast-track commercial projects.

- Foundation and Structural Embeds Placement: Concrete contractors employ robotic total stations and autonomous marking systems to position anchor bolts, embeds, rebar supports, and foundation corners accurately before pours. Precise embed placement ensures structural integrity, enables accurate equipment installation, and eliminates expensive corrective demolition while accelerating forming and placement cycles.

- Infrastructure Linear Projects: Civil contractors leverage GPS-guided layout robots for highway alignments, bridge pier and abutment locations, airport runway markings, rail track positioning, and utility corridor installation across expansive sites. These systems eliminate survey crew bottlenecks, remove personnel from traffic hazard exposure, and maintain accuracy over mile-long linear extents without line-of-sight limitations.

- Residential Production Building: Large-scale production homebuilders and multifamily developers utilize semi-autonomous layout robots for repetitive foundation footprint layout, wall line positioning, and MEP rough-in marking across hundreds of identical units. These systems enable smaller crews to maintain aggressive production schedules while ensuring consistent quality and reducing warranty callbacks.

Global Construction Layout Robots Market: Stats & Facts

- The McKinsey Global Institute reports that global construction labor productivity has grown at less than 1% annually over the past two decades, creating an estimated USD 1.6 trillion annual productivity gap. Layout and positioning errors account for 3–5% of total project costs, representing USD 150–250 billion annually in addressable opportunity for robotic layout solutions.

- The U.S. Bureau of Labor Statistics indicates the U.S. construction industry faces over 400,000 unfilled craft positions (2025), with the average age of layout professionals exceeding 48 years. Nearly 70% of contractors report difficulty hiring qualified layout and surveying workers.

- The Associated General Contractors of America 2025 Workforce Survey states that layout robots are the most commonly adopted construction robotics solution (47%) among robotics investors. Contractors report 50–60% crew size reductions for layout tasks and 12–18 month payback periods.

- The European Construction Sector Observatory and Euroconstruct report that firms using robotic layout systems achieve 15–20% project schedule reductions and over 30% rework cost reductions, with the strongest adoption in high labor cost countries such as Switzerland, Germany, Norway, and Denmark.

- The Japan Ministry of Land, Infrastructure, Transport and Tourism notes the construction workforce declined by approximately 30% from 2000 to 2025, with a projected additional 20% decline by 2040. Robotic layout pilots under the i-Construction initiative achieved 30–40% reductions in surveying and marking labor hours.

- The China Ministry of Housing and Urban-Rural Development mandates construction digitalization under its Five-Year Plans, targeting 30% productivity improvement by 2030 and universal BIM adoption by 2027. Projects specifying robotic layout solutions in tenders increased by over 200% between 2023 and 2026.

- The International Federation of Robotics states that construction robot density is significantly lower than manufacturing, indicating substantial growth potential. Shipments of construction layout and positioning robots grew at an average rate of 28% annually from 2023 to 2026, making it the fastest-growing segment within construction robotics.

Global Construction Layout Robots Market: Market Dynamic

Driving Factors in the Global Construction Layout Robots Market

Persistent Skilled Labor Shortages Across Global Construction

The construction industry worldwide faces an unprecedented and worsening shortage of skilled craftspeople, particularly in layout and surveying trades. Experienced layout professionals require years of training to develop the precision and speed demanded by modern construction schedules. As aging baby boomer cohorts retire and younger workers gravitate toward other industries, the talent pipeline has collapsed. This structural labor deficit forces contractors to either delay projects or accept higher error rates from undertrained personnel. Layout robots offer an immediate, scalable solution by enabling one operator to perform work previously requiring two or three skilled tradespeople. The business case strengthens each year as labor costs rise and robotic solutions become more affordable and capable.

Increasing Project Complexity and Tighter Tolerances

Modern building designs feature increasingly complex geometries, tighter tolerances, and accelerated construction schedules that push manual layout methods beyond their practical limits. Curtain wall systems, prefabricated components, and advanced MEP systems require positioning accuracy measured in millimeters rather than centimeters. Manual measurement using tape measures and chalk lines introduces cumulative errors that cascade through subsequent trades, resulting in costly field modifications and schedule delays. Layout robots translate digital BIM coordinates directly to the physical job site with consistent, verifiable accuracy. As building codes tighten and owner expectations for quality rise, robotic layout transitions from competitive advantage to competitive necessity.

Restraints in the Global Construction Layout Robots Market

High Initial Capital Investment and Utilization Concerns

The upfront cost of a robotic total station or autonomous layout printer typically ranges from USD 50,000 to over USD 100,000, representing a significant capital commitment for small to mid-sized contractors. Unlike traditional layout tools with decades of amortized cost recovery, robotic systems carry concerns about technological obsolescence and utilization rates across variable project portfolios. Many contractors lack confidence that they can maintain sufficient continuous deployment to achieve attractive return on investment. This hesitation slows adoption among the vast middle market of construction firms, even as large national contractors standardize on robotic platforms. Equipment rental models and robotics-as-service offerings are emerging to address this barrier but remain less developed than in mature equipment categories.

Workflow Integration Challenges and Learning Curve Resistance

Implementing layout robots requires changes to established workflows, software integrations, and role definitions that many construction organizations resist. BIM models must be properly prepared and coordinated before robotic layout can function effectively, exposing deficiencies in digital workflows that previously remained hidden. Field personnel accustomed to traditional methods may resist adoption, viewing robots as either job threats or unnecessary complications. Successful deployment demands commitment to training, process reengineering, and often dedicated champion roles that smaller organizations struggle to resource. These cultural and operational barriers can be more difficult to overcome than the pure financial considerations of equipment acquisition.

Opportunities in the Global Construction Layout Robots Market

Integration with Broader Construction Automation Ecosystems

Layout robots represent an entry point for broader construction automation adoption, creating opportunities for vendors to expand into adjacent workflows. Once a contractor deploys robotic layout, the foundational requirements for BIM execution, field digitization, and data-driven quality control are established. This enables logical expansion into robotic total stations for verification, autonomous drones for progress tracking, and robotic equipment for material installation. Vendors that position layout robots as the first component of integrated construction automation platforms can capture significantly higher customer lifetime value through software subscriptions, additional hardware sales, and professional services.

Expansion into Renovation and Specialty Construction Segments

While new commercial construction currently dominates layout robot deployments, substantial untapped opportunities exist in renovation, restoration, and specialty construction segments. Historic preservation projects require extreme precision for replication of ornamental elements. Tenant improvement build-outs demand rapid, accurate layout within occupied spaces under compressed schedules. Theme park and exhibit construction involves complex, non-orthogonal geometries that challenge traditional methods. Vendors developing specialized workflows, compact form factors, and application-specific software tools for these adjacent segments can access high-value niches with reduced competitive intensity and premium pricing potential.

Trends in the Global Construction Layout Robots Market

Convergence of Layout and Verification Workflows

The historical separation between layout (marking where to build) and verification (confirming what was built) is rapidly dissolving. Modern layout robots increasingly incorporate as-built capture capabilities, enabling real-time quality control and immediate deviation reporting. This convergence transforms layout from a discrete pre-construction task into a continuous feedback loop throughout the construction process. Contractors gain unprecedented visibility into installation accuracy, enabling rapid correction before errors are concealed by subsequent work. This trend elevates layout robots from productivity tools to comprehensive quality management platforms with substantial risk mitigation value.

Shift Toward Autonomous Field-to-BIM Feedback

The next frontier in construction layout robotics is autonomous synchronization between physical construction and digital models without human intervention. Emerging systems automatically compare as-built conditions captured through integrated sensors against original BIM requirements, flagging discrepancies and updating digital records in real time. This creates a living digital twin that reflects actual site conditions rather than design intent alone. Facility owners increasingly demand these as-built digital records for ongoing operations and maintenance. Vendors that deliver seamless, automated field-to-BIM feedback will capture significant value by addressing owner requirements while simultaneously reducing contractor risk and rework exposure.

Global Construction Layout Robots Market: Research Scope and Analysis

By Product Type Analysis

Semi-autonomous robots are expected to dominate the product type segment by holding approximately 58.1% of the total market share in 2026. This dominance is rooted in the fact that these systems, requiring an operator for setup and navigation while automating the marking process, offer the most accessible entry point for the broad construction market. The majority of commercial and residential construction projects benefit from the 2-3x labor productivity improvement these systems provide, while the operator maintains supervisory control and can manage multiple robots across a job site. The extensive installed base of robotic total stations from surveying applications has familiarized the construction workforce with this operational model, further cementing this segment's leading position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fully autonomous robots represent the fastest-growing product segment, as large general contractors and advanced specialty firms seek to eliminate labor dependencies entirely. These systems navigate job sites independently using SLAM technology, pre-programmed BIM data, and integrated obstacle avoidance to mark layout points without any on-site human operation. Major infrastructure projects and mega-scale commercial developments increasingly favor these systems to accelerate timelines and enable simultaneous operation across multiple shifts. While currently representing a smaller revenue share due to higher costs and longer adoption cycles, the segment's growth trajectory steepens as technology matures and major vendors bring production-ready autonomous platforms to market. The convergence of persistent labor shortages and advancing autonomy algorithms positions this segment for accelerated capture of market share through the forecast period.

By Technology Analysis

Total station-based technology currently commands the largest revenue share within the construction layout robots market in 2026. This leadership position reflects the deep heritage of robotic total stations in professional surveying and their seamless transition into construction layout applications. These systems deliver the highest absolute accuracy available, typically within 1-2 millimeters, making them indispensable for critical applications including equipment setting, embeds placement, and complex architectural feature installation.

Laser-guided technology represents the second-largest technology segment, favored for interior layout tasks, elevation control, and repetitive marking applications where absolute positioning requirements are less stringent. These systems utilize rotating laser planes and automated receiver systems to establish horizontal and vertical reference points rapidly across job sites. The segment maintains strong positions in residential construction and light commercial applications where value engineering drives technology selection.

By Application Analysis

Commercial construction is expected to lead the application segment in 2026. This dominance reflects the segment's demanding tolerance requirements, complex architectural geometries, and compressed project schedules that render manual layout methods increasingly untenable. Office towers, healthcare facilities, data centers, hotels, and large-scale retail developments require thousands of precisely positioned layout points across multiple floors, with errors cascading through curtain wall installation, MEP rough-in, and interior finishes.

Residential construction represents the fastest-growing application segment, as production homebuilders and large-scale multifamily developers seek productivity solutions amid persistent skilled labor shortages. While individual unit layouts are repetitive, the aggregate volume of layout points across large residential communities creates substantial labor demand. The segment is characterized by demand for intuitive, portable systems operable by existing field personnel with minimal specialized training. As building codes tighten and home designs grow more complex, the business case for automation in residential layout continues to strengthen across North America, Europe, and developed Asia-Pacific markets.

By End-User Analysis

Construction companies, including general contracting and construction management firms, constitute the largest end-user segment. These organizations recognize robotic layout as a strategic investment in productivity, quality control, and competitive differentiation rather than merely an equipment purchase. Large national and regional contractors are increasingly standardizing on specific robotic platforms and developing in-house training programs and dedicated automation teams to maximize utilization across their project portfolios. The segment is characterized by demand for enterprise software integration, fleet management tools, multi-unit pricing, and responsive technical support. As these organizations accumulate experience with robotic layout, they expand deployment from flagship projects to standard practice across their entire operations.

Contractors, encompassing specialty trade subcontractors including concrete, framing, mechanical, electrical, and drywall firms, represent the second-largest and fastest-growing end-user segment. These organizations adopt layout robots to improve the accuracy and speed of their rough-in work, reducing costly callbacks and protecting thin profit margins. The segment values portability, ease of use, clear return-on-investment calculations, and equipment rental options that align with project-based business models.

The Global Construction Layout Robots Market Report is segmented on the basis of the following:

By Product Type

- Semi-Autonomous Robots

- Fully Autonomous Robots

By Technology

- Total Station-Based

- Laser-Guided

- GPS-Guided

- Others

By Application

- Commercial Construction

- Residential Construction

- Industrial Construction

- Infrastructure Construction

By End-User

- Construction Companies

- Contractors

- Surveyors

- Architects

- Others

Impact of Artificial Intelligence in the Global Construction Layout Robots Market

Artificial intelligence is transforming the global Construction Layout Robots Market by enhancing positioning accuracy, operational efficiency, and autonomous decision-making across construction sites. AI-driven computer vision enables layout robots to recognize reference points, detect obstacles, and adapt to changing site conditions without human intervention. Machine learning algorithms analyze historical layout data, project schedules, and trade sequencing to optimize marking sequences and minimize conflicts between concurrent operations. This intelligence reduces the cognitive load on operators while improving overall project workflow coordination.

AI is also enabling the evolution from simple marking machines to comprehensive construction quality platforms. Advanced systems utilize deep learning to compare as-built conditions against BIM requirements in real time, automatically flagging deviations and recommending corrective actions before errors propagate. Natural language processing interfaces allow field personnel to query layout status, request additional points, or report issues using voice commands. By embedding artificial intelligence into layout robot controllers and cloud-based fleet management platforms, vendors deliver measurable improvements in construction quality, schedule certainty, and labor productivity while positioning their solutions as indispensable components of the digital construction ecosystem.

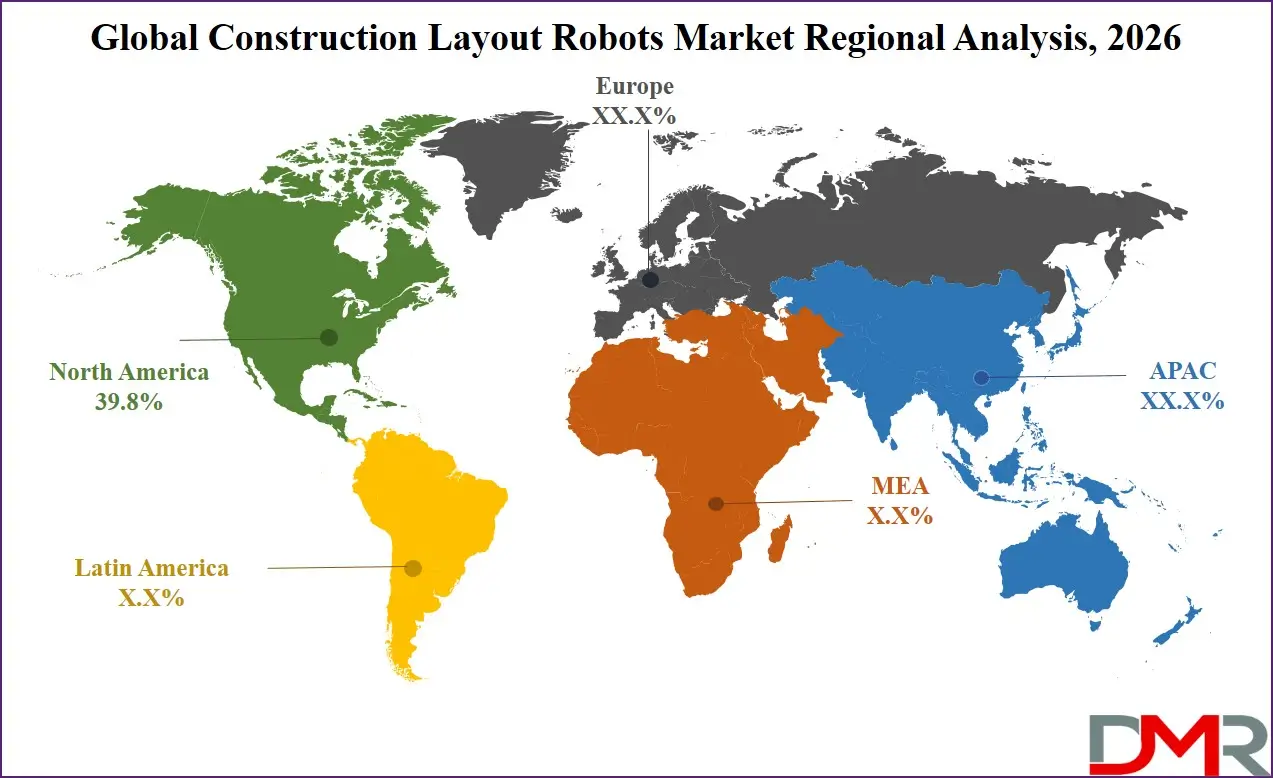

Global Construction Layout Robots Market: Regional Analysis

Region with the Largest Revenue Share

North America is expected to lead the global Construction Layout Robots Market with a share of 39.8% in 2026. This dominance is anchored by the region's acute skilled labor shortage, with over 400,000 unfilled construction positions and the average age of experienced layout professionals exceeding 48 years. The U.S. Infrastructure Investment and Jobs Act continues deploying billions in federal funding for transportation, water, and energy projects, many mandating or incentivizing modern construction methods. North America hosts the world's largest concentration of early-adopter general contractors, advanced specialty trades, and innovative construction technology vendors. The region's sophisticated equipment rental ecosystem, including industry leaders like United Rentals and Sunbelt Rentals, accelerates market penetration by lowering entry barriers for small and mid-sized contractors. Strong venture capital investment in construction robotics startups further fuels innovation and competitive intensity. These converging factors ensure North America maintains revenue leadership through the forecast period while other regions exhibit higher growth rates from smaller bases.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia-Pacific is emerging as the region with the most significant growth in the global Construction Layout Robots Market, projected to achieve a CAGR of 21.6% from 2026 to 2035. This explosive growth is driven by China's mandated construction digitalization under successive Five-Year Plans, requiring state-owned enterprises to achieve specific productivity and automation targets. India's National Infrastructure Pipeline, encompassing over USD 1.4 trillion in projected investments, creates massive demand for productivity-enhancing technologies amid acute skilled labor shortages. Japan's demographic emergency, with construction workforce decline exceeding 30% since 2000, compels rapid automation adoption across residential, commercial, and infrastructure sectors. Southeast Asian nations, including Singapore, Malaysia, and Vietnam, are aggressively modernizing construction practices to support rapid urbanization and foreign investment. The region's dominance in electronics and robotics manufacturing fosters competitive supply chains and enables local vendors to offer cost-optimized solutions tailored to regional requirements. The confluence of government mandates, infrastructure investment, labor scarcity, and manufacturing capability positions Asia-Pacific as the decisive growth engine for global market expansion through 2035.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Construction Layout Robots Market: Competitive Landscape

The competitive landscape is characterized by the presence of established surveying and machine control technology leaders, specialized construction robotics startups, and diversified industrial automation firms. Competition is intensifying around technological innovation, particularly in autonomous navigation, software integration, and ease of use. Strategic partnerships between hardware manufacturers, software developers, equipment rental companies, and general contractors are increasingly common to accelerate market adoption and refine product-market fit. The ability to provide robust, accurate, and intuitive systems supported by accessible training, responsive service, and flexible commercial models is key to gaining and sustaining market share.

Some of the prominent players in the Global Construction Layout Robots Market are:

- Trimble Inc.

- Topcon Corporation

- Leica Geosystems

- Hilti Group

- Dusty Robotics

- HP Inc.

- Construction Robotics

- Caterpillar Inc.

- Brokk AB

- Boston Dynamics

- Built Robotics

- Fujita Corporation

- Komatsu Ltd.

- Advanced Construction Robotics

- Robotics Plus

- Civdrone

- Scaled Robotics

- Rugged Robotics

- Ekso Bionics Holdings, Inc.

- Autonomous Solutions, Inc.

- Other Key Players

Recent Developments in the Global Construction Layout Robots Market

- December 2025: Multiple UK construction firms have started reporting productivity gains using HP SitePrint, an autonomous construction layout robot that prints layout marks, lines, and symbols from digital plans directly onto site surfaces, a concrete example of layout robot adoption in practice.

- November 2025: Dusty Robotics expanded its automated construction layout capabilities through a partnership with Hexagon Manufacturing Intelligence, enhancing precision and collaboration between digital design files and on‑site robotic layout workflows for its FieldPrint platform.

- July 2025: Civ Robotics secured USD 7.5 million in Series A funding for its CivDot autonomous layout robot, an outdoor construction layout solution that marks survey points with high precision using GPS/RTK technology, reflecting increased investor confidence in construction layout automation.

- January 2025: FBR Ltd completed a U.S. demonstration of its Hadrian X autonomous bricklaying robot in Florida, constructing multiple house exteriors and establishing a joint venture with CRH Ventures to deploy up to 20 robots, showing commercial viability of advanced construction robotics.

- January 2024: Dusty Robotics introduced its second‑generation FieldPrinter layout robot and the integrated FieldPrint Platform that supports BIM‑to‑field workflows, enabling automated printing of jobsite layout plans directly from digital models with improved navigation and edge‑printing capabilities.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 761.8 Mn |

| Forecast Value (2035) |

USD 3,233.3 Mn |

| CAGR (2026–2035) |

17.4% |

| The US Market Size (2026) |

USD 255.0 Mn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Semi-Autonomous Robots and Fully Autonomous Robots), By Technology (Total Station-Based, Laser-Guided, GPS-Guided and Others), By Application (Commercial Construction, Residential Construction, Industrial Construction and Infrastructure Construction), By End-User (Construction Companies, Contractors, Surveyors, Architects and Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Trimble Inc., Topcon Corporation, Leica Geosystems, Hilti Group, Dusty Robotics, HP Inc., Construction Robotics, Caterpillar Inc., Brokk AB, Boston Dynamics, Built Robotics, Fujita Corporation, Komatsu Ltd., Advanced Construction Robotics, Robotics Plus, Civdrone, Scaled Robotics, Rugged Robotics, Ekso Bionics Holdings, Inc., Autonomous Solutions, Inc., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Construction Layout Robots Market?

▾ The Global Construction Layout Robots Market size is estimated to have a value of USD 761.8 million in 2026 and is expected to reach USD 3,233.3 million by the end of 2035.

What is the growth rate in the Global Construction Layout Robots Market in 2026?

▾ The market is growing at a CAGR of 17.4 percent over the forecasted period of 2026.

What is the size of the US Construction Layout Robots Market?

▾ The US Construction Layout Robots Market is projected to be valued at USD 255.0 million in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 994.3 million in 2035 at a CAGR of 16.3%.

Which region accounted for the largest Global Construction Layout Robots Market?

▾ North America is expected to have the largest market share in the Global Construction Layout Robots Market with a share of about 39.8% in 2026.

Who are the key players in the Global Construction Layout Robots Market?

▾ Some of the major key players in the Global Construction Layout Robots Market are Trimble Inc., Topcon Corporation, Hilti Group, HP Inc., Caterpillar Inc., and many others.