Market Overview

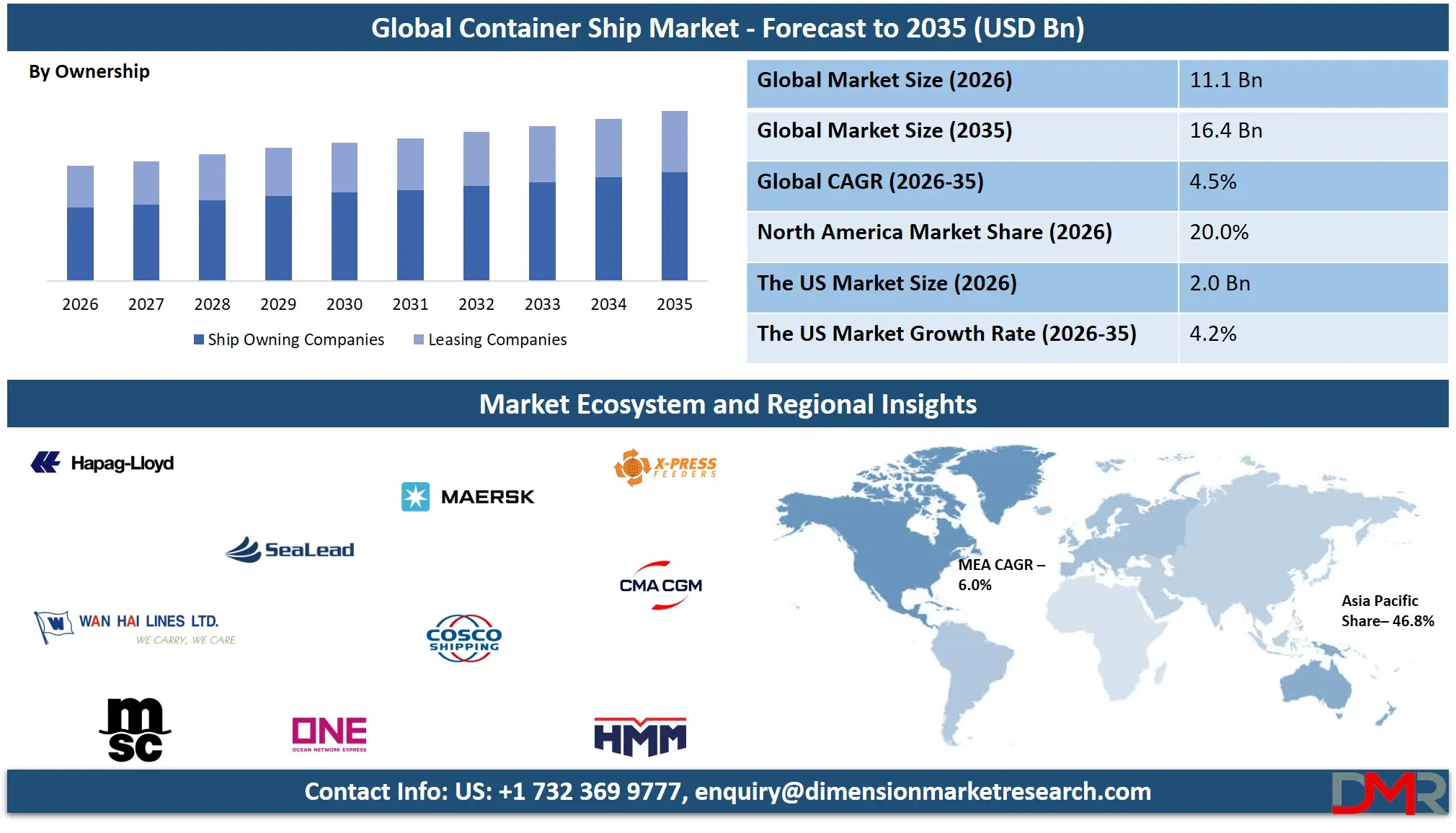

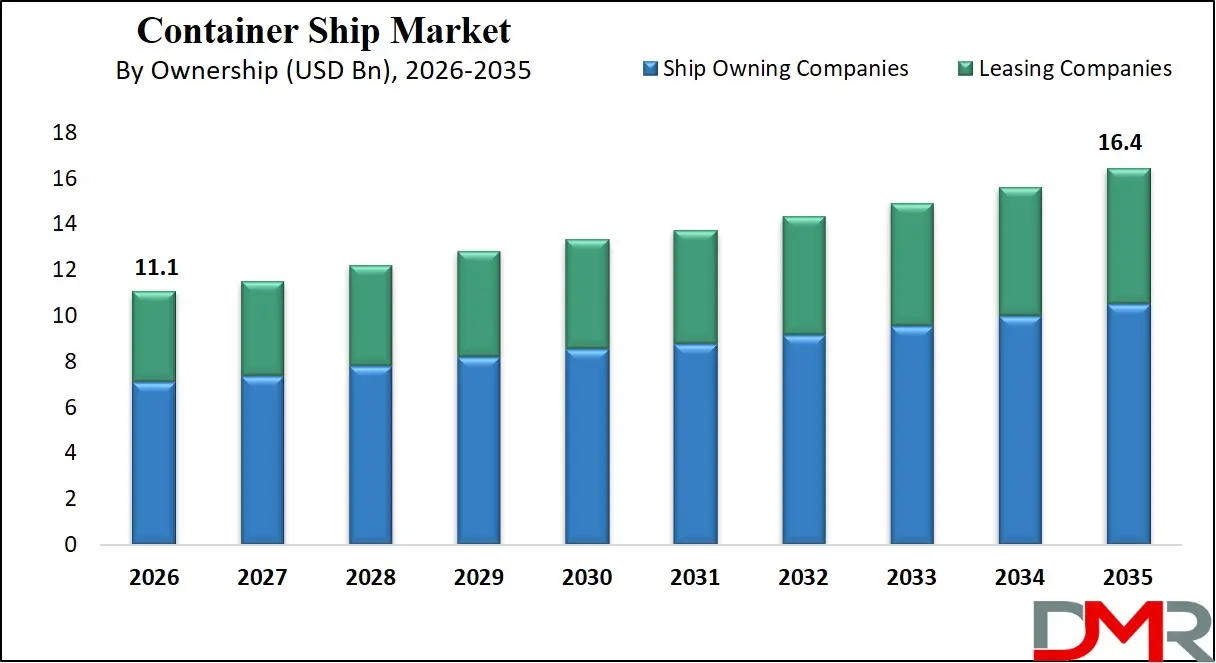

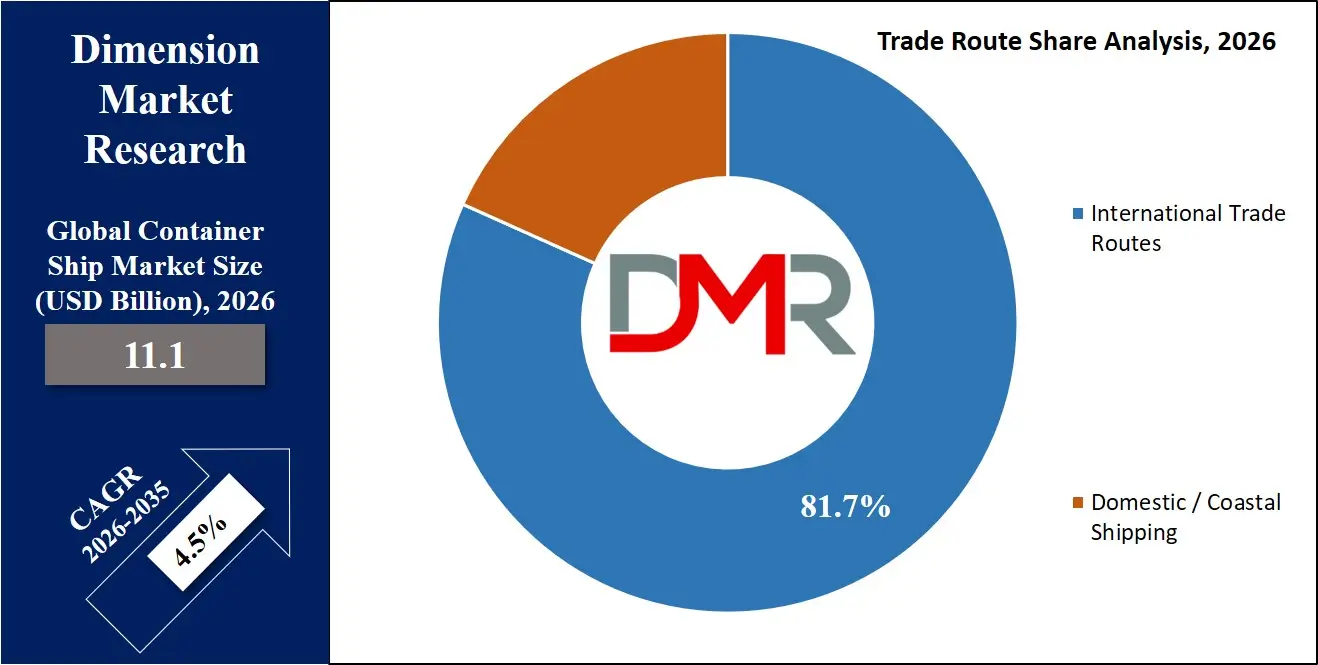

The Global Container Ship Market size is projected to reach USD 11.1 billion in 2026 and grow at a compound annual growth rate of 4.5% to reach a value of USD 16.4 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Container ships are specialized cargo vessels designed to transport standardized intermodal containers used in global trade. These vessels are a fundamental component of the international logistics ecosystem, enabling efficient movement of goods across oceans and connecting manufacturing hubs with global consumer markets. Container ships operate within an integrated supply chain framework that includes ports, terminals, freight forwarders, and inland transportation networks. Modern vessels vary in size and capacity, ranging from small feeder ships that serve regional ports to ultra-large container ships capable of carrying more than 20,000 twenty-foot equivalent units (TEUs). Their role is essential in supporting industries such as retail, automotive, electronics, and manufacturing by ensuring reliable and cost-efficient maritime transportation.

The container shipping industry has evolved significantly due to advances in ship design, port automation, and digital logistics systems. Increasing global trade volumes and expanding e-commerce markets have heightened the demand for efficient maritime transport solutions. Shipping companies are investing in larger and more fuel-efficient vessels to reduce per-unit transport costs and improve operational efficiency. Environmental considerations are also influencing vessel design, leading to the adoption of alternative fuels such as liquefied natural gas (LNG), methanol, and hybrid propulsion technologies. These innovations aim to reduce emissions and align maritime transport with global sustainability goals.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Recent years have witnessed significant structural shifts in the industry driven by port infrastructure upgrades, fleet modernization programs, and strategic alliances among shipping operators. Many carriers are focusing on expanding fleet capacity while integrating digital technologies for route optimization, cargo tracking, and predictive maintenance. Investments in smart ports and automated container terminals are also improving cargo handling efficiency. Additionally, regulatory frameworks targeting carbon reduction and maritime safety are reshaping operational strategies across the sector, pushing companies toward greener and more technologically advanced shipping solutions.

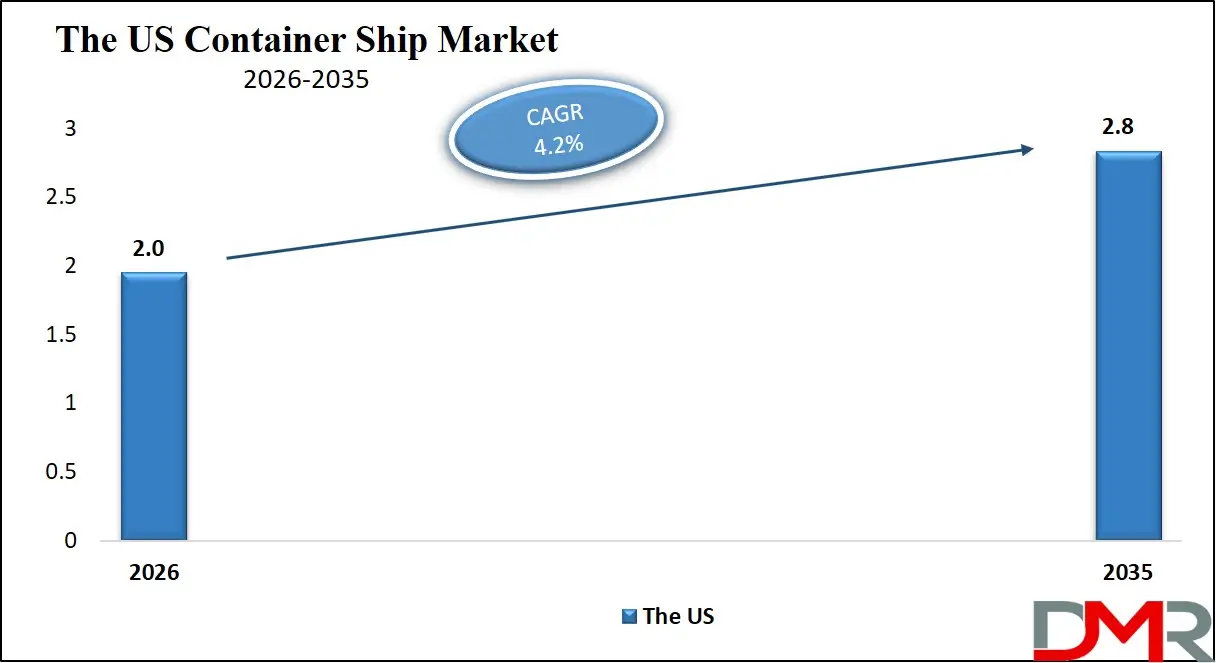

The US Container Ship Market

The US Container Ship Market size is projected to reach USD 2.0 billion in 2026 at a compound annual growth rate of 4.2% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US container ship market is shaped by its extensive port infrastructure and high dependence on international trade. Major ports such as Los Angeles, Long Beach, and New York–New Jersey serve as critical gateways for imports and exports. Government initiatives aimed at improving port capacity, supply chain resilience, and maritime infrastructure modernization are strengthening the country's shipping ecosystem. Increasing trade with Asia and growing consumer demand for imported goods continue to support container shipping activity. Investments in port automation, digital cargo management systems, and cleaner maritime fuels are further influencing the evolution of the US container shipping landscape.

Europe Container Ship Market

Europe Container Ship Market size is projected to reach USD 1.9 billion in 2026 at a compound annual growth rate of 4.3% over its forecast period.

The European container ship market is influenced by strong maritime trade networks and strict environmental regulations. Major ports including Rotterdam, Antwerp-Bruges, and Hamburg play central roles in global shipping routes. Regional sustainability initiatives, particularly policies aligned with the European Green Deal, are encouraging shipping operators to adopt low-carbon technologies and alternative fuels. Europe is also witnessing increased investments in green port infrastructure, shore-power facilities, and smart logistics systems. The region's advanced maritime technology sector and strong regulatory framework are accelerating innovation in ship efficiency, emissions reduction, and digital supply chain integration.

Japan Container Ship Market

Japan Container Ship Market size is projected to reach USD 999.0 million in 2026 at a compound annual growth rate of 4.0% over its forecast period.

Japan's container ship market is driven by its export-oriented economy and advanced shipbuilding industry. The country plays a significant role in global maritime logistics, supported by technologically advanced ports such as Yokohama and Kobe. Government initiatives promoting maritime decarbonization and smart shipping technologies are influencing fleet modernization strategies. Japanese shipping companies are actively investing in LNG-powered vessels and alternative propulsion systems to meet global emission standards. While Japan faces challenges such as port congestion and fluctuating trade volumes, its strong engineering capabilities and technological expertise provide opportunities for innovation in next-generation container ship design and maritime logistics solutions.

Container Ship Market: Key Takeaways

- Market Growth: The Container Ship Market size is expected to grow by USD 4.9 billion, at a CAGR of 4.5%, during the forecasted period of 2027 to 2035.

- By Ownership: The ship owning companies segment is anticipated to get the majority share of the Container Ship market in 2026.

- By Trade Route: The international trade route segment is expected to get the largest revenue share in 2026 in the Container Ship market.

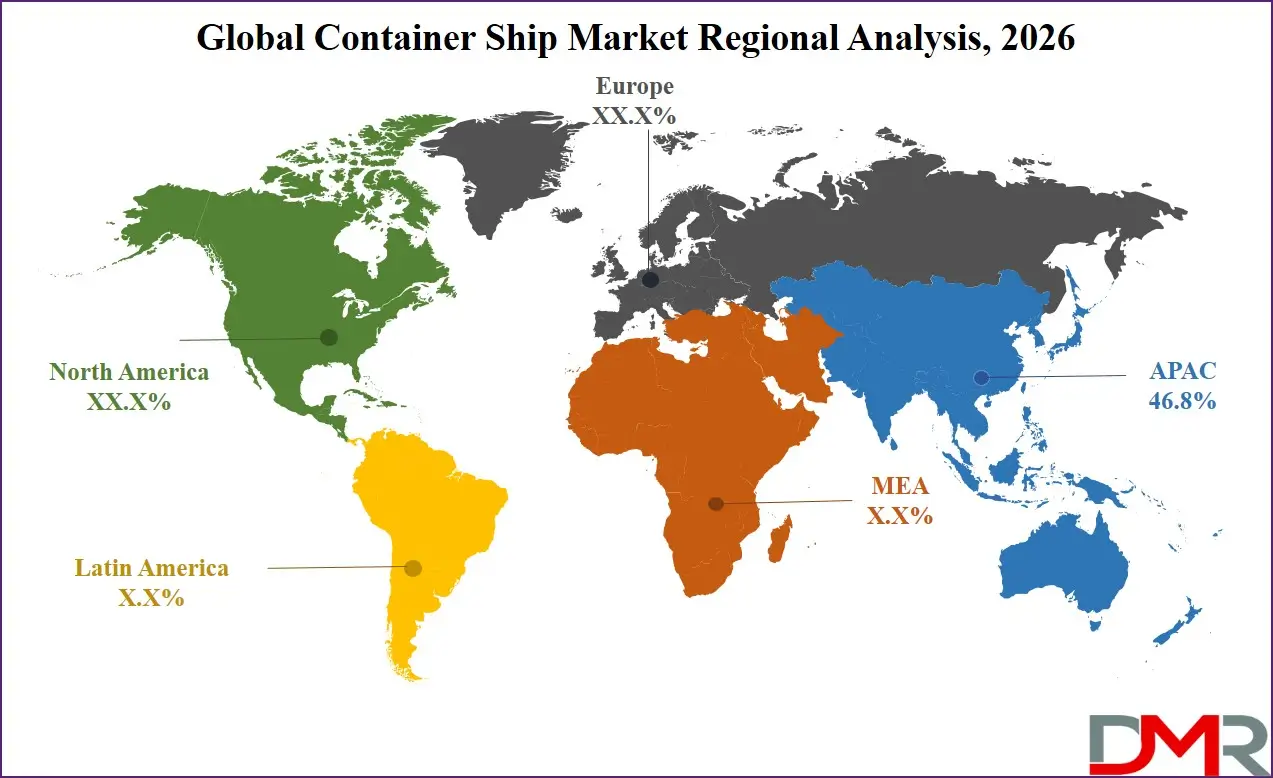

- Regional Insight: Asia Pacific is expected to hold a 46.8% share of revenue in the global Container Ship market in 2026.

- Use Cases: Some of the use cases of Container Ship include e-commerce logistics, agricultural & food trade, and more.

Container Ship Market: Use Cases:

- Global Manufacturing Supply Chains: Container ships enable efficient transport of raw materials, components, and finished products between manufacturing hubs and global markets, supporting industries such as electronics, automotive, and machinery.

- Retail and Consumer Goods Distribution: Large retail chains rely on container shipping to move consumer goods from production centers to distribution hubs worldwide, ensuring consistent product availability across international markets.

- Agricultural and Food Trade: Container vessels facilitate the movement of packaged agricultural products, refrigerated foods, and processed goods across continents using specialized refrigerated containers.

- E-commerce Logistics: The rapid growth of cross-border e-commerce has increased demand for container shipping services to transport bulk orders from manufacturing regions to fulfillment centers.

- Energy and Industrial Equipment Transport: Heavy industrial equipment, machinery parts, and renewable energy components such as wind turbine parts are frequently transported via container vessels.

- Government and Humanitarian Logistics: Governments and international agencies use container ships to transport aid supplies, disaster relief materials, and infrastructure equipment during humanitarian missions.

- Regional Feeder Shipping Networks: Smaller feeder container ships distribute cargo from large transshipment hubs to smaller regional ports, improving connectivity in coastal and island economies.

Stats & Facts

- International Maritime Organization reported in 2024 that maritime transport carries around 80% of global trade by volume.

- United Nations Conference on Trade and Development stated in 2024 that the global merchant fleet surpassed 2.3 billion deadweight tons capacity.

- World Bank indicated in 2024 that global container port throughput exceeded 850 million TEUs annually.

- International Energy Agency reported in 2025 that shipping contributes roughly 2% to 3% of global carbon dioxide emissions.

- U.S. Department of Transportation noted in 2024 that American ports handle more than 40 million container units annually.

- European Commission stated in 2024 that over 75% of EU external trade is transported by sea.

- Japan Ministry of Land, Infrastructure, Transport and Tourism reported in 2025 that Japanese ports handle over 18 million TEUs of container cargo each year.

- International Chamber of Shipping stated in 2024 that more than 50,000 merchant ships operate globally in international trade.

- Organisation for Economic Co-operation and Development reported in 2024 that maritime transport demand is expected to triple by 2050.

- U.S. Maritime Administration noted in 2025 that the United States maintains more than 360 commercial seaports supporting international trade.

- Eurostat reported in 2024 that EU ports handled more than 3.5 billion tonnes of seaborne goods.

- Asian Development Bank stated in 2025 that Asia accounts for nearly 65% of global container port traffic.

- International Transport Forum reported in 2024 that container ships larger than 20,000 TEU now represent a significant share of newly delivered vessels.

Market Dynamic

Driving Factors in the Container Ship Market

Expansion of Global Trade and Supply Chains

Globalization and expanding international trade networks are major factors driving the demand for container ships. As manufacturing supply chains extend across multiple continents, efficient maritime transportation has become essential for moving large volumes of goods at competitive costs. Container ships offer standardized cargo handling, reducing loading times and improving logistics efficiency. Growing trade between Asia, Europe, and North America continues to increase container traffic on major shipping routes. Additionally, the rise of cross-border e-commerce and just-in-time inventory systems has increased the reliance on reliable maritime transport, encouraging shipping companies to expand fleet capacity and invest in larger, more efficient container vessels.

Advancements in Ship Technology and Fuel Efficiency

Technological innovations in shipbuilding and propulsion systems are significantly contributing to the growth of the container ship industry. Modern vessels are designed with improved hydrodynamics, lightweight materials, and advanced navigation systems that enhance fuel efficiency and operational performance. Shipping operators are increasingly adopting alternative fuels such as LNG, methanol, and hybrid propulsion systems to comply with international environmental regulations. Automation, digital navigation tools, and predictive maintenance technologies are also improving vessel performance and reducing operational costs. These advancements allow shipping companies to operate larger vessels while maintaining lower emissions and improved cargo handling efficiency.

Restraints in the Container Ship Market

High Capital Investment and Fleet Maintenance Costs

The container ship industry requires significant capital investment for vessel construction, maintenance, and operational management. Building modern container ships with advanced fuel systems and high capacity involves substantial financial resources. Additionally, ongoing costs related to crew training, fuel, insurance, and regulatory compliance place pressure on shipping companies. Shipowners must also regularly upgrade vessels to meet evolving environmental standards and safety requirements. Smaller shipping operators often face challenges in accessing sufficient capital for fleet expansion, which can limit market participation and slow overall industry growth.

Port Infrastructure Limitations and Congestion

Port congestion and infrastructure limitations remain significant challenges for container ship operations. As vessel sizes continue to increase, many ports require upgrades to accommodate ultra-large container ships and handle higher cargo volumes efficiently. Inadequate port equipment, limited berth availability, and insufficient hinterland transport connectivity can create logistical bottlenecks. Delays in cargo unloading and customs processing further increase operational costs and disrupt supply chains. Developing regions particularly face infrastructure gaps that restrict efficient maritime trade, affecting the smooth functioning of container shipping networks.

Opportunities in the Container Ship Market

Growth of Green Shipping Technologies

The global push toward decarbonization is creating new opportunities for innovation in container shipping. Governments and international organizations are encouraging the development of low-carbon maritime technologies to reduce greenhouse gas emissions. Shipping companies are exploring alternative fuels such as hydrogen, ammonia, and biofuels, alongside energy-efficient vessel designs. Investments in green shipping infrastructure, including shore power and carbon-neutral fuels, are expected to create long-term growth prospects for shipbuilders and technology providers. These developments can transform the maritime sector by aligning shipping operations with global climate objectives.

Expansion of Smart Ports and Digital Logistics

The integration of digital technologies into port operations and shipping logistics presents significant growth opportunities for the container ship industry. Smart ports equipped with automated cranes, digital cargo tracking systems, and AI-based logistics platforms are improving operational efficiency and reducing turnaround times. Shipping companies are increasingly adopting digital tools to optimize routes, manage cargo flows, and enhance fleet management. The expansion of integrated logistics platforms connecting ports, shipping lines, and inland transportation networks is expected to streamline global supply chains and strengthen the role of container shipping in international trade.

Trends in the Container Ship Market

Shift Toward Mega Container Vessels

One of the most prominent trends in the container ship industry is the growing deployment of mega container vessels with capacities exceeding 20,000 TEUs. Shipping companies are investing in larger ships to achieve economies of scale and reduce per-unit transportation costs. These vessels are particularly suitable for high-volume trade routes such as Asia–Europe corridors. However, the trend also requires significant port infrastructure upgrades and improved logistics coordination. The increasing presence of ultra-large container ships is reshaping maritime trade patterns and influencing port development strategies worldwide.

Increasing Digitalization of Maritime Operations

Digital transformation is rapidly changing the operational landscape of container shipping. Advanced technologies such as satellite connectivity, blockchain-based cargo documentation, and real-time tracking systems are improving transparency and efficiency in maritime logistics. Digital platforms allow shipping companies to monitor vessel performance, optimize shipping routes, and manage cargo flows more effectively. The adoption of data analytics and automated systems is also enhancing decision-making processes, reducing operational risks, and improving overall supply chain reliability.

Impact of Artificial Intelligence in Container Ship Market

- Route Optimization: AI algorithms analyze weather patterns, fuel consumption, and port congestion to determine the most efficient shipping routes, reducing fuel usage and travel time.

- Predictive Maintenance: AI-powered monitoring systems analyze engine and equipment data to predict potential failures, helping shipping companies perform maintenance before breakdowns occur.

- Cargo Tracking and Visibility: AI systems enable real-time monitoring of container locations, improving transparency across the supply chain and allowing better coordination between ports and logistics providers.

- Port Operations Automation: AI assists automated cranes, container sorting systems, and yard planning tools, improving cargo handling efficiency and reducing turnaround times.

- Demand Forecasting: Machine learning models analyze trade patterns and shipping demand to help companies optimize fleet deployment and capacity planning.

- Safety and Navigation Assistance: AI-based navigation tools support captains with collision avoidance, weather risk assessment, and route adjustments for safer maritime operations.

- Energy Efficiency Management: AI helps monitor fuel consumption and engine performance to optimize vessel energy usage and reduce emissions.

- Smart Container Monitoring: AI-enabled sensors track temperature, humidity, and container conditions, particularly important for perishable or sensitive cargo.

- Autonomous Shipping Development: AI technologies are supporting the development of semi-autonomous and fully autonomous container ships for future maritime operations.

Impact of the Iran War in Container Ship Market

The Iran war is creating disruptions in global container shipping by increasing geopolitical risks across key maritime routes such as the Strait of Hormuz and nearby Middle Eastern waters. Shipping companies are facing higher security concerns, leading to route diversions and longer transit times for container vessels. These disruptions reduce fleet efficiency and increase operational costs. In addition, war-risk insurance premiums and freight rates are rising due to heightened uncertainty. Port congestion and delays in cargo deliveries are also becoming more common. Overall, the conflict is contributing to supply chain instability and cost volatility, affecting global trade flows and container ship market operations.

Research Scope and Analysis

By Ship Capacity Analysis

Panamax container ships remain one of the most widely used vessel categories in global maritime trade due to their operational flexibility and compatibility with a wide range of ports. These ships are designed to fit within the original Panama Canal lock dimensions, making them suitable for numerous international trade routes. Their balanced cargo capacity allows shipping operators to maintain efficient operations without requiring extremely large port infrastructure upgrades. As of 2026, Panamax ships are projected to hold around 22.6% market share in the global container ship fleet capacity distribution. Many shipping companies continue to deploy these vessels for medium-distance routes, regional services, and feeder networks between major ports and smaller terminals. Their relatively lower operational cost compared to ultra-large vessels and their ability to access ports with moderate draft restrictions contribute significantly to their continued dominance in several shipping corridors.

Ultra Large Container Ships represent the fastest-growing vessel category in the container shipping industry. These ships are primarily used on high-volume international trade routes such as Asia-Europe and Asia-North America. Shipping companies are increasingly investing in ULCS vessels to benefit from economies of scale, enabling them to transport larger volumes of cargo at lower per-container costs. Growing global trade and rising demand for efficient cargo transportation have accelerated the adoption of these large-capacity ships. Additionally, new ULCS vessels are being designed with improved fuel efficiency, alternative propulsion technologies, and enhanced cargo handling capabilities. As global port infrastructure continues to upgrade to accommodate these massive vessels, the deployment of ULCS fleets is expected to expand rapidly in the coming years.

By Propulsion Type Analysis

Conventional fuel-powered container ships currently dominate the maritime transport sector, primarily relying on heavy fuel oil (HFO) and marine diesel oil (MDO) as their primary energy sources. These vessels remain widely used due to the established global fuel supply infrastructure and the lower cost associated with traditional marine fuels. In 2026, conventional fuel-powered ships are estimated to account for around 68.3% of the container ship propulsion market share. Despite growing environmental concerns, many shipping companies continue to operate these vessels because of their reliability and compatibility with existing fleet operations. However, stricter environmental regulations and emission reduction targets are encouraging operators to gradually transition toward cleaner propulsion technologies. Nevertheless, conventional fuel-powered ships will likely remain a significant part of the global fleet for the foreseeable future.

Alternative fuel-powered container ships are emerging as the fastest-growing propulsion segment as the maritime industry moves toward decarbonization. Ships powered by LNG, methanol, and hybrid-electric propulsion systems are gaining popularity among shipping companies seeking to reduce greenhouse gas emissions and comply with international maritime regulations. LNG-powered vessels, in particular, have seen rapid adoption due to their lower sulfur emissions compared to traditional fuels. Governments and international organizations are also promoting cleaner maritime technologies through environmental policies and incentives. As research into hydrogen and ammonia-based propulsion systems continues, the adoption of alternative fuel container ships is expected to expand significantly, making them an important component of future maritime transport systems.

By Ownership Analysis

Ship owning companies represent the dominant ownership structure in the container shipping industry, as many large maritime operators maintain direct control over their fleets. These companies invest heavily in vessel construction, fleet expansion, and technological upgrades to maintain competitive advantages in global trade routes. In 2026, ship owning companies are projected to hold approximately 63.9% market share within the container ship ownership segment. Direct ownership allows shipping operators to manage operational efficiency, optimize fleet utilization, and control long-term investment strategies. Many major shipping lines prefer owning vessels to ensure flexibility in route deployment and scheduling. Additionally, owning ships enables companies to integrate digital fleet management systems, improve fuel efficiency, and implement sustainability initiatives aligned with international maritime regulations.

Leasing companies represent a rapidly expanding segment within the container ship ownership landscape. Instead of purchasing vessels outright, many shipping operators prefer leasing arrangements to reduce upfront capital investment and maintain financial flexibility. Leasing companies acquire ships and provide them to shipping lines under long-term charter agreements. This model enables smaller operators and emerging shipping firms to access modern vessels without the burden of significant capital expenditure. The growing volatility in global trade and shipping rates has also encouraged companies to adopt leasing strategies that allow them to scale fleet capacity based on market demand. As financial institutions increasingly support maritime leasing programs, this segment is expected to witness steady growth.

By Trade Route Analysis

International trade routes account for the majority of container ship operations, connecting manufacturing regions with global consumer markets. Major corridors such as Asia-Europe, Trans-Pacific, and Asia-Middle East dominate global maritime cargo flows. In 2026, international trade routes are expected to represent approximately 81.7% of the container ship market share due to the high volume of goods transported across continents. Globalized supply chains and the expansion of cross-border e-commerce continue to drive demand for container shipping services. Additionally, multinational corporations rely heavily on maritime logistics to distribute products worldwide. Investments in port infrastructure, transshipment hubs, and shipping alliances further strengthen the role of international trade routes in the container ship industry.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Domestic and coastal shipping is emerging as a fast-growing segment, particularly in countries with extensive coastlines and strong regional trade networks. Coastal container shipping allows efficient movement of cargo between ports within the same country or nearby regions, reducing reliance on road and rail transport. Governments in several countries are encouraging coastal shipping to improve logistics efficiency and reduce carbon emissions associated with land transport. As port infrastructure expands and smaller feeder vessels are deployed, domestic container shipping services are expected to grow steadily. This segment plays a critical role in connecting smaller regional ports with major international shipping hubs.

By End User Analysis

Shipping lines and ocean carriers represent the largest end-user segment in the container ship market as they operate fleets responsible for transporting goods across international trade routes. These companies manage large networks of vessels, shipping schedules, and global logistics partnerships. In 2026, shipping lines and ocean carriers are expected to hold around 70.5% of the total market share among end users. Their dominance is driven by their extensive operational capacity, global trade presence, and ability to invest in advanced container vessels. Major shipping companies are increasingly focusing on fleet modernization, digital logistics platforms, and fuel-efficient ship designs to remain competitive. Their role in managing large-scale cargo flows and maintaining international trade connectivity ensures their continued leadership in the container ship market.

Logistics and freight forwarding companies represent the fastest-growing end-user segment as global supply chains become more integrated and complex. These organizations coordinate cargo transportation across multiple modes including sea, rail, road, and air. Freight forwarders increasingly charter container vessels or secure shipping capacity through long-term agreements with maritime operators. As international trade volumes expand and e-commerce logistics networks grow, freight forwarding companies are playing a more active role in maritime transport coordination. Their expertise in cargo consolidation, customs documentation, and supply chain management enables them to support efficient container shipping operations across global markets.

The Container Ship Market Report is segmented on the basis of the following:

By Ship Capacity

- Small Feeder Ships (Up to 3,000 TEU)

- Feeder Ships (3,001 – 5,000 TEU)

- Panamax Ships (5,001 – 10,000 TEU)

- Post-Panamax Ships (10,001 – 14,500 TEU)

- Very Large Container Ships (VLCS) (14,501 – 20,000 TEU)

- Ultra Large Container Ships (ULCS) (Above 20,000 TEU)

By Propulsion Type

- Conventional Fuel-Powered Ships

- Heavy Fuel Oil (HFO)

- Marine Diesel Oil (MDO)

- Alternative Fuel Ships

- LNG-Powered Container Ships

- Methanol-Powered Ships

- Hybrid / Electric Container Ships

By Ownership

- Ship Owning Companies

- Leasing Companies

By Trade Route

- International Trade

- Domestic / Coastal Shipping

By End User

- Shipping Lines / Ocean Carriers

- Logistics & Freight Forwarding Companies

- Government & Defense Logistics

Regional Analysis

Leading Region in the Container Ship Market

Asia Pacific dominates the global container ship market due to its strong manufacturing base, high export activity, and extensive maritime infrastructure. Countries such as China, South Korea, Japan, and Singapore serve as major hubs for shipbuilding, cargo handling, and international maritime trade. In 2026, the Asia Pacific region is projected to hold approximately 46.8% market share in the global container ship market. The presence of some of the world's busiest container ports, including Shanghai, Singapore, and Busan, significantly contributes to regional dominance. Additionally, the region hosts leading shipbuilding companies that produce advanced container vessels for global fleets. Continuous investments in port modernization, logistics connectivity, and smart maritime technologies further strengthen Asia Pacific's leadership in container shipping operations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Container Ship Market

The Middle East and Africa region is emerging as the fastest-growing market for container shipping due to increasing trade activity and strategic investments in port infrastructure. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are expanding port capacities and developing advanced logistics hubs to support global maritime trade. Major transshipment ports in the region are becoming critical connectors between Asia, Europe, and Africa. Governments are also investing heavily in economic diversification programs and trade corridor development, which is boosting maritime transportation demand. As regional trade volumes grow and logistics infrastructure improves, the Middle East and Africa are expected to experience rapid expansion in container shipping activity.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The container ship market is highly competitive and characterized by the presence of large global shipping operators alongside regional carriers and maritime leasing firms. Companies compete primarily through fleet capacity expansion, operational efficiency, and cost optimization strategies. Strategic alliances and vessel-sharing agreements have become common in the industry as operators seek to optimize shipping routes and reduce operational costs. Investment in fuel-efficient vessels, alternative propulsion technologies, and digital logistics systems also plays a significant role in maintaining competitiveness. Barriers to entry remain high due to the substantial capital required for vessel construction and fleet management. Additionally, shipping companies are increasingly focusing on sustainability initiatives, advanced port partnerships, and technology integration to strengthen their long-term market positioning.

Some of the prominent players in the global Container Ship are:

- Mediterranean Shipping Company (MSC)

- A.P. Moller–Maersk

- CMA CGM Group

- COSCO Shipping Lines

- Hapag-Lloyd

- Ocean Network Express (ONE)

- Evergreen Marine Corporation

- HMM Co., Ltd.

- ZIM Integrated Shipping Services

- Yang Ming Marine Transport Corporation

- Wan Hai Lines

- Pacific International Lines (PIL)

- SeaLead Shipping

- X-Press Feeders Group

- SITC Container Lines

- Unifeeder

- Islamic Republic of Iran Shipping Lines (IRISL)

- Korea Marine Transport Company (KMTC)

- Sinokor Merchant Marine

- Global Feeder Shipping

- Other Key Players

Recent Developments

- In April 2025, A.P. Moller–Maersk announced a major investment in expanding its fleet of methanol-powered container ships as part of its decarbonization strategy. The company confirmed orders for multiple large vessels capable of operating on green methanol fuel. These ships are expected to significantly reduce carbon emissions compared to conventional fuel-powered vessels. The initiative forms part of Maersk's broader commitment to achieving carbon-neutral shipping operations in the coming decades.

- In February 2025, Mediterranean Shipping Company announced the launch of a new series of LNG-powered container ships designed to improve fuel efficiency and reduce greenhouse gas emissions in maritime transport. The vessels were developed as part of the company's long-term sustainability strategy aimed at lowering carbon intensity across its global fleet. Each ship incorporates advanced propulsion systems and optimized hull designs that improve fuel performance while meeting international emission regulations.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 11.1 Bn |

| Forecast Value (2035) |

USD 16.4 Bn |

| CAGR (2026–2035) |

4.5% |

| The US Market Size (2026) |

USD 2.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Ship Capacity (Small Feeder Ships, Feeder Ships, Panamax Ships, Post-Panamax Ships, Very Large Container Ships (VLCS), Ultra Large Container Ships (ULCS)), By Propulsion Type (Conventional Fuel-Powered Ships, Alternative Fuel Ships), By Ownership (Ship Owning Companies, Leasing Companies), By Trade Route (International Trade, Domestic / Coastal Shipping), By End User (Shipping Lines / Ocean Carriers, Logistics & Freight Forwarding Companies, Government & Defense Logistics) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Mediterranean Shipping Company (MSC), A.P. Moller–Maersk, CMA CGM Group, COSCO Shipping Lines, Hapag-Lloyd, Ocean Network Express (ONE), Evergreen Marine Corporation, HMM Co., Ltd., ZIM Integrated Shipping Services, Yang Ming Marine Transport Corporation, Wan Hai Lines, Pacific International Lines (PIL), SeaLead Shipping, X-Press Feeders Group, SITC Container Lines, Unifeeder, Islamic Republic of Iran Shipping Lines (IRISL), Korea Marine Transport Company (KMTC), Sinokor Merchant Marine, Global Feeder Shipping, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Container Ship Market?

▾ The Global Container Ship Market size is expected to reach USD 11.1 billion by 2026 and is projected to reach USD 16.4 billion by the end of 2035.

Which region accounted for the largest Global Container Ship Market?

▾ Asia Pacific is expected to have the largest market share in the Global Container Ship Market, with a share of about 46.8% in 2026.

How big is the Container Ship Market in the US?

▾ The US Container Ship market is expected to reach USD 2.0 billion by 2026.

Who are the key players in the Container Ship Market?

▾ Some of the major key players in the Global Container Ship Market include MSC, Maersk, Cosco, and others.

What is the growth rate in the Global Container Ship Market?

▾ The market is growing at a CAGR of 4.5 percent over the forecasted period.