Market Overview

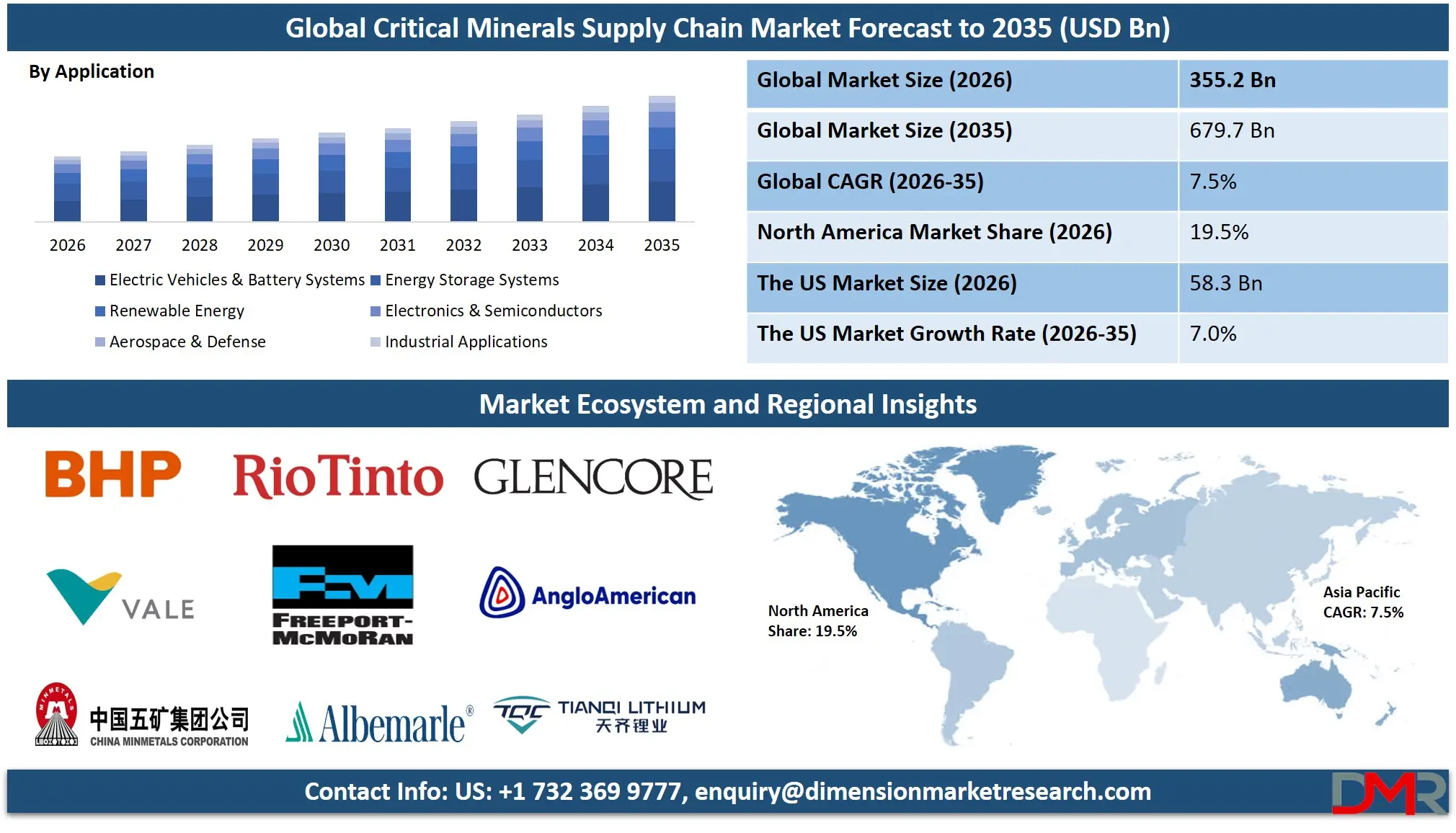

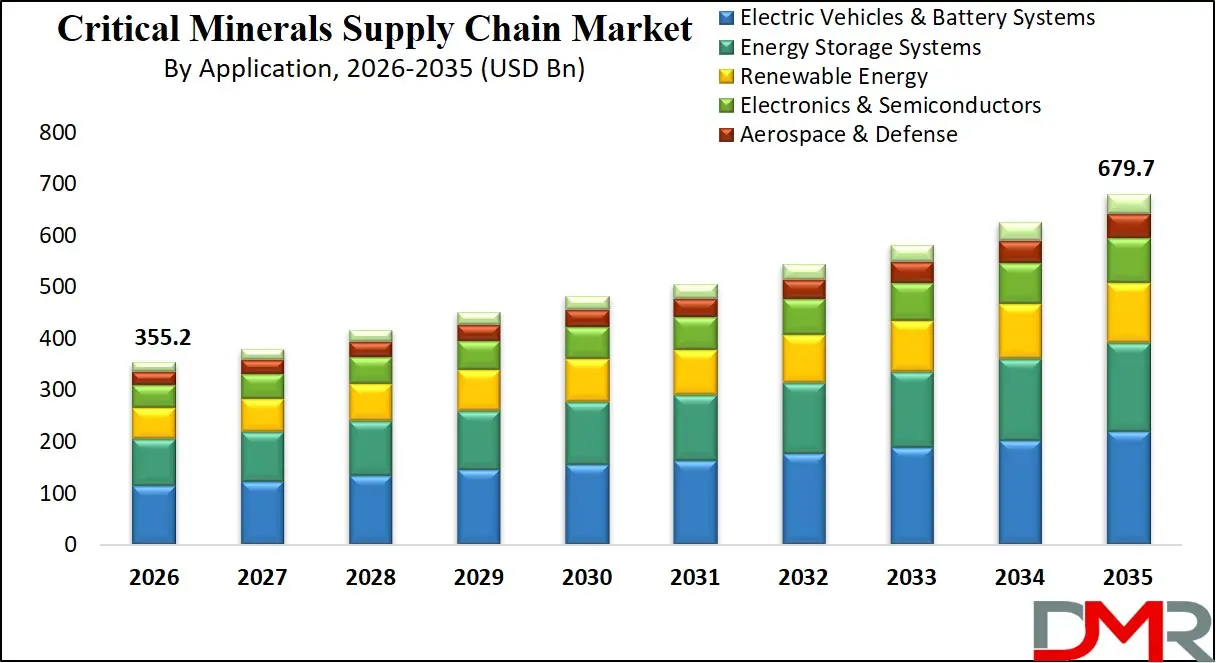

The global critical minerals supply chain market is expected to expand from USD 355.2 billion in 2026 to about USD 679.7 billion by 2035, reflecting a solid CAGR of around 7.5%, as governments and industries rush to secure the raw materials needed for clean energy, electric mobility, and advanced manufacturing. According to the International Energy Agency (IEA), demand for key energy transition minerals such as lithium, cobalt, nickel, copper, and rare earths is rising sharply as countries deploy more electric vehicles, batteries, wind turbines, and solar systems.

UNCTAD reports that lithium demand alone is projected to grow by about 353% between 2024 and 2040, while graphite demand may rise by roughly 131%, showing how fast downstream industries are scaling up. This surge in consumption forces governments and companies to invest in new mining projects, refining capacity, recycling, logistics, and traceability systems, all of which add value along the critical minerals supply chain.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

At the macro level, national net-zero targets and industrial policies are directly translating into multi-billion-dollar procurement of batteries, EVs, grid upgrades, and data centres, each of which requires large volumes of copper, lithium, nickel, and rare earth elements. For example, the IEA notes that clean energy technologies are capturing a rising share of total demand for many critical minerals, turning them from niche materials into strategic commodities.

As more countries introduce export controls and sign bilateral critical minerals partnerships, supply risks and price volatility increase, encouraging firms to diversify suppliers, build strategic stockpiles, and create more resilient and transparent supply chains. These structural shifts mean that spending on exploration, processing, logistics, digital tracking, and recycling of critical minerals is set to grow faster than underlying GDP, supporting a sustained 7–8% annual expansion of the global critical minerals supply chain market through 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Critical Minerals Supply Chain Market

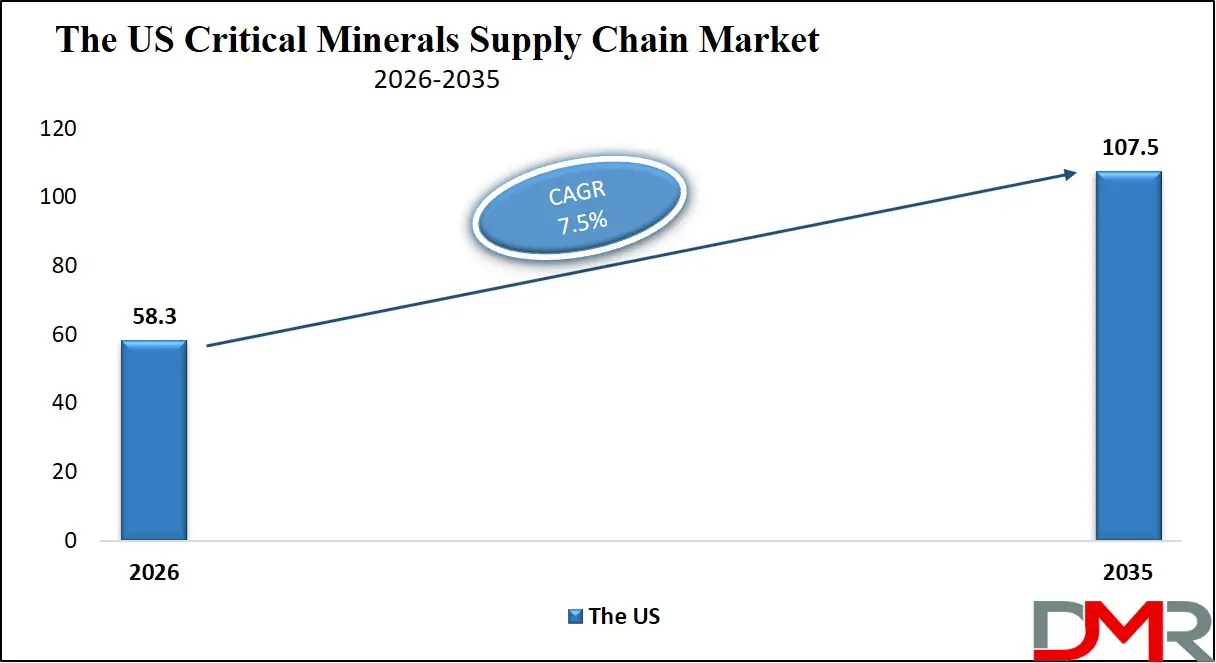

The US Critical Minerals Supply Chain Market is estimated to grow to USD 58.3 billion in 2026 with a compound annual growth rate of 7.0% during the forecast period.

The US market is defined by the existence of significant federal funding schemes like the National Critical Minerals Initiative, the DOE-based battery manufacturing and refining centers, the DOD-involved AI/ML-enabled process control pathways to rare earth and battery material production, all of which will help the development of the necessity of AI-driven grade engineering, real-time processing telemetry of automated leach reactors and robotic sorters, and predictive supply chain software.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Automated refining hardware systems continue to be adopted more rapidly in the region, and the US needs highly developed interoperability frameworks, integration of real-world evidence from digital mine and refinery logs, and verifiable critical-minerals AI assurance. Also, service providers are being pressured by initiatives like the Inflation Reduction Act and national AI in mining strategies to create dedicated integration and deployment services to guarantee data interoperability, security, and compliance across a variety of mining R&D departments and academic research centers.

Europe Critical Minerals Supply Chain Market

The Europe Critical Minerals Supply Chain Market is estimated to be valued at USD 64.6 million in 2026, witnessing growth at a CAGR of 6.9%, during the forecast period.

The market is mature in Europe, and it has a strong effect on the regulatory specifications and the regional policies, including the EU Critical Raw Materials Act, the European Battery Recycling Pilot Lines, and national digital mining programs (e.g., the France-Mineral Initiative and the German Rohstoffstrategie 2030 strategy). Another area that countries are working towards is smart refinery modularization in order to align research and production workload demands and interoperability of cross-border mineral data supply chains. It is driven by advanced technologies, such as real-time ore body modeling engines and high-reliability purity forecasting systems with an in-built predictive algorithm on the development of refined mineral streams. Adoption is facilitated by the use of public-private partnerships and harmonization of supply chain standards. Technologies like real-time computational workload balancing and smart contract-based data sharing are commonly practiced as research-centric programs, and Europe is a frontrunner in terms of the digital transformation of safe and efficient critical minerals-enabled processing.

Japan Critical Minerals Supply Chain Market

The Japan Critical Minerals Supply Chain Market is projected to be valued at USD 24.4 million in 2026, progressing at a CAGR of 7.2%, during the period spanning from 2026 to 2035.

Japan boasts a mature critical minerals market supported by high-performance automated mineral sorting systems, diagnostic refining integration technology, and a wide network of robotic processing AI innovations. Automation, precision, and process integrity are the priorities in the country and are achieved by predictive refining progression models and intelligent process management systems for industrial mineral processing. Growth is stimulated by government actions under the Society 5.0 initiative and constant investment in digital mineral processing infrastructure. The high volume of battery R&D, industrial grade development for lithium and rare earths, and mineral processing lab automation requires efficient AI for real-time evidence-based inference. The difficulties are high validation costs for new mineral processing automation architectures and integration with legacy extraction systems, yet the prospects are in exporting developed critical minerals technologies to Asian and Pacific markets.

Key Takeaways

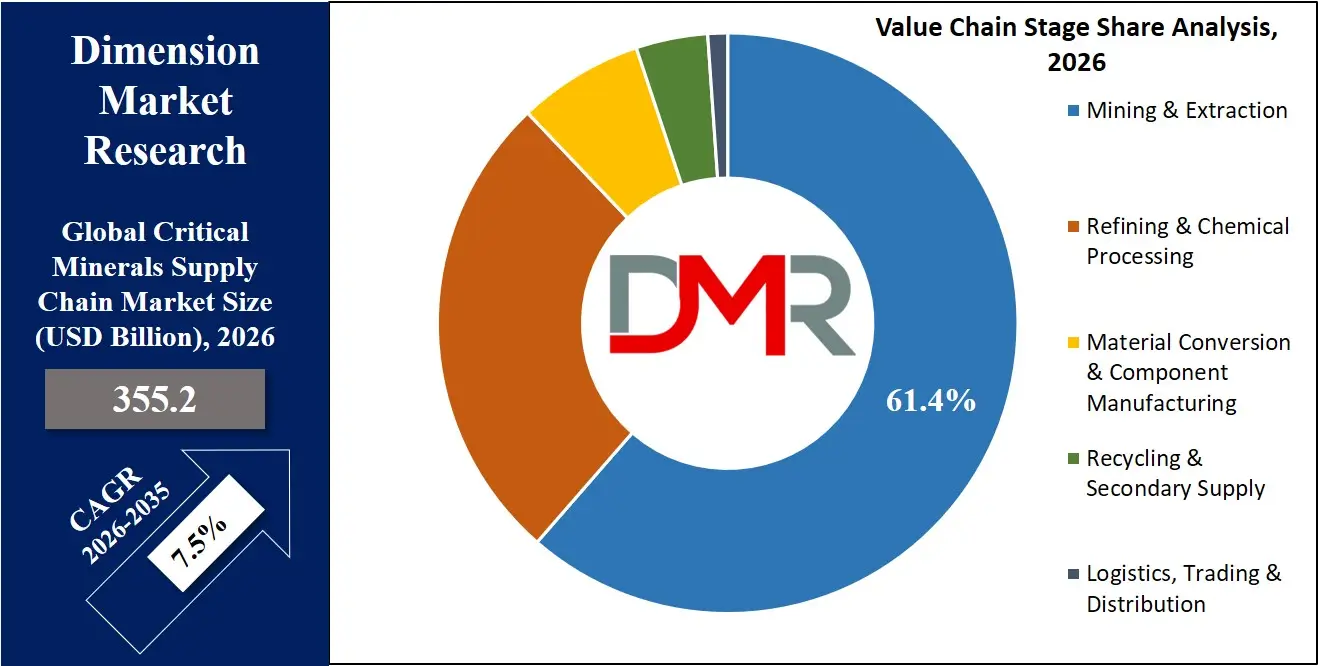

- The global Critical Minerals Supply Chain market is valued at USD 355.2 billion in 2026 and is projected to reach USD 679.7 billion by 2035, growing at a CAGR of 7.5%.

- By Value Chain Stage, Mining & Extraction is the dominant segment, accounting for 61.4% of the market in 2026.

- By Mineral Type, Lithium leads with a share of 27.2% in 2026, driven by surging demand from EV battery production and energy storage systems.

- By Application, Electric Vehicles & Battery Systems is the dominant segment, representing 44.2% of the market in 2026.

- Asia-Pacific dominates the global market with a share of 47.3%, while North America is identified as the fastest-growing region.

- The US Critical Minerals Supply Chain market is valued at USD 58.3 billion in 2026, expanding at a CAGR of 7.0% through 2035.

- Europe's market is projected to reach USD 64.6 million, growing at a CAGR of 6.9%, while Japan is expected to reach USD 24.4 million at a CAGR of 7.2%.

- Leading players in the Critical Minerals Supply Chain market include BHP Group Limited, Rio Tinto Group, and Glencore plc.

Use Cases

- Ore Grade Engineering for Battery Metals: Critical minerals supply chains are capable of designing high-throughput mineral processing flowsheets in real-time to discover optimal recovery routes for lithium and rare earth elements with latency on the order of weeks, saving orders of magnitude over time compared with manually testing mineral samples.

- Refining Pathway Optimization: Long-term leaching and separation data, such as cumulative recovery yields and impurity accumulation, are modeled to give process adjustment recommendations and keep safely managing production runs without interruption to ensure process stability and manufacturing confidence.

- Mining & Extraction Monitoring & Control: Industrial deployments are employing machine learning and concentrator analytics to perform on-device real-time recovery prediction, process anomaly detection, and automated reagent feed adjustment with quantifiable and proven accuracy.

- Population Health & Government Programs: More efficient critical minerals supply chains contribute to the success of battery innovation, defense material development, and smart mineral surveillance, facilitate national resource adoption, contribute to deployment reliability, and help implement policies, such as the critical minerals governance policy and refining standards.

What is the Critical Minerals Supply Chain?

Critical minerals supply chain refers to an integrated, automated network that combines robotics, artificial intelligence, and high-throughput mineral processing tools to execute the exploration-extraction-refining-recycling cycle for strategic mineral resources. These systems use automated sorting, leaching, solvent extraction, and analytical technologies to enable rapid grade engineering, improved recovery accuracy, and accelerated prototyping and scale-up of mineral processing. Critical minerals supply chains are increasingly used in battery manufacturing and electronics R&D to enhance process efficiency, support domestic production development, and advance the production of refined chemicals and materials.

How AI Is Transforming the Global Critical Minerals Supply Chain Market?

Artificial intelligence is revolutionizing the field of critical minerals, allowing predictive modeling of the likelihood of refining pathway success, automatic detection of anomalies in leaching data patterns, and optimization of extraction design parameters in a mineral-specific scenario. Refinery-generated telemetry and mineralogy data can be processed using AI algorithms to identify any degradation or performance drift and optimize production outcomes at scale. This saves time, is verifiable and cheaper than manual data analysis.

Moreover, AI enhances process assurance through offering adaptive computational event-based scheduling, anticipating workflow threats to extraction accuracy, and intelligent prioritization of mineral processing module health monitoring. It is also involved in reducing the cost of baseline testing and ongoing performance tracking, allowing mineral processing IT operators to reduce the cost and physical footprint of on-prem test campaigns and improve the reliability of critical minerals workloads and their financial returns.

Value Chain Stage Analysis

Mining and extraction will retain the largest share of the critical minerals supply chain, accounting for 61.4%, as every downstream activity depends on primary ore availability and grade. UNCTAD notes that a few mining hubs dominate global supply: in 2025 the Democratic Republic of the Congo supplied 74% of cobalt ore, Indonesia 67% of nickel ore, and China 69% of rare earths mine output, underscoring how value creation starts at the pit. The IEA reports tight supply and rebounding prices for critical minerals through 2026, reinforcing continued capex into mining as the economic bottleneck of the entire chain.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Meanwhile, the Refining & Chemical Processing segment is witnessing strong growth, driven by rising demand for purified battery-grade materials and government incentives for domestic refining capacity in the US and Europe. Adoption is further supported by workflow optimization, real-time efficiency improvements, and modular configurations that integrate multiple process logic types for improved workflow flexibility and operator satisfaction.

Mineral Type Analysis

Lithium is set to command a leading share of critical minerals, at 27.2%, by 2026 because it is chemically indispensable to high-energy-density rechargeable batteries powering EVs and grid-scale storage. Lithium demand rose nearly 30% in 2024, far outpacing other energy minerals, as surging EV sales and storage projects accelerated. UNCTAD projects lithium demand to increase 353% between 2024 and 2040, with clean technologies' share of lithium use rising from 62% to 87%. This tight, battery-driven demand pipeline structurally channels capital and volume toward lithium.

Application Analysis

Electric vehicles and battery systems are set to command the largest application share in the critical minerals supply chain, at 44.2%, because they are the single biggest demand sink for battery metals such as lithium, nickel, cobalt and graphite. The IEA projects mineral demand from EVs and battery storage to grow at least thirtyfold by 2040 in climate-aligned scenarios, making this the dominant growth engine for critical minerals. The Global EV Outlook confirms that soaring EV sales are directly driving battery production and associated mineral demand, structurally concentrating value in this segment.

The Global Critical Minerals Supply Chain Market Report is segmented based on the following:

By Value Chain Stage

- Mining & Extraction

- Refining & Chemical Processing

- Material Conversion & Component Manufacturing

- Recycling & Secondary Supply

- Logistics, Trading & Distribution

By Mineral Type

- Lithium

- Nickel

- Cobalt

- Copper

- Rare Earth Elements

- Graphite

- Manganese

- Others

By Application

- Electric Vehicles & Battery Systems

- Energy Storage Systems

- Renewable Energy

- Electronics & Semiconductors

- Aerospace & Defense

- Industrial Applications

Regional Analysis

Leading Region in the Critical Minerals Supply Chain Market

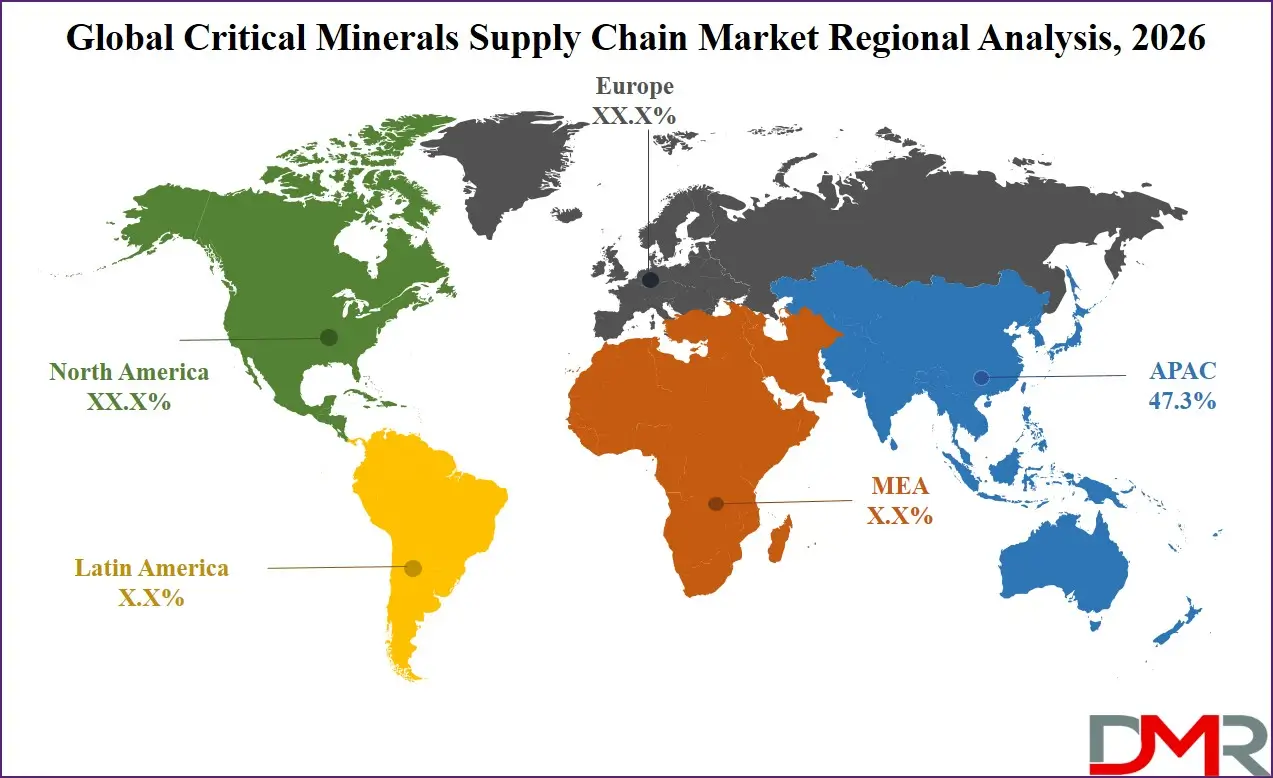

It is projected that Asia-Pacific will take the lead in the global critical minerals supply chain market (by value), covering a market share of about 47.3% in the year 2026. The region's dominance is driven by concentrated refining capacity in China for lithium, cobalt, and rare earths, large-scale battery manufacturing across China, South Korea, and Japan, strong government-backed resource initiatives (e.g., China's strategic minerals stockpiling, Japan's Society 5.0, India's critical minerals mission), and the presence of major mining and refining companies. The widespread adoption of advanced automation and AI-based mineral processing for battery metals and electronics further strengthens Asia-Pacific's leading position in the market. Additionally, continuous investments in downstream material conversion and recycling infrastructure are further reinforcing regional supply chain leadership.

Fastest-Growing Region in the Critical Minerals Supply Chain Market

North America is the fastest-growing region, supported by aggressive domestic refining capacity buildout under the Inflation Reduction Act, increasing resource sovereignty initiatives (US National Critical Minerals Initiative, Canadian Critical Minerals Strategy), rising investments in domestic mining and refining capabilities, and growing adoption of automated extraction and recycling systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The region benefits from substantial federal funding for new refineries and battery material plants, increasing commercial participation from automotive OEMs directly securing supply chains, and alignment with national defense and energy roadmaps. Countries across the region are actively deploying critical minerals supply chains to reduce import dependence and strengthen processing infrastructure. Growing emphasis on rare earth separation and lithium refining further accelerates market expansion in the region.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Market Dynamics

Key Drivers

Rapid developments in Machine Learning and Real-Time Processing Inference

The market is being pushed by a fast uptake of AI-driven grade and refining optimization, high-efficiency mineral processing data processing, API-based interoperability with digital mine logs and laboratory information management systems (LIMS), and real-time telemetry analytics from leach reactors and concentrators. These technologies enable monitoring of the performance of mineral processing systems in real-time, identify process anomalies early, predict recovery rates, and simplify the process of experimental validation. Consequently, operational uptime and R&D efficiency are highly enhanced while minimizing the costs of manual data analysis. The growth of machine learning models for refining design, in particular, is also accelerating the need for intelligent mineral processing automation, as mining operators are increasingly adopting automation and workflow optimization based on mineral processing data.

Growing Focus on Mineral Processing Regulation and Sustainable Supply Chains

The world is increasingly focused on mineral processing safety and quality, with governments and regulatory bodies introducing refining efficiency frameworks, such as the EU Critical Raw Materials Act provisions and the US DOE's Advanced Manufacturing Technologies framework for battery materials. These structures are driving demand for efficient mineral processing automation capable of supporting real-time process monitoring and continuous learning. In parallel, global initiatives promoting supply chain standardization and workforce development are encouraging the adoption of evidence-based mineral processing architectures. The increasing focus on transparency in refining design and reduction in production failure rates is also enhancing the necessity of reliable and scalable mineral processing automation in both public and private supply chain systems.

Market Restraints

High Costs of Integration and Process Validation

Mineral processing platforms are expensive and time-intensive to implement, need to be heavily tested in production settings, process logic reliability needs to be tested, and long-term performance evaluation of new components is needed. Also, regulatory limitations and data privacy regulations (e.g., trade secret protections, resource nationalism laws) add to the complexity and cost of deployment. These aspects pose barriers to entry, lengthen deployment, and raise initial capital investments.

Limited Standardization Across Mineral Processing Data and Workflows

The industry continues to rely on multiple mineral processing automation architectures, including robotics-based, AI-based for process optimization, and sensor-based for ore sorting. However, the lack of standardized mineral processing data interfaces remains a key challenge. The industry lacks universal plug-and-play standards compared to traditional refining modules, making integration complex and limiting interoperability of mineral processing models across different R&D and production systems.

Growth Opportunities

Expansion of Emerging Mining Programs

Developing mining markets such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are investing in digital mineral processing infrastructure and advanced critical minerals capabilities. These regions present strong growth potential due to increasing demand for automated grade development, refining monitoring, and remote mineral processing consultation applications. With limited legacy refining infrastructure, they provide opportunities for the deployment of modern mineral processing automation optimized for R&D and production environments.

Rising Demand for Cloud-Based Supply Chain Deployment

The increased requirement for advanced mineral processing automation is being generated by the growth of remote R&D collaboration, distributed refining, and real-time process control applications. These technologies play a vital role in virtual mineral processing platforms, remote production facilities, and mining innovation hubs. With the rising importance of sub-hour process latency as a major production concern, cloud-based mineral processing inference capabilities are likely to be fundamental to future mineral processing and mining IT infrastructure.

Market Trends

Predictive Mineral Recovery Monitoring and Computational Analytics

Mineral processing platforms are being monitored and process logic anomalies are detected in real time, and recovery override patterns are predicted using on-system learning. The use of digital twin models of refining circuits and machine learning algorithms is enhancing process workflow scheduling, system lifespan, and deployment reliability. This shift is transforming mineral processing management from manual data review to a fully automated, continuously optimized system for monitoring.

Cloud-Based Telemetry and Fleet Management Systems

Cloud computing and digital twin technologies are taking centre stage in the operations of mineral processing clusters. These platforms enable real-time storage and analysis of mineral processing performance data, centralized fleet management of automated processing cells, and remote monitoring of mineral processing module health. Cloud-based systems enhance transparency, lower on-prem infrastructure expenses, and provide quicker responses to workflow changes across R&D sites, as experienced by operators of large mineral processing networks.

Competitive Landscape

The critical minerals supply chain market is highly competitive, with innovation and strategic alliances shaping the competitive environment. In order to achieve a competitive advantage, companies and research labs are focused on the development of advanced automation architectures (e.g., AI-based refining design, robotics for high-throughput mineral sorting, and machine learning for process optimization), AI-powered mineral processing telemetry, and digital twin-enabled process monitoring platforms. There are high barriers to entry due to capital-intensive process validation infrastructure, specialized mineral processing expertise, and the need for mature software ecosystems and mining regulatory and procurement compliance.

Strategic approaches in the market to increase market presence include partnerships with battery manufacturers and mining companies, mergers between automation solution providers and system integrators, and long-term support contracts with R&D labs and academic institutions. Moreover, research and development in interoperability frameworks and scalable software architectures are important factors in maintaining competitiveness and addressing the evolving needs of the critical minerals industry.

Some of the prominent players in the Global Critical Minerals Supply Chain Market are:

- BHP Group Limited

- Rio Tinto Group

- Glencore plc

- Vale S.A.

- Freeport-McMoRan Inc.

- Anglo American plc

- China Minmetals Corporation

- Albemarle Corporation

- Sociedad Química y Minera de Chile S.A.

- Tianqi Lithium Corporation

- Ganfeng Lithium Group Co., Ltd.

- Pilbara Minerals Limited

- Lithium Americas Corp.

- MP Materials Corp.

- Lynas Rare Earths Limited

- China Northern Rare Earth Group High-Tech Co., Ltd.

- Iluka Resources Limited

- Neo Performance Materials Inc.

- Energy Fuels Inc.

- Nornickel

- Other Key Players

Recent Developments

- April 2026: Albemarle Corporation reported strong lithium demand growth driven by EV and energy storage markets, with lithium prices rebounding sharply in 2026. The company also expanded cost efficiency programs and reaffirmed long-term lithium demand growth expectations of 15–40% annually.

- November 2025: Ganfeng Lithium Group Co., Ltd. expanded its global lithium asset portfolio by advancing development of new lithium brine and hard-rock projects in Argentina and Africa, reinforcing its position as one of the world's largest integrated lithium producers amid rising demand from electric vehicle battery manufacturers.

- April 2025: MP Materials Corp. expanded domestic rare earth processing capacity in the United States by commissioning new separation facilities at its Mountain Pass site, increasing output of high-purity rare earth elements used in EV motors, defense systems, and electronics.

- April 2026 - Critical Metals Corp announced an all-share acquisition of European Lithium valued at approximately $835 million. The deal consolidates upstream spodumene and hydroxide assets across Europe and Australia.

- April 2026 - The United States and European Union signed a Strategic Partnership MOU on critical minerals. The joint Action Plan includes price floors, offtake mechanisms, and stockpiling cooperation frameworks.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 355.2 Bn |

| Forecast Value (2035) |

USD 679.7 Bn |

| CAGR (2026–2035) |

7.5% |

| The US Market Size (2026) |

USD 58.3 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Value Chain Stage (Mining & Extraction, Refining & Chemical Processing, Material Conversion & Component Manufacturing, Recycling & Secondary Supply, Logistics, Trading & Distribution), By Mineral Type (Lithium, Nickel, Cobalt, Copper, Rare Earth Elements, Graphite, Manganese, Others), By Application (Electric Vehicles & Battery Systems, Energy Storage Systems, Renewable Energy, Electronics & Semiconductors, Aerospace & Defense, Industrial Applications) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Critical Minerals Supply Chain Market?

▾ The Global Critical Minerals Supply Chain Market size is estimated to have a value of USD 355.2 billion in 2026 and is expected to reach USD 679.7 billion by the end of 2035.

What is the CAGR of the Global Critical Minerals Supply Chain Market from 2026 to 2035?

▾ The market is growing at a CAGR of 7.5% over the forecasted period.

What factors are driving the growth of the Global Critical Minerals Supply Chain Market?

▾ The market is driven by advancements in machine learning-based refining optimization, real-time processing analytics, regulatory pressure to expand refining capacity, and increasing government investment in critical mineral infrastructure.

What are the major trends in the Global Critical Minerals Supply Chain Market?

▾ The key market trends include the adoption of predictive mineral recovery monitoring and real-time refining control, along with a growing shift toward cloud-based mineral processing platforms and telemetry-enabled workflow management systems.

Which region held the largest share of the Global Critical Minerals Supply Chain Market in 2026?

▾ Asia Pacific is expected to account for the largest market share in 2026, at about 47.3%.

Which region is expected to grow the fastest in the Global Critical Minerals Supply Chain Market?

▾ North America is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Critical Minerals Supply Chain Market?

▾ Some of the major key players in the Global Critical Minerals Supply Chain Market are Albemarle Corporation, Ganfeng Lithium Group, Glencore plc, Lynas Rare Earths, MP Materials, and many others.

How is the Global Critical Minerals Supply Chain Market segmented?

▾ The market is segmented by value chain stage, mineral type, and application.