What is the Demineralized Bone Matrix (DBM) Market Size?

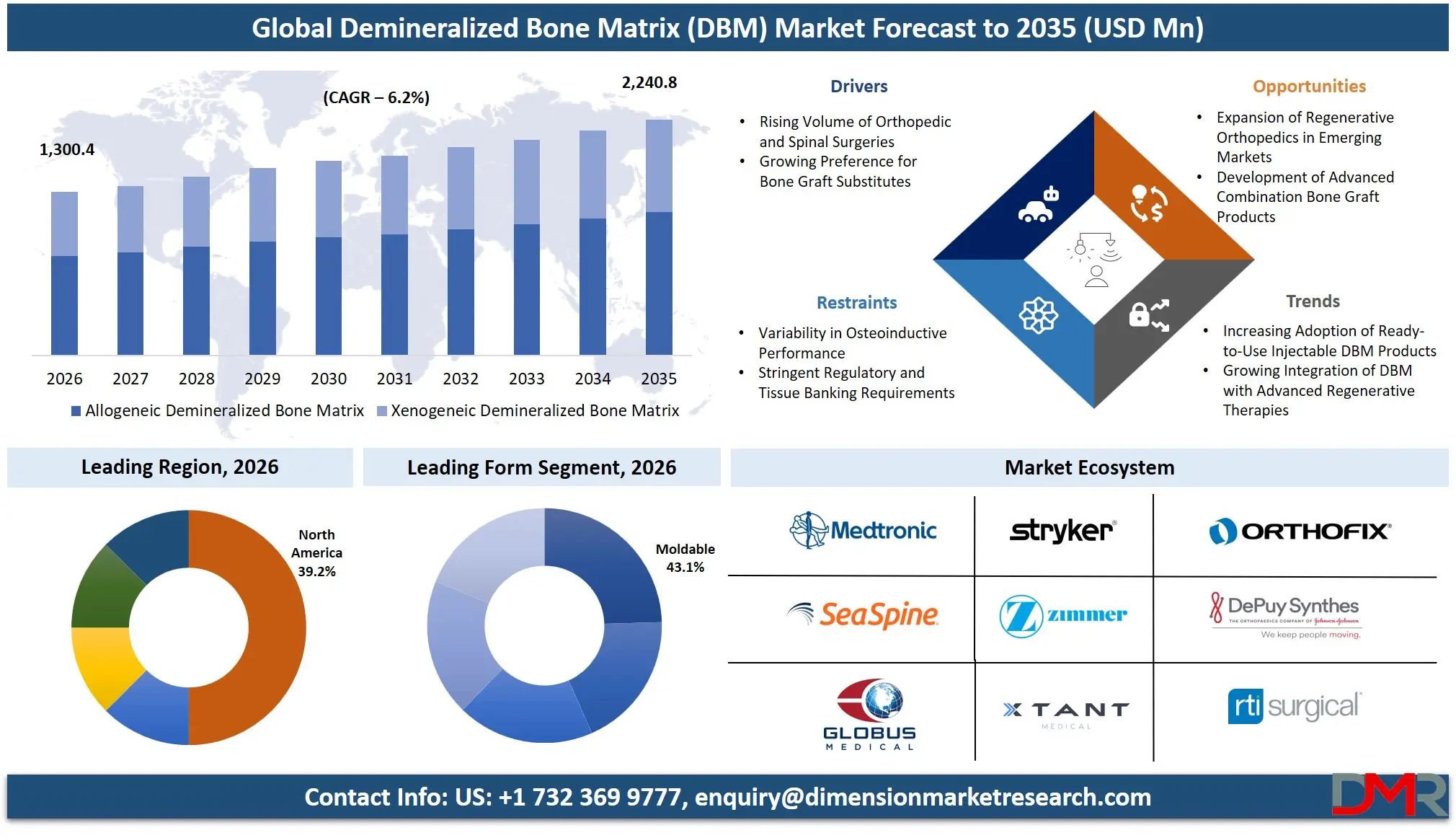

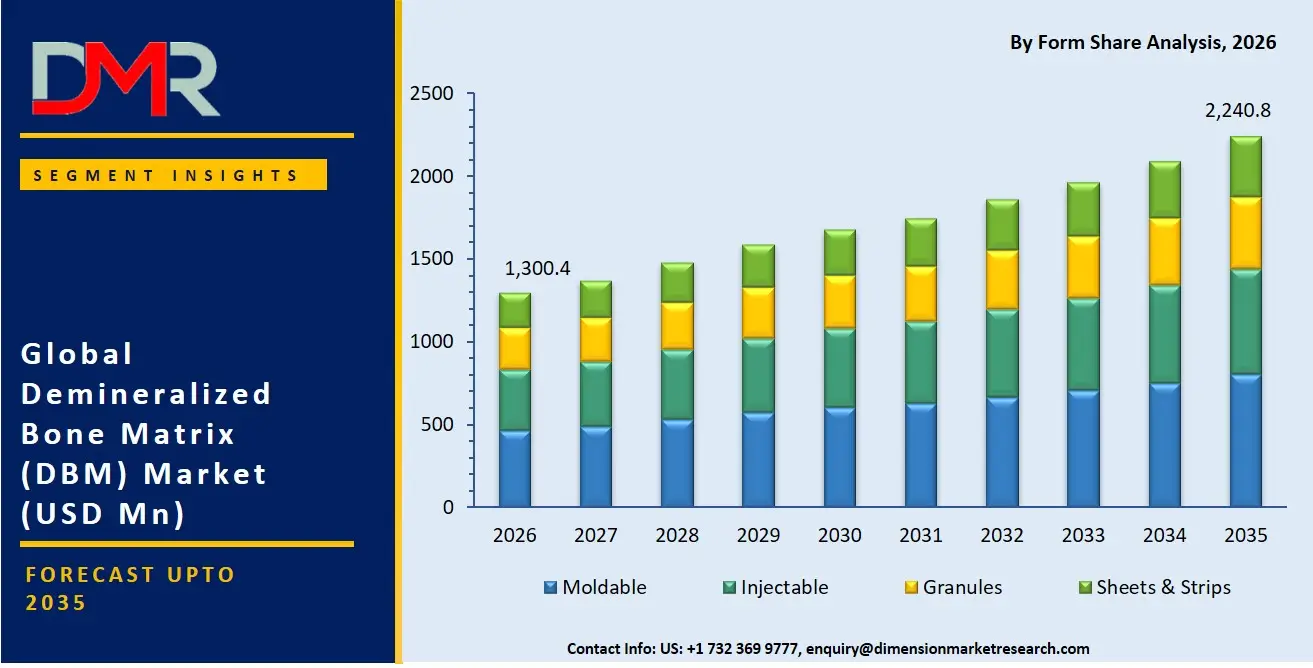

The Global Demineralized Bone Matrix (DBM) Market is expected to reach a value of USD 1,300.4 million in 2026, and it is further anticipated to reach USD 2,240.8 million by 2035, growing at a CAGR of 6.2% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The demineralized bone matrix market has been growing at a steady rate, driven by the rising global prevalence of musculoskeletal disorders and a demographic shift toward an aging population. The market consists of a variety of bone graft substitutes processed from allogeneic or xenogeneic bone, which are utilized to confer osteoconductive and osteoinductive properties required for bone regeneration. The increasing demand to support complex spinal fusion procedures, address traumatic bone defects, and facilitate maxillofacial reconstruction is driving the necessity of specialized DBM products. Orthopedic surgeons and dental specialists are the most frequent adopters, with moldable putties and injectable formulations remaining the most popular because of their intraoperative handling versatility and biocompatibility. The hospital, specialized orthopedic and dental clinics, and ambulatory surgical center segments are key adopters, as they require safe, effective, and clinically validated bone healing solutions.

The US Demineralized Bone Matrix (DBM) Market

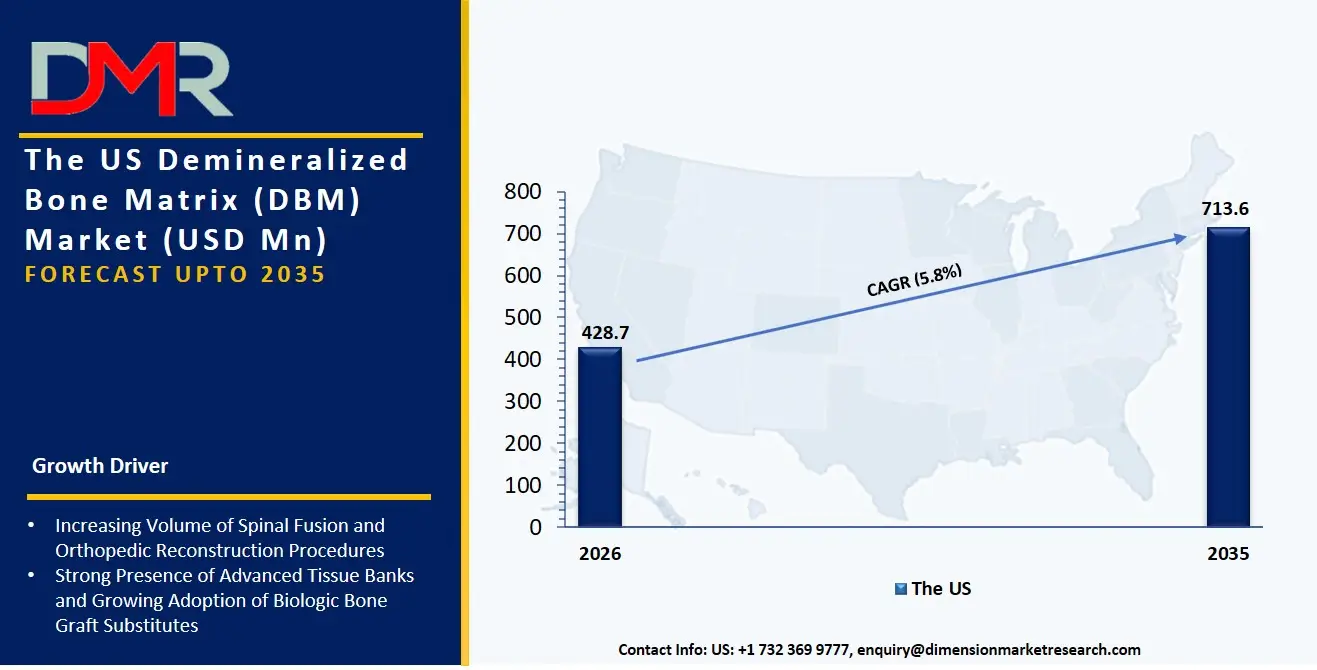

The US Demineralized Bone Matrix (DBM) Market is projected to reach USD 428.7 million in 2026 at a compound annual growth rate of 5.8% over its forecast period, culminating in a value of USD 713.6 million by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US continues to be the largest and most developed market for demineralized bone matrix due to a high surgical volume for spinal arthrodesis and a robust regulatory framework that expedites the clearance of novel tissue-based products. The market has been typified by high demand for moldable putty and injectable DBM products, whereby surgeons are aiming for minimally invasive delivery methods that reduce operative time and donor site morbidity. Besides, the development of advanced DBM composites combined with autograft extenders is producing a similar need in trauma and sports medicine applications to optimize the fusion rate and mechanical stability in load-bearing defects.

The Europe Demineralized Bone Matrix (DBM) Market

The Europe Demineralized Bone Matrix (DBM) Market is estimated to be valued at USD 364.1 million in 2026 and is further anticipated to reach USD 627.4 million by 2035 at a CAGR of 6.2%. The regulatory frameworks including the EU Medical Device Regulation (MDR) and national tissue banking directives have a significant impact on the European market, driving the need to employ high-quality allogeneic DBM products with rigorous safety profiles. Accelerated growth of dental bone grafting services is also being experienced in the region as the dental tourism sector in Germany, Spain, and Hungary seeks to incorporate advanced osteoinductive biomaterials for predictable implantology outcomes. In addition, the push for value-based healthcare is challenging service providers to create dedicated clinical training programs to ensure optimal handling characteristics and reproducible outcomes across European surgical ecosystems.

The Japan Demineralized Bone Matrix (DBM) Market

The Japan Demineralized Bone Matrix (DBM) Market is projected to be valued at USD 90.0 million in 2026 at a CAGR of 6.2%. The Japanese market is unique, with a corporate drive to address super-aged societal challenges in response to a steep rise in osteoporotic fragility fractures and degenerative spinal disease. Bioactive bone void fillers and moldable DBM forms make up a large part of the spending as surgeons seek alternatives to iliac crest bone graft harvesting for lumbar interbody fusion. There is also a strong need to integrate deeply with the local market to bridge the gaps between traditional surgical preferences and new injectable, self-setting scaffolds, which forms a niche in patient-specific craniomaxillofacial and foot & ankle surgeries.

Key Takeaways

- Market Size & Forecast: The Global Demineralized Bone Matrix (DBM) market is projected to reach USD 1,300.4 million in 2026, expanding to USD 2,240.8 million by 2035, fueled by the dual drivers of advanced bone graft delivery technology and the escalating surgical management of degenerative bone diseases.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 6.2%, driven by a continuous shift from autograft to allograft-based solutions and the escalating complexity of managing critical-sized bone defects in a compromised host environment.

- Primary Growth Drivers: Key forces include the widespread adoption of minimally invasive surgical techniques requiring injectable and moldable DBM forms, the need for composite grafting solutions to avoid the morbidity of secondary harvest sites, and the integration of validated osteoinductive potential assessment as a critical quality metric for product selection.

- Key Market Trends: Major trends include the development of procedure-specific DBM products (e.g., foot & ankle, craniomaxillofacial blocks), the use of optimized carrier technology within injectable pastes to resist irrigation washout, and the shift toward next-generation allogeneic products as regulators prioritize stringent donor screening and terminal sterilization protocols.

- By Application Analysis: Spinal Fusion models are expected to dominate clinical demand due to the critical need for a biological scaffold to achieve a solid interbody union. DBM products are increasingly required to provide a balanced osteoinductive signal that complements rigid instrumentation in posterolateral gutter and transforaminal lumbar interbody fusion (TLIF) procedures.

- By End User Analysis: Hospitals and Orthopedic Clinics are the most lucrative end-user segments due to the high incidence of total joint arthroplasty complications requiring revision. Dental Clinics represent the fastest-growing sector as socket preservation and ridge augmentation procedures require robust particulate and moldable grafts for predictable osseointegration.

- Regional Leadership: North America is poised to dominate this market with 39.2% of the market share in 2026 due to its well-developed biotechnology ecosystem that utilizes advanced tissue processing infrastructure to its fullest and makes it a leader in this market.

What is the Demineralized Bone Matrix (DBM)?

Demineralized Bone Matrix (DBM) represents a specialized category of osteoinductive and osteoconductive bone graft substitutes that are offered by tissue banks and musculoskeletal biologics companies to assist surgeons in restoring skeletal integrity. These products, unlike structural allografts (which provide load-bearing support), are related to the biological signaling of bone formation. This involves processed cortical bone that has undergone acid extraction to expose underlying bone morphogenetic proteins (BMPs) and growth factors. With over 60% of graft procedures incorporating a biological component, DBM products are needed to achieve cost-effective, shelf-stable osteogenesis, translating a donor's biologic potential into tangible clinical fusion and bone healing, as opposed to mere void filling.

Use Cases

- Multilevel Spinal Arthrodesis in Geriatrics: Spine surgeons hire specialized DBM Putty with Chips products to extend the volume of locally harvested autograft in patients with poor bone quality, providing an osteoinductive stimulus critical for bridging long-segment fusions without iliac crest morbidity.

- Alveolar Ridge Augmentation in Implantology: Periodontists use injectable DBM pastes and moldable gels to fill extraction sockets and buccal plate defects, preparing the bony architecture to receive dental implants by preserving native bone volume and density.

- Non-Union Fracture Management in Trauma: Orthopedic trauma surgeons utilize DBM fibers and chips combined with a carrier to create a biologically active periosteal-like graft that jumpstarts the stalled healing cascade in atrophic non-unions of the tibia or humerus.

- Foot & Ankle Arthrodesis: Podiatric surgeons use DBM paste and putty formulations to pack subtalar and ankle fusion sites, where the mechanical environment of compressive fixation is ideal for DBM's biological properties, providing a safe alternative to standalone autograft.

How AI is Transforming the Demineralized Bone Matrix (DBM) Market?

AI is changing the demineralized bone matrix sector by accelerating the processing quality assurance, as well as enhancing surgical planning efficacy. In donor-to-recipient matching, AI-based imaging analysis tools have the potential to automatically verify cortical bone architecture and DBM particle geometry, greatly minimizing the risk of batch variability and ensuring reproducible osteoinductive potential. Meanwhile, AI-powered algorithms in clinical outcome tracking allow manufacturers to better correlate specific DBM formulation properties with fusion rates by detecting subtle patterns in postoperative CT scans, predicting subsidence risk, and suggesting formulation adjustments to reinforce evidence-based surgical protocols.

Tissue processing and business development projects are also revolving around AI. In the area of product development, intelligent simulation software is used to continuously model the impact of varying particle size distributions on cellular migration and vascular ingrowth, identifying optimal pore structures that keep organizations in line with surgical handling expectations. Moreover, generative AI assistants are complementing surgeon education by simulating fusion procedures and modeling expected graft remodeling timelines to give stakeholders a visualization of the biological healing cascade before committing to a specific DBM product type.

Market Dynamics

Key Drivers in the Global Demineralized Bone Matrix (DBM) Market

Rising Volume of Orthopedic and Spinal Surgeries

The increasing incidence of degenerative bone diseases, traumatic fractures, spinal disorders, and age-related musculoskeletal conditions is significantly driving demand for demineralized bone matrix products. An expanding elderly population, coupled with higher rates of osteoporosis and osteoarthritis, has resulted in greater numbers of spinal fusion, trauma reconstruction, and joint repair procedures. DBM serves as an effective bone graft substitute or extender by promoting bone regeneration while reducing the need for autograft harvesting. As healthcare systems continue expanding orthopedic care capabilities and surgeons increasingly adopt biologic graft materials, demand for DBM products continues to grow steadily across global healthcare markets.

Growing Preference for Bone Graft Substitutes

Surgeons are increasingly shifting toward bone graft substitutes that minimize complications associated with autograft harvesting, including donor-site pain, infection risk, prolonged surgery, and limited graft availability. Demineralized bone matrix provides osteoinductive potential while offering convenient handling characteristics and broad applicability across multiple orthopedic procedures. Continuous improvements in tissue processing technologies have enhanced product consistency, sterility, and clinical performance, strengthening physician confidence. In addition, expanding awareness of regenerative medicine and biologic solutions has encouraged healthcare providers to integrate DBM into routine surgical practice, supporting sustained market expansion across developed and emerging healthcare systems worldwide.

Restraints in the Global Demineralized Bone Matrix (DBM) Market

Variability in Osteoinductive Performance

One of the major challenges facing the DBM market is the variability in osteoinductive performance resulting from differences in donor characteristics, tissue quality, and processing techniques. Variations in bone morphogenetic protein content and demineralization procedures can influence clinical effectiveness between products from different manufacturers. Such inconsistencies may affect surgeon confidence and create concerns regarding predictable treatment outcomes. Although regulatory standards and quality control measures continue improving, achieving uniform biological activity across all tissue-derived products remains difficult, limiting wider clinical acceptance in highly standardized surgical environments requiring consistent regenerative performance.

Stringent Regulatory and Tissue Banking Requirements

The production and commercialization of DBM products are subject to rigorous regulatory oversight governing donor screening, tissue procurement, processing, sterilization, storage, and distribution. Compliance with tissue banking standards increases manufacturing complexity and operational costs while extending product approval timelines. Maintaining traceability and ensuring biological safety require significant investments in quality management systems and specialized infrastructure. Additionally, regulatory requirements vary across countries, creating challenges for manufacturers seeking international expansion. These compliance burdens may delay product launches, increase production expenses, and limit market participation, particularly for smaller companies with limited regulatory resources.

Growth Opportunities in the Global Demineralized Bone Matrix (DBM) Market

Expansion of Regenerative Orthopedics in Emerging Markets

Rapid improvements in healthcare infrastructure, increasing orthopedic procedure volumes, and expanding access to advanced surgical treatments across emerging economies present significant growth opportunities for DBM manufacturers. Rising healthcare expenditure, improving insurance coverage, and greater availability of specialized orthopedic centers are supporting wider adoption of biologic bone graft materials. Governments are investing in modern healthcare facilities while private hospitals continue expanding orthopedic services. As awareness of regenerative medicine grows among surgeons and patients, demand for DBM products is expected to increase substantially across Asia-Pacific, Latin America, and parts of the Middle East.

Development of Advanced Combination Bone Graft Products

Manufacturers are increasingly developing next-generation DBM formulations combined with synthetic biomaterials, stem cell technologies, growth factors, and advanced carrier materials to improve bone regeneration outcomes. These innovative products aim to provide enhanced osteoinductive potential, improved graft stability, better handling characteristics, and faster healing. Continued investment in biomaterials research and regenerative medicine is creating opportunities to expand DBM applications beyond traditional orthopedic procedures into complex reconstructive surgeries. Strategic collaborations between tissue banks, biotechnology companies, and medical device manufacturers are expected to accelerate commercialization of advanced combination bone graft solutions worldwide.

Trends in the Global Demineralized Bone Matrix (DBM) Market

Increasing Adoption of Ready-to-Use Injectable DBM Products

A prominent trend in the DBM market is the growing adoption of ready-to-use injectable formulations that simplify surgical procedures and improve handling efficiency. Injectable DBM enables minimally invasive delivery, precise placement within bone defects, and reduced operating time while maintaining osteoinductive potential. These products are increasingly used in spinal fusion, trauma surgery, and orthopedic reconstruction because they enhance workflow efficiency and reduce preparation requirements in operating rooms. Continuous innovation in carrier materials and viscosity optimization is further improving product performance, making injectable DBM an increasingly attractive option for modern orthopedic surgeons.

Growing Integration of DBM with Advanced Regenerative Therapies

The market is witnessing increasing integration of DBM with regenerative medicine technologies, including stem cells, platelet-rich plasma, bioactive proteins, and tissue engineering approaches. Manufacturers are focusing on multifunctional graft solutions that enhance bone healing while supporting faster tissue regeneration and improved clinical outcomes. Research collaborations between academic institutions, biotechnology firms, and orthopedic companies are accelerating the development of biologically enhanced graft materials. This trend reflects the broader shift toward personalized regenerative therapies, where biologic bone substitutes are designed to deliver superior healing performance for complex orthopedic and reconstructive surgical applications.

Research Scope and Analysis

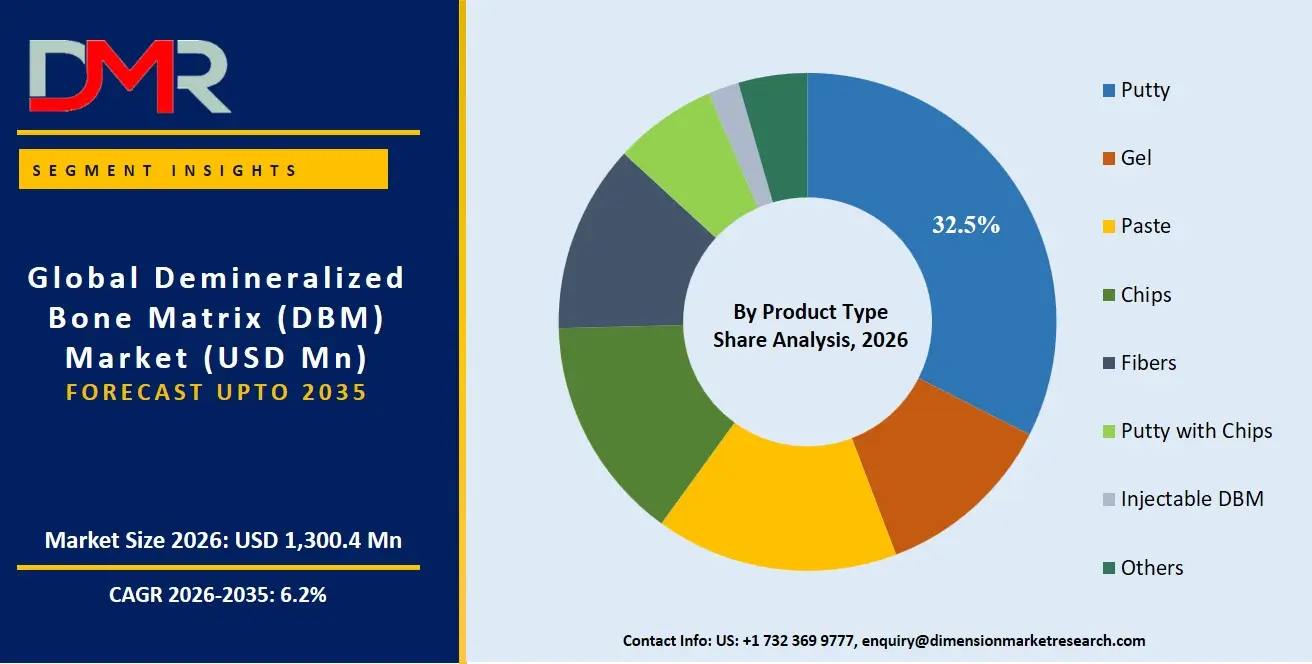

The Global Demineralized Bone Matrix (DBM) Market is segmented by Product Type (Putty, Gel, Paste, Chips, Fibers, Putty with Chips, Injectable DBM, Others), Source (Allogeneic, Xenogeneic), Form (Moldable, Injectable, Granules, Sheets & Strips), Application, Distribution Channel, and End User, addressing diverse orthopedic, spinal, trauma, dental, and reconstructive surgery requirements across healthcare settings worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Type Analysis

Putty is projected to dominates the global Demineralized Bone Matrix (DBM) market due to its superior handling characteristics, moldability, and ability to conform to irregular bone defects during surgery. It is widely preferred by orthopedic and spinal surgeons because it remains in place after implantation, reducing graft migration and simplifying surgical procedures. Putty formulations are frequently combined with carriers that improve osteoconductive performance while maintaining the osteoinductive properties of DBM. Their extensive use in spinal fusion, trauma, and reconstructive surgeries, along with broad product availability from leading manufacturers and favorable clinical outcomes, has established putty as the most widely adopted DBM product type globally.

By Source Analysis

Allogeneic Demineralized Bone Matrix is expected to hold the dominant position because it is sourced from screened human donors and provides clinically proven osteoinductive properties without requiring autograft harvesting. It eliminates donor-site morbidity, shortens operating time, and offers consistent quality through regulated tissue banking processes. Allogeneic DBM is extensively used in orthopedic, spinal, and dental procedures owing to its established safety profile, broad regulatory acceptance, and widespread commercial availability. Healthcare providers prefer allogeneic products because they are supported by strong clinical evidence and standardized processing methods, making them the primary source material across hospitals and specialty surgical centers worldwide.

By Form Analysis

Moldable DBM products is projected to dominate the market because they provide surgeons with excellent flexibility during implantation, allowing the graft to adapt precisely to complex bone defects and irregular anatomical structures. Their ease of handling reduces procedure time while ensuring optimal graft placement and retention.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Moldable formulations are especially preferred in spinal fusion, trauma repair, and orthopedic reconstruction where stability and conformity are essential for successful bone regeneration. Continuous product innovation has enhanced the consistency, viscosity, and biological performance of moldable DBM products, making them the preferred form across a wide range of surgical applications in modern orthopedic practice.

By Application Analysis

Spinal Fusion is poised to represent the leading application segment due to the increasing global prevalence of degenerative spine disorders, spinal deformities, traumatic injuries, and the growing volume of fusion procedures. DBM is widely utilized as a bone graft extender or substitute in spinal surgeries because of its osteoinductive properties and ability to promote successful bone healing while reducing dependence on autografts. Rising adoption of minimally invasive spine procedures and increasing demand from aging populations further support this segment. Continuous advancements in spinal implants and biologic graft materials have strengthened DBM's role in achieving reliable spinal fusion outcomes.

By Distribution Channel Analysis

Direct Sales is expected to dominate the distribution channel segment because manufacturers of DBM products primarily supply hospitals and major healthcare institutions through dedicated sales teams and contractual agreements. This channel ensures product integrity, regulatory compliance, timely delivery, technical support, and effective inventory management for biologic products requiring specialized handling. Direct engagement also enables manufacturers to provide surgeon training, clinical education, and post-sales assistance while maintaining stronger customer relationships. Since DBM products are primarily used in complex surgical procedures requiring consistent quality assurance, healthcare providers generally prefer purchasing directly from manufacturers or their authorized representatives.

By End User Analysis

Hospitals are projected to account for the largest share of the global DBM market because they perform the majority of orthopedic, spinal, trauma, and reconstructive surgeries requiring bone graft materials. Large hospitals possess advanced surgical infrastructure, specialized orthopedic departments, experienced surgeons, and accredited tissue handling capabilities necessary for the safe use of biologic graft products. The growing number of complex musculoskeletal procedures, increasing healthcare expenditure, and availability of reimbursement in many developed countries further support hospital adoption. Additionally, hospitals are typically the primary purchasers through long-term procurement agreements, making them the dominant end-user segment in the global market.

The Global Demineralized Bone Matrix (DBM) Market Report is segmented on the basis of the following:

By Product Type

- Putty

- Gel

- Paste

- Chips

- Fibers

- Putty with Chips

- Injectable DBM

- Others

By Source

- Allogeneic Demineralized Bone Matrix

- Xenogeneic Demineralized Bone Matrix

By Form

- Moldable

- Injectable

- Granules

- Sheets & Strips

By Application

- Spinal Fusion

- Trauma Surgery

- Dental Bone Grafting

- Joint Reconstruction

- Foot & Ankle Surgery

- Craniomaxillofacial Surgery

- Sports Medicine

- Others

By Distribution Channel

- Direct Sales

- Third-Party Distributors

- Online Procurement

By End User

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers (ASCs)

- Dental Clinics

- Specialty Surgical Centers

- Research & Academic Institutes

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

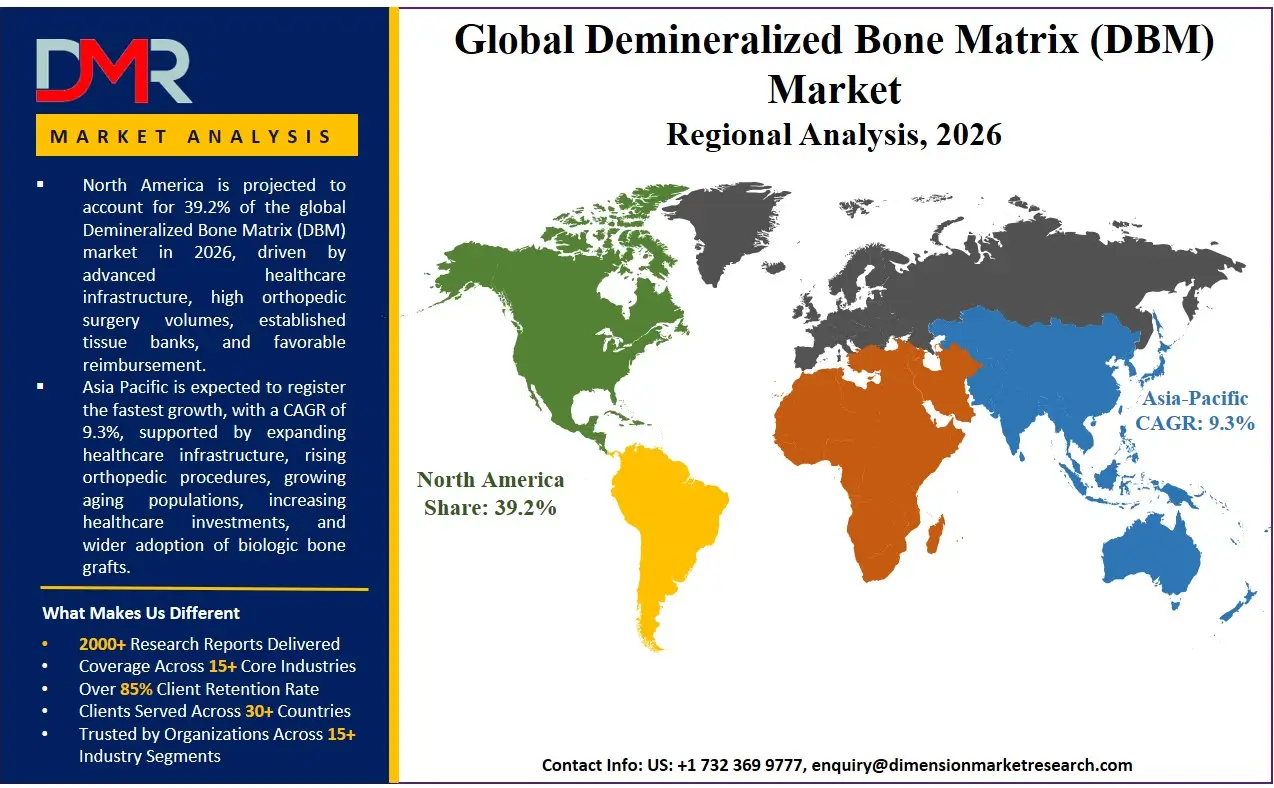

North America is poised to dominate the global demineralized bone matrix market as it is projected to hold 39.2% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the DBM market because of the unmatched concentration of American Association of Tissue Banks (AATB)-accredited processors and the aggressive clinical adoption of biologics for Medicare-age spine patients. The area has an established ecosystem of musculoskeletal biologics innovators, independent tissue banks, and a rich pool of spine and trauma surgeon key opinion leaders. Hospital investment in outpatient spine surgery, advanced image-guided delivery systems, and the overall shift from simple allograft to composite DBM products contribute to the continued demand for moldable and injectable osteoinductive matrices along with continuous training support. Moreover, a positive private health insurance climate for tissue products persistently finances upcoming cost-effectiveness studies that necessitate expert biologic solutions to achieve expeditious clinical outcomes and surgical discharge protocols.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding demineralized bone matrix market, driven by government-led sweeping healthcare infrastructure modernization initiatives in India, China, Japan, and Southeast Asia. The fast-paced growth of medical tourism, the rise of a health-insured middle-income population, and the dynamic expansion of the orthopedic implant sector is compelling established public hospitals and private chains to discard unvalidated allograft sources. Biologics strategy consulting is in high demand to help these large organizations head in the direction of regenerative DBM-based treatment algorithms. There is also a severe lack of local accredited tissue banking capacity in the region, and it is necessary to import premium DBM products with long shelf lives and terminal sterilization to implement safe, modern bone grafting techniques and bridge the supply chain gap for faster investments in advanced surgical biologics projects.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global demineralized bone matrix sector has become highly dynamic with a heterogeneous array of multinational orthopedic giants, specialized tissue-banking organizations, and niche regenerative medicine start-ups. The key to success will be the profound strategic alliances with hospital systems and GPOs because they will open the necessary formulary access and contracted revenue streams. The movement towards market consolidation is rapidly progressing with the traditional spine implant companies acquiring DBM-biologic specialized innovators to stay afloat. Proprietary intellectual property, including validated donor screening assays, carrier technology that resists surgical irrigation, and industry-specific bioactive fiber architectures, is becoming a more important basis of competitive differentiation than just generic lyophilized bone powder or comparable particulate-based approaches.

Some of the prominent players in the Global Demineralized Bone Matrix (DBM) Market are:

- Medtronic plc

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Johnson & Johnson MedTech (DePuy Synthes)

- Orthofix Medical Inc.

- Globus Medical, Inc.

- SeaSpine Holdings Corporation

- Xtant Medical Holdings, Inc.

- RTI Surgical Holdings, Inc.

- Aziyo Biologics, Inc.

- MTF Biologics

- LifeNet Health

- AlloSource

- Arthrex, Inc.

- Bioventus LLC

- Bone Bank Allografts

- Organogenesis Holdings Inc.

- Surgalign Holdings, Inc.

- Hans Biomed Co., Ltd.

- Berkeley Advanced Biomaterials, Inc.

- Other Key Players

Recent Developments

- March 2026: MTF Biologics expanded its demineralized bone matrix portfolio with an advanced moldable DBM formulation designed for spinal fusion and complex orthopedic reconstruction, offering improved graft handling and enhanced defect conformity during surgery.

- November 2025: Orthofix Medical Inc. introduced an updated DBM putty solution featuring improved carrier technology to increase graft stability and ease of application in minimally invasive spine and trauma procedures.

- August 2025: LifeNet Health expanded its tissue processing capabilities by investing in advanced donor tissue manufacturing technologies to improve consistency, sterility, and supply of demineralized bone matrix allografts for global healthcare providers.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1,300.4 Mn |

| Forecast Value (2035) |

USD 2,240.8 Mn |

| CAGR (2026–2035) |

6.2% |

| The US Market Size (2026) |

USD 428.7 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product Type, By Source, By Form, By Application, By Distribution Channel, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Demineralized Bone Matrix (DBM) Market?

▾ The Global Demineralized Bone Matrix (DBM) market is poised to be valued at USD 1,300.4 million in 2026 and is projected to reach USD 2,240.8 million by 2035, driven by the universal need for specialized osteoinductive scaffolds in spinal fusion, bone void filling, and tissue regeneration.

What is the CAGR of the Global Demineralized Bone Matrix (DBM) Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 6.2% from 2026 to 2035, reflecting the accelerating complexity of graft site containment and the persistent clinical demand to avoid autograft-related donor site morbidity.

What factors are driving the growth of the Global Demineralized Bone Matrix (DBM) Market?

▾ Key drivers include the global shift from autograft to allograft alternatives, the imperative to manage critical-sized bone defects, the surgical handling complexity of minimally invasive applications, and the surge in demand for Osteoinductive Putty amid evolving tissue-processing quality standards.

Which region held the largest share of the Demineralized Bone Matrix (DBM) Market in 2026?

▾ North America is projected to hold 39.2% of the market share in 2026, driven by a mature tissue banking ecosystem and aggressive surgical investment in Spinal Fusion and advanced DBM-based composite grafts.

Which region is expected to grow the fastest in the Demineralized Bone Matrix (DBM) Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid healthcare expansion in India, China, and Japan, where Biologics Adoption is critical for transitioning large public hospitals to validated allogeneic bone healing protocols.

What are the major trends in the Global Demineralized Bone Matrix (DBM) Market?

▾ Major trends include the development of composite DBM-Cellular Bone Matrices, the rise of ASC-focused pre-filled delivery systems, the demand for procedure-specific anatomic forms, and the focus on terminal sterilization and enzymatic processing techniques within complex graft formulation environments.

Who are the key players in the Global Demineralized Bone Matrix (DBM) Market?

▾ Key players include orthopedic market leaders like Medtronic, Stryker, and J&J, as well as the tissue bank divisions of MTF Biologics and LifeNet Health, alongside specialized pure-play regenerative medicine innovators like Xtant Medical and VIVEX Biologics.

How is the Global Demineralized Bone Matrix (DBM) Market segmented?

▾ The market is segmented by Product Type, Source, Form, Application, Distribution Channel, and End User.