Market Overview

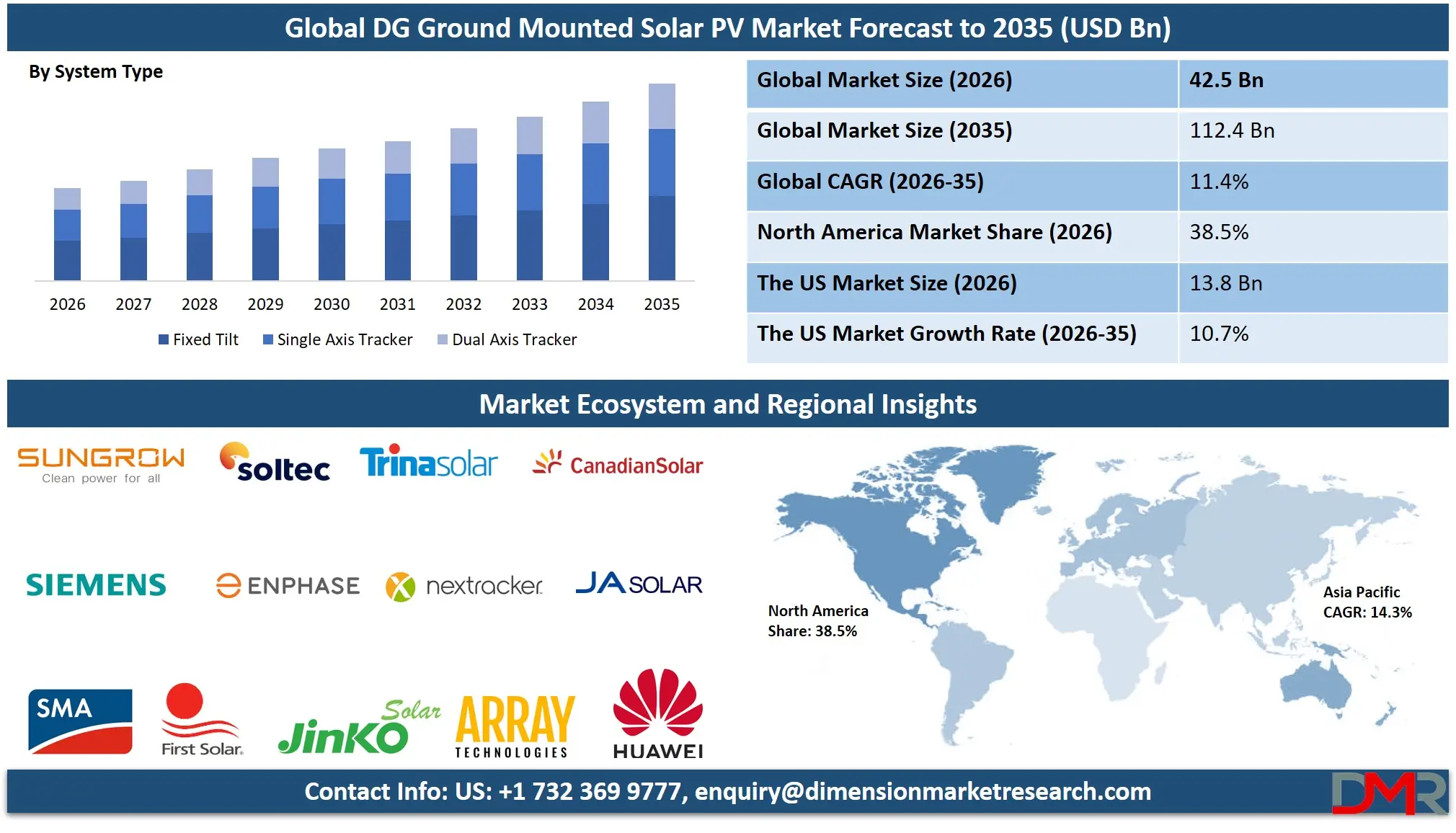

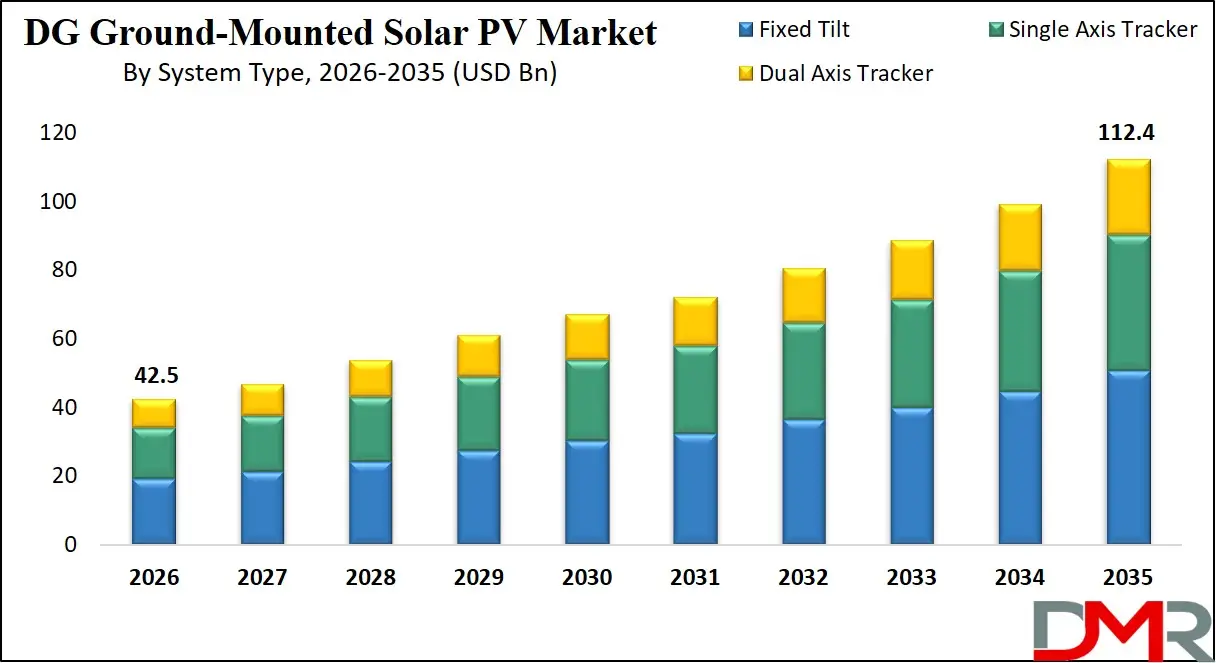

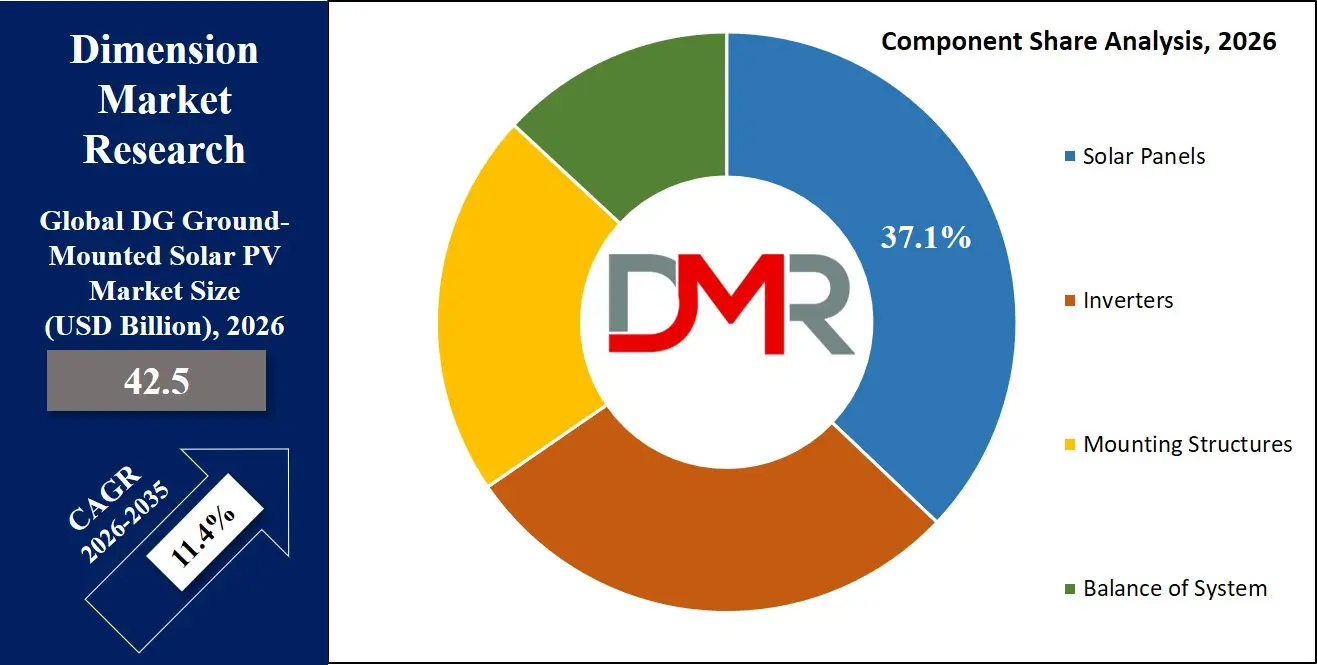

The Global DG Ground Mounted Solar PV Market is projected to reach USD 42.5 billion in 2026 and is expected to grow at a CAGR of 11.4% from 2026 to 2035, attaining a value of USD 112.4 billion by 2035. The market's rapid growth is driven by increasing global emphasis on energy independence, declining Levelized Cost of Electricity (LCOE) for solar, favorable distributed generation policies, and rising corporate procurement of renewable energy through captive and behind-the-meter installations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Distributed generation ground-mounted solar PV enables commercial, industrial, and utility customers to deploy solar arrays directly on owned land parcels, providing direct electricity offset, grid stability benefits, and predictable long-term energy pricing through modular, site-tailored system configurations. The model addresses critical industry challenges related to transmission infrastructure bottlenecks, rising grid tariffs, and energy security concerns, supporting businesses and public institutions in achieving decarbonization and cost reduction targets.

Technological advancements, including bifacial solar modules, high-power density inverters, AI-driven trackers, digital twin-based plant modeling, and advanced SCADA integration for distributed asset management, are transforming the market into a highly efficient and digitally optimized ecosystem. Integration of machine learning algorithms for soiling loss prediction, predictive O&M scheduling, and real-time performance optimization is reshaping distributed solar reliability and bankability.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government initiatives promoting decentralized renewable generation, net metering frameworks, and green hydrogen hybridization in C&I parks further accelerate global adoption. However, barriers such as land availability constraints, interconnection backlogs, variable tariff policies, and supply chain concentration in module manufacturing remain. Despite these limitations, the convergence of PV technology, digital energy platforms, and decentralized financing models positions DG ground mounted solar as a central driver of global energy transition through 2035.

The US DG Ground-Mounted Solar PV Market

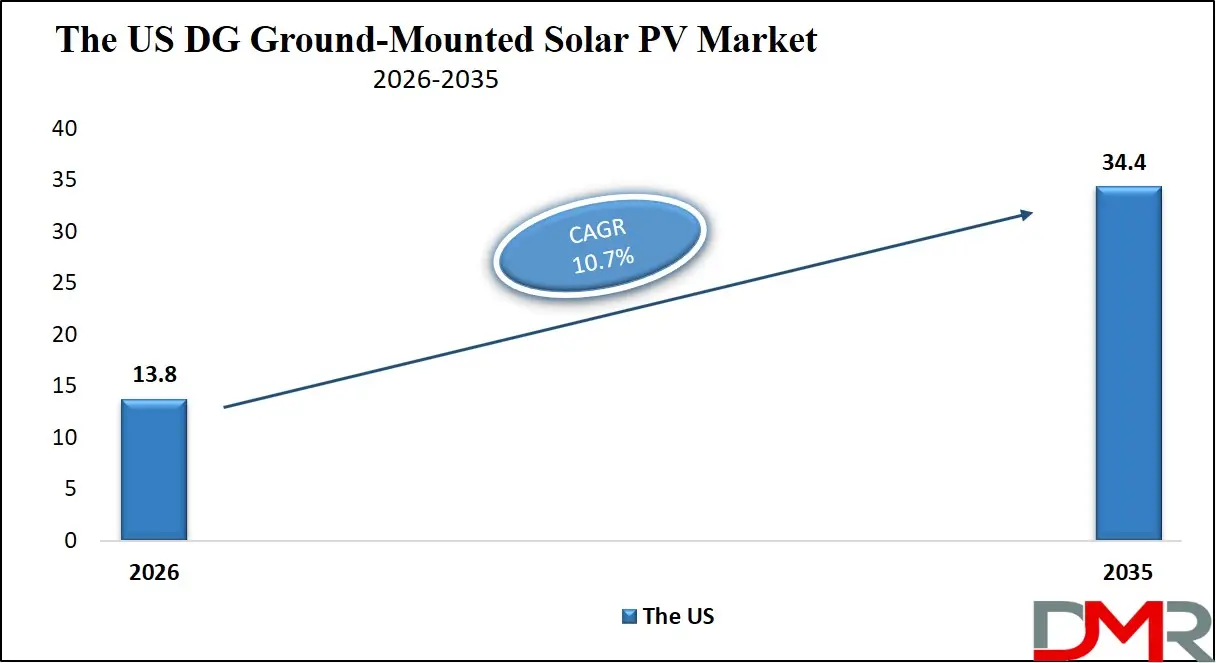

The U.S. DG Ground Mounted Solar PV Market is projected to reach USD 13.8 billion in 2026 and grow at a CAGR of 10.7%, reaching USD 34.4 billion by 2035. The U.S. leads global adoption due to its robust investment tax credit (ITC) extension, strong C&I renewable procurement commitments, and rapid build-out of community solar programs targeting underserved customer segments.

The accelerating corporate net zero pledges, coupled with rising utility tariffs in key commercial hubs, fuels demand for behind-the-meter ground mount solar among Fortune 500 manufacturers, data center operators, and retail chains. Major corporations such as Amazon, Walmart, and Meta are anchoring large-scale DG ground mount portfolios to power distribution centers and logistics hubs directly.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. regulatory support under the Inflation Reduction Act, including direct pay provisions and domestic content adders, encourages investment in locally manufactured components. Emerging state-level policies in California, Texas, and New York mandating solar on commercial properties further solidify long-term demand visibility.

The rapid rise of solar-plus-storage ground mount configurations, advanced tracker optimization software, and standardized mounting solutions for brownfield development continues to redefine the U.S. distributed generation landscape, positioning the country as a global leader in C&I solar deployment.

The Europe DG Ground-Mounted Solar PV Market

The Europe DG Ground Mounted Solar PV Market is projected to be valued at approximately USD 9.7 billion in 2026 and is projected to reach around USD 24.1 billion by 2035, growing at a CAGR of about 10.7% from 2026 to 2035. Europe's leadership is anchored by strong regulatory emphasis on energy sovereignty, REPowerEU targets, and accelerated permitting for decentralized renewables.

Countries such as Germany, Spain, France, the Netherlands, and Poland are widely adopting DG ground mounted solar, driven by high commercial electricity prices, corporate PPAs, and government-backed initiatives like EU Solar Rooftop Strategy expansion into small-scale ground arrays. The German Mittelstand of specialized EPC firms and mounting system manufacturers is particularly active in developing modular, biodiversity-inclusive ground mount solutions.

Europe's industrial decarbonization mandates, demand for agricultural dual-use (agrivoltaic) ground mount systems, and circular economy requirements for module recycling further drive technology differentiation. Funding through Horizon Europe and national energy transition funds supports R&D in lightweight frameless modules, robotic cleaning for distributed arrays, and AI-based yield forecasting.

Corporate net zero commitments across retail, automotive, and logistics sectors increasingly deploy standardized ground mount solutions on brownfield sites, warehouse adjacencies, and industrial buffer lands. With strong technical standards, digital permitting platforms, and emphasis on community energy models, Europe remains one of the most advanced regions in DG ground mounted solar penetration.

The Japan DG Ground-Mounted Solar PV Market

The Japan DG Ground Mounted Solar PV Market is anticipated to be valued at approximately USD 2.8 billion in 2026 and is expected to attain nearly USD 7.9 billion by 2035, expanding at a CAGR of about 12.2% during the forecast period. Japan's limited utility-scale land availability and high industrial power costs drive strong demand for distributed ground mount configurations on corporate campuses, factory premises, and reclaimed industrial lands.

The Ministry of Economy, Trade and Industry (METI) actively supports on-site solar generation through feed-in-premium schemes, capex subsidies for SMEs, and streamlined grid connection protocols for distributed assets. Japan's leadership in high-efficiency heterojunction technology, space-efficient mounting design, and seismic-certified racking systems accelerates innovation in compact, high-yield ground mount suitable for dense urban peripheries and disaster-resilient microgrids.

Japan's concept of "Floating Solar 2.0" and dual-use agricultural PV, driven by conglomerates like Sharp Energy Solutions, Kyocera, and Toshiba, integrates DG ground mount with existing industrial land use. Distributed solar arrays are being deployed across Toyota's supply chain campuses, logistics hubs in Greater Tokyo, and semiconductor facilities in Kyushu. Japan's cultural emphasis on precision manufacturing and long-term asset performance positions the country as a high-growth innovator in premium-efficiency DG ground mount.

Global DG Ground-Mounted Solar PV Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global DG Ground Mounted Solar PV Market is expected to be valued at USD 42.5 billion in 2026 and is projected to reach USD 112.4 billion by 2035, showcasing rapid expansion supported by rising corporate renewables procurement and favorable distributed generation economics.

- High CAGR Driven by C&I Adoption: The market is expected to grow at an impressive CAGR of 11.4% from 2026 to 2035, fueled by accelerating corporate decarbonization, AI-driven energy management, declining balance of system costs, and increasing behind-the-meter solar penetration worldwide.

- Strong Growth Trajectory in the United States: The U.S. DG Ground Mounted Solar PV Market stands at USD 13.8 billion in 2026 and is projected to reach USD 34.4 billion by 2035, expanding at a CAGR of 10.7% due to robust ITC incentives, corporate PPA demand, and rapid community solar expansion.

- North America Maintains Regional Dominance: North America is expected to capture approximately 38.5% of the global market share in 2026, supported by mature distributed solar financing infrastructure, significant technology R&D investment, and early adoption of tracker-integrated DG configurations.

- Rapid Advancement in PV Component Technologies: Innovations including bifacial monocrystalline modules, 1500V DC inverter architectures, ballasted low-penetration mounting systems, and cloud-based distributed asset management platforms are significantly accelerating energy yield, land-use efficiency, and system ROI for DG ground mounted solar.

- Growing Corporate PPAs Boost Adoption: Rising global commitment from commercial and industrial entities to source 24/7 carbon-free energy, coupled with favorable on-site generation economics, is driving sustained demand for scalable, predictable, and directly controllable ground mount solar assets.

Global DG Ground-Mounted Solar PV Market: Use Cases

- Manufacturing Facility Captive Power: Large-scale industrial consumers deploy ground mounted arrays on adjacent land parcels to offset baseload consumption, hedge against grid tariff escalation, and meet science-based carbon reduction targets.

- Logistics & Distribution Center Microgrids: E-commerce and third-party logistics operators integrate ground mount solar with EV charging infrastructure and battery storage to power automated warehousing and last-mile delivery fleets.

- Commercial Campus & Corporate Headquarters: Multi-building corporate campuses deploy centralized ground mount PV systems to achieve net zero energy status and qualify for green building certifications like LEED and BREEAM.

- Agricultural & Dual-Use Solar Farms: Agrivoltaic ground mount installations enable simultaneous crop production or livestock grazing beneath elevated PV arrays, optimizing land productivity for rural commercial enterprises.

- Community Solar & Shared Renewables: Third-party developers build and operate medium-scale ground mount solar gardens, enabling residential subscribers and small businesses to access solar savings without on-site installation.

Global DG Ground-Mounted Solar PV Market: Stats & Facts

Ministry of New & Renewable Energy (MNRE), Government of India

- India's total installed solar power capacity reached 140.60 GW (as of January 2026).

- Ground-mounted solar PV installed capacity stood at 107.26 GW.

- Grid-connected rooftop solar capacity reached 24.30 GW.

- Hybrid solar projects accounted for 3.36 GW of installed capacity.

- Off-grid solar capacity stood at 5.68 GW.

- Solar capacity reached 132.85 GW by November 2025.

- Ground-mounted solar capacity within that total was 100.80 GW (Nov 2025).

- Solar installations added in 2025 (till November) totaled 34.98 GW.

- Renewable energy capacity added in 2025 (till November) was 44.51 GW.

- Solar contributed the largest share of renewable additions in 2025 (~35 GW).

- India's total non-fossil fuel installed power capacity crossed 250 GW in 2025.

- Renewable energy met approximately 51.5% of peak electricity demand on certain days in 2025.

- Installed solar capacity increased from 2.82 GW in 2014 to over 140 GW in 2026.

- Solar capacity added during FY 2024-25 was 23,832.87 MW (23.83 GW).

- Solar capacity added during FY 2023-24 was 15,033.24 MW (15.03 GW).

International Renewable Energy Agency (IRENA)

- Global solar PV capacity additions in 2024 totaled 451.9 GW.

- Total global installed solar PV capacity reached approximately 1,865 GW (1.865 TW) by end of 2024.

- Solar PV accounted for approximately 77.8% of total renewable capacity additions in 2024.

- More than 92% of global renewable capacity additions in 2024 came from solar and wind combined.

- China accounted for approximately 61% of global solar PV additions in 2024.

Global DG Ground-Mounted Solar PV Market: Market Dynamic

Driving Factors in the Global DG Ground Mounted Solar PV Market

Corporate Decarbonization & Energy Cost Control

The accelerating global commitment from commercial and industrial entities to achieve net zero emissions is a major driver for DG ground mounted solar adoption. Faced with rising grid tariffs, carbon border adjustment mechanisms, and investor pressure for ESG performance, corporations are systematically deploying on-site generation assets. Ground mount configurations offer superior scalability, orientation flexibility, and expansion capacity compared to rooftop alternatives. This allows manufacturing plants, data centers, and logistics hubs to directly replace grid-supplied brown power with low-cost, long-term contracted solar electricity, fundamentally reshaping industrial energy procurement.

Technology Innovation and Integration

DG ground mounted solar benefits heavily from rapid progress in high-efficiency module architectures, advanced power electronics, and digital O&M platforms. Key innovations include 500W+ bifacial monocrystalline panels, string inverters with module-level rapid shutdown, trackers optimized for variable terrain, and drone-based thermal inspection integrated with AI analytics. These advancements enable higher energy density per land area, improved performance ratio, and enhanced bankability for distributed assets. The convergence of ground mount solar with behind-the-meter storage, EV fleet infrastructure, and virtual power plant aggregation further expands the value proposition for commercial prosumers.

Restraints in the Global DG Ground Mounted Solar PV Market

Land Availability & Permitting Complexity

The significant land footprint required for ground mounted solar typically 4-6 acres per MW limits deployment opportunities in dense urban environments and high-value real estate markets. Industrial and commercial entities often lack adjacent greenfield parcels, requiring consideration of brownfield sites, landfills, or dual-use agricultural arrangements that introduce remediation costs and stakeholder complexity. Additionally, local zoning restrictions, historic preservation reviews, and interconnection study backlogs can extend development timelines by 12-24 months, creating friction for corporate procurement deadlines.

Supply Chain Concentration & Trade Policy Uncertainty

Global PV manufacturing remains heavily concentrated in China across polysilicon, wafer, cell, and module production stages. This geographic concentration exposes the DG ground mounted market to trade policy volatility, including anti-dumping duties, forced labor import restrictions, and retaliatory tariffs. EPC contractors and developers face procurement complexity in verifying domestic content compliance for tax credit adders while managing module availability and price fluctuation. Supply chain regionalization efforts remain in early stages, with non-Chinese manufacturing capacity requiring sustained policy support to achieve cost parity.

Opportunities in the Global DG Ground Mounted Solar PV Market

Expansion into Emerging Economy Industrial Corridors

Emerging markets represent major growth opportunities due to rapid industrialization, government-backed special economic zones, and international climate finance mobilization. Countries in Southeast Asia, Latin America, and Africa are launching dedicated solar parks for export-oriented manufacturing, where DG ground mount can provide reliable, low-cost power to offset unreliable grid infrastructure and diesel generator dependence. Local module assembly partnerships, equipment leasing models, and green bank capitalization can improve accessibility, driving the next wave of market expansion.

Agrivoltaics & Multi-Functional Land Use

The integration of solar generation with agricultural production, biodiversity enhancement, and soil regeneration creates substantial value accretion opportunities. Dual-use ground mount systems with elevated structures, rotational grazing compatibility, and pollinator-friendly vegetation management enable commercial farmers and rural landowners to diversify revenue streams while maintaining agricultural use classification. Advanced modeling tools now optimize trade-offs between panel density, crop light availability, and microclimate effects, transforming previously non-productive land into hybrid economic assets.

Trends in the Global DG Ground Mounted Solar PV Market

Digital Twin & AI-Optimized Plant Operations

The deployment of cloud-native digital twin platforms for distributed ground mount portfolios is gaining significant traction. These systems ingest satellite irradiance data, sensor telemetry, and weather forecasting to create continuously updated performance models for each site. AI algorithms detect underperformance at string or module level, automatically dispatch cleaning or maintenance crews, and optimize inverter power factor settings in response to grid signals. This trend transforms DG ground mount arrays from passive assets into actively managed, grid-interactive energy resources.

Integrated Solar-Storage as Standard Configuration

Rapid battery cost declines and expanding commercial time-of-use rate differentials are driving standardization of DC-coupled and AC-coupled storage alongside new ground mount installations. Commercial customers increasingly require evening load coverage, demand charge reduction, and islanding capability for business continuity. This convergence creates opportunities for integrated EPC offerings combining PV, storage, and energy management software under single-performance contracts, improving project IRR and customer retention.

Global DG Ground-Mounted Solar PV Market: Research Scope and Analysis

By Component Analysis

Solar Panels are projected to dominate the Component segment of the Global DG Ground Mounted Solar PV Market. This dominance is driven by the fundamental role of PV modules as the primary energy conversion asset, representing the largest single cost component and the most critical determinant of long-term system performance and yield. Continuous efficiency improvements in monocrystalline PERC and TOPCon architectures, combined with declining $/Wp pricing, have made premium module selection a high-ROI decision for C&I owners prioritizing land-use efficiency and 25-year degradation guarantees. The technology for high-power terrestrial modules is also the most mature, with bifacial capability now standard in DG ground mount configurations, offering proven reliability and clearly modeled backside gain contributions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

While Inverters address the essential function of DC-AC conversion with increasingly sophisticated grid-support and rapid shutdown features, their adoption is driven more by compliance and safety requirements than primary investment differentiation. The technical complexity of 1500V architecture and integrated AFCI protection has increased system-level value, yet inverter cost remains a smaller fraction of total Capex. Mounting Structures represent a highly engineered but regionally optimized segment, with domestic content requirements driving local manufacturing of steel and aluminum racking. Balance of System, encompassing wiring, combiner boxes, monitoring platforms, and labor, remains essential but fragmented across multiple sub-suppliers. Therefore, the technological centrality and investment weight of solar panels secure their leading market position throughout the forecast period.

By System Type Analysis

Fixed Tilt Systems are projected to dominate the global DG ground mounted solar market, fundamentally representing the most widely deployed configuration due to their simplicity, lowest initial capital cost, and proven bankability. Their dominance stems from an unmatched value proposition for cost-sensitive commercial and industrial customers prioritizing rapid payback and minimal moving parts. By eliminating motors, controllers, and ongoing mechanical maintenance, fixed tilt systems deliver predictable energy profiles with virtually zero O&M complexity over 30-year asset lives. The driving forces behind their market leadership are tri-fold: the broad suitability for mid-latitude sites where tracker gains are modest, the increasing competitiveness of high-efficiency modules that partially offset fixed tilt yield disadvantages, and the financing community's deep familiarity with fixed tilt performance models. As corporate customers prioritize execution speed and lowest risk over marginal yield optimization, fixed tilt remains the cornerstone of mainstream DG ground mount deployment.

Single-Axis Trackers form the crucial and rapidly growing second-largest segment, effectively bridging the gap between lowest-cost fixed tilt and maximum-yield dual-axis configurations. These systems, which rotate panels along a north-south axis to follow the sun's daily arc, deliver 15-25% annual energy gain versus fixed tilt with only modest capital cost increment. Their strength lies in optimizing land productivity for constrained sites and maximizing IRR in high-latitude or high-electricity-price markets. By increasing capacity factor toward utility-scale benchmarks, single-axis trackers enable commercial customers to achieve higher self-consumption and faster carbon payback. This balance of yield enhancement and manageable complexity makes them the preferred choice for sophisticated corporate buyers with ample land and sustainability mandates. Dual-Axis Trackers, while offering maximum theoretical yield, remain a niche segment reserved for specialized applications such as EV charging canopies and research installations due to higher capital intensity and mechanical complexity.

By Technology Analysis

Monocrystalline Silicon is poised to be the largest and most dominant technology segment for DG ground mounted solar, driven by compelling efficiency, degradation, and density advantages. The relentless pursuit of higher wattage per square meter now exceeding 22% panel efficiency for mainstream TOPCon and approaching 24% for heterojunction creates a compelling use case for land-constrained commercial and industrial sites. This performance density is where premium silicon excels, enabling 30-40% more capacity per acre compared to legacy multicrystalline or thin film alternatives. The sector also benefits from massive global manufacturing scale, continued cost reduction through wafer size standardization, and established module-level bankability trackers from Tier-1 suppliers. Beyond pure efficiency, monocrystalline's superior temperature coefficient and low-light performance deliver tangible yield advantages across varied DG deployment environments.

Thin Film technologies, primarily cadmium telluride and emerging perovskite-on-silicon tandems, rank as the second-largest segment, fueled by distinct advantages in specific DG applications. Their superior high-temperature performance, uniform appearance, and reduced manufacturing carbon footprint appeal to sustainability-focused corporate buyers and architectural sensitive sites. However, lower conversion efficiency requires approximately 30% more land area per MW, limiting suitability for land-constrained C&I deployments. Multicrystalline Silicon, once the industry workhorse, continues its structural decline in DG applications as monocrystalline pricing parity and superior performance drive universal specification phase-out. The technology segment therefore reflects a clear hierarchy: monocrystalline as the dominant standard, thin film as the specialist alternative, and multicrystalline as the diminishing legacy option.

By Application Analysis

Industrial Construction and Manufacturing is poised to be the largest and most dominant application segment for DG ground mounted solar, driven by powerful global macro-trends in supply chain decarbonization. The intensive 24/7 load profile of heavy industry, automotive plants, and chemical facilities creates a perfect use case: continuous daytime baseload absorption of solar generation without export curtailment. This load matching is where DG ground mount excels, directly displacing grid imports at retail rates while improving manufacturing facilities' carbon intensity metrics for export competitiveness. The sector is also acutely affected by carbon border adjustment mechanisms and EU deforestation regulations, making on-site solar a strategic compliance tool beyond simple energy economics. From Thai industrial estates to German automotive supplier parks, the operational and reputational pressures in industrial manufacturing make DG ground mount adoption not merely advantageous but increasingly essential for global supply chain participation.

Commercial Application ranks as the second-largest segment, fueled by its own distinct demand drivers. Office campuses, retail big-box stores, hotels, and hospitals feature substantial daytime loads and available adjacent land for medium-scale arrays. The precision and predictability of ground mount generation directly address corporate ESG targets and shareholder climate resolutions, reducing purchased electricity volatility. Furthermore, the scale of corporate real estate portfolios many publicly traded REITs with centralized procurement justifies standardized, repeatable ground mount designs deployed across dozens of sites simultaneously. While more varied in site conditions than industrial brownfields, commercial projects increasingly adopt tracker-equipped configurations to maximize yield within fixed property boundaries. Utility application in the DG context refers to smaller-scale, grid-connected ground mount assets developed by municipal utilities and cooperatives to serve localized load pockets, representing the third significant application tier. Residential remains nascent due to land constraints, though rural residential acreage offers future opportunity.

The Global DG Ground-Mounted Solar PV Market Report is segmented on the basis of the following:

By Component

- Solar Panels

- Inverters

- Mounting Structures

- Balance of System

By System Type

- Fixed Tilt

- Single Axis Tracker

- Dual Axis Tracker

By Technology

- Monocrystalline Silicon

- Thin Film

- Multicrystalline Silicon

By Application

- Residential

- Commercial

- Industrial

- Utility

Impact of Artificial Intelligence in the Global DG Ground-Mounted Solar PV Market

- AI for Soiling Loss Detection & Cleaning Optimization: AI algorithms analyze power output data against satellite-derived particulate matter concentrations and rainfall records to predict soiling accumulation, optimizing robotic or manual cleaning schedules to maximize yield while minimizing water and labor costs.

- AI-Driven Inverter & Tracker Performance Tuning: Machine learning models continuously adjust tracker angles, inverter voltage setpoints, and reactive power injection based on real-time cloud passage, albedo conditions, and grid frequency signals, extracting marginal efficiency gains across heterogeneous site conditions.

- Predictive Failure Diagnostics & Remote Remediation: AI-powered analytics platforms monitor string-level current-voltage curves, thermal signatures, and insulation resistance to identify potential failure modes including hotspot formation, PID degradation, and connector corrosion weeks before critical underperformance occurs.

- Automated Shading & Obstacle Detection: Computer vision applied to site survey imagery automatically identifies nearby vegetation growth, adjacent construction crane shadows, and permanent obstructions, enabling dynamic re-routing of electrical stringing or proactive vegetation management.

- Portfolio-Level Performance Benchmarking: AI systems aggregate operational data across hundreds of geographically distributed DG ground mount assets, benchmarking each site against its peer group to identify systematic underperformance, validate EPC quality, and optimize O&M resource allocation.

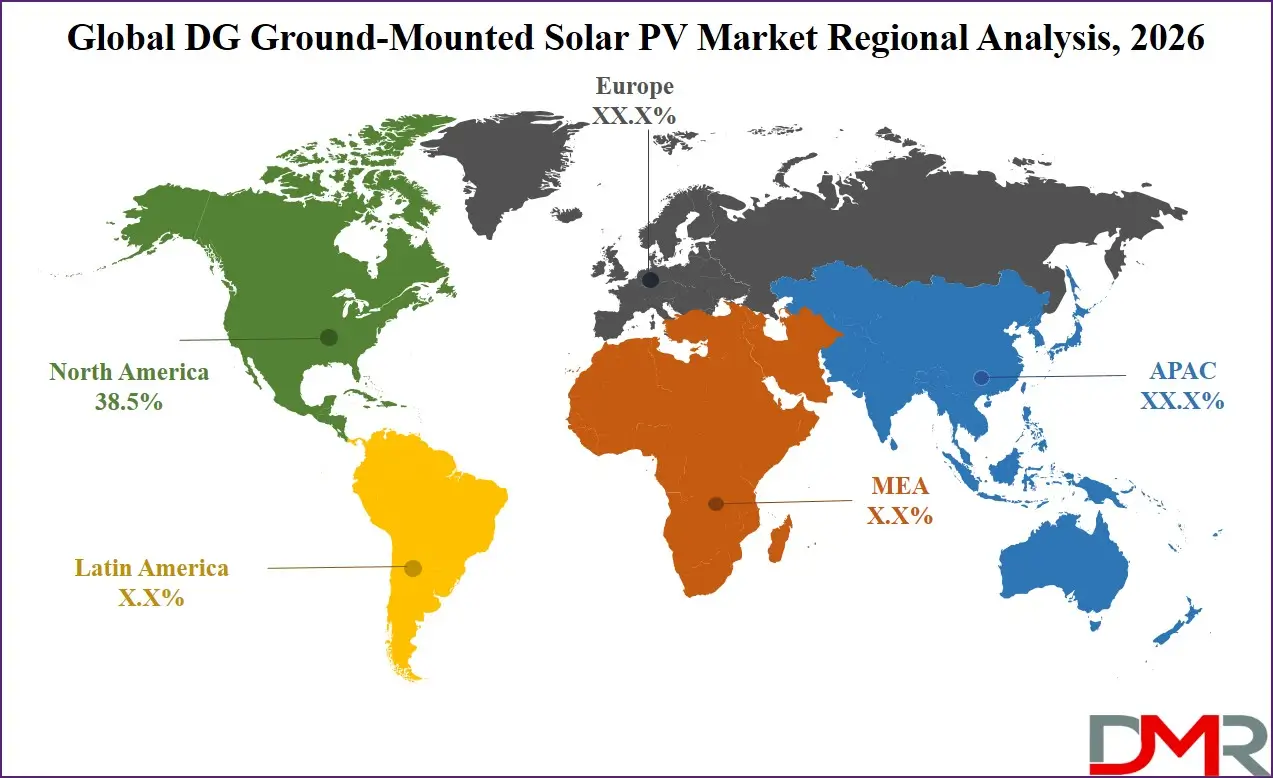

Global DG Ground-Mounted Solar PV Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to dominate the Global DG Ground Mounted Solar PV Market with 38.5% of market share by the end of 2026, owing to a powerful combination of investment tax credit certainty, surging corporate renewable procurement, and mature distributed solar financing infrastructure. The United States and Canada have rapidly integrated behind-the-meter solar into corporate energy strategy, supported by favorable third-party ownership models and securitization of distributed generation assets. Major Fortune 500 corporations are institutionalizing DG ground mount deployment to meet 2030 sustainability milestones.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The region's booming data center construction, manufacturing reshoring, and electric vehicle factory build-out, coupled with attractive risk-adjusted returns, create a strong economic case for ground mount solar. Supportive treasury guidance on direct pay and transferability provisions further solidify North America's leadership position.

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR and is poised to achieve rapid market share growth due to its massive industrial electricity demand, government emphasis on manufacturing competitiveness, and severe air quality constraints driving renewable alternatives. Countries like India, China, Vietnam, and Thailand are investing heavily in distributed solar to power export-oriented industrial zones with verifiable green attributes. India's Production Linked Incentive scheme for solar manufacturing and Vietnam's direct PPA pilot program are creating fertile ground for adoption. The region's cost sensitivity is being addressed through domestic module production, standardized EPC practices, and multilateral development bank financing for private industrial parks. This, combined with an immense corporate decarbonization pipeline, positions APAC as the fastest-growing market for DG ground mounted solar systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global DG Ground-Mounted Solar PV Market: Competitive Landscape

The Global DG Ground Mounted Solar PV Market is moderately fragmented, featuring a mix of vertically integrated module manufacturers, specialized tracking and mounting solution providers, power electronics leaders, and EPC platform companies scaling through acquisition. Leading equipment players LONGi Green Energy, JinkoSolar, and Trina Solar are leveraging their module dominance to offer vertically bundled DG solutions inclusive of racking and monitoring. Pure-play tracker innovators such as Array Technologies, Nextracker, and Soltec are driving market dynamics with software-optimized, terrain-following single-axis systems purpose-built for distributed generation terrain constraints.

Inverter and power electronics specialists like SMA Solar, Sungrow, and Enphase play increasingly influential roles through module-level power electronics, AFCI safety compliance, and grid-forming capabilities essential for behind-the-meter microgrid integration. Traditional EPC and development firms are also entering manufacturing and tracker supply through strategic JVs and backward integration, aiming to capture margin across the DG ground mount value chain.

Some of the prominent players in the Global DG Ground-Mounted Solar PV Market are:

- LONGi Green Energy Technology Co., Ltd.

- JinkoSolar Holding Co., Ltd.

- Trina Solar Co., Ltd.

- Canadian Solar Inc.

- JA Solar Technology Co., Ltd.

- First Solar, Inc.

- Nextracker Inc.

- Array Technologies, Inc.

- Soltec Power Holdings S.A.

- SMA Solar Technology AG

- Sungrow Power Supply Co., Ltd.

- Enphase Energy, Inc.

- Huawei Digital Power Technologies Co., Ltd.

- ABB Ltd.

- Schneider Electric SE

- Siemens AG

- BayWa r.e. AG

- Sterling and Wilson Renewable Energy Ltd.

- Tata Power Solar Systems Ltd.

- Mahindra Susten Private Limited

- Other Key Players

Recent Developments in the Global DG Ground-Mounted Solar PV Market

- November 2025: Nextracker introduced its decoupled, terrain-following single-axis tracker variant specifically optimized for uneven commercial brownfield sites, featuring reduced pile depth requirements and AI-based backtracking algorithms that increase annual yield by 6% on non-ideal topography.

- October 2025: LONGi set a new world record for commercial-size tandem solar cells, targeting premium C&I DG segment with 30-year warranty, bifacial factor exceeding 90%, and significantly reduced land-use footprint for constrained ground mount installations.

- September 2025: Sungrow announced a multi-year strategic supply agreement for 2.5 GW of 1500V string inverters and medium-voltage stations dedicated to US distributed ground mount community solar portfolios, signaling domestic content qualification and scaled localization.

- August 2025: Array Technologies completed acquisition of a specialist predictive analytics firm to enhance its tracker software suite with real-time soiling detection, inverter-agnostic performance monitoring, and automated alarm triage for distributed solar fleets.

- June 2025: First Solar initiated construction of a specialized logistics and distribution hub in Tamil Nadu, India, exclusively serving C&I ground mount developers with rapid-deployment thin film modules pre-configured for 1000V DC commercial architectures.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 42.5 Bn |

| Forecast Value (2035) |

USD 112.4 Bn |

| CAGR (2026–2035) |

11.4% |

| The US Market Size (2026) |

USD 13.8 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Component (Solar Panels, Inverters, Mounting Structures, Balance of System), By System Type (Fixed Tilt, Single Axis Tracker, Dual Axis Tracker), By Technology (Monocrystalline Silicon, Thin Film, Multicrystalline Silicon), By Application (Residential, Commercial, Industrial, Utility) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

LONGi Green Energy Technology Co., Ltd., JinkoSolar Holding Co., Ltd., Trina Solar Co., Ltd., Canadian Solar Inc., JA Solar Technology Co., Ltd., First Solar, Inc., Nextracker Inc., Array Technologies, Inc., Soltec Power Holdings S.A., SMA Solar Technology AG, Sungrow Power Supply Co., Ltd., Enphase Energy, Inc., Huawei Digital Power Technologies Co., Ltd., ABB Ltd., Schneider Electric SE, Siemens AG, BayWa r.e. AG, Sterling and Wilson Renewable Energy Ltd., Tata Power Solar Systems Ltd., Mahindra Susten Private Limited., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global DG Ground Mounted Solar PV Market?

▾ The Global DG Ground Mounted Solar PV Market size is estimated to have a value of USD 42.5 billion in 2026 and is expected to reach USD 112.4 billion by the end of 2035.

What is the growth rate in the Global DG Ground Mounted Solar PV Market?

▾ The market is growing at a CAGR of 11.4 percent over the forecasted period of 2026 to 2035.

What is the size of the US DG Ground Mounted Solar PV Market?

▾ The US DG Ground Mounted Solar PV Market is projected to be valued at USD 13.8 billion in 2026. It is expected to witness subsequent growth in the upcoming period as it reaches USD 34.4 billion in 2035 at a CAGR of 10.7%.

Which region accounted for the largest Global DG Ground Mounted Solar PV Market?

▾ North America is expected to have the largest market share in the Global DG Ground Mounted Solar PV Market with a share of about 38.5% in 2026.

Who are the key players in the Global DG Ground Mounted Solar PV Market?

▾ Some of the major key players in the Global DG Ground Mounted Solar PV Market are LONGi Green Energy, JinkoSolar, Trina Solar, First Solar, Nextracker, Array Technologies, Sungrow, SMA Solar, and many others.