The Diabetes Drug Market is poised for rapid expansion due to demographic shifts, economic factors and technological advancements. Rising global diabetes prevalence due to an aging population with less physical activity leading to greater obesity rates serves as one key market driver.

Regulative regimes play an essential role in assuring the efficacy and safety of new pharmaceuticals; yet their high prices continue to pose barriers, particularly for low and middle-income countries - emphasizing the necessity of cost-effective solutions and personalized therapy based on genetic research or patient data analytics in shaping market trends for tomorrow.

Key Takeaways

- The global diabetes drugs market is expected to reach USD 157.46 Bn by 2024 with a CAGR of 7.1%.

- GLP-1 receptor agonists held a 32.9% market share as of 2024.

- Due to its higher global prevalence, the Type 2 segment held the highest market share with 62.97%.

- Subcutaneous administration was dominant with a 45.9% market share.

- Retail pharmacies held onto the highest market share for sales of diabetes medicines in 2024 with 62.7 %, due to competitive pricing within retail channels.

- North America had an astounding 51.5% market share for diabetes drugs sold across North America by 2024.

Use Cases

- Patient Management Improvement: Continuous glucose monitoring systems combined with advanced insulin therapies allow real-time data analysis and customized treatment adjustments, leading to enhanced glycemic control with less complications.

- Pharmaceutical Innovation: Companies are creating oral GLP-1 receptor agonists as an alternative to injections and increasing patient compliance - particularly among those suffering from needle phobia.

- Cost-Effective Treatment Solutions: Glenmark's Lirafit provides more affordable alternatives to more costly brand medications and can expand access to diabetes treatments in emerging markets.

- Integrated Care Solutions: Digital health platforms that combine medication adherence tools, diet tracking capabilities and telehealth consultations improve diabetes management and patient outcomes by offering comprehensive support services.

- Approvals and Market Expansion: Sanofi's Soliqua in India received regulatory approval, giving pharmaceutical companies more market access and offering advanced diabetes treatments to more people.

Driving Factors

Key Market Driver

Diabetes's increased global prevalence is prompting market expansion for its drug market. According to estimates by the International Diabetes Federation, 463 million people living with diabetes today may increase to 700 million by 2045 due to ageing populations, sedentary lifestyles, increasing obesity rates and expanding treatment options which result in greater demand for both existing medications as well as novel therapeutics, driving substantial market expansion.

Advancements in Drug Development

Technological advances are revolutionizing the diabetes Drug Market. Modern medications, including GLP-1 receptor agonists and SGLT2 inhibitors, offer glucose management along with additional health benefits like weight loss and cardiovascular protection; continuous glucose monitoring devices and smart insulin pens represent major advances in medication administration that enhance compliance for treatment, improving patient compliance with medications. Pharmaceutical company investments in R&D projects to meet growing diabetes care demand while expanding revenue channels are driving this forward momentum.

Rising Healthcare Expenditure

One key driver of growth in the diabetes drug market is rising global healthcare expenditure. According to figures released by the World Health Organization, global healthcare expenditure will reach $8.3 trillion by 2020 with much of this money going toward chronic disease management - such as managing diabetes. Greater healthcare budgets encourage novel drug therapies and increase access to innovative diabetes treatments, with government initiatives and regulations targeting strengthening healthcare infrastructure and expanding insurance coverage aiding market accessibility further. Furthermore, as healthcare expenses rise the financial capacity will allow widespread adoption of cutting-edge diabetes medications which drives long-term market expansion.

Growth Opportunities

Personalized medicine

Personalized medicine provides an exciting breakthrough in diabetes care, offering tailor-made plans based on an individual's genetic profile, lifestyle choices and

medical history. Taking this approach enhances diabetes management's effectiveness by permitting precise adjustments of medication types and doses; in turn improving patient outcomes.

As genomics and big data analytics become integrated into clinical practice, their application should advance personalized treatment protocols tailored specifically for each patient and reduce side effects while optimizing efficacy. With pharmaceutical companies and healthcare providers increasingly turning towards personalized medicine solutions tailored specifically for patient needs, demand will likely increase significantly for innovative diabetes drugs designed specifically to address them.

Telemedicine and Digital Health Solutions

Telemedicine and digital health solutions represent another significant opportunity in diabetes management. COVID-19's pandemic was an accelerant to its adoption; and this trend continues today, revolutionizing diabetes management with digital tools such as mobile health apps, continuous glucose monitoring (CGM) systems and remote patient monitoring devices that offer real-time tracking of blood glucose levels, patient engagement tools and timely healthcare provider interventions that improve treatment efficacy overall and increase market expansion for related drugs.

Combination Therapies

Combination therapies offer an exciting prospect for improving diabetes treatment outcomes. By employing two or more drugs with complementary mechanisms of action, combination therapies offer superior glycemic control compared to monotherapies; GLP-1 receptor agonists combined with SGLT2 inhibitors or DPP-4 inhibitors may improve therapeutic efficacy while decreasing treatment-related complications, providing additional options while simultaneously expanding market growth by expanding treatment choices available to patients.

Key Trends

Shift to Oral Anti-Diabetics Agents

An emerging trend is the increasing preference for oral anti-diabetic agents over injectable forms, due to their ease of administration, improved compliance and convenience. Furthermore, innovations like oral GLP-1 receptor agonists expand effective treatment options available while eliminating common barriers associated with injectable therapies, like needle phobia or complex dosing regimens - improving overall treatment adherence and outcomes as a result.

Focus on Weight Management Strategies

Weight management and diabetes treatment strategies have increasingly interwoven. Many diabetes drugs, particularly newer classes like GLP-1 receptor agonists and SGLT2 inhibitors, have demonstrated impressive effects on weight reduction. With obesity being one of the risk factors associated with Type 2 diabetes, medications that address both blood glucose control and weight management become even more beneficial - thus driving patient preferences and physician recommendations towards such therapies as part of treatment strategies in 2024.

Biosimilar and Biological Drugs

Market trends indicate an increasing use of biological and biosimilar drugs, both known for their superior efficacy and targeted action, are becoming more widely adopted into diabetes care. Biosimilar medications offer cost-cutting alternatives which increase accessibility and affordability. Their approval and adoption is rapidly increasing to offer patients more choices while driving competitive pricing within the market; this trend should play a crucial role in expanding access to advanced diabetes treatments worldwide.

Restraining Factors

High Cost of Diabetes Drugs Is an Obstacle to Widespread Adoption

Diabetes medications' expensive pricing poses an obstacle to their wider adoption on the market. Many advanced therapies like GLP-1 receptor agonists and SGLT2 inhibitors come with steep price tags; Newer insulin analogs often cost multiple times higher than older human insulins, restricting access, especially in low and middle income countries with limited healthcare budgets and significant out-of-pocket expenses for patients.

Financial burden associated with medications remains an enormous barrier in high-income countries and, due to high costs associated with them, can result in non-adherence or reduced compliance by patients; ultimately affecting market growth. Therefore, developing affordable strategies remains crucial.

Adverse Side Effects

Adverse side effects related to diabetes medications are another key factor limiting their market success. While certain new classes offer promising therapeutic results, there may also be adverse reactions which deter patients from using them. GLP-1 receptor agonists have been reported to cause nausea and vomiting while SGLT2 inhibitors may increase your risk for urinary tract infections and ketoacidosis.

These adverse effects may lead to discontinuing treatment altogether and reduce patient compliance - essential elements for effective diabetes management. Furthermore, perceptions of potential side effects may influence both patients and healthcare providers alike, prompting a preference for older, less efficacious therapies despite their lower efficacy levels. Such hesitation to adopt new treatments could slow market expansion and limit adoption rates of innovative medicines.

By Drug Class

In 2024, GLP-1 receptor agonists held a dominant market position in the Drug Class segment of the Diabetes Drug Market, capturing more than a 32.9% share. GLP-1s have become widely-accepted medication to assist in controlling glucose and providing weight management benefits; healthcare providers as well as patients are finding them invaluable. With oral formulations now readily available as convenient alternative injection solutions and thus improved patient adherence.

Insulin remains a cornerstone of diabetes management for both Type 1 diabetes patients and advanced Type 2 diabetics alike. While its market share faces challenges from high costs for newer insulin analogs and an increasing preference for alternative treatments, insulin pumps and smart pens continue to help keep it relevant and relevant among diabetics worldwide.

DPP-4 inhibitors remain an influential market segment, valued for their proven efficacy and reduced side effect profiles. Their popularity can be explained by being suitable as monotherapy or used with other anti-diabetic agents; their usage increased because newer drug classes competed against their proven safety and effectiveness despite competition from newer classes.

SGLT2 inhibitors have become a fast-rising market force due to their dual benefits of improving glycemic control while offering cardiovascular and renal protection. Their wide array of health advantages has lead to their widespread adoption by clinicians worldwide - further clinical evidence will likely only further cement this growth trend.

By Diabetes Type

Type 2 diabetes held a commanding market position within the Diabetes Drug Market by 2024, accounting for more than 62.9 %. Its rising global prevalence - driven by factors such as an aging population, sedentary lifestyles and rising obesity rates - significantly contributed to its overwhelming dominance. With increasing incidence comes increased need for treatments addressing both weight management and glycemic control which further drive its market. Development innovations further expanding treatment for Type 2 Diabetes treatments further solidifying this dominance.

Type 1 diabetes accounts for a smaller market share compared to Type 2, yet is an integral segment within the Diabetes Drug Market. Insulin therapy remains key in managing Type 1 diabetes patients' wellbeing and survival. Improvements to insulin formulation and delivery technologies such as pumps and continuous glucose monitoring (CGM) systems continue to enhance the quality of life for Type 1 diabetic patients.

Furthermore, novel therapeutic approaches including immunotherapies and beta-cell regeneration treatments demonstrate ongoing efforts to bring innovation within this segment. While the Type 1 diabetes market holds only a smaller share, its importance remains imperative due to insulin's essential nature as a management solution and the demand for improved solutions for treatment management.

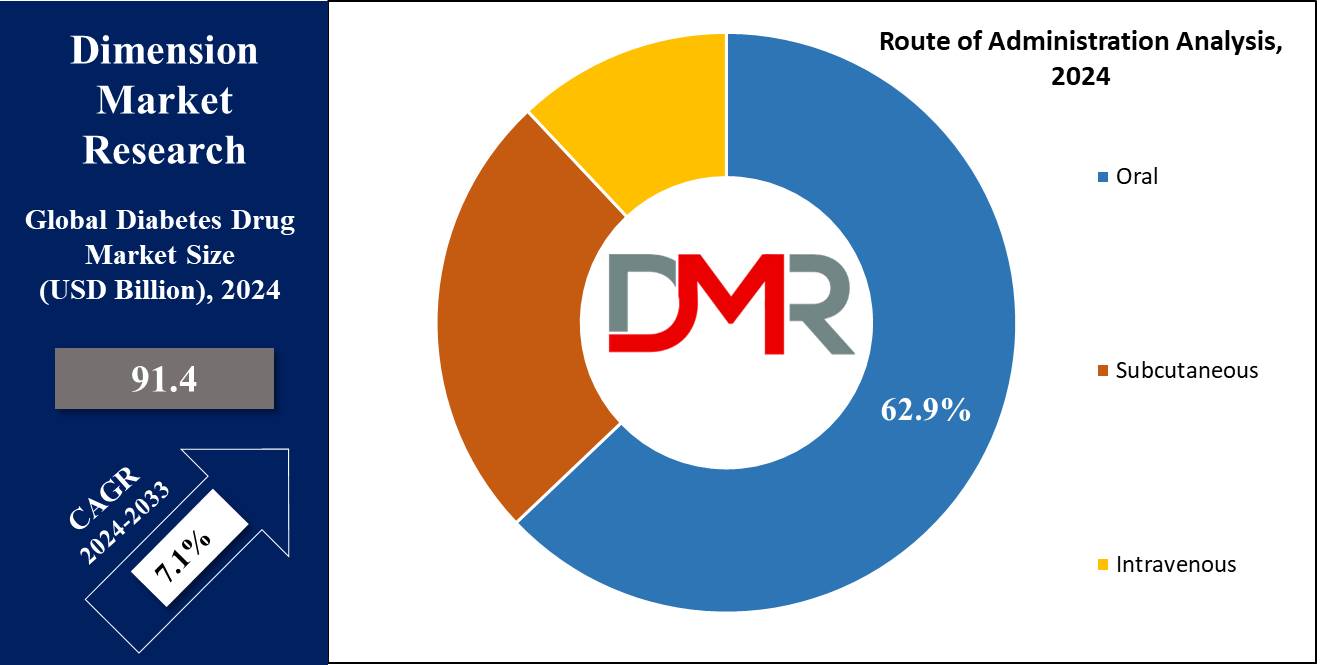

By Route of Administration

Subcutaneous administration held an overwhelming market share of 45.9% for route of administration within the diabetes drug market in 2024. Insulin therapy and GLP-1 receptor agonists that must be injected subcutaneously primarily driven this trend; their efficient administration also contributes to rapid glycemic control with fast onset time of action, making subcutaneous delivery attractive among users and increasing patient compliance and treatment outcomes, further solidifying this route's position at the top.

Oral administration continues to gain in popularity among patients and healthcare providers alike, due to its ease of use for both patient adherence and satisfaction purposes. Oral antidiabetic agents like DPP-4 inhibitors, SGLT2 inhibitors and recently introduced oral GLP-1 receptor agonists are driving this market growth due to their convenient nature - eliminating injections altogether while alleviating patient concerns like needle phobia or complex dosing schedules - giving rise to oral formulations' growing market share - aligned with larger trends toward increasing patient adherence or satisfaction - further increasing market shares within diabetes drug markets overall - thus cementing oral's prominence within diabetes drug markets overall and expanding diabetes drug markets overall.

Intravenous administration holds an invaluable yet subordinate place within the diabetes drug market. Primarily utilized to quickly intervene and stabilize blood glucose levels during emergency cases of hyperglycemia or diabetic ketoacidosis (DKA), intravenous insulin therapy remains vital in acute care settings despite having only a limited market presence.

With its niche application serving acute care settings like these cases quickly and safely. Intravenous delivery must remain relevant despite limited market shares owing to its unique capabilities of rapid intervention and stabilizing blood glucose levels rapidly while stabilizing levels rapidly during acute/emergencies cases of acute/emergencies ensuring its continued relevance despite having such limited market shares!

By Distribution Channel

Retail pharmacies were the dominant market player in the Distribution Channel segment of the Diabetes Drug Market in 2024, holding more than 62.7 % share. Given their convenient access and wide selection of diabetes medicines - such as insulin injections and oral anti-diabetic agents as well as combination therapies - retail pharmacies provided many patients managing their condition with them, including personalized service from pharmacists that assisted patients better educate on and adhere to treatment regimens more easily than any other method available at that time. Retail pharmacys' established presence and close relationships with patients helped keep them at the top position within this particular segment of market.

Online pharmacies are experiencing exponential growth due to increasing adoption of digital health solutions and home delivery services, with patients increasingly turning towards them due to ease of ordering, competitive prices and accessibility in underserved or remote areas. With COVID-19 pandemic's impact and emphasis on consistent medication supply during lockdowns or social distancing measures highlighting this shift even further; market shares of online pharmacies should increase substantially with improved digital infrastructures and customer trust in these online services expected to significantly expand further their market presence and market share will undoubtedly expand tremendously over the coming years!

Hospital pharmacies play a unique and vital role in the diabetes drug market, especially for acute and complex cases. Hospital pharmacies play an integral part in managing inpatient settings by administering intravenous therapies to address severe hyperglycemia or diabetic ketoacidosis (DKA), providing advanced medications, or offering comprehensive and critical care - although their market shares might be smaller relative to retail or online pharmacies - giving hospital pharmacies their essential role as integrative part of overall distribution channel landscape.

The Diabetes Drug Market Report is segmented based on the following:

By Drug Class

- Insulin

- DPP-4 Inhibitors

- GLP-1 Receptor Agonists

- SGLT2 Inhibitors

- Others

By Diabetes Type

By Route of Administration

- Oral

- Subcutaneous

- Intravenous

By Distribution Channel

- Online Pharmacies

- Hospital Pharmacies

- Retail Pharmacies

Regional Analysis

North America hold the highest of 51.5% market share in the Diabetes Drug Market by 2024, driven by factors including high prevalence rates for diabetes, advanced healthcare infrastructure, and substantial healthcare spending in this region. U.S. and Canadian consumers led in adopting innovative diabetes treatments such as continuous glucose monitoring systems and next-generation insulin therapies from companies such as Eli Lilly and Novo Nordisk respectively as well as favorable reimbursement policies, increasing awareness about managing the condition, as key contributors.

Europe represents an essential segment of the Diabetes Drug Market, featuring strong growth and innovation. Germany, France, and the UK lead this field due to high diabetes prevalence rates combined with strong healthcare systems. European markets enjoy substantial R&D investments as well as an established regulatory environment that supports advanced therapy interventions; biosimilars and personalized medicine approaches have seen increasing uptake as they improve treatment efficacy while patient compliance increases; collaborative efforts by governments and healthcare providers in improving care delivery are further spurring market expansion.

Asia Pacific diabetes drug market growth is being propelled by rising prevalence rates and improved healthcare access, particularly among populations living in China, India and Japan. Lifestyle changes due to urbanization and age have driven an upsurge in diabetes cases necessitating more treatment options; government initiatives geared at expanding healthcare infrastructure as well as insurance coverage have played an essential part in expanding access to medications; local pharmaceutical firms also play a vital role by providing cost-effective treatments and biosimilars, further expanding market expansion within this region.

By Region

North America

Europe

- Germany

- U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

Eli Lilly, Novo Nordisk and Sanofi remain at the forefront of innovation for diabetes medications in 2024's Diabetes Drug Market with each company striving to advance and expand their market shares through innovation and diversification of product portfolios and R&D investments. Of particular note is Eli Lilly's efforts towards next-generation insulin and GLP-1 receptor agonist development to enhance both treatment efficacy and patient compliance whereas Novo Nordisk stands out for pioneering its insulin therapies while expanding presence into oral antidiabetics while Sanofi offers personalized medicine solutions and integrated care solutions designed to strengthen market position and strengthen market shares of competitors.

Abbott and Dexcom have led technological innovations in diabetes management with continuous glucose monitoring (CGM) systems that offer real-time blood glucose monitoring with improved patient outcomes. AstraZeneca and Merck have expanded their market shares with innovative antidiabetic agents such as SGLT2 inhibitors and DPP-4 inhibitors which offer substantial advantages in controlling glycemic levels while protecting cardiovascular health, while Biocon and Sun Pharma stand out for biosimilar treatments which enhance access in emerging markets.

Some of the prominent players in the Global Diabetes Drug Market are:

- Eli Lilly

- Novo Nordisk

- Abbott

- AstraZeneca

- Biocon

- Sunpharma

- Sanofi

- Novartis

- Merck

- Pfizer

- Daiichi Sankyo

- Boehringer Ingelheim

- Akros Pharma

- Amgen

- Adocia

- Peptron

- Takeda

Recent developments

- In 2024, Glenmark Pharmaceuticals Ltd. released Lirafit in India as an anti-diabetic biosimilar drug; the daily cost for one standard 1.2 mg dose averages USD 1.21.

- Sanofi India received approval from India's Central Drugs Standard Control Organization in March 2024 to commercially produce the diabetes drug Soliqua as a prefilled pen, under a license granted from CDSCO.

- Akums Drugs and Pharmaceutical Limited of India launched Lobeglitazone as an FDA-approved treatment for type 2 diabetes back in February 2024. The contract drug manufacturing enterprise made this available worldwide as well.

Report Details

| Report Characteristics |

| Market Size (2024) |

USD 84.93 Bn |

| Forecast Value (2033) |

USD 157.46 Bn |

| CAGR (2024-2033) |

7.1% |

| Historical Data |

2018 – 2023 |

| Forecast Data |

2024 – 2033 |

| Base Year |

2023 |

| Estimate Year |

2024 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Drug Class(Insulin, DPP-4 Inhibitors, GLP-1 Receptor Agonists, SGLT2 Inhibitors, Others), By Diabetes Type(Type 1, Type 2), By Route of Administration(Oral, Subcutaneous, Intravenous), By Distribution Channel(Online Pharmacies, Hospital Pharmacies, Retail Pharmacies) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA

|

| Prominent Players |

Eli Lilly, Novo Nordisk, Abbott, AstraZeneca, Biocon, Sunpharma, Sanofi, Novartis, Merck, Pfizer, Daiichi Sankyo, Boehringer Ingelheim, Akros Pharma, Amgen, Adocia, Peptron, Takeda |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |