What is the Digital Sovereignty Market Size?

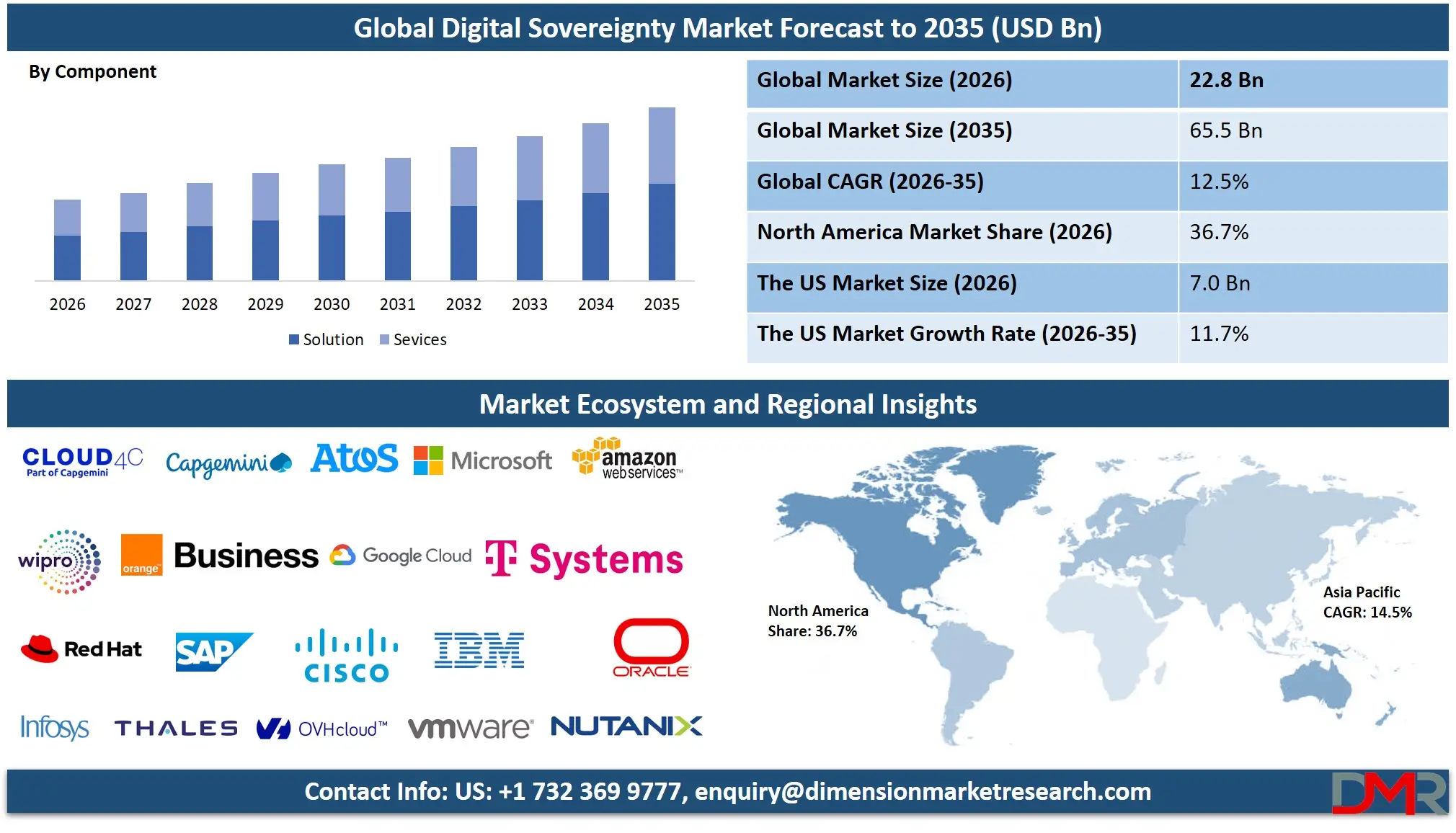

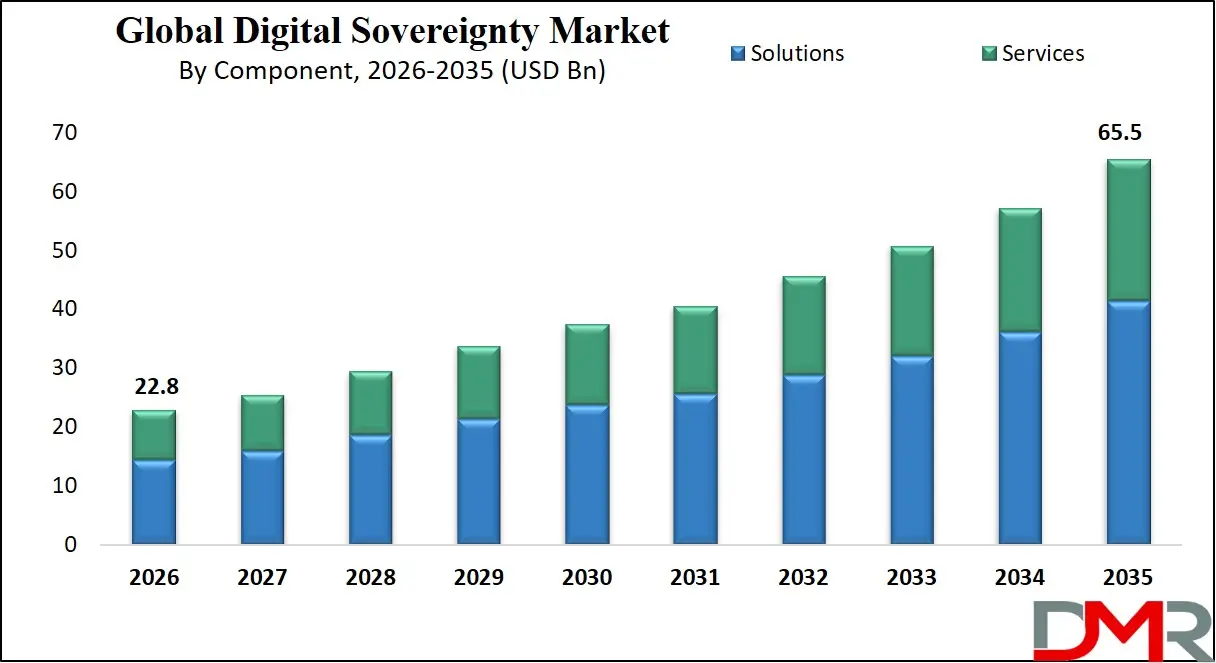

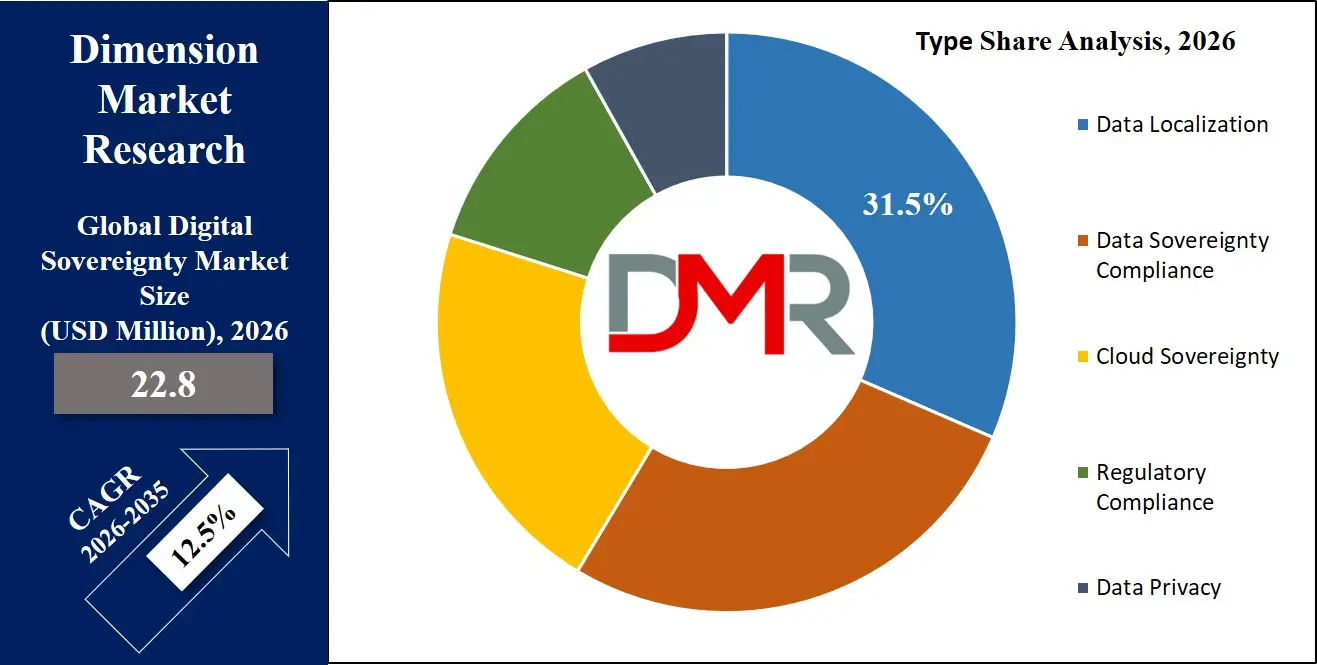

The Global Digital Sovereignty Market is expected to reach a value of USD 22.8 billion in 2026, and it is further anticipated to reach USD 65.5 billion by 2035, growing at a CAGR of 12.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market of digital sovereignty is expanding at an increased rate as nations and corporations are becoming increasingly interested in regulating their digital property, information, and technology infrastructure with the increasing geopolitical conflicts and changing regulatory landscapes. The market consists of sovereign cloud platforms, data governance solutions, identity and access management systems, and specialized consulting and managed services, enabling organizations to exercise jurisdictive control over sensitive information and fulfill complex national and regional data protection structures. The growing necessity to implement data localization requirements, cross-border data transfer policy, and sovereign cloud structures is creating a new demand in holistic offerings of digital sovereignty.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

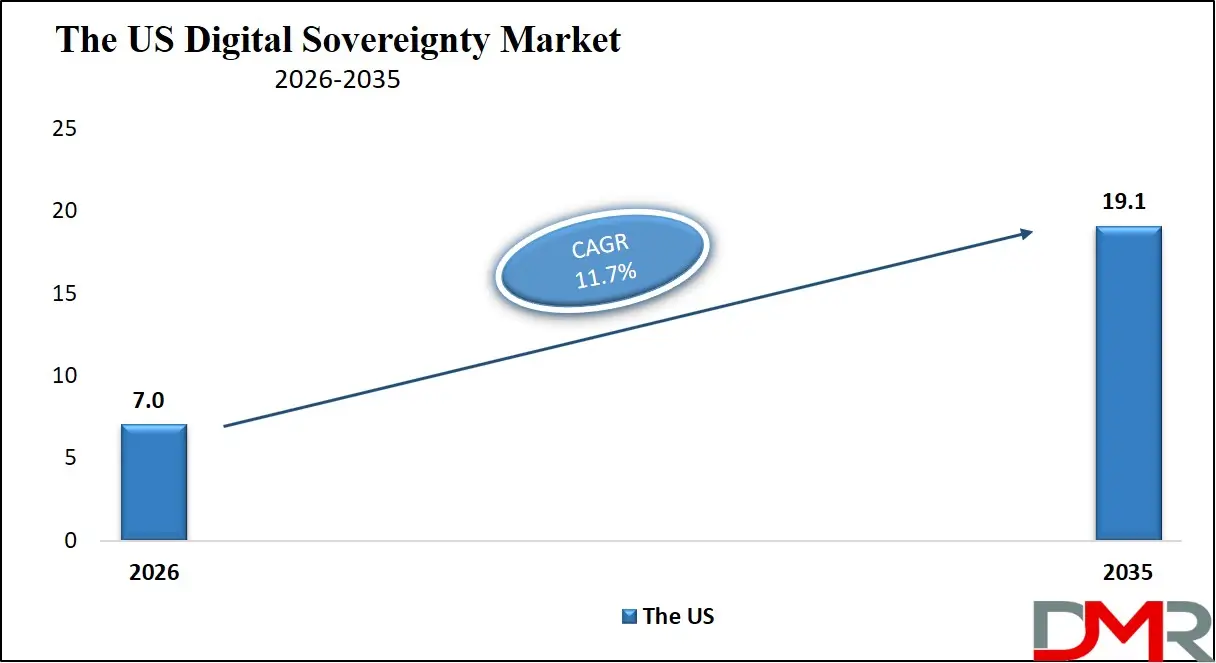

The US Digital Sovereignty Market

The US Digital Sovereignty Market is projected to reach USD 7.0 billion in 2026 at a compound annual growth rate of 11.7% over its forecast period, which is further poised to reach a value of USD 19.1 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US is a distinct and challenging market to offer digital sovereignty solutions, with a tension between the dominance of hyperscale cloud providers, headquartered in the US, and increasing domestic anxieties about data safety, access by foreign adversaries, and integrity of supply chains. The presence of the executive orders that mandate all the federal agencies to adopt the zero-trust architecture, the Cybersecurity Maturity Model Certification (CMMC) regulation on defense contractors, and the increased focus on cross-border data flows involving sensitive technologies have influenced the market. The sovereign cloud services offering logical or physical segregation of commercial cloud infrastructure are also creating a high level of demand in federal and state government agencies, whereas the organizations of the critical infrastructure sector of the private segment are investing in data governance systems, identity and access management solutions, to make sure that they are in compliance with their industry-specific regulations, and to mitigate the risk of foreign ownership or control of critical digital infrastructure.

The Europe Digital Sovereignty Market

The Europe Digital Sovereignty Market is estimated to be valued at USD 6.8 billion in 2026 and is further anticipated to reach USD 19.7 billion by 2035 at a CAGR of 12.5%.

Europe is the most powerful centre and the primary motor of the digital sovereignty movement with such landmark regulatory texts as the General Data Protection Regulation (GDPR), the proposed EU AI Act, the Data Governance Act, and the Data Act. Minimization of dependence on non-European cloud and technology vendors and the creation of a competitive ecosystem of European-owned and operated digital infrastructure is a core characteristic of the European market. The move towards sovereign cloud platforms such as GAIA-X and the European Alliance for Industrial Data, Edge, and Cloud is accelerating the process of investment in cloud platforms with data residency in EU jurisdiction and free operation without extraterritorial legal regimes, such as the US cloud act.

The Japan Digital Sovereignty Market

The Japan Digital Sovereignty Market is projected to be valued at USD 2.3 billion in 2026. It is further expected to witness robust growth, holding USD 6.4 billion in 2035 at a CAGR of 12.0%. The Japanese market indicates a unique attitude to the digital sovereignty that consists of a compromise between the requirements of technological modernization and the ingrained fears of losing the economic security and the confidentiality of industrial and personal information. The digital sovereignty strategy in Japan is significantly driven by the Economic Security Promotion Act and its deep security relationship with the United States, which provides a subtle marketplace where companies are demanding sovereign cloud infrastructures to not only support the need to have its data in the country, but also to have access to secure and controlled data exchange with other trusted foreign partners.

The sovereign cloud platforms and data governance solutions are being significantly funded via government initiatives, such as the Gov-Cloud (Government Cloud) procurement framework and the Digital Agency promoting the adoption of modernised digital infrastructure. Increasing interest in industry-specific compliance solutions, depending on sectors like manufacturing, where the protection of intellectual property and industrial control systems information against outside access is central, and in healthcare, where protection of personal information is highly valued, is also seen in the Japanese market.

Key Takeaways

- Market Size & Forecast: The Global Digital Sovereignty market is projected to reach USD 22.8 billion in 2026, expanding significantly to USD 65.5 billion by 2035, as international political tensions, increasing data protection laws, and rising awareness of extraterritorial legal risks caused by foreign-controlled cloud infrastructure converge to drive the market growth.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 12.5%, as mandatory data residency is implemented in various jurisdictions, the complexity of operating in multi-jurisdictional compliance arises, and expertise in negotiating cross-border data transfer frameworks is urgently needed.

- Primary Growth Drivers: The main drivers of growth are the adoption of national data protection laws that follow or are more stringent than those in GDPR, the strategic need to attain infrastructure sovereignty and technical sovereignty, as well as the growing need to consult services to create detailed data localization and compliance roadmaps.

- Key Market Trends: Significant trends are the introduction of sovereign cloud platforms delivered by partnerships between global hyperscalers and local trusted entities, the adoption of advanced cryptographic mechanisms to protect and encrypt data as part of consent management systems, and transitioning to managed services to provide continuous sovereignty compliance and audit support.

- By Component Analysis: Solutions are poised to dominate the digital sovereignty market since organizations focus on secure and compliant infrastructure. Sovereign cloud, data governance, and IAM platforms are highly adopted and provide quantifiable benefits such as regulatory compliance, increased security and operational independence, which makes them the leading revenue generators.

- By Type Analysis: Cloud sovereignty is expected to lead this segment because of the growing need towards data control and jurisdictional confidence. It unites the aspects of compliance, scalability, and innovation, allowing the organizations to take advantage of the benefits of the cloud and stay governed.

- By Deployment Mode Analysis: Cloud-based deployment is poised to lead this segment as it scale advantage, flexibilities as well as compliance benefits. It makes it possible to provide real-time analytics, automation, and cost-effectiveness with data control.

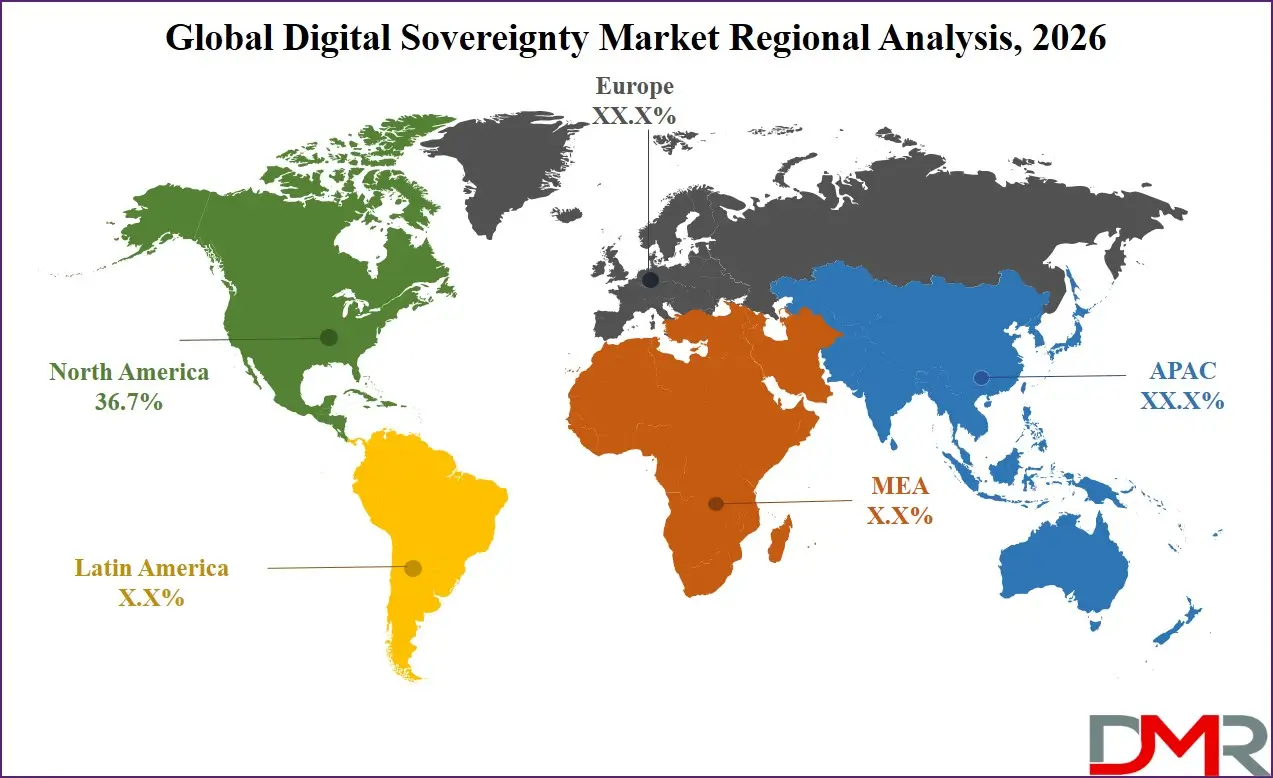

- Regional Leadership: North America is poised to dominate this market with 36.7% of the market share in 2026, due to the high numbers of hyperscale cloud providers, developed digital infrastructure, and early adopters of sovereign cloud and data governance models.

What is the Digital Sovereignty?

Digital Sovereignty is the ability of states, institutions and individuals to exert free authority over their digital property, information, and technological infrastructure without excessive reliance on or exposure to external jurisdiction, law, or corporate entities. The Digital Sovereignty Market is the overall portfolio of solutions and services that facilitate and maintain this control. These are Sovereign Cloud Platforms that make sure that data is not over the territorial jurisdiction of trusted local authorities, Data Governance Platforms that provide automated classification, tracking, and enforcement of sensitive information in hybrid configuration, and Identity and Access management (IAM) systems that implement jurisdiction-aware access control.

Consulting Services, Integration and Deployment, and Managed Services are professional services that are needed in this market to deal with the complex legal, technical, and operational aspects of attaining and sustaining digital sovereignty. As more than three-quarters of the world GDP is now subject to some degree of data localization demand, digital sovereignty solutions are becoming less of a fringe compliance issue, and more of an infrastructure of enterprise and nation-state security.

Use Cases

- Government Secure Cloud for Citizen Data: National and regional government agencies implement sovereign cloud platforms and data governance platforms to store data on citizen records, tax information, and social services.

- Cross-Border Financial Services Compliance: Hospital networks and health information exchanges adopt data protection and encryption systems coupled with a consent management platform to gain access to protected health information (PHI) and allow the sharing of data in a compliant manner to support research and care coordination.

- Healthcare Data Protection and Interoperability: Hospital networks and health information exchanges implement data protection and encryption solutions integrated with consent management platforms to secure protected health information (PHI) while enabling compliant data sharing for research and care coordination.

- Manufacturing Intellectual Property Safeguarding: Global manufacturing companies implement on-premise sovereign cloud platforms and IAM to secure proprietary design files, production process data and industrial control system configurations.

How AI is Transforming the Digital Sovereignty Market?

The emerging global environment of data protection laws, economic security policies and geopolitical competitions is radically altering the digital sovereignty market. The growth in the number of detailed data protection legislations, where more than 160 countries now have in some form of data protection law, is forming a confusing network of compliance requirements that companies have to overcome. Each of these regulations has unique data residency, cross-border transfer, and individual rights management requirements, including GDPR, China's PIPL, Brazil's LGPD, and India's Digital Personal Data Protection Act, which prompts the need to use an advanced data governance infrastructure that can comply with multiple jurisdictions simultaneously.

At the same time, the weaponization of economic interdependence and the issue of technology supply chain security are driving investments in technical sovereignty and infrastructure sovereignty. Governments are also requiring that essential digital infrastructure such as cloud services supplied by government entities and operators of essential services must be offered by entities subject to national legal jurisdiction and free of foreign ownership or control that could affect national security.

Market Dynamics

Key Drivers in the Global Digital Sovereignty Market

Proliferation of Mandatory Data Localization Laws

The governments of countries all over the world are starting to pass laws that specifically mandate that some types of information, especially personal details of citizens, government data, data of financial transactions and health data, should be stored and processed only within national borders. These data localization requirements impose a non-discretionary compliance requirement on organizations with business operations in impacted jurisdictions, and directly lead to investment in sovereign cloud platforms, data residency solutions, and the consulting services to design compliant infrastructure. The trend does not seem to be slowing down and new localization requirements are being proposed or implemented every year in Asia, Middle East, Africa, and Latin America.

Geopolitical Risk and Extraterritorial Legal Exposure

Geopolitical tensions and the broad scope of the laws like the US CLOUD Act, which provides the authority to the US law enforcement to force the technology companies to release the data stored anywhere on the planet, have made the vulnerability of jurisdiction more conscious to non-US governments and businesses. Organizations are becoming more aware of the fact that dependence on cloud infrastructure that is controlled by foreigners subjects sensitive information and core operations to foreign legal coercion, imposition of economic sanctions, and intelligence gathering efforts. Such a risk perception is a strong driver towards investment in digital sovereignty solutions that offer legally-defensible isolation against extraterritorial jurisdiction.

Restraints in the Global Digital Sovereignty Market

High Cost and Complexity of Sovereign Infrastructure

Realising digital sovereignty, especially infrastructure sovereignty, can frequently require substantial investments in purpose-built, physically distinct data centres and cloud systems. They are generally non-hyperscale environments that do not achieve the large economies of scale of the global hyperscale providers of a public cloud, which makes the cost of operations of compute, storage and networking resources more expensive. Integrating sovereign platforms with the existing enterprise IT environments and keeping pace with feature and innovation velocity with the global public cloud presents significant technical and financial burdens, which may discourage adoption, particularly in small and medium-sized businesses.

Fragmentation and Interoperability Challenges

The digital sovereignty principle of establishing separate, jurisdictionally constrained digital spaces is an antithesis to the global, borderless design of the internet and contemporary digital commerce. The emergence of national and regional sovereign cloud infrastructures poses a threat of a splinternet of fractured data and applications in which data and applications cannot easily cross borders. In the case of multinational enterprises, there is high operational overhead in overcoming this fragmentation and constrained capabilities of exploiting global data analytics, AI model training and unified business processes.

Growth Opportunities in the Global Digital Sovereignty Market

Trusted Sovereign Cloud Partnerships

Major expansion prospect includes the establishment and functioning of sovereign cloud frameworks offered by organized collaborations between worldwide hyperscalers and neighborhood, confided organizations. This model enables countries and businesses to enjoy the superior technology, ongoing innovation and global ecosystem of large-scale cloud providers and meet legal and policy demands of data residency and operational control by a domestic organization. The expertise needed to design, rule and operate these complicated forms of partnership constitute a large and burgeoning segment of the market.

AI Governance and Sovereign AI Infrastructure

With the acceleration of AI usage, states and businesses have started to prioritize the assurance that the data on which AI models are trained and run is national sovereign and compliant with regulatory norms. This is leading to the need of sovereign AI infrastructure, dedicated cloud providers with hardware accelerators and data governance controls to support the creation of AI applications and to ensure that training data and model outputs are not outside of their jurisdictional scope. AI governance, data provenance and model compliance consulting services in a sovereignty context is a high-growth niche.

Trends in the Global Digital Sovereignty Market

Emergence of Confidential Computing for Sovereignty

Confidential computing technologies, where the trusted execution environments are hardware-based, and data is encrypted during processing in memory, are becoming a popular technical enabler of digital sovereignty. Confidential computing has a technical protection to keep data inaccessible even to the administrators or hypervisor of the cloud provider, which can be used to strengthen or even replace physical data residency requirements in some scenarios. The development of sovereign cloud solutions and the introduction of a new sovereign cloud platform together with confidential computing capabilities are one of the main trends that allow creating new models of secure cross-border data collaboration.

Standardization of Sovereignty Controls and Certifications

The market is slowly shifting towards a more standardized notion of what is an acceptable degree of digital sovereignty. Programs like the European Cybersecurity Certification Scheme of Cloud Services (EUCS) are meant to develop a standard scheme of evaluating and certifying the sovereignty properties of cloud services. The introduction of established certifications of sovereignty and attestations will contribute to minimizing confusion on the part of buyers, simplifying procurement procedures, and developing better competitive differentiation between solution vendors, which will speed up the overall market maturing process.

Research Scope and Analysis

The digital sovereignty market is driven by solutions-led growth, cloud sovereignty adoption, data control requirements, and government demand, with strong emphasis on compliance, security, and regulated digital infrastructure across industries.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

The digital sovereignty market is poised to be dominated by solutions as organizations focus on creating secure, compliant, and autonomous digital infrastructures. Sovereign cloud platforms, data governance platforms and identity and access management (IAM) are sub-segments that are experiencing high adoption as regulatory pressures and data protection needs continue to increase. Business and governments are making massive investments in end to end platforms that facilitate the ability to control data storage, data processing and access at national or regional borders. Although services such as consulting, integration, and managed services become very important in the supporting role, they are highly reliant on solution deployment cycles. This capability of solutions to provide quantifiable results like compliance assurance, improved security, and operational autonomy makes this segment the main revenue generator in industries.

By Type Analysis

The type segment is expected to be dominated by cloud sovereignty as the shift to cloud infrastructure is faster and the fear of loss of control of data and risk of jurisdiction is increasing. Companies are increasingly requiring infrastructure, platform, and application-level sovereignty to make sure sensitive information is controlled by the national or organizational level. This has given rise to sovereign cloud services in collaboration with local organizations and governments. Although the localization of data and regulatory compliance are critical, cloud sovereignty offers a more holistic approach, which combines compliance, scalability, and innovation. It allows businesses to make use of the advantages of the cloud without neglecting the need to manage data governance. With the acceleration of the digital transformation process in the global arena, cloud sovereignty emerges as the foundation of the national digital strategies and enterprise IT modernization processes.

By Deployment Mode Analysis

Cloud-based deployment is projected to dominate this segment because it is compatible with the increasing demands of scalable, flexible, and compliant digital infrastructure. Sovereign cloud solutions enable organizations to have control over data, but enjoy cloud-native features like real-time analytics, automation, and remote accessibility. The use of cloud-based models is on the rise to modernize the legacy systems and facilitate cross-border transactions in regulated environments by governments and businesses. Cloud-based solutions are more appealing to large-scale digital sovereignty projects than on-premises solutions since they can be implemented faster, are cheaper initially, and updated regularly. Furthermore, alliances between hyperscalers and regional vendors are raising confidence towards cloud environments, which is further boosting the adoption and making cloud-based deployment the mainstream segment.

By Functionality Analysis

Data sovereignty is poised to dominate the functionality segment since it embodies the fundamental purpose of all digital sovereignty programs, which is to ensure that data is controlled, stored, and processed within particular legal jurisdictions. To address the needs of national regulations and to avoid geopolitical risks, organizations emphasize such capabilities as the ability to manage data residency and control its lifecycle and secure access to data. Technical sovereignty (infrastructure independence) and operational sovereignty (vendor autonomy) are increasingly becoming important, but are frequently practiced towards more comprehensive data sovereignty objectives. The growing amount of sensitive data, combined with strict regulatory frameworks, is necessitating the need to have solutions that would offer full visibility and control of data flows. Consequently, the most essential and popular functionality that has been widely used across sectors is data sovereignty.

By Industry Vertical Analysis

Government and defense is projected to dominate the digital sovereignty market as they have a strong demand to have a secure and sovereign control of national data and digital infrastructure. These industries deal with very sensitive data concerning national security, intelligence and administration of people and adherence to data sovereignty rules is not negotiable. Governments are taking the lead in investing in sovereign cloud, national databases and regulatory systems to achieve digital sovereignty and vulnerability to external threats. Even though other sectors like BFSI, healthcare, and IT and telecommunications are quickly moving towards digital sovereignty solutions, government regulations and policies tend to affect their efforts. The fact that government and defense are the key market drivers is due to the strategic role of safeguarding national interests and data control.

The Global Digital Sovereignty Market Report is segmented on the basis of the following:

By Component

- Solutions

- Sovereign Cloud Platforms

- Data Governance Platforms

- Identity & Access Management (IAM)

- Services

- Consulting Services

- Integration & Deployment

- Managed Services

By Type

- Data Localization

- Mandatory Data Residency

- Data Replication & Storage Controls

- Data Sovereignty Compliance

- National Regulations Compliance

- Cross-border Data Transfer Governance

- Cloud Sovereignty

- Infrastructure Sovereignty

- Platform Sovereignty

- Application Sovereignty

- Regulatory Compliance

- GDPR & Regional Framework Alignment

- Industry-specific Compliance

- Data Privacy

- Consent Management

- Data Protection & Encryption

By Deployment Mode

By Functionality

- Data Sovereignty

- Technical Sovereignty

- Operational Sovereignty

By Industry Vertical

- IT & Telecommunications

- Government & Defense

- BFSI (Banking, Financial Services, Insurance)

- Healthcare

- Energy & Utilities

- Manufacturing

- Others

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global digital sovereignty market, projected to hold 36.2% of the market share by the end of 2026. This leadership position in the region is backed up by its very developed digital infrastructure and a good representation of the major cloud providers, including Amazon Web Services, Microsoft Azure, and Google Cloud. The area enjoys the advantage of early adopting cloud computing, AI, and cybersecurity technologies and allows enterprises to build sovereign-ready architecture. Moreover, strong investment capacity, well-established regulatory environments, and the growing issues surrounding data privacy and national security are driving the need to demand controlled data environments. Localized data processing, secure cloud configurations, and compliance-driven infrastructure are some other areas that governments and enterprises are concentrating on. The ecosystem is further reinforced with strategic partnerships between public institutions and private technology providers in North America, which is a major contributor of revenue and an innovation centre in the changing digital sovereignty environment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific will be the fastest-growing market of digital sovereignty, motivated by a surge of novel and more restrictive data protection and localization regulations passed by the key economies in the area. The Personal Information Protection Law of China (PIPL), Data Security Law (DSL), and Cybersecurity Law have created one of the most restrictive and thorough data governance regimes in the world, where data is required to be mainly localized and monitored by the government. The Digital Personal Data Protection Act of India brings new limitations on cross-border data transfer and gives the government a lot of rule-making power. Indonesia, Vietnam, South Korea and Australia are all enacting or reinforcing their own data sovereignty models. The regulatory rush is forcing both local businesses and multinational organizations doing business within the area to radically re-architect their data infrastructure and pour significant resources into sovereign cloud solutions, data governance systems, and domestic compliance expertise.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The digital sovereignty market competition is a place where a very intricate balance exists between the global hyperscale cloud providers, regional and nationwide telecommunications and technology champions, specialist software vendors, and systems integrators and consulting firms. To address sovereignty requirements, the largest global cloud providers, such as AWS, Microsoft Azure, and Google Cloud, are creating dedicated sovereign cloud solutions, often via collaborations with locally trusted partners or physically and logically separated regions that can fulfill certain government and regulatory needs. At the same time, European powerhouses like OVHcloud, Deutsche Telekom (T-Systems) and Orange Business Services are also establishing themselves as naturally sovereign options, using their European ownership and presence as a competitive differentiator. Market champions are also becoming national in places like India, Middle East, and Asia, with the government policy and procurement preferences usually supporting them.

Some of the prominent players in the Global Digital Sovereignty Market are:

- Microsoft

- Amazon Web Services (AWS)

- Google Cloud

- IBM

- Oracle

- Cisco

- SAP

- Nutanix

- Red Hat

- VMware

- OVHcloud

- T-Systems

- Orange Business

- Atos

- Thales

- Capgemini

- Infosys

- Wipro

- Cloud4C

- Nextcloud

- Other Key Players

Recent Developments

- March 2026: AWS introduced the general availability of its European Sovereign Cloud, a physically and logically isolated cloud area, fully within the European Union and managed by an entity within the EU, and specifically to satisfy the demanding data residency and operational sovereignty needs of its European public sector and highly regulated clientele.

- December 2025: Microsoft has added more features to its Cloud for Sovereignty service to offer more policy-driven data residency enforcement, integration of confidential computing to protect data-in-use, and new transparency logs that give customers verifiable attestations about access to their data by Microsoft staff.

- September 2025: OVHcloud, a major European cloud provider, has also announced a strategic collaboration with multiple European defense contractors to build a specifically designed, highly secured sovereign cloud platform to host classified defense and national security workloads, in full compliance with NATO and national security guidelines.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 22.8 Bn |

| Forecast Value (2035) |

USD 65.5 Bn |

| CAGR (2026–2035) |

12.5% |

| The US Market Size (2026) |

USD 7.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component (Solutions, Services), By Type (Data Localization, Data Sovereignty Compliance, Cloud Sovereignty, Regulatory Compliance, Data Privacy), By Deployment Mode (On-Premises, Cloud-Based), By Functionality (Data Sovereignty, Technical Sovereignty, Operational Sovereignty), By Industry Vertical (IT & Telecommunications, Government & Defense, BFSI (Banking, Financial Services, Insurance), Healthcare, Energy & Utilities, Manufacturing, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Digital Sovereignty Market?

▾ The Global Digital Sovereignty market is poised to be valued at USD 22.8 billion in 2026 and is projected to reach USD 65.5 billion by 2035, driven by the universal imperative for nations and enterprises to assert control over their data and digital infrastructure in an era of heightened geopolitical tension and regulatory enforcement.

What is the CAGR of the Global Digital Sovereignty Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 12.5% from 2026 to 2035, reflecting the accelerating enactment of data localization laws worldwide and the growing strategic priority placed on infrastructure sovereignty and technical sovereignty.

What factors are driving the growth of the Global Digital Sovereignty Market?

▾ Key drivers include the proliferation of mandatory data residency laws, rising awareness of extraterritorial legal risks associated with foreign-controlled cloud providers, and strategic autonomy imperatives in critical sectors such as government, defense, finance, and healthcare.

What is the CAGR of the Global Healthy Snacks Market from 2026 to 2035?

▾ The market is growing at a CAGR of 6.8% over the forecasted period.

Which region is expected to grow the fastest in the Digital Sovereignty Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by the rapid implementation of stringent data protection and localization laws in China, India, Indonesia, and other major economies, compelling significant investment in compliant sovereign infrastructure.

What are the major trends in the Global Digital Sovereignty Market?

▾ Major trends include the emergence of trusted sovereign cloud partnerships between global hyperscalers and local entities, the integration of confidential computing to strengthen technical assurances of data protection, and the development of standardized sovereignty certifications such as EUCS.

Who are the key players in the Global Digital Sovereignty Market?

▾ Key players include global cloud providers adapting to sovereignty demands (AWS, Microsoft, Google), European sovereign cloud champions (OVHcloud, T-Systems, Orange), specialized software and security vendors (Thales), and global system integrators providing critical consulting and deployment expertise (Accenture, Deloitte, Capgemini).

How is the Global Digital Sovereignty Market segmented?

▾ The market is segmented by Component, type, Deployment Mode, Functionality, and Industry Vertical.