Market Overview

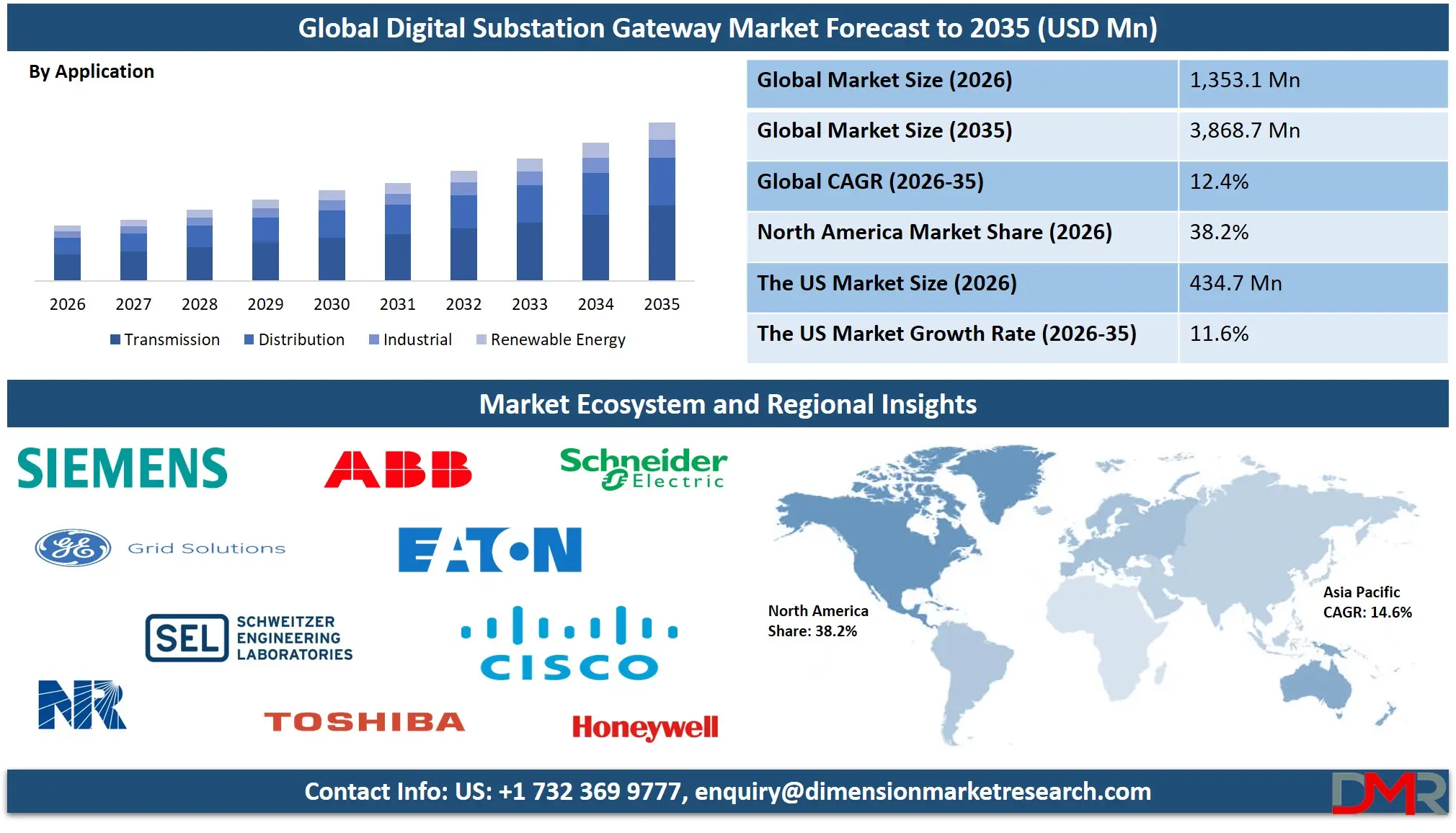

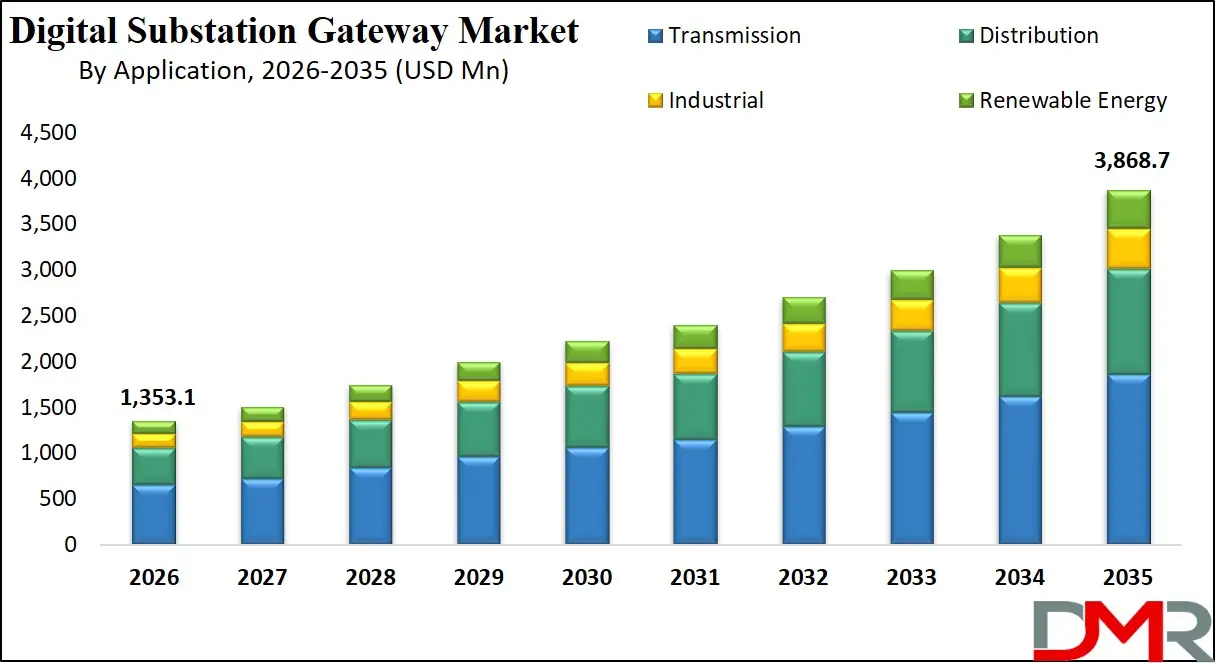

The Global Digital Substation Gateway Market is projected to reach USD 1,353.1 million in 2026 and grow at a compound annual growth rate of 12.4% from there until 2035 to reach a value of USD 3,868.7 million.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

A digital substation gateway serves as a critical communication and data management node within modern electrical substations. It facilitates secure and standardized data exchange between intelligent electronic devices (IEDs), control systems, and utility networks by translating between various industrial communication protocols. This enables real-time monitoring, control, and protection of power assets, enhancing grid reliability, operational efficiency, and cybersecurity. By aggregating and converting data from legacy and new systems, digital gateways are foundational to the transition toward fully digital, interoperable, and data-driven substation automation architectures.

The global digital substation gateway market encompasses the worldwide industry providing hardware, software, and services that enable protocol conversion, data aggregation, and secure communication within digital and hybrid substations. This market includes a range of providers from specialized industrial communication firms to broad automation solution vendors. Growth is fueled by global investments in smart grid infrastructure, the replacement of aging electromechanical systems, and stringent regulatory mandates for grid reliability and cybersecurity. The expansion of distributed energy resources (DERs) and the need for seamless integration further propel demand for advanced gateway solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market is also being shaped by technological advancements in edge computing, cloud integration, and artificial intelligence. Modern gateways are evolving into intelligent edge devices capable of local data processing, analytics, and decision-making. Simultaneously, the increasing focus on cybersecurity within critical infrastructure is driving the adoption of gateways with built-in advanced security features, positioning them as essential components for both operational excellence and resilient grid management.

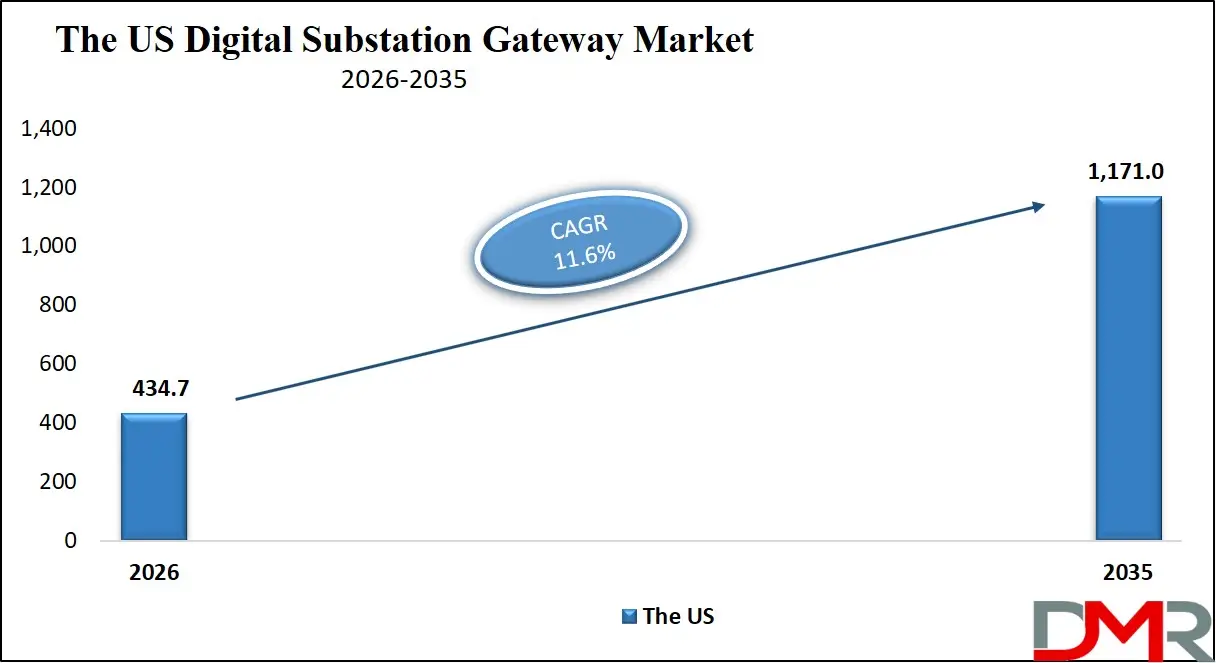

The US Digital Substation Gateway Market

The US Digital Substation Gateway Market is projected to reach USD 434.7 million in 2026 at a compound annual growth rate of 11.6% over its forecast period.

The US market is a critical driver, supported by substantial investments in grid modernization initiatives, aging infrastructure replacement, and stringent reliability standards set by organizations like NERC. The presence of a large and complex transmission & distribution network, coupled with a growing penetration of renewable energy, creates strong demand for interoperable and secure communication solutions. Utilities and independent system operators (ISOs) are increasingly deploying digital gateways to enable IEC 61850 standardization, integrate distributed energy resources, and enhance situational awareness.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market is further strengthened by rapid technological adoption, including the integration of cybersecurity frameworks and cloud-based asset management platforms. A robust ecosystem of technology providers, engineering firms, and system integrators allows for comprehensive solution deployment, from new greenfield projects to brownfield retrofits.

The Europe Digital Substation Gateway Market

The Europe Digital Substation Gateway Market is expected to reach USD 325.0 million in 2026, supported by the region's leadership in energy transition, ambitious carbon neutrality goals, and well-established standards like IEC 61850. Countries such as Germany, the UK, France, and the Nordic nations are at the forefront of digital substation deployment, driven by the integration of wind and solar power, grid decentralization, and cross-border interconnection projects.

A CAGR of 12.8% indicates sustained growth, fueled by EU funding for smart grid projects and regulations emphasizing grid digitalization and cybersecurity. The retrofit of existing substations to digital standards represents a significant market segment. European providers are also pioneering the integration of gateways with energy management systems and digital twins, enhancing grid optimization and predictive maintenance capabilities.

The Japan Digital Substation Gateway Market

The Japan Digital Substation Gateway Market is expected to reach USD 78.0 million in 2026, driven by the need for grid resilience following natural disasters, the integration of a growing renewable energy base, and a strong focus on technological precision and reliability. Japan's advanced manufacturing and technology sector supports the development and deployment of high-quality gateway hardware and software.

A CAGR of 13.0% reflects the accelerated pace of digital substation adoption. Utilities are investing in gateway solutions to modernize legacy infrastructure, improve energy efficiency, and facilitate the stable integration of solar and other distributed resources. The adoption of advanced communication protocols and cybersecurity measures is a key priority, strengthening the long-term market outlook.

Global Digital Substation Gateway Market: Key Takeaways

- Grid Modernization Driving Sustained Double-Digit Growth: The market is projected to grow from USD 1,353.1 million in 2026 to USD 3,868.7 million by 2035 at a robust CAGR of 12.4%, underpinned by unprecedented global investment in aging grid infrastructure replacement and the strategic imperative to digitalize transmission and distribution networks for enhanced reliability and operational efficiency.

- Asia-Pacific Emerges as the Decisive Growth Engine: While North America maintains revenue leadership through 2035, Asia-Pacific delivers the highest CAGR, driven by China's State Grid digitalization mandate, India's Green Energy Corridor investments, and ASEAN nations' aggressive grid expansion programs, collectively representing the largest addressable opportunity for new entrant and established vendors alike.

- Renewable Integration as the Primary Demand Catalyst: The exponential growth of utility-scale solar, wind, and battery storage assets is creating non-negotiable requirements for interoperable communication gateways, positioning this application segment as the fastest-growing revenue stream and making gateways indispensable for grid compliance and stable variable renewable energy integration.

- Interoperability Standards (IEC 61850) Are Unifying the Ecosystem: The widespread adoption of IEC 61850 is reducing integration complexity and vendor lock-in, making gateways essential for creating future-proof, multi-vendor digital substation environments.

- Brownfield Retrofits Represent a Major Market Opportunity: The need to extend the life and capabilities of existing substations is driving significant demand for gateway solutions designed for seamless integration into legacy brownfield environments.

Global Digital Substation Gateway Market: Use Cases

- Transmission Grid Modernization: Utilities deploy digital gateways in transmission substations to enable wide-area monitoring, real-time control, and seamless communication between Phasor Measurement Units (PMUs), relays, and SCADA systems, enhancing grid stability and fault response.

- Distribution Automation for DER Integration: At the distribution level, gateways aggregate data from smart inverters, reclosers, and feeders, facilitating the visibility and management of distributed solar, wind, and storage resources.

- Industrial Microgrid Management: Industrial enterprises use substation gateways as the communication backbone for campus microgrids, coordinating between on-site generation, storage, and the main grid to ensure power quality and optimize energy costs.

- Renewable Energy Plant Grid Connection: Solar and wind farm operators utilize gateways at the point of interconnection substation to comply with grid codes, provide necessary telemetry to grid operators, and ensure stable plant operation.

Global Digital Substation Gateway Market: Stats & Facts

- International Energy Agency (IEA)

- Global investment in electricity grids increased by 10% year-over-year in 2024, reaching approximately USD 375 billion, with over 25% allocated to digitalization and automation infrastructure.

- The global integration capacity for variable renewable energy (VRE) such as wind and solar grew from 1,200 GW in 2023 to over 1,900 GW by the end of 2025, driving a corresponding 40% increase in demand for advanced communication and control systems like digital substation gateways.

- U.S. Department of Energy (DOE)

- Federal funding for grid resilience and smart grid initiatives under the Grid Deployment Office rose by 18.3% from FY2023 to FY2024, with USD 3.2 billion allocated to digital substation and grid-edge automation projects.

- The Energy Information Administration (EIA) reported that the number of U.S. utilities implementing digital substation pilots or full-scale deployments grew from 47 in 2023 to 89 by the end of 2025, representing a 90% increase over two years.

- European Network of Transmission System Operators for Electricity (ENTSO-E)

- According to the ENTSO-E Ten-Year Network Development Plan (TYNDP) 2024, over 65% of planned substation investments across Europe now include digitalization components, with IEC 61850 compliance mandated in 42% of all new and retrofit substation tenders as of 2024.

- Cross-border interconnection projects under the Connecting Europe Facility (CEF) have driven a 30% year-over-year increase in procurement of interoperable digital communication systems since 2023, with gateway solutions featuring prominently in key corridors such as North Sea Wind Power Hub and the Iberian Peninsula–France interconnection.

- Asia Pacific Energy Research Centre (APERC)

- Grid modernization investments across the APEC region totaled USD 220 billion from 2023–2025, with China, India, and ASEAN member states accounting for 78% of this expenditure. Over 35% was directed toward automation, digital substations, and communication networking.

- The proportion of digital vs. conventional greenfield substation projects in Asia Pacific shifted from 28% in 2022 to 52% by 2025, with China’s State Grid Corporation alone planning over 800 fully digital substations by 2030.

- Japan Ministry of Economy, Trade and Industry (METI)

- Under the Green Transformation (GX) Promotion Strategy, Japan allocated approximately USD 14 billion toward grid digitalization and resilience from 2024–2028, with a focus on substation automation and cybersecurity.

- The number of digital substation gateway installations in Japan grew by 22% annually from 2023–2025, driven by regulatory updates from the Organization for Cross-regional Coordination of Transmission Operators (OCCTO) requiring enhanced grid monitoring and renewable integration capabilities.

- International Renewable Energy Agency (IRENA)

- IRENA’s World Energy Transitions Outlook 2025 highlighted that digital substation and grid-edge automation technologies could reduce grid integration costs for renewables by up to 20%, accelerating the business case for investments in solutions such as protocol gateways and data aggregators.

Global Digital Substation Gateway Market: Market Dynamic

Driving Factors in the Global Digital Substation Gateway Market

Accelerated Grid Modernization and Investment

Global investment in smart grid infrastructure has surged as utilities prioritize replacing outdated systems. This is fueled by mandates for reliability, renewable integration, and cybersecurity. Governments and regulators worldwide are backing grid upgrades through significant funding initiatives, particularly in regions like North America and Europe. The transition from conventional to digital substations creates a sustained, high-value demand for communication gateways. These gateways form the foundational layer for all subsequent automation and monitoring systems. Consequently, every major grid modernization project now incorporates a substantial budget for digital communication components. This continuous investment cycle establishes a powerful, long-term driver for the gateway market’s expansion.

Rise of Distributed Energy Resources and Renewable Integration

The unprecedented global growth of solar, wind, and battery storage is fundamentally reshaping power grids. These distributed and variable resources require real-time visibility and precise control to maintain grid stability. Digital substation gateways provide the essential protocol translation and data aggregation needed to integrate these assets. They enable inverters, meters, and controllers to communicate seamlessly with utility management systems. Without this interoperability, the large-scale integration of renewables would be technically and economically challenging. Therefore, the clean energy transition directly translates into escalating demand for advanced gateway solutions. This driver is especially potent in high-growth markets across Asia-Pacific and Europe.

Restraints in the Global Digital Substation Gateway Market

High Initial Investment and Integration Complexity

The total deployment cost extends beyond hardware to include expensive software licenses and specialized engineering services. Retrofitting brownfield substations adds technical difficulty and risk. Integrating new gateways with legacy systems demands meticulous planning and can cause unexpected downtime. These financial and technical hurdles slow procurement cycles, particularly for smaller utilities with constrained budgets. The complexity acts as a significant barrier to widespread adoption.

Cybersecurity Concerns and Skills Shortage

As critical data conduits, gateways represent attractive targets for cyber-attacks on grid infrastructure. A successful breach could lead to widespread outages, creating immense regulatory and reputational risk. This necessitates built-in advanced security features, increasing product cost and complexity. Furthermore, there is a global shortage of engineers skilled in both operational technology and cybersecurity. This skills gap forces increased reliance on expensive external consultants, delaying or scaling back digitalization projects.

Opportunities in the Global Digital Substation Gateway Market

Adoption of Edge Computing and IIoT Platforms

The Industrial Internet of Things (IIoT) is transforming gateways from simple converters into intelligent edge devices. Modern gateways now feature local processing power to run analytics and make autonomous control decisions. This reduces latency, minimizes bandwidth needs, and enhances grid responsiveness. Providers are offering new value-added services like predictive analytics for transformer health based on gateway data. This evolution unlocks premium pricing models and deeper integration with utility IT strategies. The ability to process data at the source is becoming a key differentiator among vendors. This trend is creating a new market segment focused on computational power and advanced software capabilities at the edge.

Growth in Microgrids and Virtual Power Plants

The decentralization of power generation accelerates microgrid and Virtual Power Plant deployment. Each microgrid requires its own sophisticated communication hub, typically built around a substation gateway. This creates replicated demand for gateway technology across countless new sites. Similarly, VPPs depend on secure data aggregation from numerous dispersed assets. This emerging application represents a high-growth, diversified market beyond traditional utility substations. It drives demand for more compact, scalable, and easily deployable gateway solutions.

Trends in the Global Digital Substation Gateway Market

Convergence of Operational and Information Technology

Gateways are the pivotal hardware enabling the closure between OT grid operations and IT business systems. They provide a secure, standardized data pipeline from substation to cloud platforms. This allows for holistic asset performance management and data-driven grid optimization. The trend demands that vendors ensure compatibility with major IT systems and data protocols. As utilities pursue unified data strategies, the gateway’s role as an IT/OT bridge becomes indispensable. This convergence makes the gateway a strategic component of the entire digital architecture.

Shift Toward Software-Defined Functionality

The core value proposition of gateways is increasingly defined by their software, not their hardware. Features like protocol support, cybersecurity policies, and data handling rules are now configurable via software. This allows for remote updates and feature upgrades without physical intervention, extending product lifecycles. Vendors are consequently shifting toward service-based models, including software subscriptions and cloud management platforms. This trend reduces reliance on cyclical hardware sales and creates recurring revenue streams. It also lowers barriers for utilities to trial and scale new functionalities. Ultimately, competition is pivoting toward software innovation, ecosystem partnerships, and the quality of digital services offered.

Global Digital Substation Gateway Market: Research Scope and Analysis

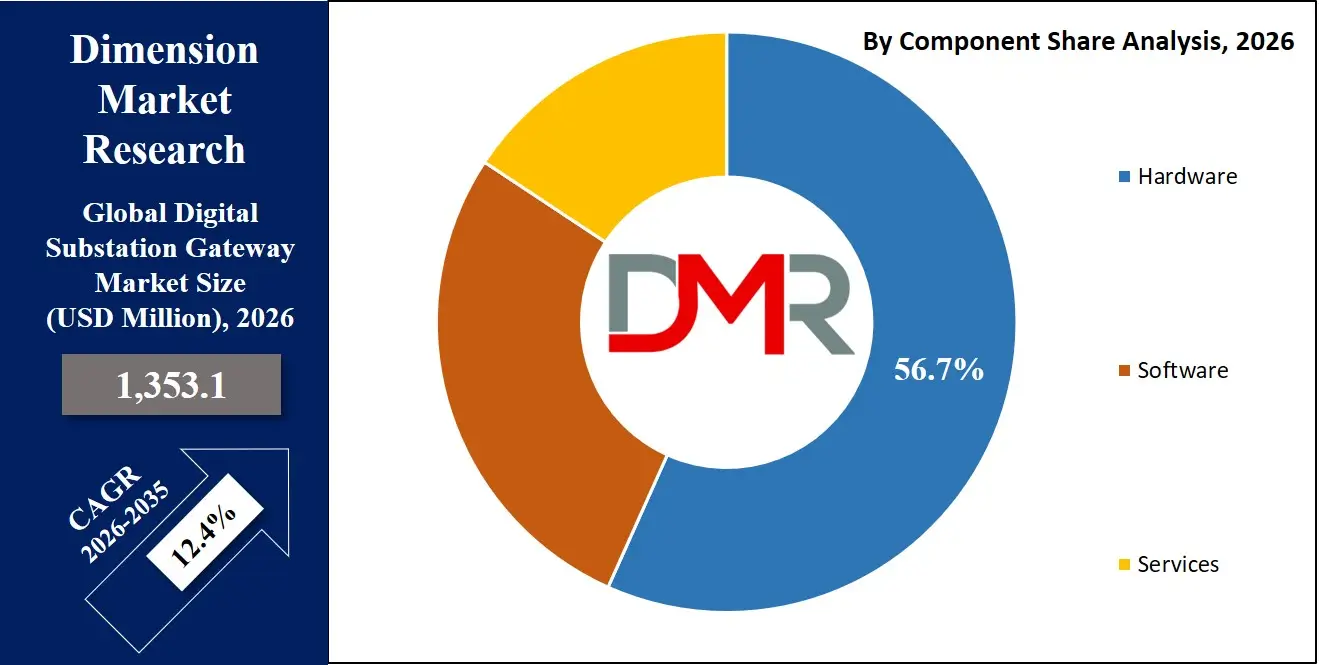

By Component Analysis

Hardware, encompassing protocol gateways, communication interfaces, and embedded data aggregators, is expected to dominate the component segment by holding 56.7% of the total market share in 2026. This dominance is rooted in the fact that physical gateway units form the essential, non-negotiable foundation of any digital substation deployment, providing the critical interface between legacy equipment and modern networks. Every substation automation project, whether a new greenfield installation or a brownfield retrofit, requires these dedicated hardware devices to perform real-time protocol conversion, data concentration, and secure communication. The growing complexity of grids integrating diverse IEDs, renewable resources, and control systems has increased reliance on robust, high-availability hardware that ensures seamless interoperability and meets stringent environmental and reliability standards, cementing this segment's leading position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Software, including protocol conversion platforms, data aggregation tools, and integrated cybersecurity suites, plays an increasingly vital role by delivering the intelligence, configurability, and security that define modern gateway functionality. This segment is the fastest-growing, as utilities seek advanced software to manage the flood of grid data, enforce cybersecurity policies, and enable remote device management and analytics. The value proposition is shifting from pure hardware to software-defined features that allow for future-proofing through updates and customization. As digital substation architectures evolve toward cloud integration and edge computing, the demand for sophisticated, scalable software solutions that can turn raw data into actionable grid intelligence continues to rise, making this segment a primary driver of innovation and competitive differentiation.

By Communication Protocol Analysis

IEC 61850 is expected to lead the communication protocol segment, capturing the largest revenue share, as it has become the globally recognized standard for interoperable substation communication and engineering. Its dominance is driven by its comprehensive framework that simplifies integration, reduces wiring costs, and enables advanced functions like GOOSE messaging and Sampled Values, which are critical for protection and automation schemes. The protocol's widespread mandate in utility specifications for new and retrofit projects worldwide ensures its continued market leadership, as it future-proofs investments and reduces vendor lock-in, making it the cornerstone of modern digital substation design.

DNP3 retains a significant and stable share, particularly in North America and for wide-area network (WAN) communications between substations and control centers. Its entrenched position in existing SCADA infrastructure and its robustness for reliable, long-distance telemetry ensure continued demand. Meanwhile, Modbus and PROFIBUS/PROFINET maintain relevance primarily within industrial substations and for interfacing with legacy field devices in brownfield retrofit scenarios, serving as crucial bridges during the transitional phase of grid modernization.

By Deployment Type Analysis

New Installations (Greenfield projects) represent a key high-value segment, driven by rapid grid expansion in emerging economies and the development of new renewable energy plants and transmission corridors. These projects allow for the deployment of fully integrated, state-of-the-art gateway solutions without legacy constraints, enabling optimal system architecture and performance. They are particularly prevalent in high-growth regions like Asia-Pacific and the Middle East, where utilities are building modern grid infrastructure from the ground up.

Retrofit/Brownfield Upgrades constitute a substantial and strategically vital segment, representing the predominant market activity in mature grids across North America and Europe. This segment addresses the critical need to enhance the functionality, monitoring, and cybersecurity of thousands of existing substations without complete overhaul. The complexity of integrating new digital gateways with legacy protection and control systems demands specialized solutions and services, creating a sustained market for backward-compatible, scalable upgrade packages that maximize existing asset lifespans while delivering digital capabilities.

By Voltage Level Analysis

High Voltage (HV) and Extra High Voltage (EHV) applications for transmission substations account for the largest portion of market revenue. Gateways deployed at these voltage levels are critical for wide-area monitoring, system protection, and bulk power transfer stability, requiring the highest levels of reliability, security, and performance. The high cost of grid failure at this tier justifies investment in premium, redundant gateway solutions, making this a technologically advanced and value-intensive segment.

The Medium Voltage (MV) segment is projected to exhibit the highest growth rate, fueled by global smart grid and distribution automation initiatives. The integration of distributed energy resources (DERs), advanced fault detection, isolation, and restoration (FDIR) schemes, and the need for granular visibility at the distribution level are driving massive deployments of gateways in MV substations and feeder circuits. This segment's expansion is central to achieving grid resilience, renewable hosting capacity, and customer-centric grid services.

By Application Analysis

Transmission Substations lead the application segment in terms of strategic importance and solution sophistication. Gateways in these nodes are essential for real-time grid management, phasor measurement, and ensuring the stability of the interconnected transmission network. The complex communication requirements and critical nature of these assets make them a primary focus for advanced gateway deployments with strong cybersecurity and interoperability features.

Renewable Energy Substations are projected to be the fastest-growing application segment. The global surge in utility-scale solar PV and wind farms necessitates specialized substation gateways at the point of interconnection (POI). These gateways manage grid compliance, power plant control, and the secure flow of generation and meteorological data to grid operators, making them indispensable for the reliable and dispatchable integration of variable renewable energy into the power system.

By End-User Analysis

Utilities, including Transmission & Distribution System Operators, remain the dominant end-user segment, responsible for the majority of market demand through large-scale, regulated grid modernization programs. Their procurement drives standardization, cybersecurity requirements, and long-term service contracts, establishing the foundational trends for the entire gateway market.

Independent Power Producers (IPPs), particularly in the renewable energy sector, constitute the most rapidly growing end-user segment. As developers and owners of wind, solar, and storage assets, IPPs require reliable, grid-code-compliant gateway solutions to ensure their plants can connect to and interact with the utility grid efficiently. Their demand is characterized by a focus on cost-effectiveness, rapid deployment, and remote management capabilities.

The Global Digital Substation Gateway Market Report is segmented on the basis of the following:

By Component

- Hardware

- Protocol Gateways

- Communication Interfaces

- Embedded Data Aggregators

- Software

- Protocol Conversion Software

- Data Aggregation Tools

- Cybersecurity Software

- Services

- Installation and Commissioning

- Cybersecurity Consulting and Monitoring

- Maintenance and Support Contracts

By Communication Protocol

- IEC 61850

- DNP3

- Modbus

- PROFIBUS/PROFINET

- Others

By Deployment Type

- New Installations

- Retrofit Brownfield Upgrades

By Voltage Level

- Low Voltage (LV)

- Medium Voltage (MV)

- High Voltage (HV)

- Extra High Voltage (EHV)

By Application

- Transmission Substations

- Distribution Substations

- Industrial Substations

- Renewable Energy Substations

By End-User

- Utilities

- Independent Power Producers (IPPs)

- Industrial Enterprises

- Commercial Establishments

Impact of Artificial Intelligence in the Global Digital Substation Gateway Market

Artificial intelligence is transforming the global Digital Substation Gateway Market by enhancing reliability, automation, and decision-making across power grids. AI-driven predictive analytics enable utilities to detect equipment anomalies, forecast faults, and optimize maintenance schedules, reducing downtime and operational costs. Machine learning-powered systems improve substation operations by analyzing real-time sensor data, enabling faster fault isolation and overall grid optimization. Enhanced monitoring supported by AI provides actionable insights for network operators, improving system resilience and efficiency.

In addition, AI facilitates autonomous substation operations, where smart controllers process sensor and communication data to manage the grid with minimal human intervention. Intelligent automation and advanced analytics reduce operational risks and human errors. By integrating AI with digital twins and IoT-enabled substation networks, stakeholders gain deeper insights into equipment performance and system bottlenecks, driving innovation and competitiveness in the global Digital Substation Gateway Market.

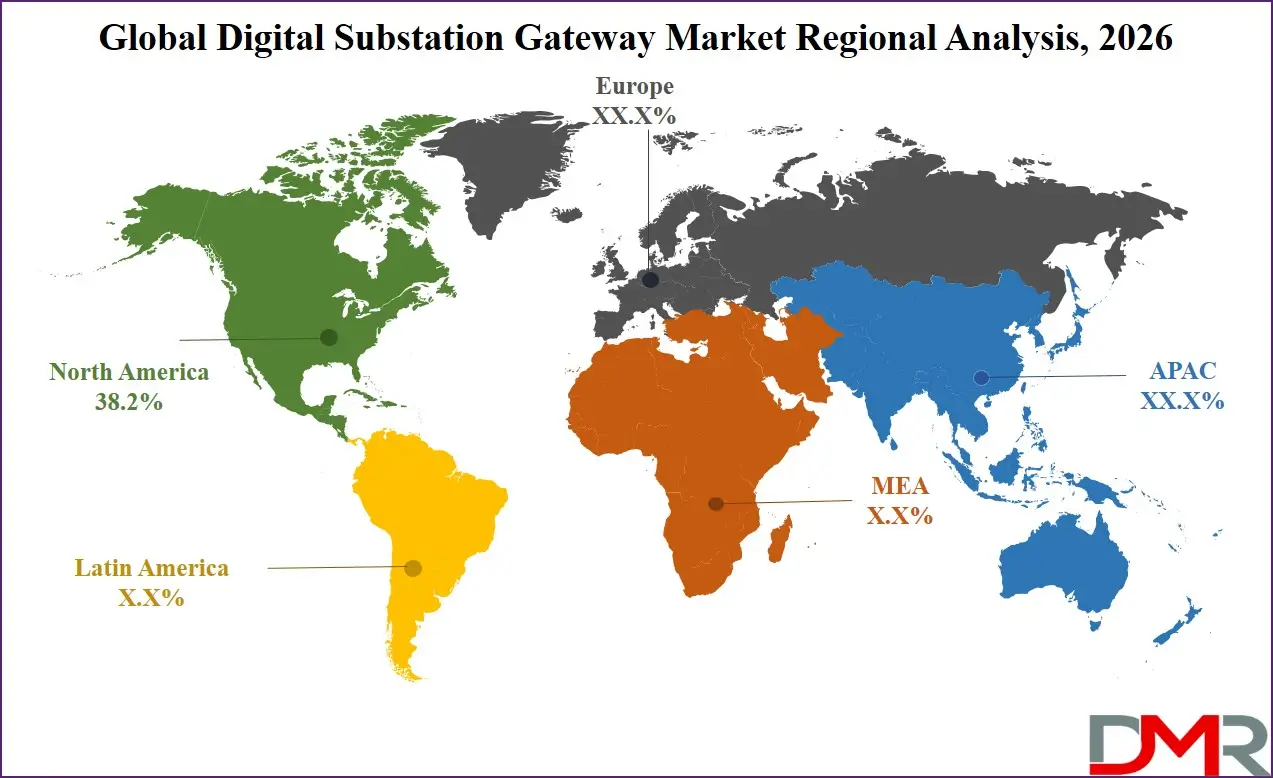

Global Digital Substation Gateway Market: Regional Analysis

Region with the Largest Revenue Share

North America is expected to lead the global Digital Substation Gateway Market with a share of 38.2% in 2026. This dominance is anchored by unprecedented regulatory and financial support for grid modernization, including the U.S. Infrastructure Investment and Jobs Act, which allocates billions specifically for grid resilience and smart infrastructure. The region hosts a mature yet aging grid network, prompting utilities to invest heavily in digital retrofits and new installations to enhance reliability and integrate renewable energy. Furthermore, North America is home to leading technology vendors and utilities that serve as early adopters, setting de facto standards for cybersecurity and interoperability. A strong culture of innovation and significant private investment in grid-edge technologies further consolidate its market position. The pressing need to harden infrastructure against climate and cyber threats continues to drive procurement, ensuring North America remains the revenue and innovation epicenter for the foreseeable future.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia-Pacific is emerging as the region with the most significant growth in the global Digital Substation Gateway Market, driven by colossal national-level investments in power infrastructure and ambitious renewable energy targets. China's State Grid and Southern Power Grid corporations are executing massive digitalization plans, incorporating thousands of digital substations as part of broader smart grid initiatives. In parallel, India’s Green Energy Corridors and Revamped Distribution Sector Scheme (RDSS) are fueling large-scale deployments to manage its rapidly expanding renewable capacity. Southeast Asian nations, along with Japan and South Korea, are aggressively modernizing grids to improve efficiency and support economic growth. This growth is further amplified by the region's leadership in electronics manufacturing, which fosters competitive supply chains and innovation in gateway hardware. The confluence of government mandates, urbanization, and the need to decarbonize energy systems positions Asia-Pacific as the primary growth engine for global market expansion through 2035.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Digital Substation Gateway Market: Competitive Landscape

The competitive landscape is characterized by the presence of global industrial automation giants, specialized power system communication vendors, and cybersecurity firms. Competition is intensifying around technological innovation, particularly in cybersecurity, edge intelligence, and software-defined capabilities. Strategic partnerships between hardware manufacturers, software developers, and system integrators are common to deliver complete solutions. The ability to provide robust, secure, and interoperable products supported by strong services is key to gaining market share.

Some of the prominent players in the Global Digital Substation Gateway Market are:

- Siemens AG

- ABB Ltd.

- General Electric (GE) Grid Solutions

- Schneider Electric SE

- Eaton Corporation plc

- Cisco Systems, Inc.

- Honeywell International, Inc.

- Schweitzer Engineering Laboratories (SEL)

- Toshiba Energy Systems & Solutions

- NR Electric Co., Ltd.

- Open Systems International (OSI)

- NovaTech LLC

- ZIV Automation

- Advantech Co., Ltd.

- Iskra Sistemi d.d.

- Locamation B.V.

- Arteche

- Belden, Inc.

- Hitachi Energy Ltd.

- ECI Telecom, Ltd.

- Other Key Players

Recent Developments in the Global Digital Substation Gateway Market

- February 2026: GE Vernova announced the launch of GridBeats APS (Automation and Protection System), a software‑defined grid automation and protection platform that simplifies substation operations by consolidating multiple protection and control applications into a single platform and reducing hardware footprint while enhancing resilience and scalability.

- February 2026: At DTECH 2026, Siemens highlighted its latest innovations in grid automation and electrification, including secure communication solutions and digital twin technologies designed to support modern substation digitalization and improve operational efficiency, transparency, and decision‑making for utilities.

- November 2025: At Enlit Europe 2025, Advantech and ecosystem partners showcased future‑proof substation automation solutions, including certified computing and connectivity platforms that support secure communication and virtualized protection, directly influencing next generation gateways and automation ecosystems.

- January 2025: Siemens launched the SICAM A8000 gateway series, supporting high‑capacity IEC 61850 communication and improved throughput for digital substation connectivity and interoperability, strengthening utility data handling capabilities.

- December 2024: Hitachi Energy announced certification and enhancements for IEC 61850 tools such as PCM600 and IET600, advancing interoperability and security in digital substation automation tools, relevant to gateway‑related integration.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1,353.1 Mn |

| Forecast Value (2035) |

USD 3,868.7 Mn |

| CAGR (2026–2035) |

12.4% |

| The US Market Size (2026) |

USD 434.7 Mn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Component (Hardware, Software and Services), By Communication Protocol (IEC 61850, DNP3, Modbus, PROFIBUS/PROFINET, Others), By Deployment Type (New Installations and Retrofit Brownfield Upgrades), By Voltage Level (Low Voltage (LV), Medium Voltage (MV), High Voltage (HV) and Extra High Voltage (EHV)), By Application (Transmission Substations, Distribution Substations, Industrial Substations and Renewable Energy Substations), By End-User (Utilities, Independent Power Producers (IPPs), Industrial Enterprises and Commercial Establishments) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Siemens AG, ABB Ltd., General Electric (GE) Grid Solutions, Schneider Electric SE, Eaton Corporation plc, Cisco Systems, Inc., Honeywell International, Inc., Schweitzer Engineering Laboratories (SEL), Toshiba Energy Systems & Solutions, NR Electric Co., Ltd., Open Systems International (OSI), NovaTech LLC, ZIV Automation, Advantech Co., Ltd., Iskra Sistemi d.d., Locamation B.V., Arteche, Belden, Inc., Hitachi Energy Ltd., ECI Telecom, Ltd., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Digital Substation Gateway Market?

▾ The Global Digital Substation Gateway Market size is estimated to have a value of USD 1,353.1 million in 2026 and is expected to reach USD 3,868.7 million by the end of 2035.

What is the growth rate in the Global Digital Substation Gateway Market in 2026?

▾ The market is growing at a CAGR of 12.4 percent over the forecasted period of 2026.

What is the size of the US Digital Substation Gateway Market?

▾ The US Digital Substation Gateway Market is projected to be valued at USD 434.7 million in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 1,171.0 million in 2035 at a CAGR of 11.6%.

Which region accounted for the largest Global Digital Substation Gateway Market?

▾ North America is expected to have the largest market share in the Global Digital Substation Gateway Market with a share of about 38.2% in 2026.

Who are the key players in the Global Digital Substation Gateway Market?

▾ Some of the major key players in the Global Digital Substation Gateway Market are Siemens AG, ABB Ltd., Schneider Electric SE, Eaton Corporation plc, Honeywell International, Inc. and many others.