Market Overview

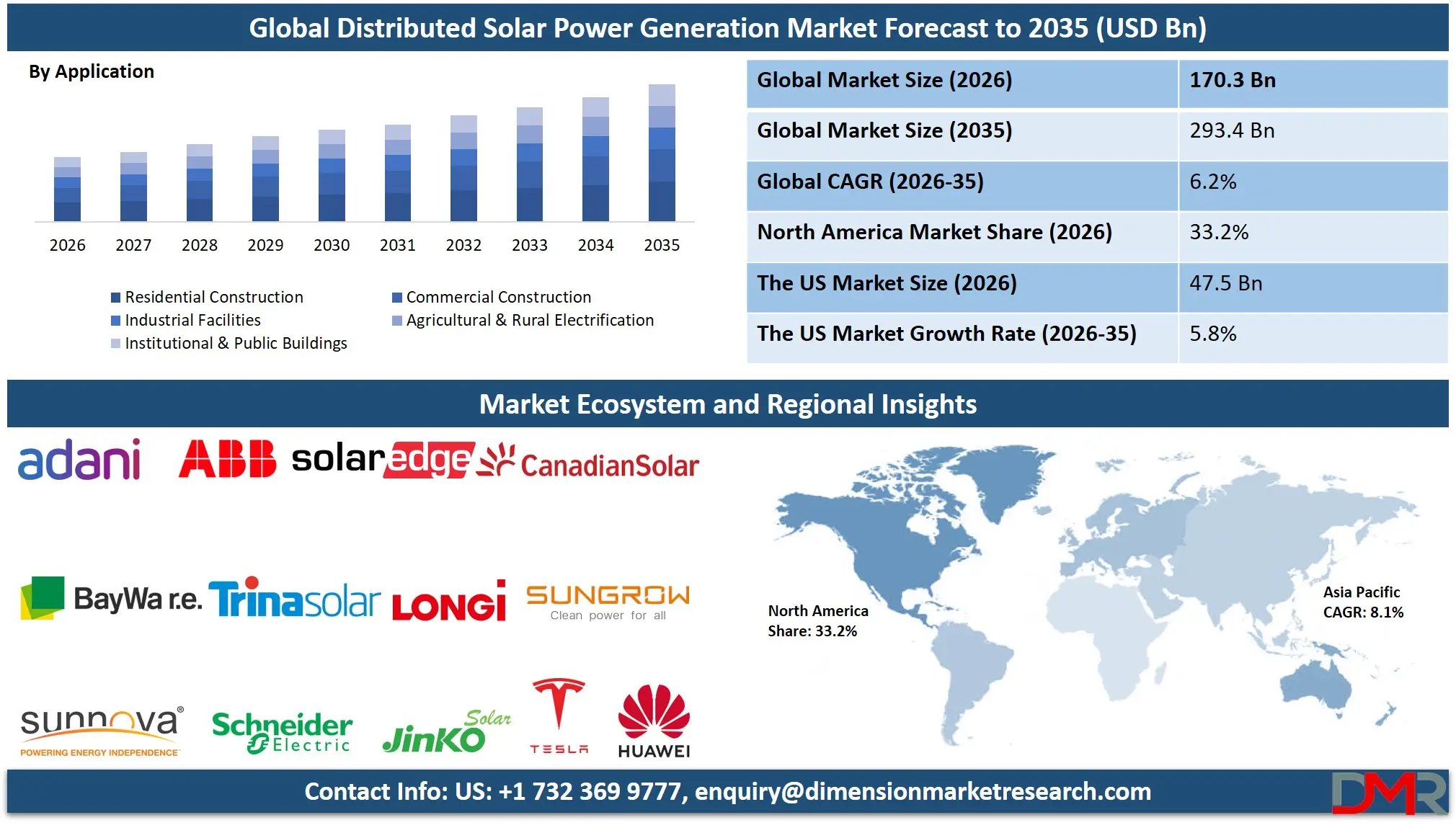

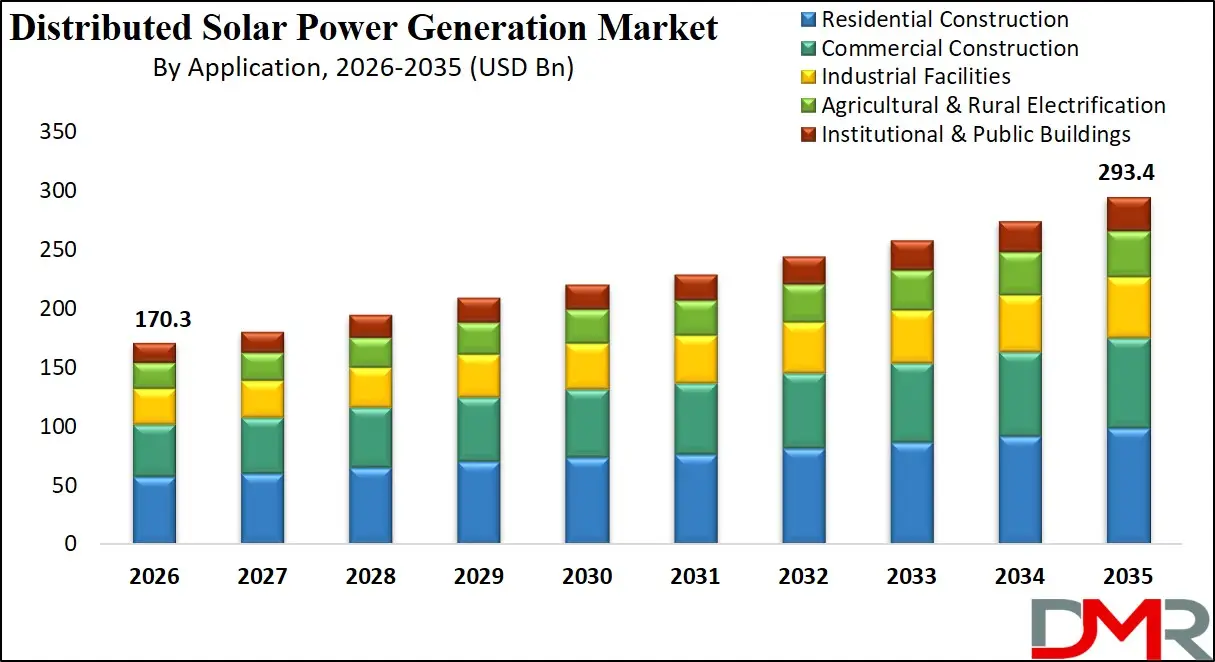

The Global Distributed Solar Power Generation Market is anticipated to reach USD 170.3 billion in 2026 and is projected to expand at a compound annual growth rate (CAGR) of 6.2% during the forecast period of 2026–2035, ultimately reaching an estimated market valuation of USD 293.4 billion by 2035, driven by accelerating rooftop solar adoption, decentralized energy transition initiatives, supportive net-metering policies, declining photovoltaic module costs, integration of battery energy storage systems (BESS), smart inverter deployment, grid modernization investments, carbon reduction commitments, and increasing demand for resilient, distributed power infrastructure across residential, commercial, industrial, and rural electrification applications worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Distributed solar power generation enables electricity production at or near the point of consumption through rooftop arrays, community solar gardens, and small-scale ground-mounted systems. The model addresses critical energy challenges related to grid congestion, transmission losses, energy access in remote areas, and carbon emissions reduction, supporting homeowners, businesses, and utilities in achieving greater energy resilience and cost predictability.

Technological advancements, including bifacial solar modules, smart inverters with grid-support functions, AI-driven energy management systems, blockchain-based peer-to-peer energy trading, and integrated battery storage solutions, are transforming the market into a dynamic and highly intelligent energy ecosystem. Integration of Internet of Things (IoT) sensors for real-time performance monitoring, predictive maintenance algorithms, and automated demand response capabilities is reshaping how distributed solar assets are managed and optimized.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government initiatives promoting renewable energy adoption, net metering frameworks, green building certifications, and climate resilience further accelerate global deployment. However, barriers such as intermittency challenges, grid integration complexities, variable regulatory policies across jurisdictions, and upfront capital requirements remain. Despite these limitations, the convergence of solar technology, digitalization, and decentralized energy models positions distributed solar generation as a central pillar of the global energy transition through 2035.

The US Distributed Solar Power Generation Market

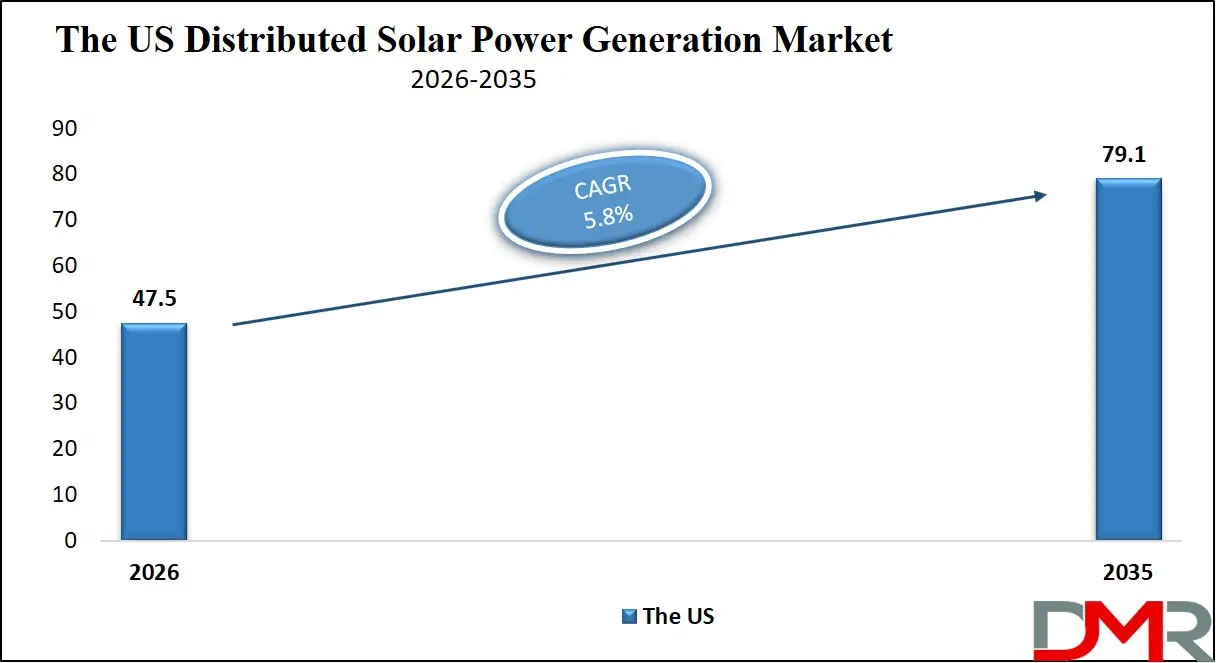

The U.S. Distributed Solar Power Generation Market is projected to reach USD 47.5 billion in 2026 and grow at a CAGR of 5.8%, reaching USD 79.1 billion by 2035. The U.S. maintains its leadership position due to federal tax incentives, state-level renewable portfolio standards, falling system costs, and growing corporate renewable procurement commitments.

The extension of the Investment Tax Credit (ITC) through the Inflation Reduction Act, combined with rising retail electricity rates, creates compelling economic returns for residential and commercial solar adopters. Major solar installers such as Sunrun, Sunnova, SunPower, and Tesla continue to expand their distributed generation portfolios, increasingly bundling solar with battery storage to offer whole-home backup and grid services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. regulatory support at the state levels for value-of-solar tariffs, community solar enabling legislation, and streamlined interconnection processes accelerates adoption across customer segments. The emergence of solar-plus-storage virtual power plants (VPPs), where aggregated distributed resources participate in wholesale markets, represents a significant value enhancement opportunity.

The rapid adoption of high-efficiency modules, module-level power electronics, and AI-powered energy management platforms continues to redefine the U.S. distributed solar landscape, positioning the country as a global leader in decentralized renewable energy deployment.

The Europe Distributed Solar Power Generation Market

The Europe Distributed Solar Power Generation Market is projected to be valued at approximately USD 51.0 billion in 2026 and is projected to reach around USD 88.0 billion by 2035, growing at a CAGR of about 6.2% from 2026 to 2035. Europe's strong market position is anchored by ambitious EU climate targets, the REPowerEU plan to reduce fossil fuel dependence, and mature feed-in tariff and net metering frameworks.

Countries such as Germany, Italy, the Netherlands, Spain, and Poland lead in distributed solar adoption, driven by high retail electricity prices, strong public awareness, and supportive policies including tax reductions and grant programs for residential PV. The EU's Solar Rooftop Initiative, mandating solar installations on new public and commercial buildings, provides sustained market momentum.

Europe's energy security concerns following geopolitical tensions, combined with consumer desire for energy independence, have dramatically accelerated residential and commercial solar installations. Community energy projects and energy cooperatives play a significant role, particularly in Germany and Scandinavia, democratizing energy generation and keeping economic benefits local.

Innovations in building-integrated photovoltaics (BIPV), smart home energy management integration, and vehicle-to-grid (V2G) ready systems are gaining traction. With strong technical standards, circular economy principles in module recycling, and emphasis on energy sovereignty, Europe remains one of the most sophisticated distributed solar markets globally.

The Japan Distributed Solar Power Generation Market

The Japan Distributed Solar Power Generation Market is anticipated to be valued at approximately USD 17.0 billion in 2026 and is expected to attain nearly USD 29.3 billion by 2035, expanding at a CAGR of about 6.2% during the forecast period. Japan's limited land availability for utility-scale projects and post-Fukushima focus on energy diversification drive strong demand for distributed solar solutions, particularly rooftop and parking lot canopy installations.

The Ministry of Economy, Trade and Industry (METI) continues to support distributed generation through feed-in premiums, low-interest financing for residential systems, and streamlined permitting processes. Japan's leadership in power electronics, high-efficiency module manufacturing, and disaster-resilient energy systems accelerates innovation in compact, high-performance distributed solar solutions suited for dense urban environments.

Japan's concept of "Zero Energy Houses" (ZEH) and "Zero Energy Buildings" (ZEB), promoted through government targets and subsidies, integrates solar PV with advanced insulation, efficient appliances, and storage. Major conglomerates like Panasonic, Sharp, and Kyocera offer integrated residential energy systems combining solar, storage, and energy management. The cultural emphasis on preparedness for natural disasters further boosts the adoption of solar-plus-storage for backup power, positioning Japan as a high-value innovator in resilient distributed generation.

Global Distributed Solar Power Generation Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Distributed Solar Power Generation Market is expected to be valued at USD 170.3 billion in 2026 and is projected to reach USD 293.4 billion by 2035, showcasing robust expansion supported by declining costs, policy support, and rising energy autonomy demand.

- Healthy CAGR Driven by Decarbonization Goals: The market is expected to grow at an impressive CAGR of 6.2% from 2026 to 2035, fueled by accelerating renewable energy targets, corporate sustainability commitments, electrification trends, and improving storage economics.

- Strong Growth Trajectory in the United States: The U.S. Distributed Solar Power Generation Market stands at USD 47.5 billion in 2026 and is projected to reach USD 79.1 billion by 2035, expanding at a CAGR of 5.8% due to favorable tax credits, rising electricity rates, and growing consumer demand for energy resilience.

- North America Maintains Regional Dominance: North America is expected to capture approximately 33.2% of the global market share in 2026, supported by mature installer networks, innovative financing models, and early adoption of integrated solar-plus-storage solutions.

- Rapid Advancement in Solar Technologies: Innovations including bifacial modules for residential applications, advanced microinverters and power optimizers, AI-based energy forecasting, and AC-coupled storage systems are significantly improving energy yield, reliability, and system intelligence.

- Growing Energy Independence Focus Boosts Adoption: Rising global concerns over grid reliability, electricity price volatility, and energy security, coupled with the falling cost of backup-capable systems, is driving sustained demand for distributed solar generation.

Global Distributed Solar Power Generation Market: Use Cases

- Residential Rooftop Solar: Homeowners install PV systems to reduce monthly electricity bills, hedge against rising rates, and increase property value, often paired with battery storage for backup during grid outages.

- Commercial & Industrial Rooftop Arrays: Businesses deploy solar on warehouse roofs, factory buildings, and office complexes to lower operating expenses, meet sustainability targets, and demonstrate environmental leadership.

- Community Solar Gardens: Multiple subscribers share the output of a centrally located solar array, enabling renters, low-income households, and those with unsuitable roofs to access solar benefits.

- Agricultural & Rural Electrification: Farms utilize solar for irrigation, livestock operations, and remote equipment, while off-grid rural communities gain access to reliable electricity through mini-grids and solar home systems.

- Solar Canopies & Carports: Parking lots are transformed into energy-generating assets, providing shade and EV charging while utilizing otherwise unused space for commercial, institutional, and municipal applications.

Global Distributed Solar Power Generation Market: Stats & Facts

International Energy Agency (IEA)

- Solar PV generated over 1,600 TWh of electricity globally in 2023.

- Solar PV accounted for 5.4% of total global electricity generation in 2023.

- Solar PV was the fastest-growing source of electricity generation in 2023, with output increasing by around 25% year-over-year.

- Solar PV additions reached approximately 420 GW globally in 2023.

- Utility-scale solar represented the majority of new capacity additions globally in 2023.

- Solar PV is expected to become the largest source of renewable capacity globally by installed capacity before 2030 under current policies.

IEA Photovoltaic Power Systems Programme (IEA-PVPS)

- Global cumulative installed PV capacity surpassed 2.2 terawatts (TW) by the end of 2024.

- More than 34 countries installed over 1 GW of solar capacity in 2024.

- At least 23 countries have cumulative installed PV capacity exceeding 10 GW.

- Distributed solar represents a significant share of total PV installations in Europe and parts of Asia-Pacific.

- Residential and commercial PV segments continue to expand in both mature and emerging markets.

International Renewable Energy Agency (IRENA)

- Global renewable power capacity reached approximately 4,443 GW in 2024.

- Solar PV accounted for about 452 GW of renewable capacity additions in 2024, representing the largest share.

- Solar PV represented over 70% of total renewable capacity additions in 2023.

- Renewable energy accounted for more than 90% of new global power capacity additions in 2024.

- Asia contributed the largest share of new solar capacity additions in 2023 and 2024.

U.S. Energy Information Administration (EIA)

- The United States added approximately 31 GW of new solar capacity in 2023.

- Distributed solar installations in the U.S. accounted for roughly 8 GW in 2023.

- Solar generation in the U.S. increased by more than 20% year-over-year in 2023.

- Solar energy represented about 5% of total U.S. electricity generation in 2023.

U.S. Department of Energy (DOE)

- The cost of solar PV modules has declined by more than 80% since 2010.

- The U.S. solar workforce exceeded 260,000 jobs in recent years.

- Distributed energy resources, including rooftop solar, are a key component of U.S. grid modernization initiatives.

European Commission

- The European Union installed over 60 GW of new solar capacity in 2023.

- Solar energy became the fastest-growing electricity source in the EU in 2023.

- Rooftop solar is a major contributor to distributed generation across EU member states.

Government of India – Ministry of New and Renewable Energy (MNRE)

- India's cumulative installed solar capacity exceeded 70 GW by 2023.

- India's rooftop solar capacity surpassed 11 GW by 2023.

- The government targets significant expansion of distributed rooftop solar under national solar missions.

National Energy Administration (China)

- China added over 200 GW of solar capacity in 2023, the highest globally.

- Distributed solar installations in China accounted for a substantial portion of annual additions.

REN21 – Renewable Energy Policy Network

- Solar PV capacity grew by approximately 37% globally between 2023 and 2024.

- Distributed solar systems continue expanding in residential and commercial sectors worldwide.

Global Distributed Solar Power Generation Market: Market Dynamics

Driving Factors in the Global Distributed Solar Power Generation Market

Falling System Costs & Improving Economics

The sustained decline in solar module, inverter, and balance-of-system costs, combined with rising retail electricity rates, has made distributed solar economically compelling across an expanding range of markets. Payback periods in many regions now fall below 5-8 years, with system lifetimes exceeding 25-30 years, generating significant long-term savings. The addition of storage further enhances value by enabling the consumption of stored solar during peak-rate evening hours. This improved economic equation, supported by third-party ownership models like leases and power purchase agreements, reduces upfront barriers and accelerates adoption across residential and commercial segments.

Supportive Policy Frameworks & Decarbonization Targets

Governments worldwide are implementing ambitious renewable energy targets, building codes mandating solar readiness, and financial incentives including tax credits, rebates, feed-in tariffs, and net metering. The EU's Green Deal, the U.S. Inflation Reduction Act, and China's 14th Five-Year Plan for renewable energy create long-term visibility for distributed solar investment. Corporate sustainability commitments, with over 300 major companies committed to 100% renewable energy through RE100, further drive commercial and industrial adoption. This policy tailwind creates a stable, growth-oriented environment for market expansion.

Restraints in the Global Distributed Solar Power Generation Market

Grid Integration & Interconnection Challenges

The rapid growth of distributed solar creates technical challenges for distribution grids designed for one-way power flow. Voltage fluctuations, reverse power flows, and hosting capacity limitations can necessitate costly grid upgrades before additional solar can be interconnected. Lengthy and variable interconnection processes across different utility territories create uncertainty and delays for installers and customers. Without modernization of grid planning, operational practices, and tariff structures, these constraints may limit distributed solar penetration in certain regions.

Regulatory Uncertainty & Policy Retroactivity

Distributed solar markets remain sensitive to changes in supporting policies. Reductions in feed-in tariffs, modifications to net metering compensation, and expiration of tax credits can dramatically impact customer economics and installer business models. Several markets have experienced boom-bust cycles driven by policy changes, creating industry instability. The complexity of navigating varying regulations across states, provinces, and countries imposes compliance costs on installers operating in multiple jurisdictions.

Opportunities in the Global Distributed Solar Power Generation Market

Solar-Plus-Storage & Smart Energy Management

The pairing of distributed solar with battery storage creates transformative opportunities for enhanced customer value and grid services. Storage enables self-consumption optimization, backup power during outages, participation in demand response programs, and aggregation into virtual power plants. As battery costs continue to decline and software platforms mature, integrated solar-storage systems become the new standard, expanding the total addressable market and revenue per customer. Smart energy management systems that optimize solar, storage, EV charging, and smart appliances create comprehensive home energy solutions.

Emerging Market Leapfrogging & Energy Access

Distributed solar offers a pathway to leapfrog traditional grid extension in underserved regions of Africa, Asia, and Latin America. Pay-as-you-go (PAYG) solar home systems, enabled by mobile money and IoT connectivity, have already brought basic electricity access to millions. As incomes rise and systems scale, these customers represent a growing market for larger distributed solar solutions. Mini-grids powered by solar-storage combinations provide village-level electrification, supporting productive uses like irrigation, milling, and commerce that drive economic development.

Trends in the Global Distributed Solar Power Generation Market

Digitalization & AI-Powered Energy Platforms

Advanced software platforms are transforming distributed solar from passive generation assets into intelligent, grid-interactive resources. AI-powered energy forecasting optimizes storage dispatch based on weather, usage patterns, and utility rate structures. Blockchain-enabled peer-to-peer trading platforms allow prosumers to sell excess generation to neighbors. Digital twins and IoT monitoring enable predictive maintenance and remote troubleshooting. This digitalization trend enhances system value, customer engagement, and grid integration capabilities.

Building-Integrated & Aesthetic Solar Solutions

The integration of solar into building materials roofing tiles, facades, windows, and canopies addresses aesthetic concerns that previously limited adoption, particularly in premium residential and historic districts. Products like Tesla's Solar Roof and various BIPV solutions from European manufacturers offer curb appeal while generating power. This trend expands market potential among homeowners unwilling to mount traditional racked systems, opening new segments and increasing overall penetration.

Global Distributed Solar Power Generation Market: Research Scope and Analysis

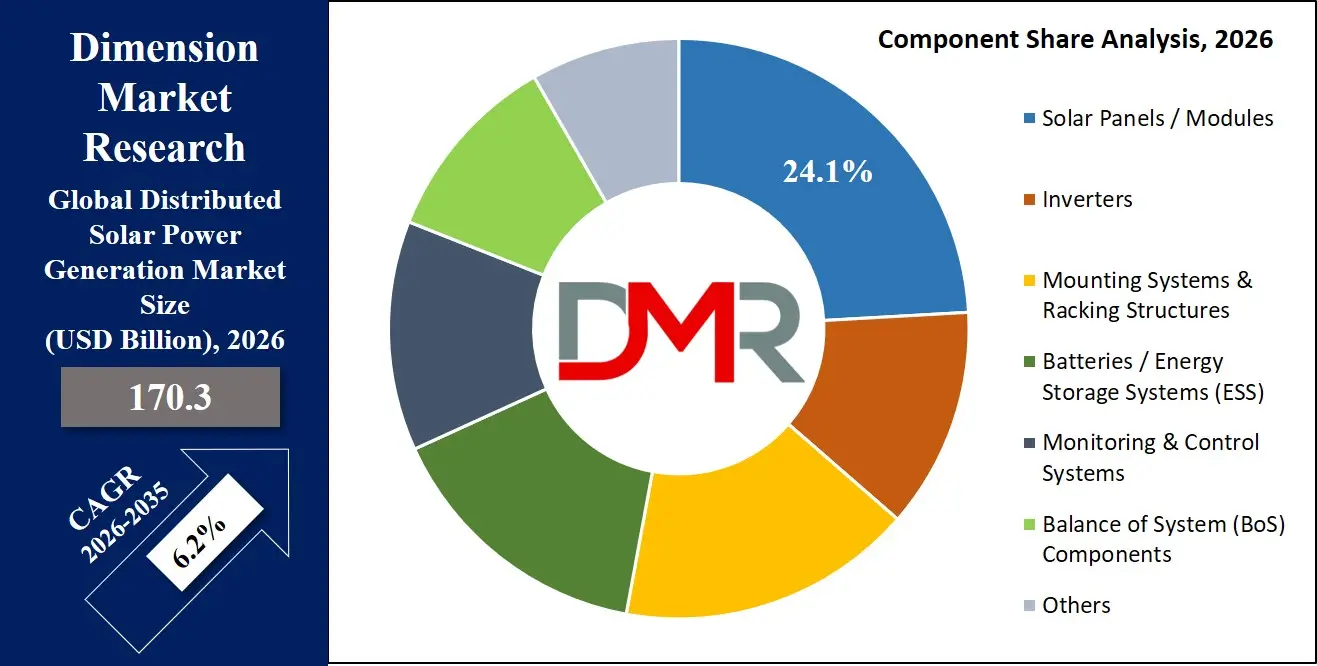

By Component Analysis

Solar Panels/Modules are projected to represent the largest component segment, capturing the highest share of system value and serving as the essential energy-generating element of any distributed solar installation. Continued improvements in module efficiency with mainstream products now exceeding 20-22% enable greater energy production from limited roof areas, directly impacting project economics and addressable market. Tier-1 module manufacturers offer products with 25+ year performance warranties, underpinning long-term customer confidence.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Inverters, as the second-largest component, are rapidly evolving from simple DC-AC converters to intelligent energy management hubs with grid-support functions, integrated storage capabilities, and advanced monitoring. The rise of module-level power electronics (microinverters and optimizers) addresses shading challenges and enhances safety and system monitoring. Batteries/Energy Storage represent the fastest-growing component segment, transforming distributed solar from intermittent generation to a dispatchable, resilient power source. Mounting systems, while lower in value, are critical for long-term system integrity, with innovations in aesthetics and ease of installation. Monitoring systems increasingly leverage AI and cloud platforms to provide actionable insights and predictive analytics, completing the intelligent distributed generation ecosystem.

By Technology Analysis

Solar Photovoltaic (PV) Systems are projected to dominate the Technology segment of the Global Distributed Solar Power Generation Market. This dominance is driven by PV technology's maturity, declining cost trajectory, scalability across applications from watts to megawatts, and ease of integration with buildings and existing electrical systems. Crystalline silicon modules, accounting for over 95% of the market, benefit from decades of manufacturing optimization and reliable performance data. The modular nature of PV allows systems of any size, from small residential rooftops to large commercial arrays, making it universally applicable. While Concentrated Solar Power (CSP) systems offer advantages in thermal storage integration, their complexity, scale requirements, and land needs make them poorly suited for true distributed applications at commercial or residential sites. CSP remains viable primarily for utility-scale projects in high-DNI regions. Therefore, PV technology's versatility, cost-effectiveness, and broad applicability secure its dominant market position throughout the forecast period.

By Grid Type

In the Global Distributed Solar Power Generation Market, on-grid systems clearly dominate the grid type segment due to their widespread adoption and economic advantages. On-grid (grid-connected) systems are directly linked to the public electricity grid, allowing users to draw power when solar generation is low and export excess electricity back to the grid. This bidirectional capability, often supported by net metering policies, significantly improves return on investment and makes on-grid systems the most preferred choice for residential, commercial, and industrial users.

The dominance of on-grid systems is further driven by supportive government policies, subsidies, and incentives across major solar markets. Urban areas, where reliable grid infrastructure is already in place, heavily favor on-grid installations due to lower upfront costs compared to systems requiring battery storage. Additionally, businesses and industries adopt on-grid solar to reduce electricity bills and meet sustainability targets without investing heavily in storage solutions.

Hybrid systems are gaining traction as they combine grid connectivity with battery storage, offering backup during outages and improved energy independence. However, higher initial costs limit their widespread adoption compared to on-grid systems.

Off-grid systems hold a smaller share and are primarily used in remote or rural areas with limited or no access to grid infrastructure. While essential in such regions, their niche application keeps them behind on-grid systems, reinforcing the latter’s clear market dominance.

By Application Analysis

Residential Construction is poised to be the largest and most dominant application segment for distributed solar generation, driven by powerful consumer trends toward energy independence, sustainability, and protection from rising utility rates. The residential segment benefits from supportive policies, including net metering, ITC eligibility, and financing innovations like solar loans and PPAs that make ownership accessible to mainstream homeowners. The integration of battery storage, EV charging, and smart home management creates compelling whole-home solutions that extend value beyond simple bill savings. Millennial homebuyers increasingly prioritize energy-efficient, solar-equipped homes, influencing new construction trends. The sheer number of dwellings globally, combined with declining system costs and rising electricity rates, creates a multi-decade growth runway for residential solar, securing its dominant market position.

Commercial Construction ranks as the second-largest application segment, encompassing office buildings, retail centers, schools, hospitals, and warehouses with large, suitable roof areas and daytime load profiles well-matched to solar generation. The commercial segment's decision-making, based on ROI and payback period, is increasingly favorable as system costs decline and alternative financing options expand. Corporate sustainability commitments drive many commercial installations, with solar serving as a visible demonstration of environmental leadership. Power purchase agreements (PPAs) allow commercial customers to adopt solar with zero upfront capital while immediately reducing electricity costs. As more jurisdictions implement building energy performance standards, commercial solar becomes not just economically attractive but strategically essential for compliance and asset valuation.

By End User Analysis

Residential Consumers/Homeowners are anticipated to dominate the market as the primary end-user segment, reflecting the fundamental premise of distributed generation power produced where it is consumed. The residential segment's diversity, spanning single-family homes, townhouses, and multi-tenant buildings, requires flexible solutions ranging from traditional rooftop arrays to community solar subscriptions. The emotional appeal of energy independence, combined with rational economic calculation of savings, drives homeowner adoption. The rise of integrated home energy solutions, combining solar, storage, EV charging, and smart controls, positions residential solar as the cornerstone of the future networked, electrified home. With millions of suitable, untapped rooftops globally and strong consumer interest, residential end users represent the largest and most sustainable demand base.

Commercial & Industrial (C&I) Entities represent the vital second-largest end-user segment, characterized by larger system sizes, more complex financing, and decision-making driven by CFOs and sustainability officers. C&I customers benefit from economies of scale that lower per-watt costs compared to residential systems, often achieving faster paybacks. Corporate power purchase agreements (PPAs) and green leases align landlord-tenant interests in solar adoption. As stakeholder pressure for ESG performance intensifies and carbon reporting becomes mandatory in more jurisdictions, C&I solar adoption moves from optional to expected. The diversity of C&I facilities from big-box retail to data centers to manufacturing plants requires sophisticated engineering and financing solutions, creating opportunities for specialized developers and financiers.

The Global Distributed Solar Power Generation Market Report is segmented on the basis of the following:

By Component

- Solar Panels / Modules

- Inverters

- String Inverters

- Micro Inverters

- Central Inverters

- Mounting Systems & Racking Structures

- Batteries / Energy Storage Systems (ESS)

- Monitoring & Control Systems

- Balance of System (BoS) Components

- Others

By Technology

- Solar Photovoltaic (PV) Systems

- Concentrated Solar Power (CSP) Systems

By Grid Type

- On-Grid Systems

- Off-Grid Systems

- Hybrid Systems

By Application

- Residential Construction

- Commercial Construction

- Industrial Facilities

- Agricultural & Rural Electrification

- Institutional & Public Buildings

By End User

- Residential Consumers/Homeowners

- Commercial & Industrial (C&I) Entities

- Utilities & Energy Service Providers

- Government & Public Sector

- Community Solar Subscribers

Impact of Artificial Intelligence in the Global Distributed Solar Power Generation Market

- AI for Solar Resource Assessment & Site Suitability: AI analyzes satellite imagery, LiDAR data, and shading patterns to accurately predict solar potential for specific rooftops and sites, streamlining sales processes and ensuring system performance meets expectations.

- AI-Driven Energy Forecasting & Storage Optimization: Machine learning models integrate weather forecasts, historical consumption patterns, and utility rate structures to optimize battery dispatch, maximizing self-consumption, bill savings, and grid service revenues.

- Predictive Maintenance & Fault Detection: AI-powered monitoring continuously analyzes system performance data to identify underperforming modules, inverter anomalies, or soiling issues before they cause significant energy losses, enabling proactive maintenance.

- Grid Services & Virtual Power Plant (VPP) Coordination: AI platforms aggregate thousands of distributed solar-plus-storage systems, forecasting available capacity and dispatching resources to participate in wholesale markets, frequency regulation, and distribution grid support.

- Automated Customer Acquisition & System Design: AI streamlines the customer journey from initial interest to installed system, automating shade analysis, preliminary design, permit package generation, and financial payback calculations, reducing soft costs and sales cycle time.

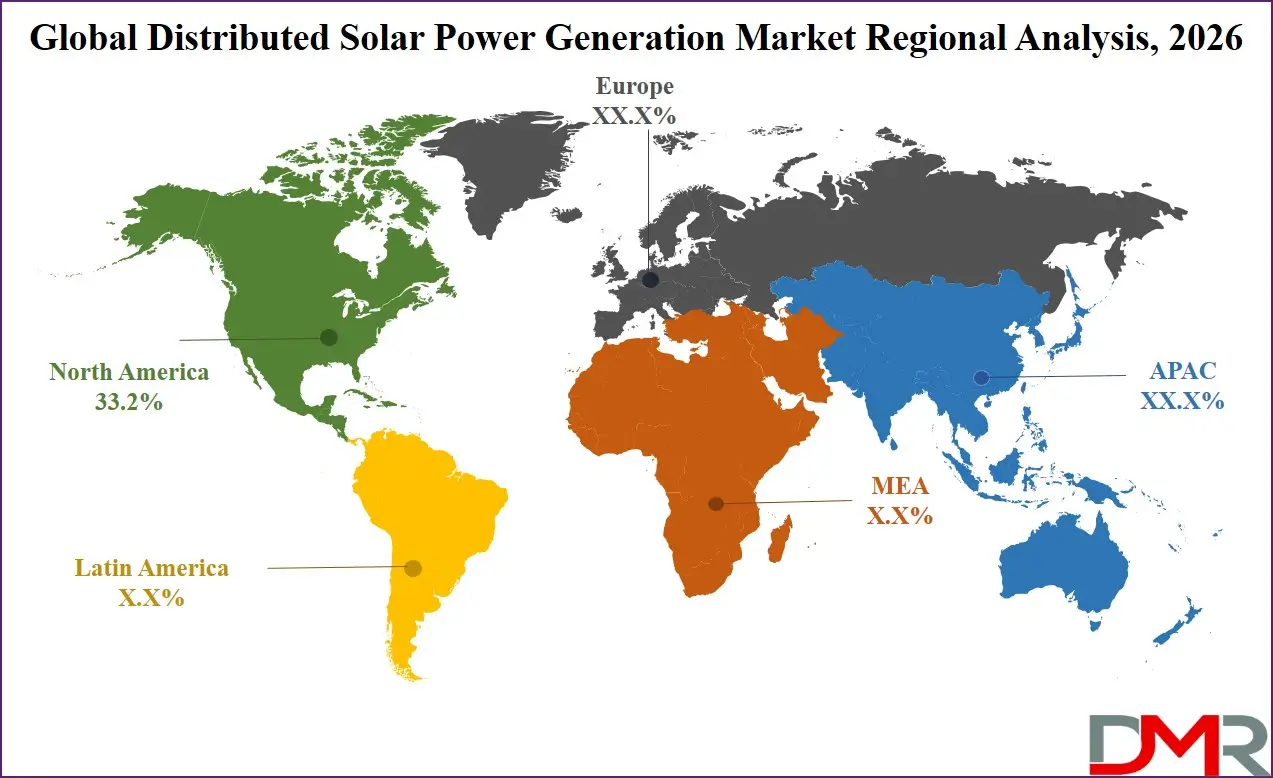

Global Distributed Solar Power Generation Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to dominate the Global Distributed Solar Power Generation Market with 33.2% of market share by the end of 2026, owing to a powerful combination of attractive federal incentives (ITC), high retail electricity rates in key states, mature installer ecosystems, and innovative financing models. The United States, in particular, benefits from strong state-level policies in California, New York, Massachusetts, and other leading solar states, alongside growing adoption in previously untapped Southeast and Midwest markets. Canada's distributed solar market, while smaller, is accelerating with favorable feed-in tariffs in some provinces and federal carbon pricing that improves solar economics. The region's culture of consumer technology adoption, robust venture capital investment in solar startups, and progressive utilities embracing distributed resources further solidify North America's leadership position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR and is poised to achieve rapid market share growth due to its massive population, rapid urbanization, rising electricity demand, and severe air quality concerns, driving policy support for clean energy. China leads the region in distributed solar volumes, with ambitious targets for rooftop PV under its "Whole Country" distributed solar program. India's "PM Surya Ghar" scheme aims to solarize 10 million households with significant subsidies. Southeast Asian nations like Vietnam, Thailand, and the Philippines are experiencing distributed solar booms driven by high commercial/industrial tariffs and falling system costs. Australia maintains one of the world's highest residential solar penetrations, with storage attachment rates accelerating. This combination of sheer scale, supportive policies, and improving economic positions positions APAC as the fastest-growing distributed solar market globally.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Distributed Solar Power Generation Market: Competitive Landscape

The Global Distributed Solar Power Generation Market is highly competitive and fragmented, featuring a mix of global solar manufacturers, specialized downstream installers, financing platforms, and technology providers. Leading module manufacturers Longi, JinkoSolar, Trina Solar, and Canadian Solar supply the majority of panels globally, competing on efficiency, reliability, and cost. Downstream specialists such as Sunrun, Sunnova, SunPower, and Tesla dominate the U.S. residential market with vertically integrated offerings including financing, installation, and storage.

European installers like E.ON, Engie, and BayWa r.e. serve commercial and residential customers across multiple countries. Emerging players in financing and software, including Sunstone Credit, Palmetto, and Aurora Solar, are transforming customer acquisition, system design, and access to capital. Utilities increasingly enter the space through community solar offerings and partnerships with installers.

Some of the prominent players in the Global Distributed Solar Power Generation Market are:

- Longi Green Energy Technology Co., Ltd.

- JinkoSolar Holding Co., Ltd.

- Trina Solar Co., Ltd.

- Canadian Solar Inc.

- Sunrun Inc.

- Sunnova Energy International Inc.

- SunPower Corporation

- Tesla, Inc.

- Enphase Energy, Inc.

- SolarEdge Technologies, Inc.

- Sungrow Power Supply Co., Ltd.

- Huawei Technologies Co., Ltd. (Digital Power)

- ABB Ltd.

- Schneider Electric SE

- Siemens AG

- Engie SA

- E.ON SE

- BayWa r.e. AG

- Adani Green Energy Limited

- Tata Power Solar Systems Limited

- Other Key Players

Recent Developments in the Global Distributed Solar Power Generation Market

- January 2026: Sunrun launches next-gen home energy system with integrated EV bidirectional charging. Sunrun introduced its comprehensive home energy platform combining high-efficiency solar, LFP battery storage, and bidirectional EV charger capability, enabling customers to power their homes from their electric vehicle during outages.

- October 2025: Longi announces 27%+ efficiency perovskite-silicon tandem module for residential applications. Longi unveiled its breakthrough tandem solar module, achieving record efficiency for commercially viable products, enabling homeowners to generate significantly more power from limited roof space.

- September 2025: Enphase and Sunnova partner on a nationwide virtual power plant in Texas. The partnership will aggregate thousands of solar-plus-storage systems across Texas, dispatching stored energy to support grid reliability during peak demand periods, with participating customers receiving compensation.

- August 2025: EU launches "Solar Rooftops for All" initiative with EUR 5 billion funding. The European Commission announced major funding to accelerate residential and community solar adoption, with particular focus on energy-poor households and multi-family buildings, targeting 10 million new installations by 2030.

- July 2025: Tesla expands solar roof production at Buffalo Gigafactory. Tesla ramped up production of its solar roof tiles, announcing improved installation processes and lower costs, targeting broader adoption among homeowners seeking aesthetically integrated solar solutions.

- June 2025: India launches PM Surya Ghar scheme targeting 10 million solar roofs. The Indian government announced a comprehensive subsidy program for residential rooftop solar, providing up to 40% cost coverage for eligible households and aiming to transform the country's distributed solar trajectory.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 170.3 Bn |

| Forecast Value (2035) |

USD 293.4 Bn |

| CAGR (2026–2035) |

6.2% |

| The US Market Size (2026) |

USD 47.5 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Component (Solar Panels/Modules, Inverters, Mounting Systems & Racking Structures, Batteries/Energy Storage Systems (ESS), Monitoring & Control Systems, Balance of System (BoS) Components, Others), By Technology (Solar Photovoltaic (PV) Systems, Concentrated Solar Power (CSP) Systems), By Grid Type (On-Grid Systems, Off-Grid Systems, Hybrid Systems), By Application (Residential Construction, Commercial Construction, Industrial Facilities, Agricultural & Rural Electrification, Institutional & Public Buildings), By End User (Residential Consumers/Homeowners, Commercial & Industrial (C&I) Entities, Utilities & Energy Service Providers, Government & Public Sector, Community Solar Subscribers). |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Longi Green Energy Technology Co., Ltd., JinkoSolar Holding Co., Ltd., Trina Solar Co., Ltd., Canadian Solar Inc., Sunrun Inc., Sunnova Energy International Inc., SunPower Corporation, Tesla, Inc., Enphase Energy, Inc., SolarEdge Technologies, Inc., Sungrow Power Supply Co., Ltd., Huawei Technologies Co., Ltd. (Digital Power), ABB Ltd., Schneider Electric SE, Siemens AG, Engie SA, E.ON SE, BayWa r.e. AG, Adani Green Energy Limited, and Tata Power Solar Systems Limited, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Distributed Solar Power Generation Market?

▾ The Global Distributed Solar Power Generation Market size is estimated to have a value of USD 170.3 billion in 2026 and is expected to reach USD 293.4 billion by the end of 2035.

What is the growth rate in the Global Distributed Solar Power Generation Market?

▾ The market is growing at a CAGR of 6.2 percent over the forecasted period of 2026-2035.

What is the size of the US Distributed Solar Power Generation Market?

▾ The US Distributed Solar Power Generation Market is projected to be valued at USD 47.5 billion in 2026. It is expected to reach USD 79.1 billion in 2035 at a CAGR of 5.8%.

Which region accounted for the largest Global Distributed Solar Power Generation Market?

▾ North America is expected to have the largest market share in the Global Distributed Solar Power Generation Market with a share of about 33.2% in 2026.

Who are the key players in the Global Distributed Solar Power Generation Market?

▾ Some of the major key players in the Global Distributed Solar Power Generation Market are Longi, JinkoSolar, Trina Solar, Canadian Solar, Sunrun, Sunnova, SunPower, Tesla, Enphase Energy, SolarEdge Technologies, and many others.