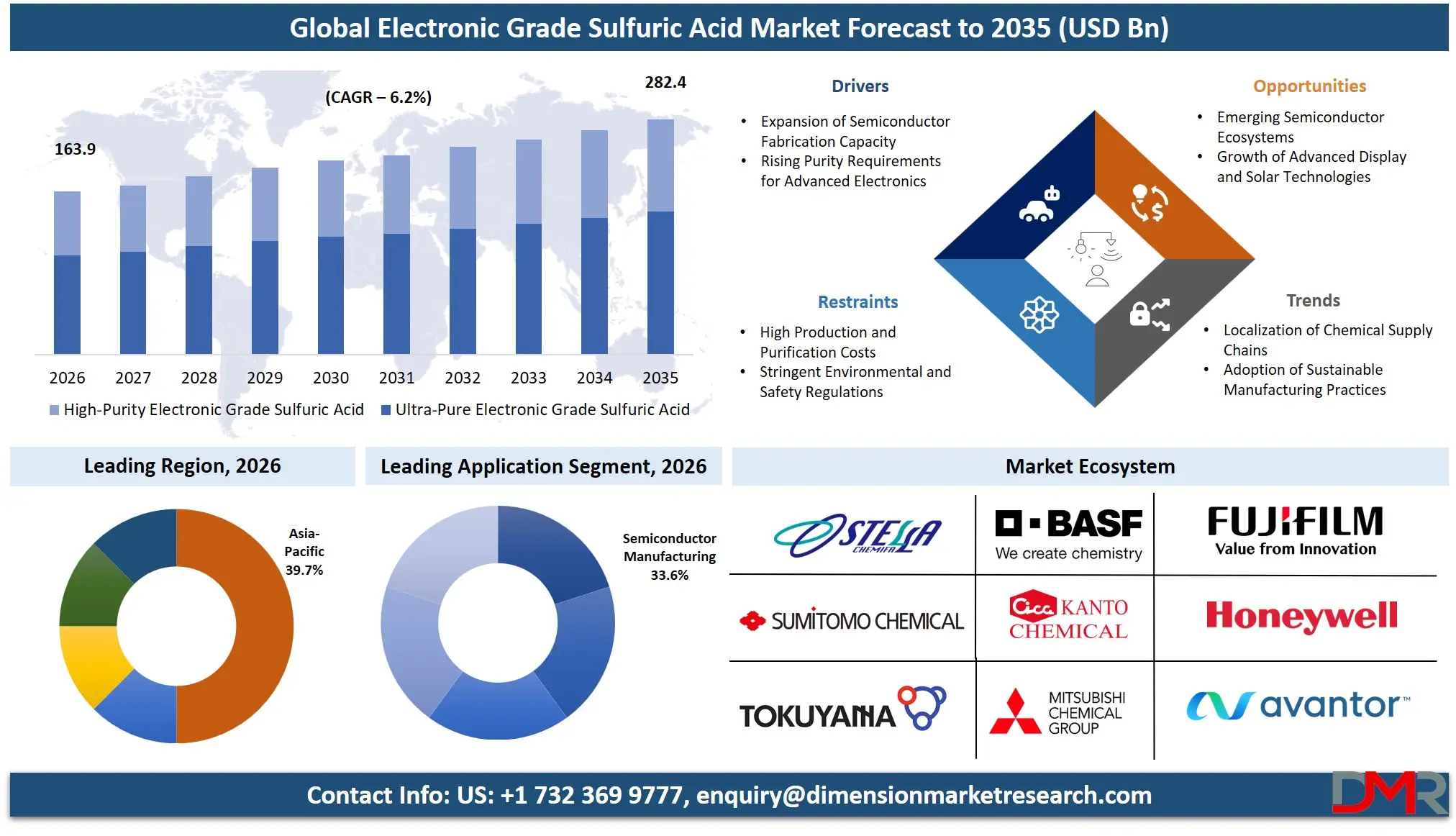

What is the Global Electronic Grade Sulfuric Acid Market Size?

The Global Electronic Grade Sulfuric Acid Market is expected to reach a value of USD 163.9 billion in 2026, and it is further anticipated to reach USD 282.4 billion by 2035, growing at a CAGR of 6.2% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The electronic grade sulfuric acid market has been experiencing robust growth, driven by the exponential demand for advanced semiconductors and the global expansion of electronics manufacturing. This market encompasses ultra-high-purity chemicals essential for etching, cleaning, and surface preparation in wafer fabrication. The increasing complexity of integrated circuits (ICs), the transition to 3D NAND architectures, and the proliferation of photovoltaic manufacturing are driving the necessity for specialized, contamination-free chemical inputs. Semiconductor foundries and integrated device manufacturers (IDMs) are the most significant consumers, with ultra-pure grades remaining the most critical due to their role in achieving high manufacturing yields. The Asia-Pacific region, led by Taiwan, South Korea, and China, are key ecosystems as they require a secure, high-volume supply chain for advanced node production and display fabrication.

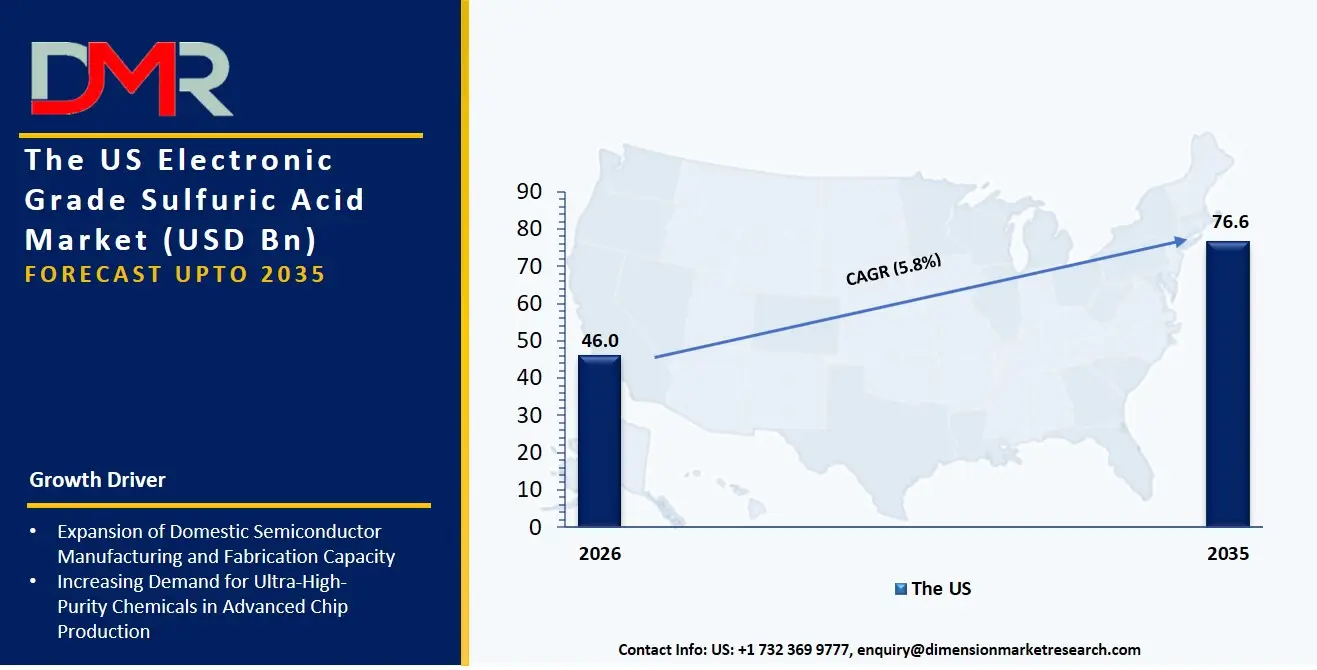

The US Electronic Grade Sulfuric Acid Market

The US Electronic Grade Sulfuric Acid Market is projected to reach USD 53.1 billion in 2026, growing at a compound annual growth rate of 5.8% over its forecast period, culminating in a value of USD 88.3 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US remains a strategically vital market for electronic grade sulfuric acid, underpinned by the CHIPS Act-driven resurgence of domestic semiconductor manufacturing and the construction of leading-edge foundries. The market has been typified by high demand for ultra-pure grades, as organizations focus on sub-5nm node fabrication that requires parts-per-trillion (ppt) level purity to prevent wafer defects. Besides, the reshoring of advanced packaging and IC substrate production is producing a parallel need in direct sales channels to manage the highly sensitive logistics of high-purity chemical distribution to secure fab sites.

The Europe Electronic Grade Sulfuric Acid Market

The Europe Electronic Grade Sulfuric Acid Market is estimated to be valued at USD 28.4 billion in 2026 and is further anticipated to reach USD 46.5 billion by 2035, growing at a CAGR of 5.6%. The European market is uniquely shaped by its leadership in automotive-grade semiconductors, power electronics, and micro-electromechanical systems (MEMS). This specialization drives a critical need for High-Purity Electronic Grade Sulfuric Acid tailored for silicon carbide (SiC) and gallium nitride (GaN) wafer processing, which are essential for electric vehicle (EV) inverters and industrial motor drives. In addition, the region's focus on sustainable manufacturing is pushing the adoption of advanced chemical recycling and reclamation systems within fabs. This trend is compelling specialty chemical suppliers in the distribution channel to provide not just virgin acids, but also closed-loop purification services that reduce chemical waste without compromising the ultra-pure quality required for flat panel display and sensor fabrication.

The Japan Electronic Grade Sulfuric Acid Market

The Japan Electronic Grade Sulfuric Acid Market is projected to hold a value of USD 3.8 billion in 2026 at a CAGR of 5.6%. Japan's market is distinguished by its deep-rooted materials science expertise and the presence of leading-edge chemical conglomerates that supply the global electronics value chain. Domestic demand is heavily concentrated in the manufacturing of advanced photoresists, specialty films, and cleaning solutions for Integrated Circuits (ICs), where local fabs are engaged in a strategic push towards 2nm and beyond process nodes. There is also a pronounced focus on the Direct Sales channel model, where chemical manufacturers engage in deep co-engineering partnerships with Semiconductor Foundries. This collaboration is critical for developing customized acid formulations that minimize surface roughness and particle defects on next-generation silicon wafers, securing Japan's position as a critical hub for electronic material innovation.

Key Takeaways

- Market Size & Forecast: The Global Electronic Grade Sulfuric Acid market is projected to reach USD 163.9 billion in 2026, expanding steadily to USD 282.4 billion by 2035, fueled by the dual drivers of advanced node semiconductor proliferation and the global build-out of photovoltaic manufacturing capacity.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 6.2%, driven by the critical shortage of ultra-pure chemical production capacity and the escalating complexity of cleaning steps in 3D device architectures and multi-patterning lithography.

- Primary Growth Drivers: Key forces include the massive capital expenditure on new semiconductor foundries globally, the need for ultra-pure sulfuric acid to avoid yield-killing metallic contamination in ICs, and the rising production of solar cells requiring high-purity acids for texturing and cleaning steps.

- Key Market Trends: Major trends include the rise of node-specific chemical formulations for gate-all-around (GAA) transistors, the use of digital twins within direct sales models to predict chemical replenishment cycles, and the shift toward regionalized ultra-pure acid production to secure supply chains against geopolitical disruption.

- By Grade Analysis: Ultra-Pure Electronic Grade Sulfuric Acid is expected to dominate as leading-edge logic and memory fabrication demands contamination levels below 100 ppt. Professional chemical services are increasingly required to build seamless, high-purity distribution loops that connect on-site purification systems directly to the point-of-use in the fab.

- By Application Analysis: Semiconductor Manufacturing, specifically Integrated Circuits (ICs), is the most dominant and lucrative application due to the sheer number of cleaning and etching steps. Photovoltaic (Solar Cell) Manufacturing is the fastest-growing sector, as the global energy transition drives massive demand for high-purity acids in PERC and heterojunction cell production.

- Regional Leadership: Asia-Pacific is poised to dominate this market with a 39.1% of the market share in 2026, due to its unparalleled concentration of semiconductor foundries and display manufacturers in Taiwan, South Korea, and China.

What is the Electronic Grade Sulfuric Acid?

Electronic Grade Sulfuric Acid is a highly specialized, ultra-high-purity chemical used as a critical process material in the manufacturing of semiconductor wafers, ICs, and other electronic components. These services, unlike industrial-grade acid production, are related to achieving and maintaining parts-per-trillion levels of metallic contamination. This involves expert consulting on purification technologies to establish a strategic quality roadmap, direct sales and supply chain management to deliver the chemical without degradation, and specialty distribution to ensure that acid can be safely integrated with the existing on-site chemical delivery systems. With 90% of advanced fabs running high-volume manufacturing, professional, high-purity chemical supply is needed to achieve defect-free wafer yields and process stability, making chemical investments translate into tangible manufacturing excellence, as opposed to mere commodity supply.

Use Cases

- Advanced Gate-All-Around Transistor Cleaning in Foundries: Leading-edge semiconductor foundries utilize Ultra-Pure Electronic Grade Sulfuric Acid for single-wafer cleaning tools to remove residues and particles from nanosheet structures without etching or damaging the delicate silicon-germanium layers, enabling high-performance mobile processors.

- PERC Solar Cell Texturing: Solar Cell Manufacturers use High-Purity Electronic Grade Sulfuric Acid in a direct sales model to perform saw damage removal and create uniform surface texturing on monocrystalline wafers, directly boosting light absorption and photoelectric conversion efficiency in large-scale manufacturing lines.

- MEMS Sensor Deep Trench Etching: MEMS and sensor manufacturers rely on specialty chemical suppliers for custom-blended, ultra-pure sulfuric acid solutions to achieve precise, high-aspect-ratio etching for inertial sensors and microphones, ensuring zero contamination that could cause stiction or device failure.

- High-Resolution Flat Panel Display Backplane Manufacturing: Display manufacturers integrate high-purity sulfuric acid into the etching of copper interconnects and oxide semiconductor layers for OLED and next-generation LCD backplanes, ensuring uniform electrical performance across Gen 8.5 and larger substrates.

How AI is Transforming the Electronic Grade Sulfuric Acid Market

AI is fundamentally reshaping the electronic grade sulfuric acid market by accelerating the development of purification processes and enhancing real-time quality assurance. In ultra-pure grade qualification, AI-based analytical tools can automatically analyze trace metal detection data from ICP-MS, identifying nascent contamination trends and predicting required maintenance for distillation units, thereby minimizing manual testing and supply risks. Meanwhile, AI-powered features in direct sales and distribution allow chemical suppliers to better manage customer fab consumption patterns by analyzing wafer start rates and bath life, predicting future usage, and suggesting optimized delivery schedules to prevent chemical aging and ensure just-in-time manufacturing support.

Quality control and supply chain resilience projects are also revolving around AI. In the area of consulting services, intelligent compliance-monitoring agents are used to continuously monitor the purity of chemical batches across multi-site supply chains, identifying statistical deviations, trace impurity spikes, and lot-to-lot variance to keep shipments in line with SEMI Grade 1 to 4 standards. Moreover, generative AI assistants are complementing new fab startup consulting by simulating chemical delivery system dynamics and modeling total cost of ownership for on-site vs. off-site purification, giving stakeholders a visualization of the supply chain and purity economics before committing capital.

Market Dynamics

Key Drivers in the Global Electronic Grade Sulfuric Acid Market

Expansion of Semiconductor Fabrication Capacity

The worldwide construction of new wafer fabrication facilities is significantly increasing demand for electronic grade sulfuric acid. Every stage of semiconductor manufacturing, from wafer cleaning to photoresist stripping, requires ultra-pure chemicals to ensure high yields and device reliability. Government incentives supporting domestic chip production and the rapid growth of applications such as artificial intelligence, electric vehicles, and high-performance computing are accelerating fab investments. As process nodes continue to shrink, the quantity and purity requirements of process chemicals rise further. This sustained expansion of semiconductor capacity therefore remains one of the most powerful drivers of the electronic grade sulfuric acid market worldwide.

Rising Purity Requirements for Advanced Electronics

Modern electronic devices incorporate increasingly sophisticated architectures that are highly sensitive to trace contaminants. Consequently, manufacturers demand sulfuric acid with exceptionally low impurity levels and rigorous quality assurance. Advanced packaging, high-density memory, and next-generation display technologies all rely on superior cleaning performance to maintain yields and reliability. Suppliers capable of consistently delivering ultra-pure products gain a competitive advantage, encouraging investments in purification and quality-control technologies. The trend toward miniaturization and greater device complexity thus directly supports higher consumption of premium electronic grade sulfuric acid, strengthening market growth across semiconductor, display, and related electronics manufacturing sectors.

Restraints in the Global Electronic Grade Sulfuric Acid Market

High Production and Purification Costs

Producing electronic grade sulfuric acid requires sophisticated purification systems, contamination controls, and continuous quality monitoring. These measures entail substantial capital and operating expenditures, increasing the final product cost. Smaller manufacturers may find it difficult to justify such investments, limiting new market entrants and constraining supply expansion. In addition, the need for specialized packaging, storage, and transportation further raises costs. Fluctuations in energy prices and feedstock availability can also pressure margins. These financial barriers may slow capacity additions and discourage adoption in cost-sensitive applications, acting as a notable restraint on the broader growth of the market.

Stringent Environmental and Safety Regulations

Sulfuric acid is highly corrosive, necessitating strict handling, transportation, and disposal practices. Compliance with environmental and occupational safety regulations requires continuous investment in equipment, training, and monitoring systems. Any accidental release can lead to operational disruptions, reputational damage, and significant penalties. Manufacturers must therefore allocate considerable resources to maintain compliance and ensure worker safety. Regulatory requirements may also delay facility expansions or increase the cost of establishing new production sites. Such challenges can limit operational flexibility and raise overall expenses, thereby moderating the pace of growth within the electronic grade sulfuric acid industry.

Growth Opportunities in the Global Electronic Grade Sulfuric Acid Market

Emerging Semiconductor Ecosystems

Several countries are actively developing domestic semiconductor industries through incentives, infrastructure investments, and strategic partnerships. New fabrication plants in emerging regions create fresh demand for ultra-pure process chemicals, including electronic grade sulfuric acid. Suppliers that establish local production, distribution, or technical support capabilities can secure long-term customer relationships and reduce logistical risks. As these ecosystems mature, opportunities will extend beyond chip fabrication to associated packaging, testing, and component manufacturing activities. The geographic diversification of semiconductor production therefore represents a substantial avenue for future market expansion and revenue generation for established and new suppliers alike.

Growth of Advanced Display and Solar Technologies

The increasing adoption of high-resolution displays and efficient photovoltaic cells is expanding the use of high-purity chemicals in manufacturing processes. OLED panels, microdisplays, and next-generation solar cells demand precise surface cleaning and contamination control, favoring electronic grade sulfuric acid. Continuous innovation in these sectors creates opportunities for suppliers to develop customized formulations and value-added services. As sustainability initiatives and consumer demand for advanced electronics intensify, production volumes are expected to rise steadily. This evolution positions display and solar manufacturing as attractive complementary growth engines alongside the semiconductor industry for market participants worldwide.

Trends in the Global Electronic Grade Sulfuric Acid Market

Localization of Chemical Supply Chains

Electronics manufacturers are increasingly seeking regional sources of critical process chemicals to enhance supply security and reduce dependence on distant suppliers. This trend is prompting producers of electronic grade sulfuric acid to establish manufacturing and storage facilities closer to major fabrication hubs. Localized supply chains improve responsiveness, reduce transportation risks, and support compliance with national industrial policies. Strategic collaborations between chemical suppliers and semiconductor companies are becoming more common, fostering innovation and operational resilience. The movement toward regional self-sufficiency is therefore reshaping competitive dynamics and investment priorities throughout the global market for electronic grade sulfuric acid.

Adoption of Sustainable Manufacturing Practices

Sustainability has become a central focus for both chemical producers and electronics manufacturers. Companies are investing in energy-efficient purification technologies, recycling systems, and waste-reduction initiatives to lower environmental impacts. Customers increasingly evaluate suppliers based not only on product quality but also on environmental performance and carbon footprint. The integration of circular-economy principles into chemical manufacturing is encouraging process optimization and resource recovery. As regulatory expectations and stakeholder awareness continue to rise, sustainable production practices are evolving from optional initiatives into core competitive differentiators within the electronic grade sulfuric acid market.

Research Scope and Analysis

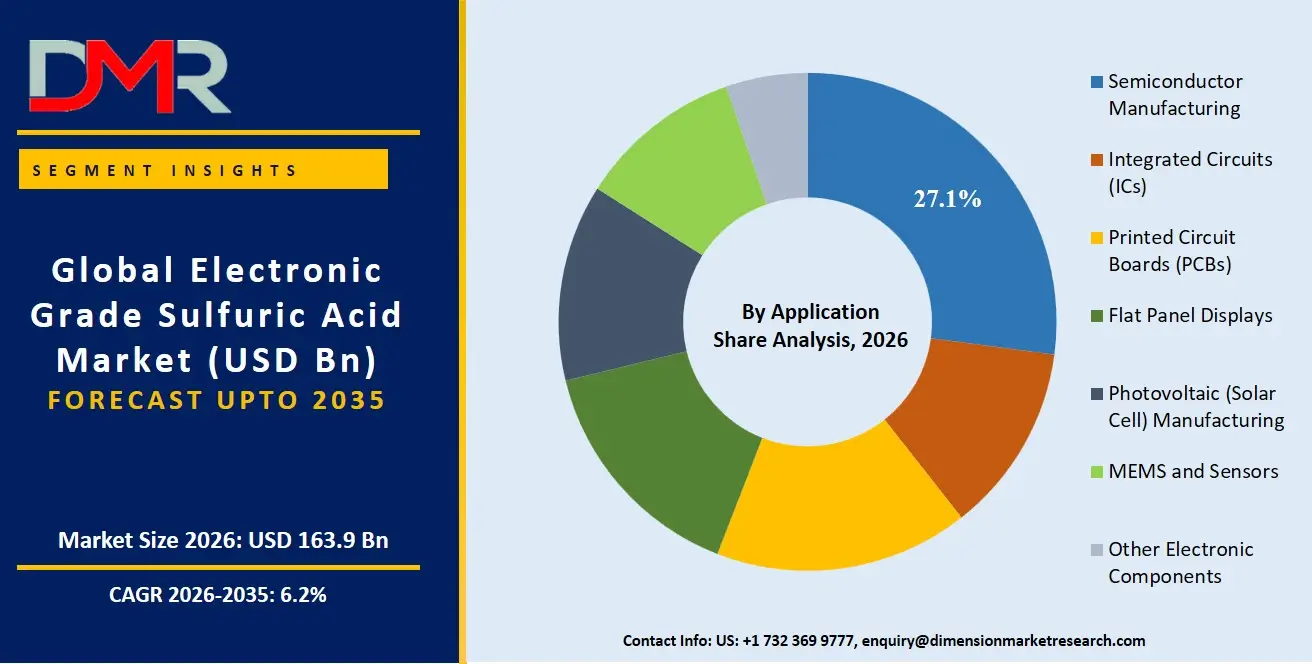

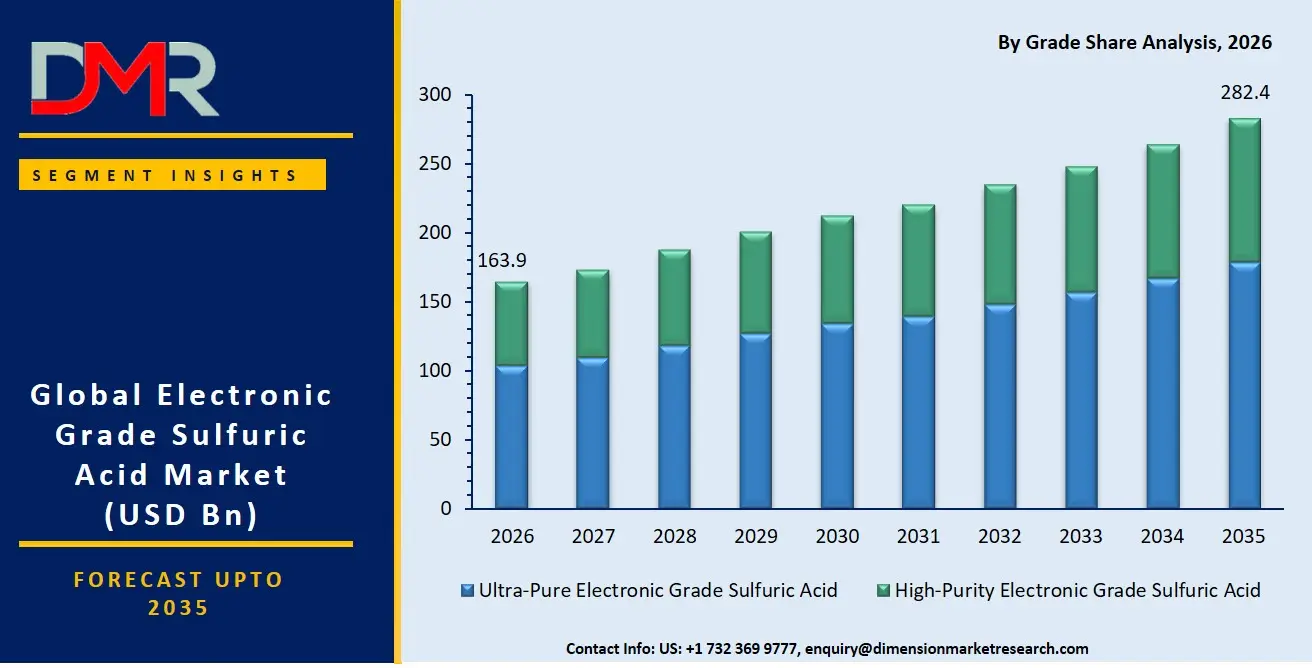

The global electronic grade sulfuric acid market is segmented by grade into ultra-pure electronic grade sulfuric acid and high-purity electronic grade sulfuric acid. Distribution channels include direct sales and specialty distributors. Applications encompass semiconductor manufacturing, integrated circuits, printed circuit boards, flat panel displays, photovoltaics, MEMS and sensors, and other electronic components. End users comprise semiconductor foundries, integrated device manufacturers, display manufacturers, solar cell manufacturers, and electronics component manufacturers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Grade Analysis

Ultra-pure electronic grade sulfuric acid is poised to dominate because advanced semiconductor fabrication requires impurity concentrations at extremely low levels to prevent defects and maintain high wafer yields. Leading-edge integrated circuits, memory devices, and logic chips employ highly sensitive cleaning and etching processes that can tolerate only trace contaminants.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

As chip geometries continue to shrink and manufacturers adopt more complex process nodes, demand for the highest purity grades rises correspondingly. The segment also benefits from stringent quality standards imposed by foundries and integrated device manufacturers, which prioritize consistent performance and process reliability. Consequently, ultra-pure grades command the largest share of consumption and value within the global market.

By Distribution Channel Analysis

Direct sales is poised to dominate as electronic grade sulfuric acid is a mission-critical input requiring assured purity, traceability, and dependable logistics. Major semiconductor and display manufacturers typically establish long-term supply agreements directly with producers to guarantee uninterrupted deliveries and tailored specifications. Direct relationships facilitate technical support, quality audits, and coordinated inventory management, all of which are essential for high-volume fabrication facilities. In addition, direct sourcing minimizes handling steps that could introduce contamination, preserving product integrity. The strategic nature of the material and the need for close collaboration between suppliers and end users therefore make direct sales the preferred and largest distribution channel globally.

By Application Analysis

Semiconductor manufacturing is projected to be the leading application because sulfuric acid is indispensable for wafer cleaning, photoresist stripping, and surface preparation throughout chip production. The rapid expansion of computing, artificial intelligence, consumer electronics, and automotive electronics has significantly increased wafer output worldwide. Modern fabrication plants consume large quantities of ultra-high-purity chemicals to achieve stringent yield and performance targets. Continuous investment in new fabs and process-node advancements further reinforces demand from this application. Since semiconductor production represents the most chemically intensive and highest-value use of electronic grade sulfuric acid, it consistently accounts for the largest share of global consumption.

By End User Analysis

Semiconductor foundries is expected to dominate the end-user landscape owing to their immense production volumes and central role in manufacturing chips for numerous fabless companies. These facilities operate around the clock and require substantial quantities of ultra-pure process chemicals to sustain high yields and meet exacting quality standards. The ongoing construction of new foundries and expansion of existing plants, particularly in Asia-Pacific, further strengthens their purchasing power. Foundries also tend to adopt the latest process technologies first, increasing the intensity of chemical usage per wafer. Their scale and technological sophistication firmly establish semiconductor foundries as the leading end-user segment in the market.

The Global Electronic Grade Sulfuric Acid Market Report is segmented on the basis of the following:

By Grade

- Ultra-Pure Electronic Grade Sulfuric Acid

- High-Purity Electronic Grade Sulfuric Acid

By Distribution Channel

- Direct Sales

- Distributors and Specialty Chemical Suppliers

By Application

- Semiconductor Manufacturing

- Integrated Circuits (ICs)

- Printed Circuit Boards (PCBs)

- Flat Panel Displays

- Photovoltaic (Solar Cell) Manufacturing

- MEMS and Sensors

- Other Electronic Components

By End User

- Semiconductor Foundries

- Integrated Device Manufacturers (IDMs)

- Display Manufacturers

- Solar Cell Manufacturers

- Electronics Component Manufacturers

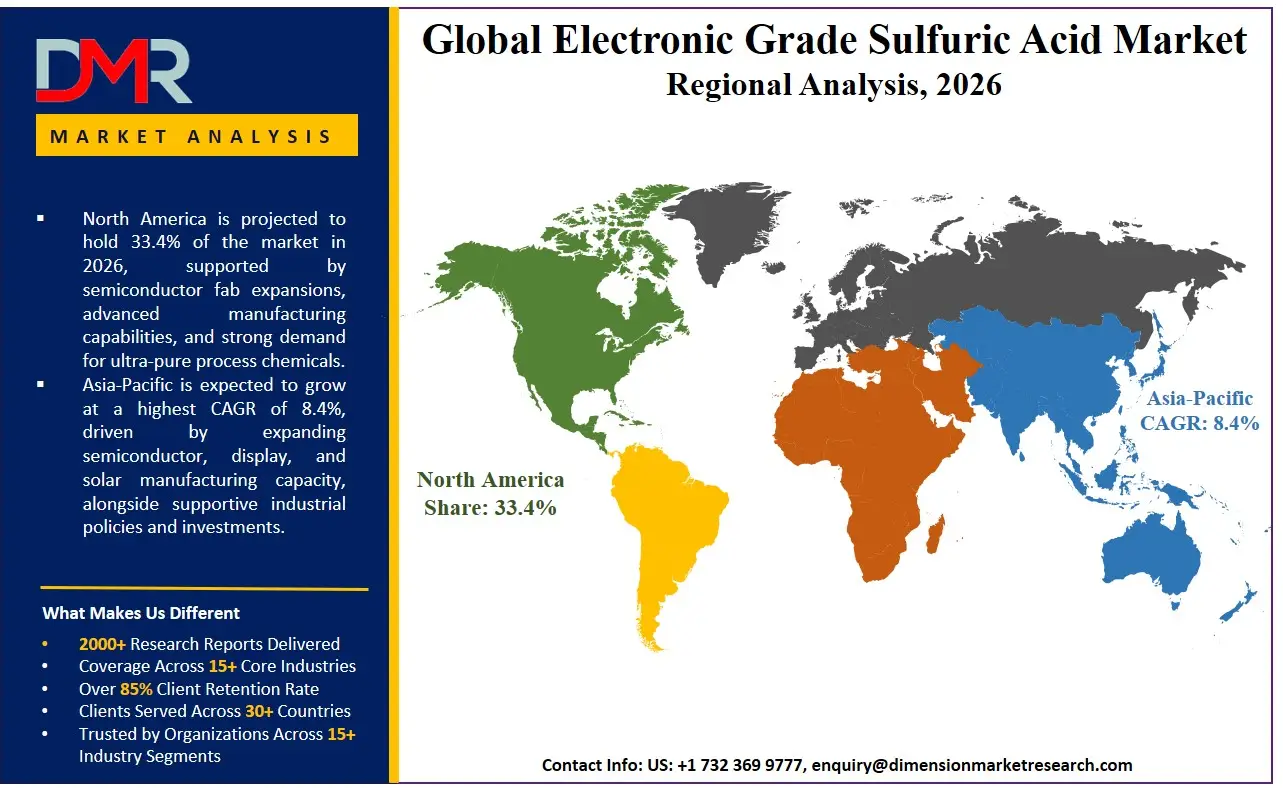

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia-Pacific is poised to dominate the global electronic grade sulfuric acid market, holding a 39.1% of the share in 2026, due to its unparalleled concentration of semiconductor foundries, IDMs, and display manufacturers. The region, led by Taiwan, South Korea, and China, has the highest share in electronic grade sulfuric acid consumption because of the massive scale of advanced node chip fabrication and the expansive build-out of photovoltaic cell capacity. The area has an established ecosystem of global chemical conglomerates, local high-purity specialists, and a rich pool of process engineers. Manufacturing investment in 3D NAND, DRAM, and the overall transition to gate-all-around transistor structures contribute to the continued demand for ultra-pure grades, with a direct sales model tightly integrated into fab chemical management systems. Moreover, aggressive government subsidy programs perpetually finance new mega-fab construction projects that require expert chemical supply partners to achieve immediate high-yield ramp-ups.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the fastest-growing regional market for electronic grade sulfuric acid, driven by sustained investments in semiconductor, display, and photovoltaic manufacturing. China, South Korea, Taiwan, India, and emerging Southeast Asian economies are expanding fabrication and component production capacities to meet rising global demand for advanced electronics. Supportive industrial policies, incentives for domestic chip production, and increasing adoption of next-generation technologies are accelerating the need for ultra-pure process chemicals. The region also benefits from a well-established supply chain, a skilled workforce, and the presence of major chemical suppliers that provide localized production and direct sales services. These advantages position Asia-Pacific for robust and sustained market growth throughout the forecast period.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global electronic grade sulfuric acid market has become highly dynamic, characterized by a heterogeneous array of multinational chemical giants, specialist Asian high-purity suppliers, and the on-site chemical service divisions of industrial gas companies. The key to success lies in profound strategic alliances with leading semiconductor foundries and IDMs, as these co-development partnerships open necessary qualification windows and align production capacity with advanced node requirements. The movement towards market consolidation is rapidly progressing, with traditional commodity chemical players acquiring boutique ultra-pure specialists to secure their technical purification know-how and existing fab qualification status. Proprietary intellectual property, including energy-efficient distillation processes and part-per-quadrillion analytical metrology, is becoming a more critical basis of competitive differentiation than simple production scale or low-cost feedstock access.

Some of the prominent players in the Global Electronic Grade Sulfuric Acid Market are:

- BASF SE

- KMG Electronic Chemicals

- Kanto Chemical Co., Inc.

- Stella Chemifa Corporation

- Mitsubishi Chemical Group Corporation

- Sumitomo Chemical Co., Ltd.

- Tokuyama Corporation

- Avantor, Inc.

- Honeywell International Inc.

- FUJIFILM Holdings Corporation

- Merck KGaA

- Entegris, Inc.

- Soulbrain Co., Ltd.

- OCI Company Ltd.

- Linde plc

- Moses Lake Industries, Inc.

- The Chemours Company

- Dongwoo Fine-Chem Co., Ltd.

- Grupa Azoty S.A.

- LSB Industries, Inc.

- Other Key Players

Recent Developments

- April 2025: BASF announced the construction of a new semiconductor-grade sulfuric acid plant at Ludwigshafen, Germany, to supply the growing European semiconductor industry with ultra-pure chemicals.

- August 2025: Entegris unveiled plans for an additional US technology center and R&D investment, further strengthening its advanced-purity and semiconductor materials capabilities that support high-purity process chemistries.

- February 2026: BASF reported that construction of its Ludwigshafen semiconductor-grade sulfuric acid facility was underway, reinforcing regional supply-chain resilience for European chipmakers.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 163.9 Bn |

| Forecast Value (2035) |

USD 282.4 Bn |

| CAGR (2026–2035) |

6.2% |

| The US Market Size (2026) |

USD 46.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Grade, By Distribution Channel, By Application, By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Electronic Grade Sulfuric Acid Market?

▾ The Global Electronic Grade Sulfuric Acid market is poised to be valued at USD 163.9 billion in 2026 and is projected to reach USD 282.4 billion by 2035, driven by the universal need for ultra-high-purity process chemicals in advanced semiconductor and photovoltaic manufacturing.

What is the CAGR of the Global Electronic Grade Sulfuric Acid Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 6.2% from 2026 to 2035, reflecting the accelerating complexity of chip architectures and the persistent capital investment in new global fabrication facilities.

What factors are driving the growth of the Global Electronic Grade Sulfuric Acid Market?

▾ Key drivers include the structural undersupply of ultra-pure chemical capacity, the imperative to clean next-generation 3D transistor structures without defects, the management complexity of multi-source chemical supply chains, and the surge in demand for direct sales quality agreements amid geopolitical trade disruption risks.

Which region held the largest share of the Electronic Grade Sulfuric Acid Market in 2026?

▾ Asia-Pacific is poised to hold the dominant share with 39.1% of market share in 2026, driven by a mature, dense ecosystem of leading-edge semiconductor foundries and display manufacturers in Taiwan, South Korea, and China. wNorth America held a 38.5% market share in 2026.

Which region is expected to grow the fastest in the Electronic Grade Sulfuric Acid Market?

▾ The North American region is expected to grow at the fastest rate, fueled by rapid, government-subsidized semiconductor fab construction in the US, where building a local ultra-pure supply chain is critical for transitioning new fabs to high-volume operations.

What are the major trends in the Global Electronic Grade Sulfuric Acid Market?

▾ Major trends include the integration of on-site purification systems at mega-fabs, the rise of acid reclamation and circular economy models, the demand for grade purity specific to new transistor architectures, and the focus on regionalized direct sales models to mitigate supply chain risk.

Who are the key players in the Global Electronic Grade Sulfuric Acid Market?

▾ Key players include global chemical giants like BASF SE, Mitsubishi Chemical Group, and KMG Chemicals, as well as regional ultra-pure specialists like Asia Union Electronic Chemical Corp. and Kanto Chemical, alongside industrial gas companies providing on-site solutions.

How is the Global Electronic Grade Sulfuric Acid Market segmented?

▾ The market is segmented by Grade, Distribution Channel, Application, and End User.