What is the Global Energy as a Service Market Size?

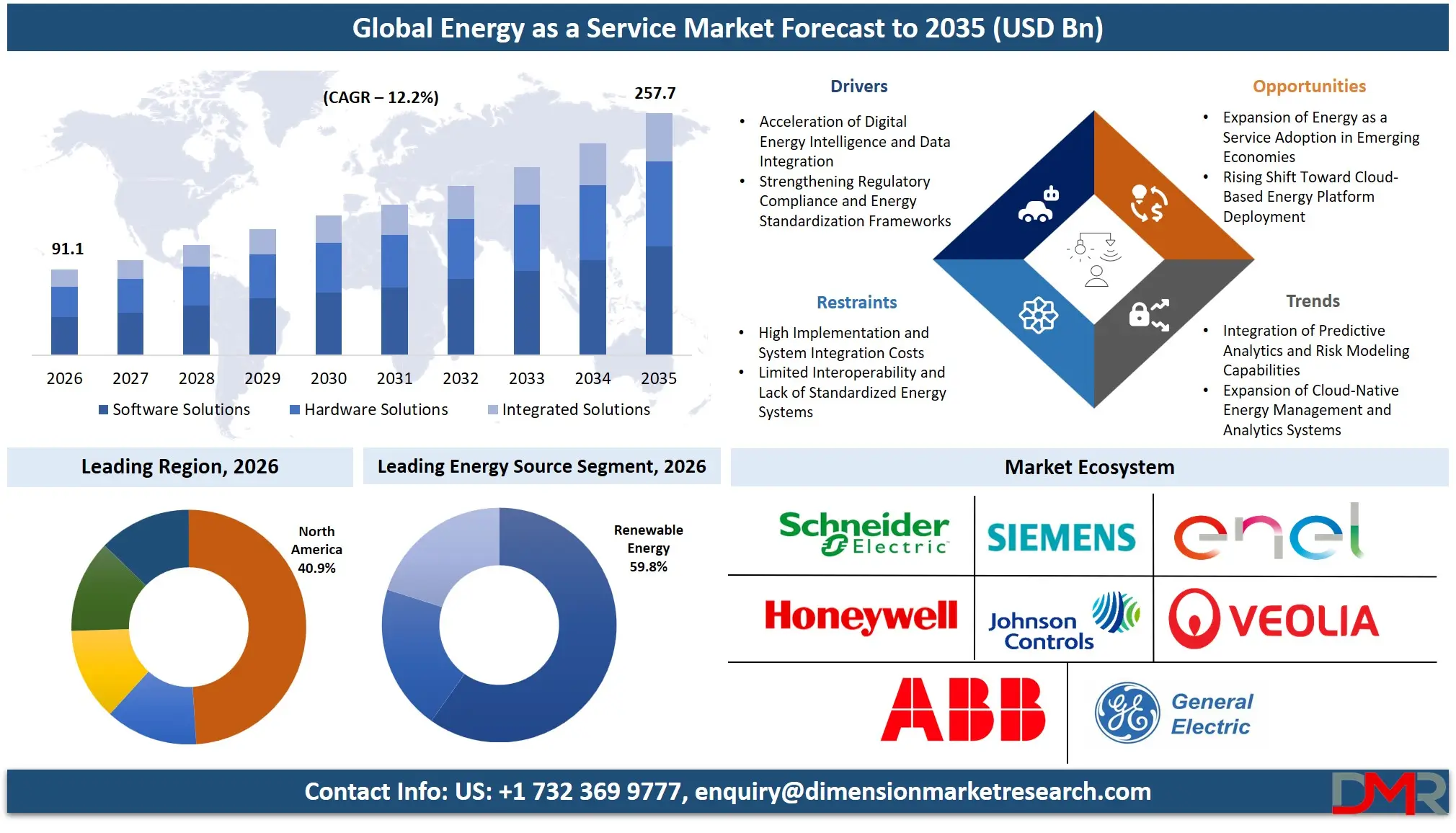

The Global Energy as a Service Market size is estimated at USD 91.1 billion in 2026 and is projected to reach USD 257.7 billion by 2035, exhibiting a CAGR of 12.2% during the forecast period, driven by the rising use of better digital tools in energy consumption optimization, automated load balancing in manufacturing, and connected climate action management systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global energy as a service market is expanding because of increasing use of smart software in detecting and analyzing energy reduction patterns and efficiency effectiveness; increasing approvals, which reduce the chance of rule-breaking during energy credit issuance and speed up the review process for new energy projects; and more funding in automating the use of energy-related data.

Some other reasons for expansion in this market include new technologies in real-time energy assurance, demand risk prediction through market makers, automated supply chain handling, and high-volume digital platforms, as well as better data-sharing rules. The digital shift in energy and utility companies has been helpful in speeding up product development and making energy management easier. This includes emissions tracking research. In addition, government plans focusing on preventing energy leakage and the clean energy economy have ensured steady research in energy storage and grid modernization systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

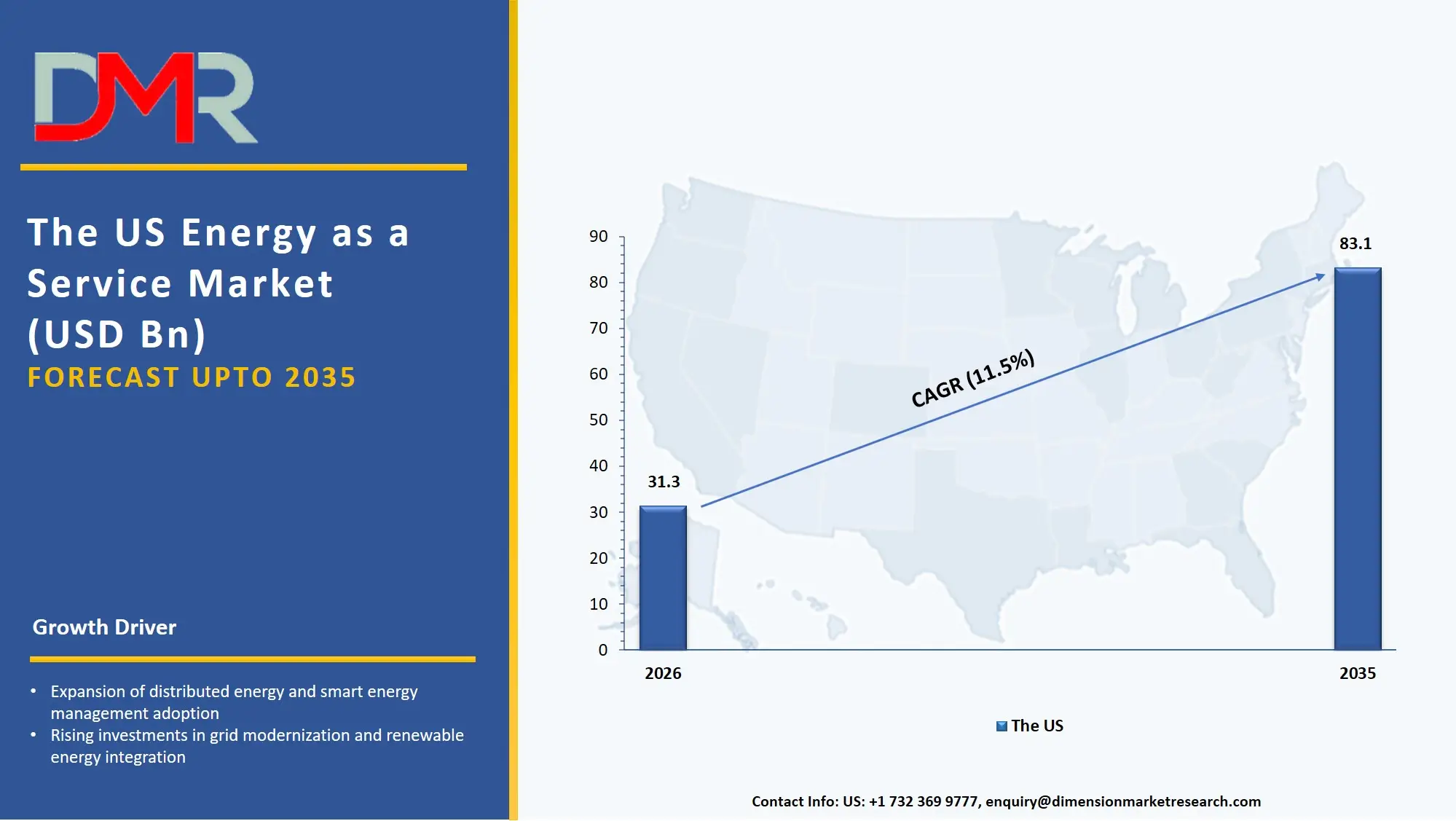

The US Energy as a Service Market

The US Energy as a Service Market is estimated to grow to USD 31.3 billion in 2026 with a compound annual growth rate of 11.5% during the forecast period.

The US market is shaped by major federal and state-level programs promoting net-zero emissions, clean energy affordability programs supported by the DOE and FERC, and DOE-led grid modernization initiatives. These programs encourage the use of smart energy testing, real-time corporate energy data analysis, and predictive forecasting software. Automated energy platforms are being rapidly adopted, and the US continues to invest in better data sharing between research labs, energy record systems, and reliable smart tools for energy platforms. Service providers are also influenced by laws like the Energy Policy Act and national digital climate strategies to offer services that ensure data safety, rule-following, and smooth integration across energy sources and grids.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Energy as a Service Market

The European Energy as a Service Market is estimated to be valued at USD 25.0 billion in 2026, witnessing growth at a CAGR of 11.1%, during the forecast period.

Europe's energy as a service market is well-established, shaped by EU-wide policies such as the EU Green Deal, the Clean Energy for All Europeans package, and national policies to support digital energy markets (e.g., Germany's energy transition plans and France's carbon neutrality strategies 2030). Countries are also making energy processes more flexible to align producer and consumer demands and enable the sharing of grid data across borders. The market grows due to new tools like software for real-time energy validation and scoring systems for efficiency projects. Use is made easier by teamwork between public and private groups and shared data rules. Manufacturers have access to technologies such as cloud computing and secure record-keeping, and Europe is at the forefront of the digitisation of safe and efficient energy operations.

Japan Energy as a Service Market

The Japan Energy as a Service Market is projected to be valued at USD 4.2 billion in 2026, progressing at a CAGR of 13.8%, during the period spanning from 2026 to 2035.

Japan's energy as a service market is well developed, with high-quality digital forecasting platforms, connected energy management systems, and a wide array of smart energy risk analysis software tools. National focus on automation, efficiency and process integrity is delivered via predictive energy models and smart asset management. Growth opportunities are helped by government measures under the Green Growth Strategy by Japan's Ministry of Economy, Trade and Industry (METI), and continued investment in digital energy market modernization. Energy research, industrial consumption analysis for condition-specific energy efficiency development, and virtual power plants all need effective smart software to keep pace with data analysis. Higher costs for validating new automation systems and connecting them with older grid registries are significant, but there are opportunities for the export of Japanese energy technologies to the Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Energy as a Service Market is estimated to be valued at USD 91.1 billion in 2026 and is expected to grow to USD 257.7 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 12.2% in the forecast period.

- Primary Growth Drivers: The availability of new energy processing technologies that use smart software, the need to speed up carbon neutrality results and improve success rates of renewable integration, and more government investment in national digital energy market infrastructure are key growth drivers.

- Key Market Trends: The predictive profiling of individual energy risks, real-time energy data handling, and the shift to cloud-based energy platforms and asset management platforms are key market trends.

- By Service Offering: Energy Efficiency & Optimization Services is expected to take the largest revenue share in 2026 in the global energy as a service market.

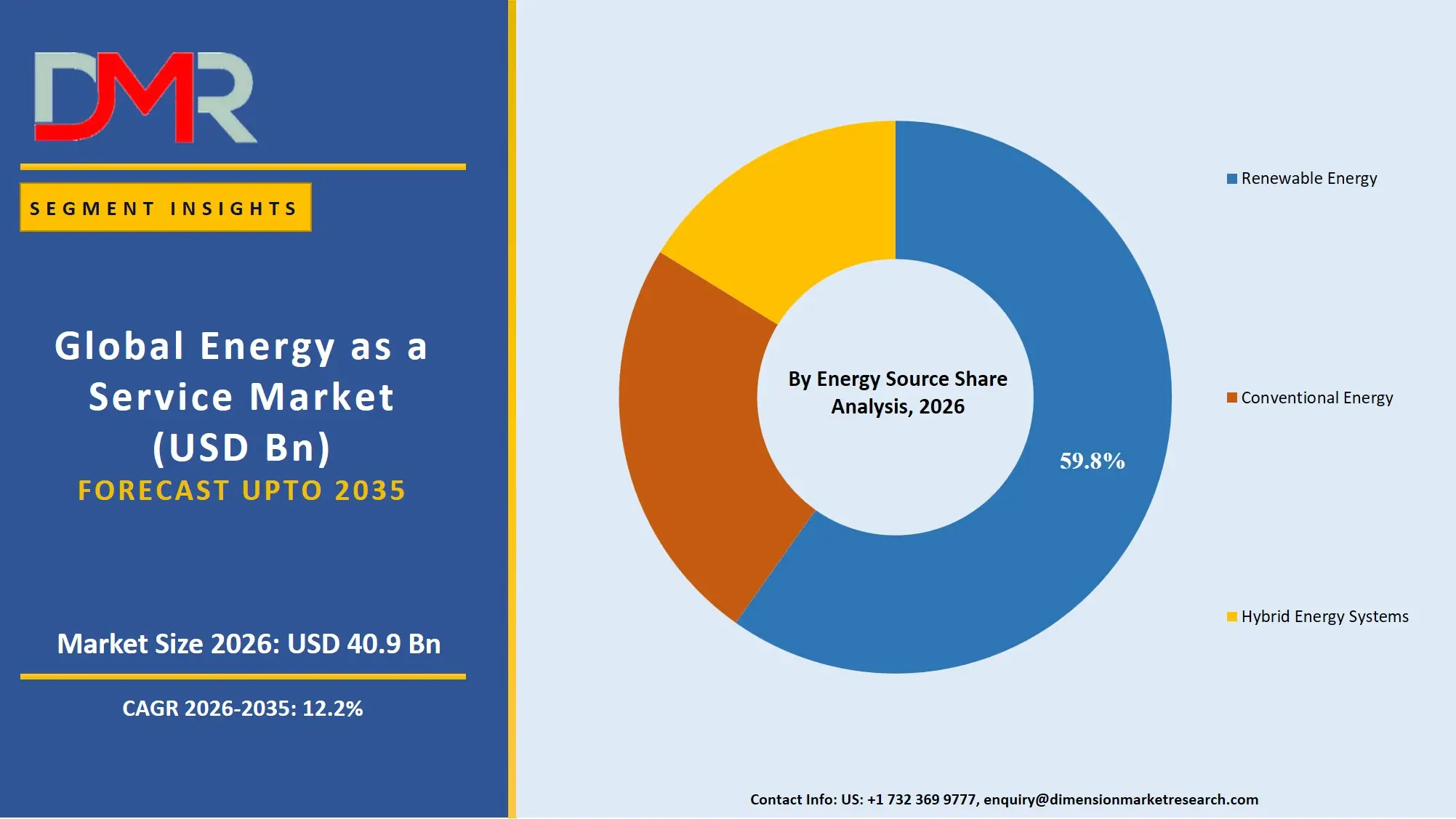

- By Energy Source: Renewable Energy is expected to take the largest revenue share in 2026 in the energy as a service market.

- By End-User: Commercial is estimated to take the lead in 2026 with the largest share in the energy as a service market, owing to digital adoption and ease of energy integration.

- Regional Leadership: North America is estimated to take the lead in 2026 with 40.9% share in the energy as a service market, owing to significant investment in energy market modernization and renewable energy technologies.

What is Energy as a Service?

Energy as a Service (EaaS) is a business model where customers pay for energy outcomes (e.g., kilowatt-hours, heating, cooling) without upfront capital investment in energy assets. EaaS providers develop, finance, own, operate, and maintain energy systems including distributed generation, storage, efficiency measures, and microgrids. These platforms use modern systems such as real-time energy verification, asset management software, and remote energy advisory to manage, verify, and track energy events and results. To improve energy market outcomes, manage demand variability and condition-specific energy programs, and expand service into personalized energy coverage to support individual customer care and promote the development of clean energy products.

Use Cases

- Market Stability for Daily Operations: Energy as a Service platforms can provide market-balancing benefits through software (analytics, control systems) to reduce volatility risk and support settlement in minutes, compared to days that it would take with only manual clearing.

- Long-Term Energy Asset Management: Long-term data on ongoing energy issues, including renewable intermittency, price spikes, or battery degradation, are studied to better understand market performance and to help plan long-term software-based care.

- Energy Load Balancing: Energy management is handled through digital platforms and smart software in commercial and industrial settings to support market capacity balance.

- Community Energy & Government Programs: Faster energy software development helps climate innovation and development of targeted efficiency programs; government programs through smart monitoring of national energy data advance national carbon neutrality strategies and help the adoption of operational standards.

How AI Is Transforming the Global Energy as a Service Market?

Artificial intelligence (AI) is being used progressively more often in energy platforms to improve energy demand forecasting, find quality trends, and automatically spot unusual patterns in energy sourcing data. It also allows faster energy verification because it can handle digital submissions on a large scale. Energy records and electronic invoices are easier to study and help grids find integration issues, reduce mistakes, and improve the overall accuracy of energy credit issuance. This has resulted in operations being cost-effective, quicker, and more efficient than the old manual review method.

AI is also strengthening research and development by improving risk assessment and enabling more accurate capacity planning. It helps utilities predict how much energy will be needed, find possible processing delays, and monitor the performance of energy networks more effectively. In addition, automation of routine checks and performance tracking is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is leading to better financial results and more stable operations across the energy production chain.

Market Dynamics

Key Drivers of the Global Energy as a Service Market

Acceleration of Digital Energy Intelligence and Data Integration

The market is growing with the rise of digital tools to check and process energy integration, better management of energy data, and a closer connection of grid records and trading platforms. Energy management platforms provide real-time data that allows monitoring of market workflow, helping to spot discrepancies early and checking rules much faster. This has improved efficiency in operations and reduced human mistakes as well as administrative costs. At the same time, demand for more automated research and development is being helped by more activity in predictive analytics for the assessment of individual energy risks, as climate science further digitizes basic utility and production tasks.

Strengthening Regulatory Compliance and Energy Standardization Frameworks

There is increasing emphasis on openness, data accuracy, and rule-following within the energy as a service system. Rules and frameworks such as the EU ETS and energy market modernization efforts in key markets are encouraging better data handling practices and more structured market processes. These advances are supporting the need for systems that can offer steady monitoring of energy assets and standardized reporting. At the same time, active work to improve the sharing of energy data and reduce verification issues is strengthening the need for more effective management systems in both government and private market participants.

Restraints in the Global Energy as a Service Market

High Implementation and System Integration Costs

The rollout of an energy as a service platform remains costly, requiring significant investment in system integration, testing, and alignment with market workflows. In addition, following data privacy rules such as GDPR and other regional laws adds to setup complexity. These factors increase upfront costs and can limit adoption, especially among smaller energy developers and new companies entering the market.

Limited Interoperability and Lack of Standardized Energy Systems

There is still fragmentation in the market in terms of data formats and quality handling procedures. Although some areas have put in place organized energy management systems, many grids continue to work with both digital and manual systems. Lack of standard rules limits the ability to share data between market operators and service providers and results in inefficiencies in software deployment and system integration.

Growth Opportunities in the Global Energy as a Service Market

Expansion of Energy as a Service Adoption in Emerging Economies

Newly developing economies such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are slowly building their energy and grid management systems. These regions have long-term growth possibilities, with more people adopting clean energy, and with more people becoming aware of energy efficiency programs and slowly digitizing energy care. These markets have few older grid registry systems and can be used with new, technology-driven energy platforms that can grow over time.

Rising Shift Toward Cloud-Based Energy Platform Deployment

The move to remote energy management, decentralized energy networks, and real-time market checks is creating the adoption of cloud-based energy systems. These systems allow centralized data access, better coordination between grids and market participants, and faster asset management. Cloud-based setup is increasingly becoming a trend among modern energy platform providers as operational efficiency becomes one of the competitive factors.

Global Energy as a Service Market Trends

Integration of Predictive Analytics and Risk Modeling Capabilities

Energy as a Service platforms are gradually adding data-driven technology to find risk trends and improve accuracy in data management. These systems allow cloud providers and corporates to study their customers' data behavior better, simplify the management of their secure portfolios, and improve their overall performance. This move is slowly turning the industry more proactive and data-driven in data protection instead of being purely reactive in market operations.

Expansion of Cloud-Native Energy Management and Analytics Systems

The use of cloud-based systems is currently becoming a basic part of today's energy operations. These systems allow real-time energy monitoring, centralized asset administration, and better network coordination among market participants. Cloud-based platforms are improving the efficiency and responsiveness of energy providers that operate in different regions by removing the need to rely on physical infrastructure and allowing operations to grow more easily.

Research Scope and Analysis

The Energy-as-a-Service market is witnessing strong growth driven by rising renewable energy adoption, grid modernization initiatives, and increasing demand for energy efficiency solutions. The market is segmented based on service offering, energy source, solution type, technology, commercial & delivery model, and end user.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Service Offering Analysis

The Energy Efficiency & Optimization Services segment is likely to continue dominating the market in 2026, accounting for approximately 38.5% of the global energy as a service market share. This is due to its key role in compliance-driven emissions reduction, structured energy management mechanisms, and strong regulatory enforcement under systems such as EU ETS and California Cap-and-Trade. These systems support continuous energy activity and standardized energy management across industries. Within Energy Supply Services, the Renewable Energy sub-segment holds the largest share, driven by high credit issuance volumes, automated demand for clean energy, and decarbonization requirements. The Microgrid-as-a-Service segment is the fastest-growing due to rising demand for energy resilience and islanding capabilities.

By Energy Source Analysis

The Renewable Energy segment is expected to account for 59.8% share in 2026, due to established regulatory frameworks, lower perceived risk, and faster compliance cycles compared to other energy sources. The segment is also driven by growing adoption of complete energy management plans and combined software options to increase value for utilities in commercial and industrial settings. It is also the fastest-growing segment in the energy as a service market, due to the fast uptake of fully connected energy workflows and market infrastructure. The Hybrid Energy Systems segment offers flexibility for project-based energy management and voluntary corporate claims, making it attractive for project developers and non-compliance buyers.

By Solution Type Analysis

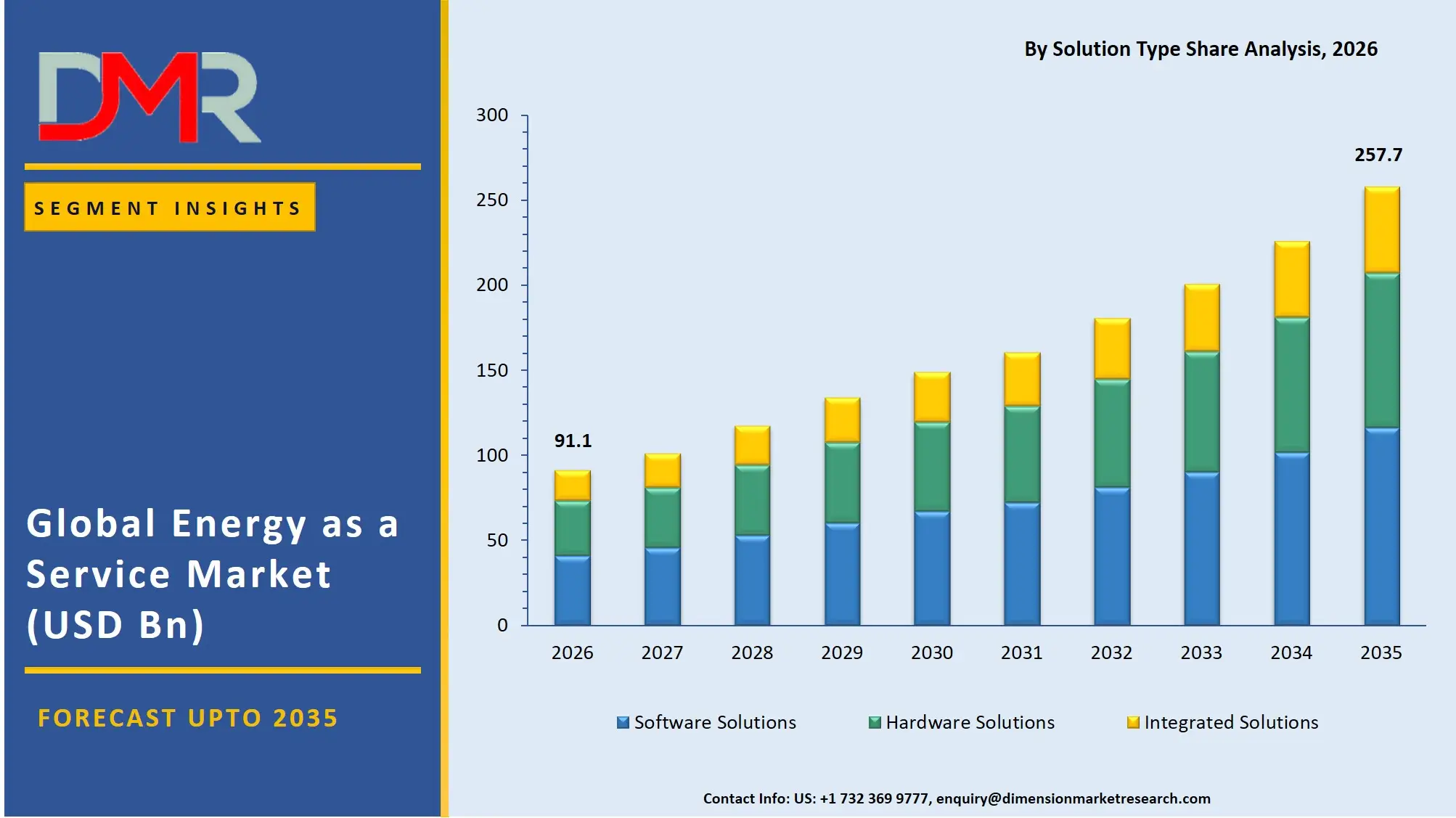

The Integrated Solutions segment is expected to dominate with around 48.5% market share in 2026, driven by greater clean energy penetration, faster software adoption, and broader market access compared to other solution types. Integrated energy solutions support customized management plans because they can offer multiple levels of daily generation forecasting, capacity amounts, and yearly plans, delivering fast results while keeping data within grid systems. The Software Solutions segment is the fastest-growing, driven by corporate digital commitments and government modernization mandates.

By Technology Analysis

The Distributed Energy Resources (DERs) segment is the largest technology segment in 2026, accounting for 32.5% share, driven by the need for compliance with emissions caps, renewable portfolio standards, regulatory mandates, and large-scale renewable integration. Businesses are adopting DERs for visibility and control over their energy profiles, while industrial users focus on energy cost reduction and carbon neutrality goals. The fastest-growing area is EV Charging Infrastructure, where commercial and industrial customers prefer smart, app-based energy storage to meet reliability requirements and voluntary carbon reduction pledges. This segment benefits from rising energy awareness, price volatility, and growing demand for integrated energy management systems linked to trading platforms.

By Commercial & Delivery Model Analysis

The Pay-for-Service (Subscription) model is expected to dominate the market in 2026, accounting for approximately 42.5% of the global energy as a service market share. This is due to its low upfront cost structure, predictable monthly billing, and ease of adoption for commercial and industrial customers seeking to outsource energy management without capital expenditure. The model is particularly popular among small and medium-sized businesses and multi-site commercial operators. The Build-Own-Operate-Transfer (BOOT) segment is the fastest-growing, especially in large-scale industrial and microgrid projects, as it allows customers to benefit from new energy infrastructure with no upfront investment and eventual asset ownership.

By End-User Analysis

The Commercial segment is the largest end-user in 2026, accounting for approximately 48.5% share, driven by the need for energy cost reduction, sustainability reporting requirements, and regulatory mandates for building energy performance. Commercial buildings, including offices, retail, hospitality, and healthcare facilities, are adopting energy as a service platforms for visibility and control over their energy consumption patterns. The fastest-growing area is the Residential segment, where homeowners prefer smart, subscription-based energy management systems, solar leasing, battery storage rental, and EV charging services to lower utility bills and reduce carbon footprints. This segment benefits from rising consumer awareness, smart home adoption, government incentives for residential efficiency, and growing demand for integrated home energy management systems.

The Global Energy as a Service Market Report is segmented based on the following:

By Service Offering

- Energy Supply Services

- Energy Efficiency & Optimization Services

- Energy Operations & Maintenance Services

- Energy Infrastructure Services

- Microgrid-as-a-Service

By Energy Source

- Renewable Energy

- Conventional Energy

- Hybrid Energy Systems

By Solution Type

- Software Solutions

- Hardware Solutions

- Integrated Solutions

By Technology

- Distributed Energy Resources (DERs)

- Energy Storage Systems

- Smart Energy Management & Analytics

- EV Charging Infrastructure

By Commercial & Delivery Model

- Pay-for-Service (Subscription)

- Performance-Based Contracting (ESCO / EPC)

- Build-Own-Operate-Transfer (BOOT)

- Leasing & Asset Rental

By End-User

- Commercial

- Industrial

- Residential

Regional Analysis

Leading Region in the Energy as a Service Market

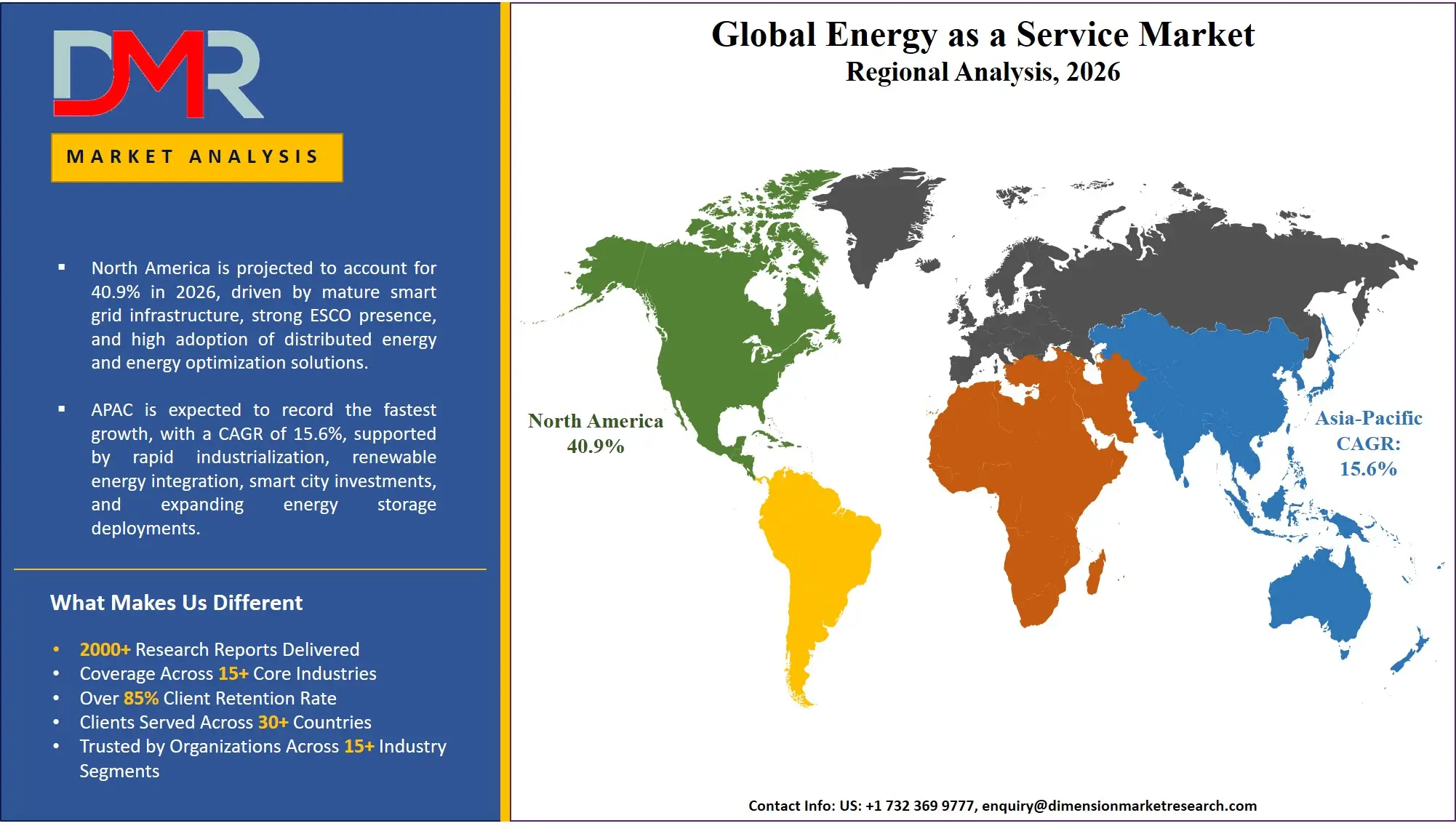

It is projected that North America will take the lead in the global energy as a service market (by value), covering a market share of about 40.9% in the year 2026. The region's dominance is driven by the world's most mature energy market infrastructure, strong energy modernization spending funded by public and private sources, higher average platform transaction fees compared to other regions, a mature digital supply chain for advanced data sharing, and the presence of major energy platform providers and trading exchanges. The widespread adoption of advanced market processing and automation for renewable energy credits, energy storage, and long-term energy management further strengthens North America's leading position. Additionally, ongoing investments in smart energy monitoring and cross-border system interoperability under USMCA and federal clean energy initiatives further reinforce the region's technology leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Energy as a Service Market

Asia-Pacific is the fastest-growing region, supported by strong digital energy market infrastructure goals in China, India, and Japan, increasing carbon neutrality awareness efforts, rising investments in local energy capabilities, and growing adoption of automated energy analysis systems. The region benefits from well-established digital payment systems for energy products, increasing business activity, and alignment with national carbon neutrality roadmaps. Countries across the region are actively setting up energy platforms to improve market efficiency and strengthen climate infrastructure. Growing focus on energy research and structured data development further speeds up market expansion. Moreover, increasing government support and corporate net-zero commitments are expected to keep growth momentum high.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The energy as a service market is highly competitive, with new ideas and strategic partnerships shaping the competitive environment. To gain an advantage, companies and providers are focused on developing better digital platforms (such as smart energy engines, automated verification systems, and mobile apps for energy management), smart data analysis, and cloud-based market monitoring. There are high barriers to entering the market due to the large amount of money needed for regulatory approval, specialized energy market knowledge, and the need for mature software systems and rule-following.

Strategic approaches to increase market presence include partnerships with climate research groups and grid operators, mergers between software providers and market operators, and long-term support contracts with customers and environmental institutions. Additionally, research and development in data-sharing rules and flexible software designs are important for staying competitive and meeting the changing needs of the energy community.

Some of the prominent players in the Global Energy as a Service Market are:

- Schneider Electric SE

- Siemens AG

- ENGIE S.A.

- Enel Group (Enel X S.r.l.)

- Honeywell International Inc.

- Johnson Controls International plc

- Veolia Environnement S.A.

- ABB Ltd.

- General Electric Company (GE Vernova)

- Eaton Corporation plc

- Électricité de France S.A. (EDF Group)

- Centrica plc

- Ørsted A/S

- Iberdrola S.A.

- Duke Energy Corporation

- NextEra Energy, Inc.

- Shell plc

- TotalEnergies SE

- NRG Energy, Inc.

- Ameresco, Inc.

- Other Key Players

Recent Developments

- January 2026: ENGIE S.A. reported expansion of renewable energy and storage assets in its January 2026 update, including large-scale wind, solar, and battery storage deployments in India, reinforcing its Energy-as-a-Service-driven decentralized energy strategy.

- November 2025: Schneider Electric SE launched EcoStruxure Foresight Operation, an AI-powered energy management solution integrating building, power, and industrial systems to optimize performance, efficiency, and sustainability across enterprise Energy-as-a-Service deployments.

- November 2025: Siemens AG highlighted advancements in AI-enabled smart infrastructure solutions, strengthening its Energy-as-a-Service capabilities through digital grid management, electrification technologies, and automation systems supporting large-scale energy efficiency and decarbonization programs.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 91.1 Bn |

| Forecast Value (2035) |

USD 257.7 Bn |

| CAGR (2026–2035) |

12.2% |

| The US Market Size (2026) |

USD 31.3 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Service Offering, By Energy Source, By Solution Type, By Technology, By Commercial & Delivery Model, and By End-User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Energy as a Service Market?

▾ The Global Energy as a Service Market size is estimated to have a value of USD 91.1 billion in 2026 and is expected to reach USD 257.7 billion by the end of 2035.

What is the CAGR of the Global Energy as a Service Market from 2026 to 2035?

▾ The market is growing at a CAGR of 12.2% over the forecasted period.

What factors are driving the growth of the Global Energy as a Service Market?

▾ The market is driven by advances in smart software-based energy processing, regulatory pressure to speed up carbon neutrality results and reduce verification mistakes, and increased government investment in national digital energy market infrastructure.

What are the major trends in the Global Energy as a Service Market?

▾ The key market trends include the adoption of predictive energy risk tracking and real-time energy data analysis, along with a growing shift toward cloud-based energy platforms and data-enabled asset management systems.

Which region held the largest share of the Global Energy as a Service Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 40.9%.

Which region is expected to grow the fastest in the Global Energy as a Service Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Energy as a Service Market?

▾ Some of the major key players in the Global Energy as a Service Market are Siemens AG, Schneider Electric SE, Engie SA, Veolia Environnement S.A., Honeywell International Inc., Johnson Controls International plc, Enel X S.r.l., and many others.

How is the Global Energy as a Service Market segmented?

▾ The market is segmented by service offering, energy source, solution type, technology, commercial & delivery model, and end-user.