What is the EU AI Act Compliance Solutions Market Size?

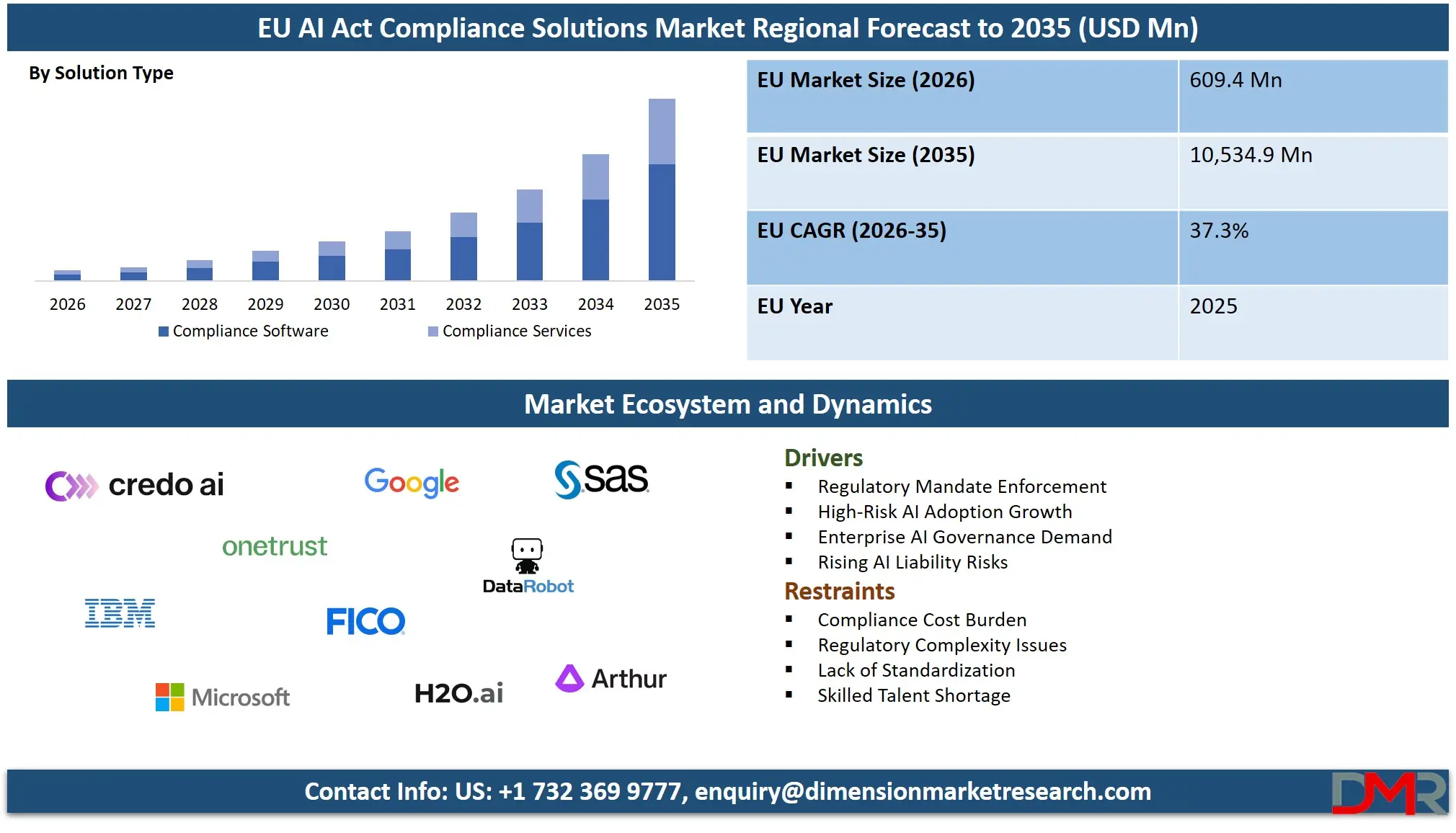

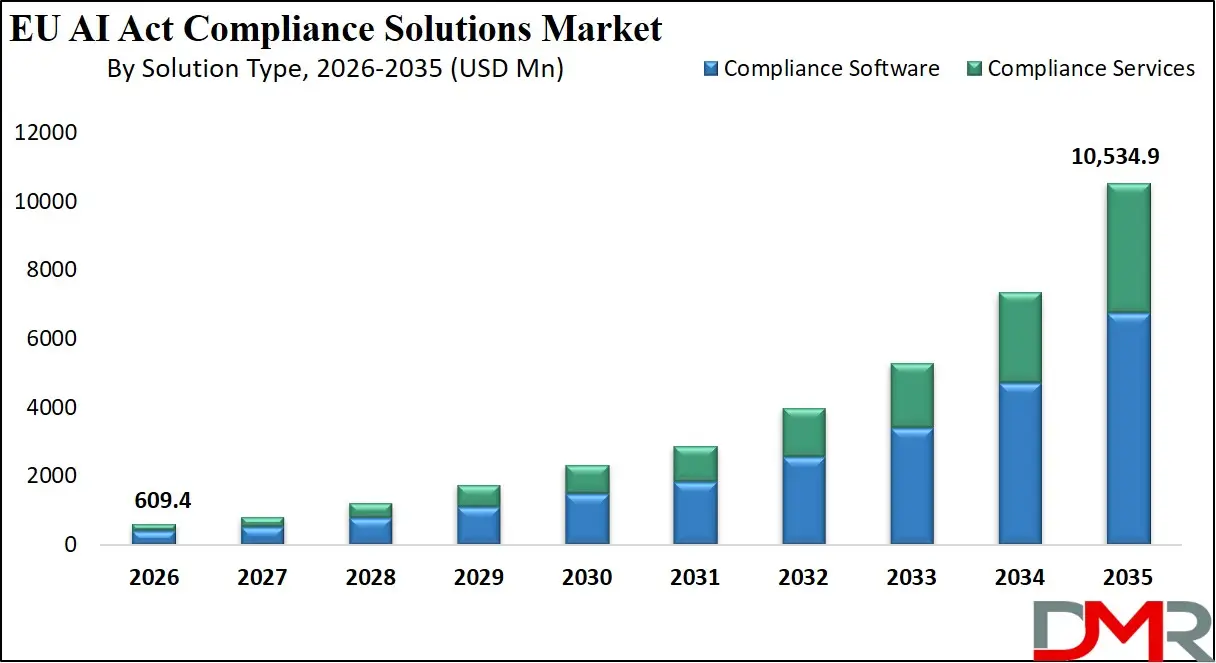

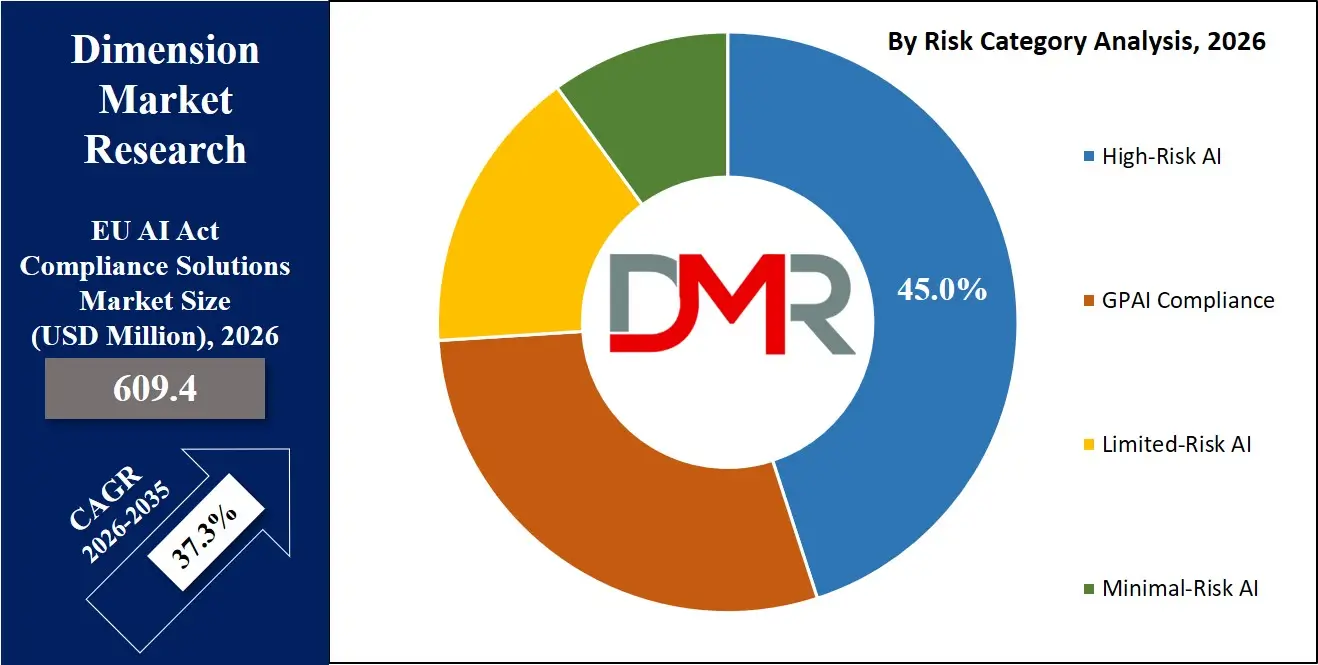

The EU AI Act Compliance Solutions Market size is projected to reach USD 609.4 million in 2026 and grow at a 37.3% CAGR, reaching USD 10,534.9 million by 2035, driven by demand for AI governance and compliance solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The EU AI Act Compliance Solutions Market is defined as software solutions and services assisting organizations in fulfilling the requirements of the Regulation EU 2024/1689. This market is expanding as a result of regulatory requirements like risk categorization, transparency, and human controls of AI systems. The adoption is being fast-tracked in enterprises by government-led initiatives and gradual implementation beginning in 2025.

The demand is also growing with the rise in the use of AI in controlled industries such as the health sector, financial sector, and government. The EU AI Act will be a global standard in the future, which will enhance the sustainability of compliance solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size: The EU AI Act Compliance Solutions Market is estimated to reach USD 609.4 million in 2026 and is projected to grow to USD 10,534.9 million by 2035, reflecting strong regulatory-driven expansion.

- Growth Rate and Outlook: The market is expected to grow at a CAGR of 37.3% from 2026 to 2035, driven by increasing AI adoption and mandatory compliance requirements.

- Primary Growth Drivers: Growth is driven by strict EU AI Act regulations, rising demand for AI governance solutions, and increasing deployment of high-risk AI systems requiring compliance.

- By Solution Type Analysis: Compliance Software dominates the segment, capturing 64.0% of the market share in 2026 due to strong demand for automated governance, risk management, and real-time monitoring solutions.

- By Compliance Function Analysis: Risk Classification leads the segment with a 21.0% share, as it is critical for categorizing AI systems under regulatory risk levels and ensuring appropriate compliance measures.

- By Deployment Model Analysis: Cloud deployment dominates with a 61.0% share, driven by scalability, flexibility, and seamless integration with enterprise AI and compliance systems.

- Country Leadership: Germany leads the market with a 22.0% share in 2026, supported by strong industrial AI adoption and high regulatory compliance requirements.

What are AI Act Compliance Solutions?

AI Act Compliance Solutions are software and services that assist organisations to comply with the Artificial Intelligence Act of the European Union. These solutions allow categorizing risks, being transparent, documenting and constantly monitoring AI systems. The EU system is risk-based, classifying AI as prohibited, high risk, limited risk, and minimal risk, but making high-risk systems subject to more stringent regulations. The regulation has took effect on August 2024, and has been phased in starting in 2025 and completed by 2026. According to the European Commission, non-compliance may lead to fines up to the value of 35 million euros or 7 percent of the annual global turnover. Such solutions are imperative to companies that have implemented AI in the EU, even international firms. All in all, they favor safe, transparent, and responsible AI adoption in line with the government regulations.

Use Cases

- Risk Classification & Documentation: Enterprises classify AI systems under risk categories and generate compliance documents. Platforms automate records for conformity checks. This reduces manual effort and speeds up regulatory approvals.

- Bias Detection & Explainability: Solutions identify bias and provide explainable outputs. This ensures transparency in regulated AI decisions. It also helps build trust among regulators and end users.

- Continuous Monitoring & Logging: Platforms track AI performance and capture audit logs. This supports ongoing compliance and risk control. It enables quick detection of anomalies and model drift.

- Data Governance & Lineage: Tools ensure dataset traceability and quality validation. This helps maintain compliant AI systems. It also supports accountability across the AI lifecycle.

Market Dynamics

Key Drivers in the EU AI Act Compliance Solutions Market

Regulatory Enforcement

Mandatory compliance under the EU AI Act is driving strong demand for compliance solutions across industries. Organizations must adhere to strict requirements for high-risk AI systems, including documentation and oversight. This is creating consistent demand for automated compliance tools. It also encourages early investment in governance frameworks. Overall, regulation is the primary growth driver of the market.

Enterprise AI Adoption

Rapid adoption of AI across sectors such as BFSI, healthcare, and public services is increasing compliance needs. Enterprises require structured systems to manage AI risks and regulatory obligations. This is accelerating investment in AI governance and compliance platforms. Growing AI deployment directly expands the compliance ecosystem. As AI use scales, compliance demand rises proportionally.

Restraints in the EU AI Act Compliance Solutions Market

High Compliance Costs

Implementing AI compliance solutions entails high costs for software, integration, and a skilled workforce. Many organizations face budget constraints when deploying full-scale compliance systems. This is particularly challenging for small and medium enterprises. High upfront investment slows adoption rates in price-sensitive markets. Cost pressure remains a key barrier to market expansion.

Regulatory Complexity

The EU AI Act introduces a complex and evolving regulatory framework that is difficult to interpret. Organizations often struggle to align internal processes with detailed compliance requirements. This increases dependency on external consultants and legal experts. Complexity also delays implementation timelines. Frequent regulatory updates further add to operational uncertainty.

Growth Opportunities in the EU AI Act Compliance Solutions Market

AI Governance Platforms

Growing demand for centralized AI governance platforms is creating strong market opportunities. Vendors are focusing on automated tools for risk management and compliance tracking. These platforms enable scalable and standardized AI operations. Cloud-based delivery models are further enhancing accessibility. This trend is opening new revenue streams for solution providers.

Cross-border Standardization

The EU AI Act is expected to influence global AI regulations, creating opportunities beyond Europe. Organizations operating internationally will need to align with EU standards. This increases demand for globally adaptable compliance solutions. It also encourages the development of standardized compliance frameworks. As a result, vendors can expand into new geographic markets.

Trends in the EU AI Act Compliance Solutions Market

Integrated Compliance in MLOps

Compliance capabilities are increasingly being integrated directly into MLOps pipelines. This allows real-time monitoring and automated validation of AI systems. Organizations are shifting from standalone tools to embedded compliance solutions. This improves operational efficiency and reduces manual intervention. Integrated compliance is becoming a standard practice in AI workflows.

Rise of Explainable AI

There is a growing focus on explainability to meet transparency requirements of the EU AI Act. Organizations are adopting explainable AI tools to interpret model decisions. This is especially critical in high-risk applications such as finance and healthcare. Explainability enhances trust among regulators and users. It is emerging as a core component of AI compliance strategies.

Research Scope and Analysis

By Solution Type Analysis

Compliance Software is expected to dominate the solution type segment, capturing 64.0% of the market share in 2026, driven by rising demand for automated AI governance, risk management, and compliance platforms. Organizations prefer scalable software for real-time monitoring, documentation, and risk classification of AI systems. These solutions streamline compliance processes and reduce manual effort. Meanwhile, Compliance Services support the market by providing legal advisory, conformity assessment, and integration expertise. Enterprises rely on these services to navigate complex regulations and implement compliance frameworks effectively. Together, services complement software by enabling complete compliance execution.

By Compliance Function Analysis

Risk Classification is expected to dominate the compliance function segment, capturing 21.0% of the market share in 2026, as it forms the foundation of the EU AI Act's risk-based framework. Organizations must categorize AI systems into defined risk levels, making automated classification tools essential for regulatory adherence. These solutions enable accurate identification of high-risk applications and ensure proper controls are applied. At the same time, Lifecycle Governance plays a critical role by managing compliance across the entire AI lifecycle from development to deployment and monitoring. It ensures continuous validation, updates, and oversight of AI systems. Together, both functions drive structured and end to end compliance management.

By Compliance Stage Analysis

The compliance stage segment is likely to be dominated by post-deployment, which will have 42.0% of the market share in 2026, due to the necessity of constant monitoring and the implementation of continuous regulatory compliance of AI systems. To be able to stay afloat in the long run, organizations need to monitor performance, identify drift in their models, and have audit logs. This step is essential because the EU AI Act puts an emphasis on the lifecycle responsibility beyond the first deployment. Pre-deployment, meanwhile, has a foundational role as it makes sure that risk assessment, data validation and compliance checks are fulfilled prior to the launching of AI systems. It assists organizations to detect possible risks at the early stages and align systems to the requirements of the regulators. This combination of the two stages guarantees the thoroughness of compliance throughout the AI lifecycle.

By Integration Type Analysis

Standalone Platforms are expected to dominate the integration type segment, capturing 38.0% of the market share in 2026, as organizations prefer dedicated compliance systems for centralized control and regulatory management. These platforms offer independent functionality for risk assessment, documentation, and audit readiness without relying on existing AI infrastructure. They are widely adopted by enterprises seeking quick deployment and standardized compliance processes. Meanwhile, MLOps integrated solutions are gaining traction as they embed compliance directly into AI development pipelines. This approach enables real-time validation, monitoring, and automated checks within workflows. Together, both models address different enterprise needs for compliance implementation.

By Deployment Model Analysis

The deployment model segment is likely to be dominated by cloud with a market share of 61.0% in 2026 due to the need to have scalable, flexible, and cost-effective compliance solutions. Organizations use cloud platforms to monitor in real-time, automatic updates, and integrate easily with AI systems. These solutions allow quicker deployment and adhere to changing regulatory needs. In the meantime, on-premises implementation is still applicable to the businesses with sensitive information and working in highly regulated industries. It provides an increased level of control over the data security, privacy and customization of the system. The two models combine to serve various compliance and infrastructure requirements.

By Risk Category Analysis

High Risk AI will be the lead in the risk category segment, as it will take 45.0% of the market share in 2026, when the EU AI Act comes into effect with its stringent requirements on systems utilized in the critical sectors of healthcare, finance, and public services. Companies should put in place effective compliance programs such as risk management, documentation, and human controls that increase the need of sophisticated compliance systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

These necessities render high risk AI as the main focus area to the vendors. In the meantime, the GPAI compliance is becoming increasingly significant as foundation models and general-purpose AI systems are becoming increasingly popular. It includes the model transparency, documentation, and usage controls obligations. Combined, both types are influencing the changing landscape of compliance.

By Organization Size Analysis

Large Enterprises will take up majority of the market share in organization size segment, with 68.0% of the market share in 2026, due to their large deployments of AI and the greater regulatory risk. These bodies possess the financial and technical resources to invest in sophisticated compliance systems and special governance frameworks. They are also given a more rigorous scrutiny, particularly in high risk AI applications, with more comprehensive solutions being adopted. In the meantime, the adoption of compliance solutions is slowing growing in SMEs as the use of AI is on the rise amongst small business owners. Nevertheless, small budgets and lack of in-house expertise are some of the restrictive factors. Though, SMEs demand will rise gradually with affordable solutions and cloud-based solutions available.

By End-use Industry Analysis

The end-use industry segment is projected to lead the market with BFSI dominating the segment with a market share of 22.0% in 2026 due to the widespread applications of AI in credit scoring, fraud detection, and risk analysis. These applications are classified as high-risk applications and they need high compliance, transparency and auditability. To cope with regulatory exposure and accountability of decisions, financial institutions are spending so much on compliance solutions. In the meantime, the Healthcare industry is also one of the most important since AI is gaining use in the field of diagnostics, clinical decision support, and medical imaging. These systems demand a high degree of precision, data control and regulatory approval. Consequently, compliance solutions play an essential role in providing safe and reliable AI implementation in the healthcare industry.

The EU AI Act Compliance Solutions Market Report is segmented on the basis of the following:

By Solution Type

- Compliance Software

- AI GRC Platforms

- Model Risk Tools

- Documentation Engines

- XAI Engines

- Audit Logging Systems

- Compliance Services

- Legal Advisory

- Conformity Assessment

- System Integration

- Managed Compliance

By Compliance Function

- Risk Classification

- Lifecycle Governance

- Data Governance

- Transparency Management

- Audit & Reporting

- Model Security

By Compliance Stage

- Pre-deployment

- Deployment

- Post-deployment

By Integration Type

- Standalone Platforms

- MLOps-integrated

- Pipeline Integration

- Model Registry Sync

- GRC-integrated

By Deployment Model

- Cloud

- SaaS Platforms

- API Modules

- On-premise

- Private Deployments

- Isolated Systems

- Hybrid

- Federated Setup

- Multi-cloud Control

By Risk Category

- High-Risk AI

- Conformity Systems

- Oversight Controls

- GPAI Compliance

- Model Governance

- Model Disclosure

- Limited-Risk AI

- Interaction Disclosure

- Content Labeling

- Minimal-Risk AI

By Organization Size

- Large Enterprises

- Multinationals

- Regulated Firms

- SMEs

By End-use Industry

- BFSI

- Healthcare

- Public Sector

- IT & Telecom

- Retail

- Manufacturing

- Others

By Region

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Competitive Landscape

Competition is moderately fragmented, consisting of both large technology providers, specialized compliance vendors, and new startups. Innovation, regulatory competence and the ability to integrate systems drive competition.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Automation, analytics, and industry-specific solutions are some of the ways vendors are differentiating. Market expansion and competitiveness is being influenced by strategic partnerships and acquisitions.

Some of the prominent players in the EU AI Act Compliance Solutions Market are:

- Credo AI

- OneTrust

- IBM

- Microsoft

- Google

- SAS Institute

- FICO

- DataRobot

- H2O.ai

- Arthur AI

- Holistic AI

- CalypsoAI

- Truera

- LatticeFlow AI

- KPMG

- Deloitte

- PwC

- CompliAI

- ActTier

- AIComply

- Other Key Players

Recent Developments

- April 2026: IBM launched enhanced AI governance and compliance capabilities within its watsonx platform to support automated risk classification and EU AI Act-aligned monitoring frameworks.

- March 2026: Accenture acquired an AI governance startup to strengthen its regulatory compliance and responsible AI service portfolio in Europe.

- February 2026: Holistic AI secured new funding to expand its AI risk management and compliance platform aligned with EU AI Act requirements.

- September 2025: Actus Digital introduced its upgraded Actus X AI-powered monitoring platform with advanced compliance logging and workflow automation features.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 609.4 Mn |

| Forecast Value (2035) |

USD 10,534.9 Mn |

| CAGR (2026–2035) |

37.3% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Solution Type (Compliance Software, Compliance Services), By Compliance Function (Risk Classification, Lifecycle Governance, Data Governance, Transparency Management, Audit & Reporting, Model Security), By Compliance Stage (Pre-deployment, Deployment, Post-deployment), By Integration Type (Standalone Platforms, MLOps-integrated, GRC-integrated), By Deployment Model (Cloud, On-premise, Hybrid), By Risk Category (High-Risk AI, GPAI Compliance, Limited-Risk AI, Minimal-Risk AI), By Organization Size (Large Enterprises, SMEs), By End-use Industry (BFSI, Healthcare, Public Sector, IT & Telecom, Retail, Manufacturing, Others) |

| Regional Coverage |

Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe |

Frequently Asked Questions

How big is the EU AI Act Compliance Solutions Market?

▾ The EU AI Act Compliance Solutions Market is expected to be valued at USD 609.4 million in 2026 and is projected to reach USD 10,534.9 million by 2035, reflecting rapid expansion driven by regulatory adoption.

What is the CAGR of the EU AI Act Compliance Solutions Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 37.3% during the forecast period from 2026 to 2035.

What factors are driving the growth of the EU AI Act Compliance Solutions Market?

▾ Growth is driven by strict EU AI Act regulations requiring risk classification, transparency, and continuous monitoring of AI systems. Rising adoption of AI in regulated sectors and increasing compliance and liability risks are also key drivers. Additionally, the global applicability of the EU AI Act is pushing enterprises to invest in governance solutions.

What are the major trends in the EU AI Act Compliance Solutions Market?

▾ Key trends include integration of compliance within MLOps pipelines, rising demand for explainable AI, and increased adoption of automated governance platforms. Continuous lifecycle monitoring and real-time audit capabilities are also becoming standard.

Who are the key players in the EU AI Act Compliance Solutions Market?

▾ Key players include Credo AI, OneTrust, IBM, Microsoft, Google, SAS Institute, FICO, DataRobot, H2O.ai, Arthur AI, Holistic AI, CalypsoAI, Truera, LatticeFlow AI, KPMG, Deloitte, PwC, CompliAI, ActTier, AIComply, and other key players.

How is the EU AI Act Compliance Solutions Market segmented?

▾ The market is segmented by Solution Type, Compliance Function, Compliance Stage, Integration Type, Deployment Model, Risk Category, Organization Size, and End-use Industry.