What is the Europe Electric Vehicle Charging Station Market Size?

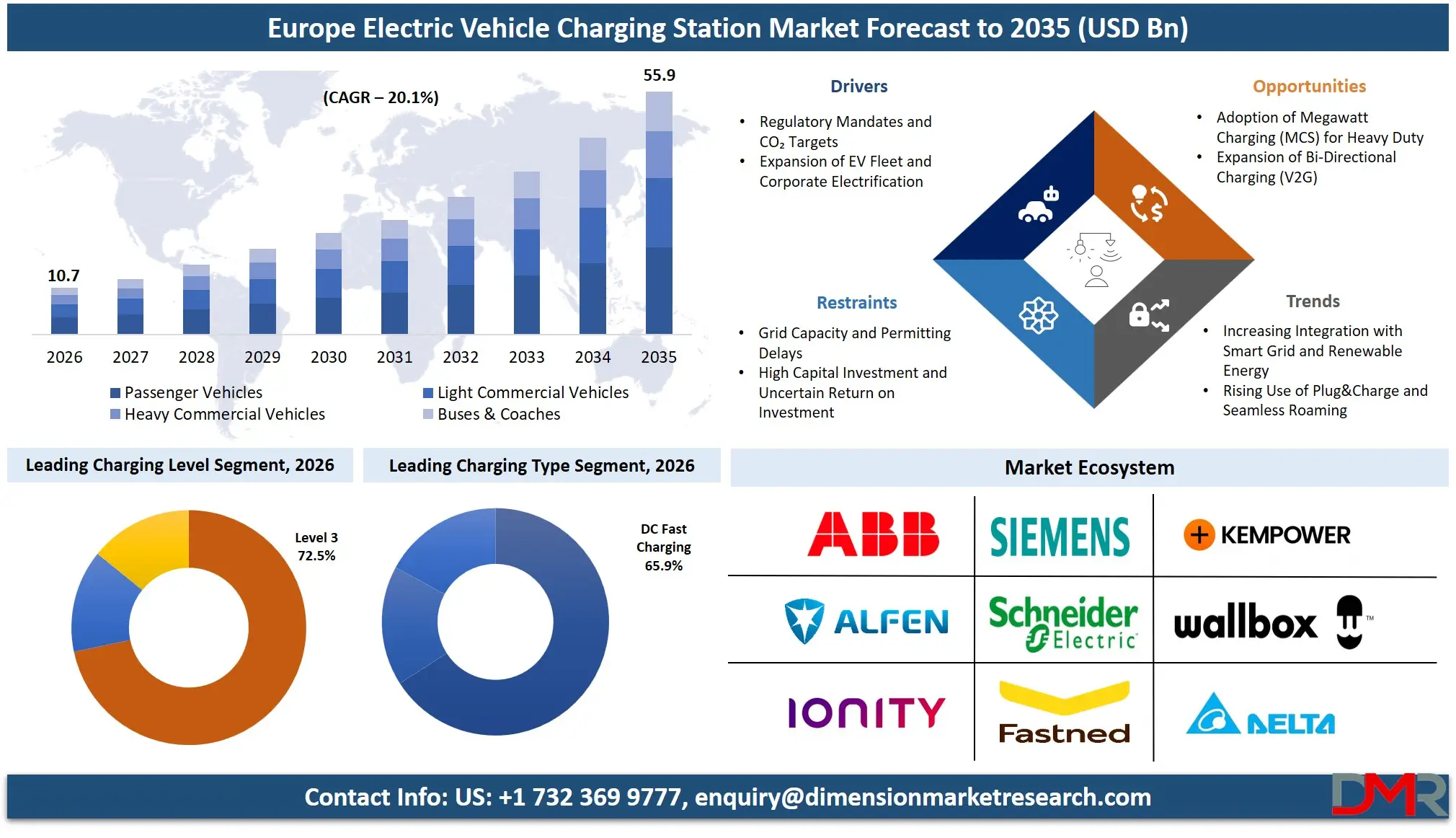

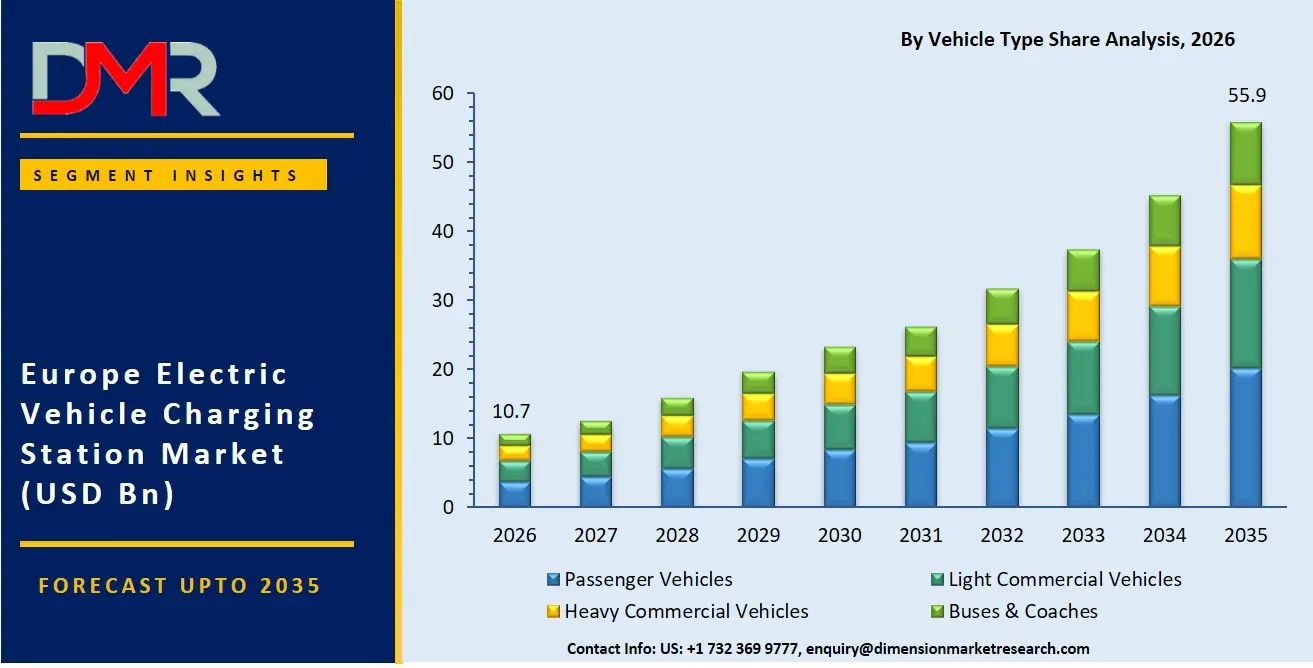

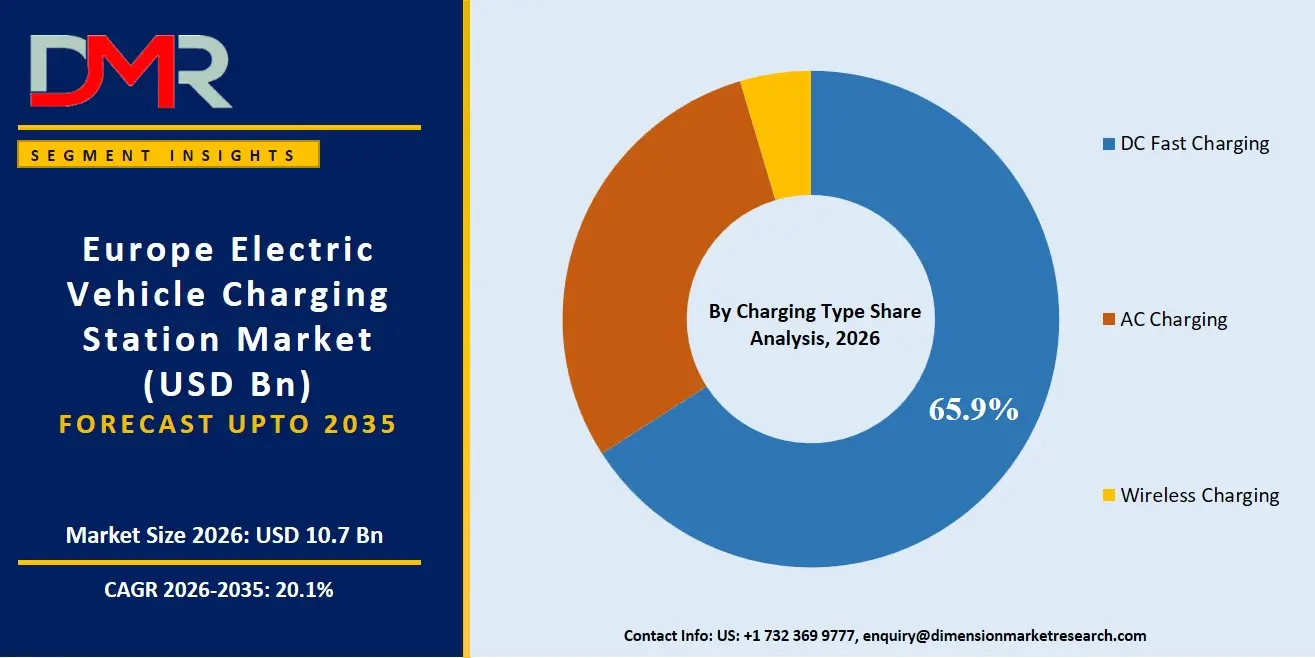

The Europe Electric Vehicle Charging Station Market size is estimated at USD 10.7 billion in 2026 and is projected to reach USD 55.9 billion by 2035, exhibiting a CAGR of 20.1% during the forecast period, fueled by a rise in EV usage in both passenger and commercial vehicles, expansion of charging infrastructure, deployment of fast-charging DC networks, and investments in intelligent charging technology, V2G technology, and renewable energy-powered charging technology.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The EV charging stations market has been witnessing steady growth on account of growing popularity of electric vehicles in several prominent economies in Europe, tough carbon dioxide emissions targets, and the initiatives by the EU to develop alternative fuels infrastructure. The EV charging stations include a variety of charging hardware and software as well as services that help businesses, cities, utilities, and fleets deploy robust and scalable charging networks. A rising demand for professional services has also become necessary because of the need to integrate charging infrastructure with renewable power generation facilities, manage grid limitations, and ensure a smooth customer experience with the help of advanced digital payments and charging network platforms. The public charging sector is expected to lead in terms of installations, while the market segment based on fast charging stations is predicted to account for the lion's share of the market value due to their high cost and rising adoption on highways and fast charging corridors within cities.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Europe Electric Vehicle Charging Station Market is estimated to be valued at USD 10.7 billion in 2026 and is expected to grow to USD 55.9 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 20.1% in the forecast period.

- Primary Growth Drivers: The availability of new charging processing technologies that use real-time degradation detection, the need to speed up compliance results and improve success rates of charging data sharing, and more government investment in national secure EV infrastructure are key growth drivers.

- Key Market Trends: The real-time profiling of charger thermal stability risks, high-power connector handling, and the shift to AI-driven charging load platforms and automated charger inventory management are key market trends.

- By Charging Type: The DC Fast Charging segment is expected to take the largest revenue share in the Europe electric vehicle charging station market in 2026.

- By Charging Level: Level 3 charging is expected to take the largest revenue share in 2026 in the charging station market.

- By Installation: The Commercial & Public Charging segment is estimated to take the lead in 2026 with the largest share in the charging station market.

What is an Electric Vehicle Charging Station?

An EV Charging Station refers to the suite of hardware, connectivity, and services required to charge EVs with electricity obtained from the grid. Unlike wallboxes installed at home, the term "EV Charging Station" applies to "how and where" EVs get charged using the grid in an industrial and public context. This involves using Charging Units (AC, DC, and wireless) for the purpose of providing electricity to EVs in a secure manner, and Software & Services for authentication, billing, load balancing, and monitoring. Given that Europe is stepping up its ban on combustion engines, it becomes critical to ensure that the charging systems are available.

Use Cases

- Fast Charging Corridors for Highways: Ministries of transport and charging network operators make use of DC fast chargers along TEN-T core network corridors for facilitating long haul EV journeys with the ability to recharge within less than 20 minutes.

- Fleet Electrification: Logistic firms depend on fleet charging at depots using load management software for overnight charging of commercial trucks.

- Destination Charging at Retail Sites: Shopping malls and supermarket chains use AC level 2 chargers as an attraction for consumers, providing them with discounted and free charges.

- On Street Residential Charging for Urban Areas: Municipality authorities install lamp post or bollard chargers in the central city areas where individuals do not have private parking space facilities.

How AI Is Transforming the Europe Electric Vehicle Charging Station Market?

The importance of artificial intelligence technology in the charging stations for electric vehicles market cannot be overstated, considering that AI enhances efficiency of networks, effective energy management, and utilization of charging stations infrastructure. Using AI technology platforms helps collect information about current and past demand, traffic, weather conditions, energy prices, and behavior of users to enhance operation at charging stations. Such a process facilitates better prediction of future demand for services, avoids overloading of charging stations with clients, and makes chargers available whenever needed. Using AI-based dynamic load management systems makes it possible to distribute energy effectively and avoid excessive consumption of energy during peak times.

Furthermore, AI is improving the dependability and scalability of electric vehicle (EV) charging infrastructures via predictive maintenance and intelligent management of assets. With the use of continuous monitoring of chargers, AI technology can identify performance discrepancies, predict possible equipment problems, and suggest maintenance procedures even before the occurrence of any interruptions. Additionally, AI is contributing to smart charging solutions and vehicle-to-grid (V2G) technologies that enable scheduling of charging processes according to grid status and renewable energy sources. The increasing application of AI-enabled analytics by charging providers helps make decisions regarding location of chargers, EV charging fleet management, and scaling up charging networks.

Market Dynamics

Key Drivers of the Europe Electric Vehicle Charging Station Market

Regulatory Mandates and CO₂ Targets

The binding goals established under the Alternative Fuels Infrastructure Regulation (AFIR) of the European Union and the national energy and climate plans in the Member States have revolutionized the landscape of EV charger installation. The regulation mandates fast-charging infrastructure within every 60 kilometers of all core TEN-T road networks and a power supply of at least 100 kW to each charging cluster from 2026 onwards. Moreover, there is also a multi-billion-euro opportunity in the EV charging industry due to the phasing out of internal combustion engine vehicles by 2035. These regulatory drivers form an essential part of long term investment certainty. Professional services involve compliance advisory and grant application support to help operators access EU funding mechanisms such as the CEF (Connecting Europe Facility) and national recovery plans.

Expansion of EV Fleet and Corporate Electrification

The increasing deployment of passenger cars, delivery vans, trucks, and buses in the European market is leading to high requirements in the charging industry within different domains, including logistics, public transport, carsharing, and staff mobility. In the current era, organizations implement solutions related to smart charging and depot charging to control the costs involved in energy consumption, prepare their fleet for the day's activities, and demonstrate the reduction in carbon footprints. Due to binding obligations under ESG policies, businesses are now more inclined toward managed charging systems. In addition, there is a growing need for guaranteed uptime and transparent billing, which increases the adoption rate of networked charging stations.

Restraints in the Europe Electric Vehicle Charging Station Market

Grid Capacity and Permitting Delays

The increasingly complex grid connection processes and lengthy permitting procedures in many European countries have brought about difficulties for charging station vendors as well as infrastructure operators. Local distribution system operators (DSOs) are tightening their technical requirements for simultaneous high power connections, which can lead to months or years of delay, especially in Germany, Italy, and Spain. Operators are expected to navigate highly variable local regulations, making their project timelines more complicated and costly. The violation of grid codes subjects a charging point operator to fines, output curtailment, and reputational harm.

High Capital Investment and Uncertain Return on Investment

The implementation of DC fast charging and ultra-fast charging systems would involve significant upfront investments in the charging systems, grid connection facilities, site developments, software platforms, and regular maintenance. Powerful charging stations may necessitate expensive electrical installation and additional grid capacity, resulting in higher total expenses. In some parts of the world, the usage rate of the charger system is not at an optimum level, especially in remote areas where electric vehicles are not yet widely used, increasing the payback period.

Growth Opportunities in the Europe Electric Vehicle Charging Station Market

Adoption of Megawatt Charging (MCS) for Heavy Duty

There exist many growth opportunities in the EV charging market in Europe through the increasing implementation of Megawatt Charging System (MCS) for heavy commercial vehicles and buses. MCS allows charging at up to 3.75 MW, drastically reducing downtime for electric trucks. Branded corridor charging, depot integration, and dynamic power sharing are some features that may be implemented by logistics companies in charging their fleets. Operators based in Germany, Sweden, and the Netherlands are starting to consider implementing MCS as an alternative for cost effective electric freight. With improved MCS standards and European funding for green freight corridors, many logistics organisations will spend much money on charging systems.

Expansion of Bi Directional Charging (V2G)

Integration of vehicle to grid technology into the charging infrastructure is bringing about great prospects for charging point operators in Europe. Many utilities and aggregators are now deploying V2G capable chargers that allow EV batteries to feed power back to the grid during peak demand. V2G can help building owners reduce energy bills, stabilize local grids, and generate revenue from frequency regulation services. The increasing use of fleet depots, bus garages, and workplace charging in different sectors such as logistics, public transport, and corporate campuses is driving demand for innovative bi directional hardware and energy management software.

Europe Electric Vehicle Charging Station Market Trends

Increasing Integration with Smart Grid and Renewable Energy

Increasingly, European charging operators are integrating with smart grid platforms and on site renewables (solar PV, BESS) to help reduce operating costs and CO₂ intensity. Smart charging allows operators to dynamically adjust power draw based on grid signals, local generation, and real time electricity prices. The advantages associated with grid integration include demand charge management, participation in flexibility markets, and green energy certification. Due to the growing adoption of corporate net zero approaches in addition to electrified transport, the use of energy optimised charging has been steadily increasing. The adoption of solar canopied charging hubs and battery buffered fast charging has continued to gain popularity in Europe.

Rising Use of Plug&Charge and Seamless Roaming

Seamless authentication approaches are being incorporated by European operators in order to facilitate EV drivers' experience using a combination of ISO 15118 Plug&Charge, RFID roaming, and mobile apps. Operators are focusing on creating an open roaming experience that ensures consistency in the quality of charging access through different network providers (e.g., Hubject, Gireve, eClearing). CCS2 connectors and the Plug&Charge standard continue to be an integral part of these interoperability approaches owing to their security and user convenience. Operators from sectors such as highway service areas, retail, commercial real estate, and municipal parking have been integrating Plug&Charge into their customer engagement solutions.

Research Scope and Analysis

The Europe EV Charging Station Market is segmented by charging type, charging level, installation, vehicle type, and connector type. The market supports passenger, commercial, and fleet charging across public, workplace, depot, and residential segments through smart, networked, and high‑power charging solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Charging Type Analysis

The DC Fast Charging segment is likely to continue dominating the market in 2026, accounting for approximately 65.9% of the Europe EV charging station market share. This is due to its key role in enabling highway corridor charging, reducing dwell time to under 30 minutes, and delivering high power output for long distance travel across Germany, France, and the Netherlands. Within this segment, ultra fast chargers (150kW–350kW) hold the largest share, driven by established highway deployment, long term real world utilization data, and continued EU co funding programmes under CEF and AFIR. The AC Charging segment is driven by lower installation costs and suitability for destination and workplace charging. These systems support ongoing commercial real estate activity and standardized safety management across residential and retail settings.

By Charging Level Analysis

The Level 3 charging segment is likely to continue holding the lead in 2026, accounting for approximately 72.5% of the Europe EV charging station market share, driven by excellent power delivery (150kW+), ability to support 800V vehicle architectures, and alignment with mandatory TEN T coverage targets. This segment reflects the continued need for high throughput, low dwell time chargers despite higher grid connection costs. The Level 2 segment is the second largest, supported by widespread workplace and residential adoption and lower installation complexity, while the Level 1 segment is also present, driven by legacy trickle charging for plug in hybrids and very low daily mileage users.

By Installation Analysis

The Commercial & Public Charging segment is expected to dominate with around 48.8% market share in 2026, driven by national government mandates for public charger density, established operator familiarity with motorway and retail site business models, and continued expansion into urban hub and destination charging programmes. Public charging supports long term e mobility adoption because of its well characterized utilization patterns and real world uptime durability data. The Fleet Charging segment is the fastest growing, driven by corporate ESG commitments for depot electrification and logistics fleet conversion. This segment is seeing strong growth with increasing venture capital investment and utility led depot modernization schemes. The Residential Charging segment remains significant but with lower growth due to longer replacement cycles.

By Vehicle Type Analysis

The Passenger Vehicles segment is the largest vehicle type in 2026, accounting for 61.5% share, driven by widespread EV adoption among private owners and corporate salary sacrifice schemes, use for daily commuting and regional travel, and integration with home and workplace charging. These applications provide predictable charging patterns and support both grid load management and user convenience. The Light Commercial Vehicles segment is the second largest, supported by last mile delivery electrification and urban low emission zone compliance, while Buses & Coaches is the fastest growing, driven by municipal zero emission fleet targets and the need for depot and pantograph charging infrastructure. Heavy Commercial Vehicles is also expanding rapidly with the emergence of megawatt charging corridors.

By Connector Type Analysis

The CCS2 segment is the largest connector type in 2026, accounting for 57.2% share, driven by regulatory mandate under AFIR, seamless interoperability across European charging networks, and adoption by all major automotive OEMs selling EVs in Europe. Comprehensive highway charging corridors and specialised fleet depots are adopting CCS2 for direct vehicle compatibility. The Type 2 segment is the second largest, supported by AC destination charging for passenger EVs, and the CHAdeMO segment is gradually declining as Japanese OEMs transition to CCS. The Pantograph Charging segment is the fastest growing, driven by electric bus and coach opportunity charging at terminuses, with increasing partnerships between public transport authorities and charging infrastructure providers.

The Europe Electric Vehicle Charging Station Market Report is segmented based on the following:

By Charging Type

- AC Charging

- DC Fast Charging

- Wireless Charging

By Charging Level

By Installation

- Residential Charging

- Commercial Public Charging

- Fleet Charging

By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Buses & Coaches

By Connector Type

- CCS1

- CCS2

- NACS

- GB/T

- CHAdeMO

- Type 1

- Type 2

- Pantograph Charging

By Region

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Competitive Landscape

The competitive landscape of the Europe EV Charging Station Market is highly dynamic, with a mix of charge point operators (CPOs), energy utilities, oil & gas companies, charging hardware manufacturers, and technology providers competing to expand their market presence. Companies are focusing on the deployment of high-power DC fast-charging networks, expansion of public and fleet charging infrastructure, and integration of smart charging and energy management solutions. Strategic partnerships with utilities, automakers, fleet operators, and local authorities have become increasingly important for securing grid access, accelerating infrastructure deployment, and enhancing charging network coverage.

Market participants are also investing in interoperability, roaming capabilities, and digital charging platforms to improve user experience and network utilization. In addition, mergers, acquisitions, and strategic collaborations continue to shape the competitive environment as companies seek to strengthen their geographic footprint and charging portfolios. As the market matures, factors such as charging reliability, network availability, smart energy integration, and operational efficiency are becoming key differentiators alongside hardware performance and pricing.

Some of the prominent players in the Europe Electric Vehicle Charging Station Market are:

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Alfen N.V.

- Kempower Oyj

- Wallbox N.V.

- Eaton Corporation plc

- Delta Electronics, Inc.

- Webasto SE

- IONITY GmbH

- Fastned B.V.

- Allego N.V.

- Electra SAS

- Atlante S.r.l.

- Virta Ltd.

- ChargePoint Holdings, Inc.

- Shell plc

- BP p.l.c.

- TotalEnergies SE

- EnBW Energie Baden-Württemberg AG

- Other Key Players

Recent Developments

- August 2025: EnBW Energie Baden-Württemberg AG expanded its fast-charging network in Germany with consistent monthly growth, reinforcing its leadership position in one of Europe's most dense EV charging markets.

- July 2025: Motor Fuel Group (MFG), a major UK charging infrastructure operator competing with Shell plc and BP p.l.c., announced expansion plans targeting 500 ultra-rapid EV charging hubs by 2030 under its £400 million rollout strategy.

- May 2025: Fastned B.V. continued rapid expansion across the Netherlands and Western Europe, strengthening its high-power charging footprint and increasing fast-charging capacity, reinforcing its position as one of Europe's leading pure-play CPOs alongside IONITY GmbH.

- April 2025: IONITY GmbH, Fastned B.V., Allego N.V., and Electra SAS formed the "Spark Alliance," creating Europe's largest interoperable ultra-fast charging network with ~11,000 charging points across 25 countries, enabling unified access and roaming across operators.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 10.7 Bn |

| Forecast Value (2035) |

USD 55.9 Bn |

| CAGR (2026–2035) |

20.1% |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Charging Type, By Charging Level, By Installation, By Vehicle Type, By Connector Type |

| Regional Coverage |

Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe |

Frequently Asked Questions

How big is the Europe Electric Vehicle Charging Station Market?

▾ The Europe Electric Vehicle Charging Station Market is estimated to be valued at USD 10.7 billion in 2026 and is expected to reach USD 55.9 billion by the end of 2035.

What is the CAGR of the Europe Electric Vehicle Charging Station Market from 2026 to 2035?

▾ The market is growing at a CAGR of 20.1% over the forecasted period.

What factors are driving the growth of the Europe Electric Vehicle Charging Station Market?

▾ Key growth drivers include increasing electric vehicle adoption, implementation of the EU's Alternative Fuels Infrastructure Regulation (AFIR), expansion of public and private charging networks, growing investments in DC fast-charging infrastructure, and the integration of smart charging and vehicle-to-grid (V2G) technologies.

What are the major trends in the Europe Electric Vehicle Charging Station Market?

▾ Major trends include the expansion of high-power DC fast-charging networks, increasing integration of renewable energy and smart grid technologies, growing adoption of Plug & Charge and roaming solutions, deployment of Megawatt Charging Systems (MCS) for heavy-duty vehicles, and the development of vehicle-to-grid (V2G) capabilities.

Who are the key players in the Europe Electric Vehicle Charging Station Market?

▾ Some of the major key players in the Europe Electric Vehicle Charging Station Market are ABB Ltd., Siemens AG, Schneider Electric SE, Alfen N.V., Kempower Oyj, Wallbox N.V., Eaton Corporation plc, IONITY GmbH, Fastned B.V., and many others.

How is the Europe Electric Vehicle Charging Station Market segmented?

▾ The market is segmented by charging type, charging level, installation, vehicle type, and connector type.