Market Overview

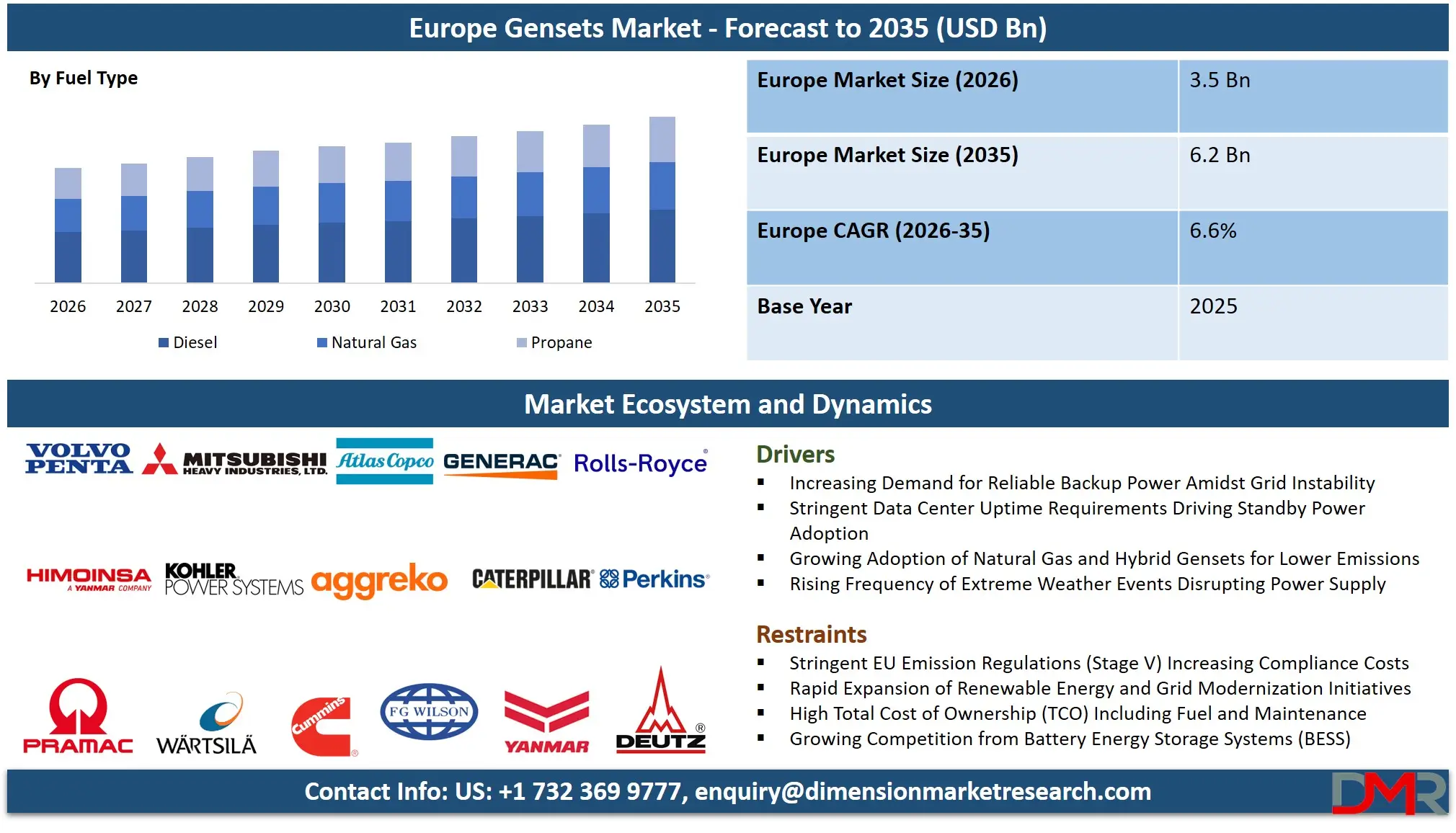

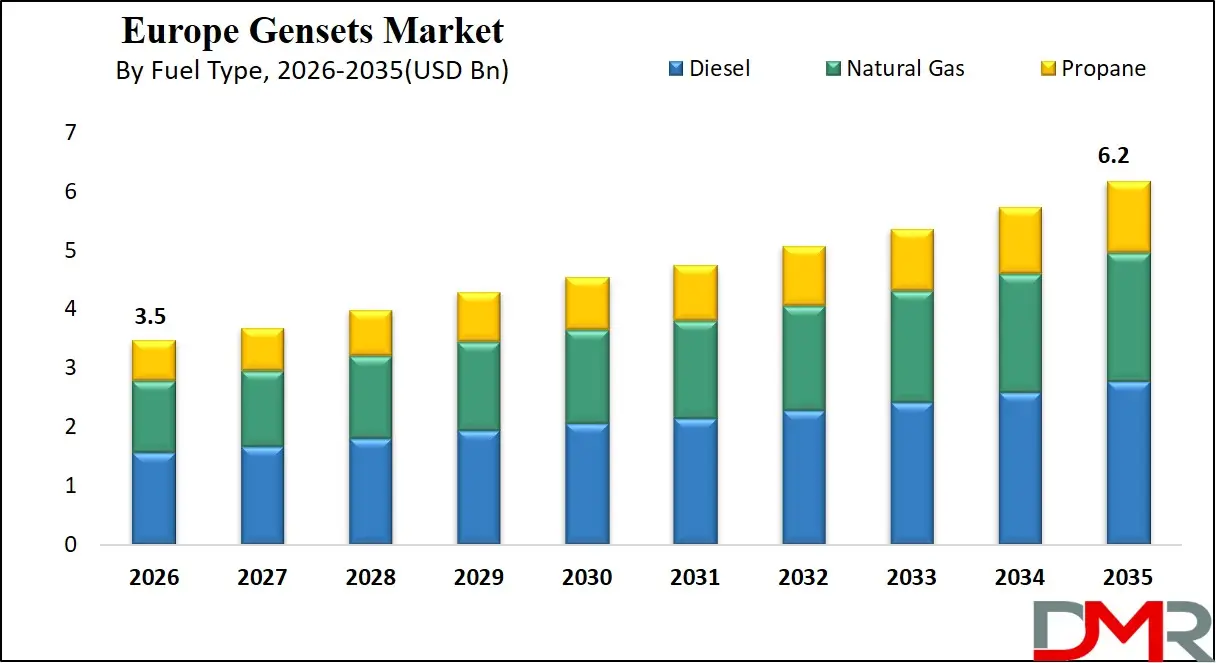

The Europe Gensets Market is projected to reach USD 3.5 billion in 2026 and is expected to grow at a CAGR of 6.6% from 2026 to 2035, reaching approximately USD 6.2 billion by 2035. Europe’s position in the global gensets industry is highly distinctive, shaped by its aggressive environmental policies, advanced industrial base, and increasing demand for energy resilience across both public and private sectors.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Unlike emerging markets where gensets are primarily used due to inadequate grid infrastructure, Europe represents a mature ecosystem where generator sets serve as a strategic complement to a well-developed but increasingly complex energy system. The region’s strong commitment to decarbonization, underpinned by regulatory frameworks such as the European Green Deal, has significantly influenced the evolution of genset technologies. Manufacturers are increasingly focusing on low-emission solutions, including natural gas, biofuel-compatible, and hydrogen-ready gensets, to comply with stringent EU Stage V emission standards.

Countries such as Germany, the United Kingdom, France, and Italy are at the forefront of adopting cleaner genset technologies. These nations are investing heavily in hybrid power systems that integrate gensets with renewable energy sources such as wind and solar. The growing share of renewables in the energy mix, while beneficial for sustainability, introduces intermittency challenges that necessitate reliable backup and balancing solutions. As a result, gensets are becoming critical components in maintaining grid stability and ensuring uninterrupted power supply.

Europe’s industrial landscape further contributes to sustained demand. The presence of highly automated manufacturing facilities, advanced logistics networks, and energy-intensive industries requires dependable power systems capable of preventing costly downtime. Additionally, the rapid expansion of data centers across Northern and Western Europe is creating significant demand for high-capacity gensets, particularly those exceeding 750 kVA, which can support mission-critical operations.

Another key factor driving the market is the increasing frequency of energy supply disruptions and extreme weather events. These challenges have heightened awareness around energy security, prompting governments and businesses to invest in robust backup power infrastructure. The integration of digital technologies, such as IoT-enabled monitoring and predictive maintenance, is also enhancing the efficiency and reliability of genset systems across the region.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Furthermore, Europe’s focus on circular economy principles and sustainable development is encouraging innovation in alternative fuels. Biofuels, hydrogen blends, and synthetic fuels are being explored as viable options for reducing carbon emissions associated with genset operations. Public funding and cross-border collaborations are accelerating research and development efforts in this area.

In summary, the Europe Gensets Market is characterized by a transition toward cleaner, smarter, and more integrated power solutions. While traditional diesel gensets continue to play a significant role, the future of the market lies in sustainable and technologically advanced systems that align with the region’s long-term energy goals.

Europe Gensets Market: Key Takeaways

- Steady Europe Market Growth Outlook: The Europe Gensets Market is expected to be valued at USD 3.5 billion in 2026 and is projected to reach USD 6.2 billion by 2035, showcasing steady expansion supported by rising power demand and grid unreliability.

- Moderate CAGR Growth: The market is expected to grow at a CAGR of 6.6% from 2026 to 2035, fueled by increasing infrastructure projects, urbanization, and a growing focus on energy security across industries.

- Diesel Dominance Faces Regulatory Pressure: Diesel gensets remain market leaders due to reliability and established infrastructure, but EU Stage V emissions standards and Green Deal objectives are accelerating the shift toward cleaner natural gas and hybrid alternatives.

- Data Centers Drive High-Capacity Demand: The Above 750 kVA segment is propelled by hyperscale data center expansion across FLAP-D markets, requiring multi-unit configurations with advanced emissions controls to meet stringent urban air quality regulations.

- Standby Power Reigns Across Sectors: Standby power dominates as critical infrastructure vulnerabilities grow, with hospitals, financial institutions, and SMEs investing in backup systems to counter grid instability from extreme weather and renewable integration.

- Manufacturing and Digital Infrastructure Lead End-Users: Manufacturing remains foundational across Germany, Italy, and Poland, while the data center segment emerges as the fastest-growing end-user, demanding hyper-reliable genset installations across Ireland, the Netherlands, and the Nordics.

Impact of Iran Conflict on Europe Gensets Market

- Increased Emphasis on Energy Security: Geopolitical tensions affecting global energy supply chains have reinforced the importance of reliable backup power systems in Europe. Disruptions in oil and gas supplies have prompted countries to strengthen their energy resilience strategies.

- Rising Fuel Costs Impacting Operations: Fluctuations in global fuel prices have increased the operational costs of gensets, encouraging the adoption of more efficient and alternative fuel-based systems.

- Acceleration of Renewable and Hybrid Solutions: The conflict has indirectly accelerated Europe’s transition toward renewable energy and hybrid power systems, reducing dependence on imported fossil fuels.

Europe Gensets Market: Use Cases

- Primary Power in Remote and Industrial Locations: Gensets provide essential primary power for remote industrial sites and infrastructure projects operating beyond grid reach, ensuring reliable electricity for critical operations in isolated environments.

- Backup Power for Business Continuity: Hospitals, data centers, and financial institutions depend on gensets for seamless backup power during outages, safeguarding critical functions, preserving data, and maintaining essential services without interruption.

- Peak Shaving for Energy Cost Optimization: Industrial facilities utilize gensets for peak shaving, strategically reducing demand from the grid during peak hours to lower electricity bills and optimize overall energy costs.

- Temporary Power for Events and Construction: Rental gensets deliver scalable, flexible temporary power solutions for large-scale events and construction projects, providing reliable electricity where permanent grid infrastructure is unavailable or impractical.

- Support for Renewable Integration: Gensets stabilize grids with high renewable penetration by compensating for solar and wind intermittency, ensuring a consistent power supply through fast response to generation fluctuations.

Europe Gensets Market: Stats & Facts

European Commission / Eurostat (EU Official Statistics)

- Renewable energy accounted for around 47% of EU electricity generation in 2025, increasing intermittency and backup power demand.

- The EU produces only about 44% of its total energy domestically, increasing reliance on backup power systems.

- Fossil fuels continue to contribute a significant share to the EU energy mix, supporting diesel genset usage.

ENTSO-E (European Network of Transmission System Operators for Electricity)

- Europe’s transmission network includes over 3,600 substations, many requiring backup power systems such as gensets.

- The European grid consists of more than 6,000 high-voltage transmission lines, increasing dependency on reliable backup systems.

European Energy & Infrastructure Data (Institutional / Industry-backed Studies)

- Around 1,500 grid substations in Europe integrated emergency gensets in 2024 for resilience.

- More than 500 emergency diesel gensets were deployed in tunnels and metro systems during 2023–2024.

- Approximately 200+ hospitals in Eastern Europe installed new gensets in 2024 for regulatory compliance.

- Europe accounts for about 25% of global emergency diesel generator projects.

- Around 30% of genset installations include noise and emission control systems due to EU regulations.

- About 15% of genset orders in Nordic countries require cold-weather performance upgrades.

- Roughly 7% of genset exports to Africa are routed via European distribution networks.

Carbon Monitor Europe / European Energy Bodies

- Europe tracks daily power sector emissions across 27 EU countries and the UK, reflecting monitoring of diesel-based backup generation.

- Power sector emissions in Europe have declined by nearly 46% from peak levels, encouraging cleaner genset technologies.

- In 2023, Europe’s power sector emissions declined by around 19% year-on-year.

Country-Level Capacity Data (European Energy / Institutional Sources)

- Germany had over 770 MW of diesel generator capacity projected by 2025.

- The UK’s genset capacity is expected to reach around 646 MW by 2025.

- France’s genset capacity is projected at approximately 429 MW by 2025.

- Italy’s genset capacity is expected to reach around 262 MW by 2025.

- Total European genset capacity is projected to reach about 2,487 MW by 2025.

- Europe’s genset capacity increased from around 1,859 MW in 2017 to over 2,012 MW in 2019.

Ember / European Power Mix Insights

- Renewable sources contribute around 48% of electricity generation in Europe, increasing variability and backup demand.

- Nuclear energy accounts for about 25% of electricity generation, requiring backup during outages.

- Fossil fuels still represent around 27% of electricity generation, supporting genset fuel demand.

Europe Gensets Market: Market Dynamic

Driving Factors in the Europe Gensets Market

Increasing Demand for Reliable Power Supply

The rapid digitalization of Europe’s economy has significantly increased dependence on uninterrupted electricity. Critical infrastructure such as data centers, telecom networks, healthcare facilities, and automated manufacturing plants require continuous power to prevent operational disruptions and financial losses. Even short outages can result in substantial downtime costs, especially in sectors like cloud computing and financial services. As a result, gensets are widely deployed as primary backup solutions to ensure business continuity and maintain system reliability across both urban and remote locations.

Expansion of Renewable Energy Capacity

Europe’s aggressive transition toward renewable energy sources such as wind and solar has introduced variability into the power grid due to their intermittent nature. While renewable energy improves sustainability, it also creates instability during periods of low generation. Gensets play a crucial role in balancing this variability by providing instant backup power during fluctuations or grid failures. This is particularly important in countries with high renewable penetration, where hybrid energy systems combining renewables and gensets are becoming standard practice.

Restraints in the Europe Gensets Market

Stringent Environmental Regulations

European governments have implemented strict emission standards, including Stage V regulations, which limit nitrogen oxide (NOx) and particulate matter emissions from diesel gensets. Compliance with these standards requires advanced exhaust after-treatment systems, increasing manufacturing complexity and costs. Additionally, growing pressure to reduce carbon footprints is discouraging the use of traditional diesel gensets, pushing manufacturers to invest heavily in cleaner alternatives. These regulatory challenges can slow adoption, particularly among cost-sensitive users.

High Initial Investment Costs

Modern gensets, especially those equipped with advanced control systems, noise reduction technologies, and emission compliance features, require substantial upfront investment. High-capacity gensets used in industrial and data center applications involve not only equipment costs but also installation, fuel storage, and maintenance infrastructure expenses. For small and medium-sized enterprises, these costs can be prohibitive, limiting market penetration and encouraging the adoption of rental or leasing models instead.

Opportunities in the Europe Gensets Market

Development of Hydrogen and Biofuel Gensets

The shift toward decarbonization has opened new opportunities for alternative fuel-based gensets. Hydrogen-powered generators and biofuel-compatible systems are gaining traction as sustainable solutions that align with Europe’s climate targets. These technologies significantly reduce greenhouse gas emissions while maintaining performance levels comparable to conventional gensets. As hydrogen infrastructure develops and biofuel availability increases, manufacturers are expected to accelerate innovation and commercialization in this segment.

Integration of Digital Technologies

The adoption of IoT, artificial intelligence, and remote monitoring systems is transforming genset operations. Smart gensets can provide real-time performance data, predictive maintenance alerts, and fuel optimization insights, reducing downtime and operational costs. Digital integration also enables better energy management by synchronizing gensets with grid supply and renewable sources. This technological advancement enhances efficiency and reliability, making gensets more attractive to modern industries.

Trends in the Europe Gensets Market

Shift Toward Hybrid Power Solutions

Hybrid systems combining gensets with renewable energy sources such as solar and battery storage are becoming increasingly prevalent. These systems reduce fuel consumption, lower emissions, and improve overall energy efficiency. Businesses and utilities are adopting hybrid solutions to meet sustainability goals while ensuring uninterrupted power supply, particularly in off-grid and remote applications.

Growth of Rental and Service Models

The high capital cost of gensets has led to a growing preference for rental and subscription-based models. Businesses are increasingly opting for flexible power solutions that allow them to scale usage based on demand without significant upfront investment. Rental services are particularly popular in construction, events, and emergency applications, where temporary power is required. Additionally, service-based models that include maintenance and monitoring are gaining traction.

Europe Gensets Market: Research Scope and Analysis

By Fuel Type Analysis

The diesel gensets segment continues to hold a dominant position in the European market, driven by its reliability, high power density, and established service networks across the continent. Diesel remains the preferred choice for critical backup applications in European hospitals, data centers, and telecommunications infrastructure, particularly in regions where grid reliability varies significantly between Western and Eastern Europe. The extensive existing fleet of diesel units across the EU, combined with mature fuel distribution networks, has created a strong replacement and maintenance-driven market. However, the segment faces increasing regulatory pressure as the European Union tightens emissions standards under the Stage V regulations and advances its Green Deal objectives, pushing manufacturers toward cleaner diesel technologies and hybrid solutions.

The natural gas gensets segment is experiencing the strongest growth trajectory across Europe, fueled by the continent's focus on decarbonization and energy security following geopolitical disruptions. European nations with extensive gas pipeline infrastructure, particularly in Germany, Italy, the Netherlands, and the United Kingdom, are witnessing accelerated adoption of gas gensets for combined heat and power (CHP) applications, district heating systems, and industrial cogeneration. The segment's growth is further supported by EU policies promoting the transition from coal to natural gas as a bridge fuel, along with incentives for high-efficiency cogeneration plants that meet the criteria for the Energy Efficiency Directive. Biogas and biomethane gensets are emerging as a specialized sub-segment, benefiting from Europe's strong agricultural sector and renewable energy support mechanisms.

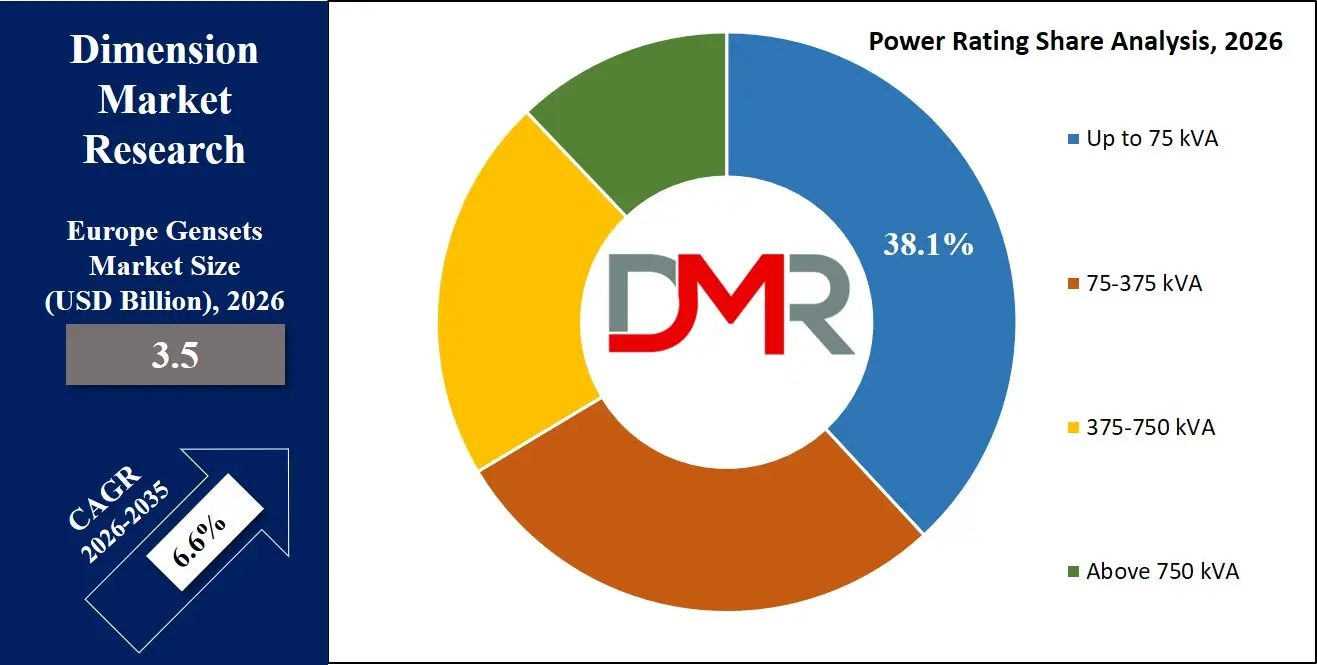

By Power Rating Analysis

The Above 750 kVA segment represents a critical component of Europe's critical infrastructure protection strategy, serving large-scale data centers across the Dublin, Frankfurt, London, Amsterdam, and Paris (FLAP-D) markets, major healthcare facilities, and industrial complexes. The rapid expansion of hyperscale data centers across Europe, driven by cloud computing growth and the EU's digital transformation agenda, has created sustained demand for high-capacity gensets capable of delivering extended runtime during grid events. These installations increasingly feature multi-unit parallel configurations with sophisticated emissions control systems to comply with stringent local air quality regulations, particularly in urban areas where large facilities are often located.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The 75-375 kVA segment forms the backbone of Europe's commercial and municipal backup power infrastructure, serving office buildings, retail centers, public sector facilities, and small to medium manufacturing operations. This segment benefits from consistent replacement cycles driven by EU emissions compliance requirements and the aging installed base across European cities. The 375-750 kVA segment addresses the needs of regional data centers, university campuses, district heating plants, and medium-scale industrial facilities. The Up to 75 kVA segment serves a mature but stable market across European small businesses, agricultural operations, and residential applications, with growing interest in bi-fuel and LPG configurations as homeowners and small enterprises seek alternatives to diesel for backup power.

By Application Analysis

The standby power application dominates the European gensets market, driven by the continent's increasing awareness of critical infrastructure vulnerabilities following extreme weather events, grid strain from renewable integration, and the geopolitical energy crisis of the 2020s. European hospitals, financial institutions, emergency services, and transportation hubs face rigorous regulatory requirements for backup power continuity, with standards varying by member state but generally mandating comprehensive emergency power systems. The digitalization of European economies has expanded the definition of critical infrastructure, with small and medium enterprises increasingly investing in standby protection to safeguard operations against the rising frequency of localized grid disruptions.

The prime/continuous power application remains vital for Europe's remote and island communities, particularly across the Mediterranean, the Nordic regions, and the Atlantic territories. Greece, Italy, Spain, and Portugal host numerous islands where gensets provide primary power during grid constraints or seasonal demand surges. The construction and infrastructure development sector across Europe relies on prime power gensets for major projects, including transportation corridors, renewable energy installations, and urban development sites where temporary power solutions are essential before grid connections are established. The peak shaving application is gaining traction among European industrial facilities facing rising electricity costs and complex demand charge structures, with manufacturers in Germany, France, and Italy increasingly deploying gensets to manage energy expenses and participate in grid stabilization programs.

By End-User Analysis

The manufacturing sector stands as a foundational end-user across the European gensets market, with Germany, Italy, France, and Poland representing significant concentrations of industrial activity requiring reliable power protection. European manufacturers face unique challenges including aging grid infrastructure in industrial zones, the need for production continuity in just-in-time manufacturing environments, and increasing exposure to electricity price volatility. The automotive, chemical, pharmaceutical, and food processing industries maintain particularly stringent requirements for power continuity, often implementing multi-layered backup systems that combine gensets with uninterruptible power supplies to protect sensitive equipment and maintain regulatory compliance for product quality.

The data center segment has emerged as the most demanding and fastest-growing end-user category across Europe, driven by the continent's position as a global hub for digital infrastructure. The concentration of hyperscale facilities in markets such as Ireland, the Netherlands, Germany, and the Nordic countries has created intense demand for high-reliability genset installations with extended fuel storage, advanced emissions control, and integration with increasingly complex electrical architectures. The healthcare sector maintains critical backup requirements across Europe's public and private hospital networks, with national health systems mandating comprehensive emergency power coverage for acute care facilities. The telecommunications sector, undergoing 5G infrastructure expansion across member states, represents a growing market for distributed backup solutions, particularly for remote towers and network nodes requiring compact, reliable power systems. The retail and hospitality sectors complete the market landscape, with supermarkets, shopping centers, and hotels maintaining genset installations to protect perishable inventory, ensure guest safety, and maintain operations during outages that increasingly accompany severe weather events across the continent.

The Europe Gensets Market Report is segmented on the basis of the following:

By Fuel Type

- Diesel

- Natural Gas

- Propane

By Power Rating

- Up to 75 kVA

- 75-375 kVA

- 375-750 kVA

- Above 750 kVA

By Application

- Standby Power

- Peak Shaving

- Prime/Continuous Power

By End-User

- Construction

- Manufacturing

- Telecom

- Healthcare

- Retail

- Data Centers

- Others

Impact of Artificial Intelligence in the Europe Gensets Market

- Predictive Maintenance and Monitoring: Artificial intelligence enables real-time condition monitoring of gensets, predicting component failures before they occur. This reduces unplanned downtime, lowers maintenance costs, extends equipment lifespan, and ensures reliable power supply across critical infrastructure sectors.

- Optimized Fuel Consumption: AI-driven analytics optimize fuel usage by adjusting generator load and performance based on demand patterns. This improves operational efficiency, minimizes fuel wastage, reduces emissions, and supports cost savings for businesses relying on continuous power supply.

- Integration with Energy Management Systems: Artificial intelligence enhances integration of gensets with energy management systems by synchronizing power generation with renewable sources. This enables efficient load balancing, reduces dependency on grid electricity, and supports sustainable energy usage across various industries.

- Remote Operations and Diagnostics: AI-powered remote monitoring systems allow operators to control and diagnose gensets from centralized locations. Real-time data insights improve decision-making, enhance operational reliability, reduce manual intervention, and ensure faster response to system irregularities.

- Advanced Fault Detection: Artificial intelligence algorithms detect anomalies in genset performance by analyzing operational data patterns. Early fault identification prevents major breakdowns, improves safety, reduces repair costs, and ensures uninterrupted power supply in critical and industrial applications.

Europe Gensets Market: Regional Analysis

Western Europe represents the largest and most mature segment of the European gensets market, with Germany, France, the United Kingdom, Italy, and the Benelux countries accounting for the majority of installed capacity. These nations benefit from robust industrial bases, extensive data center concentrations, and well-established healthcare infrastructure that demands high-reliability backup power systems. However, market growth in this region is increasingly shaped by stringent emissions regulations under the EU Stage V standards, urban air quality restrictions, and ambitious decarbonization goals that are accelerating the transition toward natural gas, hybrid, and hydrogen-ready genset technologies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Northern Europe, particularly the Nordic countries, presents a distinctive market characterized by high reliance on renewable energy sources and extreme weather conditions that create unique power resilience requirements. Sweden, Finland, Norway, and Denmark have advanced grid infrastructures but face challenges related to winter storm events and remote population centers where gensets serve essential prime power functions for telecommunications, emergency services, and critical infrastructure.

Southern Europe, encompassing Spain, Italy, Greece, Portugal, and the Mediterranean islands, demonstrates strong demand driven by tourism infrastructure, island power systems, and increasing grid instability associated with high solar photovoltaic penetration. The island nations and coastal regions rely heavily on gensets for seasonal peak support and backup during summer months when tourist loads strain local distribution networks.

Central and Eastern Europe, including Poland, Czech Republic, Hungary, Romania, and the Baltic states, represents the fastest-growing regional market, driven by industrial expansion, infrastructure modernization, and ongoing improvements in healthcare and data center infrastructure supported by EU cohesion funds.

By Region

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Europe Gensets Market: Competitive Landscape

The Europe gensets market features a competitive landscape characterized by the presence of established global manufacturers alongside specialized regional players serving distinct application segments. Leading multinational corporations maintain dominant positions across the continent, leveraging extensive distribution networks, comprehensive service infrastructure, and broad product portfolios spanning diesel, natural gas, and hybrid technologies.

The competitive environment is increasingly shaped by the transition toward cleaner power solutions, with manufacturers investing significantly in Stage V-compliant diesel engines, natural gas systems, and hydrogen-capable platforms to align with European Union decarbonization targets. Companies are differentiating through integrated solutions that combine gensets with energy storage systems, microgrid controls, and remote monitoring capabilities, addressing customer demand for optimized energy management and reduced carbon footprints.

Regional dynamics influence competitive strategies, with Western European markets emphasizing emissions compliance and technological sophistication, while Central and Eastern European markets remain more price-sensitive with continued demand for traditional diesel solutions. The rental segment represents a distinct competitive arena, with specialized providers maintaining extensive fleets to serve construction, events, and temporary power applications across the continent.

Service and aftermarket support have emerged as critical differentiators, as customers prioritize reliable maintenance networks and rapid response capabilities for mission-critical applications in data centers, healthcare facilities, and industrial operations.

Some of the prominent players in the Europe Gensets Market are:

- Caterpillar Inc.

- Cummins Inc.

- Kohler Co.

- Generac Holdings Inc.

- Rolls-Royce plc

- Mitsubishi Heavy Industries Ltd.

- Yanmar Holdings Co., Ltd.

- Kubota Corporation

- Atlas Copco AB

- Doosan Corporation

- Ashok Leyland Ltd.

- Mahindra Powerol

- Kirloskar Oil Engines Ltd.

- Honda Motor Co., Ltd.

- Briggs & Stratton Corporation

- FG Wilson

- Perkins Engines Company Limited

- Himoinsa S.L.

- SDMO Industries

- Wärtsilä Corporation

- Other Key Players

Recent Developments in the Europe Gensets Market

- January 2026: Siemens AG announced the acquisition of ASTER Technologies, strengthening its industrial electronics and power system capabilities, supporting advanced genset integration and monitoring solutions.

- December 2025: Siemens Gamesa Renewable Energy completed the sale of its Gamesa Electric division to ABB Ltd., enhancing ABB’s portfolio in power electronics and hybrid energy systems relevant to gensets.

- October 2025: Siemens AG partnered with rhobot.ai to launch an AI-based energy optimization platform, improving efficiency in generator-supported power systems.

- June 2025: MAN Energy Solutions rebranded to Everllence, focusing on hydrogen-ready engines and sustainable genset technologies aligned with Europe’s decarbonization goals.

- November 2024: Ignitis Group announced participation in a 700 MW offshore wind project, increasing renewable penetration and indirectly driving demand for backup gensets across Europe.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 3.5 Bn |

| Forecast Value (2035) |

USD 6.2 Bn |

| CAGR (2026–2035) |

6.6% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Fuel Type (Diesel, Natural Gas, Propane), By Power Rating (Up to 75 kVA, 75-375 kVA, 375-750 kVA, Above 750 kVA), By Application (Standby Power, Peak Shaving, Prime/Continuous Power), By End-User (Construction, Manufacturing, Telecom, Healthcare, Retail, Data Centers, Others) |

| Regional Coverage |

Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe |

| Prominent Players |

Caterpillar Inc. (Cat), Cummins Inc., Rolls-Royce Power Systems (MTU), Kohler-SDMO (now rebranded as Rehlko), Aggreko PLC, Atlas Copco AB, FG Wilson, Pramac S.p.A., HIMOINSA S.L., Wärtsilä Corporation, Volvo Penta AB, Deutz AG, Mitsubishi Heavy Industries Engine & Turbocharger Ltd., Generac Power Systems, Yanmar Holdings Co. Ltd., AKSA Power Generation, Perkins Engines Company, Grupel S.A., JCB Power Products, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Europe Gensets Market?

▾ The Europe Gensets Market size is estimated to have a value of USD 3.5 billion in 2026 and is expected to reach USD 6.2 billion by the end of 2035.

What is the growth rate in the Europe Gensets Market?

▾ The market is growing at a CAGR of 6.6 percent over the forecasted period of 2026-2035.

Who are the key players in the Europe Gensets Market?

▾ Some of the major key players in the Europe Gensets Market are Caterpillar Inc., Cummins Inc., Generac Holdings Inc., Kohler Co., Mitsubishi Heavy Industries, Ltd., Yanmar, Rolls-Royce plc, and many others.