Market Overview

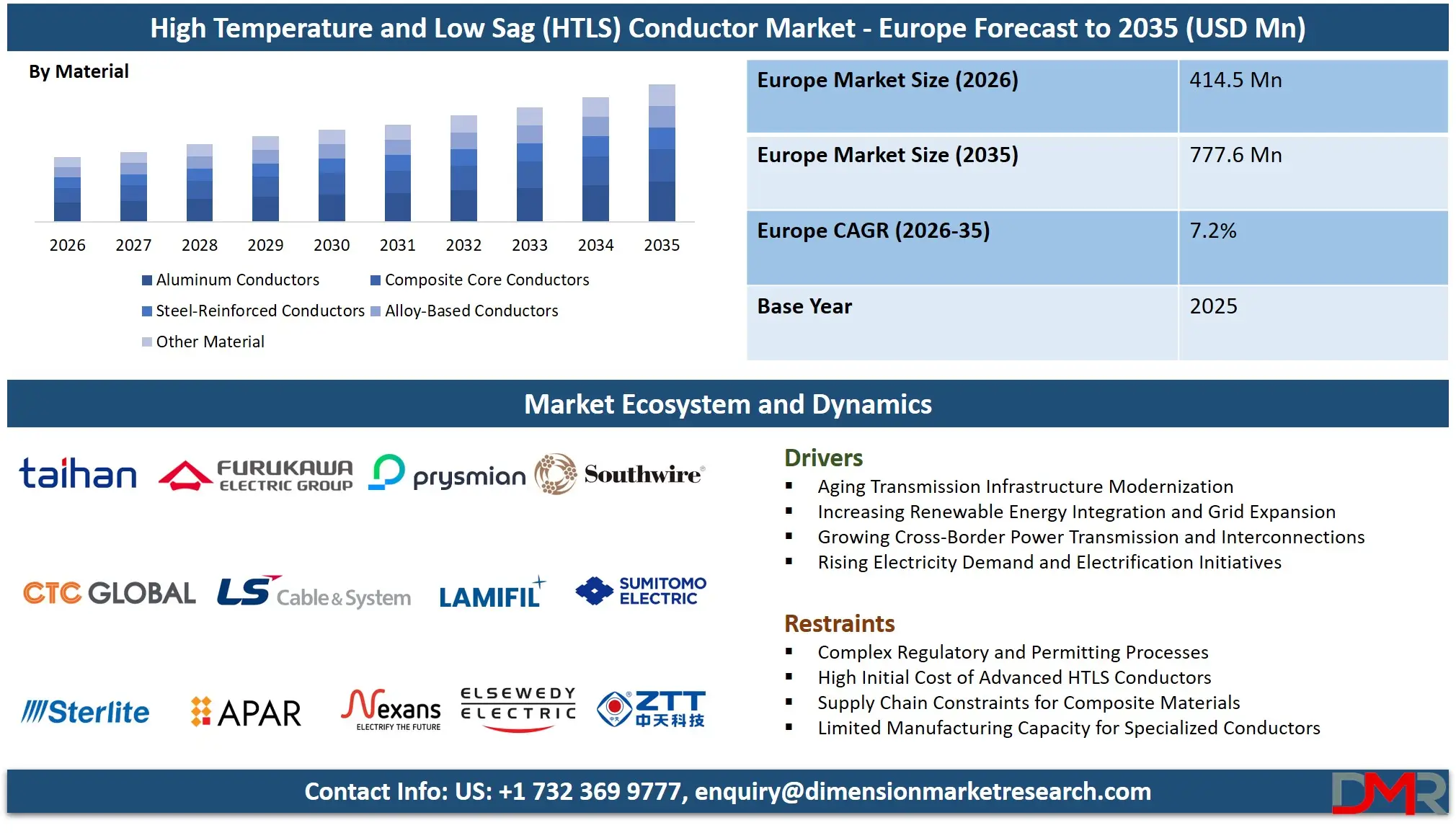

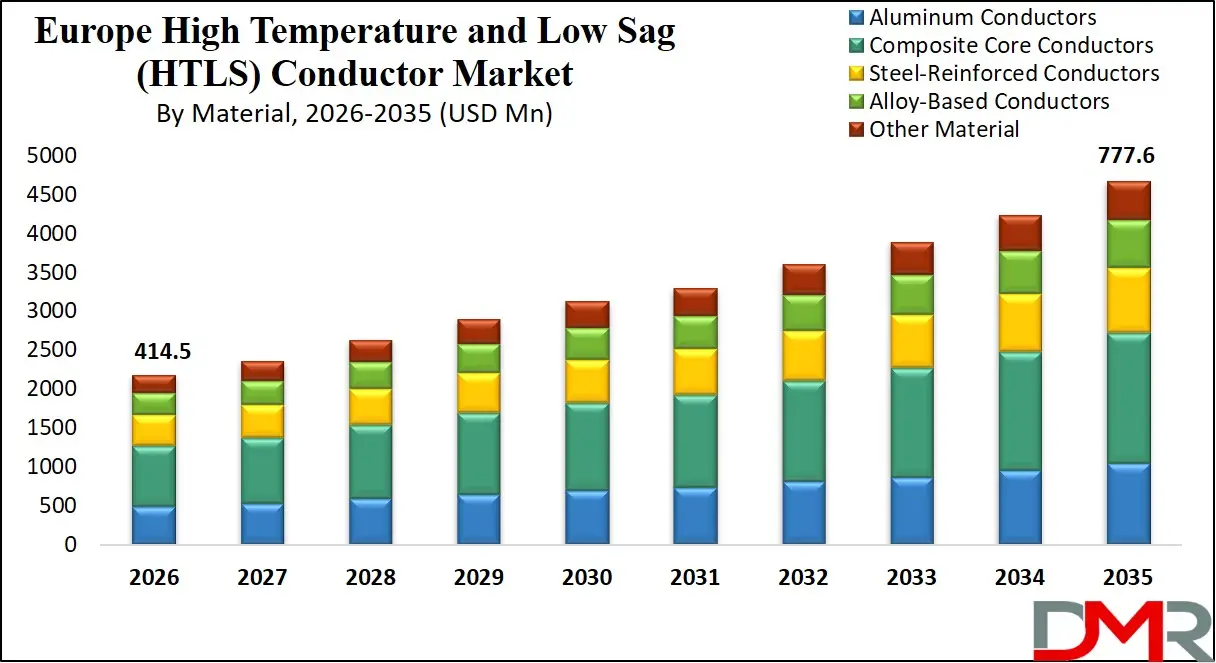

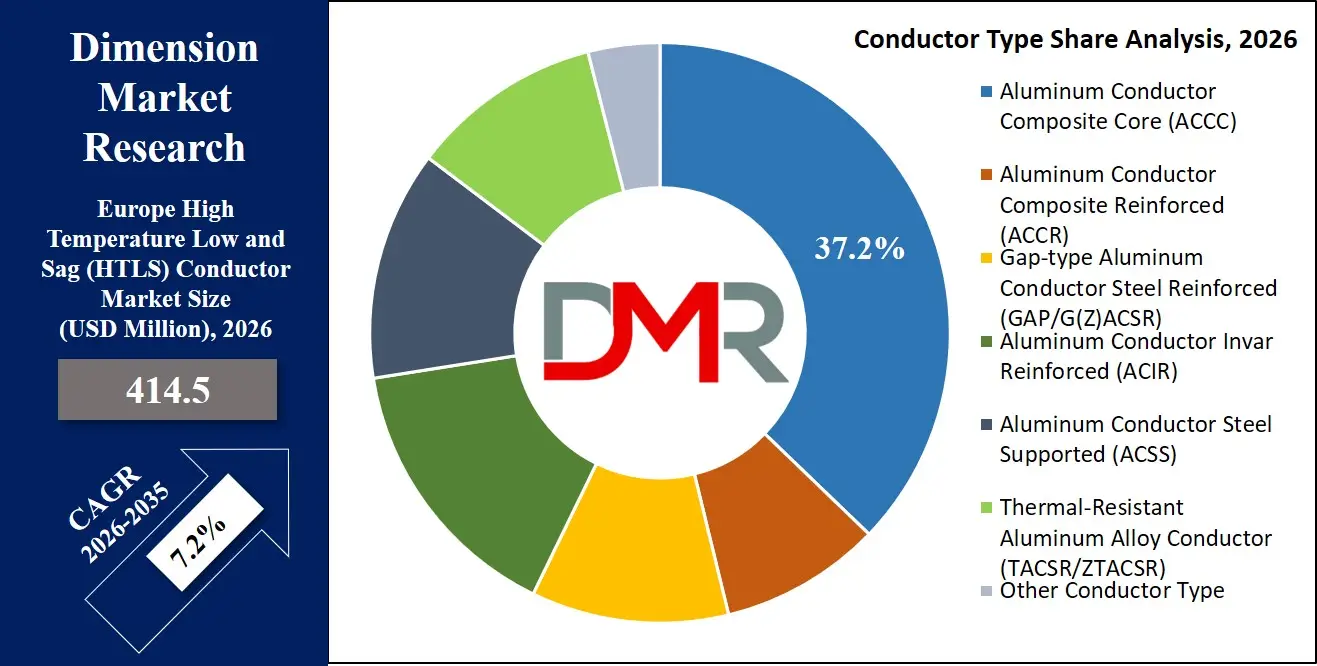

The Europe High Temperature and Low Sag (HTLS) Conductor Market is projected to be valued at approximately USD 414.5 million in 2026 and is projected to reach around USD 777.6 million by 2035, growing at a CAGR of about 7.2% from 2026 to 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The expansion of the market is strongly supported by European grid modernization programs, renewable energy expansion policies, cross-border electricity interconnection initiatives, and large-scale infrastructure investment under the European Green Deal and REPowerEU programs. The transition toward a decarbonized energy system is fundamentally reshaping Europe's electricity infrastructure, creating substantial demand for advanced transmission technologies such as HTLS conductors.

Europe's power transmission infrastructure is undergoing a structural transformation due to the rapid expansion of offshore wind power in the North Sea and Baltic Sea, solar photovoltaic installations across Southern Europe, and increasing electrification of transportation, heating, and industrial sectors. These developments significantly increase electricity transmission requirements and require grid operators to expand network capacity efficiently.

A significant portion of Europe's transmission network was originally constructed during the post-World War II industrialization era, particularly between the 1950s and 1970s, meaning that many transmission corridors are approaching or exceeding their original design capacity. As a result, transmission system operators (TSOs) increasingly rely on HTLS conductor technologies to upgrade existing transmission lines through reconductoring, enabling capacity expansion while maintaining existing rights-of-way.

This strategy is particularly valuable in Europe, where permitting processes for new transmission corridors can take many years due to environmental regulations, land-use constraints, and public opposition. By replacing conventional conductors with HTLS technologies such as ACCC, ACSS, GAP-type ACSR, and advanced aluminum alloy conductors, utilities can increase power transfer capability without constructing new towers or acquiring additional land.

Furthermore, European transmission operators including RTE (France), TenneT (Netherlands/Germany), Amprion (Germany), Terna (Italy), and National Grid (UK) are facing rising grid congestion levels due to rapidly increasing renewable generation capacity. HTLS conductors provide an efficient solution to increase transmission capacity, improve thermal performance, and maintain safety clearances even under high-temperature operating conditions.

Another key growth driver is the integration of remote renewable energy sources, particularly offshore wind farms located far from major electricity demand centers. High-capacity transmission lines are required to transport electricity from these remote generation hubs to urban load centers, making advanced conductor technologies critical for grid reliability and efficiency.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

European policy frameworks such as the Trans-European Networks for Energy (TEN-E) regulation, the European Green Deal, and the REPowerEU strategy are also accelerating investments in transmission infrastructure. These policies promote cross-border interconnection, grid resilience improvements, and renewable energy integration, all of which increase the demand for HTLS conductors.

Despite these favorable market conditions, certain factors continue to pose challenges for the industry. These include high installation costs, regulatory fragmentation across EU member states, supply chain limitations for advanced composite materials, and competition from conventional conductor technologies.

Nevertheless, continuous technological advancements in composite core materials, thermal-resistant aluminum alloys, dynamic line rating technologies, and digital grid monitoring systems are expected to further strengthen the role of HTLS conductors in Europe's evolving electricity transmission landscape.

Impact of Iran War on the Europe High Temperature and Low Sag (HTLS) Conductor Market

- Acceleration of Energy Security and Grid Resilience Initiatives: The Russia–Ukraine conflict significantly reshaped Europe's energy strategy by accelerating efforts to reduce dependence on Russian fossil fuel imports. This shift has resulted in increased investment in renewable energy projects and grid infrastructure modernization, indirectly strengthening demand for HTLS conductors used in high-capacity transmission upgrades.

- Volatility in Aluminum and Critical Raw Material Prices: HTLS conductors rely heavily on high-grade aluminum, aluminum-zirconium alloys, and advanced composite materials. The geopolitical instability triggered disruptions in metal supply chains and increased price volatility, affecting manufacturing costs and project budgets for transmission infrastructure projects.

- Logistics and Supply Chain Disruptions: Transportation disruptions across Eastern Europe affected the movement of industrial metals, engineering materials, and electrical equipment. Higher freight costs and delayed shipments created supply challenges for conductor manufacturers and grid operators implementing large-scale transmission upgrades.

- Rising Energy and Manufacturing Costs: Aluminum smelting and conductor manufacturing are energy-intensive processes. The surge in European electricity and natural gas prices following the conflict increased production costs for conductor manufacturers, which in turn impacted overall project costs for utilities.

- Strengthening Cross-Border Electricity Interconnection: The geopolitical crisis also reinforced the importance of regional electricity integration within Europe. Governments and TSOs increased investments in cross-border transmission capacity, driving demand for high-performance conductor technologies capable of handling increased power flows between interconnected grids.

Europe High Temperature and Low Sag (HTLS) Conductor Market: Key Takeaways

- Stable Market Expansion Driven by Grid Modernization: The Europe HTLS conductor industry is projected to expand steadily, reaching USD 777.6 million by 2035 as transmission infrastructure modernization continues across the world.

- Consistent CAGR Supported by Energy Transition Policies: A 7.2% CAGR is expected during the forecast period, supported by growing renewable energy installations, cross-border electricity trade, and increasing electricity demand from electrified transport systems.

- ACCC Conductors Expected to Dominate the Market: Aluminum Conductor Composite Core (ACCC) technology is expected to maintain the 37.2% of market share in 2026 due to its low thermal expansion, high tensile strength, and improved current-carrying capacity, making it ideal for reconductoring projects.

- Reconductoring and Capacity Upgrade Applications Leading Demand: Most HTLS deployments in Europe are associated with transmission line reconductoring projects, enabling utilities to increase capacity without constructing new transmission corridors.

- Transmission System Operators as the Primary Buyers: TSOs remain the largest end-use segment due to their responsibility for maintaining national transmission networks and implementing EU-mandated grid expansion targets.

- Growing Transmission Congestion Driving Technology Adoption: Increasing power flows from renewable energy projects have intensified transmission congestion across European electricity networks, increasing demand for advanced conductors capable of handling higher current loads.

Europe High Temperature and Low Sag (HTLS) Conductor Market: Use Cases

- Offshore Wind Power Grid Integration: Transmission operators in the North Sea region, including operators such as TenneT and Energinet, utilize HTLS conductors to connect large offshore wind farms to onshore substations while maintaining high transfer capacity.

- Cross-Border Transmission Interconnector Upgrades: European utilities deploy HTLS conductors on critical interconnection lines between neighboring countries, enabling increased electricity trading and improved system reliability.

- Urban Transmission Network Capacity Enhancement: Major European cities require higher electricity transmission capacity due to increasing electrification. Reconductoring with HTLS technologies allows utilities to upgrade existing lines entering dense urban areas without acquiring additional land.

- Transmission Infrastructure in Mountainous Regions: In Alpine regions, utilities deploy HTLS conductors because their reduced sag characteristics maintain safe ground clearance even in challenging terrain conditions.

- Renewable Energy Zone Transmission Development: Solar-rich regions of Southern Europe rely on HTLS technologies to transport electricity from large utility-scale solar plants to major consumption centers.

Europe High Temperature and Low Sag (HTLS) Conductor Market: Stats & Facts

ENTSO-E (European Network of Transmission System Operators for Electricity)

- Europe operates over 300,000 kilometers of high-voltage transmission lines above 220 kV

- Nearly 40% of transmission infrastructure is more than 40 years old

- Cross-border interconnection capacity is projected to increase over 50% by 2035

- Transmission congestion results in multi-billion-euro annual costs for European electricity consumers

- Renewable energy interconnection queues represent hundreds of gigawatts of pending generation capacity

European Commission

- The European Green Deal aims to reduce greenhouse gas emissions by at least 55% by 2030

- Europe targets climate neutrality by 2050

- More than 100 energy infrastructure projects are classified as Projects of Common Interest (PCI)

- EU member states aim to reach 15% cross-border electricity interconnection capacity by 2030

- Grid investment requirements exceed EUR 500 billion by 2030

European Environment Agency

- Renewable energy generated approximately 37% of EU electricity in 2023

- Offshore wind capacity could exceed 100 GW by 2030

- Solar power installations are expanding at annual growth rates exceeding 25%

- Electricity demand is expected to rise significantly due to transport and heating electrification

International Energy Agency

- Europe currently leads global offshore wind deployment with more than 30 GW installed capacity

- Electricity consumption may grow 2–3% annually through 2030

- Grid investment needs are expected to double by 2030

- Renewable energy capacity in Europe surpassed 600 GW in 2023

Europe High Temperature and Low Sag (HTLS) Conductor Market: Market Dynamic

Driving Factors in the Europe High Temperature and Low Sag (HTLS) Conductor Market

Aging Transmission Infrastructure and Capacity Constraints

The growing need to modernize Europe's aging transmission infrastructure and address rising electricity demand is a major factor driving HTLS conductor adoption. A significant portion of the European high-voltage transmission network was developed between the 1960s and 1980s and now requires modernization to support electrification, renewable energy expansion, and cross-border power flows. HTLS conductor technologies provide higher ampacity without requiring major tower modifications or new right-of-way development, making them an efficient solution for upgrading legacy infrastructure.

European transmission system operators (TSOs) increasingly utilize HTLS reconductoring programs to maximize existing transmission corridors while improving system reliability and operational flexibility. This approach is particularly valuable in densely populated regions where building new transmission lines is challenging due to land availability, environmental constraints, and public opposition. By increasing capacity on existing lines, utilities can accommodate growing electricity demand and maintain grid stability across interconnected European power markets.

Renewable Energy Integration and Cross-Border Grid Expansion

Europe's aggressive renewable energy targets and regional decarbonization strategies significantly accelerate HTLS conductor adoption. The European Union's climate policies, including the Green Deal and the "Fit for 55" initiative, require large-scale deployment of renewable energy sources such as wind and solar power. These resources are often located far from major load centers, creating a strong need for transmission capacity expansion.

HTLS conductors provide an efficient solution for increasing transmission capacity between renewable generation zones and demand hubs without constructing entirely new transmission corridors. Many European countries are also strengthening cross-border interconnections to improve energy security and facilitate electricity trading within the integrated European power market. Reconductoring existing transmission lines with HTLS technology enables faster implementation of these grid expansion projects while minimizing environmental impacts and regulatory delays.

Restraints in the Europe High Temperature and Low Sag (HTLS) Conductor Market

Complex Permitting and Environmental Approval Processes

One of the key challenges affecting HTLS conductor deployment in Europe is the complexity of permitting and environmental approval procedures. Transmission infrastructure projects often require extensive environmental impact assessments, public consultations, and approvals from multiple regulatory bodies at national and regional levels. These processes can extend project timelines and create uncertainty for utilities planning transmission upgrades.

In several European countries, public opposition to new transmission infrastructure has also increased due to concerns related to environmental protection, landscape preservation, and land use restrictions. Although HTLS reconductoring projects typically face fewer obstacles than greenfield transmission development, regulatory approvals and compliance requirements can still slow deployment in certain regions.

Supply Chain Constraints for Advanced Materials

The supply chain for advanced HTLS conductor materials presents another challenge for the European market. Many HTLS conductor technologies rely on specialized materials such as carbon fiber composite cores, high-performance aluminum alloys, and advanced thermal-resistant components. Fluctuations in global supply chains for these materials can result in price volatility and extended procurement timelines.

In addition, Europe currently depends on a limited number of manufacturers for certain high-performance conductor technologies. This dependence on international suppliers may increase procurement risks, particularly during periods of geopolitical tension or disruptions in global industrial supply chains. As demand for HTLS conductors increases across Europe, strengthening domestic manufacturing capabilities and supply chain resilience will become increasingly important.

Opportunities in the Europe High Temperature and Low Sag (HTLS) Conductor Market

Transmission Expansion for Renewable Energy Corridors

Europe's large pipeline of renewable energy projects creates substantial opportunities for HTLS conductor deployment. Offshore wind developments in the North Sea and Baltic Sea, large-scale solar projects in Southern Europe, and expanding onshore wind capacity across several countries require enhanced transmission infrastructure to transport electricity efficiently across regions.

HTLS reconductoring provides a practical solution for strengthening key transmission corridors that connect renewable generation hubs with urban and industrial demand centers. By increasing power transfer capability on existing lines, transmission system operators can accelerate grid integration of renewable projects and reduce congestion within the European electricity network.

Integration with Grid Digitalization and Smart Transmission Technologies

Another emerging opportunity in the European HTLS conductor market is the integration of these conductors with advanced grid-enhancing technologies. Dynamic line rating (DLR) systems, real-time grid monitoring, and advanced transmission management platforms are increasingly being implemented across European networks to improve grid efficiency.

When deployed alongside HTLS conductors, these technologies enable utilities to optimize real-time power transfer capacity, improve operational flexibility, and enhance situational awareness across transmission networks. This combination transforms HTLS conductors from passive infrastructure components into part of an intelligent and adaptive grid system that supports Europe's broader energy transition and digitalization strategies.

Trends in the Europe High Temperature and Low Sag (HTLS) Conductor Market

Growing Adoption of Composite Core Conductors

Composite core conductor technologies, including Aluminum Conductor Composite Core (ACCC) and similar designs, are gaining strong traction across European transmission networks. These conductors utilize lightweight composite materials such as carbon fiber or glass fiber cores that enable higher operating temperatures while maintaining minimal sag.

The superior mechanical strength and thermal performance of composite core conductors allow transmission operators to significantly increase line capacity without requiring major structural modifications to existing towers. In addition, these conductors offer lower electrical resistance and reduced energy losses compared to traditional steel-reinforced conductors. As European utilities prioritize efficiency improvements and grid modernization, composite core technologies are increasingly specified in high-capacity reconductoring projects.

Increased Deployment of Gap-Type High-Temperature Conductors

Gap-type conductors, including G(Z)ACSR designs, are also witnessing increased adoption across European transmission networks. These conductors feature a gap between the steel core and aluminum strands filled with heat-resistant grease, allowing thermal expansion to occur independently while maintaining stable sag characteristics at high operating temperatures.

Gap-type HTLS conductors are often selected for projects that require improved thermal performance while maintaining compatibility with existing transmission infrastructure. Their proven reliability, well-established manufacturing base, and relatively lower cost compared to some composite solutions make them an attractive option for utilities implementing large-scale transmission upgrades across Europe.

Europe High Temperature and Low Sag (HTLS) Conductor Market: Research Scope and Analysis

By Conductor Type Analysis

The Aluminum Conductor Composite Core (ACCC) segment is projected to dominate the Europe HTLS Conductor Market, accounting for approximately 37.2% of the market share in 2026, representing the largest share among conductor types. The strong adoption of ACCC conductors is driven by the growing need for high-capacity transmission solutions that can increase power transfer capability without requiring major structural modifications to existing towers.

European utilities and transmission system operators increasingly deploy composite core conductors to support grid modernization and renewable energy integration. ACCC conductors can operate at elevated temperatures of up to 180°C while maintaining minimal sag due to their low coefficient of thermal expansion compared with traditional steel cores. These characteristics enable transmission capacity increases of 30–100% on existing rights-of-way while improving overall system efficiency.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In addition, composite core conductors offer benefits such as lightweight construction, corrosion resistance, and improved durability under varying climatic conditions. These advantages make them suitable for long-distance transmission lines and high-capacity corridors connecting renewable energy zones to load centers.

While other HTLS technologies such as Gap-type ACSR (G(Z)ACSR) and Aluminum Conductor Steel Supported (ACSS) continue to maintain strong market positions for specific applications, ACCC conductors remain the preferred solution for projects requiring maximum capacity upgrades and advanced thermal performance. As Europe accelerates its energy transition and expands transmission capacity, the ACCC segment is expected to maintain its leading position.

By Material Analysis

Composite core materials are expected to dominate the material segment, accounting for approximately 35.4% of market share in 2026 due to their superior mechanical and thermal performance. These materials offer an exceptional strength-to-weight ratio, enabling conductors to carry higher electrical loads while maintaining minimal sag and structural stress on transmission towers.

European transmission operators increasingly prefer composite core conductors because they allow significant increases in ampacity without requiring tower reinforcement or replacement. This capability is particularly valuable in densely populated regions where building new transmission infrastructure can be difficult due to regulatory restrictions and land-use limitations.

Composite materials also provide high resistance to corrosion, improved durability in extreme weather conditions, and reduced susceptibility to mechanical fatigue. These features enhance long-term reliability and reduce maintenance requirements across large transmission networks.

Furthermore, the favorable economics of capacity gain per investment dollar make composite core conductors an attractive solution for utilities seeking cost-effective grid upgrades. Although steel-reinforced and alloy-based conductors remain relevant for certain voltage levels and applications, their performance limitations at higher operating temperatures reduce their competitiveness in advanced HTLS deployments. As European transmission networks continue to expand and modernize, composite core materials are expected to maintain their leading market position.

By Voltage Level Analysis

High Voltage (HV) transmission applications are expected to dominate the voltage level segment within the Europe HTLS conductor market due to their critical role in bulk power transmission and cross-border electricity exchange. Voltage levels ranging from approximately 110 kV to 220 kV form the backbone of many European transmission networks, linking generation sources with major consumption centers.

HTLS conductor deployment at HV levels is particularly effective because it enables substantial capacity increases within existing transmission corridors. Transmission system operators frequently utilize HTLS reconductoring to upgrade aging lines, reduce congestion, and enhance power transfers between interconnected regional grids.

Extra High Voltage (EHV) networks, typically operating at 380 kV, also represent an important application area as Europe strengthens long-distance power transmission and international interconnections. These networks play a key role in supporting large-scale renewable integration and facilitating electricity trading within the European internal energy market.

Although medium-voltage distribution networks are gradually adopting advanced conductor technologies to support distributed generation and electrification, HV and EHV transmission applications remain the dominant segment. Their central role in enabling large-scale power transfers and maintaining system reliability ensures continued demand for HTLS conductors across Europe.

By Application Analysis

Grid reconductoring and transmission capacity upgrades are projected to dominate the application segment within the Europe HTLS conductor market. With limited availability of new transmission corridors and increasing public resistance to greenfield infrastructure development, European utilities increasingly rely on reconductoring existing lines to enhance grid capacity.

HTLS conductors enable transmission operators to replace aging conductors with advanced high-temperature designs capable of carrying significantly higher electrical loads. This approach allows utilities to upgrade network performance without constructing new transmission lines or acquiring additional land.

Transmission system operators across Europe implement reconductoring programs to relieve congestion on heavily utilized corridors, improve cross-border electricity flows, and integrate growing volumes of renewable generation. In addition, reconductoring helps accelerate grid connection timelines for renewable energy projects that require access to transmission infrastructure.

While applications such as renewable energy integration and new transmission construction also contribute to market growth, reconductoring and capacity upgrades remain the primary revenue drivers. As Europe continues expanding renewable energy generation and electrifying key sectors, these applications will remain central to the development of the HTLS conductor market.

By End-Use Industry Analysis

The electric utilities sector is expected to dominate the end-use industry segment in the Europe HTLS conductor market due to its ownership and operation of most transmission infrastructure across the region. Transmission system operators and major utility companies are responsible for maintaining grid reliability while expanding capacity to support growing electricity demand.

European energy transition policies require utilities to modernize transmission networks to accommodate increasing renewable energy generation and electrification of transportation and industry. As a result, utilities are investing heavily in advanced conductor technologies that enable higher power transfer capability and improved grid efficiency.

Independent transmission operators and infrastructure developers also contribute to market demand by implementing new interconnection projects and upgrading cross-border transmission links. Given the capital-intensive nature of transmission infrastructure, utilities prioritize technologies such as HTLS conductors that maximize the utilization of existing assets while meeting regulatory and reliability requirements.

Although renewable energy developers, industrial energy users, and transportation infrastructure operators also influence demand for transmission upgrades, electric utilities remain the largest market participants due to their extensive asset base and mandatory responsibility for grid operation and expansion.

Europe High Temperature and Low Sag (HTLS) Conductor Market Report is segmented on the basis of the following:

By Conductor Type

- Aluminum Conductor Composite Core (ACCC)

- Aluminum Conductor Composite Reinforced (ACCR)

- Gap-type Aluminum Conductor Steel Reinforced (GAP/G(Z)ACSR)

- Aluminum Conductor Invar Reinforced (ACIR)

- Aluminum Conductor Steel Supported (ACSS)

- Thermal-Resistant Aluminum Alloy Conductor (TACSR/ZTACSR)

- Other Conductor Type

By Material

- Aluminum Conductors

- Composite Core Conductors

- Steel-Reinforced Conductors

- Alloy-Based Conductors

- Other Material

By Voltage Level

- Low Voltage (LV)

- Medium Voltage (MV)

- High Voltage (HV)

- Extra High Voltage (EHV)

By Application

- Power Transmission

- Power Distribution

- Renewable Energy Grid Integration

- Grid Reconductoring / Capacity Upgrade

- Other Application

By End-Use Industry

- Electric Utilities

- Renewable Energy Integration

- Oil & Gas

- Mining & Metal Processing

- Railways & Transportation

- Other End-Use Industry

Impact of Artificial Intelligence in Europe High Temperature and Low Sag (HTLS) Conductor Market

- AI-Enabled Advanced Composite Core Development: Artificial Intelligence is increasingly used in Europe to accelerate the development of advanced composite core materials used in HTLS conductors. AI-driven material simulation and predictive modeling help engineers analyze the mechanical strength, thermal stability, and fatigue resistance of carbon fiber and glass fiber composite cores.

- AI-Optimized High-Temperature Alloy Performance: AI is also transforming the design and performance optimization of high-temperature aluminum alloys used in HTLS conductors. Machine learning models can analyze metallurgical data to predict how aluminum-zirconium and other heat-resistant alloys behave under extreme electrical loads and environmental conditions.

- AI-Driven Engineering for Gap-Type Conductors: Gap-type conductor designs benefit significantly from artificial intelligence applications in engineering and product optimization. AI-based simulation tools can evaluate conductor expansion behavior, mechanical stresses, and sag performance under different temperature conditions.

- Predictive Maintenance and Corrosion Monitoring: Artificial intelligence is also enhancing the durability and operational reliability of HTLS conductors through predictive maintenance systems. AI-powered monitoring platforms analyze data collected from sensors, drones, and satellite imaging to detect early signs of corrosion, mechanical stress, and conductor degradation.

- AI-Supported Computational Modeling for Conductor Design: Computational modeling plays a critical role in designing HTLS conductors suited for specific transmission applications, and artificial intelligence significantly enhances these modeling capabilities.

By Region

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Europe High Temperature and Low Sag (HTLS) Conductor Market: Competitive Landscape

The Europe HTLS Conductor Market is moderately consolidated, featuring a combination of global cable manufacturers, specialized conductor technology providers, and advanced materials companies. Major European cable manufacturers such as Prysmian Group and Nexans play a significant role in the regional market due to their extensive manufacturing infrastructure and long-standing relationships with European transmission system operators.

Specialized conductor technology providers such as CTC Global, known for its ACCC composite core conductor technology, contribute significantly to innovation within the market. These companies focus on high-performance HTLS conductor technologies that enable substantial increases in transmission capacity while maintaining reliability under high operating temperatures.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Traditional cable manufacturers and international suppliers including LS Cable & System, ZTT International, and Midal Cables also play an important role by supplying HTLS conductors and components for transmission infrastructure projects across Europe. At the same time, materials science companies such as Toray Industries, which supply carbon fiber used in composite conductor cores, support the production of advanced HTLS technologies.

Regional manufacturers and engineering companies also participate in the European market, supplying conductors for specific national grid modernization projects and renewable energy transmission programs. As Europe accelerates its energy transition and transmission expansion, competition among global and regional suppliers is expected to intensify, particularly for high-capacity conductor technologies supporting renewable energy integration and cross-border electricity transmission.

Some of the prominent players in Europe High Temperature and Low Sag (HTLS) Conductor Market are:

- Southwire Company, LLC

- CTC Global Corporation

- LS Cable & System Ltd.

- Nexans S.A.

- Prysmian S.p.A.

- Midal Cables Ltd.

- ZTT International Limited

- Lamifil N.V.

- Hengtong Group

- Sumitomo Electric Industries, Ltd.

- Fujikura Ltd.

- Furukawa Electric Co., Ltd.

- AFL

- Walsin Lihwa Corporation

- Eland Cables

- APAR Industries Limited

- Sterlite Power

- Taihan Electric Wire Co., Ltd.

- KEC International Limited

- Kalpataru Power Transmission Limited

- Other Key Players

Recent Developments in Europe High Temperature and Low Sag (HTLS) Conductor Market

- April 2025: Prysmian Group announced the acquisition of Encore Wire Corporation for approximately USD 4.15 billion. The acquisition strengthens Prysmian's global conductor manufacturing capabilities and supports the company's strategy to expand power transmission solutions for grid modernization and renewable energy integration projects.

- February 2025: Nexans S.A. expanded its European transmission solutions portfolio by introducing advanced high-capacity overhead conductors designed for large-scale renewable energy transmission corridors and cross-border grid expansion projects.

- January 2025: CTC Global Corporation strengthened collaboration with European utilities and transmission operators to promote deployment of ACCC composite-core HTLS conductors for reconductoring projects aimed at increasing transmission capacity without constructing new towers.

- October 2024: Lamifil NV participated in European power transmission industry events showcasing next-generation HTLS conductor technologies designed for high-capacity transmission networks supporting renewable energy integration.

- September 2024: Nexans S.A. supplied advanced overhead conductors for transmission network upgrade projects supporting renewable energy integration and capacity expansion in several European grid modernization programs.

- July 2024: Sumitomo Electric Industries Ltd. supported European utilities with high-temperature conductor solutions designed to increase ampacity and reduce sag on existing transmission lines as part of reliability and grid reinforcement programs.

- May 2024: LS Cable & System Ltd. partnered with European transmission utilities and infrastructure developers to demonstrate high-capacity overhead conductor technologies for renewable energy transmission corridors.

- March 2024: Sterlite Power promoted HTLS conductor technologies during European energy infrastructure forums, highlighting their role in enabling higher-capacity transmission lines and accelerating renewable energy grid integration.

- January 2024: Lamifil NV collaborated with European research institutions and transmission operators to evaluate high-temperature conductor materials and performance characteristics for next-generation power transmission networks.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 414.5 Mn |

| Forecast Value (2035) |

USD 777.6 Mn |

| CAGR (2026–2035) |

7.2% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Conductor Type (Aluminum Conductor Composite Core (ACCC), Aluminum Conductor Composite Reinforced (ACCR), Gap-type Aluminum Conductor Steel Reinforced (GAP/G(Z)ACSR), Aluminum Conductor Invar Reinforced (ACIR), Aluminum Conductor Steel Supported (ACSS), Thermal-Resistant Aluminum Alloy Conductor (TACSR/ZTACSR), Other Conductor Type), By Material (Aluminum Conductors, Composite Core Conductors, Steel-Reinforced Conductors, Alloy-Based Conductors, Other Material), By Voltage Level (Low Voltage (LV), Medium Voltage (MV), High Voltage (HV), Extra High Voltage (EHV)), By Application (Power Transmission, Power Distribution, Renewable Energy Grid Integration, Grid Reconductoring / Capacity Upgrade, Other Application), and By End-Use Industry (Electric Utilities, Renewable Energy Integration, Oil & Gas, Mining & Metal Processing, Railways & Transportation, Other End-Use Industry). |

| Regional Coverage |

Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe |

| Prominent Players |

Southwire Company, LLC, CTC Global Corporation, LS Cable & System Ltd., Nexans S.A., Prysmian S.p.A., Midal Cables Ltd., ZTT International Limited, Lamifil N.V., Hengtong Group, Sumitomo Electric Industries, Ltd., Fujikura Ltd., Furukawa Electric Co., Ltd., AFL, Walsin Lihwa Corporation, Eland Cables, APAR Industries Limited, Sterlite Power, Taihan Electric Wire Co., Ltd., KEC International Limited, Kalpataru Power Transmission Limited, and Other Key Players. |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Europe High Temperature and Low Sag (HTLS) Conductor Market?

▾ The Europe HTLS Conductor Market size is estimated to have a value of USD 414.5 million in 2026 and is expected to reach USD 777.6 million by the end of 2035.

What is the growth rate in the Europe High Temperature and Low Sag (HTLS) Conductor Market?

▾ The market is growing at a CAGR of 7.2 percent over the forecasted period of 2026-2035.

Who are the key players in the Europe High Temperature and Low Sag (HTLS) Conductor Market?

▾ Some of the major key players in the Europe HTLS Conductor Market are Nexans S.A., Prysmian S.p.A., Southwire Company, CTC Global Corporation, NKT A/S, LS Cable & System, Lamifil N.V., and many others.